Impacts of Carbon Pricing on Brazilian Industry: Domestic Vulnerability and International Trade Exposure

Abstract

:1. Introduction

2. Carbon Pricing Instruments in the Brazilian Climate Policy Framework

2.1. Defining and Designing Carbon Pricing Instruments

2.2. Carbon Pricing in the Brazilian Climate Policy

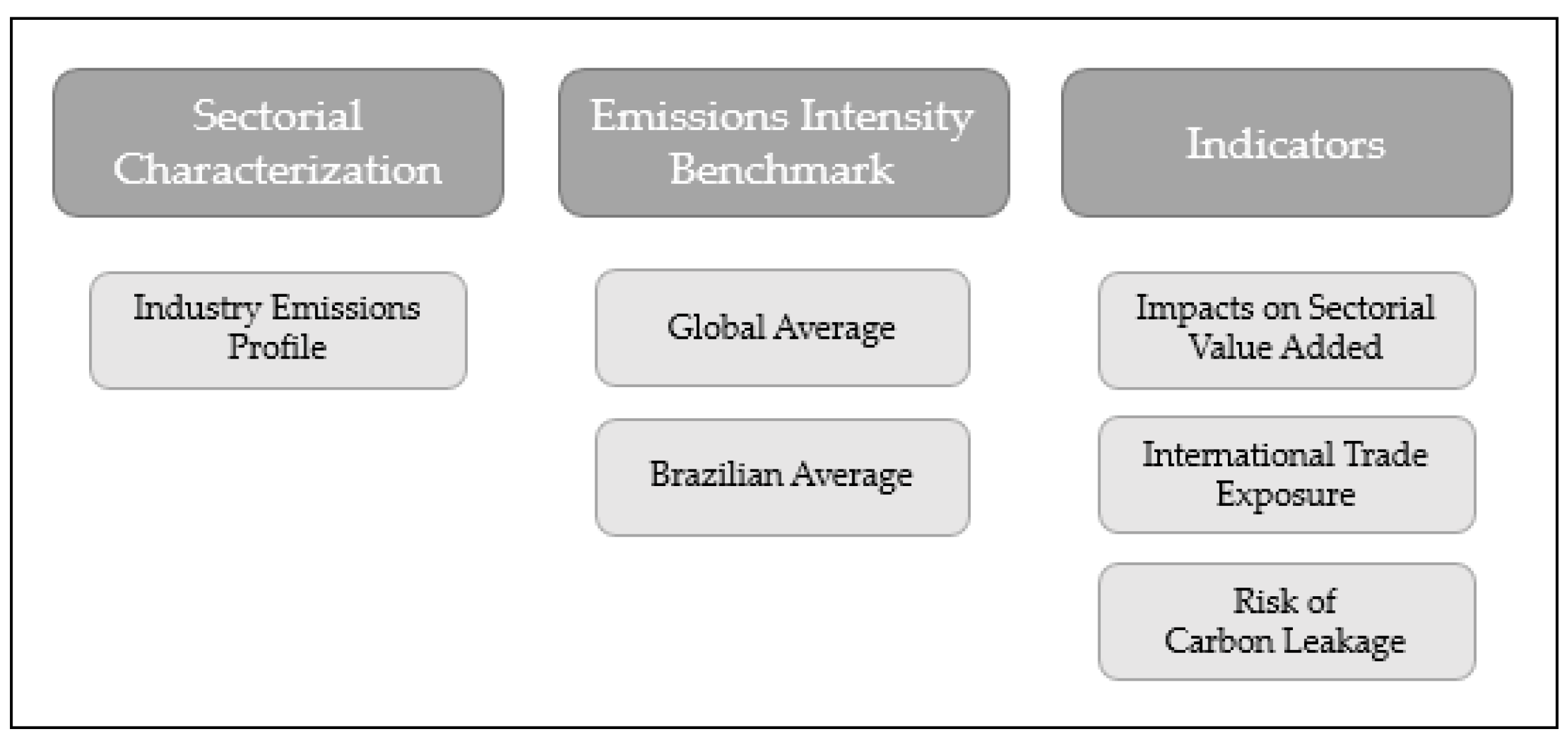

3. Methods

3.1. Sectorial Characterization

3.2. Emissions Intensity Benchmark

3.3. Definition of Indicators

3.3.1. Sectorial Value Added (VA)

3.3.2. Emissions Intensity, International Trade Exposure, and Risk of Carbon Leakage

4. Results

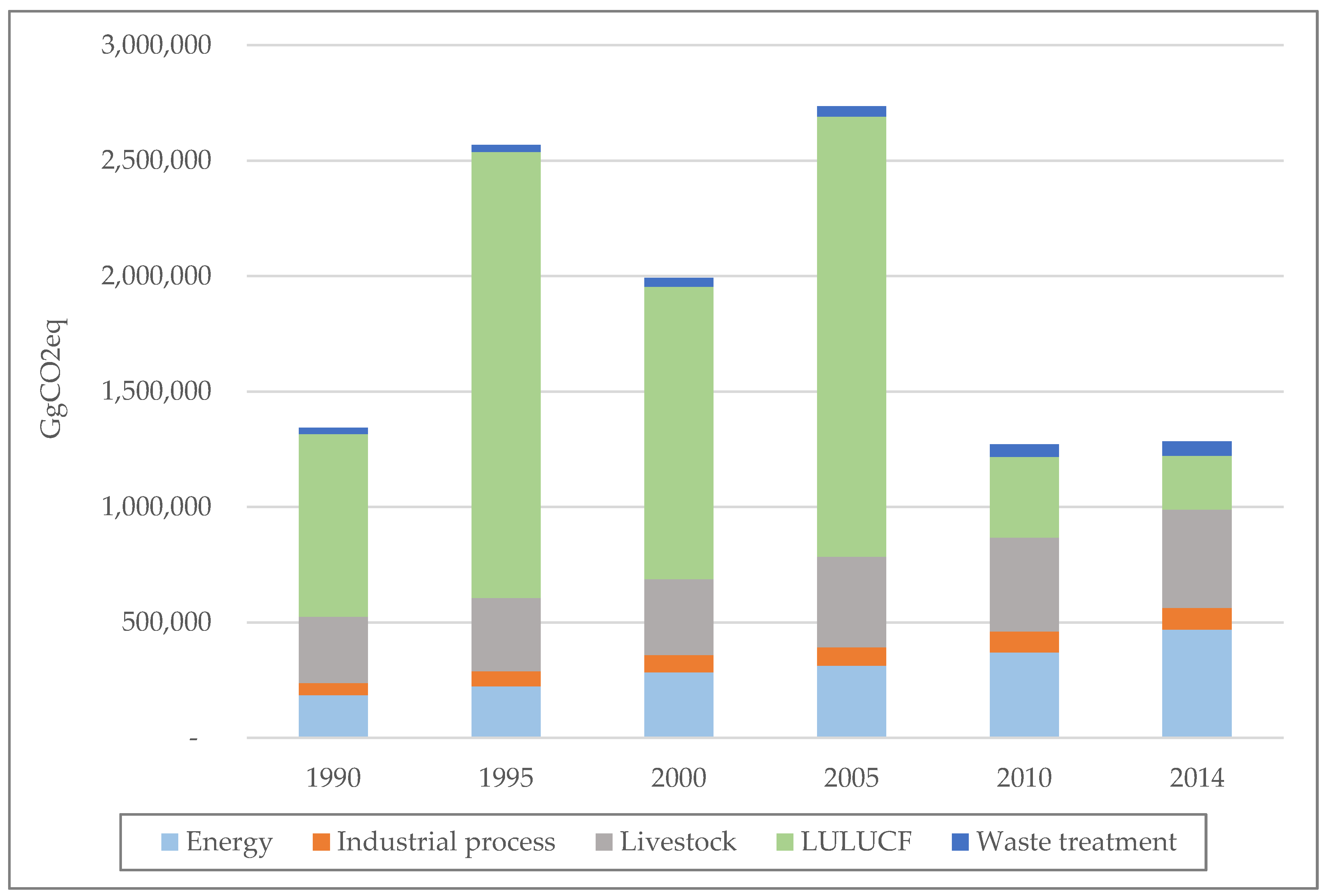

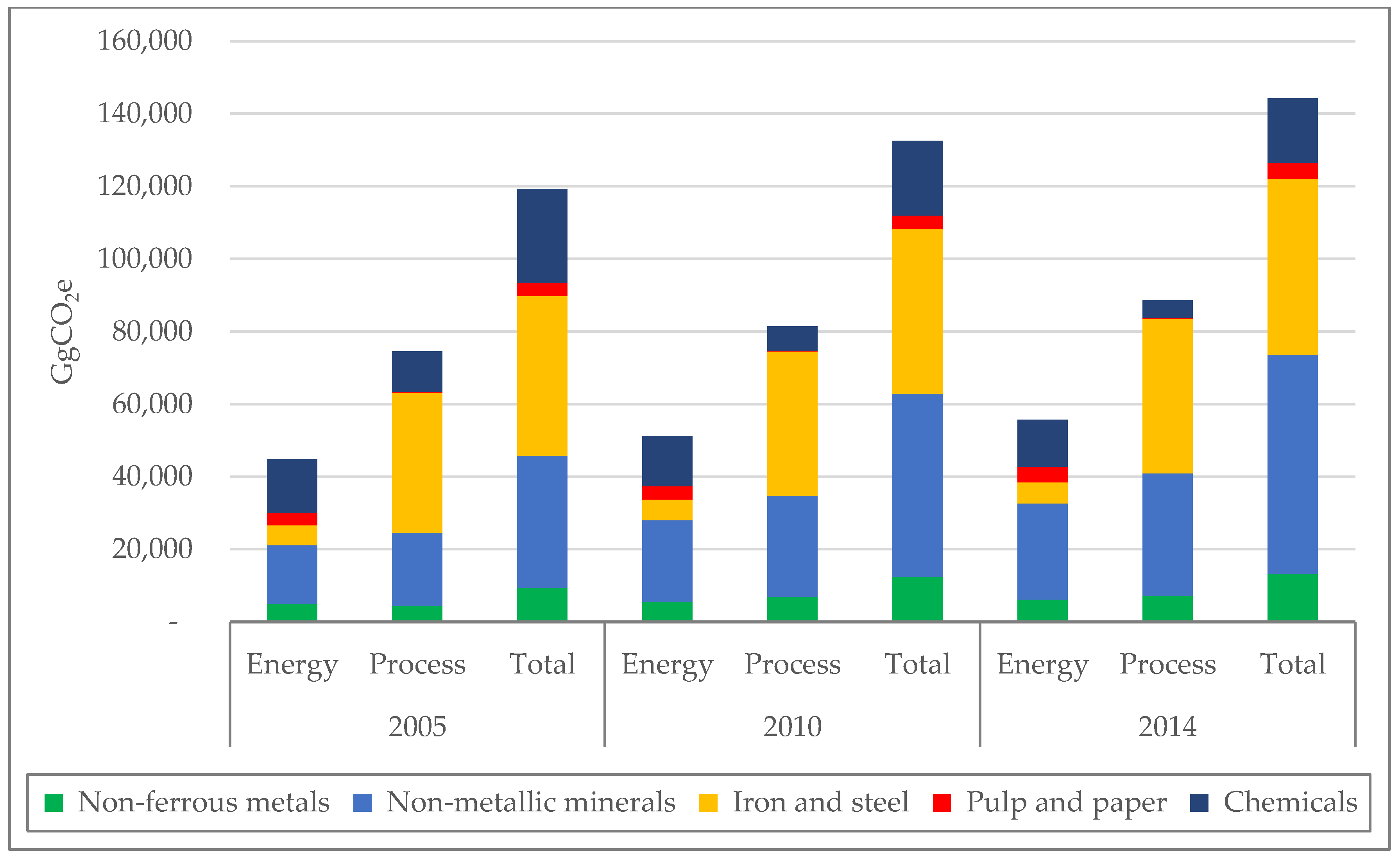

4.1. Characterization of the Brazilian Industry

4.1.1. Industry Emissions Profile

4.1.2. International Emissions Intensity Comparison

4.2. Impacts of Carbon Pricing on the Brazilian Industry

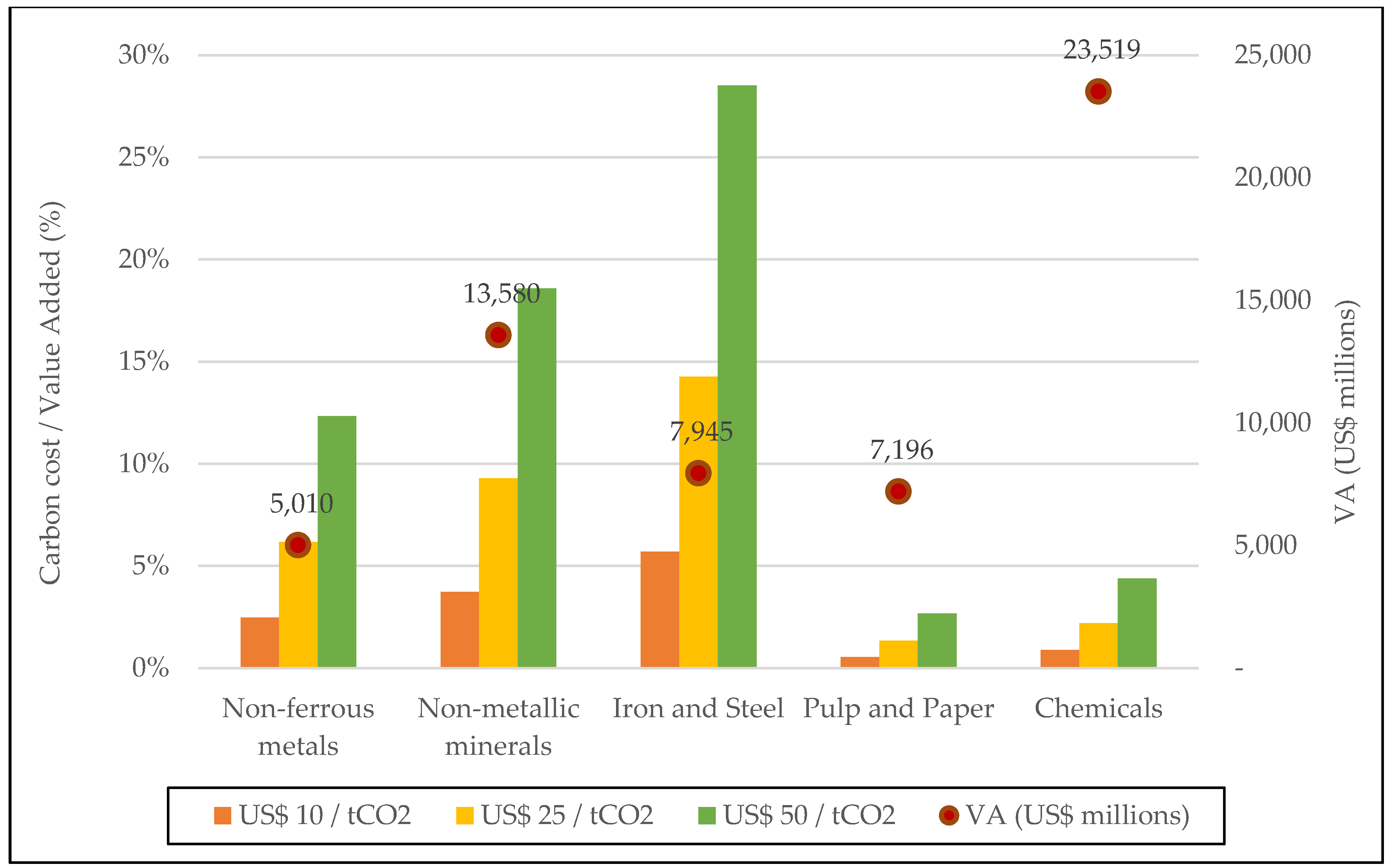

4.2.1. Sectorial Value Added (VA)

4.2.2. Emissions Intensity, International Trade Exposure, and Risk of Carbon Leakage

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Intergovernmental Panel on Climate Change (IPCC). Climate Change 2014: Synthesis Report; Contribution of Working Groups I, II and III to the Fifth Assessment Report of the IPCC; IPCC: Geneva, Switzerland, 2014; p. 151. [Google Scholar]

- Schütze, F.; Fürst, S.; Mielke, J.; Steudle, G.A.; Wolf, S.; Jaeger, C.C. The Role of Sustainable Investments in Climate Policy. Sustainability 2017, 9, 221. [Google Scholar] [CrossRef]

- Partnership for Market Readiness (PMR); International Carbon Action Partnership (ICAP). Emissions Trading in Practice: A Handbook on Design and Implementation; World Bank: Washington, DC, USA, 2016. [Google Scholar]

- Knight, E.R.W. The economic geography of European carbon market trading. J. Econ. Geogr. 2011, 11, 817–841. [Google Scholar] [CrossRef]

- High-Level Commission on Carbon Prices. Report of the High-Level Commission on Carbon Prices; World Bank: Washington, DC, USA, 2017; Available online: https://static1.squarespace.com/static/54ff9c5ce4b0a53decccfb4c/t/59244eed17bffc0ac256cf16/1495551740633/CarbonPricing_Final_May29.pdf (accessed on 2 April 2018).

- International Carbon Action Partnership (ICAP). Emissions Trading Worldwide: Status Report 2018; ICAP: Berlin, Germany, 2018; Available online: https://icapcarbonaction.com/en/?option=com_attach&task=download&id=547 (accessed on 15 April 2018).

- Perthuis, C.; Trotignon, R. Governance of CO2 markets: Lessons from the EU ETS. Energy Policy 2014, 75, 100–106. [Google Scholar] [CrossRef]

- Da Motta, R.S. A política nacional sobre mudança do clima: Aspectos regulatórios e de governança. In Mudança do Clima no Brasil: Aspectos Econômicos, Sociais e Regulatórios; da Motta, R.S., Hargrave, J., Luedemann, G., Sarmiento Gutierrez, M.B., Eds.; IPEA: Brasília, Brazil, 2011; Volume 1, ISBN 978-85-7811-108-3. [Google Scholar]

- Hasselknippe, H. Systems for carbon trading: An overview. Clim. Policy 2003, 3, 43–57. [Google Scholar] [CrossRef]

- World Bank; Ecofys; Vivid Economics. State and Trends of Carbon Pricing 2017; World Bank: Washington, DC, USA, 2017; ISBN (electronic) 978-1-4648-1218-7. [Google Scholar]

- Carbon Pricing Leadership Coalition (CPLC). What Are the Options for Using Carbon Pricing Revenues? Executive Briefing CPLC. 2016. Available online: http://pubdocs.worldbank.org/en/668851474296920877/CPLC-Use-of-Revenues-Executive-Brief-09-2016.pdf (accessed on 23 March 2018).

- Centro de Estudos em Sustentabilidade da Fundação Getúlio Vargas (GVces). Requerimento para um Sistema Nacional de Monitoramento, Relato e Verificação de Emissões de Gases de Efeito Estufa. Elementos para um Mercado de Carbono no Brasil; GVces-FGV/SP: São Paulo, Brazil, 2013; Available online: http://bibliotecadigital.fgv.br/dspace/bitstream/handle/10438/15351/Requerimentos%20para%20um%20Sistema%20Nacional%20de%20Monitoramento%2c%20Relato%20e%20Verifica%C3%A7%C3%A3o%20de%20Emiss%C3%B5es%20de%20Gases%20de%20Efeito%20Estufa%20-%20Vol.%201.pdf?sequence=1&isAllowed=y (accessed on 10 February 2018).

- Fankhauser, S.; Hepburn, C.; Park, J. Combining Multiple Climate Policy Instruments: How Not to Do It. Working Paper No. 48. 2011. Available online: http://www.lse.ac.uk/GranthamInstitute/wp-content/uploads/2014/02/WP38_UK-carbon-tax.pdf (accessed on 7 March 2018).

- Ministério da Ciência, Tecnologia e Inovação (MCTI). Cenários Integrados de Mitigação de Emissões de Gases de Efeito Estufa para o Brasil até 2050—Opções de Mitigação de Emissões de Gases de Efeito Estufa em Setores-Chave do Brasil; ONU Meio Ambiente: Brasília, Brazil, 2016. [Google Scholar]

- World Bank. Brazil Low-Carbon Country Study—Case Study; World Bank: Washington, DC, USA, 2010; Available online: http://siteresources.worldbank.org/BRAZILEXTN/Resources/Brazil_LowcarbonStudy.pdf (accessed on 12 January 2018).

- Conselho Empresarial Brasileiro para o Desenvolvimento Sustentável (CEBDS). Oportunidades e Desafio da NDC Brasileira para o Setor Empresarial—Setor Industrial; CEBDS: Rio de Janeiro, Brazil, 2017; Available online: http://biblioteca.cebds.org/oportunidades-desafios-metasndc (accessed on 25 March 2018).

- Precificação de Carbono: O Que o Setor Empresarial Precisa Saber para se Posicionar. 2016. Available online: http://biblioteca.cebds.org/precificacao-de-carbono (accessed on 3 April 2018).

- Pinto, R.G.D.; Szklo, A.S.; Rathmann, R. CO2 emissions mitigation strategy in the Brazilian iron and steel sector—From structural to intensity effects. Energy Policy 2018, 114, 380–393. [Google Scholar] [CrossRef]

- Henriques, M.F.; Dantas, F.; Schaeffer, R. Potential for reduction of CO2 emissions and a low-carbon scenario for the Brazilian industrial sector. Energy Policy 2010, 38, 1946–1961. [Google Scholar] [CrossRef]

- Alier, J.; Schulüpman, K. La Ecolología y la Economía; Fondo de Cultura Económica: México city, Mexico, 1998; ISBN 9789681636166. [Google Scholar]

- Perman, R.; Ma, Y.; McGilvray, J.; Common, M. Natural Resource and Environmental Economics, 3rd ed.; Longman: Harlow, UK, 1996; ISBN 0273655590. [Google Scholar]

- Pearce, D.; Turner, R. Economics of Natural Resources and the Environment; Johns Hopkins University Press: Baltimore, MD, USA, 1989; ISBN 9780745002026. [Google Scholar]

- Crampton, P.; MacKay, D.J.C.; Ockenfels, A.; Stoft, S. Global Carbon Pricing—The Path to Climate Collaboration; MIT Press: Cambridge, MA, USA, 2017; ISBN 9780262036269. [Google Scholar]

- Narassimahn, E.; Gallagher, K.S.; Koester, S.; Rivera Alejo, J. Carbon Pricing in Practice: A Review of the Evidence; Climate Policy Lab: Medford, MA, USA, 2017; Available online: https://sites.tufts.edu/cierp/files/2017/11/Carbon-Pricing-In-Practice-A-Review-of-the-Evidence.pdf (accessed on 13 April 2018).

- Rathmann, R. Impactos da Adoção de Metas de Redução de Emissão de Gases de Efeito Estufa Sobre a Competitividade de Setores Industriais Energo Intensivos do Brasil. Ph.D. Thesis, Energy Planning Program from the Federal University of Rio de Janeiro (COPPE/UFRJ), Rio de Janeiro, Brazil, 2012. [Google Scholar]

- Thomas, J.N.; Callan, S.J. Economia Ambiental: Fundamentos, Políticas e Aplicações; Cengage Learning: São Paulo, Brazil, 2010; ISBN 9788522109784. [Google Scholar]

- Shu, T.; Peng, Z.; Chen, S.; Wang, S.; Lai, K.K.; Yang, H. Government Subsidy for Remanufacturing or Carbon Tax Rebate: Which Is Better for Firms and a Low-Carbon Economy. Sustainability 2017, 9, 156. [Google Scholar] [CrossRef]

- Pollitt, H. The E3-razil Model. 2015. Available online: http://www.spe.fazenda.gov.br/noticias/seminario-politica-fiscal-verde/e3-brasil (accessed on 15 April 2018).

- IES-Brasil. Implicações Econômicas e Sociais de Cenários de Mitigação no Brasil—2030. 2015. Available online: http://www.centroclima.coppe.ufrj.br/images/Noticias/documentos/ies-brasil-2030/8_setor-industrial.pdf (accessed on 8 March 2018).

- Chen, Y.H.H.; Timilsina, G.R.; Landis, F. Economic implications of reducing carbon emissions from energy use and industrial processes in Brazil. J. Environ. Manag. 2013, 130, 436–446. [Google Scholar] [CrossRef] [PubMed]

- Wills, W. Modelagem dos Efeitos de Longo Prazo de Políticas de Mitigação de Emissão de Gases de Efeito Estufa na Economia do Brasil. Ph.D. Thesis, Energy Planning Program from the Federal University of Rio de Janeiro (COPPE/UFRJ), Rio de Janeiro, Brasil, 2013. [Google Scholar]

- Grottera, C. Impactos de Políticas de Redução de Emissão de Gases de Efeito Estufa sobre a Desigualdade de Renda no Brasil. Master’s Thesis, Energy Planning Program from the Federal University of Rio de Janeiro (COPPE/UFRJ), Rio de Janeiro, Brasil, 2013. [Google Scholar]

- Chen, W.; Zhou, J.-F.; Li, Y.-C. Effects of an Energy Tax (Carbon Tax) on Energy Saving and Emission Reduction in Guangdong Province-Based on a CGE Model. Sustainability 2017, 9, 681. [Google Scholar] [CrossRef]

- Magalhães, A.; Domingues, E.; Hewings, G. A Low Carbon Economy in Brazil: Policy Alternatives, Costs of Reducing Greenhouse Gas Emissions and Impacts on Households. Presented at the 18th Annual Conference on Global Economic Analysis, Melbourne, Australia, 17–19 June 2015. [Google Scholar]

- Instituto Escolhas. Impactos Sociais e Econômicos da Tributação de Carbono no Brasil. 2015. Available online: http://escolhas.org/wp-content/uploads/2016/09/impactos-economicos-e-sociais-da-tributacao-de-carbono-no-brasil.pdf (accessed on 14 March 2018).

- Wills, W.; Lefevre, J. The Impact of a Carbon Tax over the Brazilian Economy in 2030—Imaclim: The Hybrid CGE Model Approach. In Proceedings of the ISEE 2012 Conference—Ecological Economics and Rio +20: Challenges and Contributions for a Green Economy, Rio de Janeiro, Brasil, 16–19 June 2012. [Google Scholar]

- Yang, B.; Liu, C.; Su, Y.; Jing, X. The Allocation of Carbon Intensity Reduction Target by 2020 among Industrial Sectors in China. Sustainability 2017, 9, 148. [Google Scholar] [CrossRef]

- Ye, B.; Jiang, J.; Miao, L.; Li, J.; Peng, Y. Innovative Carbon Allowance Allocation Policy for the Shenzhen Emission Trading Scheme in China. Sustainability 2016, 8, 3. [Google Scholar] [CrossRef]

- Santos, L. Otimização do Valor de Produção no Brasil com Restrição de Emissão de Gases de Efeito Estufa a Partir de uma Análise Insumo-Produto. Master’s Thesis, Energy Planning Program from the Federal University of Rio de Janeiro (COPPE/UFRJ), Rio de Janeiro, Brazil, 2014. [Google Scholar]

- Gurgel, A.C.; Paltsev, S.; Reilly, J.; Metcalf, G. An analysis of US greenhouse gas cap-and-trade proposals using a forward-looking economic model. Environ. Dev. Econ. 2011, 16, 155–176. [Google Scholar] [CrossRef]

- Rathmann, R.; Júnior, M.F.H.; Szklo, A.S.; Schaeffer, R. Sistema Brasileiro de Cap-and-Trade no Setor Industrial: Vantagens, Desafios, Reflexos na Competitividade Internacional e Barreiras à Implementação; Policy Paper; Energy Planning Program from the Federal University of Rio de Janeiro (COPPE/UFRJ): Rio de Janeiro, Brazil, 2010. [Google Scholar]

- Keohane, N. Cap-and-trade rehabilitated: Using Tradable Permits to Control U.S. Greenhouse Gases. Rev. Environ. Econ. Policy 2009, 3, 42–62. [Google Scholar] [CrossRef]

- Choi, Y.; Lee, H.S. Are Emissions Trading Policies Sustainable? A Study of the Petrochemical Industry in Korea. Sustainability 2016, 8, 1110. [Google Scholar] [CrossRef]

- Laing, T.; Sato, M.; Grubb, M.; Comberti, C. The effects and side-effects of the EU emissions trading scheme. Wiley Interdiscip. Rev. Clim. Chang. 2014, 5, 509–519. [Google Scholar] [CrossRef] [Green Version]

- Castro, A.L.; Seroa da Motta, R. Mercado de Carbono no Brasil: Analisando efeitos de eficiência e distributivos. Rev. Parana. Desenvolv. 2013, 125, 57–78. [Google Scholar]

- Lise, W.; Sijm, J.; Hobbs, B.F. The Impact of the EU ETS on Prices, Profits and Emissions in the Power Sector: Simulation Results with the COMPETES EU20 Model. Environ. Resour. Econ. 2010, 47, 23–44. [Google Scholar] [CrossRef]

- Paltsev, S.; Reilly, J.M.; Jacoby, H.D.; Gurgel, A.C.; Metcalf, G.E.; Sokolov, A.P.; Holak, J.F. Assessment of US GHG cap-and-trade proposals. Clim. Policy 2008, 8, 395–420. [Google Scholar] [CrossRef]

- Stavins, R.N. A Meaningful U.S. Cap-and-Trade System to Address Climate Change. Harv. Environ. Law Rev. 2008, 32, 293–371. [Google Scholar] [CrossRef]

- Lei no. 12.187, de 29 Dezembro de 2009—Institui a Política Nacional Sobre Mudança do Clima (PNMC) e dá Outras Providências. 2009. Available online: http://www.planalto.gov.br/ccivil_03/_ato2007-2010/2009/lei/l12187.htm (accessed on 9 March 2018).

- Fundamentos para a Elaboração da Pretendida Contribuição Nacionalmente Determinada (iNDC) do Brasil no Contexto do Acordo de Paris sob a UNFCCC. 2015. Available online: http://www.mma.gov.br/images/arquivos/clima/convencao/indc/Bases_elaboracao_iNDC.pdf (accessed on 16 February 2018).

- Pretendida Contribuição Nacionalmente Determinada para Consecução do Objetivo da Convenção-Quadro das Nações Unidas sobre Mudança do Clima. 2015. Available online: http://www.mma.gov.br/images/arquivos/clima/convencao/indc/BRAZIL_iNDC_english.pdf (accessed on 16 February 2018).

- Pereira, C.; Bertholini, F. Beliefs or ideology: The imperative of social inclusion in Brazilian politics. Commonw. Comp. Politics 2017, 55, 377–401. [Google Scholar] [CrossRef]

- Decreto nº 7.390, de 9 de Dezembro de 2010—Regulamenta os Arts. 6o, 11 e 12 da Lei no 12.187, de 29 de Dezembro de 2009, Que Institui a Política Nacional sobre Mudança do Clima—PNMC, e dá Outras Providências. 2010. Available online: http://www.planalto.gov.br/ccivil_03/_ato2007-2010/2010/decreto/d7390.htm (accessed on 18 March 2018).

- Ministry of Finance (MF). Market Readiness Proposal under the Partnership for Market Readiness Program. 2014. Available online: https://www.thepmr.org/system/files/documents/Final%20MRP%20Brazil_29-08-2014.pdf (accessed on 1 April 2018).

- Confederação Nacional da Indústria (CNI). Projeto Sudeste Competitivo. 2015. Available online: http://arquivos.portaldaindustria.com.br/app/conteudo_18/2015/10/26/9977/ProjetoSudesteCompetitivo-SumrioExecutivo.pdf (accessed on 22 March 2018).

- Ministério da Ciência, Tecnologia e Inovação (MCTI). Terceiro Inventário Brasileiro de Emissões e Remoções Antrópicas de Gases de Efeito Estufa; MCTI: Brasília, Brazil, 2015. [Google Scholar]

- Ministério do Desenvolvimento, Indústria e Comércio (MDIC). Plano Setorial de Mitigação da Mudança Climática para a Consolidação de uma Economia de Baixa Emissão de Carbono na Indústria de Transformação—Plano Indústria. 2013. Available online: http://www.mma.gov.br/images/arquivo/80076/Industria.pdf (accessed on 15 April 2018).

- Rochedo, P.R.R.; Soares-Filho, B.; Schaeffer, R.; Viola, E.; Szklo, A.; Lucena, A.F.P.; Koberle, A.; Davis, J.L.; Rajão, R.; Rathmann, R. The threat of political bargaining to climate mitigation in Brazil. Nat. Clim. Chang. 2018, in press. [Google Scholar] [CrossRef]

- Vidal, A.C.F.; Hora, A.B. A Indústria de Papel e Celulose. BNDES Biblioteca Digital. 2012. Available online: https://www.bndes.gov.br/SiteBNDES/export/sites/default/bndes_pt/Galerias/Arquivos/conhecimento/livro60anos_perspectivas_setoriais/Setorial60anos_VOL1PapelECelulose.pdf (accessed on 15 March 2018).

- Associação Brasileira de Metalurgia, Materiais e Mineração (ABM). Panorama dos Metais Não-Ferrosos no Brasil e no Mundo. 2009. Available online: https://www.yumpu.com/pt/document/view/28541761/panorama-de-metais-nao-ferrosos-no-brasil-abm/3 (accessed on 17 March 2018).

- Ministério de Minas e Energia (MME). Anuário Estatístico do Setor de Transformação de Não-Metálicos. 2017. Available online: http://www.mme.gov.br/documents/1138775/1732813/ANU%C3%81RIO+N%C3%83O-METALICOS+2017+27.03.2018.pdf/d20dce50-bfe8-4718-8924-129038887835 (accessed on 19 March 2018).

- Centro de Gestão e Estudos Estratégicos (CGEE/MDIC). Levantamento dos Níveis de Produção de Aço e Ferro-Gusa, Cenário em 2020. Nota Técnica, Subsídios 2014 ao Plano Siderurgia do MDIC: Modernização da Produção de Carvão Vegetal. 2014. Available online: http://livrozilla.com/doc/1444319/levantamento-dos-n%C3%ADveis-de-produ%C3%A7%C3%A3o-de-a%C3%A7o-e-ferro-gusa (accessed on 19 March 2018).

- Bastos, V.D.; Costa, L.M. Déficit Comercial, Exportações e Perspectivas da Indústria Química Brasileira. 2011; pp. 163–206. Available online: https://web.bndes.gov.br/bib/jspui/bitstream/1408/2524/1/A%20BS%2033%20D%C3%A9ficit%20comercial%2c%20exporta%C3%A7%C3%B5es%20e%20perspectivas%20da%20ind%C3%BAstria%20qu%C3%ADmica%20brasileira_P.pdf (accessed on 19 March 2018).

- Carbo, M.C. Global Technology Roadmap for CCS in Industry: Biomass-Based Industrial CO2 Sources: Biofuels Production with CCS. 2011. Available online: https://www.ecn.nl/publications/PdfFetch.aspx?nr=ECN-E--11-012 (accessed on 28 March 2018).

- Heede, R. Tracing anthropogenic carbon dioxide and methane emissions to fossil fuel and cement producers, 1854–2010. Clim. Chang. 2014, 122, 229–241. [Google Scholar] [CrossRef]

- International Energy Agency (IEA). Greenhouse Gases from Major Industrial Sources—IV. The Aluminium Industry. Report PH3/23. 2000. Available online: http://www.ieaghg.org/docs/General_Docs/Reports/Aluminium%20industry.pdf (accessed on 10 March 2018).

- Greenhouse Gases from Major Industrial Sources—III. Iron and Steel Production. Report PH3/30. 2000. Available online: http://ieaghg.org/docs/General_Docs/Reports/PH3-30%20iron-steel.pdf (accessed on 11 March 2018).

- MCTI. Terceira Comunicação Nacional do Brasil à Convenção-Quadro das Nações Unidas—Volume II; MCTI: Brasília, Brasil, 2016. [Google Scholar]

- Instituto Brasileiro de Geografia e Estatística (IBGE). Matriz Insumo-Produto: Brasil 2010; Instituto Brasileiro de Geografia e Estatística: Brasília, Brasil, 2015. Available online: https://biblioteca.ibge.gov.br/pt/biblioteca-catalogo?view=detalhes&id=298180 (accessed on 4 March 2018).

- California Air Resources Board (CARB). Public Workshop Cap-and-Trade Program: Emissions Leakage Research and Monitoring. 2012. Available online: https://www.arb.ca.gov/cc/capandtrade/meetings/073012/emissionsleakage.pdf (accessed on 14 March 2018).

- Intergovernmental Panel on Climate Change (IPCC). Climate Change 2007: Working Group III: Mitigation of Climate Change; Executive Summary. 2007. Available online: http://www.ipcc.ch/publications_and_data/ar4/wg3/en/ch11s11-es.html (accessed on 1 April 2018).

- Organization for Economic Co-operation and Development (OECD). Effective Carbon Rates on Energy. 2016. Available online: http://www.oecd.org/tax/tax-policy/effective-carbon-rates-on-energy.htm (accessed on 15 April 2018).

- Nordhaus, W. Critical assumptions in the stern review on climate change. Science 2007, 317, 201–202. [Google Scholar] [CrossRef] [PubMed]

- Stern, N. The Economics of Climate Change: The Stern Review; Cambridge University Press: Cambridge, UK, 2007; Available online: https://journals.openedition.org/sapiens/240 (accessed on 3 April 2018).

- Clarke, L.K.; Jiang, K.; Akimoto, M.; Babiker, G.; Blanford, K.; Fisher-Vanden, J.-C.; Hourcade, V.; Krey, E.; Kriegler, A.; Löschel, D.; et al. Assessing Transformation Pathways. In Climate Change 2014: Mitigation of Climate Change; Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Edenhofer, O., Pichs-Madruga, R., Sokona, Y., Farahani, E., Kadner, S., Seyboth, K., Adler, A., Baum, I., Brunner, S., Eickmeier, P., et al., Eds.; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2014. [Google Scholar]

- Aldy, J.E. Long-Term Climate Policy: The Great Carbon Swap. 2016. Available online: http://www.progressivepolicy.org/wp-content/uploads/2016/11/The-Great-Swap-1.pdf (accessed on 14 April 2018).

- Instituto de Energia e Meio Ambiente (IEMA). Emissões de GEE do Setor de Energia, Processos Industriais e Uso de Produtos; Instituto de Energia e Meio Ambiente: São Paulo, Brasil, 2016; Available online: http://seeg.eco.br/wp-content/uploads/2016/09/FINAL-16-09-23-RelatoriosSEEG-PIUP_pdf (accessed on 15 April 2018).

- Empresa de Pesquisa Energética (EPE). O Compromisso do Brasil no Combate às Mudanças Climáticas: Produção e Uso de Energia; MME: Rio de Janeiro, Brasil, 2016. [Google Scholar]

- Barros, G.; Guilhoto, J.J.M. The Regional Economic Structure of Brazil in 1959: An Overview Based on an Interstate Input-Output Matrix. Rev. Bras. Econ. 2014, 68, 317–335. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Risk of Carbon Leakage | Emissions Intensity | Trade Exposure |

|---|---|---|

| High | High | High |

| Medium | ||

| Low | ||

| Medium | High | |

| Medium | Medium | Medium |

| Low | ||

| Low | High | |

| Medium | ||

| Low | Low | Low |

| Sector | Global Average | Brazilian Average |

|---|---|---|

| Non-ferrous metals | 9.1–9.6 | 5.6 |

| Non-metallic minerals | 0.6–0.8 | 0.7 |

| Iron and steel | 1.6–2.2 | 1.3 |

| Pulp and paper | 0.8–0.9 | 0.2 |

| Chemicals | n.a. | 0.3 |

| Sector | Carbon Price (US$/tCO2) | % Reduction in Sectorial Emissions | |||||

|---|---|---|---|---|---|---|---|

| 0% | 5% | 15% | 25% | 35% | 45% | ||

| Non-ferrous metals | 10 | 2.5% | 2.3% | 2.1% | 1.9% | 1.6% | 1.4% |

| 25 | 6.2% | 5.9% | 5.2% | 4.6% | 4.0% | 3.4% | |

| 50 | 12.3% | 11.7% | 10.5% | 9.3% | 8.0% | 6.8% | |

| Non-metallic minerals | 10 | 3.7% | 3.5% | 3.2% | 2.8% | 2.4% | 2.0% |

| 25 | 9.3% | 8.8% | 7.9% | 7.0% | 6.0% | 5.1% | |

| 50 | 18.6% | 17.7% | 15.8% | 13.9% | 12.1% | 10.2% | |

| Iron and steel | 10 | 5.7% | 5.4% | 4.8% | 4.3% | 3.7% | 3.1% |

| 25 | 14.3% | 13.5% | 12.1% | 10.7% | 9.3% | 7.8% | |

| 50 | 28.5% | 27.1% | 24.2% | 21.4% | 18.5% | 15.7% | |

| Pulp and paper | 10 | 0.5% | 0.5% | 0.5% | 0.4% | 0.3% | 0.3% |

| 25 | 1.3% | 1.3% | 1.1% | 1.0% | 0.9% | 0.7% | |

| 50 | 2.7% | 2.5% | 2.3% | 2.0% | 1.7% | 1.5% | |

| Chemicals | 10 | 0.9% | 0.8% | 0.7% | 0.7% | 0.6% | 0.5% |

| 25 | 2.2% | 2.1% | 1.9% | 1.6% | 1.4% | 1.2% | |

| 50 | 4.4% | 4.2% | 3.7% | 3.3% | 2.8% | 2.4% | |

+impact.

+impact.| Sectors | Emissions (tCO2) (A) | Sectorial VA (US$ Millions) (B) | Emissions/VA (tCO2/US$ Millions) (C) = (A) (B) | Emissions Intensity Classification <1000 (Low) 1000–2499 (Medium) >2500 (High) |

|---|---|---|---|---|

| Non-ferrous metals | 6,250,000 | 3411 | 1832 | Medium |

| Non-metallic minerals | 45,190,000 | 13,580 | 3328 | High |

| Iron and steel | 43,900,000 | 7945 | 5525 | High |

| Pulp and paper | 3,080,000 | 7196 | 428 | Low |

| Chemicals | 16,830,000 | 23,519 | 716 | Low |

| Sectors | Export Share (%X = Xi/(Xi + Mi)) | Trade Share (Si = Xi + Mi/Yi) | Trade Exposure Classification <10% (Low) 10–24.9% (Medium) >25% (High) |

|---|---|---|---|

| Non-ferrous metals | 60% | 52% | High |

| Non-metallic minerals | 51% | 11% | Medium |

| Iron and steel | 60% | 31% | High |

| Pulp and paper | 76% | 28% | High |

| Chemicals | 14–32% | 28–56% | High |

| Sectors | Emissions Intensity | International Trade Exposure | Risk of Carbon Leakage |

|---|---|---|---|

| Non-ferrous metals | Medium | High | High |

| Non-metallic minerals | High | Medium | High |

| Iron and steel | High | High | High |

| Pulp and paper | Low | High | Medium |

| Chemicals | Low | High | Medium |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Santos, L.; Garaffa, R.; Lucena, A.F.P.; Szklo, A. Impacts of Carbon Pricing on Brazilian Industry: Domestic Vulnerability and International Trade Exposure. Sustainability 2018, 10, 2390. https://doi.org/10.3390/su10072390

Santos L, Garaffa R, Lucena AFP, Szklo A. Impacts of Carbon Pricing on Brazilian Industry: Domestic Vulnerability and International Trade Exposure. Sustainability. 2018; 10(7):2390. https://doi.org/10.3390/su10072390

Chicago/Turabian StyleSantos, Luan, Rafael Garaffa, André F. P. Lucena, and Alexandre Szklo. 2018. "Impacts of Carbon Pricing on Brazilian Industry: Domestic Vulnerability and International Trade Exposure" Sustainability 10, no. 7: 2390. https://doi.org/10.3390/su10072390

APA StyleSantos, L., Garaffa, R., Lucena, A. F. P., & Szklo, A. (2018). Impacts of Carbon Pricing on Brazilian Industry: Domestic Vulnerability and International Trade Exposure. Sustainability, 10(7), 2390. https://doi.org/10.3390/su10072390