1. Introduction

Due to the recent economic problem of polarization linked to the unequal distribution of wealth for small-medium enterprises (SMEs) and self-employers, the importance of small-loan finance supported by the government has emerged as a major issue [

1,

2]. However, research demonstrates that small-loan finance is potentially very complex, particularly when financial support is provided by public funds [

2]. In particular, research shows that public guarantee loans are important for access to capital for self-employers and SMEs due to the positive impacts on their long-term sustainability [

3,

4]. While such research focuses on the SME and self-employer categories, how to predict the relationship between small businesses and loan repayment for managing public funds over time remains unclear.

The comparison between self-employers and SMEs demonstrates the need for a better understanding of credit ratings when financial institutions inject public loans. It is believed that such loans depend on credit rationing by lenders [

5], but the guarantee of financial support for small business management is still limited due to higher levels of insolvent enterprises than those of self-employers [

6]. The risk management theory also demonstrates that personal information is augmented with basic business-specific data to predict repayment [

7], but credit ratings for small business management will alter small-business lenders’ prospects regarding the possibility of repayment [

8], suggesting that survival rates are important to obtain more robust results. We expect that the potential of repayment may be dependent on guarantee ratios because it is closely related to a small business’s long-term survival, resulting in the optimal balance between the two parties.

Another important approach is to identify why the survival rates may differ between financial institutions if guarantee ratios are critical. It is necessary to determine the influence of these institutions at the level of guarantee ratios to reduce the probability of loan defaults [

9]. There is a considerable amount of literature on certain financial organizations that are more willing than commercial banks to lend to riskier borrowers [

10,

11,

12,

13,

14,

15]. What difference is played by the types of loan providers in the guarantee ratio incurred by the potential of borrowers?

In line with these observations, a complete understanding of the balance between the two parties is essential for researchers and practitioners alike. It enables researchers to establish a theoretical approach to managing public funds while helping practitioners ensure the optimal balance for preventing the exhaustion of public funds from a long-term perspective. In so doing, this study tests the survival trends and survival characteristics between the two parties in two important ways. First, we test the difference between public fund borrowers and providers from perspectives on their long-term survival. Second, we compare the characteristics of guarantee accidents by testing two groups (i.e., 499,554 observations). Our approach is important because there have been no previous studies in this line of research.

This study also provides useful insights for public policy planners. They need new solutions from public fund borrowers and providers. Because public financial support was originally designed and offered by public administrations, which allocate budgets to identifiable missions and programs [

16], capturing the limitations of public financial funds plays a critical role in redesigning and re-operating public financial programs.

2. Literature Review

Public guaranteed loans are widely used to support self-employers and SMEs, especially after the global financial crisis [

17,

18]. These loans mainly focus on supporting small business growth and sustainability, and the literature has well documented the positive relationship between entrepreneurship and business sustainability [

19,

20]. However, public guaranteed loans can have negative effects on the quality of small businesses [

18] such as insolvent enterprise, default, and other relevant issues. Hence, the impact of public guaranteed small loans would depend on the credit rating because banks are likely to reduce accident events [

20].

The theoretical approach is that in equilibrium, loan markets may be characterized by credit rating as financial institutions making loans consider the interest rate and the riskiness of a loan due to adverse selection or moral hazard [

21,

22]. A fundamental element of the credit market suggested by Bester [

21], especially given the focus of this study is on public loan guarantees, is that the interest rate and credit rating are critical when financial institutions evaluate small firms. For example, loan interest rates and credit ratings are viewed as a pair and are assumed to be negatively correlated because a higher credit rating should reduce the interest rate and accident rate.

Public guaranteed loan programs encourage banks to lend to self-employers and SMEs that are difficult to get financial loans through conventional methods (i.e., collateral). For example, there are two critical barriers: (1) they lack sufficient collateral, and (2) credit constraint continues to be one of the most significant huddles to self-employers and SMEs [

23]. In particular, this study focuses on the credit rating of each small business because most public small businesses suffer to provider their collateral at least in the context of Korean SMEs. As a consequence, public guaranteed small business loans could be managed by credit ratings because most defaults may be varied by the level of credit ratings. Thus, when banks implement credit rating models, they carefully screen small businesses’ eligibility for reducing the adverse selection effect [

24]. We expect that banks can manage more self-employers and SMEs motivated by opportunities in the market.

In particular, the creation of Mutual Guarantee Institutions (MGIs: private guarantee institutions created by beneficiary SMEs) is valuable for policy makers who focus on solutions that help reduce the financial constraint on self-employers and SMEs [

25]. MDIs have provided additional guarantees for public loans and, in turn, have contributed to the development of the sustainability of SMEs in European countries [

26]. Especially, MGIs are very active in Spain, France or Germany. In these countries, banks could reduce both the probability of default and the loss given default due to the overcome of the information asymmetries between financial institutions and borrowers. In this sense, MGIs are closely linked to our approach.

Both public guarantee loans and MGIs aim to promote access to credit for self-employers and SMEs [

27]. In so doing, banks consider similar strategies to support government programs for self-employers and SMEs lending, ahead of directed credit and interest rates [

28,

29]. As such, it is possible to capture the increase in the flow of funds towards self-employers and SMEs that face credit constraints, measured in terms of higher employment, investment, and sustainable performance [

30,

31,

32,

33].

4. Results

4.1. t-Test

We conducted a t-test to compare the two groups (self-employers vs. SMEs) using SPSS 23. The results of the t-test showed that the difference between the two groups was statistically significant at

p < 0.001 (see

Table 2), indicating that these groups were quite different.

4.2. Overall Review of Survival Analysis

To test the identity of the survival distribution, we conducted the log-rank, Breslow, and Tarone-Ware tests using Kaplan-Meier method. The test statistic was significant at p < 0.05, indicating that the survival time distributions of the two groups were different. The results for self-employers are provided first below, and then, the results for SMEs are provided. Finally, we discuss similarities and differences from the results of the two groups.

4.3. Result 1: Self-Employers

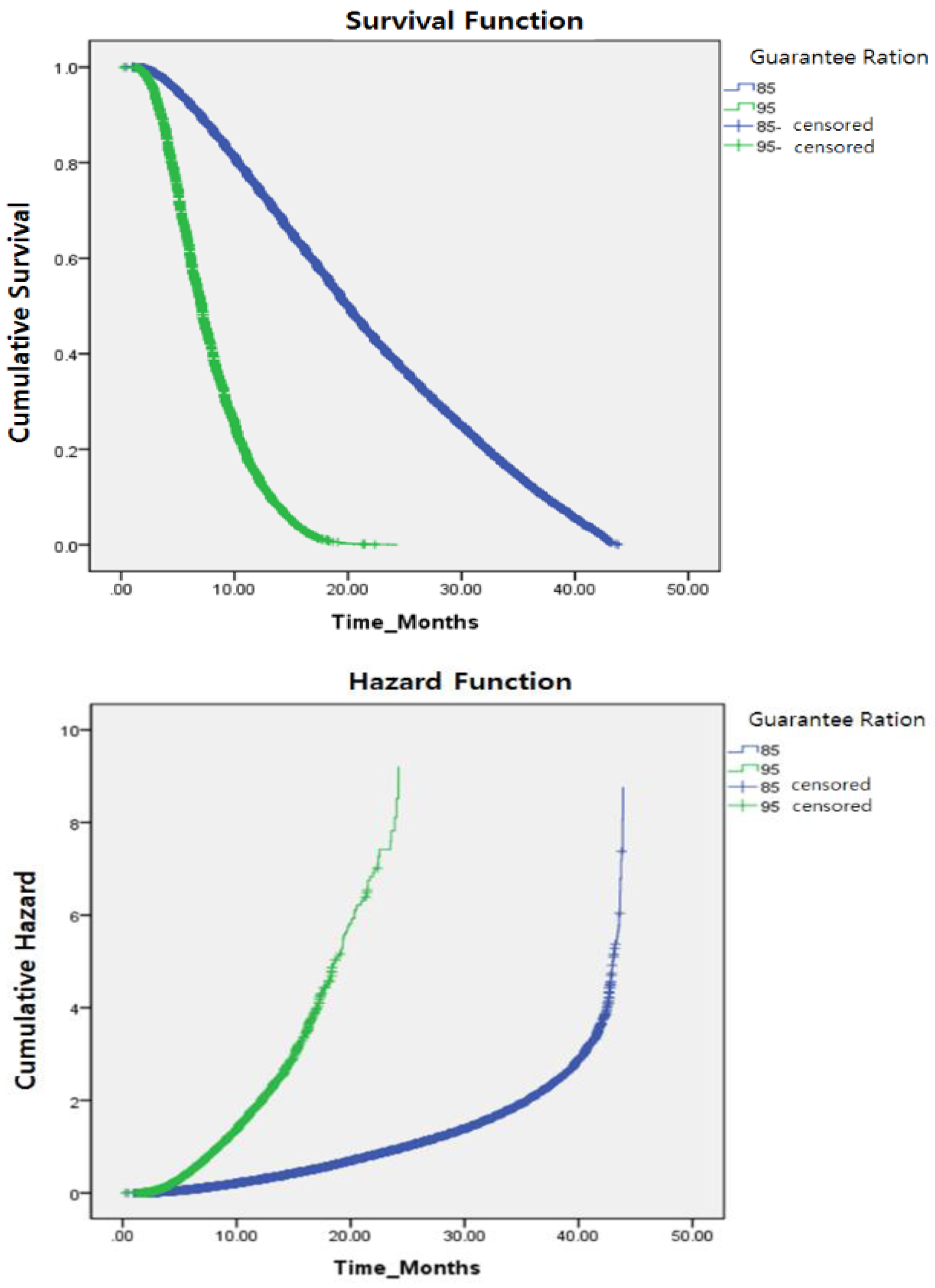

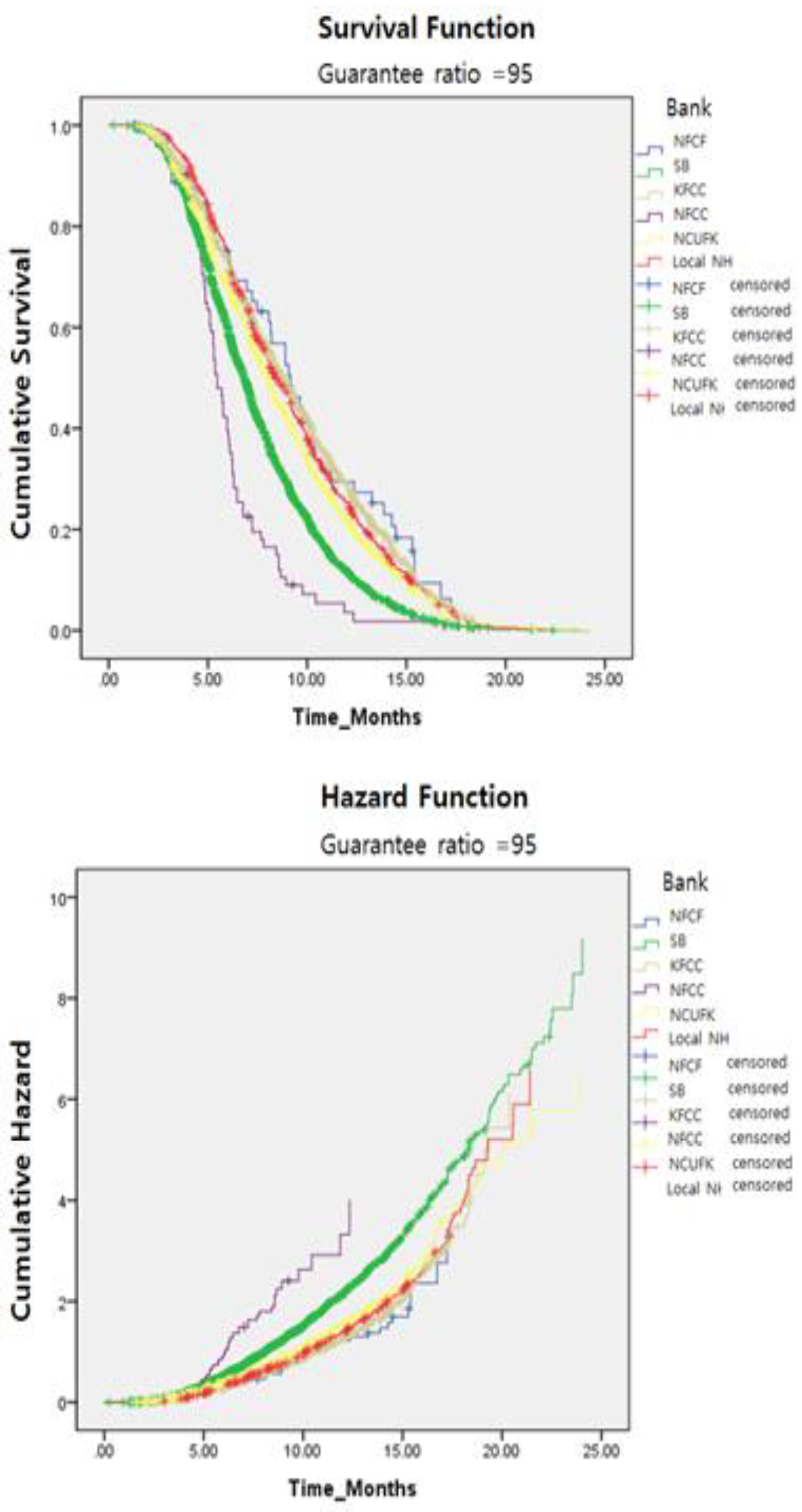

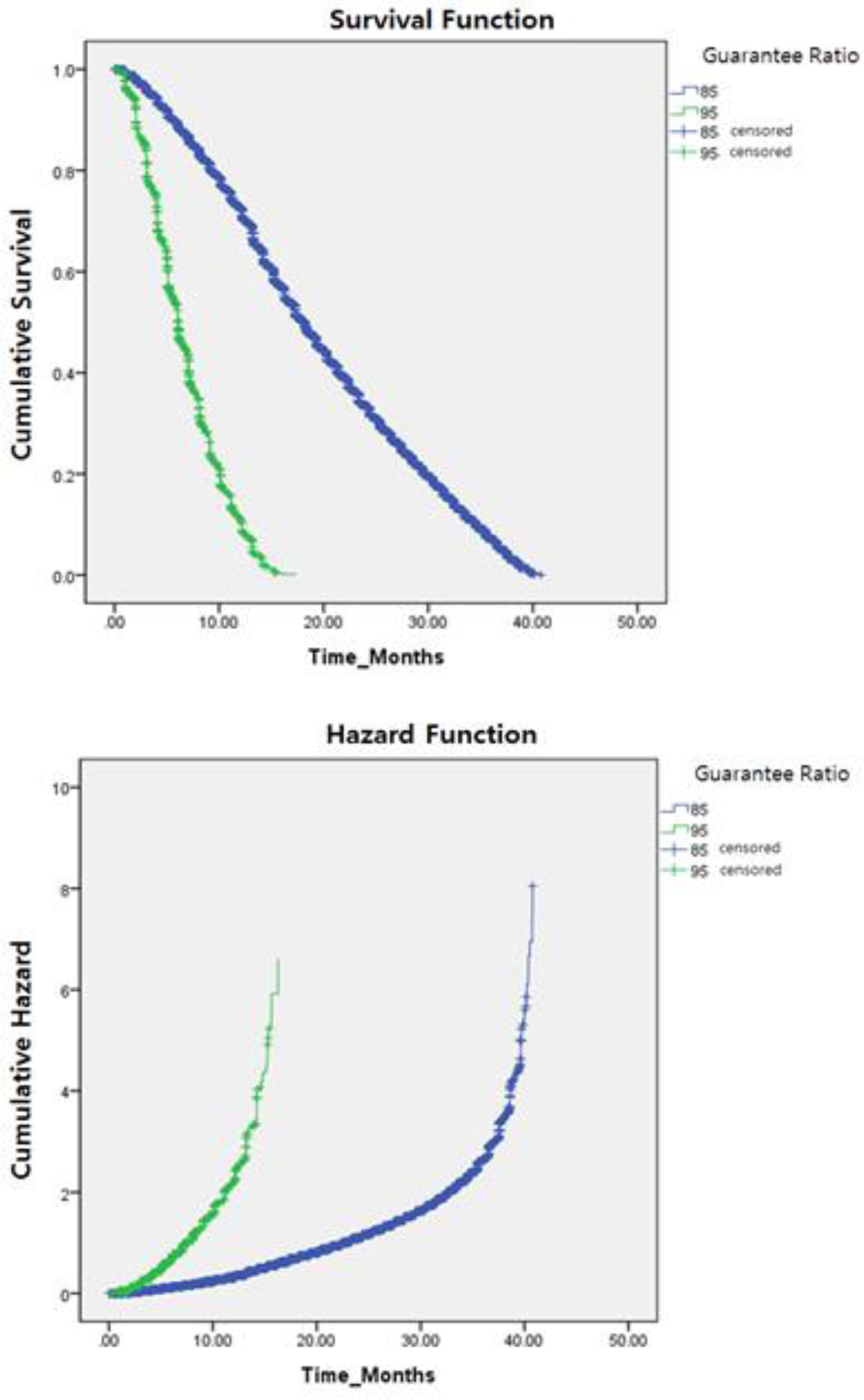

Two types (85% and 95%) of guarantee ratio were identified by the estimated values of the mean survival periods. As shown in

Table 3 and

Figure 1, the mean survival period for the 85% guarantee ratio was 20.033 months, whereas that for the 95% guarantee ratio was 7.1 months. Consequently, the 85% guarantee ratio survived much longer (12.867 months) than the 95% guarantee ratio.

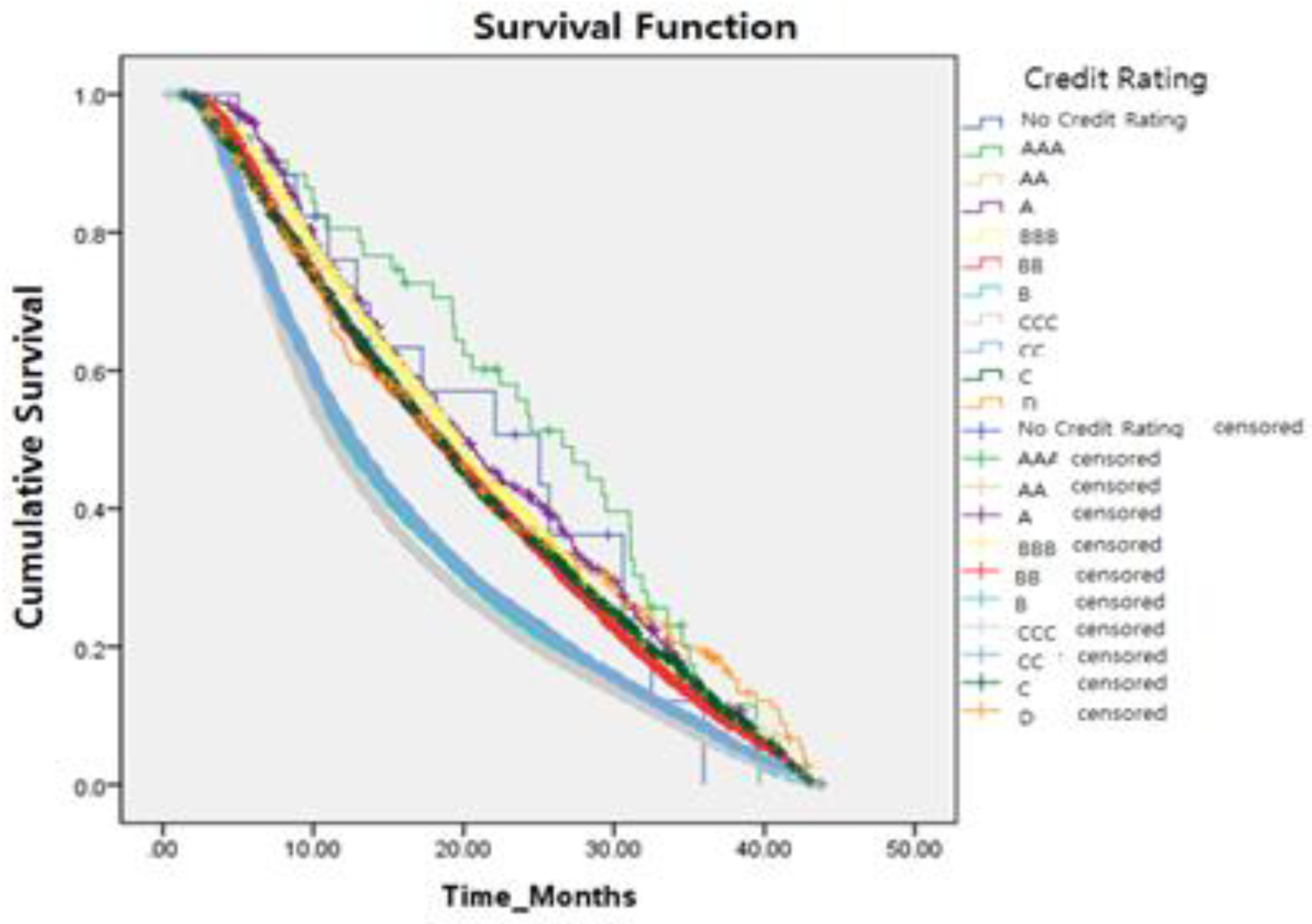

As shown in

Table 4 and

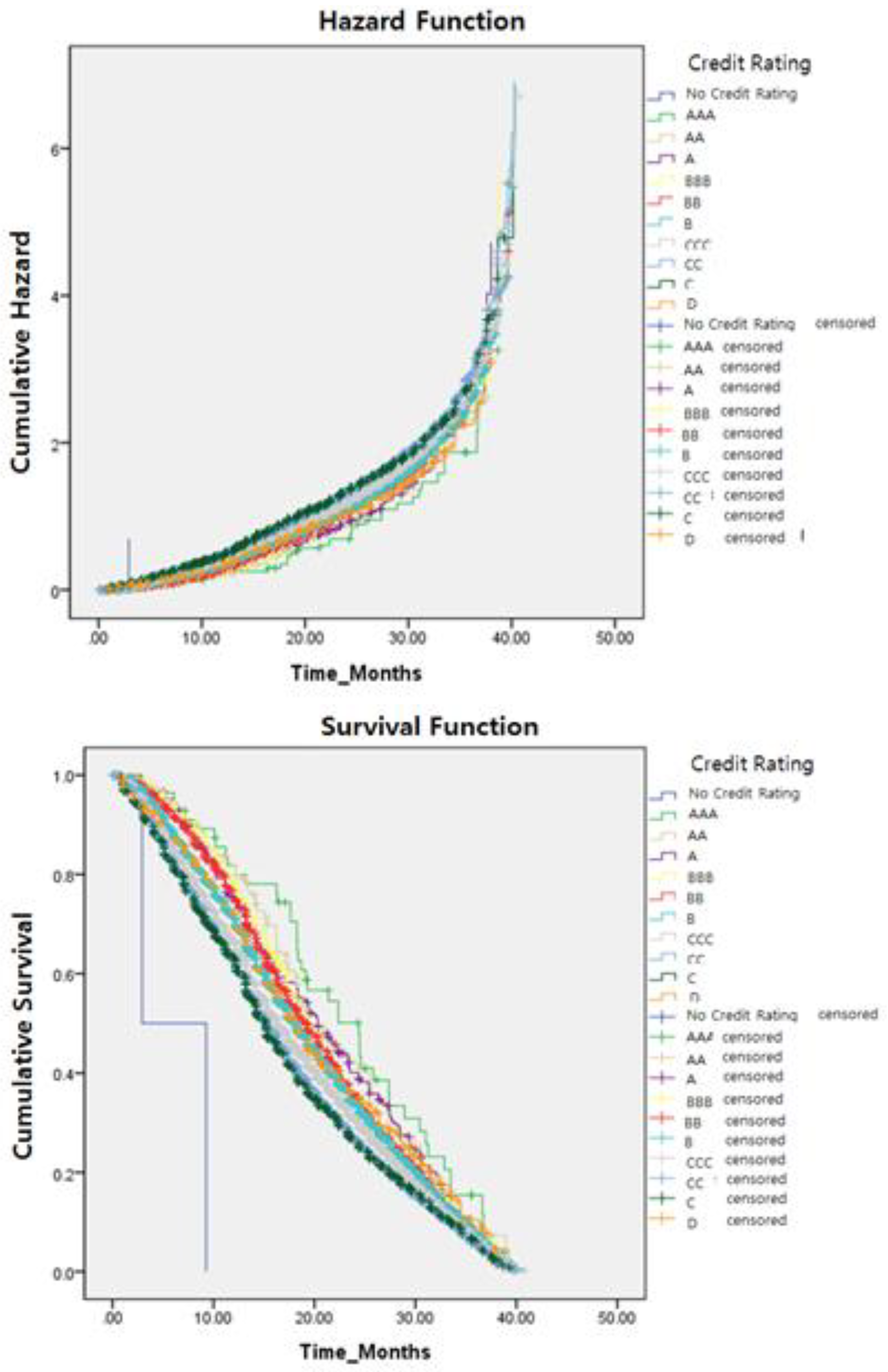

Figure 2, we estimated the mean survival period values for the credit ratings of self-employers using Kaplan–Meier method. The mean survival periods of the first to tenth credit ratings were 26.567, 19.367, 20.033, 19.433, 18.333, 12.200, 11.200, 12.600, 18.400, and 18.333 months, respectively. These results show that the mean survival periods of three credit ratings (sixth to eighth) were much shorter than those of the other credit ratings. These results are consistent with those of Kang’s study [

6], which addressed the relationship between accident rates and the subrogation ratio for self-employers with these credit ratings.

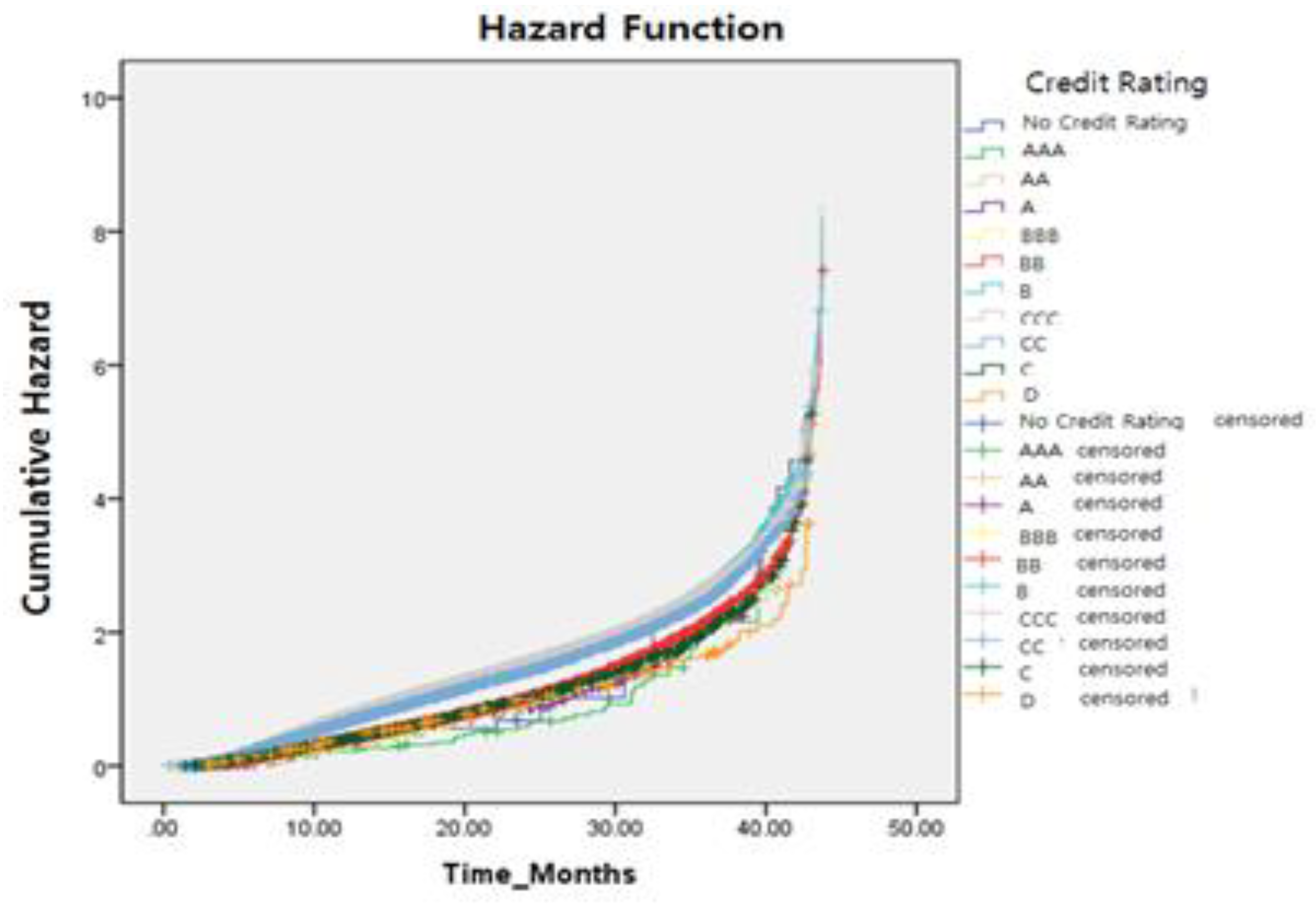

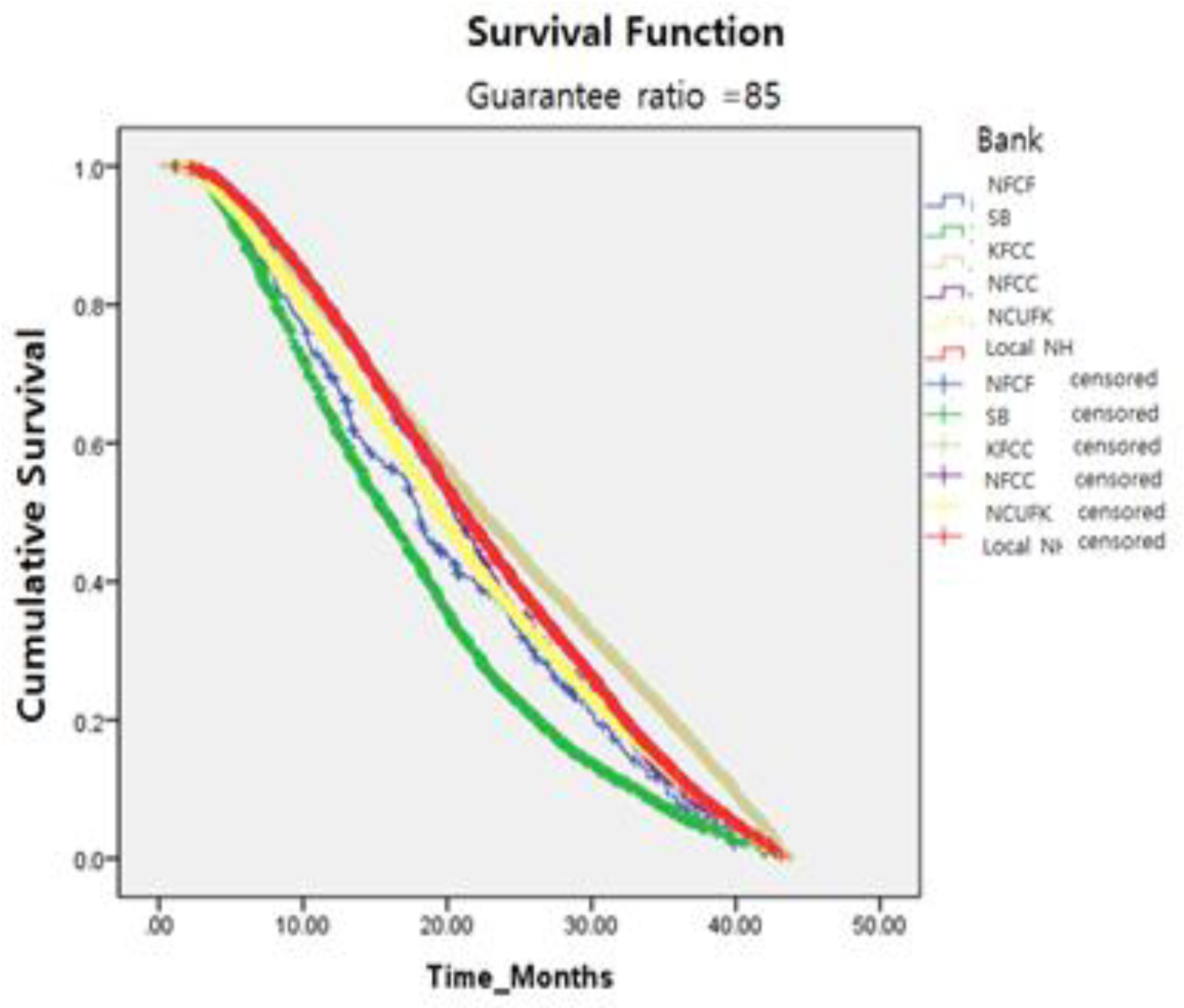

This study estimated mean survival period values based on financial banking institutions (see

Table 5 and

Figure 3). The estimated values were different across institutions. Specifically, those of NFCF, SB, KFCCC, NFFC, NCUFK, and Local NH were 16.433, 7.9, 19.3, 19.033, 16.533, and 20.067 months, respectively. Interestingly, the mean survival periods of SB were much shorter than those of other institutions. This is probably related to interest rates because the interest rates of SB were very high compared with the others.

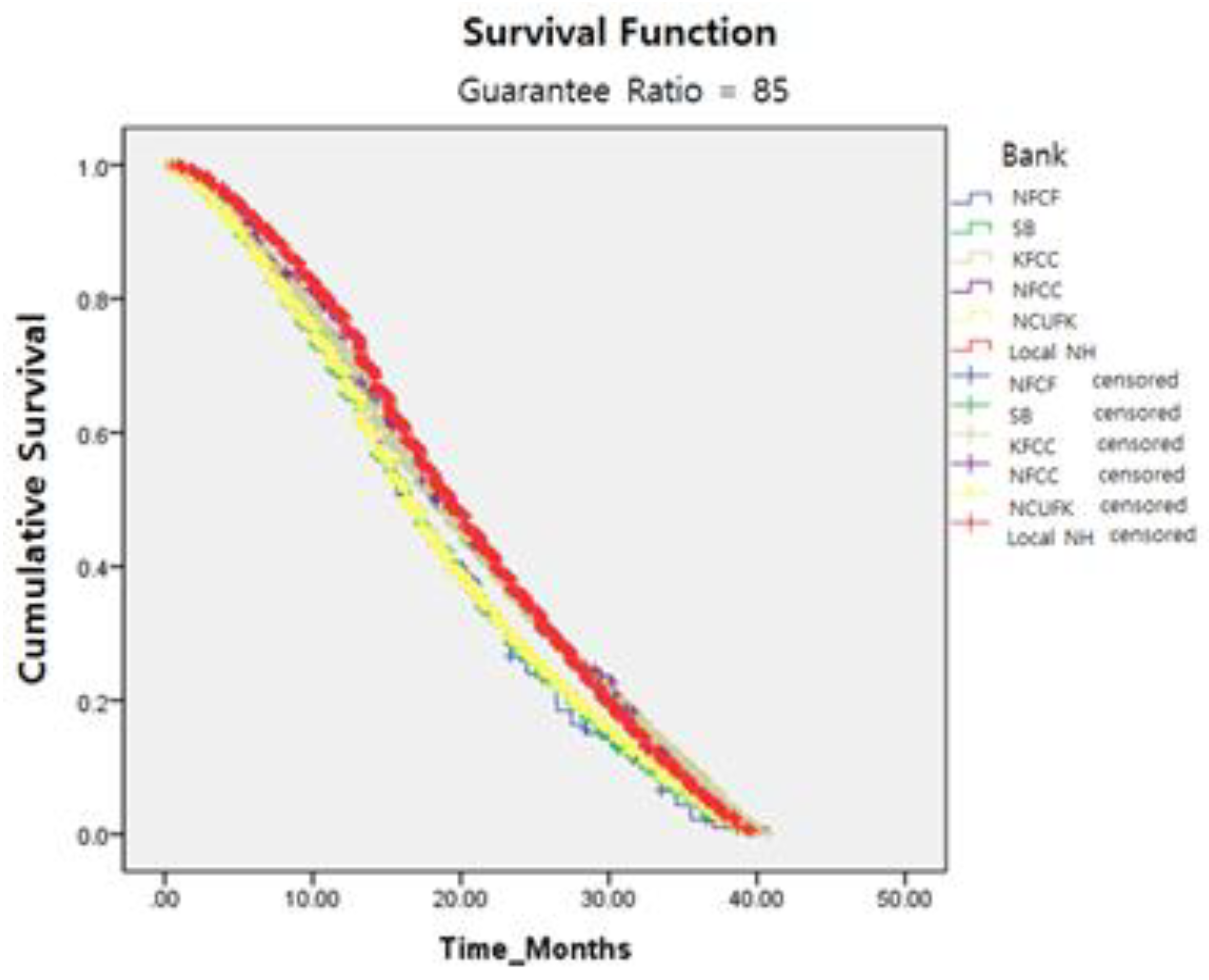

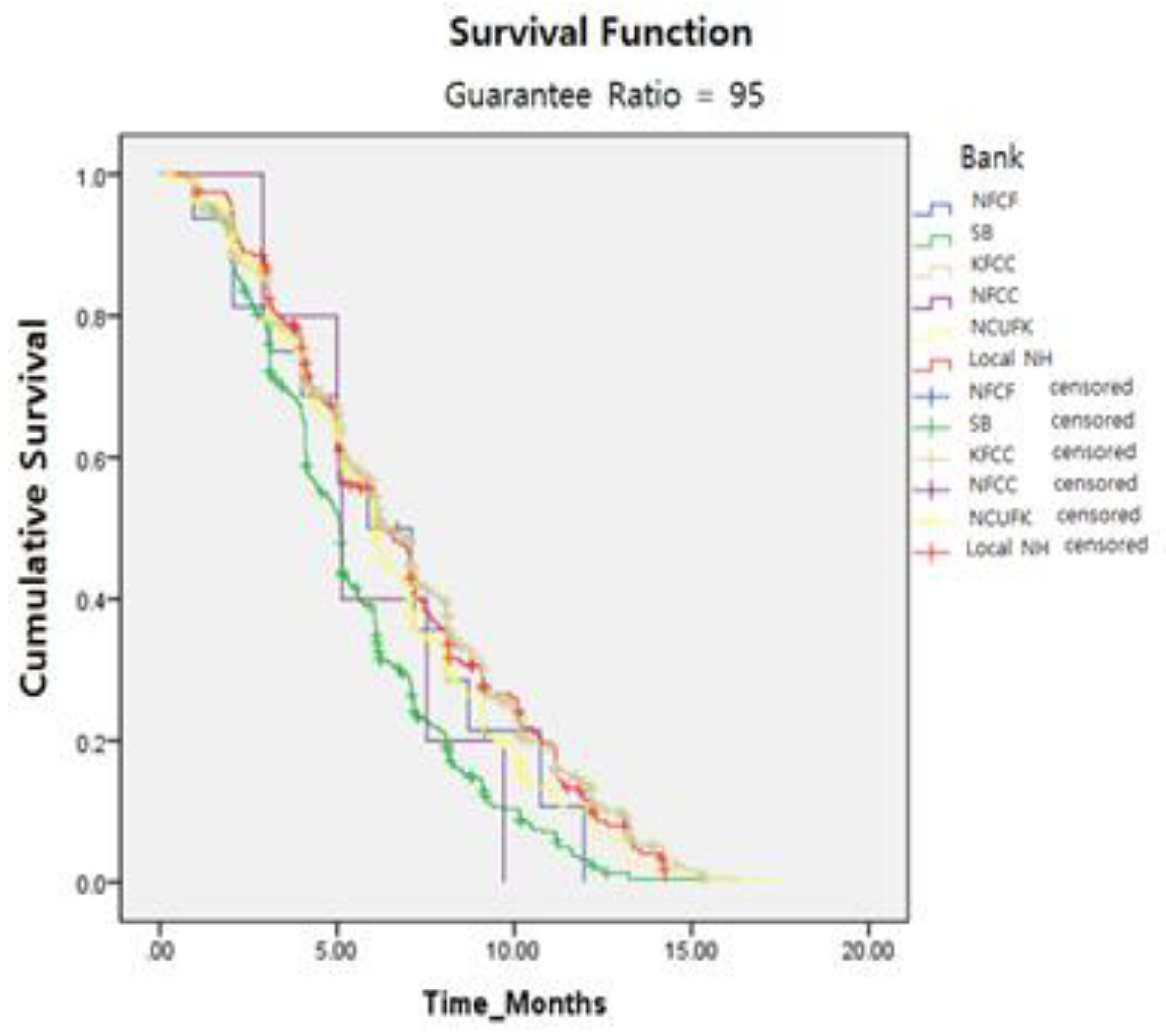

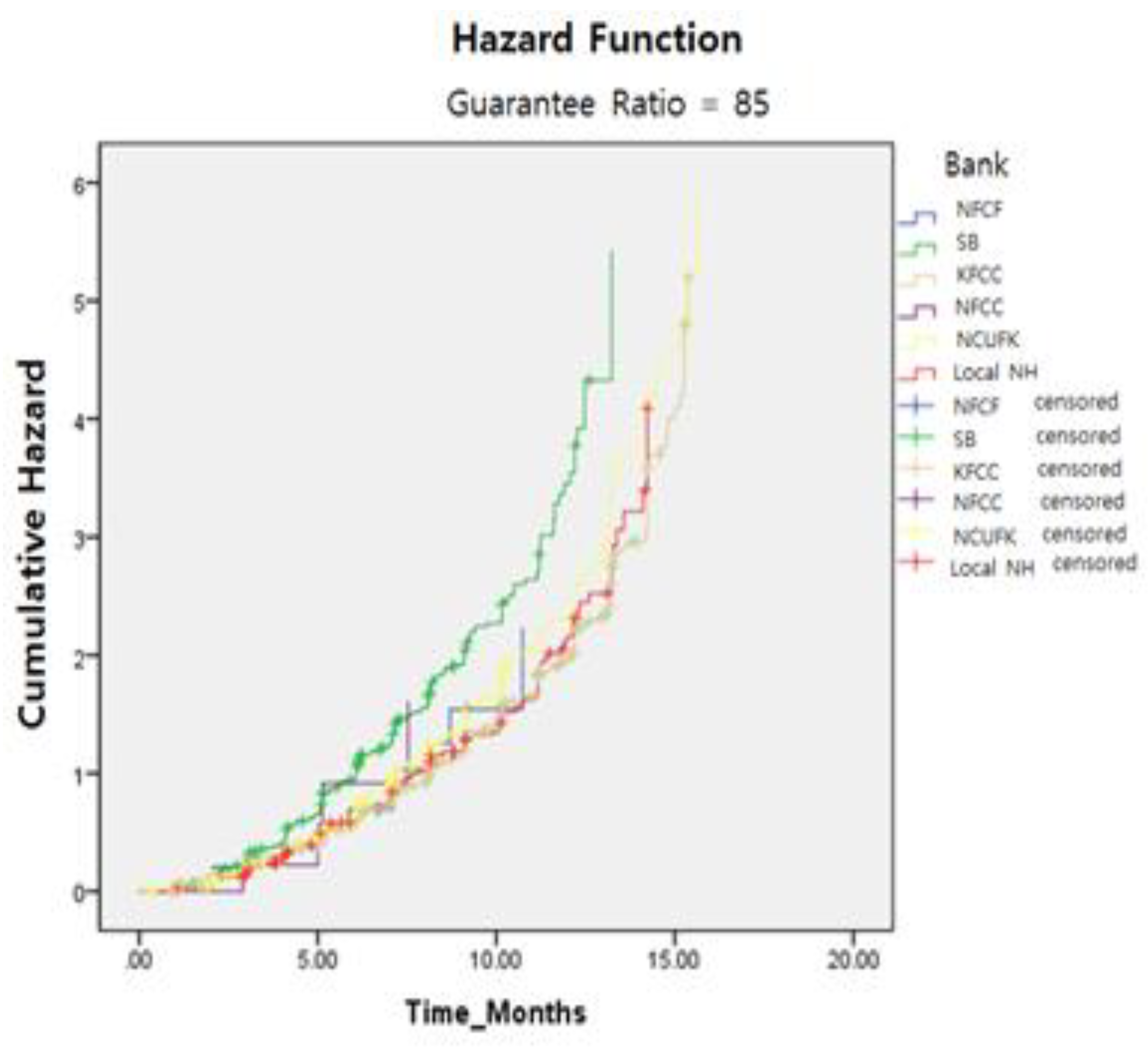

Based on these results, we additionally tested survival periods with a combined dataset (guarantee ratio and financial banking institutions). As shown in

Table 6 and

Figure 4 and

Figure 5, in the case of the 85% guarantee ratio, the mean survival duration of KFCCC was the longest (22.367 months), whereas that of SB was the shortest (15.767 months). In the case of the 95% guarantee ratio, NFCF had the longest survival duration (9.167 months), whereas NFFC had the shortest (5.467 months). More specifically, while the mean survival period for the 85% guarantee ratios was 20.033 months, that for the 95% guarantee ratios was 7.832 months. These findings indicate that lower guarantee ratios are associated with longer survival periods.

It is important to note that this study does not focus on the relationship between guarantee ratio and credit rating. The Korean Government initially designed 85% guarantee ratios based on the average guarantee ratio level offered by six small financial institutions from July 2010 to July 2012. At that time, these institutions’ risks increased by up to 15%, resulting in a reduction of the guarantee supply scale. This is because financial institutions for 85% guarantee ratios should increase the allowance for bad debts by up to 15%. In the case of 95% guarantee ratios, however, they just have to increase allowance for bad debts by up to 5%.

Since the guarantee ratio has increased by 95%, a sharp increase of guarantee supply has accompanied the risk reduction. This indicates that the survival rates of small financial institutions depend on the guarantee ratio. As shown earlier, the highest-level credit ratings are likely to decrease (or increase) risk rates (or survival rates), but the lowest-level credit ratings are likely to increase (or decrease) risk rates (or survival rates). However, financial institutions tend to avoid offering public loans to borrowers with low credit ratings. Additionally, it is difficult to determine survival rates and survival periods. In line with these observations, this study did not conduct cross-tabulation tests between guarantee ratio and credit rating.

4.4. Result 2: SMEs

As noted in Result 1, two types of guarantee ratios (85% and 95%) are identified by the estimated value of mean survival periods. As shown in

Table 7 and

Figure 6, the mean survival period for the 85% guarantee ratio was 18.2 months, whereas that for the 95% guarantee ratio was 6.1 months. Consequently, the 85% guarantee ratio survived much longer (12.1 months) than the 95% guarantee ratio.

As shown in

Table 8 and

Figure 7, we estimated the mean survival period values for the credit ratings of SMEs. The mean survival period for the noncredit rating was 2.933 months, and those for the first to tenth credit ratings were 24.4, 20.33, 20.3, 19.367, 19.2, 18.133, 16.267, 15.233, 15.167, and 18.267 months, respectively. Apart from the noncredit rating and tenth credit rating groups, these results show that the survival durations became gradually shorter from the first to tenth credit ratings. Consequently, there are no differences among credit ratings, suggesting that Regional Credit Guarantee Foundations (RCGFs) effectively deal with guaranteeing businesses.

This study estimated mean survival period values based on financial banking institutions for SME loans (see

Table 9 and

Figure 8). These estimated values were very similar to those of self-employers. Specifically, those of NFCF, SB, KFCCC, NFFC, NCUFK, and Local NH were 15.3, 13.267, 17.267, 18.267, 15.267, and 18.767 months, respectively. Consistent with the findings of self-employers, the mean survival period of SB was much shorter than those of other institutions. These results also explain the similar situation of credit ratings.

Finally, we tested survival periods based on guarantee ratio and financial banking institutions. As shown in

Table 10 and

Figure 9 and

Figure 10, in the case of the 85% guarantee ratio, the mean survival duration of Local NH was the longest (19.3 months), whereas that of NFCK was the shortest (16.267 months). The difference in survival periods was 3.033 months. These results on financial institutions are quite different from those of self-employers. In the case of the 95% guarantee ratio, the longest survival periods were those of KFCCC (6.4 months) and Local NH (6.4 months), whereas the shortest was that of SB (5.067 months). More specifically, while the mean survival period for the 85% guarantee ratios was 18.2 months, the mean survival period for the 95% guarantee ratios was 6.1 months. These survival durations were also similar to those of self-employers.

4.5. Survival Comparison Between Self-Employers and SMEs

There was a difference in the survival periods between self-employers and SMEs. While the average survival period of self-employers was 12.867 months, that of SMEs was 16.867 months. Although this difference is unique, an absolute comparison is impossible due to product characteristics. This is because in the case of operation and foundation funds for SMEs, the principal and interest after the one-year grace period are repaid, suggesting that the survival period of SMEs may be longer than that of self-employers. Considering this issue, a study comparing the two parties is needed.

In terms of guarantee ratios (see

Table 11 and

Table 12), the survival periods of self-employers were much longer than those of SMEs for both guarantee ratios (85% and 95%). Regarding credit ratings, self-employers with the sixth to eighth credit ratings were likely to have short survival periods, whereas SMEs with the seventh to ninth credit ratings had shorter survival periods. Finally, regarding small financial banking institutions, SB had the shortest survival period of both parties. Meanwhile, for the self-employer group, there were wider variations in survival periods compared to the SME group. These results are consistent with the credit rating findings.

5. Conclusions

Previous research has mainly shown that public loans, through which self-employers and SMEs borrow money from public financial institutions, yield more beneficial results than commercial bank loans [

4]. However, these studies have largely neglected the effective management of public funds. More specifically, how to ensure the optimal balance between small businesses and loan providers for managing public funds over time remains unclear. Moreover, little is known about how public funds should be managed to increase the survival periods, which are directly related to these institutions’ financial stability. To address these issues, this study explores the differences between self-employers and SMEs using survival analysis and investigated survival periods using key estimation criteria, such as guarantee ratios, credit ratings, and public financial institutions.

In the first step, we used a large empirical field dataset to investigate real customers’ reactions to survival periods. In particular, we explored survival periods for each individual group (self-employers vs. SMEs). The findings clearly show that individual-based borrowers, such as self-employers, have a strong tendency to survive much longer than SMEs. From the financial additionality perspective, these public credit schemes in Korea allow the targeted self-employers (or SMES) to borrow at longer maturities. Thus, this study elucidates which borrowers (individuals vs. small firms) are healthy and sheds light on the directions of public finance.

In the next step, we examined the differences between the two parties. Specifically, we focused on guarantee ratios, credit ratings, and banks that either enhanced the survival periods of these borrowers or decreased the financial risks of public institutions. Our results suggested that 85% guarantee ratios and high credit ratings help increase survival periods and reduce the financial solidity of public financial institutions. Moreover, no general approach is able to guide these institutions’ directions because each bank deals with its customers in a unique way.

5.1. Theoretical Implications

This study contributes to the literature in three ways. First, it extends previous research by investigating how public financial loans influence SMEs’ performance in the early stages. Although prior research has emphasized the consequences of public loans compared with commercial banks [

43,

44,

45], little is known about the survival periods of SMEs and their implications. The current empirical study represents a first attempt to address the limitations of the public-loan supply and provides key insights into how long public finance loans help SMEs survive. Specifically, our study extends the literature [

46,

47] by offering a risk theory perspective on public financial institutions that explains how both guarantee ratios and credit ratings affect the survival periods of borrowers and these institutions’ financial soundness.

Second, this study extends knowledge of the optimal balance between public-loan borrowers and financial institutions by exploring approaches to managing risks that are beyond the institutions’ control. More specifically, the current study is the first to offer a desirable approach to determining how public financial institutions can manage borrowers’ survival periods, which are outside the institutions’ direct control [

48], by showing that financial institutions can influence borrowers’ risks through the enhancement of guarantee ratios and strategic allocation of public loans for those with low credit ratings.

Finally, this study also provides new insights into the theoretical framework of MGIs on the sustainable stability of public financial loans [

20]. As noted earlier, public guaranteed loans are directed to self-employers and SMEs that can be considered as a booster of firm growth. The impact of these public financial loans is similar with MGIs, whereas the degree of effectiveness of guaranteed loans relies on the criteria according to which these loans are designed and implemented [

49]. In particular, a theoretical model—suggested by Minelli and Modica [

50] who compare the respective merits of different policies in ameliorating credit constraints—supports our findings highlighting the ways in which public loan guarantees are valuable for the financial stability of banks against incurring losses from default.

5.2. Managerial Implications

The current study provides several important implications for financial institutions. The findings suggest that for public or commercial financial institutions to avoid financial risks, they should carefully systematize their credit rating evaluation method. Specifically, financial managers should be aware that poor evaluation systems can undermine financial soundness, resulting in the decline of survival periods. Thus, it is crucial for financial institutions to develop integrated evaluation systems to decrease financial risks within public loan evaluation processes.

Financial institutions should also limit the public-loan supply for those with low credit ratings by offering additional government-support options. Specifically, as it is difficult to limit guarantee ratios for small start-up businesses, our findings suggest that those with low credit ratings should be individually managed by enhancing acceptances and guarantees. For example, the limitation of the guarantee ratio may temporarily worsen business situations, whereas it might help SMEs manage financial flows and ensure long-term business survival.

This study also offers implications for credit rating agencies that design evaluation methods for individual people and firms. Their systems primarily focus on stable recovery from financial loans, whereas they neglect business survival and competitive advantages. Our findings suggest that SMEs should be evaluated using a variety of evaluating factors, such as big data. Of course, financial institutions must reinforce their financial soundness regarding public loans, but our findings imply that identifying and segmenting borrowing groups, including self-employers, might be valuable for the development of evaluation systems.

5.3. Academic Contribution

In the presence of public guaranteed small business loans, little is known about how public funds should be managed to increase survival periods, which are directly related to these institutions’ financial stability. This study explores the differences between self-employers and SMEs using survival analysis and investigated survival periods using key estimation criteria, such as guarantee ratios, credit ratings, and public financial institutions. The findings of our study show that 85% guarantee ratios and high credit ratings help increase survival periods. The findings also show that individual-based borrowers, such as self-employers, have a strong tendency to survive much longer than SMEs. Finally, our study extends the literature by offering a risk theory perspective on public financial institutions that explains how both guarantee ratios and credit ratings affect the survival periods of borrowers, resulting in these institutions’ financial soundness. Therefore, the results hold values for both banks and small businesses

5.4. Limitations and Future Research Directions

As with all studies, this study has a few limitations that may provide potential opportunities for further research. First, in our empirical study, we investigated survival periods. Specifically, we examined how guarantee ratios and credit ratings affect them. Although the results from the empirical data from public financial institutions were valuable, further field research is needed because commercial banks also deal with similar service products, suggesting that an integrated mechanism for small business loans including self-employers would contribute to stabilizing the lending system for relevant financial issues.

Another opportunity is related to the use of big data, which these institutions may apply for the diversification of the current evaluation systems. In addition to economic data, using nonmetric resources, such as patents, trading areas, business ideas, and other intangible resources, is crucial for managing public loans and guiding the growth of SMEs, resulting in generalization to financial evaluation contexts. Thus, the application of big data may be a promising avenue for future research.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}