Risk-Neutrality of RND and Option Pricing within an Entropy Framework

Abstract

:1. Introduction

2. Entropy Valuation with RNM-Constraints

2.1. Pricing Scheme

2.2. Calculations of RNM and Derivation of RND

2.2.1. Calculations of RNM

2.2.2. Derivation of RND

2.3. Risk-Neutral underlying Paths and Option Price

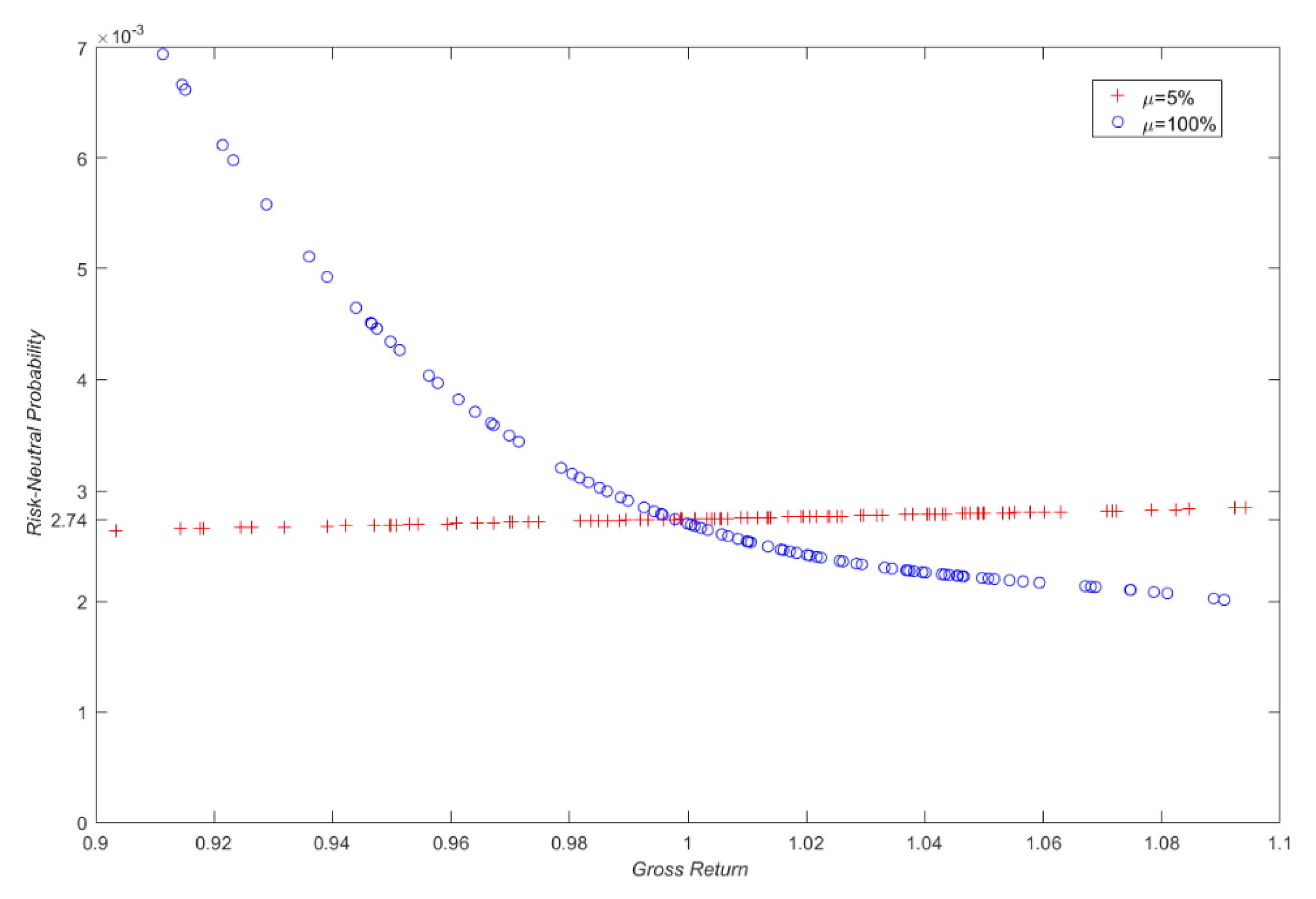

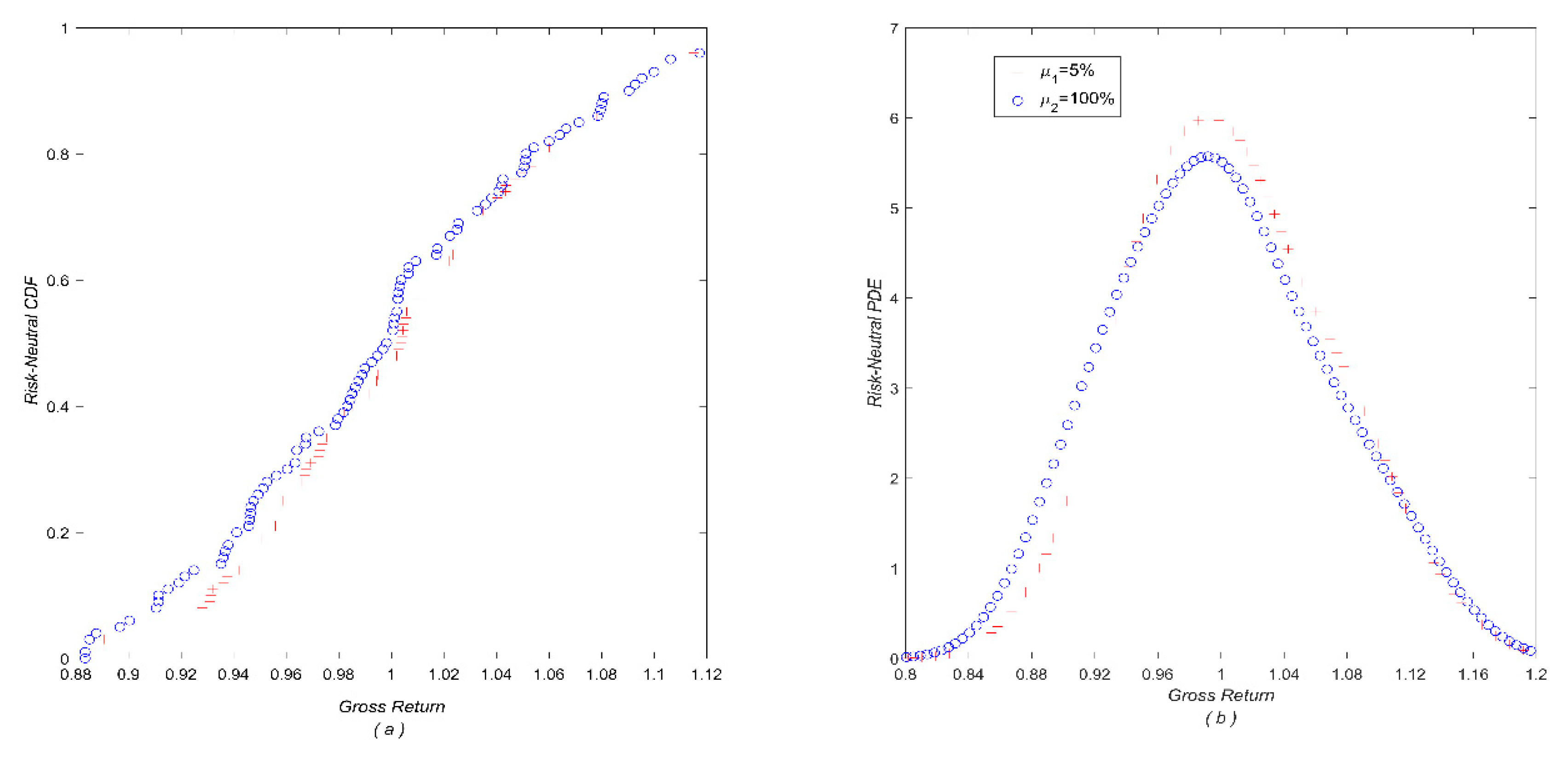

3. Verification of Correctness of Extracted RNMs and Risk-Neutrality of RND

3.1. Correctness of the Estimated RNMs

3.2. Risk-Neutrality of the Derived RND

4. Pricing Performance and Analysis

4.1. Performance in a B–S Environment

- Valuation date: t0 = 0

- Expiration date (in year): T = 1/12, 1/4, 1/2, 3/4, 1

- Strike price K = 52

- Initial asset price: S0 = 4 8, 50, 52, 54, 56

- Risk-free interest rate: r = 5%

- Drift rate: μ1 = 5%, μ2 = 100%

- Volatility: σ = 20%

- Dividend yield (Without any loss of generality but merely a computational convenience, here we set dividend yield q = 0.): q = 0

4.2. Performance in a Stochastic Volatility Model

- Drift rate: μ = 10%

- Mean reversion: κ = 3

- Long-run mean: = 4%

- Volatility: η = 40%

- Correlation: = −0.5,

- Valuation date: t0 = 0

- Expiration date (in year): T = 1/12, 1/4, 1/2, 3/4, 1

- Strike price: K = 52

- Risk-free interest rate: r = 5%

- Dividend yield: q = 0

5. Conclusions

Funding

Conflicts of Interest

References

- Harrison, M.J.; Kreps, D.M. Martingales and arbitrage in multiperiod securities markets. J. Econ. Theory 1979, 20, 381–408. [Google Scholar] [CrossRef]

- Harrison, M.J.; Pliska, S.R. Martingales and stochastic integrals in the theory of continuous trading. Stoch. Process. Their Appl. 1981, 11, 215–260. [Google Scholar] [CrossRef] [Green Version]

- Aït-Sahalia, Y.; Lo, A. Nonparametric estimation of state-price densities implicit in financial asset prices. J. Financ. 1998, 53, 499–547. [Google Scholar] [CrossRef] [Green Version]

- Garcia, R.; Gencay, R. Pricing and hedging derivative securities with neural networks and a homogeneity hint. J. Econom. 2000, 94, 93–115. [Google Scholar] [CrossRef] [Green Version]

- Broadie, M.; Detemple, J.; Ghysels, E. American options with stochastic dividends and volatility: A nonparametric investigation. J. Econom. 2000, 94, 53–92. [Google Scholar] [CrossRef] [Green Version]

- Aït-Sahalia, Y.; Duarte, J. Nonparametric option pricing under shape restrictions. J. Econom. 2003, 116, 9–47. [Google Scholar]

- Stutzer, M. A simple nonparametric approach to derivative security valuation. J. Financ. 1996, 51, 1633–1652. [Google Scholar] [CrossRef]

- Buchen, P.W.; Kelly, M. The maximum entropy distribution of an asset inferred from option prices. J. Financ. Quant. Anal. 1996, 31, 143–159. [Google Scholar] [CrossRef]

- Stutzer, M. Simple entropic derivation of a generalized Black-Scholes model. Entropy 2000, 2, 70–77. [Google Scholar] [CrossRef] [Green Version]

- Alcock, J.; Auerswald, D. Empirical tests of canonical nonparametric American option-pricing methods. J. Futures Mark. 2010, 30, 509–532. [Google Scholar]

- Neri, C.; Schneider, L. A family of maximum entropy densities matching call option prices. Appl. Math. Financ. 2013, 20, 548–577. [Google Scholar] [CrossRef] [Green Version]

- Yu, X.; Liu, Q. Canonical least-squares Monte Carlo valuation of American options: Convergence and empirical pricing analysis. Math. Probl. Eng. 2014, 2014. [Google Scholar] [CrossRef]

- Yu, X.; Xie, X. Pricing American options: RNMs-constrained entropic least-squares approach. N. Am. J. Econ. Finance. 2015, 31, 155–173. [Google Scholar] [CrossRef]

- Liu, X.; Zhou, R.; Xiong, Y.; Yang, Y. Pricing interval European option with the principle of maximum entropy. Entropy 2019, 21, 788. [Google Scholar] [CrossRef] [Green Version]

- Feunou, B.; Okou, C. Good volatility, bad volatility and option pricing. J. Financ. Quant. Anal. 2019, 54, 695–727. [Google Scholar] [CrossRef] [Green Version]

- Day, T.; Lewis, C. Stock market volatility and the information content of stock index options. J. Econom. 1992, 52, 267–287. [Google Scholar] [CrossRef]

- Jackwerth, J.C. Option-implied risk-neutral distributions and implied binomial trees: A literature review. J. Deriv. 1999, 7, 66–82. [Google Scholar] [CrossRef] [Green Version]

- Britten-Jones, M.; Neuberger, A. Option prices, implied price processes, and stochastic volatility. J. Financ. 2000, 55, 839–866. [Google Scholar] [CrossRef]

- Jiang, G.; Tian, Y. The model-free implied volatility and its information content. Rev. Financ. Stud. 2005, 18, 1305–1342. [Google Scholar] [CrossRef]

- Yu, X.; Yang, L. Pricing American options using a nonparametric entropy approach. Discrete Dyn. Nat. Soc. 2014, 2014. [Google Scholar] [CrossRef] [Green Version]

- Ben-Tal, A. The entropic penalty approach to stochastic programming. Math. Oper. Res. 1985, 10, 263–279. [Google Scholar] [CrossRef]

- Brandimarte, P. Numerical Methods in Finance and Economics: A MATLAB Based Introduction, 2nd ed.; Wiley: New York, NY, USA, 2006. [Google Scholar]

- Shreve, S.E. Stochastic Calculus for Finance II-Continuous-Time Models; Springer: Berlin, Germany, 2004. [Google Scholar]

- Heston, S.L. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 1993, 6, 327–343. [Google Scholar] [CrossRef] [Green Version]

- Haley, M.R.; Walker, T. Alternative tilts for nonparametric option pricing. J. Futures Mark. 2010, 30, 983–1006. [Google Scholar] [CrossRef] [Green Version]

- Broadie, M.; Kaya, Z. Exact simulation of stochastic volatility and other affine jump diffusion processes. Oper. Res. 2006, 54, 217–231. [Google Scholar] [CrossRef]

- Kahaner, D.; Moler, C.; Nash, S. Numerical Methods and Software; Prentice-Hall: Upper Saddle River, NJ, USA, 1989. [Google Scholar]

{kind=link}

{kind=link}

| Underling Price S0 | 48 | 50 | 52 | 54 | 56 |

| Strikes of OTM Calls | 34, 38, 42, 46 | 36, 40, 44, 48 | 38, 42, 46, 50 | 40, 44, 48, 52 | 42, 46, 50, 54 |

| Strikes of OTM Puts | 50, 54, 58, 62 | 52, 56, 60, 64 | 54, 60, 64, 68 | 56, 58, 62, 66 | 58, 62, 64, 70 |

| Underling price S0 | 48 | 50 | 52 | 54 | 56 |

| 1st-order RNM | Real value: 0.0100 | ||||

| 0.0100 | 0.0100 | 0.0100 | 0.0100 | 0.0100 | |

| 2nd-order RNM | Real value: 0.0401 | ||||

| 0.0401 | 0.0401 | 0.0401 | 0.0401 | 0.0401 | |

| Asset Price S0 | Time to Maturity (year) | μ1 = 5% | B–S Prices(True Values) | μ2 = 100% | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| RNM–Entropy | Canonical | RNM–Entropy | Canonical | |||||||

| Estimates | Diff (%) | Estimates | Diff (%) | Estimates | Diff (%) | Estimates | Diff (%) | |||

| 48 | 1/12 | 0.1272 | 0.0787 | 0.1287 | 1.2589 | 0.1271 | 0.1273 | 0.1574 | 0.1288 | 1.3674 |

| 1/4 | 0.7392 | 0.0406 | 0.7407 | 0.2436 | 0.7389 | 0.7395 | 0.0812 | 0.7423 | 0.4628 | |

| 1/2 | 1.6319 | −0.0123 | 1.6317 | −0.0245 | 1.6321 | 1.6317 | −0.0245 | 1.6314 | −0.0417 | |

| 3/4 | 2.4430 | 0.0082 | 2.4424 | −0.0164 | 2.4428 | 2.4437 | 0.0368 | 2.4422 | −0.0246 | |

| 1 | 3.1920 | −0.0438 | 3.1928 | −0.0188 | 3.1934 | 3.1918 | −0.0501 | 3.1915 | −0.0595 | |

| 50 | 1/12 | 0.4899 | 0.0408 | 0.4913 | 0.3267 | 0.4897 | 0.4902 | 0.1021 | 0.4918 | 0.4312 |

| 1/4 | 1.4161 | 0.0424 | 1.4148 | −0.0495 | 1.4155 | 1.4163 | 0.0565 | 1.4146 | −0.0653 | |

| 1/2 | 2.4961 | 0.0441 | 2.4934 | −0.0641 | 2.4950 | 2.4964 | 0.0561 | 2.4930 | −0.0788 | |

| 3/4 | 3.4095 | −0.0352 | 3.4118 | 0.0323 | 3.4107 | 3.4092 | −0.0440 | 3.4122 | 0.0426 | |

| 1 | 4.2345 | −0.0165 | 4.2345 | −0.0165 | 4.2352 | 4.2351 | −0.0024 | 4.2343 | −0.0203 | |

| 52 | 1/12 | 1.3067 | 0.0306 | 1.3053 | −0.0766 | 1.3063 | 1.3071 | 0.0612 | 1.3050 | −0.1011 |

| 1/4 | 2.4003 | 0.0208 | 2.3994 | −0.0167 | 2.3998 | 2.4005 | 0.0292 | 2.3993 | −0.0220 | |

| 1/2 | 3.5816 | −0.0140 | 3.5805 | −0.0447 | 3.5821 | 3.581 | −0.0307 | 3.5800 | −0.0590 | |

| 3/4 | 4.5610 | −0.0132 | 4.5601 | −0.0329 | 4.5616 | 4.5608 | −0.0175 | 4.5598 | −0.0405 | |

| 1 | 5.4331 | −0.0221 | 5.4361 | 0.0331 | 5.4343 | 5.4312 | −0.0570 | 5.4367 | 0.0437 | |

| 54 | 1/12 | 2.6331 | −0.0190 | 2.6354 | 0.0683 | 2.6336 | 2.6328 | −0.0304 | 2.6360 | 0.0902 |

| 1/4 | 3.6821 | −0.0244 | 3.6833 | 0.0081 | 3.6830 | 3.6825 | −0.0136 | 3.6834 | 0.0107 | |

| 1/2 | 4.8774 | −0.0266 | 4.8769 | −0.0369 | 4.8787 | 4.8772 | −0.0307 | 4.8763 | −0.0487 | |

| 3/4 | 5.8785 | −0.0459 | 5.8773 | −0.0663 | 5.8812 | 5.8784 | −0.0476 | 5.8761 | −0.0862 | |

| 1 | 6.7745 | −0.0443 | 6.7749 | −0.0384 | 6.7775 | 6.7741 | −0.0502 | 6.7733 | −0.0614 | |

| 56 | 1/12 | 4.3407 | −0.0253 | 4.3431 | 0.0299 | 4.3418 | 4.3410 | −0.0184 | 4.3434 | 0.0359 |

| 1/4 | 5.2165 | −0.0364 | 5.2165 | −0.0364 | 5.2184 | 5.2163 | −0.0402 | 5.2156 | −0.0546 | |

| 1/2 | 6.3563 | −0.0236 | 6.3560 | −0.0283 | 6.3578 | 6.3564 | −0.0220 | 6.3556 | −0.0340 | |

| 3/4 | 7.3468 | −0.0367 | 7.3462 | −0.0449 | 7.3495 | 7.3465 | −0.0408 | 7.3456 | −0.0530 | |

| 1 | 8.2449 | −0.0412 | 8.2509 | 0.0315 | 8.2483 | 8.2445 | −0.0461 | 8.2514 | 0.0378 | |

| Asset Price S0 | Time to Maturity(Year) | Heston (True Prices) | RNM–Entropy | Canonical | ||

|---|---|---|---|---|---|---|

| Estimates | Difference (%) | Estimates | Difference (%) | |||

| 48 | 1/12 | 1.1963 | 1.1970 | 0.0611 | 1.2044 | 0.6732 |

| 1/4 | 2.7061 | 2.7075 | 0.0503 | 2.7150 | 0.3287 | |

| 1/2 | 3.9327 | 3.9319 | −0.0215 | 3.9309 | −0.0465 | |

| 3/4 | 4.7408 | 4.7427 | 0.0405 | 4.7387 | −0.0454 | |

| 1 | 5.3936 | 5.3906 | −0.0552 | 5.3904 | −0.0602 | |

| 50 | 1/12 | 1.9506 | 1.9517 | 0.0547 | 1.9586 | 0.4102 |

| 1/4 | 3.6527 | 3.6553 | 0.0699 | 3.6491 | −0.0990 | |

| 1/2 | 4.9873 | 4.9903 | 0.0609 | 4.9795 | −0.1559 | |

| 3/4 | 5.8583 | 5.8558 | −0.0434 | 5.8639 | 0.0957 | |

| 1 | 6.5574 | 6.5562 | −0.0185 | 6.5539 | −0.0541 | |

| 52 | 1/12 | 2.9381 | 2.939 | 0.0302 | 2.9329 | −0.1758 |

| 1/4 | 4.7514 | 4.7527 | 0.0271 | 4.7495 | −0.0405 | |

| 1/2 | 6.1631 | 6.1621 | −0.0163 | 6.1550 | −0.1310 | |

| 3/4 | 7.0835 | 7.0846 | 0.0155 | 7.0761 | −0.1039 | |

| 1 | 7.8203 | 7.8184 | −0.0249 | 7.8291 | 0.1131 | |

| 54 | 1/12 | 4.1476 | 4.1467 | −0.0211 | 4.1567 | 0.2200 |

| 1/4 | 5.9904 | 5.9888 | −0.0275 | 5.9919 | 0.0251 | |

| 1/2 | 7.4492 | 7.4467 | −0.0329 | 7.4404 | −0.1182 | |

| 3/4 | 8.4063 | 8.4021 | −0.0496 | 8.3870 | −0.2296 | |

| 1 | 9.1727 | 9.1772 | 0.0492 | 9.1598 | −0.1410 | |

| 56 | 1/12 | 5.5532 | 5.5517 | −0.0278 | 5.5596 | 0.1157 |

| 1/4 | 7.3555 | 7.3524 | −0.0423 | 7.3458 | −0.1318 | |

| 1/2 | 8.8344 | 8.8366 | 0.0249 | 8.8253 | −0.1035 | |

| 3/4 | 9.8164 | 9.8123 | −0.0416 | 9.7998 | −0.1693 | |

| 1 | 10.6052 | 10.6102 | 0.0471 | 10.6182 | 0.1224 | |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yu, X. Risk-Neutrality of RND and Option Pricing within an Entropy Framework. Entropy 2020, 22, 836. https://doi.org/10.3390/e22080836

Yu X. Risk-Neutrality of RND and Option Pricing within an Entropy Framework. Entropy. 2020; 22(8):836. https://doi.org/10.3390/e22080836

Chicago/Turabian StyleYu, Xisheng. 2020. "Risk-Neutrality of RND and Option Pricing within an Entropy Framework" Entropy 22, no. 8: 836. https://doi.org/10.3390/e22080836

APA StyleYu, X. (2020). Risk-Neutrality of RND and Option Pricing within an Entropy Framework. Entropy, 22(8), 836. https://doi.org/10.3390/e22080836