1. Introduction

Pairs trading and cross-sectional momentum (CSM) strategies are popular investment strategies that rely, in some sense, on opposite assumptions on the behavior of asset returns. The former assumes that when the prices of two closely related assets diverge, they will eventually revert. This is equivalent to the assumption that the asset that overperforms will underperform over a subsequent period. The latter, in contrast, assumes that an asset that overperforms will continue to outperform. These strategies are very widely used by practitioners, especially in the parts of the market where active management is important. Both, in their simplest forms, are long-short strategies with net zero investment and are likely to be used, for example, by hedge funds.

Although there is a large volume of empirical research into the properties of both strategies, theoretical research investigating the relative performances of these strategies has not been attempted to the best of our knowledge. Refer, for example, to

Elliott et al. (

2005),

Gatev et al. (

2003),

Grauer (

2008),

Do and Faff (

2010),

Zhu et al. (

2021) for further details on pairs trading; and

Lo and MacKinlay (

1990),

Jegadeesh and Titman (

1993,

2001),

Lewellen (

2002),

Moskowitz et al. (

2012),

Israel and Moskowitz (

2013), and

Kwon and Satchell (

2020) for further details on CSM.

In this paper, we provide a theoretical comparison of the expected returns on the two strategies by identifying the key factors and deriving an analytic expression for the condition under which one outperforms the other. To do this, we assume that asset returns are jointly normally distributed, which we acknowledge is somewhat restrictive but necessary to derive simple analytic expressions. The Sharpe ratio and the autocorrelation of the spread in the underlying asset returns emerge as the key factors, and the condition is expressed in terms of these quantities. It is also shown that this condition is highly sensitive to the probability of the asset prices reverting, so that even a small change in the probability results in a significant change to the relative performances of the two strategies. Despite this, it is established that in the majority of the practically relevant situations where the expected spread is positive and the spread autocorrelation is small, the pairs trading strategy outperforms the CSM strategy.

The remainder of this paper is organized as follows:

Section 2 compares the CSM strategy with the perfect pairs trading strategy where the asset prices revert with certainty.

Section 3 extends the analysis to the imperfect pairs trading case under which the asset prices may not revert over a subsequent period, and the paper concludes with

Section 4.

2. Comparison of Perfect Pairs Trading and CSM

Let

be the 2-dimensional vector of asset returns over the period

t, and assume that the returns are normally distributed and stationary, so that

is a 4-dimensional vector and

where

denotes a multivariate normal distribution with mean

m and covariance matrix

,

and

. If we denote by

the spread between the two assets returns, so that

where

, and define

and

, then it follows from (

1) that the mean,

, and variance,

, of

are given by

Moreover, if we denote by

the auto-correlation of

, then we have

Finally, if we denote by

the expected return from a 2-asset cross-sectional (CSM) momentum strategy, then it follows from

Kwon and Satchell (

2018) Equation (

13) that

where

and

denote the standard normal probability density and cumulative distribution functions, respectively, and we note that the fundamental quantities that determine the expected returns from the pairs trading and the CSM strategies were

,

, and

. It follows from (

4) and (5) that

is effectively the Sharpe ratio corresponding to the portfolio consisting of a long position in the first asset and a short position in the second asset, and given the popularity of the Sharpe ratio with practitioners, we define

and rewrite

in terms of

so that

It follows immediately from (

9) that if

and

, then

. That is, if the first asset has a higher expected return and auto-correlation of the spread,

, is positive, then the expected return from the CSM strategy is positive.

We now examine the sensitivity of the expected CSM return with respect to the parameters

and

. Firstly, we have

so that the expected CSM return is an increasing function of the spread auto-correlation

. Next, we have

so that CSM return is increasing in

if

and decreasing in

if

. In particular, it then follows that for each fixed

and

, the minimum of

occurs at

, or equivalently when

, with corresponding value

.

If the investor knew with certainty that

, so that

, then the investor could construct a portfolio at time

t consisting of a long position in the first asset and a short position in the second asset. Such an investor could be considered to be a perfect-pairs trader, and the return from the strategy at time

would be

, which is normal with mean

and variance

. From (

8) and (

9), the difference between the expected return on the pairs trading strategy and the expected CSM return is

and this difference is clearly positive if

. This condition is intuitively clear, since pairs trading relies on asset prices that diverged over a prior period to revert back to their common mean, whereas the CSM strategy relies on the opposite being the case. We now proceed to analyze the difference (

10) in more detail, and begin by recognizing that the first term inside the parentheses in (

10) is related to the so-called Mill’s ratio,

, defined by

It follows from a result on page 132 of

Sampford (

1953) that if

, then

and since it is assumed that

, Mill’s ratio will satisfy (

12) in the case of a perfect-pairs trader. In what follows, we make use of the upper bound,

, in (

12) to obtain a condition under which CSM outperforms the perfect-pairs trading, and so it is of interest to examine how close

is to

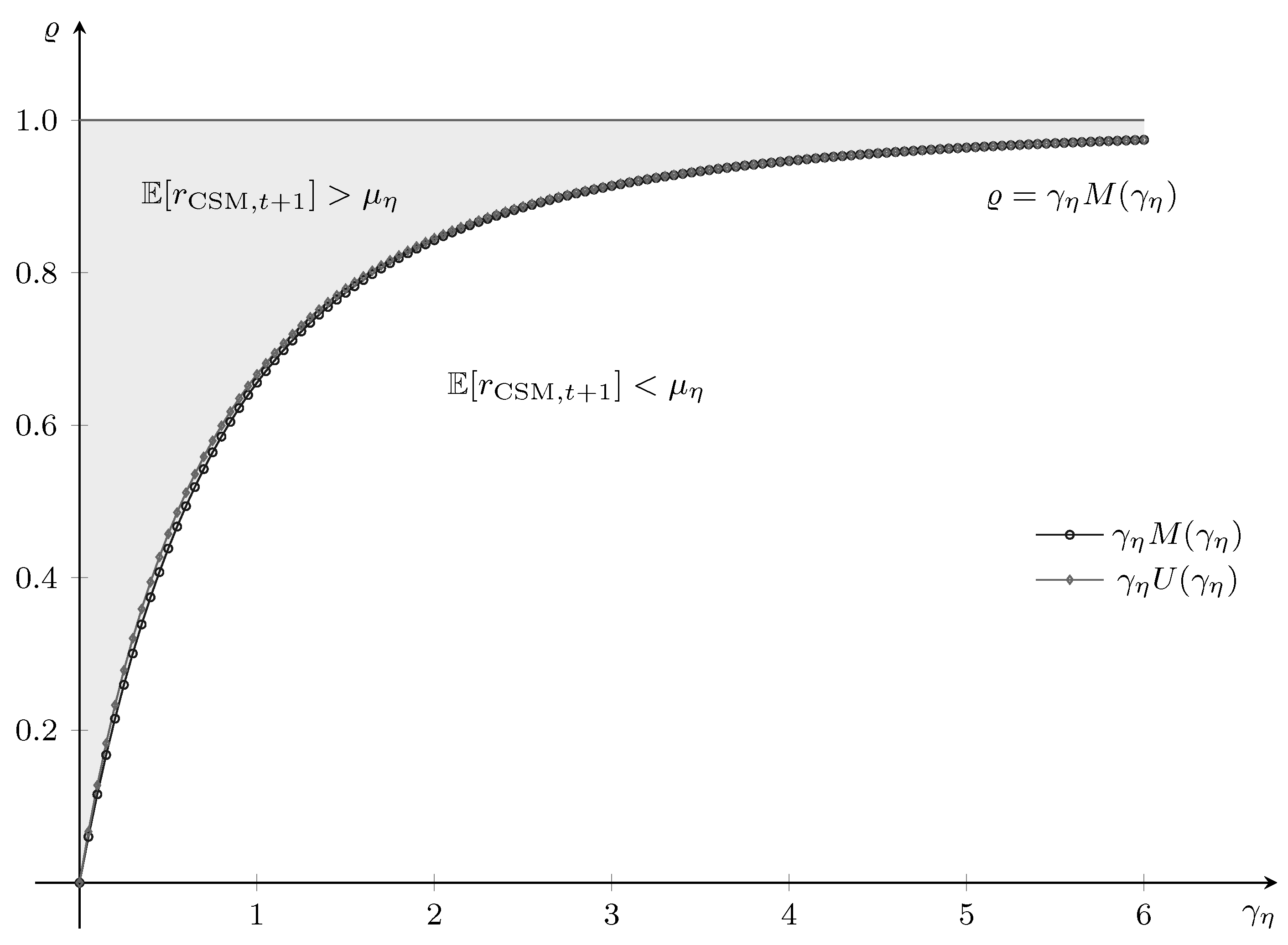

. The plot of the two functions in

Figure 1 shows that

is indeed a tight upper bound for

, with the maximum difference between

and

in the region

being approximately

at

.

Now, we have from (

10) that

and since

, a sufficient condition for

is

Given that for a perfect-pairs trader

, this is equivalent to

Denoting by

the quadratic

we have that (

13) is equivalent to

. In order to proceed further, we must consider three cases, viz.,

,

, and

. Firstly, if

, then

, and (

13) reduces to

so that the condition becomes

Next, note that if

, then the roots,

, of

are real and given by

If

, then

is concave, and taking into account the restriction

, we have

if and only if

so that the condition on

in this case is

where

is positive since

. Finally, if

, then

is convex, but surprisingly the condition on

is the same as for the case

. In summary, if we define

, where

is as given in (

16), then

if

.

As shown in

Figure 1, the interval

decreases with

so that the range of values of

over which the perfect pairs trading strategy outperforms the CSM strategy increases with

. It is worth noting that the Sharpe ratios reported in

Gatev et al. (

2003), obtained by considering pairs trading strategies using US stocks from 1962 to 2002, lie in the range

. For the CSM strategy to outperform the pairs trading strategy over such a range of

, the corresponding

will need to be in the range

. We note that

is the autocorrelation in the spread and not an individual asset autocorrelation.

3. Comparison of Imperfect Pairs Trading and CSM

We now assume that pairs trading is not perfect so that the assumed condition

is no longer certain, but instead holds with some probability

. Since the asset prices that diverged over a prior period do not always revert, this is perhaps the situation that is more likely to be of practical relevance. The expected return,

, on the pairs trading strategies in this case, is then

Moreover, the difference between the expected returns from the imperfect pairs trading and the CSM strategy is now

and it follows that

if and only if

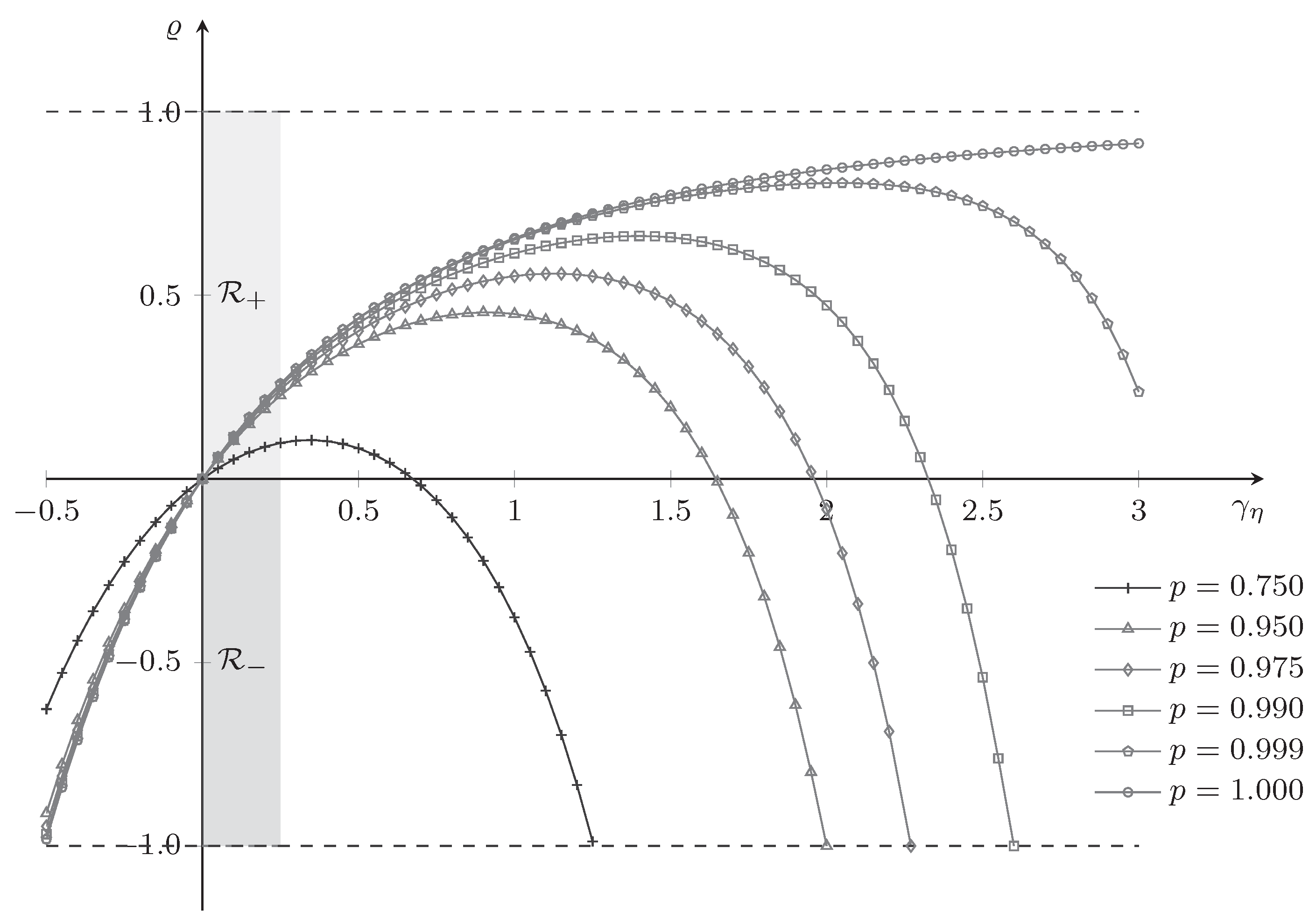

The impact of the probability

p on the right-hand side of (

20), and hence on

, is plotted in

Figure 2, and we see that the performance of the pairs trading strategy relative to the CSM strategy is extremely sensitive to

p. In fact, even the slightest uncertainty in the required condition

for the pairs trading strategy to be fully effective results in a significant change to the region in the

space over which the pairs trading outperforms CSM.

Before closing this section, we note that the situation under which pairs trading would most likely be employed in practice is where

and are small, and

. Since this corresponds to the case where the two assets have similar expected returns, any difference in the returns over a prior period is likely to reverse over the subsequent period, and the reversal will result in

. This is the region labeled

in

Figure 2, and as expected, pairs trading outperforms the CSM strategy in this region. The situation in which the CSM strategy would be appropriate is where

and

, which corresponds to the region labeled

in

Figure 2. It is interesting to note that in much of the practically relevant subregion of

where

is small, the pairs trading strategy still outperforms the CSM strategy other than when

.

4. Conclusions

In this paper, the relative performances of pairs trading and cross-sectional momentum (CSM) strategies were investigated in terms of their expected returns. The Sharpe ratio, , and the autocorrelation, , in the asset return spread were identified as the key factors that determine the performances of the two strategies, and an analytic condition specifying the region in the space over which one strategy outperforms the other was derived in terms of these factors.

It was also shown that although the performance of the pairs trading strategy is highly sensitive to the probability of the asset prices reverting, it not only outperforms the CSM strategy in situations where it is most likely to be used, but also does in the majority of the practically relevant situations where the CSM strategy would be most appropriate.

{kind=link}

{kind=link}