1. Introduction

The coronavirus crisis that started in December 2019 became a pandemic and had devastating global consequences. On 11 March 2020, the World Health Organization identified the outbreak as a pandemic. Greater attention was then given to the infection and death rates given the limited health care capacities of each country (

Milani 2021). The rapid spread of the virus led to the implementation of preventive measures as no vaccine was currently available. In March 2020, the vast majority of countries registered a large number of cases as the outbreak reached Europe and the USA. Therefore, city-, district-, and then country-wide lockdowns were implemented.

The COVID-19 shock produced variations in many key macroeconomic variables that affected economic activity (

Fuentes and Moder 2021). The purpose of this paper is to examine and compare the impact of the exogenous pandemic shock on the economy of nine different countries, namely, France, Germany, Italy, Japan, Republic of Korea, New Zealand, Sweden, U.K., and the USA. The countries included in our study took distinctive approaches in tackling the spread of the virus so that the responses were widely heterogeneous. This allows us to compare the effectiveness of the different measures taken by each country to curb the pandemic’s economic impact. France and Germany increased lockdown intensity as cases rose, while Italy implemented restrictive stay-at-home measures. Sweden did not impose a lockdown, whereas the U.K. lessened restrictions and aimed for herd immunity but soon moved away from this policy. A minority of countries, such as New Zealand, Japan, and the Republic of Korea, acted decisively and quickly, attempting to eradicate the virus before it spread. As the negative economic effects of the virus spread, the US implemented the CARES act (the Coronavirus Aid, Relief, and Economic Security) in 2020 and the Coronavirus Response and Consolidated Appropriations Act in 2021 to provide rapid and direct economic assistance for American workers, families, small businesses, and industries.

1In this paper, we study the effects of the pandemic on the price level, the unemployment rate and the three-month nominal interest rate using the dynamic response from the VAR models for each of the nine countries in question. We consider a shock to one of their variables, namely, the unemployment rate, and examine its effect on the remaining variables. However, one issue in conducting such an analysis is that such shocks registered huge data variation in the last few months of the pandemic, making the estimation of standard time series models such as VARs a challenge (

Lenza and Primiceri 2020). Should one discard the data from the pandemic? The estimation of a standard VAR model excluding the COVID-19 observations yields an impulse response function that does not generate proper predictions as it drastically underestimates uncertainty. Can one include them without distorting the parameter estimates? Moreover, does differencing our series conceal vital information about the long run relationship between our variables? These questions are crucial when generating expectations about the future trajectory of our key macroeconomic series as the latest data from the pandemic period can contaminate the time-series observations leading to weak and unreliable inferences.

A variety of models and approaches have been developed to analyze the impact of Covit-19 on macroeconomic outcomes.

Fernandez-Villaverde and Jones (

2020) combined data on GDP, unemployment, and Google’s

COVID-19 Community Mobility Reports with data on deaths from COVID-19 to study the macroeconomic outcomes of the pandemic. They find that countries such as Korea, Japan, Germany, and Norway and cities such as Tokyo and Seoul have had comparatively few deaths and low macroeconomic losses. At the other extreme, New York City, Lombardy, the United Kingdom, and Madrid have had many deaths and large macroeconomic losses. They discuss the role of good government policy in terms of non-pharmaceutical interventions (NPI’s) versus self-protecting behavior in mitigating the effects of the pandemic.

Milani (

2021) studies the interdependencies between economies and the COVID-19 shock using a Global VAR (GVAR) model and examines the transmission of the pandemic shock both domestically and globally. He exploits a dataset on existing social connections across country borders and shows that social networks help explain not only the spread of the disease but also cross-country spillovers in perceptions about coronavirus risk and in social distancing behavior.

Whether for government policy purposes or uses by central banks or private institutions, studies have been conducted to quantify the pandemic shock and to forecast its future implications.

Lenza and Primiceri (

2020) develop a vector autoregression where they modeled the change in shock volatility around the time of the pandemic, implicitly weighting observations inversely proportional to their innovation variance. Their approach is simpler than standard models of time-varying volatility because the exact timing of the increase in the variance of macroeconomic innovations due to COVID-19 is known. They then examine the implications of a shock to unemployment for unemployment, employment, consumption and prices. We discuss their results further in the sections that follow.

Alvarez et al. (

2020) develop a simple social planning problem to determine the optimal lockdown policy. They parameterize their model based on the assumption of 1% of infected agents at the outbreak, no cure for the disease, and the possibility of testing.

In what follows, we develop a Bayesian VAR to examine the impact of the pandemic on three key macroeconomic variables for the nine countries in question. It has been noted that Bayesian inference has well-known advantages when studying heavily parameterized models such as VARs (

Belloni 2017). It consists of assigning prior probabilities to the model parameters. The idea is to include informative priors to shrink the unrestricted VAR to have a parsimonious model and, hence, minimize parameter uncertainty. The BVAR will improve our forecast accuracy and will generate the future path of our macroeconomic variables for the nine distinct economies studied, with the purpose of discussing the impact of the policies that were implemented and understanding the nature of the recovery for each country. We find that the initial effects of the pandemic led to declines in the price level, an increase in the unemployment rate, and a decline in interest rates, signifying severe damage to economies around the world. Some of these effects were reversed as governments made dramatic spending pledges and countervailed market forces, with an increase in consumer prices being one of the most salient outcomes.

The rest of this paper is organized as follows.

Section 2 provides a literature review.

Section 3 describes methodology and the issues around conducting Bayesian inference in a VAR.

Section 4 provides the results, while

Section 5 presents a discussion of these results.

Section 6 concludes.

2. Literature Review

There is now a vast and varied literature that has studied the impact of the pandemic on a variety of economic and social outcomes. Various authors have attempted to answer this question using different econometric techniques and analyses. Researchers have proposed approaches to infer the relative importance of supply and demand forces during the pandemic period. The relative strength of the forces working on supply and demand during the COVID-19 crisis is a key input to effective policy, whether through measures to shield productive capacity or to address demand deficiencies arising from uncertainty and the actual and expected loss of income (

Balleer et al. 2020). These authors use planned price changes based on German firm-level survey data to argue that demand and supply forces co-exist but that demand deficiencies dominate in the short-run. They predict aggregate sectoral inflation to decline up by as much as 1.5 percentage points through August 2020, reflecting a substantial drop in aggregate demand.

Eichenbaum et al. (

2020) considered three versions of DSGE models to analyze the effects of the epidemic. They found that neoclassical model does not rationalize the positive co-movement of consumption and investment observed in recessions associated with an epidemic. By contrast, monopolistic competition models with or without price stickiness model remedy this shortcoming.

Christelis et al. (

2020) used new panel data from a representative survey of households in the six largest euro area economies to estimate the impact of the COVID-19 crisis on consumption. They showed that concern about finances due to COVID-19 from the first peak of the pandemic until October 2020 caused a significant reduction in non-durable consumption.

Ma et al. (

2020) examined the immediate effects and bounce-back from six modern health crises: 1968 Flu, SARS (2003), H1N1 (2009), MERS (2012), Ebola (2014), and Zika (2016). Based on panel regressions for a large cross-section of countries, they found that real GDP growth fell by around three percentage points in affected countries relative to unaffected countries in the year of the outbreak. The recovery of GDP growth was rapid, but output is still below pre-shock level five years later. They also found that the level and persistence of unemployment is higher for less educated workers and there is significantly greater persistence in female unemployment than male. Larger first-year responses in government spending, especially on health care, help to mitigate the negative effects on GDP and unemployment. Countries affected by the health crisis suffer declines in consumption, investment, and international trade.

In addition to the macroeconomic effects from the pandemic directly, we may consider the effects of a lockdown instituted to halt or slow its spread. Typically, the negative effects of the lockdown outweigh its upsides. While lockdowns increased the level of unemployment and generated a loss of business, the isolation imposed during this period helped improve air quality by reducing carbon emissions (

Oncioiu et al. 2021). Likewise, COVID-19 had significant impacts on the labor market in Saudi Arabia by helping to transform its service and educational sector from conventional to remote forms, where virtual skills, autonomous working, and effective communication materialized as the most important skills (

Al-Youbi et al. 2020). Such skill sets can pave the way for a renovated working approach in different sectors in the Saudi Arabian economy. On the other hand,

Pinilla et al. (

2021) showed that autonomous regions in Spain are most dependent on the service sector, especially tourism, as being the most negatively affected by Covit-19 shock and the associated confinement measures, revealing structural weaknesses in productive sectors in the Spanish economy.

Bocchino et al. (

2021) argued that an unexpected and stressful factor such as COVID-19 may lead to feelings of vulnerability and helplessness, which affect personal health and lower productivity.

Fiscal sustainability and monetary stability became important concerns amid the spread of the virus.

Meyer and Caporale (

2021) examined how varying economies, notably, the United States, the European Union, Japan, and South Korea, have changed their monetary and fiscal policies to respond to the pandemic-induced economic crisis. For example, in March 2020, as the pandemic began having negative effects on the economy, the Fed pursued an aggressive easing strategy: it quickly dropped rates from 1.50 percent to near-zero levels and increased its balance sheet from

$4.3 trillion in the beginning of March 2020 to nearly

$7.5 trillion by the end of January 2021 (

Meyer and Caporale 2021). This was accomplished mostly through the purchase of USA. Treasury securities and mortgage-backed securities.

2 Likewise, the European Central Bank supported access to credit for firms and households by increasing the amount of money that banks can borrow from the ECB and improving the ease with which banks can borrow to make loans. It also instituted a €750 billion (

$909 billion) pandemic emergency purchase program (PEPP) through which it temporarily purchased public and private sector securities to lower borrowing costs and increase lending in the euro area.

3 Nevertheless, the longer the pandemic lasts, the larger the public debt, and a nation’s adherence to its debt and liabilities will be at greater risk over time. Italy, France, and Spain, the most severely hit countries in the European Union, all increased their public debt to cover the costs of the pandemic (

Briceño and Perote 2020). According to their econometric assessment, Briceño and Perote found that a point increase in the real economic growth rate lowers the public debt ratio by more than a half point. Since the Eurozone economic growth was expected to decrease 8.7% in 2020, and then increase by 5.2% and 3.3% in 2021 and 2022, respectively, this suggests that the Eurozone increased its public debt ratio on average by about 6% for the year 2020. Developing countries received financial support from the World Bank and the International Monetary Fund. In August 2021, the Board of Governors of the IMF approved a general allocation of Special Drawing Rights (SDRs), equivalent to US

$650 billion (about SDR 456 billion) to combat the global recession induced by the pandemic.

4 Countries imposed lockdowns and took different fiscal and monetary measures to counter the reduction in consumption and the increase in the unemployment rate. However, the future macroeconomic trajectories of emerging and developing economies also depend on the path to be followed by developed economies.

Aizenman and Ito (

2020) examined two different exit strategies of the USA from the post COVID-19 debt-overhang and analyze their implications on emerging markets and global stability. The first strategy involves the USA returning to the 2019, pre-Covid mode of loose fiscal policy and accommodating monetary policy. The second strategy involves, first, turning USA fiscal priorities from fighting Covid’s medical and economic challenges towards investment in different forms of infrastructures and, second, engaging in a gradual fiscal adjustment over time to achieve primary surpluses and debt resilience. They show that the first strategy carries the risk of inducing future sudden stop crises and instability of emerging markets, while the second may contribute towards long-term global stability.

Economic growth and unemployment are linked in both developed and emerging economies and may be affected by many uncertain factors. It is beneficial for financial institutions and policymakers to develop preferences and strategy formulations using the best forecasting model (

Nguyen et al. 2021). Nguyen, Tsai, Kayral, and Lin employed the Grey theory system-based (GM), the Grey Verhulst Model (GVM), and the autoregressive integrated moving average (ARIMA) model to predict the future path of unemployment in Vietnam. On the other hand, the widely varying implications on unemployment across countries suggest that institutional differences can partially insulate a country’s population from the effects of large exogenous shocks (

Milani 2021). He finds that the lower degree of employee protections in the USA and the large share of temporary workers in the Spanish economy are likely to account for the far worse outcomes in these countries.

Davidescu et al. (

2021) used Box-Jenkins methodology based on ARIMA models to forecast the unemployment rate in Romania. The forecasted unemployment rate indicated an upward trend, reaching almost 5.15% at the beginning of 2021, with a decreasing trend for the period 2021–2023 (

Davidescu et al. 2021).

Sheldon (

2020) compared the current labor market situation with previous employment crises and presented the possible future trajectory of the unemployment rate in Switzerland on the basis of a previously used set of leading indicators. These leading indicators for the unemployment rate point towards worsening situation in the labor market for Switzerland, with an increase from 16% to 40 % in long-term unemployment.

Katris (

2021) carried out data analysis using time series models such as exponential smoothing and ARIMA approaches from the classical models, as well as feed-forward artificial neural networks and multivariate adaptive regression splines from the machine learning toolbox and examined the future impact of COVID-19 on key indicators for Greece. He provided alternative scenarios and provided an estimate for the termination or at least the beginning of the downward trend for the outbreak.

3. Methodology

In this section, we develop a Bayesian VAR as this approach has well-known advantages when studying heavily parameterized models such as VARs (

Belloni 2017). It consists of assigning prior probabilities to the model parameters. The idea is to include informative priors to shrink the unrestricted VAR to achieve a parsimonious model and hence minimize parameter uncertainty. The BVAR will improve our forecast accuracy and generate the future path of our macroeconomic variables for the nine distinct economies studied, with the purpose of discussing the policies implemented and the shape of the recovery for each country.

3.1. Some Preliminary Observations

Table 1 summarizes pre- and post-lockdown average levels of CPI, unemployment rate, and the interest rate, expressed in percentages, for the nine countries considered in this study, together with the standard deviation of the variables in the pre-lockdown era.

56 We do not specify a single lockdown date because most countries implemented regional lockdowns and had different consecutive stages. However, all lockdowns occurred by 2020 Q2.

The shock had visible effects on the economies in question starting in 2020 Q2, when country-wide lockdowns started to be implemented. In the USA, unemployment rate soared to 14.8% in April 2020, increasing by 10% in a single month. This record high rate came as a shock after years of low levels of unemployment. Likewise, an economy with an initial low unemployment such as Germany saw its unemployment rate increase from 3.1% to 4.5% from the pre-lockdown to the post-lockdown periods. Other countries also experienced increases in their unemployment rates and their price levels to varying degrees. The UK economy experienced a 20% increase in its price level following low inflation and stable growth for decades. By contrast, a deflationary economy such as Japan saw the smallest increase in its price level between the pre- and post-lockdown periods. Furthermore, compared to the pre-lockdown period, there occurred declines in the nominal interest rate for all the countries in the post-lockdown period, comprising the quarters 2020 Q3, 2020 Q4, 2021 Q1, and 2021 Q2.

In principle, economic theory suggests that an increase in the unemployment rate leads to a decrease in inflation. These variables are postulated to maintain an inverse relationship represented by the Phillips Curve,

7 as proposed by the economist

Phillips (

1958). Historically low levels of unemployment were attributed to higher inflation, while high levels of unemployment recorded lower inflation, and in certain cases, deflation. This relationship makes sense as low unemployment means more disposable income to spend on goods and services, and as demand increases, prices follow. The inverse is also true. High unemployment reduces consumers’ purchasing power and, hence, inflation.

Table 1 challenges this view, presenting an increase in both the unemployment rate and inflation.

Table 1 also shows that the lockdown period induced short-term nominal interest rates to remain low or became negative since banks held excess reserves during the period of the pandemic. To rationalize these observations, we conduct two exercises. As we discussed above, governments tried to mitigate the negative economic effects of the pandemic by engaging in massive monetary and fiscal expansion. Accordingly, we conduct one exercise where we disregard the monetary and fiscal expansion that many countries engaged in and seek to gauge the initial effects of the pandemic on our macroeconomic variables. In the second exercise, we take a further step by including the period where both monetary expansion and fiscal stimuli were introduced and examine their consequences.

3.2. Classical v/s Bayesian Inference

Time-variation in the coefficients of a vector autoregressive model leads to the proliferation of the number of parameters, while time-variation in the error covariance matrix increases concerns about over-parameterization. The use of prior information introduces shrinkage in a logical and consistent way to combat these issues (

Koop and Korobilis 2010). In addition, stationarity can pose great obstacles for time series analysis. It is essential for the researcher to ensure that all the components in the VAR are stationary to examine the statistical significance of the coefficients. Having said that, from a Bayesian point of view, no special account of non-stationarity needs to be taken. The Bayesian approach is purely grounded on the likelihood function that takes a Gaussian shape irrespective of the presence non-stationary series (

Sims et al. 1990;

Uhlig 1994). This constitutes a big difference between classical and Bayesian inference. In their paper “Inference in Linear Time Series Models with Some Unit Roots”,

Sims et al. (

1990) argued that the common practice of researchers attempting to ensure stationarity either by differencing or cointegration is not always necessary. Whether the data are integrated or not is not the issue, but rather whether the estimated coefficients have a nonstandard distribution if the regressors are in fact integrated (

Sims et al. 1990). It is often the case that their distribution is unaffected by non-stationarity, hence a Bayesian analysis finds no motive to use transformed models. Classical and Bayesian inference on unit roots differ significantly. From a Bayesian perspective, the researcher is allowed to identify the uncertainty by using weights, without taking a stand on stationarity. The unit root of a specified series is just one of several possibilities and obtains a posterior weight based on the data. Posterior probabilities are proportional to the joint probabilities of the prior and the likelihood. While the conditional likelihood function of the data may not be standard, the conditional likelihood function of the parameters is standard. In other words, non-stationarity is only present in the data, not in the parameters.

3.3. Prior Selection

Classical inference may not account for the uncertainty underlying the coefficients when pretesting for unit roots. A researcher will find it more natural to use the Bayesian approach by including parameter uncertainty and taking the observed data as given. However, applying Bayesian methods may be uncomfortable given the many choices in choosing a prior. Only a small number of priors is typically found to be useful.

Uhlig (

1994) argues that if the prior belongs to the Normal-Wishart density, then the posterior will follow a Normal-Wishart density as well. It can be convenient to choose and specify a prior that results in a posterior from a known family of distributions. The conjugate Normal-Inverse Wishart family, which includes the Minnesota prior, unites around a distaste towards explosive roots (

Giannone et al. 2015) and is represented by:

where ∑ = E(ε

tε

t′) is the variance-covariance matrix of the error terms in the VAR and ᴪ, d, b, and Ω are typically functions of a lower dimensional vector of hyperparameters, γ.

These priors are reasonable when centered at the unit root, conditional on being adjusted in reduced-form models by centralizing the prior weight for the coefficient toward zero as the largest root approaches unity from below. For persistence and medium-run forecasting, the Bayesian approach takes uncertainty about the existence of unit roots into account (

Uhlig 1994). Predictive density tails can be subtle towards the prior treatment of explosive roots. The selected prior in our research is the Minnesota prior or Litterman prior, which sets a particular structure for the prior mean and covariance. Introduced in 1980 by Litterman, the Minnesota prior assumes that each variable included in the model follows a random walk process, probably with a drift (

Giannone et al. 2015). Litterman states that it is a “reasonable approximation of the behavior of an economic variable” yet parsimonious. In other words, this approach is useful in forecasting economic series.

When the data are transformed to stationary series, we set the prior means for all coefficients to zero, instead of setting some prior means to one to shrink towards a random walk as might be appropriate if we were working with nonstationary series. In other words, when working with stationary series it is recommended to set the prior mean equal to zero. When working with non-stationary series it is recommended to set the prior mean of the first lag of each variable equal to one in its own equation and set all other coefficients at zero.

The second expression shows that the variance of the Minnesota prior is notably lower for coefficients that are associated with distant lags (through the term s2) and that the coefficients that are related to that same variable and same lag in a different equation are allowed to be correlated. The key hyperparameter, λ, is responsible for determining the overall tightness of the prior besides controlling the scale of all the variances and covariances. For λ → 0, the posterior approaches the prior, whereas λ approaching 1 makes the posterior distribution closer to the sample information or the likelihood function. Finally, ψj controls the prior’s standard deviation on lags of variables other than the dependent variable.

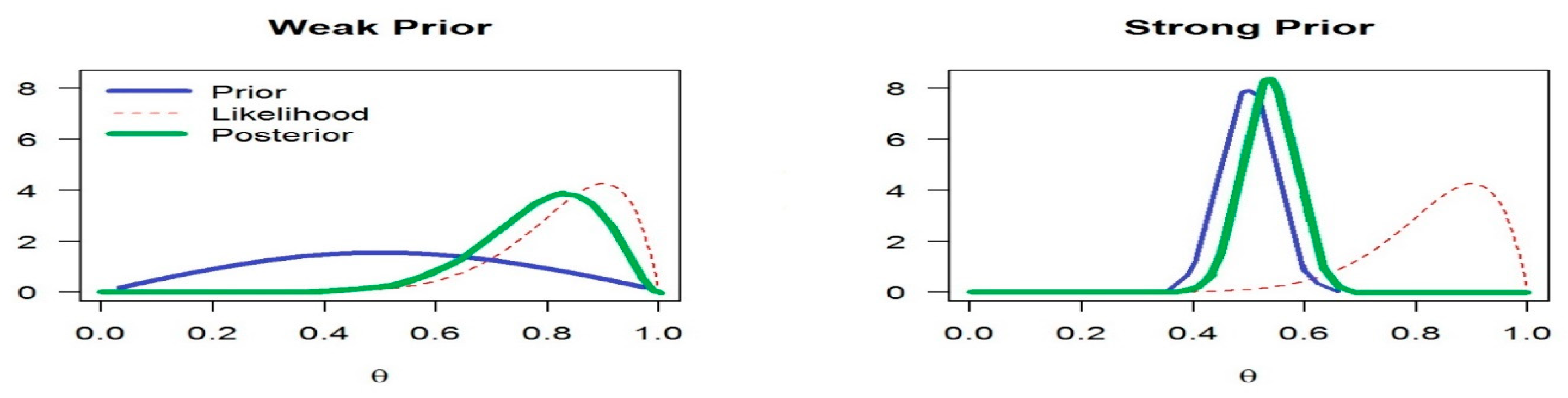

The frequentist approach to statistics treats parameters as fixed but unknown quantities, where we can estimate these parameters using a sample from the population. However, different samples will yield different estimates. The distribution of these estimates is known as a sampling distribution and quantifies the uncertainty about the estimates even though the parameter itself is considered fixed. The Bayesian approach is a different way of thinking. Our parameters are treated as random variables that can be described with a probability distribution (

Giannone et al. 2015). Probability is our degree of belief, absent data. This mathematical expression of our belief about the parameters included is called the prior distribution. Furthermore, we can investigate the effect of the prior distribution by conducting an experiment based on the likelihood function to produce another distribution, known as the posterior distribution. Bayesian inference allows the researcher to update his prior beliefs about the parameter with the results obtained from the experiment. In other words, we can compute the posterior distribution by multiplying the prior with the likelihood. Additionally, if the posterior belongs to the same family as the prior, the prior is called conjugate. The posterior can closely resemble the prior when the sample size is small and the prior is informative. In contrast, the posterior will be closer to the likelihood as we increase sample size or use an uninformative prior, such as a flat prior; see

Figure 1.

3.4. A Bayesian Vector Autoregression

To study the COVID-19 shock on our key macroeconomic variables, we examine the behavior of our variables prior to the shock. Given that we have more than one dependent variable, we introduce a set of linear dynamic equations where each equation of a dependent variable is specified as lags of itself and other remaining variables in the system. Therefore, all three variables are endogenous, and we have a set of three equations: we use a multivariate vector autoregressive (VAR) model to investigate the relationship between the consumer price index (CPI), the unemployment rate (UR), and the interbank interest rate (R) and to determine if there is any significant impact from shocks to the variables studied.

Let y

t = (CPI

t, UR

t, R

t)′ the 3 × 1 vector of the endogenous variables in our model; the parameter vectors α the 3 × 1 vector of constant terms in each equation; β

j the 3 × 3 matrix of coefficients on y

t−j for j = 1, …, p; and ε

t = (ε

1t, ε

2t, ε

3t)′ the vector of error terms. Then, our VAR model may be written as

Define X

t = (1, y

t−1′, …, y

t−p′)′ as the (3p + 1) × 1 vector of regressors and β = (α, β

1, …, β

p) as the 3 × (3p + 1) matrix of coefficients. Then, we may write the VAR model for any date

t as

The unknown parameters of the model are β and ∑, which denote the model parameters and the variance-covariance matrix of the error terms, respectively.

In principle, Bayesian estimation follows that, given the probability density function (pdf) of our data conditional on our parameters, our likelihood function corresponds to:

where Y = (y

1, y

2, …, y

T)′ is a 3T × 1 vector. Given the joint prior distribution on our parameters p (β, ∑) and according to Bayes rule, the joint posterior distribution of our model parameters conditional on our data are derived as

Of course, different priors can be chosen, reshaping our vector autoregressive model and its forecast results. However, this Bayesian VAR focuses on the Minnesota prior following a Monte Carlo integration.

5. Discussion

The rapid spread of COVID-19 and its identification as a pandemic introduced a shock to economic activity. Lockdowns were implemented in 2020 Q2 following the spread of the virus in different countries where industrial and business activity declined, and unemployment rates increased drastically. As a result, authorities took measures to counter the decline in economic activity and embarked on fiscal and monetary expansion as of 2020 Q3. The impulse response functions (IRFs) for the nine countries that we present in

Figure 2,

Figure 3,

Figure 4,

Figure 5,

Figure 6,

Figure 7,

Figure 8,

Figure 9 and

Figure 10 allow us to witness the natural response of our variables to the exogenous shock in the absence of such expansionary government measures.

Economic activity was unavoidably affected given the implementation of social distancing measures. The impulse response functions show the negative trajectory that the CPI levels are predicted to follow for different countries accompanying the lockdown shock. This initial decrease in the overall price level in different economies is reasonable given the decrease in the purchasing power due to an increase in unemployment. However, the response of the CPI and unemployment to a shock in the unemployment rate differs between one country and another as the relationship between the two varies between countries. We observed an initial negative response of the price level for France, Germany, Japan, Rep. of Korea, Sweden, and the USA as the unemployment rate increased due to the shock. For Italy, we see a slight increase in the price level, and a minor increase in the unemployment rate as Italy was already recording high levels of unemployment before the lockdown was implemented. New Zealand’s CPI is predicted to initially increase and then to subsequently decrease, but these changes are not significantly different from zero. Another effect of the pandemic is the decline in the purchasing power of households. This leads to a decline in interest rates in almost all countries in our sample, with the exception of Japan and New Zealand. For these countries, the decline in the interest rate is not significantly different from zero. Interest rates fall in response to looming uncertainty about the future and are predicted to remain low in future periods, though for countries such as Germany and Japan there is some evidence of a future rise in interest rates.

Next,

Table 2 presents results that include the effects of fiscal expansions that occurred after 2020 Q2 and it shows the posterior means of all of the variables are, on the whole, close to the post-lockdown values reported in

Table 1. We find that the average levels of the CPI in each of these countries after fiscal intervention and monetary expansion tend to increase and are expected to remain higher than their pre-lockdown level in the foreseeable future. France and Germany resorted to sizable loans to aid and support businesses. Japan’s fiscal outlay was less than 16% of its GDP, as opposed to the USA fiscal response which was above 27%. The effects of this can be observed in the high CPI levels recorded in the USA in comparison to the insignificant increase in CPI in Japan. The unemployment rate and the CPI in France both increased following the shock and are likely to remain at high levels in the future. By contrast, Germany, Sweden, Rep. of Korea, the U.K., and the USA experienced an increase in the unemployment rate in the short run, which should decline in the longer run absent monetary expansions. However, with the exception of the US, the posterior means for the unemployment rate are lower typically than the post-lockdown values. Hence, these posterior distributions show how unemployment rates increased and will remain higher than pre-lockdown rates. By contrast, New Zealand did not implement a significant decline in its interest rates. With the implementation of a strict lockdown, New Zealand rapidly eliminated the virus and allowed for a faster resumption of economic activity. As a consequence, there was no significant increase in its unemployment rate and its economy bounced back rapidly from the initial impacts of the pandemic, leading to a V-shaped recovery. The CPI increased as consumers rushed to stockpile non-durable consumption goods, anticipating any lockdown that might take place in New Zealand. It is important to note that Sweden did not implement a lockdown. However, its macroeconomic indicators behaved similarly to the countries that did impose lockdowns since consumers and businesses were affected by the novel coronavirus.

In work that is most closely related to ours,

Lenza and Primiceri (

2020) estimated a monthly Bayesian VAR, including data on employment, unemployment, consumption and prices, and use the estimated model to perform two exercises. For March, April, and May, they estimated the unknown scaling factor for the variance of the innovations, while for months afterwards, they set up a prior centered on the assumption that the residual variance after May would decay at a 20 percent monthly rate. Given the availability of new data over time, the researchers updated the prior distribution with the information contained in the likelihood function.

10 As in our analysis, they computed the impulse responses to the forecast error in unemployment and found that the real economy comprised of consumption, unemployment, and employment initially slowed down and then showed some recovery, as in our case. They also found that prices experienced downward pressure, which is consistent with the demand shock interpretation to the COVID-19 shocks. This exercise is intended to capture the response to a surprise change in unemployment and shows that our results are consistent with those in the literature. This is despite the fact that we do not employ a scaling factor for the innovation variances.

6. Conclusions

The model we have estimated incorporates highly volatile residual shocks, not only at the time of writing this research but also for the subsequent months, through the mechanisms we have presented in our analysis. Therefore, it is preferable to examine the parameters using a BVAR. Bayesian methods perform better than their non-Bayesian counterparts in terms of forecasting and accuracy. As we have discussed, Bayesian methods appear to offer rational answers to overcome the complications of overparameterization, overfitting, and unit roots when estimating vector autoregressive models. Of course, a variety of priors can be used when developing vector autoregressive models yielding distinct results. Hence, forecasts published at different dates are thus based on slightly different information, leading to different results. It is important to note that Bayesian vector autoregressive models are useful in modelling extreme observations. By providing probabilities to our statistical problems, Bayesian analysis provides us with a set of tools to update our beliefs when new data are presented. This allows the researcher to use posteriors from previous analysis as priors in new BVARs.

The macroeconomic indicators we worked with behaved similarly worldwide, with or without lockdowns. Nevertheless, there are several reasons why modelling the effects of the pandemic remains a challenge. First, there still is a good deal of uncertainty around the volatility of our key macroeconomic variables. The recent resurgence of the virus suggests the potential implementation of new lockdowns, causing large variability in the macroeconomy. In contrast, the mass vaccination campaigns can lead to a fast recovery by assuaging the volatility of the pandemic shock. This study made it possible to compare the effects of the pandemic across nine different countries and shed light on the similarities and differences in the behavior of key macroeconomic variables.

From a macroeconomic policy point of view, many countries enacted fiscal policy measures and increased the money supply to increase household consumption. While we tried to account for the impact of such fiscal and monetary policy, we did not include their effects explicitly. Hence, an extension of this analysis would consider including such variables in a Bayesian Vector Autoregression framework. This extension would provide an analysis of the countervailing effects of the lockdown, on the one hand, and the stimulus measures, on the other.

Second, it is not possible for monetary and fiscal authorities to indefinitely cover the costs of an immense shock such as the pandemic with debt and an increase in the money supply. The COVID-19 shock has real economic costs. Thus, authorities should realize that productivity and income must increase significantly in the future to compensate for what is lost today. Otherwise, compounding debt will severely affect the economy by making the losses materialize in terms of a reduction in the real value of money and savings, in addition to lower economic growth and exchange rate depreciation. Hence, a second extension could analyze the future trajectory of debt and the variables characterizing the macroeconomy to potentially trace the effects of the COVID-19 crisis on macroeconomic sustainability and stability.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}