The Barriers of the Assistive Robotics Market—What Inhibits Health Innovation?

Abstract

:1. Introduction

2. Background

Innovation through Barrier Identification

3. Methodology

4. Discussion

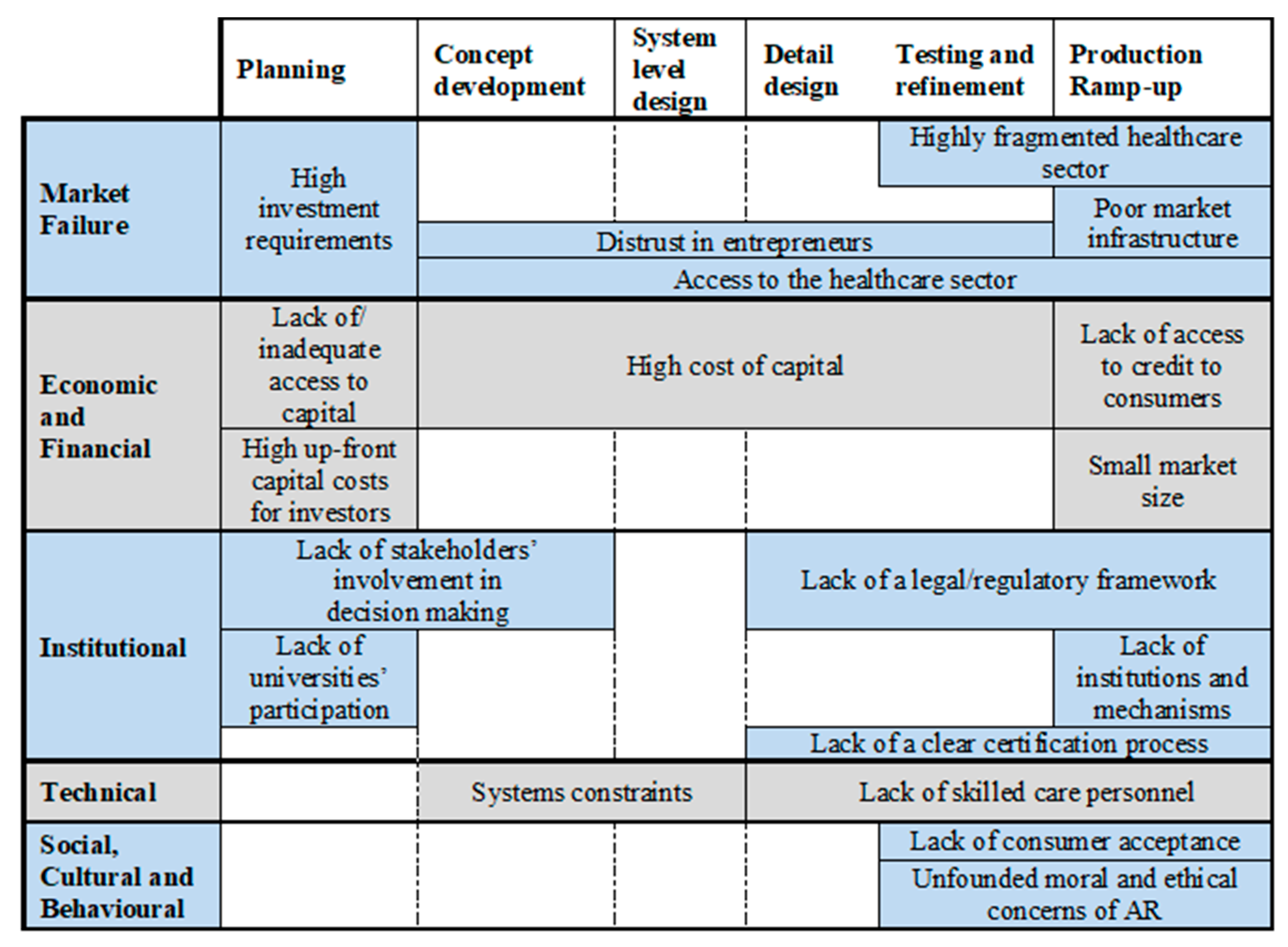

4.1. Market Failure

4.1.1. Access to Highly Fragmented Healthcare Sectors

‘Without contacts, there is not a really a way into it […] you are not exactly going to be able to walk into any care home ask them; do you want a robot? Can we now work with you?’

‘We don’t have a reputation, or much more, products to our names, so that we can go and say, this is a current problem, look what we have done, we got the solution … no one listens’.

4.1.2. Complex Market Infrastructure

‘[regarding the purchasing processes] for someone that is new to the market it is exceptionally difficult to get to the right people, to go to the people that make the choices’.

‘it is quite hard to reach the client, and distributors ask for a lot of money, raising prices’.

4.2. Economic and Financial

4.2.1. Capital and Investment

‘Finance, is so difficult, is not cheap, is an expensive journey, and this stops people from doing it’.

4.2.2. Customer Credit Facilities and Market Size

4.3. Institutional

4.3.1. Poor Legislation, Poor Policies

4.3.2. Lack of University Participation

‘You can’t put a price [university support] but, unfortunately, they are not interested in product development’.

4.3.3. Lack of a Transparent Certification Process

4.4. Technical

Skilled Health Personnel and System Constraints

4.5. Social, Cultural and Behavioural

Consumers’ Acceptance and Ethical Concerns

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Van der Zijpp, T.; Wouters, E.J.; Sturm, J. To use or not to use: The design, implementation and acceptance of technology in the context of health care. Assist. Technol. Smart Cities 2018. [Google Scholar] [CrossRef] [Green Version]

- Quilter-Pinner, H.; Muir, R. Improved Circulation: Unleashing Innovation across the NHS. Institute for Public Policy Research. 2015. Available online: https://www.ippr.org/files/publications/pdf/improved-circulation-NHS_June2015.pdf (accessed on 28 April 2021).

- Clark, D.; Dean, G.; Bolton, S.; Beeson, B. Bench to bedside: The technology adoption pathway in healthcare. Health Technol. 2019, 10, 1–9. [Google Scholar] [CrossRef] [Green Version]

- Gulbrandsen, M.; Hopkins, M.; Thune, T.; Valentin, F. Hospitals and innovation: Introduction to the special section. Res. Policy 2016, 45, 1493–1498. [Google Scholar] [CrossRef]

- Henderson, R. Innovation in the 21st Century: Architectural Change, Purpose, and the Challenges of Our Time. Manag. Sci. 2020. [Google Scholar] [CrossRef]

- World Bank Life Expectancy at Birth, Total (Years). Available online: https://data.worldbank.org/indicator/SP.DYN.LE00.IN (accessed on 22 April 2018).

- UN. World Population Ageing 2015; United Nations: New York, NY, USA, 2015; Volume 164. [Google Scholar] [CrossRef]

- Cocco, F. Highest Fertility Rates in Europe Still Below “Replenishment Level”. Financial Times. Available online: https://www.ft.com/content/d54e4fe8-3269-11e8-b5bf-23cb17fd1498 (accessed on 22 April 2018).

- Worldometers Population Mondiale (2018)—Worldometers. Available online: http://www.worldometers.info/fr/population-mondiale/ (accessed on 13 October 2018).

- EUROSTAT Population and Population Change Statistics—Statistics Explained. Available online: http://ec.europa.eu/eurostat/statistics-explained/index.php/Population_and_population_change_statistics (accessed on 22 April 2018).

- Workforce Intelligence CF WI Centre for Workforce Intelligence. Horizon Scanning. Available online: www.cfwi.org.uk (accessed on 28 April 2021).

- All-Party Parliamentary Group on Global Health Triple Impact of Nursing. APPG Glob. Health 2016. Available online: https://www.who.int/hrh/com-heeg/digital-APPG_triple-impact.pdf (accessed on 28 April 2021).

- EUrobotics Robotics 2020 Multi-Annual Roadmap. EUrobotics. (2015). Robot. 2020 Multi-Annu. Roadmap. 2017; pp. 178–228. Available online: http//www.eu-robotics.net/cms/index.php?idcat=170&idart=2016 (accessed on 28 April 2021).

- European Commission. eHealth Action Plan. 2012–2020—Innovative Healthcare for the 21st Century; 2012; Available online: https://ec.europa.eu/digital-single-market/en/news/ehealth-action-plan-2012-2020-innovative-healthcare-21st-century#:~:text=The%20European%20Commission’s%20eHealth%20Action,and%20patient%2Dcentred%20health%20services (accessed on 28 April 2021).

- EU Robotics. Strategic Research Agenda For Robotics in Europe 2014–2020. IEEE Robot. Autom. Mag. 2014, 24, 171. [Google Scholar] [CrossRef]

- Pellegrino, G. Barriers to innovation in young and mature firms. J. Evol. Econ. 2018, 28, 181–206. [Google Scholar] [CrossRef]

- Arza, V.; López, E. Obstacles to innovation and firm size. Inter. Am. Dev. Bank 2018. [Google Scholar] [CrossRef]

- Pellegrino, G.; Savona, M. No money, no honey? Financial versus knowledge and demand constraints on innovation. Res. Policy 2017, 46, 510–521. [Google Scholar] [CrossRef]

- Vargas, A.T.; Gómez, B.C. Barriers and facilitators of knowledge use in the health care system in Mexico: The Newborn Screening Programme. Innov. Dev. 2019. [Google Scholar] [CrossRef]

- Marrocu, E.; Paci, R.; Usai, S. Networks, Proximities, and Interfirm Knowledge Exchanges. Int. Reg. Sci. Rev. 2017, 40, 377–404. [Google Scholar] [CrossRef]

- Eslamian, S.; Reisner, L.A.; Pandya, A.K. Development and evaluation of an autonomous camera control algorithm on the da Vinci Surgical System. Int. J. Med. Robot. Comput. Assist. Surg. 2020, 16, e2036. [Google Scholar] [CrossRef] [PubMed]

- Wunker, C.; Montenegro, G. Use of Robotic Technology in the Management of Complex Colorectal Pathology. Mo. Med. 2020, 117, 149–153. [Google Scholar] [PubMed]

- Mehta, A.C.; Hood, K.L.; Schwarz, Y.; Solomon, S.B. The evolutional history of electromagnetic navigation bronchoscopy: State of the art. Chest 2020, 154, 935–947. [Google Scholar] [CrossRef]

- Chen, J. Playing to our human strengths to prepare medical students for the future. Korean J. Med Educ. 2017, 29, 193–197. [Google Scholar] [CrossRef]

- Young, A.J.; Ferris, D.P. State of the art and future directions for lower limb robotic exoskeletons. IEEE Trans. Neural Syst. Rehabil. Eng. 2017, 25, 171–182. [Google Scholar] [CrossRef]

- Aprile, I.; Germanotta, M.; Cruciani, A.; Loreti, S.; Pecchioli, C.; Cecchi, F. Upper limb robotic rehabilitation after stroke: A multicenter, randomized clinical trial. J. Neurol. Phys. Ther. 2020, 44, 3–14. [Google Scholar] [CrossRef]

- International Federation of Robotics. Executive Summary—World Robotics (Service Robots) 2017; International Federation of Robotics: Frankfurt, Germany, 2017. [Google Scholar]

- Butter, M.; Rensma, A.; van Boxsel, J.; Kalisingh, S.; Schoone, M.; Leis, M.; Gelderblom, G.J.; Cremers, G.; de Wilt, M.; Kortekaas, W.; et al. Robotics in Helthcare, Final Report. Robot. Helthcare 2008, 181, 4–9. [Google Scholar]

- OBI Robotic Feeding Device Designed for Home Care. Available online: https://meetobi.com/ (accessed on 22 April 2018).

- DRESS I-DRESS Project. Available online: https://i-dress-project.eu/ (accessed on 22 April 2018).

- SUPPORT i-Support Project—A Service Robotic System for Bathing Tasks. Available online: http://www.i-support-project.eu/ (accessed on 22 April 2018).

- CHIRON CHIRON. Available online: https://chiron.org.uk/ (accessed on 22 April 2018).

- Vandemeulebroucke, T.; de Casterlé, B.D.; Gastmans, C. The use of care robots in aged care: A systematic review of argument-based ethics literature. Arch. Gerontol. Geriatr. 2018, 74, 15–25. [Google Scholar] [CrossRef]

- PARO Robots U.S., Inc. PARO Therapeutic Robot. Available online: http://www.parorobots.com/ (accessed on 28 April 2021).

- Bloss, R. Mobile hospital robots cure numerous logistic needs. Ind. Robot. An. Int. J. 2011, 38, 567–571. [Google Scholar] [CrossRef]

- Wang, M.; Pan, C.; Ray, P.K. Technology Entrepreneurship in Developing Countries: Role of Telepresence Robots in Healthcare. IEEE Eng. Manag. Rev. 2021. [Google Scholar] [CrossRef]

- Dahl, T.S.; Boulos, M.N.K. Robots in health and social care: A complementary technology to home care and telehealthcare? Robotics 2014, 3, 1–21. [Google Scholar] [CrossRef] [Green Version]

- UK-RAS Network. Robotics in Social Care: A Connected Care EcoSystem for Independent Living; UK-RAS: London, UK, 2017; Available online: https://www.housinglin.org.uk/_assets/Resources/Housing/OtherOrganisation/UK_RAS_robitics-in-care-report.pdf (accessed on 28 April 2021).

- Jacobs, T.; Virk, G.S. ISO 13482-The New Safety Standard for Personal Care Robots. Available online: ieeexplore.ieee.org (accessed on 28 April 2021).

- GMI Healthcare Assistive Robot Market Size, Share Report. 2024. Available online: https://www.gminsights.com/industry-analysis/healthcare-assistive-robot-market (accessed on 22 April 2018).

- Mordor Intelligence Assistive Robotics Market. Growth, Trends, and Forecast (2020–2025). Available online: https://www.mordorintelligence.com/industry-reports/assistive-robotics-market (accessed on 7 February 2020).

- Crunchbase Jibo. Crunchbase. Available online: https://www.crunchbase.com/organization/jibo#section-overview (accessed on 1 June 2019).

- Brown, S.L.; Eisenhardt, K.M. Product development: Past research, present findings, and future directions. Acad. Manag. Rev. 1995, 20, 343–378. [Google Scholar] [CrossRef] [Green Version]

- West, J.; Salter, A.; Vanhaverbeke, W.; Chesbrough, H. Open innovation: The next decade. Res. Policy 2014, 43, 805–811. [Google Scholar] [CrossRef]

- Hadjimanolis, A. Barriers to innovation for SMEs in a small less developed country (Cyprus). Technovation 1999, 19, 561–570. [Google Scholar] [CrossRef]

- Hadjimanolis, A. The Barriers Approach to Innovation. In The International Handbook on Innovation; Elsevier: Amsterdam, The Netherlands, 2003; pp. 559–573. ISBN 9780080524849. [Google Scholar]

- Lu, J.; Ren, L.; Yao, S.; Rong, D.; Skare, M.; Streimikis, J. Renewable energy barriers and coping strategies: Evidence from the Baltic States. Sustain. Dev. 2020, 28, 352–367. [Google Scholar] [CrossRef]

- Ehrenhard, M.; Kijl, B.; Nieuwenhuis, L. Market adoption barriers of multi-stakeholder technology: Smart homes for the aging population. Technol. Forecast. Soc. Chang. 2014, 89, 306–315. [Google Scholar] [CrossRef]

- Yusif, S.; Soar, J.; Hafeez-Baig, A. Older people, assistive technologies, and the barriers to adoption: A systematic review. Int. J. Med. Inform. 2016, 94, 112–116. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Miguel Cruz, A.; Daum, C.; Comeau, A.; Salamanca, J.D.G.; McLennan, L.; Neubauer, N.; Liu, L. Acceptance, adoption, and usability of information and communication technologies for people living with dementia and their care partners: A systematic review. Disabil. Rehabil. Assist. Technol. 2020. [Google Scholar] [CrossRef] [PubMed]

- Ben-Messaoud, C.; Kharrazi, H.; MacDorman, K.F. Facilitators and barriers to adopting robotic-assisted surgery: Contextualizing the unified theory of acceptance and use of technology. PLoS ONE 2011, 6, e16395. [Google Scholar] [CrossRef]

- Wang, Y.; Hajli, N. Exploring the path to big data analytics success in healthcare. J. Bus. Res. 2017, 70, 287–299. [Google Scholar] [CrossRef] [Green Version]

- Alkhaldi, B.; Sahama, T.; Huxley, C.; Gajanayake, R. Studies in Health Technology and Informatics; IOS Press: Amsterdam, The Netherlands, 2014; pp. 875–879. [Google Scholar]

- Pereira, F.; Fife, E. A Business Model Approach to Realizing Opportunities and Overcoming Barriers in E-Health. In Proceedings of the 22nd Biennial Conference of the International Telecommunications Society, Seul, Korea, 24–27 June 2018. [Google Scholar]

- Cairo, C. The Differences between Hardware and Software Development. Available online: https://www.business.com/articles/hardware-vs-software-product-launch/ (accessed on 22 April 2018).

- Thompson, K. Hardware Vs. Software Development: Similarities and Differences. cPrime. Available online: https://www.cprime.com/2015/11/hardware-vs-software-development-similarities-and-differences/ (accessed on 22 April 2018).

- Painuly, J.P. Barriers to renewable energy penetration: A framework for analysis. Renew. Energy 2001, 24, 73–89. [Google Scholar] [CrossRef]

- Ulrich, K.; Eppinger, S. Product Design and Development, 6th ed.; McGraw-Hill Education: New York, NY, USA, 2016. [Google Scholar]

- Patton, M.Q. Qualitative Research and Evaluation Methods; SAGE: London, UK, 2014; ISBN 0761919716. [Google Scholar]

- Kvale, S. Interview: An. Introduction to Qualitative Research Interviewing; Sage Publications: New York, NY, USA, 1997; ISBN 8741228162. [Google Scholar]

- Thomas, D.R. A General Inductive Approach for Analyzing Qualitative Evaluation Data. Am. J. Eval. 2006, 27, 237–246. [Google Scholar] [CrossRef]

- Ross, J.; Stevenson, F.; Lau, R.; Murray, E. Factors that influence the implementation of e-health: A systematic review of systematic reviews (an update). Implement. Sci. 2016, 11, 1–12. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Marcolino, M.S.; Oliveira, J.A.Q.; D’Agostino, M.; Ribeiro, A.L.; Alkmim, M.B.M.; Novillo-Ortiz, D. The impact of mHealth interventions: Systematic review of systematic reviews. JMIR mHealth uHealth 2018, 6, e23. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- EU Comission, EU-Funded Projects on Robotics. Available online: https://ec.europa.eu/digital-single-market/en/programme-and-projects/project-factsheets-robotics (accessed on 22 April 2018).

- De Clercq, D.; Danis, W.M.; Dakhli, M. The moderating effect of institutional context on the relationship between associational activity and new business activity in emerging economies. Int. Bus. Rev. 2010, 19, 85–101. [Google Scholar] [CrossRef]

- Hayter, C.S.; Nelson, A.J.; Zayed, S.; O’Connor, A.C. Conceptualizing academic entrepreneurship ecosystems: A review, analysis and extension of the literature. J. Technol. Transf. 2018, 43, 1039–1082. [Google Scholar] [CrossRef]

- Holgersson, M.; Aaboen, L. A literature review of intellectual property management in technology transfer offices: From appropriation to utilization. Technol. Soc. 2019, 59, 101132. [Google Scholar] [CrossRef]

- Wettlaufer, L.; Penn, D. Medical Devices: Definition and Clinical Testing. Drug Discov. Eval. Methods Clin. Pharmacol. 2020, 613–623. [Google Scholar] [CrossRef]

- Kramer, D.B.; Xu, S.; Kesselheim, A.S. Regulation of medical devices in the United States and European Union. Ethical Chall. Emerg. Med. Technol. 2020. [Google Scholar] [CrossRef] [Green Version]

- Sethi, R.; Popli, H.; Sethi, S. Medical Devices Regulation in United States of America, European Union and India: A Comparative Study. Pharm. Regul. Aff. 2017. [Google Scholar] [CrossRef] [Green Version]

- Orwat, C.; Graefe, A.; Faulwasser, T. Towards pervasive computing in health care—A literature review. BMC Med. Inform. Decis. Mak. 2008, 8, 26. [Google Scholar] [CrossRef] [Green Version]

- Jensen, M.B.; Johnson, B.; Lorenz, E.; Lundvall, B.Å. Forms of knowledge and modes of innovation. Res. Policy 2007, 36, 680–693. [Google Scholar] [CrossRef]

- Greenhalgh, T.; Wherton, J.; Papoutsi, C.; Lynch, J.; Shaw, S. Beyond adoption: A new framework for theorizing and evaluating nonadoption, abandonment, and challenges to the scale-up, spread, and sustainability of health and care technologies. J. Med. Internet Res. 2017. [Google Scholar] [CrossRef] [Green Version]

- Castillo, V.H.; Martínez-García, A.I.; Pulido, J. A knowledge-based taxonomy of critical factors for adopting electronic health record systems by physicians: A systematic literature review. BMC Med. Inform. Decis. Mak. 2010, 10, 60. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Archer, N.; Fevrier-Thomas, U.; Lokker, C.; McKibbon, K.A.; Straus, S.E. Personal health records: A scoping review. J. Am. Med. Inform. Assoc. 2011, 18, 515–522. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Boonstra, A.; Broekhuis, M. Barriers to the acceptance of electronic medical records by physicians from systematic review to taxonomy and interventions. BMC Health Serv. Res. 2010, 10, 231. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Dean, T.J.; McMullen, J.S. Market Failure and Entrepreneurial Opportunity. Acad. Manag. Proc. 2011, 2002, F1–F6. [Google Scholar] [CrossRef]

- Rahal, R.M.; Mercer, J.; Kuziemsky, C.; Yaya, S. Factors affecting the mature use of electronic medical records by primary care physicians: A systematic review. BMC Med. Inform. Decis. Mak. 2021, 21, 1–15. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Company | Year Founded | Total Funding Amount (* M$) | Product | Currently Trading |

|---|---|---|---|---|

| SONY | * 1990 | -- | AIBO | Worldwide |

| Intuition Robotics | 2015 | 22 | ElliQ | Pre-sale US |

| Blue Frog Robotics | 2014 | 0.18 | Buddy | No |

| Emotech LTD | 2014 | 10 | Olly | No |

| Jibo | 2012 | 72.7 | Jibo | No |

| Temi | 2015 | 21 | Temi | No |

| ASUS | -- | -- | Zenbo | No |

| Groove X | 2015 | 52.7 | Lovot | Japan |

| UBTech Robotics | 2012 | 940 | Lynx | US |

| Zoetic AI | 2017 | -- | Kiki | No |

| Yukai Engineering | 2011 | -- | BOCCO emo | Japan |

| No. of Employees | Registration | Age (Date Reported, Year) | Assets (Last Reported, 1000 Eur) | Currently Trading | Country | Product Description |

|---|---|---|---|---|---|---|

| 1–10 | July-18 | 0.24 | 5.6 | No | UK | Wheelchair robotic arm |

| 1–10 | January-18 | 0.74 | 5.6 | No | UK | Therapeutic robot |

| 1–10 | November-17 | 0.91 | -- | No | UK | Emergency drone |

| 1–10 | September-17 | 1.07 | 75 | No | France | Medication reminder robot |

| 1–10 | August-17 | 1.16 | -- | No | UK | Care support robot |

| 1–10 | August-17 | 1.16 | 28.5 | No | UK | Medication delivery robot |

| 1–10 | May-17 | 1.41 | 11.2 | No | France | Smart wheelchair |

| 11–20 | September-16 | 2.07 | 155 | Yes | France | Care support robot |

| 1–10 | September-16 | 2.07 | 5 | No | France | Assistive robotic arm |

| 1–10 | July-16 | 2.24 | 192.5 | Yes | France | Care support robot |

| 1–10 | April-16 | 2.49 | 143.7 | Yes | France | Telepresence robot |

| -- | January-16 | 2.74 | -- | No | France | Medication delivery robot |

| 1–10 | July-15 | 3.25 | 50 | Yes | France | Patient monitoring solution |

| 1–10 | November-14 | 3.91 | 7.2 | Yes | France | Therapeutic robot |

| 30–50 | November-12 | 5.91 | 50.3 | Yes | France | Indoor projector robot |

| 11–50 | November-11 | 6.91 | 162.5 | No | France | Care support robot |

| 41–50 | 2007 | 11.00 | 15,400 | Yes | France | Robotic air quality purification |

| Barrier Category | Barrier | Remarks |

|---|---|---|

| Market Failure | Access to the healthcare sector | ‘without contacts, there is not really a way into it’ |

| Highly fragmented healthcare sector | ‘there are many different people involved’, ‘you can’t get to the people that make the choices’, ‘is quite hard to reach the client’ | |

| Poor market infrastructure | ‘you have to manufacture where the skills are’ | |

| Distrust in entrepreneurs | ‘people see us as buyers, instead of people trying to help others doing what we love’, ‘doors are not open to entrepreneurs with good ideas’ | |

| High investment requirements | ‘is not cheap, is an expensive journey’, ‘this stop people for doing, the cost puts an extra weight’ | |

| Economic and Financial | High cost of capital | ‘bring a project together and fund that project is really really difficult’ |

| Lack of/inadequate access to capital | ‘there are not investment opportunities for hardware’ | |

| High up-front capital costs for investors | ‘there is great risk involved in funding hardware companies’ | |

| Lack of access to credit for the consumer | ‘[the product] might be too expensive for the final user’, ‘you need to work on B2B’ | |

| Small market size | ‘we don’t know how the UK [healthcare] systems work’, ‘we will need someone to help us get to that market’ | |

| Institutional | Lack of institutions and mechanisms | ‘there is a lack of directives’, ‘government support is minimal’ |

| Lack of a legal/regulatory framework | ‘AI should be transparent’, ‘[healthcare segment] they are reluctant’ | |

| Lack of stakeholders’ involvement in decision making | ‘this is a problem, we got the solution, and no one listen [to entrepreneurs]’ | |

| Lack of universities’ participation | ‘you can’t put a price [university support] but, unfortunately, they are not interested in product development’ | |

| Lack of a clear certification process | ‘we cannot pursue a medical certification’ | |

| Technical | Lack of skilled care personnel | ‘they haven’t seen a robot, so they don’t know how to use it’ |

| Systems constraints | ‘[challenge] to know what technology to use’, ‘integrate all the technology is the main problem’ | |

| Social, Cultural and Behavioural | Lack of consumer acceptance | ‘is quite hard to reach the client’, ‘is not here to take people jobs’ |

| Unfounded moral and ethical concerns of AR | ‘[invest time] to convince people to have the robot’, ‘is not going to spy you’ |

| Barriers | Barrier Elements |

|---|---|

| 1. Market Failure | |

| Access to the healthcare sector | Access to patients for product co-creation. Disrupts the whole development process. |

| Highly fragmented healthcare sector | Different stakeholders and organisations. Slows down technology acquisition. |

| Poor market infrastructure | Lack of manufacture opportunities in Europe. Increases final product cost and slows technology acquisition. |

| Distrust in entrepreneurs | Disrupts the development process and technology adoption. |

| High investment requirements | High seed funding needed to develop prototypes. Builds an entry barrier for entrepreneurs. Discourages entrepreneurs. |

| 2. Economic and Financial | |

| High cost of capital | Fundamental differences between software and hardware investment requirements. Creates a lack of capital, high-interest rates, and risk perception by financial organisations. Impacts on economic viability. |

| Lack of/inadequate access to capital | No awareness of hardware development implications. Impacts market competition and market efficiency. |

| High up-front capital costs for investors | High seed funding need increases risk perception. Lack of understanding of AR investment needs. |

| Lack of access to credit for the consumer | High product cost. Under-developed credit market. Reduces market size. |

| Market size small | Fragment healthcare system between regions and countries. Prevents product scale and potential gains, reducing the appeal for entry of newcomers. |

| 3. Institutional | |

| Lack of institutions and mechanisms | Missing agencies at the planning level to support AR development. Inhibits information dissemination between producers and consumers, creating extra costs for companies. |

| Lack of a legal/regulatory framework | Generates liability and concerns in the adoption of new technology. |

| Lack of stakeholders’ involvement in decision making | No seeking of the involvement of developers. Creates misplaced priorities, making policymaker bodies unaware of the market barriers. |

| Lack of universities’ participation | Impacts on recruitment and R&D opportunities. |

| Lack of a transparent certification process | No clear the path for certification of AR devices. Disrupts market entry of new products. |

| 4. Technical | |

| Lack of skilled care personnel | Slows down technology adoption, creates extra expenses. |

| Systems constraints | Integration problems with healthcare IT infrastructure. Producers cannot realise the market. |

| 5. Social, Cultural and Behavioural | |

| Lack of consumer acceptance | Fears surrounding the broader impact of AR, for example, fear of robots taking jobs. Reduces the market size. |

| Unfounded moral and ethical concerns of AR | Affects market size and technology adoption. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aguiar Noury, G.; Walmsley, A.; Jones, R.B.; Gaudl, S.E. The Barriers of the Assistive Robotics Market—What Inhibits Health Innovation? Sensors 2021, 21, 3111. https://doi.org/10.3390/s21093111

Aguiar Noury G, Walmsley A, Jones RB, Gaudl SE. The Barriers of the Assistive Robotics Market—What Inhibits Health Innovation? Sensors. 2021; 21(9):3111. https://doi.org/10.3390/s21093111

Chicago/Turabian StyleAguiar Noury, Gabriel, Andreas Walmsley, Ray B. Jones, and Swen E. Gaudl. 2021. "The Barriers of the Assistive Robotics Market—What Inhibits Health Innovation?" Sensors 21, no. 9: 3111. https://doi.org/10.3390/s21093111

APA StyleAguiar Noury, G., Walmsley, A., Jones, R. B., & Gaudl, S. E. (2021). The Barriers of the Assistive Robotics Market—What Inhibits Health Innovation? Sensors, 21(9), 3111. https://doi.org/10.3390/s21093111