Evolving Network Analysis of S&P500 Components: COVID-19 Influence of Cross-Correlation Network Structure

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

1.1. Literature Review

1.2. COVID-19 History

- December 2019 The first known cases have been identified in Wuhan, China.

- January 2020 The epidemic spreads to other provinces of China.

- February 2020 Italy is affected with a rapidly growing number of infected and fatal cases.

- March 2020 The USA overtakes China and Italy with the highest number of confirmed cases in the world.

1.3. Paper Structure

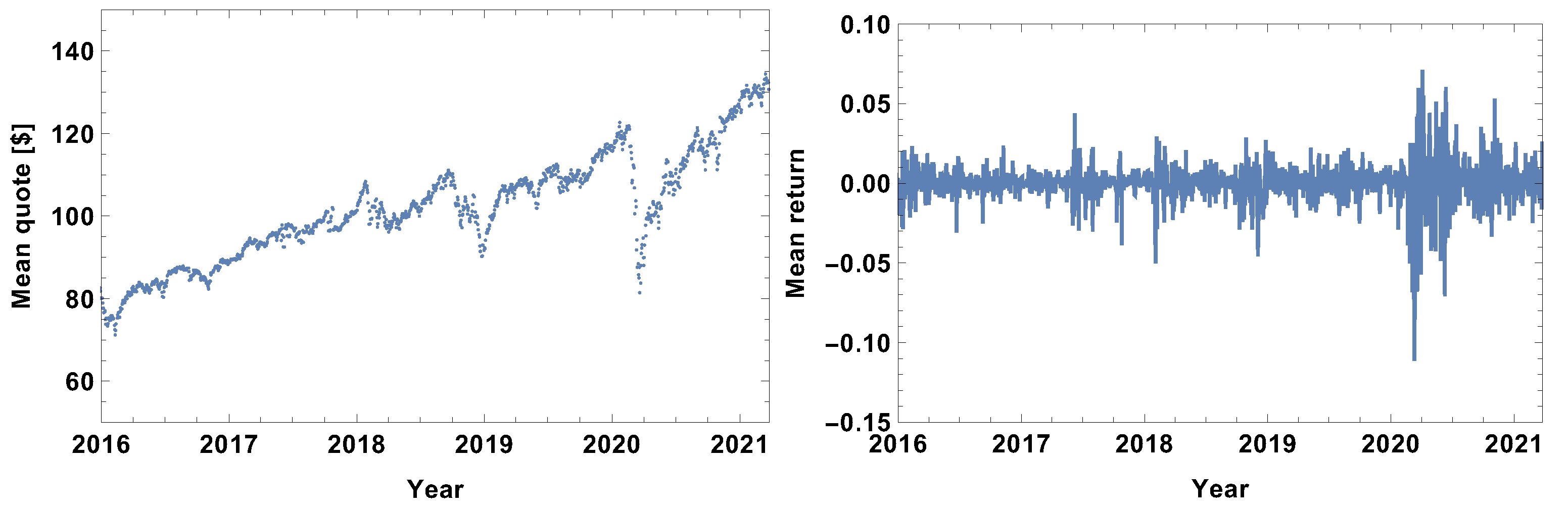

2. Data

3. Methods

- Distance matrix calculations;

- Network construction;

- Network feature analysis.

3.1. Distance Matrix

3.2. Network Construction

- Strongly connected time series—the companies are connected when the distance is shorter than the first quartile of the distances in the analysed distance matrix, so the network is built on a set of the 25% shortest links;

- Weakly connected time series—the companies are connected when the distance is longer than the third quartile of the distance in the analysed distance matrix, so the network is built on a set of the 25% longest links;

- The most typical connections—the companies are connected when the distance between them is longer than the first quartile and shorter than the third quartile of the distances in the analysed distance matrix, so the network is built on this set of 50% of the links;

- Significantly connected time series—the companies are connected in the network when the distance between them is shorter than the median of the distances in the analysed distance matrix, so the network is built on a set of 50% of the links.

3.3. Network Analysis

- Choose the representative set of companies (shares);

- Verify the integrity of the time series and their length (should be identical);

- Normalise the time series by converting them to the daily log-return time series;

- Choose the time window size;

- For each of the time series, starting at the beginning, take the interval of the time window length and calculate the time series correlation (distance) matrix;

- Based on the correlation matrix, generate the network. Here, four possible strategies are considered: (i) strongly, (ii) weakly, (iii) most typical, (iv) significantly connected networks, so the following steps should be repeated for each network type;

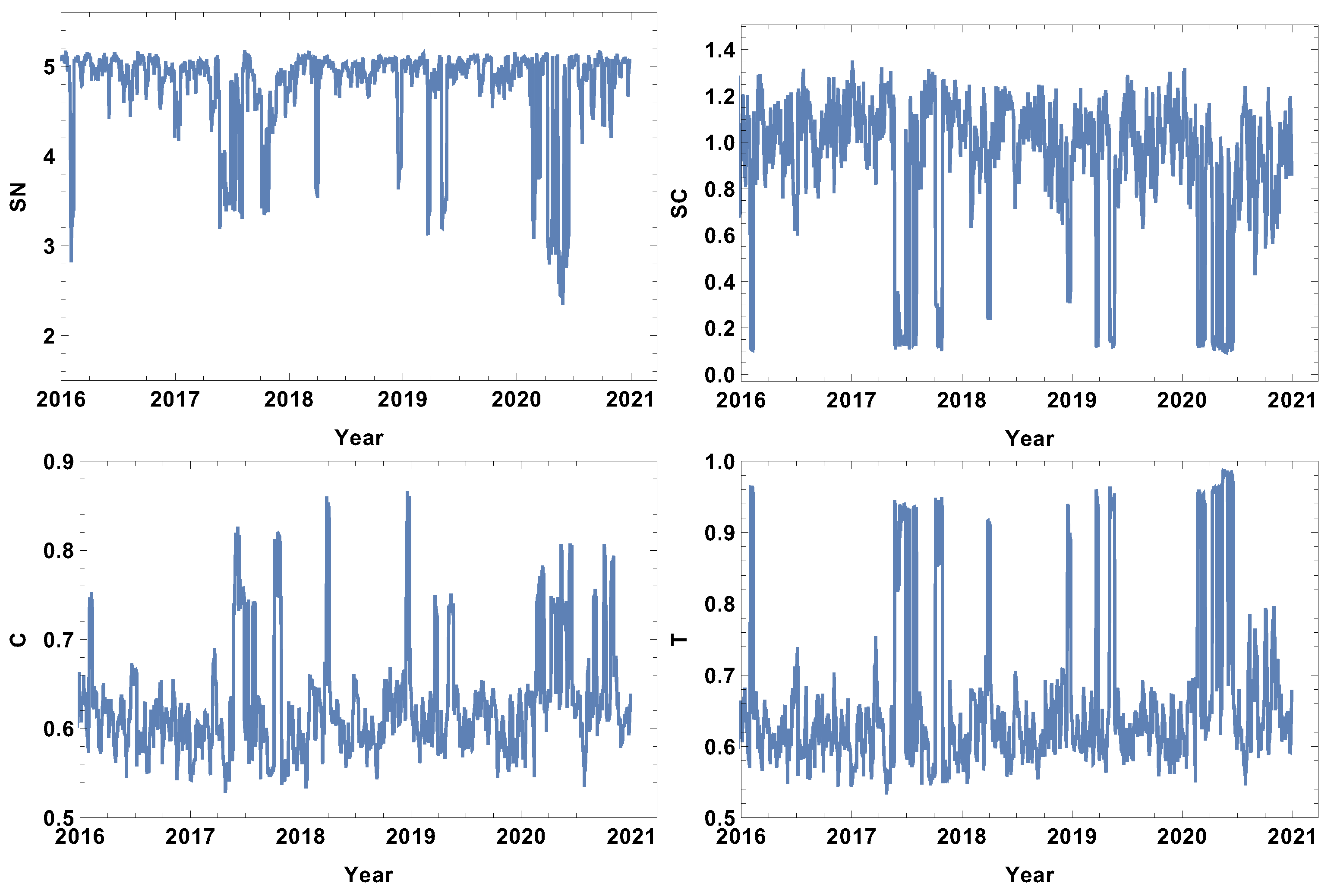

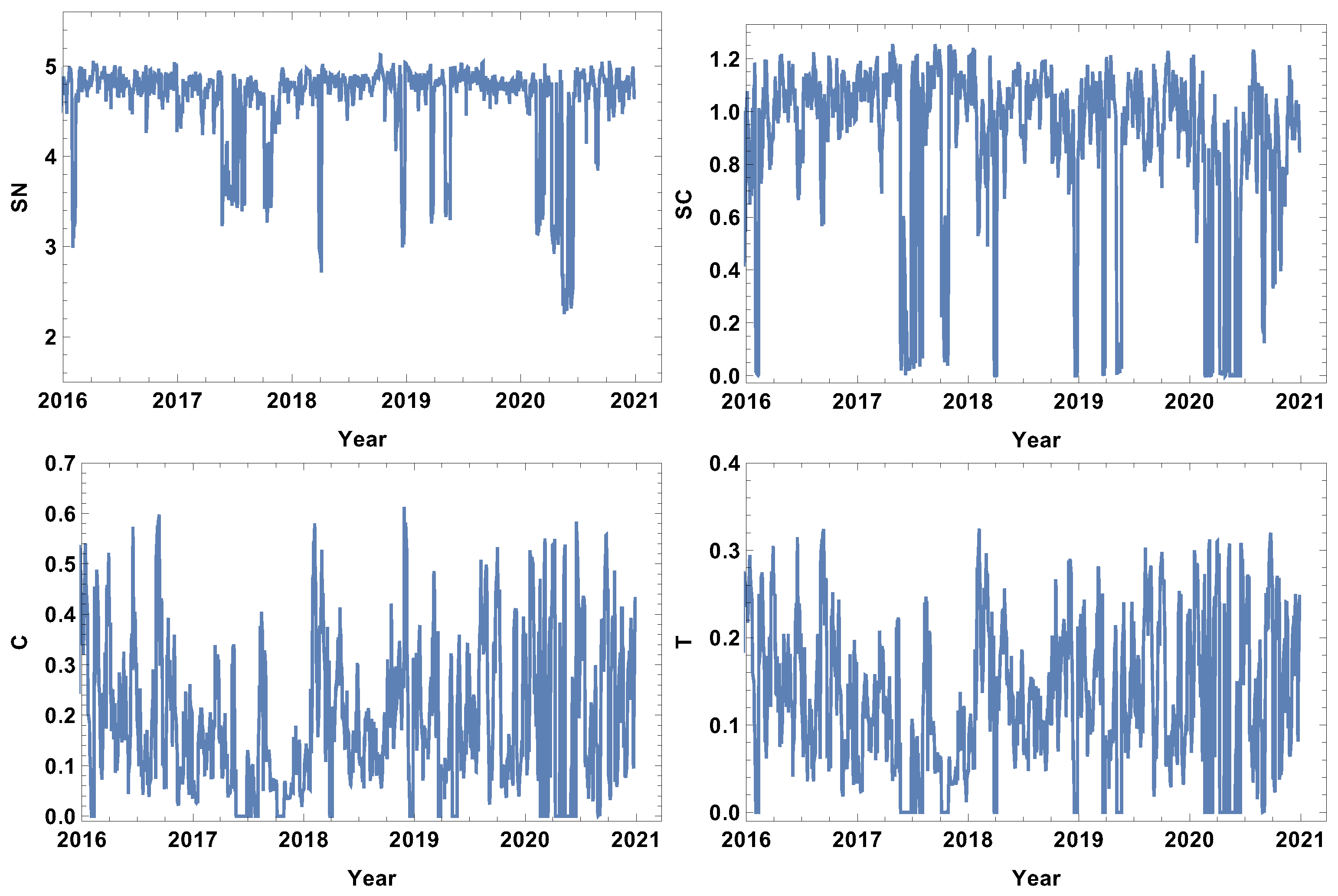

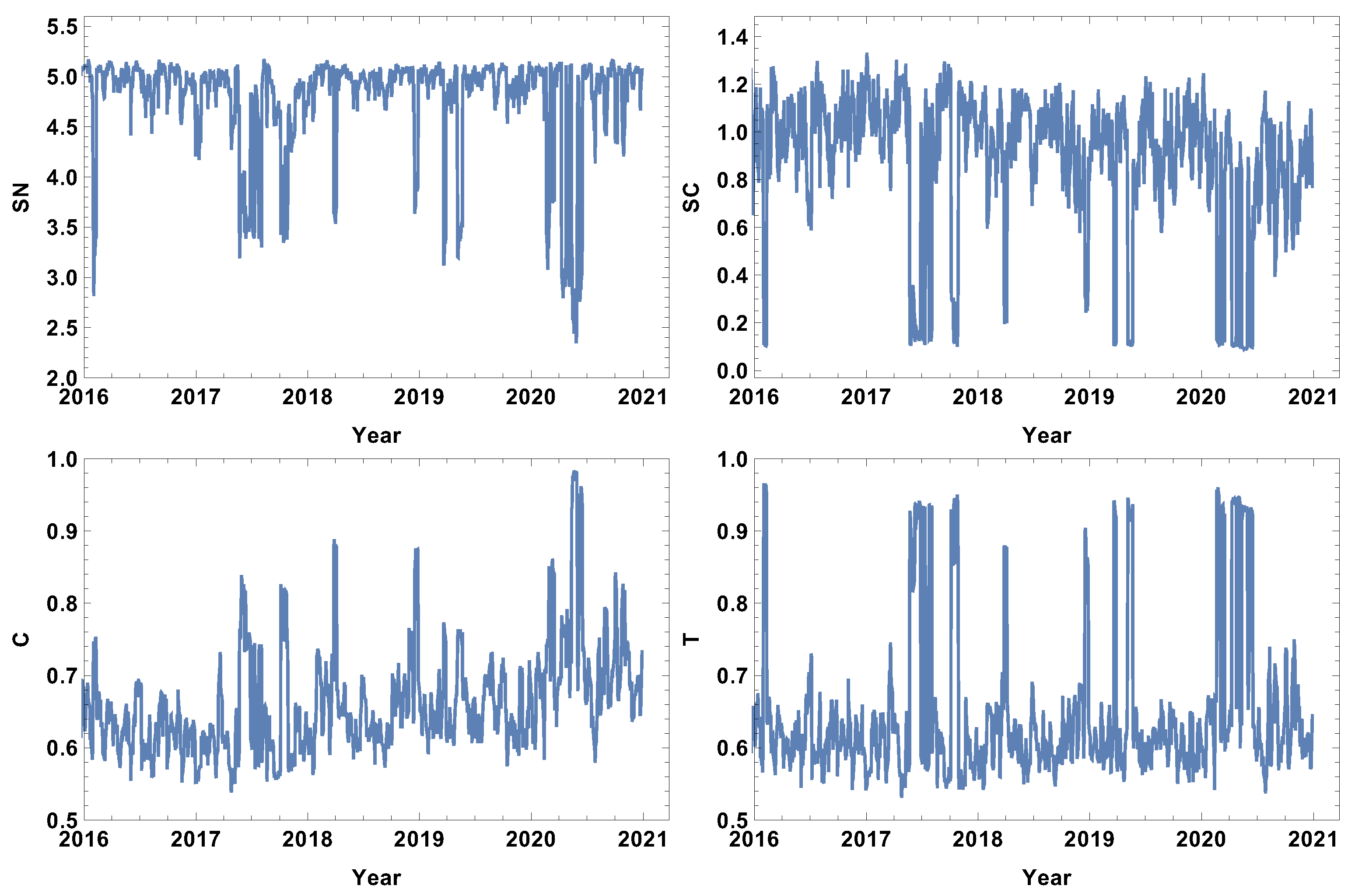

- Calculate the network’s characteristics: rank entropy, cycle entropy, averaged clustering coefficient and transitivity;

- Move the starting point by one point and repeat steps 5–8. Continue until the end of the time series length is reached.

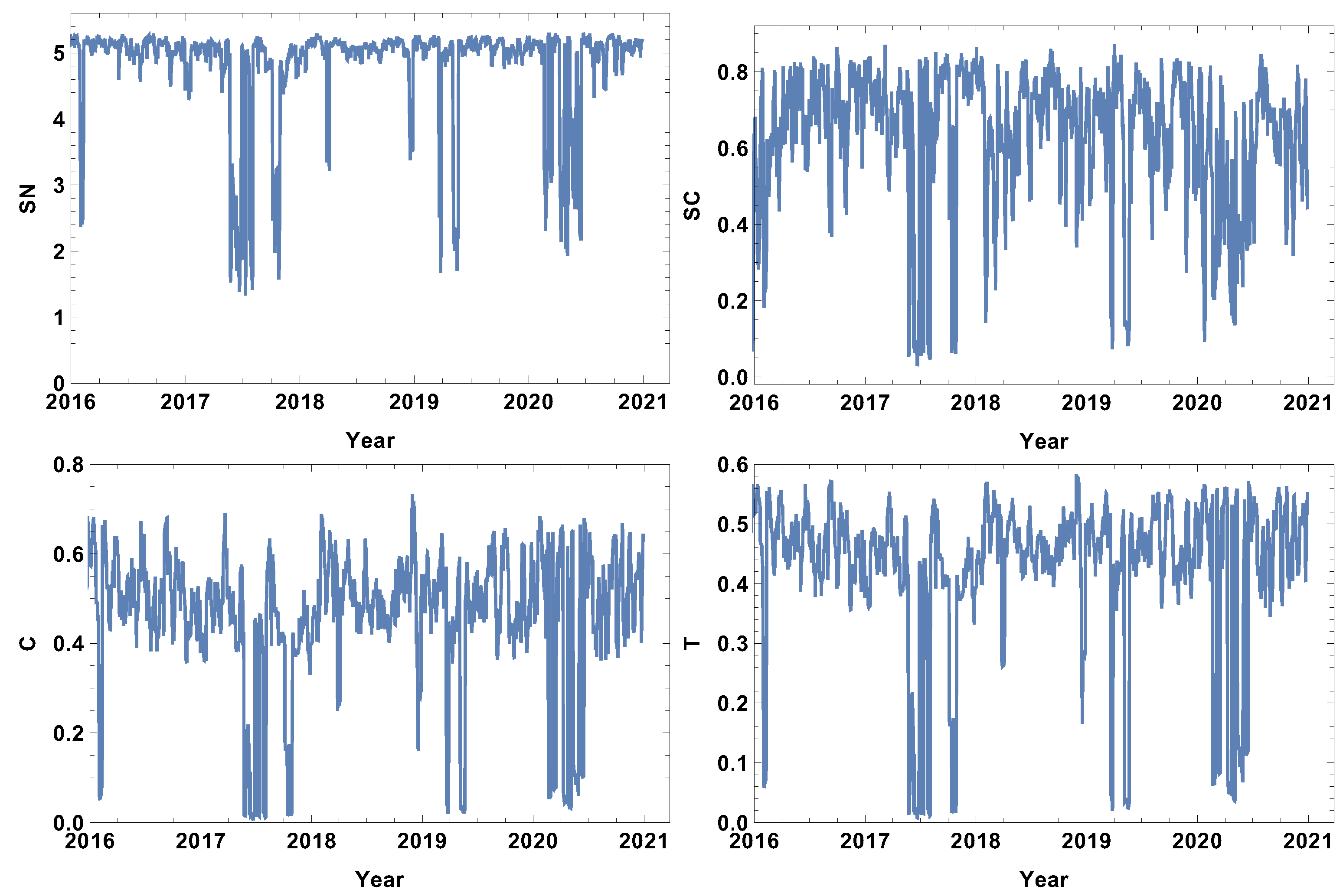

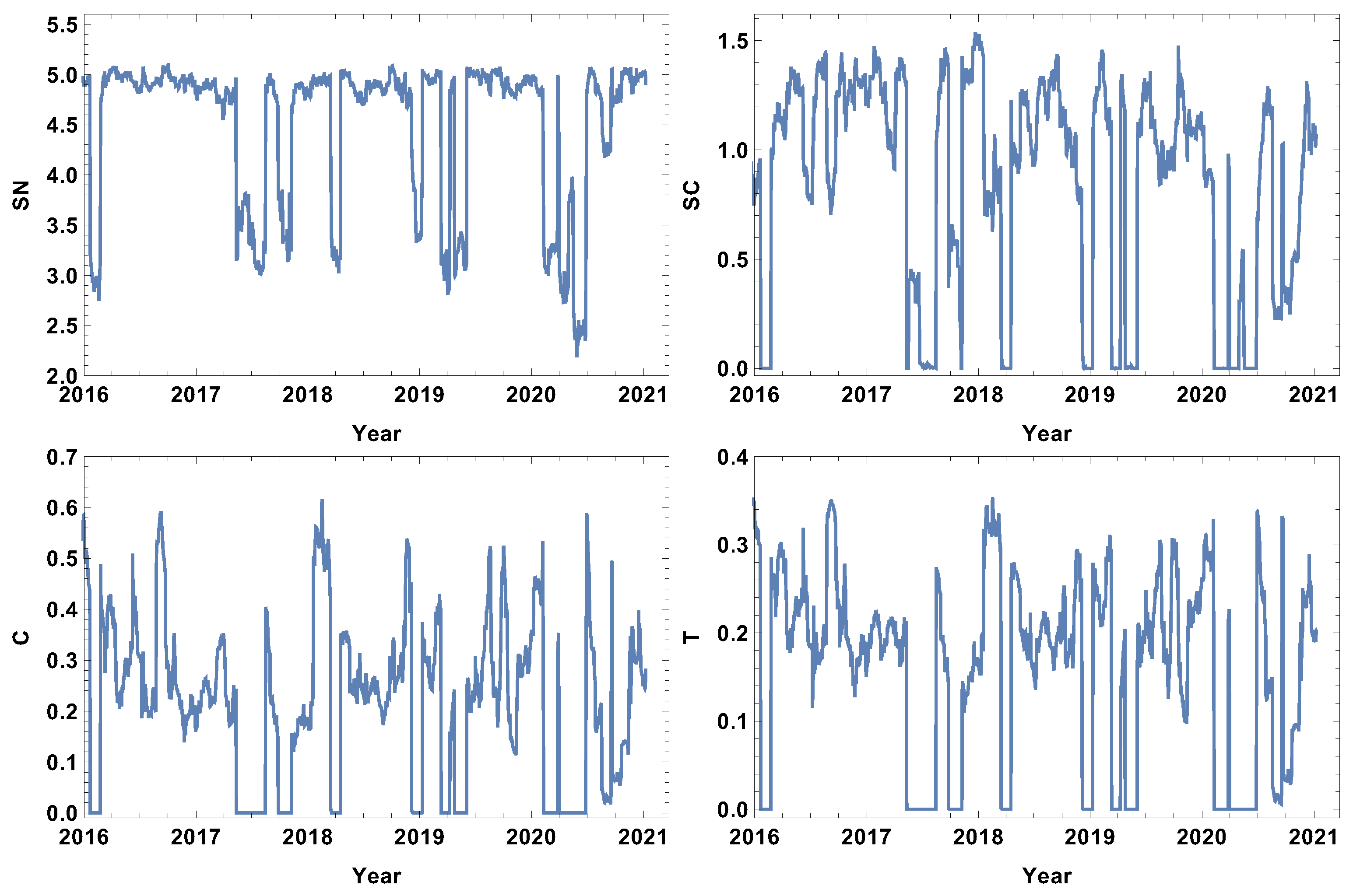

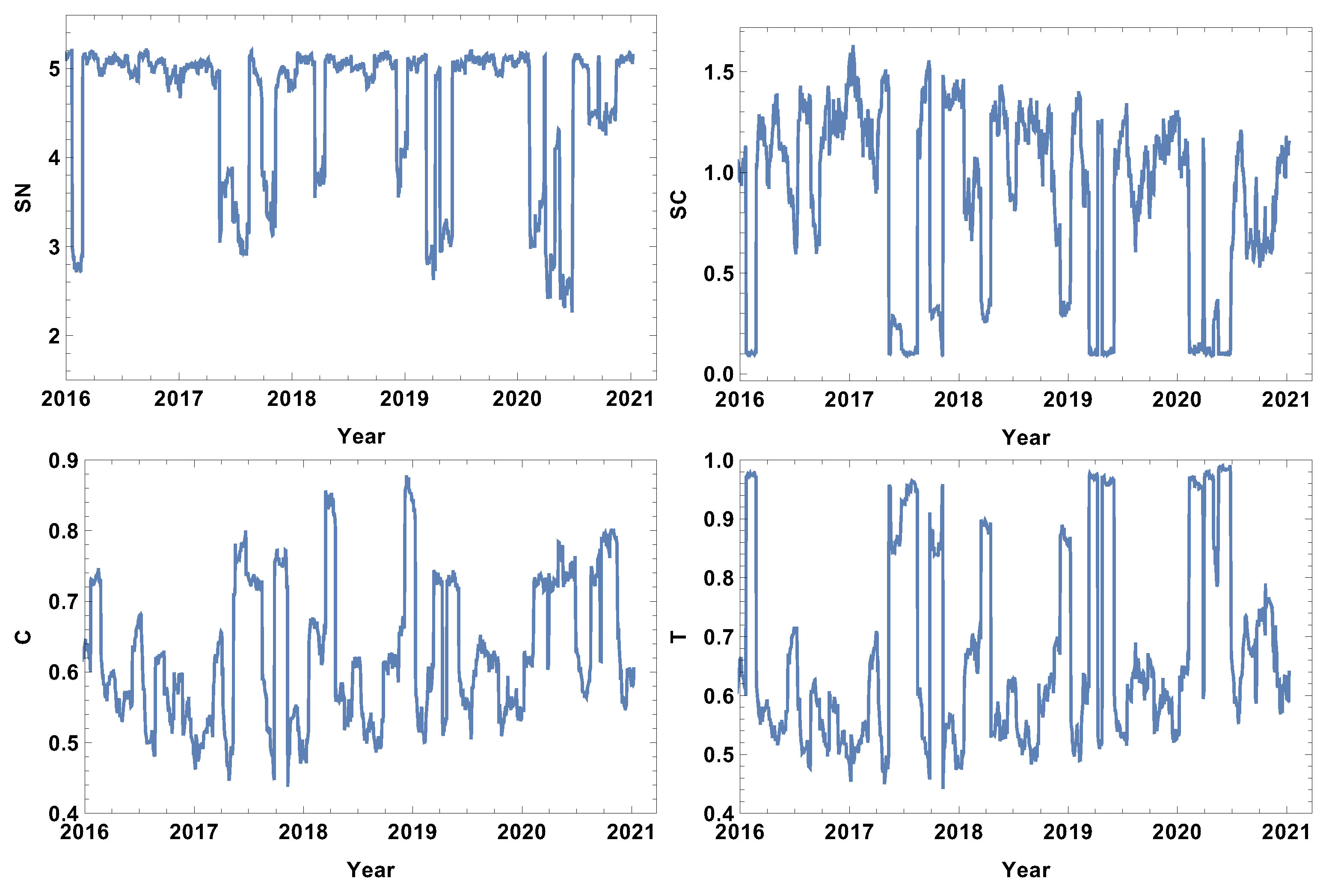

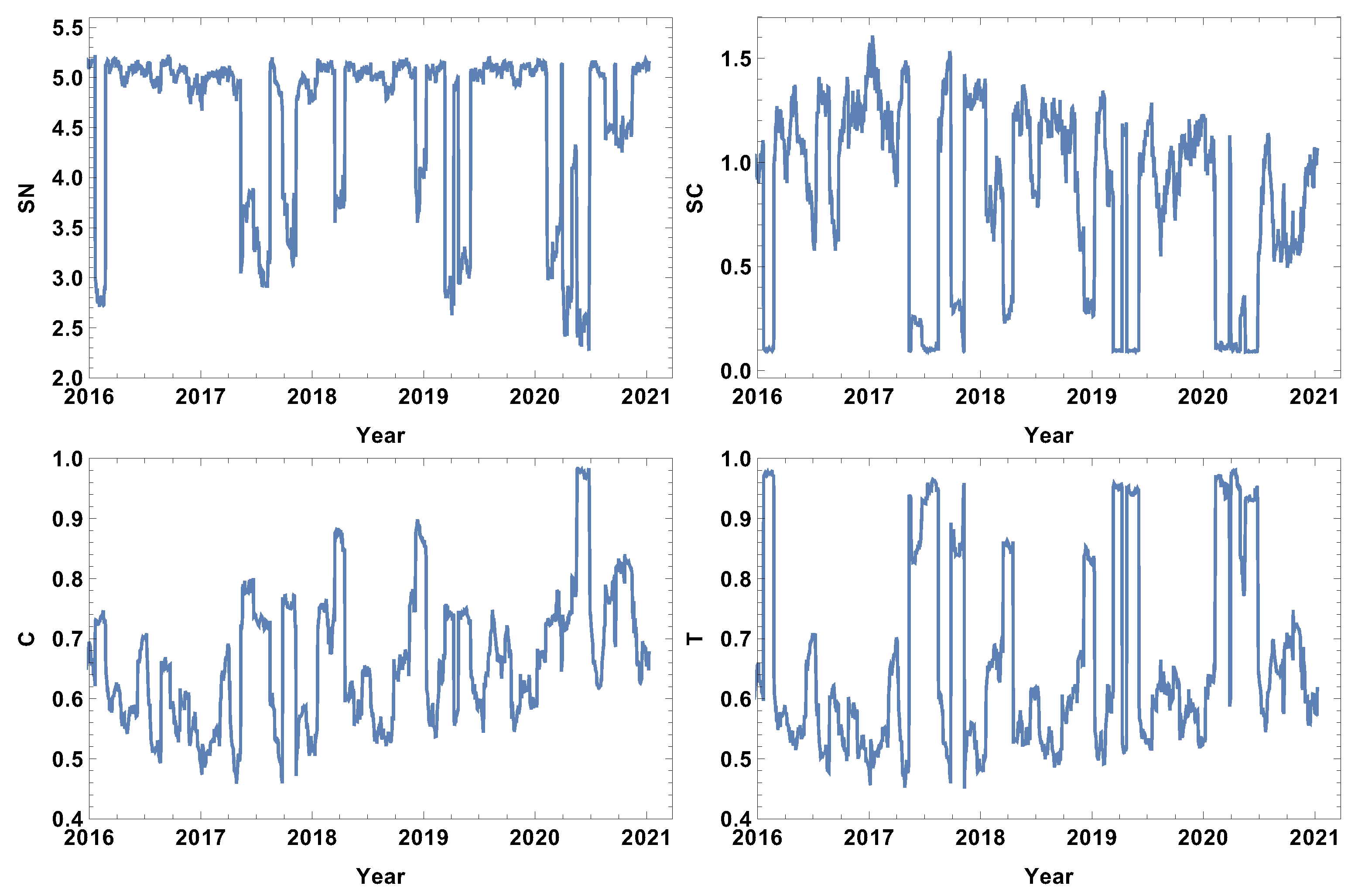

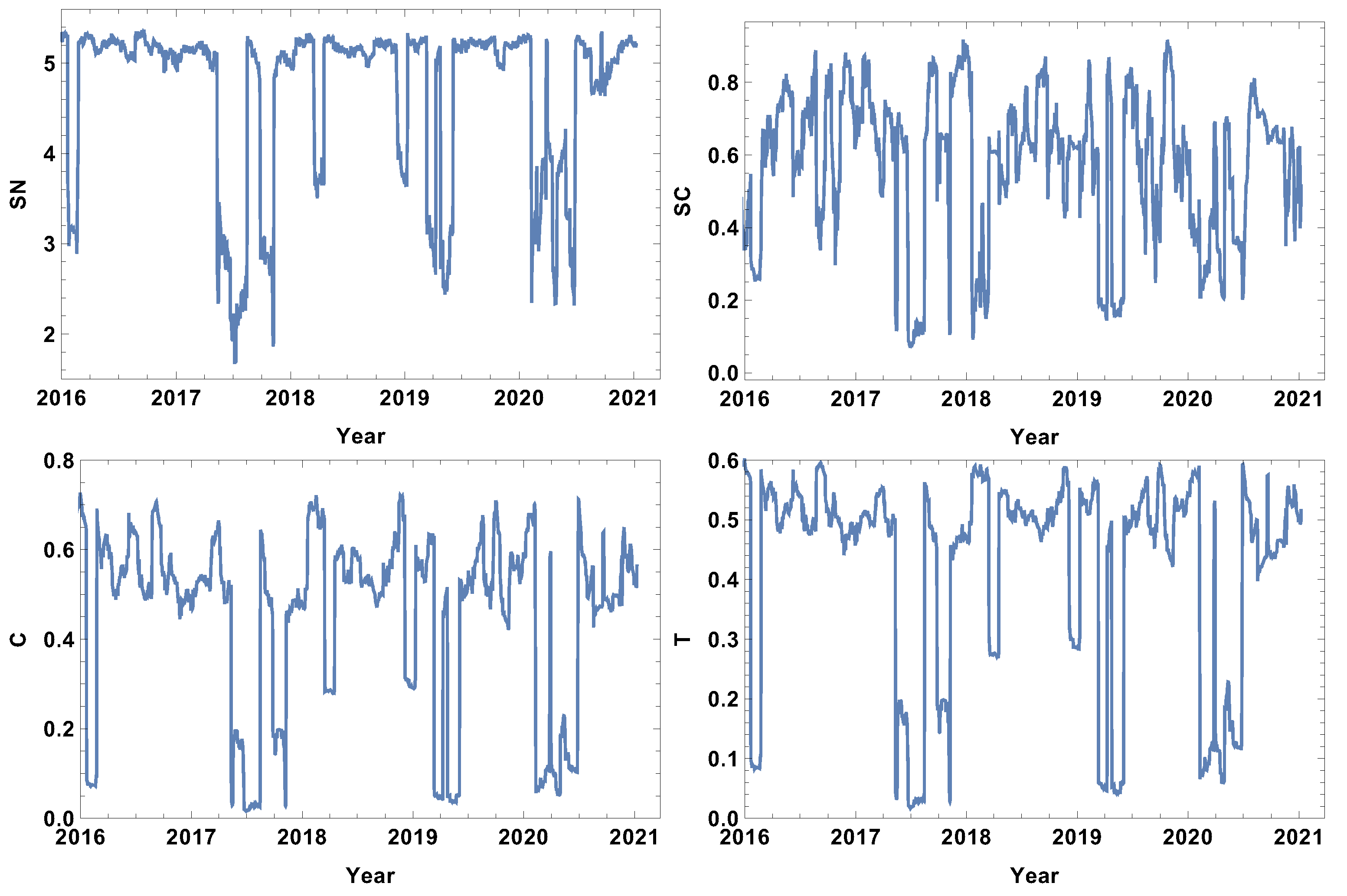

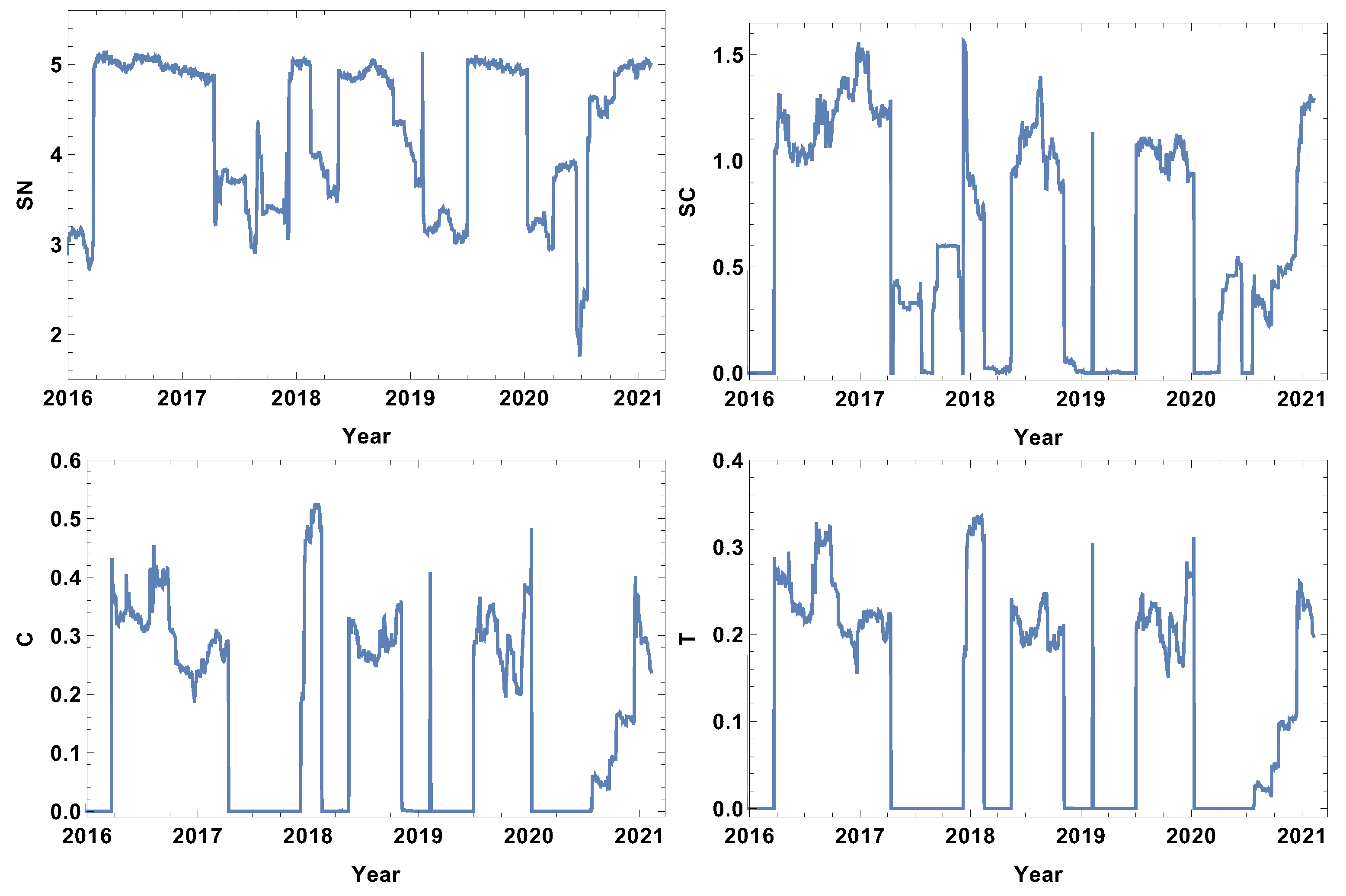

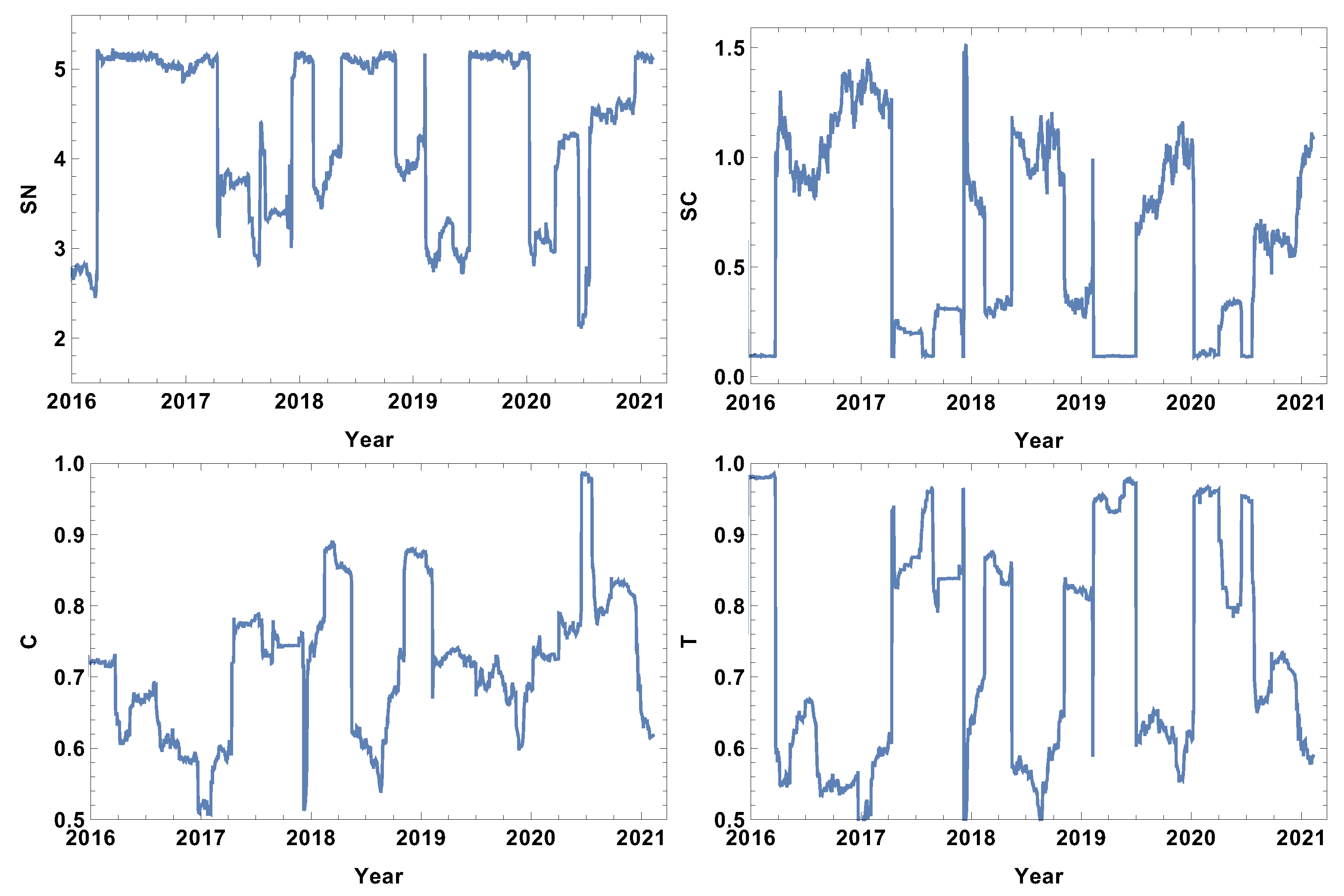

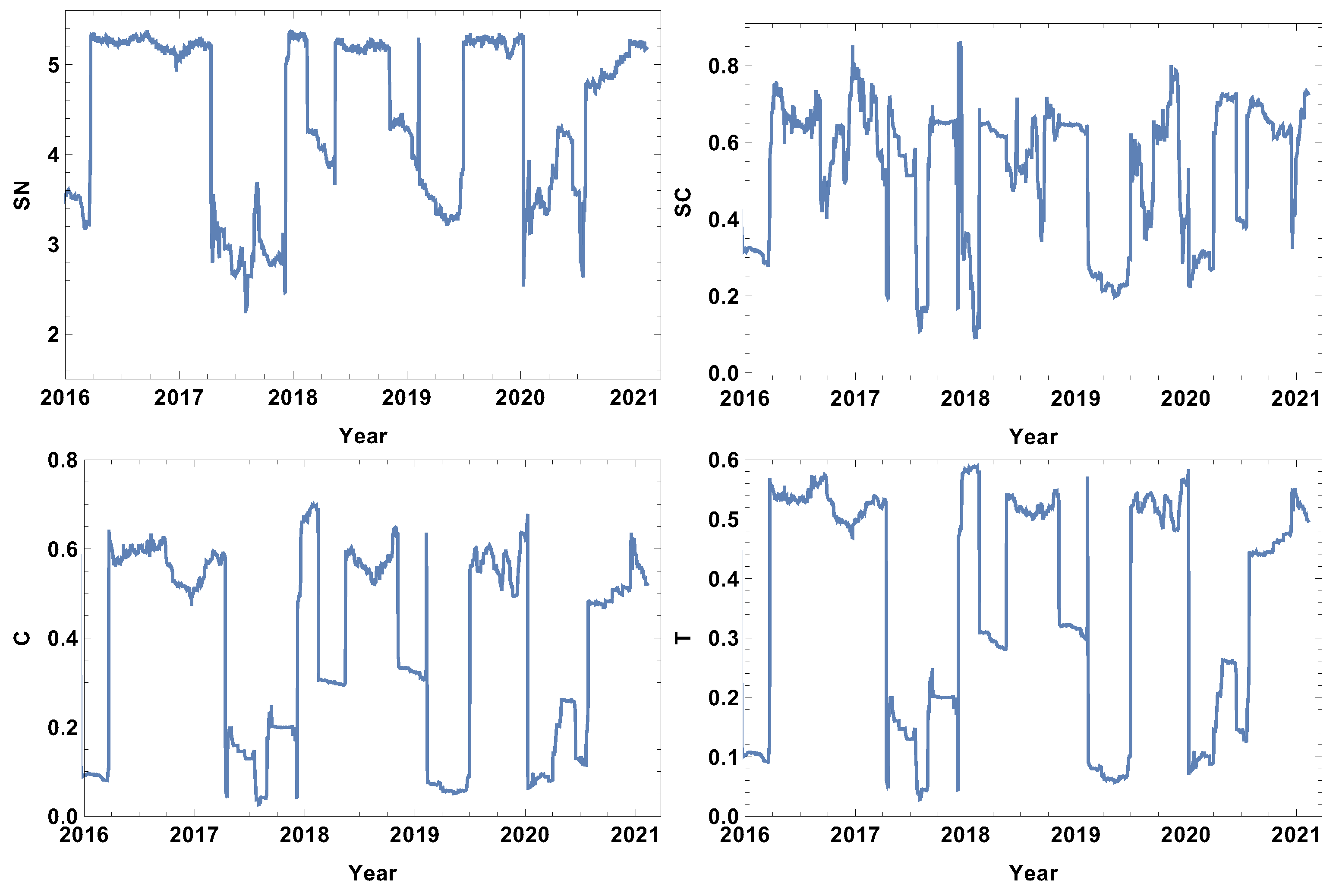

4. Results

4.1. Week Size Time Window,

4.2. Month Size Time Window,

4.3. Quarter Size Time Window,

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Companies List

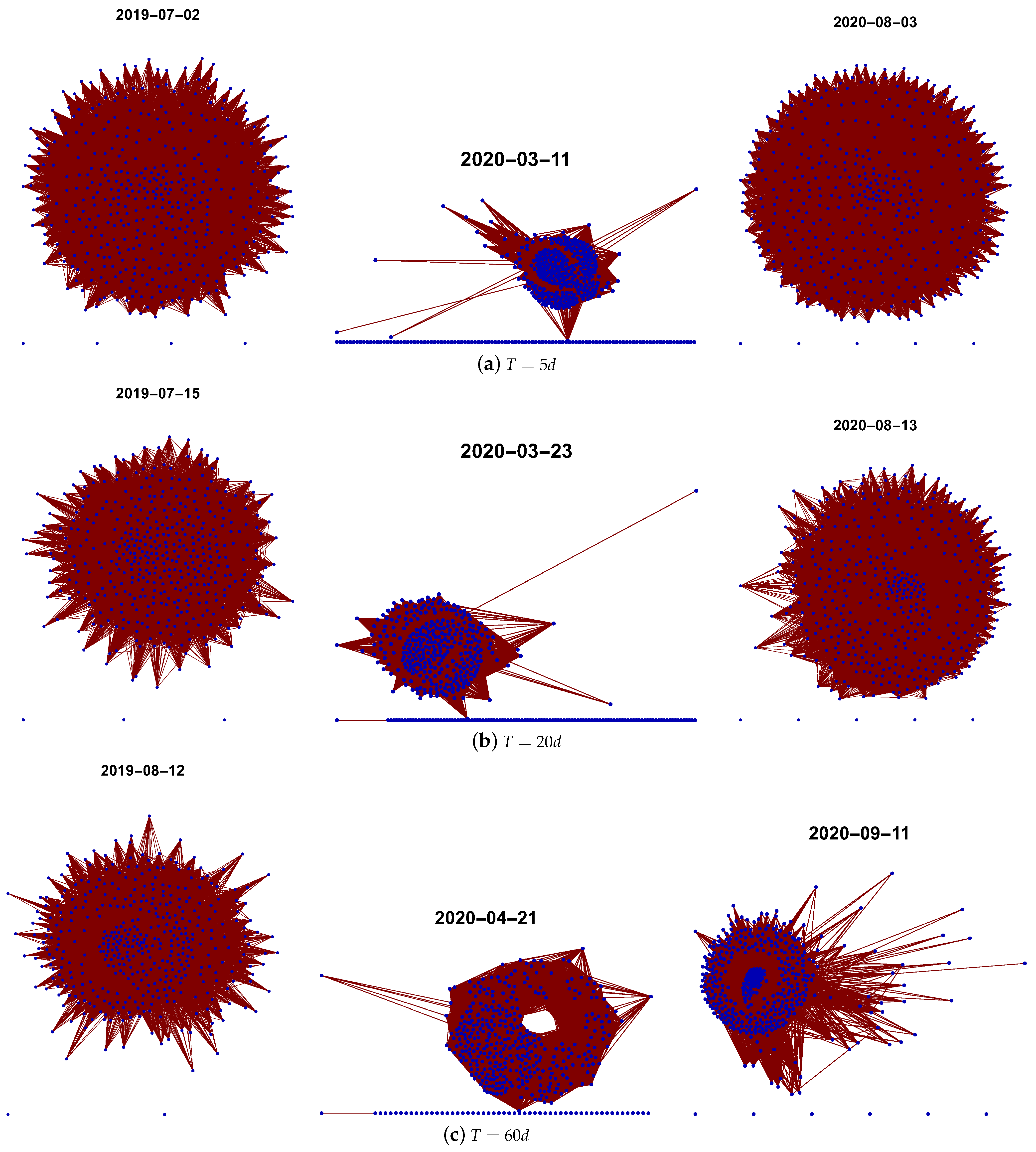

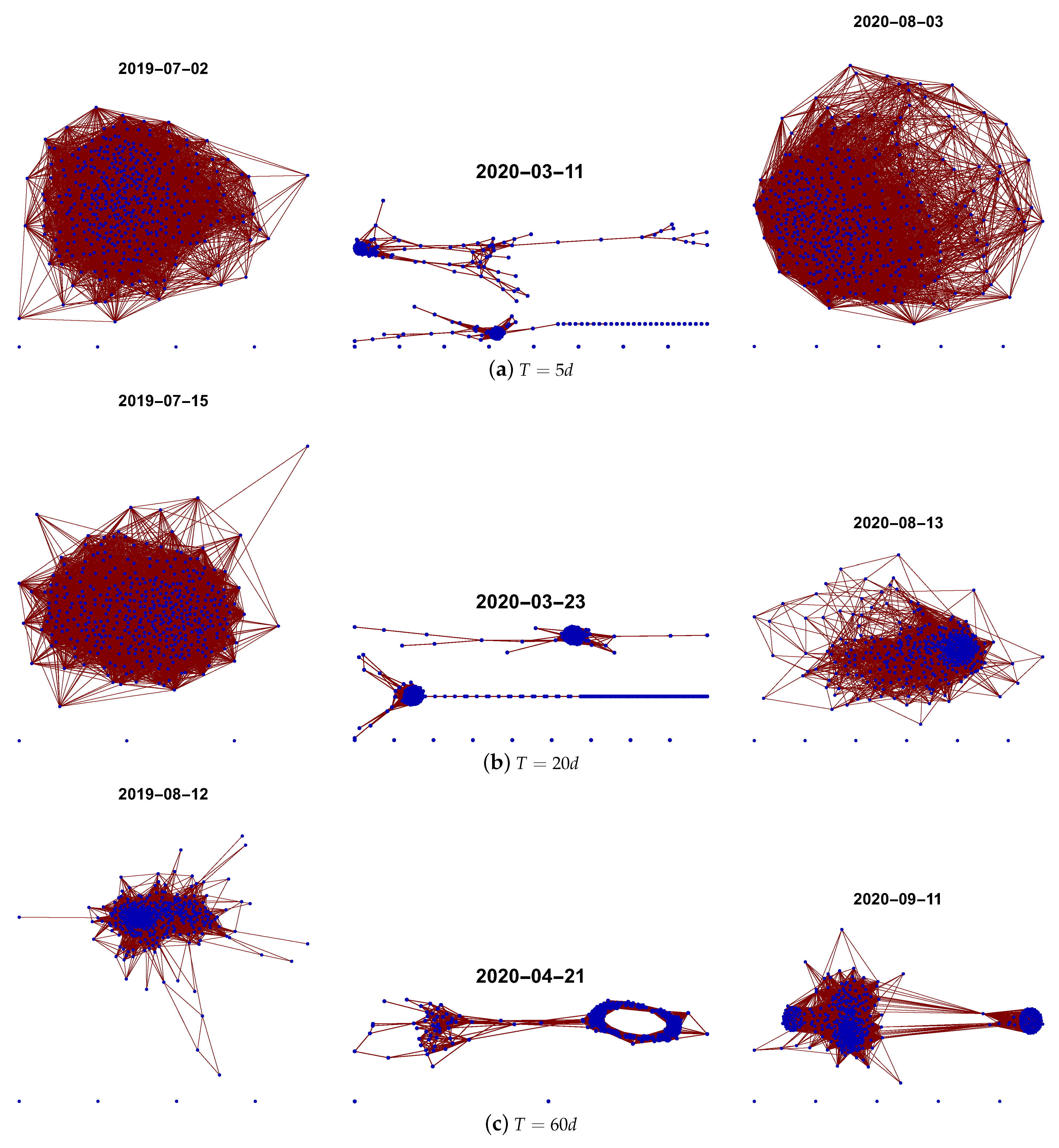

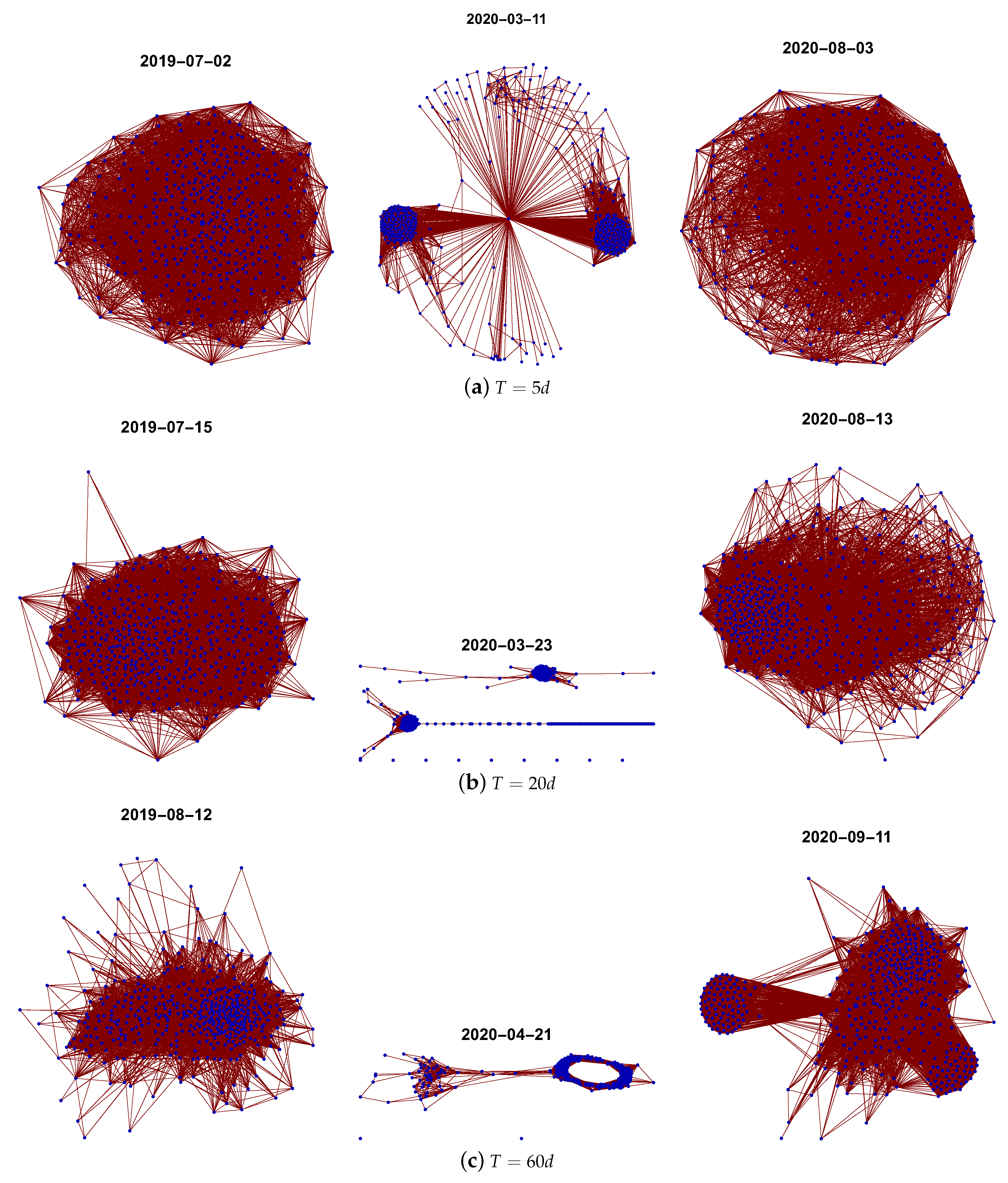

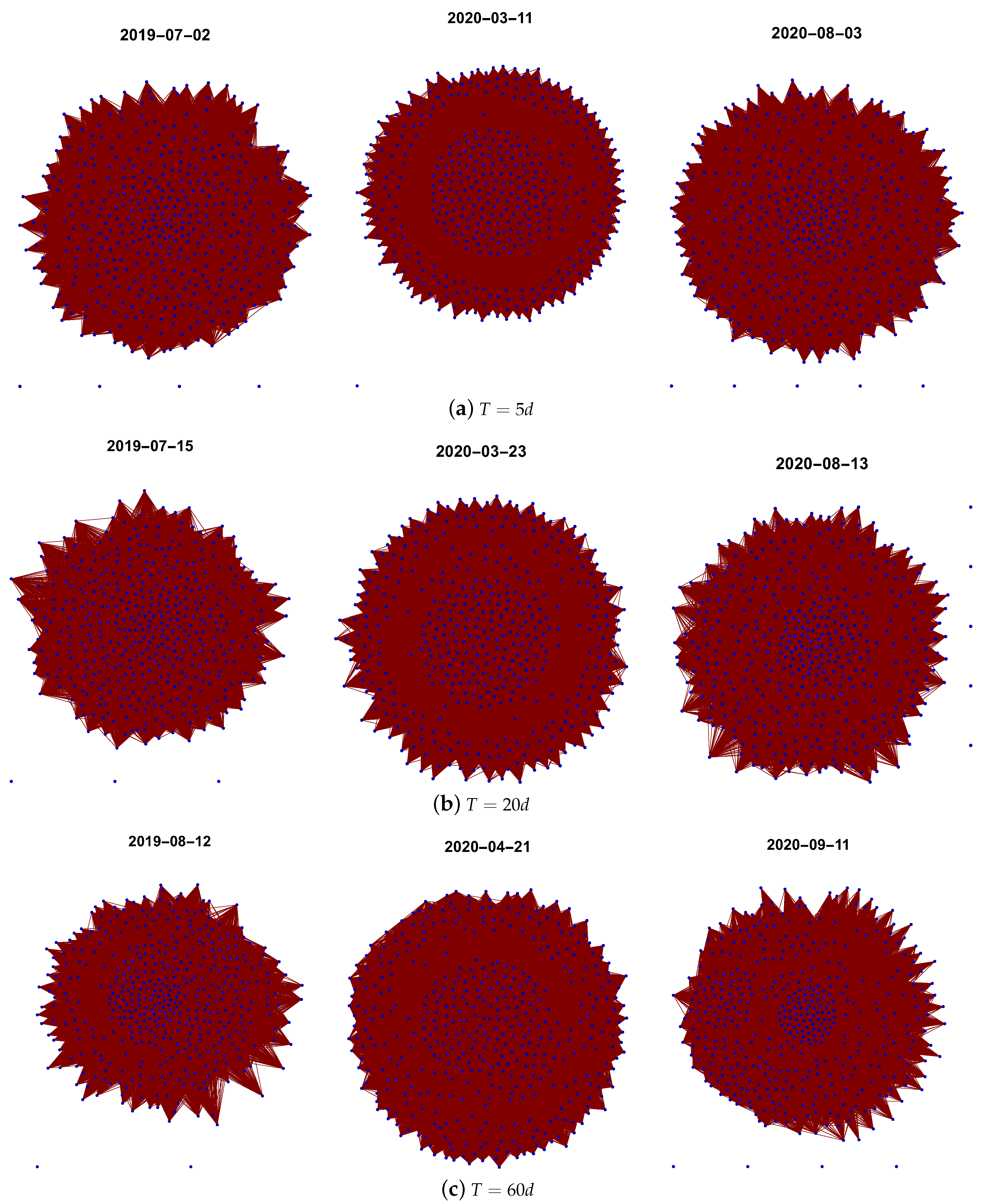

Appendix B. Graph Examples

References

- Jackson, M. Social and Economic Networks; Princeton University Press: Princeton, NJ, USA, 2008. [Google Scholar]

- Souma, W.; Fujiwara, Y.; Aoyama, H. Complex networks and economics. Phys. A Stat. Mech. Its Appl. 2003, 324, 396–401. [Google Scholar] [CrossRef]

- Bonanno, G.; Vandewalle, N.; Mantegna, R.N. Taxonomy of stock market indices. Phys. Rev. E 2000, 62, R7615–R7618. [Google Scholar] [CrossRef] [Green Version]

- Kirman, A. The economy as an evolving network. J. Evol. Econ. 1997, 7, 339–353. [Google Scholar] [CrossRef]

- Maysami, R.; Howe, L.; Rahmat, M. Relationship between Macroeconomic Variables and Stock Market Indices: Cointegration Evidence from Stock Exchange of Singapore’s All-S Sector Indices. J. Pengur. (UKM J. Manag.) 2012, 24. [Google Scholar]

- Mantegna, R.N. Hierarchical structure in financial markets. Eur. Phys. J. B 1999, 11, 193–197. [Google Scholar] [CrossRef] [Green Version]

- Stosic, D.; Stosic, D.; Ludermir, T.B.; Stosic, T. Collective behavior of cryptocurrency price changes. Phys. A Stat. Mech. Its Appl. 2018, 507, 499–509. [Google Scholar] [CrossRef]

- Ren, F.; Zhou, W.X. Dynamic Evolution of Cross-Correlations in the Chinese Stock Market. PLoS ONE 2014, 9, e97711. [Google Scholar] [CrossRef] [Green Version]

- Wang, G.J.; Xie, C.; Chen, S.; Yang, J.J.; Yang, M.Y. Random matrix theory analysis of cross-correlations in the US stock market: Evidence from Pearson’s correlation coefficient and detrended cross-correlation coefficient. Phys. A Stat. Mech. Its Appl. 2013, 392, 3715–3730. [Google Scholar] [CrossRef]

- Podobnik, B.; Stanley, H.E. Detrended Cross-Correlation Analysis: A New Method for Analyzing Two Nonstationary Time Series. Phys. Rev. Lett. 2008, 100, 084102. [Google Scholar] [CrossRef] [Green Version]

- Wątorek, M.; Drożdż, S.; Kwapień, J.; Minati, L.; Oświęcimka, P.; Stanuszek, M. Multiscale characteristics of the emerging global cryptocurrency market. Phys. Rep. 2021, 901, 1–82. [Google Scholar] [CrossRef]

- Miśkiewicz, J. Power law classification scheme of time series correlations. On the example of G20 group. Phys. A Stat. Mech. Its Appl. 2013, 392, 2150–2162. [Google Scholar] [CrossRef]

- Zou, Y.; Donner, R.V.; Marwan, N.; Donges, J.F.; Kurths, J. Complex network approaches to nonlinear time series analysis. Phys. Rep. 2019, 787, 1–97. [Google Scholar] [CrossRef]

- Silva, V.F.; Silva, M.E.; Ribeiro, P.; Silva, F. Time series analysis via network science: Concepts and algorithms. Wiley Interdiscip. Rev. Data Min. Knowl. Discov. 2021, 11, e1404. [Google Scholar] [CrossRef]

- Mantegna, R. Information and hierarchical structure in financial markets. Comput. Phys. Commun. 1999, 121–122, 153–156. [Google Scholar] [CrossRef]

- Kwapień, J.; Drożdż, S. Physical approach to complex systems. Phys. Rep. 2012, 515, 115–226. [Google Scholar] [CrossRef]

- Tumminello, M.; Lillo, F.; Mantegna, R.N. Correlation, hierarchies, and networks in financial markets. J. Econ. Behav. Organ. 2010, 75, 40–58. [Google Scholar] [CrossRef] [Green Version]

- Brida, J.G.; Risso, W.A. Hierarchical structure of the German stock market. Expert Syst. Appl. 2010, 37, 3846–3852. [Google Scholar] [CrossRef]

- Deviren, S.A.; Deviren, B. The relationship between carbon dioxide emission and economic growth: Hierarchical structure methods. Phys. A Stat. Mech. Its Appl. 2016, 451, 429–439. [Google Scholar] [CrossRef]

- Bonanno, G.; Lillo, F.; Mantegna, R. High-frequency cross-correlation in a set of stocks. Quant. Financ. 2001, 1, 96–104. [Google Scholar] [CrossRef]

- Xia, L.; You, D.; Jiang, X.; Guo, Q. Comparison between global financial crisis and local stock disaster on top of Chinese stock network. Phys. A Stat. Mech. Its Appl. 2018, 490, 222–230. [Google Scholar] [CrossRef]

- Onnela, J.P.; Chakraborti, A.; Kaski, K.; Kertiész, J. Dynamic asset trees and portfolio analysis. Eur. Phys. J. B-Condens. Matter Complex Syst. 2002, 30, 285–288. [Google Scholar] [CrossRef] [Green Version]

- Namaki, A.; Shirazi, A.; Raei, R.; Jafari, G. Network analysis of a financial market based on genuine correlation and threshold method. Phys. A Stat. Mech. Its Appl. 2011, 390, 3835–3841. [Google Scholar] [CrossRef]

- Zheng, Z.; Podobnik, B.; Feng, L.; Li, B. Changes in Cross-Correlations as an Indicator for Systemic Risk. Sci. Rep. 2012, 2, 888. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Sensoy, A.; Yuksel, S.; Erturk, M. Analysis of cross-correlations between financial markets after the 2008 crisis. Phys. A Stat. Mech. Its Appl. 2013, 392, 5027–5045. [Google Scholar] [CrossRef]

- Miśkiewicz, J.; Ausloos, M. Has the world economy reached its globalization limit? Phys. A Stat. Mech. Its Appl. 2010, 389, 797–806. [Google Scholar] [CrossRef] [Green Version]

- Miśkiewicz, J.; Ausloos, M. Correlation measure to detect time series distances, whence economy globalization. Phys. A Stat. Mech. Its Appl. 2008, 387, 6584–6594. [Google Scholar] [CrossRef]

- Kali, R.; Reyes, J. The architecture of globalization: A network approach to international economic integration. J. Int. Bus. Stud. 2007, 38, 595–620. [Google Scholar] [CrossRef]

- Tóth, B.; Kertész, J. Increasing market efficiency: Evolution of cross-correlations of stock returns. Phys. A Stat. Mech. Its Appl. 2006, 360, 505–515. [Google Scholar] [CrossRef] [Green Version]

- Lin, J.; Ban, Y. The evolving network structure of US airline system during 1990–2010. Phys. A Stat. Mech. Its Appl. 2014, 410, 302–312. [Google Scholar] [CrossRef]

- Barabasi, A.; Jeong, H.; Neda, Z.; Ravasz, E.; Schubert, A.; Vicsek, T. Evolution of the social network of scientific collaborations. Phys. A: Stat. Mech. Its Appl. 2002, 311, 590–614. [Google Scholar] [CrossRef] [Green Version]

- Kullmann, L.; Kertész, J.; Kaski, K. Time-dependent cross-correlations between different stock returns: A directed network of influence. Phys. Rev. E 2002, 66, 026125. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Eryigit, M.; Eryigit, R. Network structure of cross-correlations among the world market indices. Phys. A Stat. Mech. Its Appl. 2009, 388, 3551–3562. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J.; Kost, K.J.; Sammon, M.C.; Viratyosin, T. The Unprecedented Stock Market Impact of COVID-19; Technical Report; National Bureau of Economic Research: Cabridge, MA, USA, 2020. [Google Scholar]

- Onali, E. COVID-19 and Stock Market Volatility. 2020. Available online: https://ssrn.com/abstract=3571453 (accessed on 20 October 2021).

- Mazur, M.; Dang, M.; Vega, M. COVID-19 and the march 2020 stock market crash. Evidence from S&P1500. Financ. Res. Lett. 2021, 38, 101690. [Google Scholar] [CrossRef] [PubMed]

- Harjoto, M.A.; Rossi, F.; Paglia, J.K. COVID-19: Stock market reactions to the shock and the stimulus. Appl. Econ. Lett. 2021, 28, 795–801. [Google Scholar] [CrossRef]

- Ramelli, S.; Wagner, A. What the stock market tells us about the consequences of COVID-19. In Mitigating COVID Economic Crisis: Act Fast and Do Whatever; CEPR Press: London, UK, 2020; Volume 63. [Google Scholar]

- Miśkiewicz, J. Analysis of time series correlation. The choice of distance metrics and network structure. In Proceedings of the 5th Symposium on Physics in Economics and Social Sciences, Warszawa, Poland, 25–27 November 2010. [Google Scholar]

- Miśkiewicz, J. Distance matrix method for network structure analysis. In Statistical Tools for Finance and Insurance; Springer: Berlin/Heidelberg, Germany, 2011; pp. 251–289. [Google Scholar]

- Vandewalle, N.; Brisbois, F.; Tordoir, X. Non-random topology of stock markets. Quant. Financ. 2001, 1, 372–374. [Google Scholar] [CrossRef] [Green Version]

- Wiliński, M.; Sienkiewicz, A.; Gubiec, T.; Kutner, R.; Struzik, Z. Structural and topological phase transitions on the German Stock Exchange. Phys. A Stat. Mech. Its Appl. 2013, 392, 5963–5973. [Google Scholar] [CrossRef] [Green Version]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Miśkiewicz, J.; Bonarska-Kujawa, D. Evolving Network Analysis of S&P500 Components: COVID-19 Influence of Cross-Correlation Network Structure. Entropy 2022, 24, 21. https://doi.org/10.3390/e24010021

Miśkiewicz J, Bonarska-Kujawa D. Evolving Network Analysis of S&P500 Components: COVID-19 Influence of Cross-Correlation Network Structure. Entropy. 2022; 24(1):21. https://doi.org/10.3390/e24010021

Chicago/Turabian StyleMiśkiewicz, Janusz, and Dorota Bonarska-Kujawa. 2022. "Evolving Network Analysis of S&P500 Components: COVID-19 Influence of Cross-Correlation Network Structure" Entropy 24, no. 1: 21. https://doi.org/10.3390/e24010021

APA StyleMiśkiewicz, J., & Bonarska-Kujawa, D. (2022). Evolving Network Analysis of S&P500 Components: COVID-19 Influence of Cross-Correlation Network Structure. Entropy, 24(1), 21. https://doi.org/10.3390/e24010021