TMT’s Attention towards Financial Goals and Innovation Investment: Evidence from China

Abstract

:1. Introduction

2. Theory and Hypotheses

2.1. TMT’s Attention and Strategic Choice

2.2. TMT’s Attention towards Financial Goals and Enterprise Innovation Investment

2.3. The Moderating Role of Ownership Type and Firm Size

2.3.1. Firm Ownership

2.3.2. Firm Size

3. Methodology

3.1. Data and Sample

3.2. Measures

3.2.1. Dependent Variable

3.2.2. Independent Variable

3.2.3. Moderating Variables

3.2.4. Control Variables

4. Results

4.1. Descriptive Statistics and Correlation Analysis

4.2. Hypothesis Testing

4.2.1. Main Effect

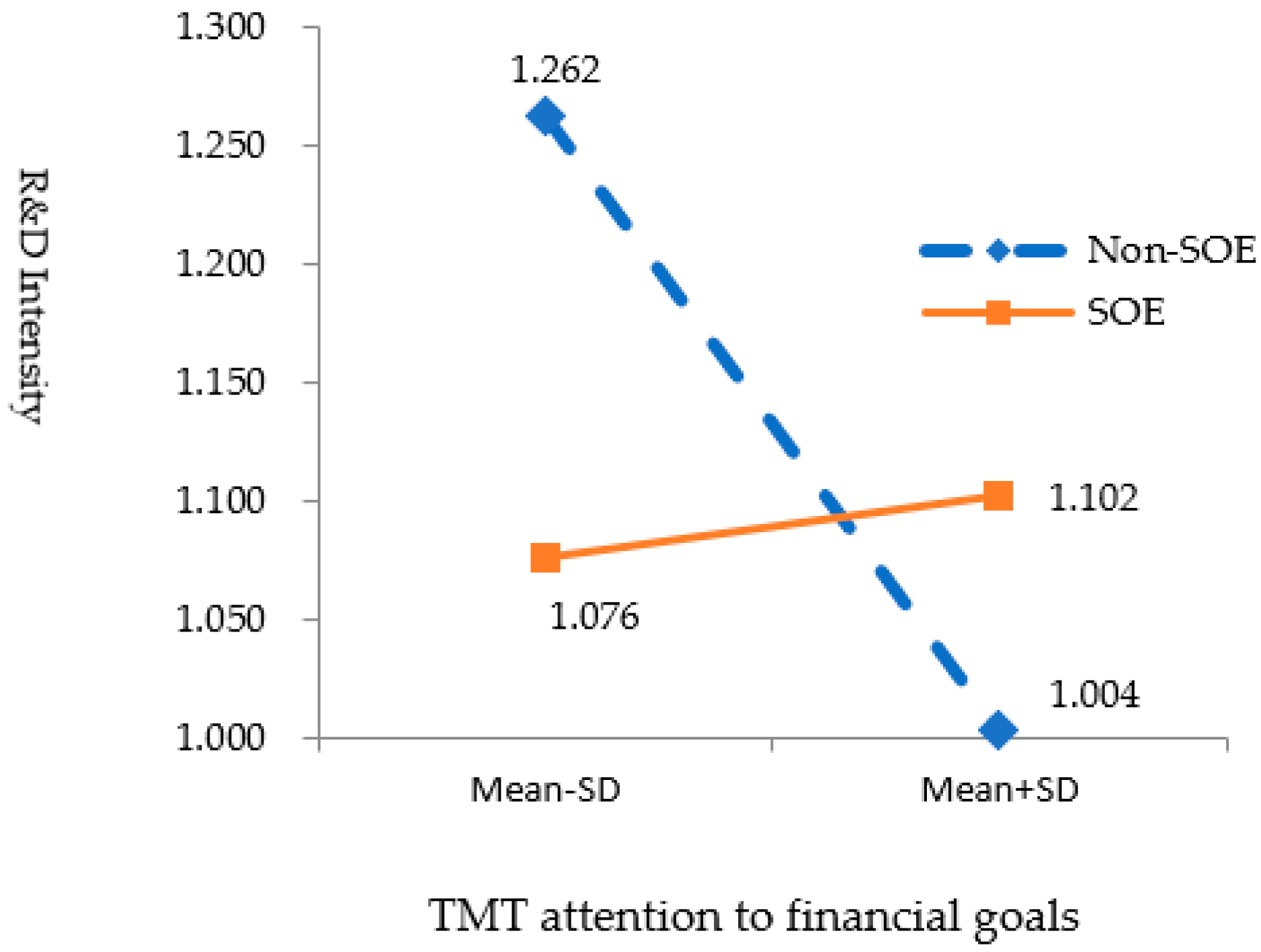

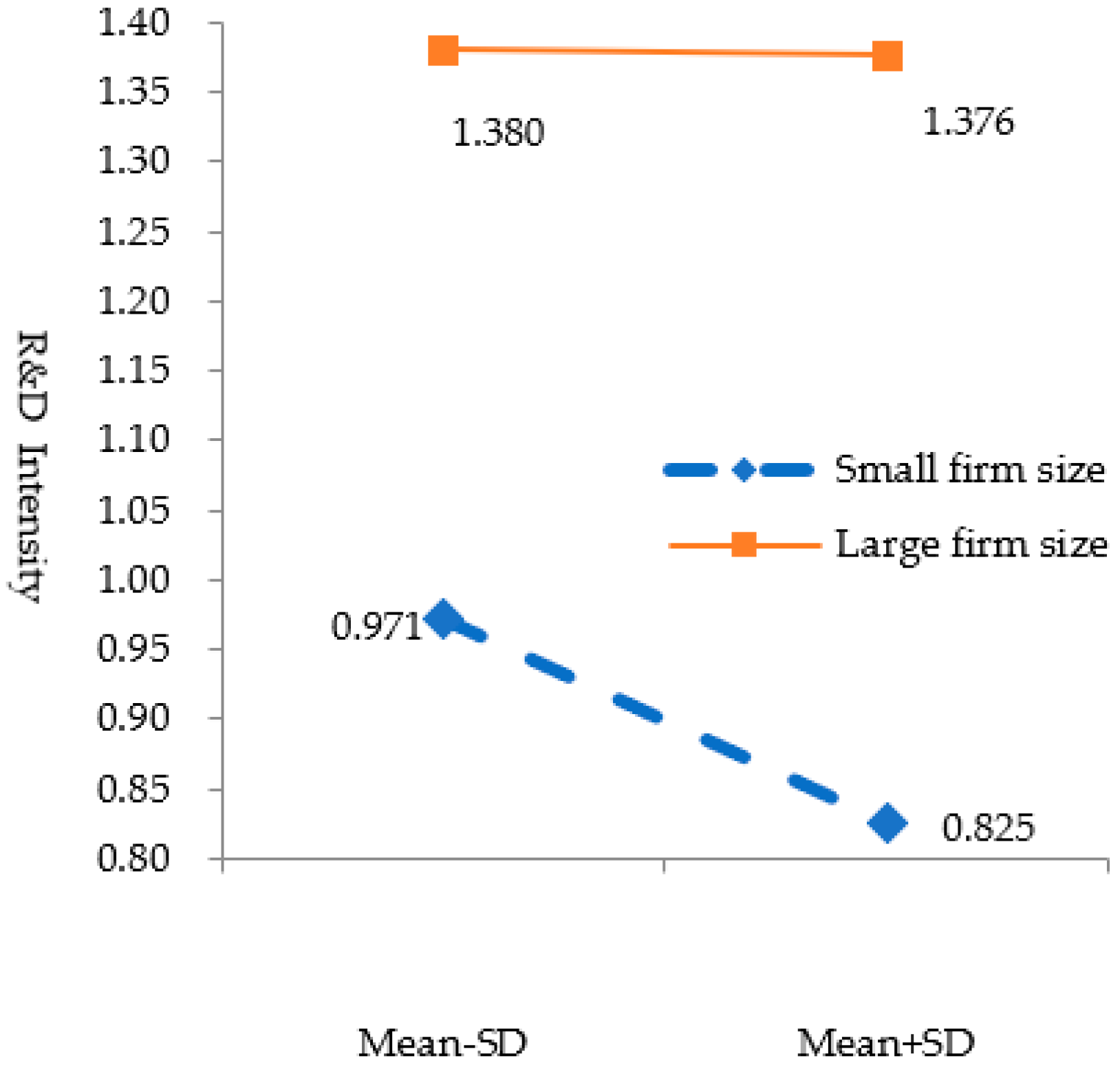

4.2.2. Moderating Effect

5. Discussion

5.1. Theoretical Implication

5.2. Practical Implications

5.3. Limitations and Future Research Directions

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Hambrick, D.C.; Mason, P.A. Upper echelons: The organization as a reflection of its top managers. Acad. Manag. Rev. 1984, 9, 193–206. [Google Scholar] [CrossRef]

- Haleblian, J.; Finkelstein, S. Top management team size, CEO dominance, and firm performance: The moderating roles of environmental turbulence and discretion. Acad. Manag. J. 1993, 36, 844–863. [Google Scholar]

- Carpenter, M.A.; Geletkanycz, M.A.; Sanders, W.G. Upper echelons research revisited: Antecedents, elements, and consequences of top management team composition. J. Manag. 2004, 30, 749–778. [Google Scholar] [CrossRef]

- Buyl, T.; Boone, C.; Hendriks, W.; Matthyssens, P. Top management team functional diversity and firm performance: The moderating role of CEO characteristics. J. Manag. Stud. 2011, 48, 151–177. [Google Scholar] [CrossRef]

- Hambrick, D.C.; Finkelstein, S.; Mooney, A.C. Executive job demands: New insights for explaining strategic decisions and leader behaviors. Acad. Manag. Rev. 2005, 30, 472–491. [Google Scholar] [CrossRef]

- Kaplan, S. Cognition, capabilities, and incentives: Assessing firm response to the fiber-optic revolution. Acad. Manag. J. 2008, 51, 672–695. [Google Scholar]

- Chadee, D.; Roxas, B. Institutional environment, innovation capacity and firm performance in Russia. Crit. Perspect. Int. Bus. 2013, 9, 19–39. [Google Scholar] [CrossRef]

- Tellis, G.J.; Prabhu, J.C.; Chandy, R.K. Radical innovation across nations: The preeminence of corporate culture. Br. J. Mark. 2009, 73, 3–23. [Google Scholar] [CrossRef]

- Fang, V.W.; Tian, X.; Tice, S. Does stock liquidity enhance or impede firm innovation? Eur. J. Financ. 2014, 69, 2085–2125. [Google Scholar] [CrossRef]

- Flammer, C.; Kacperczyk, A. The impact of stakeholder orientation on innovation: Evidence from a natural experiment. Manag. Sci. 2015, 62, 1982–2001. [Google Scholar] [CrossRef]

- Balta, M.E.; Woods, A.; Dickson, K. Strategic decision-making processes as a mediator of the effect of board characteristics on company innovation: A study of publicly-listed firms in Greece. Phys. D 2013, 79, 306–319. [Google Scholar]

- Yadav, M.S.; Prabhu, J.C.; Chandy, R.K. Managing the future: CEO attention and innovation outcomes. Br. J. Mark. 2007, 71, 84–101. [Google Scholar] [CrossRef]

- Nadkarni, S.; Chen, J. Bridging yesterday, today, and tomorrow: CEO temporal focus, environmental dynamism, and rate of new product introduction. Acad. Manag. J. 2014, 57, 1810–1833. [Google Scholar] [CrossRef]

- Tan, J. Innovation and risk-taking in a transitional economy: A comparative study of Chinese managers and entrepreneurs. J. Bus. Ventur. 2001, 16, 359–376. [Google Scholar] [CrossRef]

- Lall, S. Technological capabilities and industrialization. World Dev. 1992, 20, 165–186. [Google Scholar] [CrossRef] [Green Version]

- Li, J.; Tang, Y.I. CEO Hubris and firm risk taking in China: The moderating role of managerial discretion. Acad. Manag. J. 2010, 53, 45–68. [Google Scholar] [CrossRef]

- Hambrick, D.C. Upper echelons theory: An update. Acad. Manag. Rev. 2007, 32, 334–343. [Google Scholar] [CrossRef]

- Ocasio, W. Towards an attention-based view of the firm. Strateg. Manag. J. 1997, 18, 187–206. [Google Scholar] [CrossRef]

- Simon, H.A. Administrative Behaviour: A Study of the Decision Making Processes in Administrative Organization; Macmillan Company: London, UK, 1948. [Google Scholar]

- Cyert, R.M.; March, J.G. A Behavioral Theory of the Firm; Prentice-Hall: Englewood Cliffs, NJ, USA, 1963; Volume 2, pp. 169–187. [Google Scholar]

- March, J.G.; Olsen, J.P. Ambiguity and Choice in Organizations; Universitetsforlaget: Oslo, Norway, 1976. [Google Scholar]

- Simon, H.A. Administrative Behaviour: A Study of Decision-Making Processes in Administrative Organizations, 4th ed.; The Free Press: New York, NY, USA, 1947. [Google Scholar]

- Barnett, M.L. An attention-based view of real options reasoning. Acad. Manag. Rev. 2008, 33, 606–628. [Google Scholar] [CrossRef]

- Shepherd, D.A.; McMullen, J.S.; Ocasio, W. Is that an opportunity? An attention model of top managers’ opportunity beliefs for strategic action. Strateg. Manag. J. 2017, 38, 626–644. [Google Scholar] [CrossRef]

- Cho, T.S.; Hambrick, D.C. Attention as the mediator between top management team characteristics and strategic change: The case of airline deregulation. Organ. Sci. 2006, 17, 453–469. [Google Scholar] [CrossRef]

- Eggers, J.P.; Kaplan, S. Cognition and renewal: Comparing CEO and organizational effects on incumbent adaptation to technical change. Organ. Sci. 2009, 20, 461–477. [Google Scholar] [CrossRef]

- Chen, S.; Bu, M.; Wu, S.; Liang, X. How does TMT attention to innovation of Chinese firms influence firm innovation activities? A study on the moderating role of corporate governance. J. Bus. Res. 2015, 68, 1127–1135. [Google Scholar] [CrossRef]

- Ren, C.R.; Guo, C. Middle managers’ strategic role in the corporate entrepreneurial process: Attention-based effects. J. Manag. 2011, 37, 1586–1610. [Google Scholar] [CrossRef]

- Bouquet, C.; Deutsch, Y. The impact of corporate social performance on a firm’s international diversification. J. Bus. Ethics 2008, 80, 755–769. [Google Scholar] [CrossRef]

- Levy, O. The influence of top management team attention patterns on global strategic posture of firms. J. Organ. Behav. 2005, 26, 797–819. [Google Scholar] [CrossRef]

- Plourde, Y.; Parker, S.C.; Schaan, J.L. Expatriation and its effect on headquarters’ attention in the multinational enterprise. Strateg. Manag. J. 2014, 35, 938–947. [Google Scholar] [CrossRef]

- Amason, A.C.; Mooney, A.C. The effects of past performance on top management team conflict in strategic decision making. Int. J. Confl. Manag. 1999, 10, 340–359. [Google Scholar] [CrossRef]

- Simons, T.; Pelled, L.H.; Smith, K.A. Making use of difference: Diversity, debate, and decision comprehensiveness in top management teams. Acad. Manag. J. 1999, 42, 662–673. [Google Scholar]

- Nadler, D.A.; Heilpern, J.D. The CEO in the Context of Discontinuous Change; Harvard Business School Press: Brighton, MA, USA, 1998; pp. 3–27. [Google Scholar]

- Hambrick, D.C. Top management groups: A conceptual integration and reconsideration of the “team” label. In Research in Organizational Behavior; Staw, B., Cummings, L.L., Eds.; JAI Press: Beverly Hill, CA, USA, 1994; Volume 16, pp. 171–213. [Google Scholar]

- Daft, R.L.; Weick, K.E. Toward a model of organizations as interpretation systems. Acad. Manag. Rev. 1984, 9, 284–295. [Google Scholar] [CrossRef]

- Andrews, A.O.; Welbourne, T.M. The people/performance balance in IPO firms: The effect of the Chief Executive Officer's financial orientation. Entrep. Theory. Pract. 2000, 25, 93–106. [Google Scholar] [CrossRef]

- Aghion, P.; Howitt, P. A model of growth through creative destruction. Econometrica 1992, 60, 323–351. [Google Scholar] [CrossRef]

- Grossman, G.M.; Helpman, D. Innovation and Growth in the Global Economy; MIT Press: Cambridge, MA, USA, 1991. [Google Scholar]

- Romer, P.M. Endogenous technological change. J. Polit. Econ. 1990, 98, S71–S102. [Google Scholar] [CrossRef]

- David, P.; Hitt, M.A.; Gimeno, J. The influence of activism by institutional investors on R&D. Acad. Manag. J. 2001, 44, 144–157. [Google Scholar]

- Shleifer, A.; Summers, L.H. Breach of trust in hostile takeovers. In Corporate Takeovers: Causes and Consequences; University of Chicago Press: Chicago, IL, USA, 1988; pp. 33–68. [Google Scholar]

- Kyle, A.S.; Vila, J.L. Noise trading and takeovers. Rand. J. Econ. 1991, 22, 54–71. [Google Scholar] [CrossRef]

- Bushee, B.J. Do institutional investors prefer near-term earnings over long-run value? Contemp. Account. Res. 2001, 18, 207–246. [Google Scholar] [CrossRef]

- Bushee, B.J. The influence of institutional investors on myopic R&D investment behavior. Account. Rev. 1998, 73, 305–333. [Google Scholar]

- Reichelstein, S. Investment decisions and managerial performance evaluation. Rev. Acc. Stud. 1997, 2, 157–180. [Google Scholar] [CrossRef]

- Hansen, G.S.; Hill, C.W.L. Are institutional investors myopic? A time-series study of four technology-driven industries. Strateg. Manag. J. 1991, 12, 1–16. [Google Scholar] [CrossRef]

- Ross, L.; Nisbett, R.E. The Person and the Situation: Perspectives of Social Psychology; Pinter & Martin Publishers: London, UK, 2011. [Google Scholar]

- Fiske, S.T.; Taylor, S. Social Cognition, 2nd ed.; Random House: New York, NY, USA, 1991. [Google Scholar]

- Lioukas, S.; Bourantas, D.; Papadakis, V. Managerial autonomy of state-owned enterprises: Determining factors. Organ. Sci. 1993, 4, 645–666. [Google Scholar] [CrossRef]

- Mintzberg, H. The Nature of Managerial Work; Harper and Row: New York, NY, USA, 1973; Chapters 15–17. [Google Scholar]

- OECD. The Measurement of Scientific and Technical Activities: Proposed Standard practice for Surveys of Research and Development; OECD: Paris, France, 1963. [Google Scholar]

- PWC. State-Owned Enterprises. Catalists for Public Value Creation? Available online: www.prsc.pwc.com (accessed on 29 October 2018).

- Grout, P.A.; Stevens, M. The assessment: Financing and managing public services. Oxf. Rev. Econ. Pol. 2003, 19, 215–234. [Google Scholar] [CrossRef]

- Du, F.; Tang, G.; Young, S.M. Influence activities and favoritism in subjective performance evaluation: Evidence from Chinese state-owned enterprises. Account. Rev. 2012, 87, 1555–1588. [Google Scholar] [CrossRef]

- Jin, Z.; Shang, Y.; Xu, J. The Impact of Government Subsidies on Private R&D and Firm Performance: Does Ownership Matter in China’s Manufacturing Industry? Sustainability 2018, 10, 2205. [Google Scholar]

- Cheng, Q.; Yin, Z.; Ye, J. State-owned enterprises and regional innovation efficiency: From the externality perspective. Ind. Econ. Res. 2015, 77, 10–20. [Google Scholar]

- Liu, F.; Zhang, L. Executive turnover in China’s state-owned enterprises: Government-oriented or market-oriented? China J. Account. Res. 2018, 11, 129–149. [Google Scholar] [CrossRef]

- Schumpeter, J. Creative Destruction. Capital. Soc. Democr. 1942, 825, 82–85. [Google Scholar]

- Galbraith, J.K. American Capitalism; Houghton Mifflin: Boston, MA, USA, 1956. [Google Scholar]

- Scherer, F.M. Industrial Market Structure and Economic Performance, 2nd ed.; Houghton Mifflin: Chicago, IL, USA, 1980. [Google Scholar]

- Symeonidis, G. Innovation, Firm Size and Market Structure; OECD: Paris, France, 1996. [Google Scholar]

- Fisher, F.M.; Temin, P. Returns to scale in research and development: What does the Schumpeterian hypothesis imply? J. Polit. Econ. 1973, 81, 56–70. [Google Scholar] [CrossRef]

- Dosi, G. Sources, procedures and microeconomic effects of innovation. J. Econ. Lit. 1988, 25, 1120–1171. [Google Scholar]

- Acs, Z.J.; Audretsch, D.B. Innovation in large and small firms: An empirical analysis. Am. Econ. Rev. 1988, 78, 678–690. [Google Scholar]

- Acs, J.Z.; Audretsch, D.B. (Eds.) Innovation and Technological Change: An International Comparison; University of Michigan Press: Ann Arbor, MI, USA, 1991. [Google Scholar]

- Acs, J.Z.; Audretsch, D.B. R&D firm size and innovative activity. In Innovation and Technological Change: An International Comparison; University of Michigan Press: Ann Arbor, MI, USA, 1991. [Google Scholar]

- Simeonidis, G. Innovation, Firm Size and Market Structure: Schumpeterian Hypothesis and Some New Themes; OECD Economics Development Working Paper; OECD: Paris, France, 2001; p. 161. [Google Scholar]

- OECD. The Organisation for Economic Co-Operation and Development; OECD: Paris, France, 1963. [Google Scholar]

- UNESCO. Provisional Guide to the Collection of Science Statistics. United Nations Educational Scientific and Cultural Organization; COM/MD/3; UNESCO: Paris, France, 31 December 1968. [Google Scholar]

- Godin, B. The Making of Science, Technology and Innovation Policy: Conceptual Frameworks as Narratives; Centre-Urbanisation Culture Société de l’Institut National de la Recherche Scientifique: Montreal, QC, Canada, 2009; pp. 1945–2005. [Google Scholar]

- Godin, B. Measurement and Statistics on Science and Technology: 1920 to the Present; Routledge: Abingdon, UK, 2004. [Google Scholar]

- Wakeman, S.; Le, T. Measuring the Innovative Activity of New Zealand Firms; New Zealand Productivity Commission: Wellington, New Zealand, 2015. [Google Scholar]

- NSF. Chapter 4: Research and Development: National Trends and International Linkages. In Science and Engineering Indicators 2010; National Science Foundation, National Center for Science and Engineering Statistics, National Science Board: Arlington, VA, USA, 13 October 2015. [Google Scholar]

- Cohen, W.M.; Levin, R.C.; Mowery, D.C. Firm size and R&D intensity: A re-examination. J. Ind. Econ. 1987, 35, 543–565. [Google Scholar]

- Berelson, B. Content Analysis in Communication Research; Free Press: Glencoe, IL, USA, 1952. [Google Scholar]

- U.S. General Accounting Office. Content Analysis: A Methodology for Structuring and Analyzing Written Material; GAO/PEMD-10.3.1; U.S. General Accounting Office: Washington, DC, USA, 1996.

- Krippendorff, K. Content Analysis: An Introduction to Its Methodology; Sage: Newbury Park, CA, USA, 1980. [Google Scholar]

- Weber, R.P. Basic Content Analysis, 2nd ed.; Sage: Newbury Park, CA, USA, 1990. [Google Scholar]

- Sapir, E. Grading, a study in semantics. Philos. Sci. 1944, 11, 93–116. [Google Scholar] [CrossRef]

- Tausczik, Y.R.; Pennebaker, J.W. The psychological meaning of words: LIWC and computerized text analysis methods. J. Lang. Soc. Psychol. 2010, 29, 24–54. [Google Scholar] [CrossRef]

- Chung, C.; Pennebaker, J.W. The Psychological Functions of Function Words. In Frontiers of Social Psychology. Social Communication; Psychology Press: New York, NY, USA, 2007; pp. 343–359. [Google Scholar]

- Gephart, R.P. The textual approach: Risk and blame in disaster sense-making. Acad. Manag. J. 1993, 36, 1465–1514. [Google Scholar]

- Namenwirth, J.Z.; Weber, R.P. Dynamics of Culture; Allen & Unwin: Boston, MA, USA, 2010. [Google Scholar]

- Pennebaker, J.W.; Chung, C.K.; Ireland, M.; Gonzales, A.; Booth, R.J. The development and psychometric properties of LIWC 2007. Austin 2015, 29, 1020–1025. [Google Scholar]

- Cycyota, C.S.; Harrison, D.A. What (not) to expect when surveying executives: A meta-analysis of top manager response rates and techniques over time. Organ. Res. Methods 2006, 9, 133–160. [Google Scholar] [CrossRef]

- Chatterjee, A.; Hambrick, D.C. It’s all about me: Narcissistic chief executive officers and their effects on company strategy and performance. Adm. Sci. Q. 2007, 52, 351–386. [Google Scholar] [CrossRef]

- Roberts, B.W.; Harms, P.; Smiths, J.L.; Dustin, W.; Webb, M. Using multiple methods in personality psychology. In Handbook of Multimethod Measurement in Psychology; Diener, M., Ed.; American Psychological Association: Washington, DC, USA, 2006; pp. 321–335. [Google Scholar]

- Peterson, R.S.; Smith, D.B.; Martorana, P.V.; Owens, P.D. The impact of chief executive officer personality on top management team dynamics: One mechanism by which leadership affects organizational performance. J. Appl. Psychol. 2003, 88, 795–809. [Google Scholar] [CrossRef] [PubMed]

- Kaplan, S.; Murray, F.; Henderson, R. Discontinuities and senior management: Assessing the role of recognition in pharmaceutical firm response to biotechnology. Ind. Corp. Chang. 2003, 12, 203–233. [Google Scholar] [CrossRef]

- Osborne, J.D.; Stubbart, C.I.; Ramaprasad, A. Strategic groups and competitive enactment: A study of dynamic relationships between mental models and performance. Strateg. Manag. J. 2001, 22, 435–454. [Google Scholar] [CrossRef]

- Hu, Y.; Chen, S.; Wang, J. Managerial Humanistic Attention and CSR: Do Firm Characteristics Matter? Sustainability 2018, 10, 4029. [Google Scholar] [CrossRef]

- Roger, R.K.; Grant, J. Content Analysis of Information Cited in Reports of Sell-Side Financial Analysts. J. Financ. Statement Anal. 1997, 3, 17–30. [Google Scholar]

- Clarkson, P.M.; Kao, J.L.; Richardson, G.D. Evidence that management discussion and analysis (MD&A) is a part of a firm's overall disclosure package. Contemp. Account. Res. 1999, 16, 111–134. [Google Scholar] [CrossRef]

- Domadenik, P.; Prasnikar, J.; Svejnar, J. How to increase R&D in transition economies? Evidence from Slovenia. Rev. Dev. Econ. 2008, 12, 193–208. [Google Scholar]

- Coad, A.; Rao, R. Firm growth and R&D expenditure. Econ. Innov. New Technol. 2010, 19, 127–145. [Google Scholar] [Green Version]

- Bloch, C. R&D investment and internal finance: The cash flow effect. Econ. Innov. New Technol. 2005, 14, 213–223. [Google Scholar]

- Mulkay, B.; Hall, B.H.; Mairesse, J. Investment and R&D in France and in the United States. In Investing Today for the World Tomorrow; Herrmann, H., Strauch, R., Eds.; Springer: Berlin, Germany, 2001. [Google Scholar]

- Xu, J.; Sim, J.-W. Characteristics of Corporate R&D Investment in Emerging Markets: Evidence from Manufacturing Industry in China and South Korea. Sustainability 2018, 10, 3002. [Google Scholar]

- Brown, J.R.; Fazzari, S.M.; Petersen, B.C. Financing innovation and growth: Cash flow, external equity, and the 1990s R&D boom. J. Financ. 2009, 64, 151–185. [Google Scholar]

- Bond, S.; Harhoff, D.; Van Reenen, J. Investment, R&D and financial constraints in Britain and Germany. Annales d’Économie et de Statistique 2005, 79–80, 435–463. [Google Scholar]

- Greene, W.H. Econometric analysis. Contr. Manag. Sci. 2002, 89, 182–197. [Google Scholar]

- Wooldridge, J. Econometric Analysis of Crosssection and Panel Data; MIT Press: Cambridge, MA, USA, 2002. [Google Scholar]

- Yang, H.; Zheng, Y.; Zhao, X. Exploration or exploitation? Small firms’ alliance strategies with large firms. Strateg. Manag. J. 2014, 35, 146–157. [Google Scholar] [CrossRef]

- Zhang, Y.; Rajagopalan, N. Once an outsider, always an outsider? CEO origin, strategic change, and firm performance. Strateg. Manag. J. 2010, 31, 334–346. [Google Scholar] [CrossRef]

- Philippe, D.; Durand, R. The impact of norm-conforming behaviors on firm reputation. Strateg. Manag. J. 2011, 32, 969–993. [Google Scholar] [CrossRef]

- Aiken, L.S.; West, S.G. Multiple regression: Testing and interpreting interactions—Institute for social and economic research (ISER). J. Oper. Res. Soc. 1991, 45, 119–120. [Google Scholar]

- March, J.G.; Simon, H.A. Organizations; Wiley: New York, NY, USA, 1958. [Google Scholar]

- Dearborn, D.C.; Simon, H.A. Selective perception: A note on the departmental identifications of executives. Sociometry 1958, 21, 140–144. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Dictionary | Dimension | Amount | Sample |

|---|---|---|---|

| SC-LIWC2007 | Money | 116 | sales, expenses, remuneration, promotion bonus, tax cost, salary income budget |

| Category | Variable | Code | Meaning |

|---|---|---|---|

| Dependent Variable | R&D investment | R&D Intensity | R&D investment/Corporate total assets × 100% |

| Independent Variable | TMT’s attention to financial goals | Money | Key word frequency/Text number × 100% |

| Control Variable | Profitability | ROA | Return on total assets (%) |

| Sales growth | Sales Growth | Growth rate of sales income (%) | |

| The Cash flow of the operating activities | CFO | Operating cash net flow/Corporate total assets | |

| The proportion of the first large shareholders | CR1 | The proportion of the first large shareholder (from CSMAR) | |

| The scale of the independent directors | Board Independence | Number of independent directors/Total number of directors | |

| Firm age | Firm Age | Sample year—Year of establishment | |

| Slack resource | Slack Resource | Cash flow/Corporate total assets | |

| Moderating Variable | Ownership | Ownership | If the enterprise is a state-owned enterprise or the actual controller is a government, the value assigned is 1; otherwise, the value assigned is 0 |

| Firm size | Firm Size | Natural logarithm of corporate total assets |

| Variables | M | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | ROA | 0.031 | 0.065 | ||||||||||

| 2 | Sales Growth | 0.167 | 0.640 | 0.191 ** | |||||||||

| 3 | CFO | 0.036 | 0.074 | 0.355 ** | 0.049 * | ||||||||

| 4 | CR1 | 0.358 | 0.152 | 0.114 ** | −0.009 | 0.113 ** | |||||||

| 5 | Board Independence | 0.365 | 0.049 | −0.009 | 0.023 | −0.018 | 0.017 | ||||||

| 6 | Firm Age | 15.350 | 4.120 | −0.068 ** | 0.010 | −0.010 | −0.238 ** | −0.051 * | |||||

| 7 | Slack Resource | 0.009 | 0.083 | 0.205 ** | 0.119 ** | 0.221 ** | 0.011 | 0.017 | −0.031 | ||||

| 8 | Ownership | 0.550 | 0.497 | −0.109 ** | −0.059 ** | −0.041 * | 0.274 ** | 0.017 | −0.004 | −0.034 | |||

| 9 | Firm Size | 9.616 | 0.551 | 0.129 ** | −0.011 | 0.155 ** | 0.363 ** | −0.029 | −0.103 ** | 0.021 | 0.201 ** | ||

| 10 | Money | 0.084 | 0.012 | −0.043 * | 0.084 ** | −0.072 ** | −0.169 ** | 0.042 * | 0.151 ** | −0.013 | −0.129 ** | −0.247 ** | |

| 11 | Intensity | 1.414 | 1.449 | 0.188 ** | −0.015 | 0.146 ** | 0.054 ** | −0.009 | −0.077 ** | 0.031 | 0.004 | 0.085 ** | −0.184 ** |

| Variables | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 |

|---|---|---|---|---|---|---|

| ROA | 0.707 *** | 0.723 *** | 0.660 *** | 0.632 *** | 0.682 *** | 0.646 *** |

| −0.214 | −0.211 | −0.192 | −0.192 | −0.191 | −0.192 | |

| Sales Growth | −0.044 * | −0.036 * | −0.043 ** | −0.036 * | −0.040 ** | −0.035 * |

| −0.017 | −0.017 | −0.016 | −0.016 | −0.015 | −0.016 | |

| CFO | 0.737 *** | 0.720 *** | 0.677 *** | 0.610 *** | 0.675 *** | 0.607 *** |

| −0.162 | −0.163 | −0.153 | −0.156 | −0.151 | −0.155 | |

| CR1 | 0.069 | −0.01 | −0.452 ** | −0.449 ** | −0.457 *** | −0.455 *** |

| −0.134 | −0.139 | −0.145 | −0.142 | −0.143 | −0.141 | |

| Board Independence | 0.098 | 0.071 | −0.02 | −0.003 | 0.002 | −0.005 |

| −0.26 | −0.263 | −0.255 | −0.259 | −0.253 | −0.257 | |

| Firm Age | −0.001 | −0.001 | −0.008 | −0.006 | −0.007 | −0.005 |

| −0.005 | −0.005 | −0.005 | −0.005 | −0.005 | −0.005 | |

| Slack Resource | −0.017 | −0.026 | −0.094 | −0.072 | −0.091 | −0.071 |

| −0.111 | −0.111 | −0.107 | −0.106 | −0.106 | −0.106 | |

| Money | −6.371 *** | −4.432 *** | −4.258 *** | −3.854 *** | −4.075 *** | |

| −1.165 | −1.158 | −1.137 | −1.129 | (1.106)) | ||

| Ownership | −0.039 | −0.037 | −0.047 | 0.407 *** | ||

| −0.044 | −0.044 | −0.044 | −0.038 | |||

| Firm Size | 0.420 *** | 0.405 *** | 0.408 *** | −0.005 | ||

| −40 | −0.039 | −0.038 | −1.106 | |||

| Money * Ownership | 13.071 *** | 11.424 *** | ||||

| −2.255 | −2.366 | |||||

| Money * Firm size | 6.508 *** | 3.737 * | ||||

| −1.661 | −1.678 | |||||

| Industry sectors | Controlled | Controlled | Controlled | Controlled | Controlled | Controlled |

| Wald Chi2 | 39.83 *** | 69.68 *** | 195.85 *** | 233.10 *** | 221.02 *** | 245.44 *** |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, S.; Xu, K.; Nguyen, L.T.; Yu, G. TMT’s Attention towards Financial Goals and Innovation Investment: Evidence from China. Sustainability 2018, 10, 4236. https://doi.org/10.3390/su10114236

Chen S, Xu K, Nguyen LT, Yu G. TMT’s Attention towards Financial Goals and Innovation Investment: Evidence from China. Sustainability. 2018; 10(11):4236. https://doi.org/10.3390/su10114236

Chicago/Turabian StyleChen, Shouming, Kaidi Xu, Luu Thi Nguyen, and Guangsheng Yu. 2018. "TMT’s Attention towards Financial Goals and Innovation Investment: Evidence from China" Sustainability 10, no. 11: 4236. https://doi.org/10.3390/su10114236

APA StyleChen, S., Xu, K., Nguyen, L. T., & Yu, G. (2018). TMT’s Attention towards Financial Goals and Innovation Investment: Evidence from China. Sustainability, 10(11), 4236. https://doi.org/10.3390/su10114236