Innovative Corporate Initiatives to Reduce Climate Risk: Lessons from East Asia

{kind=link}

Abstract

:1. Introduction

2. Materials and Methods

2.1. Climate Risks Faced by Firms

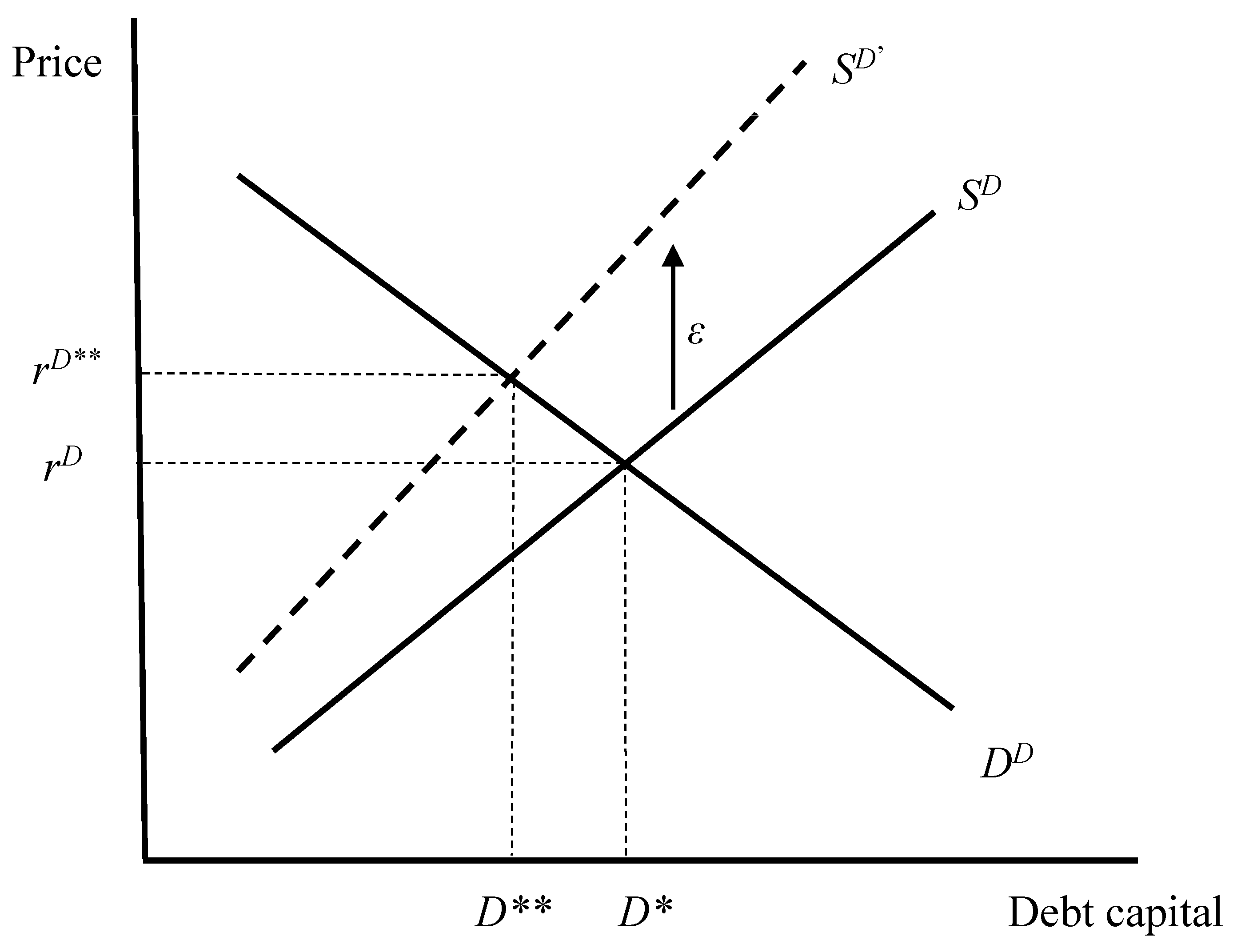

2.2. Climate Risks and Firm Debt

3. Results

3.1. Impact of Climate Risk on the Cost of Capital

3.2. Business Climate Initiatives

3.2.1. Measurement and Reporting

3.2.2. Targets and Pledges

3.2.3. Pricing Mechanisms and Business Models

3.2.4. Forums and Events

3.3. Climate Finance Initiatives

4. Discussion

4.1. Policies to Support Climate Business and Finance

- Financial regulations that support investment decision-making that takes into account improved environmental performance.

- Establishing better risk management and reporting requirements to improve environmental performance and green STI.

- Developing international guidelines and common policy and legal frameworks to support better and more comprehensive environmental risk management, assessments and reporting.

4.1.1. Support of Climate Risk Management in Investment Decisions

4.1.2. Improving Climate Performance and Green STI

- Climate and environmental management measures, which include the development of a corporate climate and environmental strategy, integration of environmental issues into strategic planning processes, environmental practices, process-driven initiatives, product-driven management systems, environmental certification, environmental management system adoption, and participation in voluntary environmental improvement programs.

- Climate and environmental performance assessments, which evaluate climate and environmental impacts through use of specific indicators such as carbon dioxide emissions, physical waste, water consumption, toxic release, chemical spills, raw material input use, or materials recycling.

- Climate and environmental disclosures, which describe the various environmental impacts of a firm’s activities, and may involve information on toxic releases, environmental accidents, and crises, as well as announcements of specific environmental investments.

4.1.3. International Climate Guidelines and Frameworks

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Barbier, E.B. The Green Economy Post Rio+20. Science 2012, 338, 887–888. [Google Scholar] [CrossRef] [PubMed]

- Barbier, E.B. Policies to Promote Green Economy Innovation in East Asia and North America. STI Policy Rev. 2015, 6, 54–69. [Google Scholar]

- Heede, R. Tracing anthropogenic carbon dioxide and methane emissions to fossil fuel and cement producers, 1854–2010. Clim. Chang. 2014, 122, 229–241. [Google Scholar] [CrossRef]

- State of Green Business 2017. Available online: https://www.greenbiz.com/report/state-green-business-2017 (accessed on 20 December 2017).

- Carbon Disclosure Project (CDP). CDP Global Water Report 2015. 2015. Available online: https://www.cdp.net/CDPResults/CDP-Global-Water-Report-2015.pdf (accessed on 20 December 2017).

- CAIT Climate Data Explorer. Business Emissions Targets; World Resources Institute: Washington, DC, USA, 2016. [Google Scholar]

- Carbon Disclosure Project (CDP). Global Corporate Use of Carbon Pricing: Disclosures to Investors. 2014. Available online: http://www.cdp.net/CDPResults/global-price-on-carbon-report-2014.pdf (accessed on 20 December 2017).

- Carbon Disclosure Project (CDP). More than Eight-Fold Leap over Four Years in Global Companies Pricing Carbon into Business Plans—CDP. 2017. Available online: https://www.cdp.net/en/articles/media/more-than-eight-fold-leap-over-four-years-in-global-companies-pricing-carbon-into-business-plans (accessed on 20 December 2017).

- Aktas, N.; De Bodt, E.; Cousin, J.-G. Do financial markets care about SRI? Evidence from mergers and acquisitions. J. Bank. Financ. 2011, 35, 1753–1761. [Google Scholar] [CrossRef]

- Albertini, E. Does Environmental Management Improve Financial Performance? A Meta-Analytical Review. Organ. Environ. 2013, 26, 431–457. [Google Scholar] [CrossRef]

- Barbier, E.B.; Burgess, J.C. Policies to Support Environmental Risk Management in Investment Decisions. Int. J. Glob. Environ. Issues 2017, in press. [Google Scholar]

- Cai, L.; Cui, J.; Jo, H. Corporate Environmental Responsibility and Firm Risk. J. Bus. Ethics 2016, 139, 563–594. [Google Scholar] [CrossRef]

- Chava, S. Environmental Externalities and Cost of Capital. Manag. Sci. 2014, 60, 2223–2247. [Google Scholar] [CrossRef]

- Ghoul, E.S.; Guedhami, O.; Kim, H.; Park, K. Corporate Environmental Responsibility and the Cost of Capital: Empirical Evidence; KAIST Business School Working Paper Series, KCB-WP-2014-008; KAIST College of Business: Soeul, Korea, 2014. [Google Scholar]

- Endrikat, J.; Guenther, E.; Hoppe, H. Making sense of conflicting empirical findings: A meta-analysis of the relationship between corporate environmental and financial performance. Eur. Manag. J. 2014, 32, 735–751. [Google Scholar] [CrossRef]

- Sharfman, M.R.; Fernando, C.S. Environmental Risk Management and the Cost of Capital. Strateg. Manag. J. 2008, 29, 569–592. [Google Scholar] [CrossRef]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate Social Responsibility and Access to Finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Covington, H.; Thornton, J.; Hepburn, C. Shareholders must vote for climate change mitigation. Nature 2016, 530, 156–157. [Google Scholar] [CrossRef] [PubMed]

- Dobler, M.; Lajili, K.; Zéghal, D. Environmental Performance, Environmental Risk Management and Risk Management. Bus. Strateg. Environ. 2014, 23, 1–17. [Google Scholar] [CrossRef]

- Nandy, M.; Lodh, S. Do banks value the eco-friendliness of firms in their corporate lending decision? Some empirical evidence. Int. Rev. Financ. Anal. 2012, 25, 83–93. [Google Scholar] [CrossRef] [Green Version]

- UN Environment Programme (UNEP). The Financial System We Need: Aligning the Financial System with Sustainable Development; UN Environment Programme (UNEP): Nairobi, Kenya, 2015; Available online: http://web.unep.org/inquiry (accessed on 20 December 2017).

- Intergovernmental Panel on Climate Change (IPCC). Climate Change 2014: Synthesis Report; Contribution of Working Groups I, II and III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Core Writing Team, Pachauri, R.K., Meyer, L.A., Eds.; Intergovernmental Panel on Climate Change (IPCC): Geneva, Switzerland, 2014. [Google Scholar]

- Principles for Responsible Investment. About the PRI. 2017. Available online: https://www.unpri.org/about (accessed on 20 December 2017).

- G20 Finance Ministers and Central Bank Governors Meeting Shanghai. Available online: http://www.g20.utoronto.ca/2016/160227-finance-en.html (accessed on 20 December 2017).

- Kane, S.; Shogren, J.F. Linking Adaptation and Mitigation in Climate Change Policy. Clim. Chang. 2000, 45, 75–102. [Google Scholar] [CrossRef]

- Porter, M.D.; van der Linde, C. Toward a New Conception of the Environment Competitiveness Relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Goss, A.; Roberts, G.S. The impact of corporate social responsibility on the cost of bank loans. J. Bank. Financ. 2011, 35, 1794–1810. [Google Scholar] [CrossRef]

- Heinkel, R.; Kraus, A.; Zechner, J. The Effect of Green Investment on Corporate Behavior. J. Financ. Quant. Anal. 2001, 36, 431–449. [Google Scholar] [CrossRef]

- Natural Capital Coalition. Available online: http://naturalcapitalcoalition.org/protocol/ (accessed on 20 December 2017).

- International Council of Forest and Paper Associations (ICFPA). ICFPA Sustainability Progress Report. Available online: http://www.icfpa.org/uploads/Modules/Publications/2015-icfpa-sustainability-progress-report.pdf (accessed on 20 December 2017).

- Global Reporting Initiative (GRI). Consolidated Set of GRI Sustainable Reporting Standards 2016. Available online: https://www.globalreporting.org/standards (accessed on 20 December 2017).

- Global Reporting Initiative (GRI). Sustainability Reporting Database. Available online: http://database.globalreporting.org/ (accessed on 20 December 2017).

- CDP Disclosure Insight Action. 2017. Available online: https://www.cdp.net/en (accessed on 20 December 2017).

- Corporate Knights. 2017 Global 100 Results. Available online: http://www.corporateknights.com/reports/2017-global-100/2017-global-100-results-14846083/ (accessed on 20 December 2017).

- Makower, J. 10th Annual State of Green Business 2017. Available online: https://www.greenbiz.com/ (accessed on 20 December 2017).

- Moving Forward with SDGs: Metrics for Action. Available online: https://www.trucost.com/ (accessed on 20 December 2017).

- International Organization for Standardization (ISO). Survey of Management System Standardization Certification. 2016. Available online: https://www.iso.org/iso-14001-environmental-management.html (accessed on 20 December 2017).

- Association of Southeast Asian Nations (ASEAN). ASEAN 2025: Forging Ahead Together; ASEAN Secretariat: Jakarta, Indonesia, 2015; Available online: http://www.asean.org/storage/2015/12/ASEAN-2025-Forging-Ahead-Together-final.pdf (accessed on 20 December 2017).

- ASEAN Centre for Energy (ACE). ASEAN Plan of Action for Energy Cooperation (APAEC) 2016–2025. Phase I: 2016–2020; ASEAN Centre for Energy (ACE): Jakarta, Indonesia, 2015; Available online: https://app.box.com/s/g6b4ynph5wwiuvtxgol3s2rwjwcmrtbj (accessed on 20 December 2017).

- ABB. Let’s Write the Future. Available online: http://new.abb.com/ (accessed on 20 December 2017).

- UN Environment Programme Financial Initiative (UNEP FI); Global Canopy Programme. Towards Including Natural Resource Risks in Cost of Capital, State of Play and the Way Forward, Natural Capital Declaration; UN Environment Programme (UNEP): Nairobi, Kenya, 2015; Available online: http://www.unepfi.org/fileadmin/documents/NCD-NaturalResourceRisksScopingStudy.pdf (accessed on 20 December 2017).

- China Water Risk. Vision and Mission. Available online: http://chinawaterrisk.org/about/vision-mission/ (accessed on 20 December 2017).

- GreenBiz. Events. Available online: https://www.greenbiz.com/events/ (accessed on 20 December 2017).

- The Economist. The Sustainability Summit. Available online: http://www.economist.com/events-conferences/emea/sustainability-summit-2017/ (accessed on 20 December 2017).

- Global Initiatives. Advancing Partnership Solutions to Global Challenges. Available online: http://www.globalinitiatives.com/ (accessed on 20 December 2017).

- Sustainable Energy and Technology Asia (SETA). Exhibit @ SETA 2018. Available online: https://www.seta.asia/ (accessed on 20 December 2017).

- IFAT. World’s Leading Trade Fair for Water, Sewage, Waste and Raw Materials Management. Available online: http://www.ifat.de/index-2.html (accessed on 20 December 2017).

- Mechler, R.; Schinko, T. Identifying the Policy Space for Climate Loss and Damage. Science 2016, 354, 290–292. [Google Scholar] [CrossRef] [PubMed]

- The Equator Principles. The Equator Principles III. Available online: http://www.equator-principles.com (accessed on 20 December 2017).

- Sullivan, R.; Feller, E.; Martindale, W.; Robinson, J. Investor Obligations and Duties in 6 Asian Markets; UN Environmental Programme Financial Initiative/Principles for Responsible Investment/The Generation Foundation: Nairobi, Kenya, 2016; Available online: http://www.unepfi.org/fileadmin/documents/Investor_obligations_and_duties_in_six_asian_markets.pdf (accessed on 20 December 2017).

- United Nations Climate Change. 2016 Forum of Standing Committee on Finance. Available online: http://unfccc.int/cooperation_and_support/financial_mechanism/standing_committee/items/9410.php (accessed on 20 December 2017).

- Beare, D.; Buslovich, R.; Searcy, C. Linkages between Corporate Sustainability Reporting and Public Policy. Corp. Soc. Responsib. Environ. Manag. 2014, 21, 336–350. [Google Scholar] [CrossRef]

- Ervin, D.; Wu, J.; Khanna, M.; Jones, C.; Wirkkala, T. Motivations and Barriers to Corporate Environmental Management. Bus. Strateg. Environ. 2013, 22, 390–409. [Google Scholar] [CrossRef]

- Lai, A.; Melloni, G.; Stacchezzini, R. Corporate Sustainable Development: Is ‘Integrated Reporting’ a Legitimization Strategy? Bus. Strateg. Environ. 2014, 25, 165–177. [Google Scholar] [CrossRef]

- Pérez-López, D.; Moreno-Romero, A.; Barkemeyer, R. The Relationship between Sustainability Reporting and Sustainability Management Practices. Bus. Strateg. Environ. 2015, 24, 720–734. [Google Scholar] [CrossRef]

- Sierra-García, L.; Zorio-Grima, A.; García-Benau, M.A. Stakeholder Engagement, Corporate Social Responsibility and Integrated Reporting: An Exploratory Study. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 286–304. [Google Scholar] [CrossRef]

- Rexhäuser, S.; Rammer, C. Environmental innovations and firm profitability: Unmasking the Porter hypothesis. Environ. Resour. Econ. 2014, 57, 145–167. [Google Scholar] [CrossRef]

- GRI. Driving Global Change Since 1997. Available online: https://www.globalreporting.org (accessed on 20 December 2017).

- Corporate Register. The World’s Largest CR Report Directory. Available online: http://www.corporateregister.com/ (accessed on 20 December 2017).

- Integrated Reporting. Progress through Reporting. Available online: http://integratedreporting.org/ (accessed on 20 December 2017).

- Barbier, E.B. Nature and Wealth: Overcoming Environmental Scarcities and Inequality; Palgrave MacMillan: London, UK, 2015. [Google Scholar]

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Barbier, E.B.; Burgess, J.C. Innovative Corporate Initiatives to Reduce Climate Risk: Lessons from East Asia. Sustainability 2018, 10, 13. https://doi.org/10.3390/su10010013

Barbier EB, Burgess JC. Innovative Corporate Initiatives to Reduce Climate Risk: Lessons from East Asia. Sustainability. 2018; 10(1):13. https://doi.org/10.3390/su10010013

Chicago/Turabian StyleBarbier, Edward B., and Joanne C. Burgess. 2018. "Innovative Corporate Initiatives to Reduce Climate Risk: Lessons from East Asia" Sustainability 10, no. 1: 13. https://doi.org/10.3390/su10010013

APA StyleBarbier, E. B., & Burgess, J. C. (2018). Innovative Corporate Initiatives to Reduce Climate Risk: Lessons from East Asia. Sustainability, 10(1), 13. https://doi.org/10.3390/su10010013