1. Introduction

With the rapid increase of the use of network based approaches in economics, more and more key questions are approached from this perspective. The applications are diverse, and many times, they bring new insights. Without trying to exhaust an already large literature, we can mention the applications to business cycles [

1], systemic risk [

2,

3,

4,

5,

6], and contagion and spillovers [

7,

8,

9].

In this paper, we aim at studying a less discussed topic from a network perspective. We aim at analyzing the transmission of monetary policy shocks to the financial markets. In this sense, we look at the way financial networks modify following monetary policy shocks. To measure the change, we use an entropy measure of networks based on singular value decomposition and on von Neumann entropy. The main question of this paper is as follows: do monetary policy shocks impact the financial networks?

There are several directions in which we contribute to the literature. Our first contribution is related to the analysis of monetary policy shocks in the context of networks. There is a rapidly growing literature, with contributions mainly focusing on the role of production networks. A reference paper in this direction is one published by Weber and Ozdagli [

10], who used the spatial structure of production in the United States (based on the input–output structure) to measure how this affects the transmission of monetary policy shocks. We can also mention Caraiani et al. [

11], who studied the propagation of monetary policy shocks using specific measures of production networks such as upstreamness and downstreamness, finding that they matter for the transmission of monetary policy shocks. In a related paper [

12], Caraiani studied in an international context the transmission of oil shocks using network measures such as density and skewness of links, finding again that the network structure matters significantly for the transmission of (oil) shocks.

A second contribution is to the field of financial networks. We have already cited some reference papers applying networks approaches to the financial markets. Here, we contribute to the understanding of the relationship between monetary policy shocks and the stock market, but we also quantify the structural changes in the financial markets networks using an entropy measure.

Finally, our last contribution is related to the use of entropy in measuring the changes in the financial markets networks following a particular shock—here, a monetary policy shock. There are various ways to measure the entropy of financial markets. A discussion of the various ways to measure entropy in financial networks is conducted in [

13]. Below, we also review a few contributions on this topic and outline our contribution in this direction.

A significant contribution was made by [

14], who applied transfer entropy to study the relationships between 187 companies in the world. This approach allowed him to identify a central role for insurance companies from large economies such as the United States and the Euro Area.

A different contribution looked at the ability of singular-value-based entropy of financial markets to signal the state of the market. In [

15], entropy is measured using a singular value decomposition of the matrix of correlations of financial stock. Caraiani also showed that this entropy measure has predictive ability for the dynamics of the stock market. More recently, Caraiani [

16] extended the work to the case of international financial markets, showing that there are spillovers of entropy between the big financial markets, with entropy measured again based on the singular value based decomposition of the financial stock.

Another contribution on the use of entropy was given by Bekiros et al. [

17], who used entropy measures of the financial markets to show that there is a decoupling between commodity and equity markets. Another approach consisted of showing that we can use permutation entropy to analyze how the degree of information changes during a market crash [

18]. The main result of this latter paper was that during financial market crashes, the permutation entropy decreases.

In this paper, we extend previous research from several literature strands (i.e., networks and monetary policy, financial networks, and entropy of financial networks) by making several contributions. First, we show that we can approach the topic of the changes in the financial networks following monetary policy shocks using networks measures. As far as we know, this has not been studied extensively before. There are, however, a few studies that are close to ours. For example, Beltran et al. [

19] found that Fed Funds networks (along with abundant reserves) tend to dampen the impact of monetary policy transmission. In a different framework, using agent-based modeling, Riccetti et al. [

20] found a significant role for a financial accelerator that was founded on three dimensions: a leverage one, a stock market one, and a network one. We can also mention the study by Silva et al. [

21], who consider a granular approach that takes into consideration the network relationships between agents, along with the balance sheets compositions. The inclusion of network data allowed them to study contagion effects as well. They applied their model to Brazilian data. However, our focus is rather on detecting the changes in financial networks following monetary policy shocks.

Second, we quantify the changes in the financial markets networks based on different measures of entropy. Different from previous studies, we focus on event studies with monetary policy shocks precisely identified following FED communications. Thus, we can to isolate the impact of such announcements by considering the changes in entropy. Since we consider windows of data before and after these announcements, we can isolate the impact solely of these announcements.

The paper is structured as follows. We first discuss the methodology used throughout the paper in the following section. In the

third Section, we present the data used in the empirical analysis. In the

fourth Section, we perform the empirical analysis by looking at the impact of monetary policy shocks on financial networks. Finally, in

Section five, we discuss the results and suggests possible extensions of the present result.

4. Results

4.1. Measuring the Entropy

In this section, we derive the measure of entropy that we are interested in. In contrast to previous contributions that have also used singular-value-based entropy to characterize financial networks (see [

15] or [

16]), we focus here on measuring the change in the singular-value-based or von Neumann entropy in pre- versus post- dates when the monetary policy shocks occur.

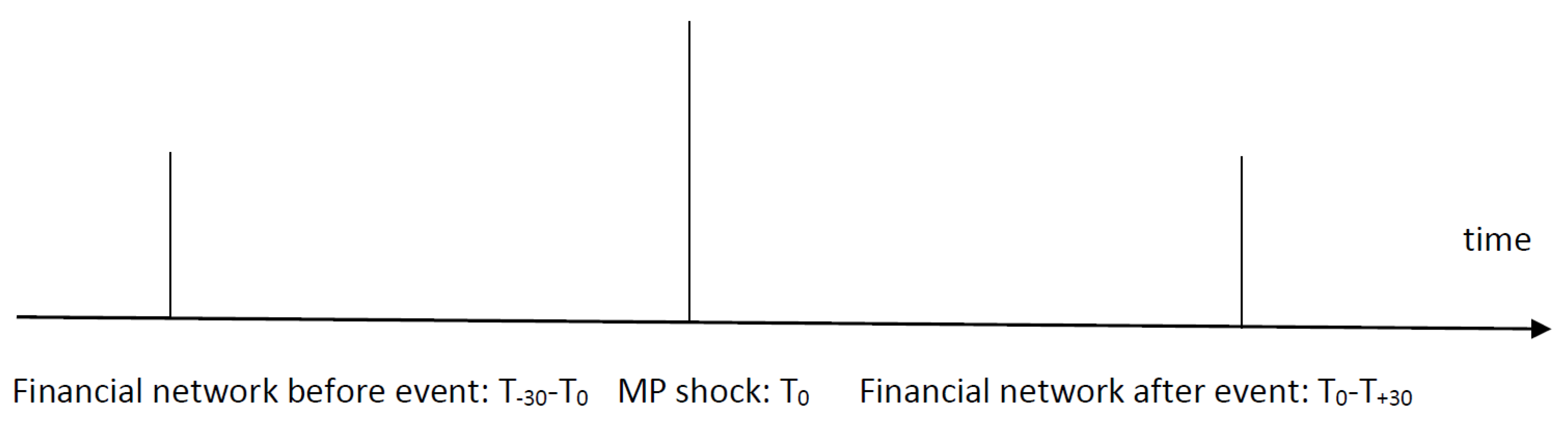

An informational issue is also critical to ensure that the change in the financial network(s) comes only from the current monetary policy shock. To counter this effect, we isolate the impact of each monetary policy shock by considering the state of the financial network (as characterized by the entropy) before and after each event (or monetary policy shock). The informational issue that we discuss is represented below, see

Figure 1:

While previous studies (see [

15,

16]) relied on a sliding window, here, we compute for each monetary policy shock that entropy for the financial networks before the event and after the event. We consider a window for which the financial network is derived. This is used only before and after the event. Thus, the resulting series is the series of changes in the singular-value-based entropy ex post compared to ex ante.

To control for the robustness of the results to the size of the window used, we vary the window’s dimension and consider windows of 20, 30, and 45 days (these correspond to calendar days, while the trading days are just at most five each week). Our main interest relies on financial networks that are affected only by the events we consider, i.e., monetary policy shocks. In this sense, considering that only windows of 20, 30, or 45 days fulfills this essential criterion while ensuring enough observations to construct the financial networks. We also consider a larger window of 60 days (with the results available at request) for robustness. However, it might sometimes overlap with previous or subsequent monetary policy shocks, but this should be taken only as additional evidence.

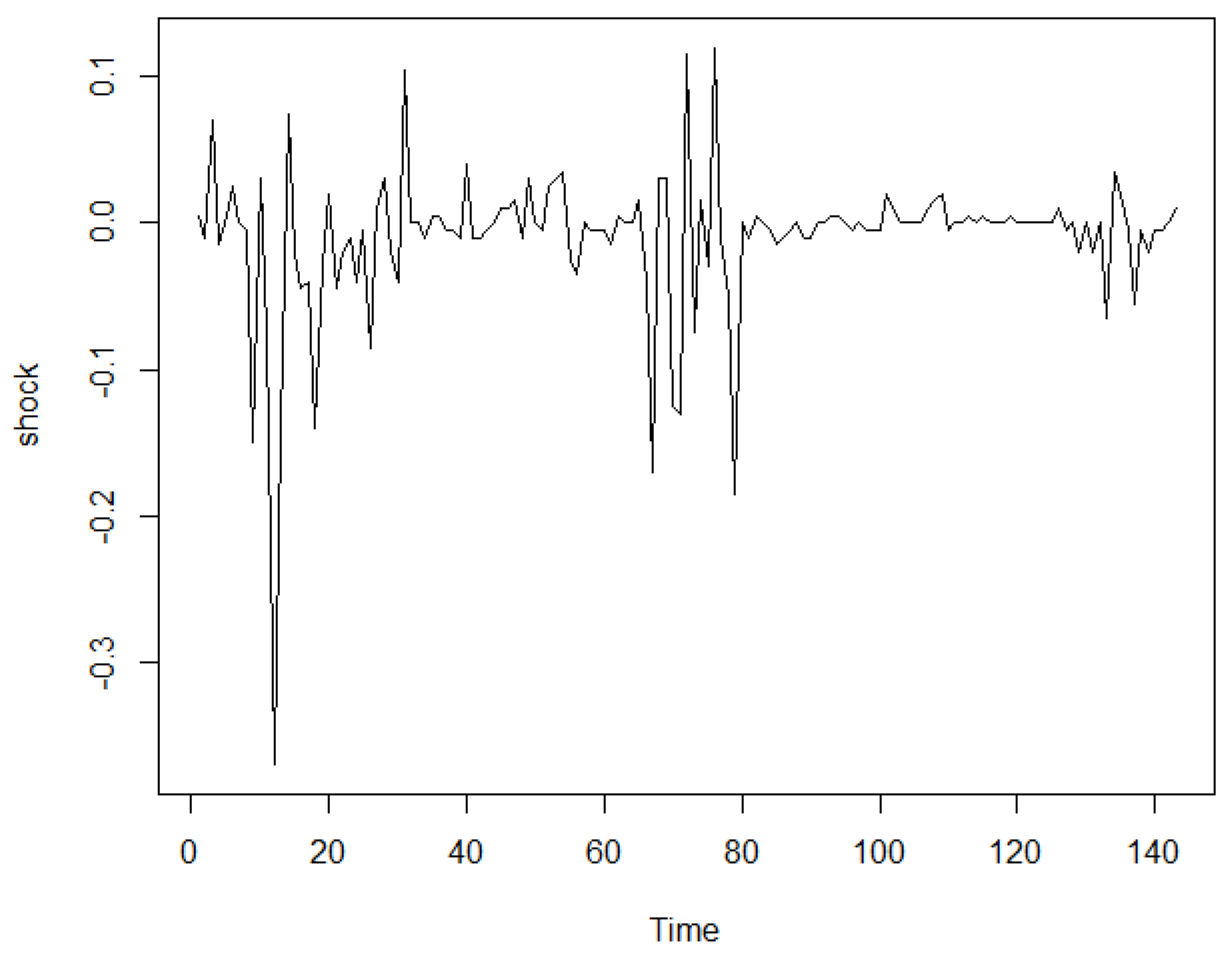

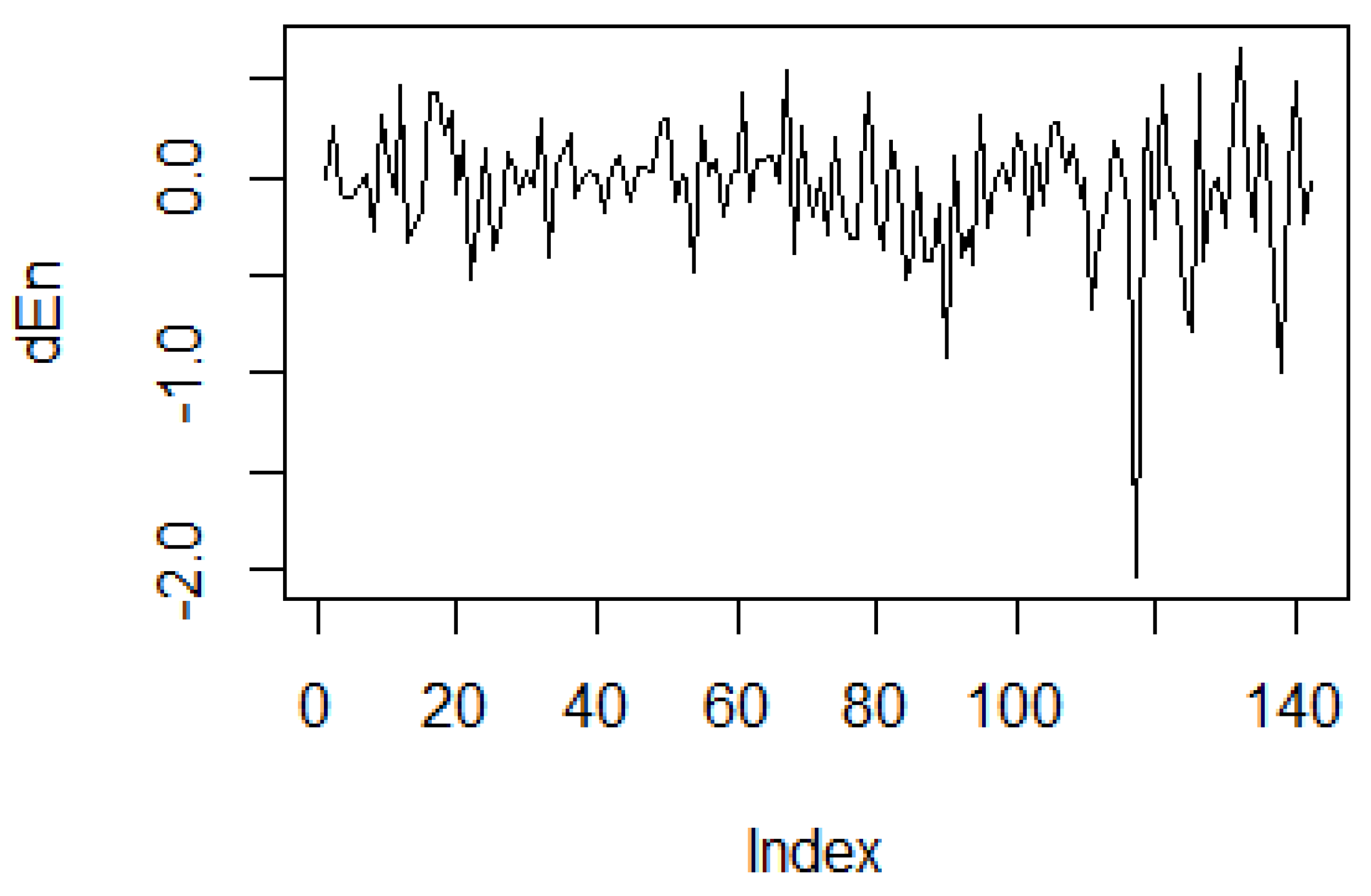

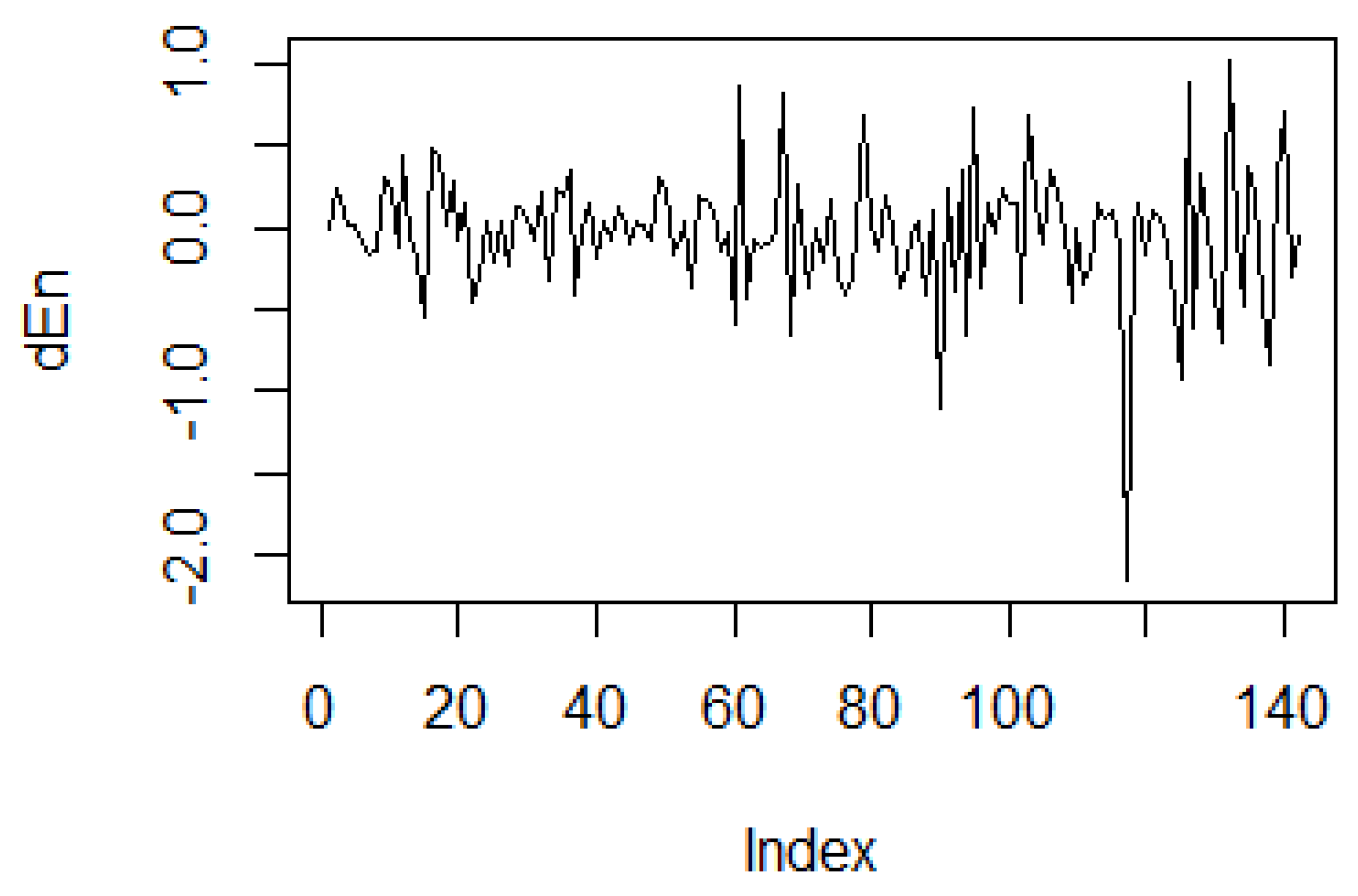

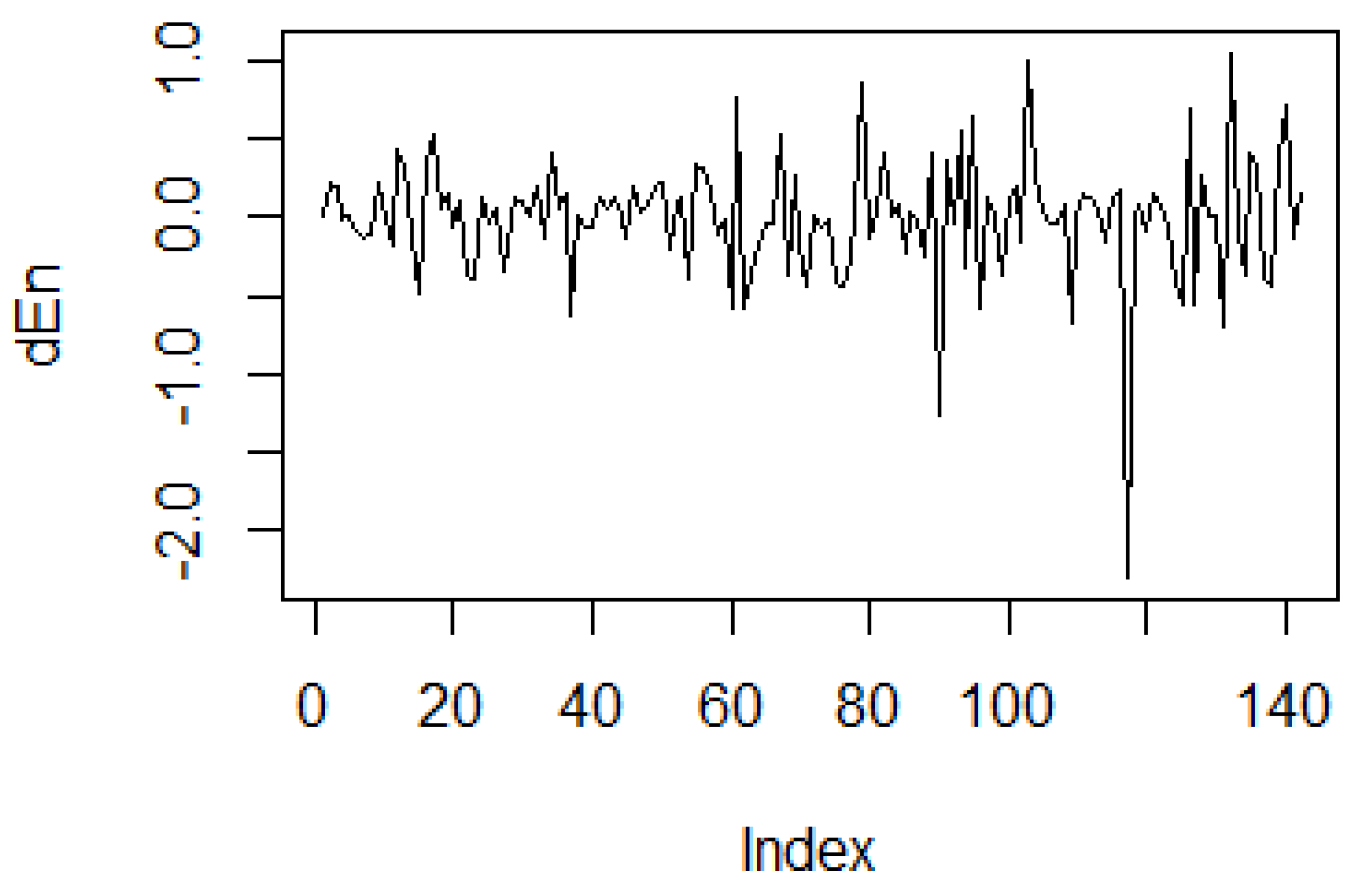

In

Appendix B and

Appendix C, we show the log-difference of the Shannon entropy measure for the different window sizes used, namely for 20, 30, and 45 days (the figures for von Neumann entropy are similar, and they are available at request). Our data start from 2000, ensuring that there are enough observations to carry the statistical analysis. The dot-com crisis from 2001 is marked through a decreasing value of entropy. A similar pattern is noticed after about eight years, corresponding to the timing of the great financial crisis. The

x-axis is interpreted as showing the observations on entropy changes, while the

y-axis shows the magnitude of the change.

4.2. The Impact of Monetary Policy Shocks on Financial Networks

This section aims to answer the paper’s central research question: do monetary policy shocks impact the financial networks? We use the singular-value-based entropy and von Neumann entropy measures derived in the last section to answer this question. We test the hypothesis of whether monetary policy shocks have a significant impact on financial networks as measured through the change in the entropy of the financial networks.

We consider the following basic regression models. The model aims at capturing the relations between the shocks (the change in the monetary policy stance) and the entropy of the financial markets.

Here, is the change in the entropy, while are the monetary policy shocks. c is a constant, while are the residuals of the regression. For robustness, we use the Shannon entropy and the von Neumann entropy, including one based on a normalized version of the Laplacian.

Before performing the regression, we also test for the unit root in both monetary policy shocks and the change in entropy for various window sizes. The results are shown in

Appendix D. The unit root hypothesis is strongly rejected in each case, for either of the monetary policy shocks, for the different measures of entropy based on different approaches and window sizes.

Table 1 shows the regression results described in Equation (

1) for the Shannon entropy for the various window sizes considered: 20, 30, and 45 days. Although the

is low, the

F-test indicates that the model is significant from a statistical point of view (For those not familiar with the regression analysis, the

F-test is an overall test of significance for the estimated regression. The null hypothesis is that the model does not have significant explanatory power).

However, the key result is the statistically significant and negative coefficient associated with the MP shock in each case considered. In other words, monetary policy shocks lead to a reduction in the financial network’s entropy, as measured by the change in the singular-value-based entropy. The results are robust to the window size used, and they tend to become stronger for larger windows.

Additionally, we consider in

Table 2 and

Table 3 the von Neumann entropy, varying the window size as well. However, the results are not statistically significant.

In

Appendix E, we further test whether controlling for the correlation threshold changes the results for the Shannon entropy (we set the correlation weaker than 0.30 to 0). We were able to derive the results only for two types of windows of 20 and 30 observations. The results remain negative and statistically significant, and the magnitude is even larger than for the baseline case. We tried the same exercise for the von Neumann entropy; however, the results remained the same.

5. Discussion

In this paper, we aimed at approaching the issue of monetary policy effects on the financial markets from a network perspective. We analyzed whether monetary policy shocks statistically impact the financial networks (as constructed from the Dow Jones Industrial Average components). To measure the change in the financial networks, we used the change in the entropy (either singular-value-based or von Neumann).

The main contribution of this paper was to show that monetary policy shocks have indeed a statistically significant impact on financial networks: a positive monetary policy shock (corresponding to a tightening of the monetary policy and a higher interest rate) had a negative impact on the singular-value-based entropy of the financial networks. Our results are robust to varying the size of the window used to construct the financial networks. They are also robust to controlling for the significance of correlation. However, the results using the von Neumann entropy are not statistically significant.

The interpretation of the result is that the release of the new information through the Fed communications on the interest decreases the entropy of the financial market networks. This is a somewhat expected result since it reduces the degree of uncertainty in the financial markets.

There are a few novel results that can be outlined. First, we highlight the fact that monetary policy shocks do affect the financial networks. Previous studies (see [

10,

12,

16]) considered (production) networks that are invariant to changes in aggregate shocks, including monetary policy shocks. Our focus was on financial networks and how they respond to monetary policy shocks. Second, we also show that entropy measures of networks can be used to detect the changes in financial networks. This has been used before in a few studies; however, in this paper, we show that event studies can be combined with entropy to evaluate the impact of financial networks.

The results here can be further extended in various ways. For example, one can consider different ways to construct entropy from financial networks. Furthermore, financial networks can also be characterized in many ways, including based on measures that are more intuitively linked to financial and economic concepts (such as risk, for example), which can be further used to analyze the impact of monetary policy shocks in a network context.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}