Is Inflation Fiscally Determined?

Abstract

:1. Introduction

2. Literature Review

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Paper | Sample | Methodology | Conclusion |

|---|---|---|---|

| Catao and Terrones [3] | 107 countries over 1960–2001 | ARDL model | Inflation and fiscal deficits are only correlated in the case of high-inflation, developing economies |

| Bohn [5] | US data 1916–1995 | OLS regressions by periods and a non-linear model for PB (based on debt) | The fiscal authority acts in a Ricardian fashion (Primary Balance adjusts) |

| Bajo-Rubio et al. [6] | 11 EU countries 1970–2005 | Cointegration analysis, Granger causality tests | Weak evidence for FTPL (Ricardian or monetary dominant regime) |

| Canzoneri et al. [7] | postwar U.S. data 1951–1995 | VAR, IRF | Evidence of a Ricardian regime |

| Favero and Monacelli [10] | US 1960–2002 | Markov-switching regression methods | Alternated Ricardian and non-Ricardian regime |

| Tanner and Ramos [18] | Brazil 1991–2000 | VAR, IRF, and Granger causality tests | Fiscal dominance for the case of Brazil for some important periods |

| Creel and Le Bihan [8] | France, Germany, Italy, the UK, and the US data 1963–2001 | VAR, IRF (same approach as [7]), and separation between structural/cyclical PB | FTPL non-valid |

| Fan and Minford [19] | The UK in the 1970s | ARIMA model for inflation, ADF, and cointegration tests | Behavior of inflation can be explained by the FTPL (government expenditures) |

3. Theoretical Model

4. Data and Approach

- Exchange rate targets: the monetary authority intervenes to maintain the exchange rate at a particular level.

- Inflation targeting: this strategy relies on the use of inflation expectations to control the price level. It involves the announcement of numerical targets, accompanied by an institutional commitment to achieve these targets. Credibility and accountability of the monetary authority in that case are crucial to the conduct of monetary policy.

- Monetary targets: the monetary authority uses its instruments to achieve a target growth rate for a monetary aggregate that becomes the nominal anchor or intermediate target of monetary policy.

- Mixed targets: the monetary authority uses monetary targets and exchange rate fixes or targets, or three full targets (or fixes) (money, exchange rates, and inflation).

- Euro zone countries: Euro zone countries have been isolated in a separate group.

- Discretion: in that case, monetary policy is based on the ad hoc judgment of policymakers as opposed to the use of predetermined rules. The degree of effectiveness and coherence of the set of objectives and instruments in this case depends on the countries and periods. Moreover, most of the countries included in this category either do not have a significant use of foreign currency among residents or have substantially reduced this usage over the studied period.

- Poorly structured monetary policy: in this group, we isolate the countries characterized by a significant dollarization of the economy, and which either have no monetary policy framework (e.g., Panama) or use a poorly effective set of instruments or an incoherent mix of objectives over most of the sample period.

5. Econometric Methodology

6. Correlation Analysis

7. Empirical Results

7.1. Recursive PVAR Model Estimation

7.1.1. Model OLS Estimates

7.1.2. Forecast Error Variance Decomposition

7.2. Unrestricted PVAR Model Estimation

7.2.1. GMM Estimates

7.2.2. GIRFs after Fiscal, Monetary, and Recessionary Shocks in the Whole Sample

- Fiscal policy shocks

- Monetary Policy Shocks

- Recessionary Shocks

7.2.3. Inflation response by Monetary Policy Framework (GIRF)

7.2.4. Inflation Response by Level of Fiscal Space (GIRF)

8. Discussion

8.1. Fiscal Policy and Inflation

8.2. Monetary Policy and the Fiscal Determinacy of Prices

8.3. The Impact of Political and Financial Factors

9. Concluding Remarks

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| FTPL | Fiscal Theory of the Price Level |

| GIRF | Generalized Impulse Response Functions |

| IRF | Impulse Response Functions |

| MPF | Monetary Policy Framework |

| PVAR | Panel Vector Auto Regression |

| VAR | Vector Auto Regression |

Appendix A. A Brief Summary of the Model of Cochrane

Appendix B. Sample Countries

| Group | Countries | ||

| ADVANCED | Australia | Austria | Belgium |

| Canada | Denmark | Finland | |

| France | Germany | Greece | |

| Iceland | Ireland | Italy | |

| Japan | Netherlands | New Zealand | |

| Norway | Portugal | South Korea | |

| Spain | Sweden | Switzerland | |

| United Kingdom | United States | ||

| EMERGING AND MIDDLE-INCOME | Argentina | Brazil | Chile |

| Colombia | Costa Rica | Dominican Republic | |

| India | Mexico | Morocco | |

| Pakistan | Panama | Paraguay | |

| Peru | Philippines | South Africa | |

| Thailand | Turkey | Uruguay | |

| LOW-INCOME AND DEVELOPING | Ghana | Haiti | |

| Honduras | |||

Appendix C. A General Overview of Data

- Level of Primary Balance/GDP (%): data for primary balances are retrieved from the dataset of Mauro et al. [57]. Missing data are completed from various databases, such as the OECD, the World Bank, and the MOxLAD database for Latin American economies, available online: http://moxlad.cienciassociales.edu.uy/en (last access on 31 May 2021).

- Log of public debt to GDP: we use the underlying dataset of the paper Mauro et al. (2013). Missing data are then completed from various sources, such as the website “tradingeconomics.com” and the database of Reinhart and Rogoff [58].

- GDP growth (%): data of GDP per capita are extracted from the World Bank database.

- Short term interest rates: data are collected from several sources, more specifically from the IFS, Eurostat, the OECD database, and in some cases from central banks’ websites.

- Inflation rate: data are calculated from the Consumer Price Index (with 2010 as the base year), taken from the World Bank database. Missing data are completed based on Reinhart and Rogoff [58].

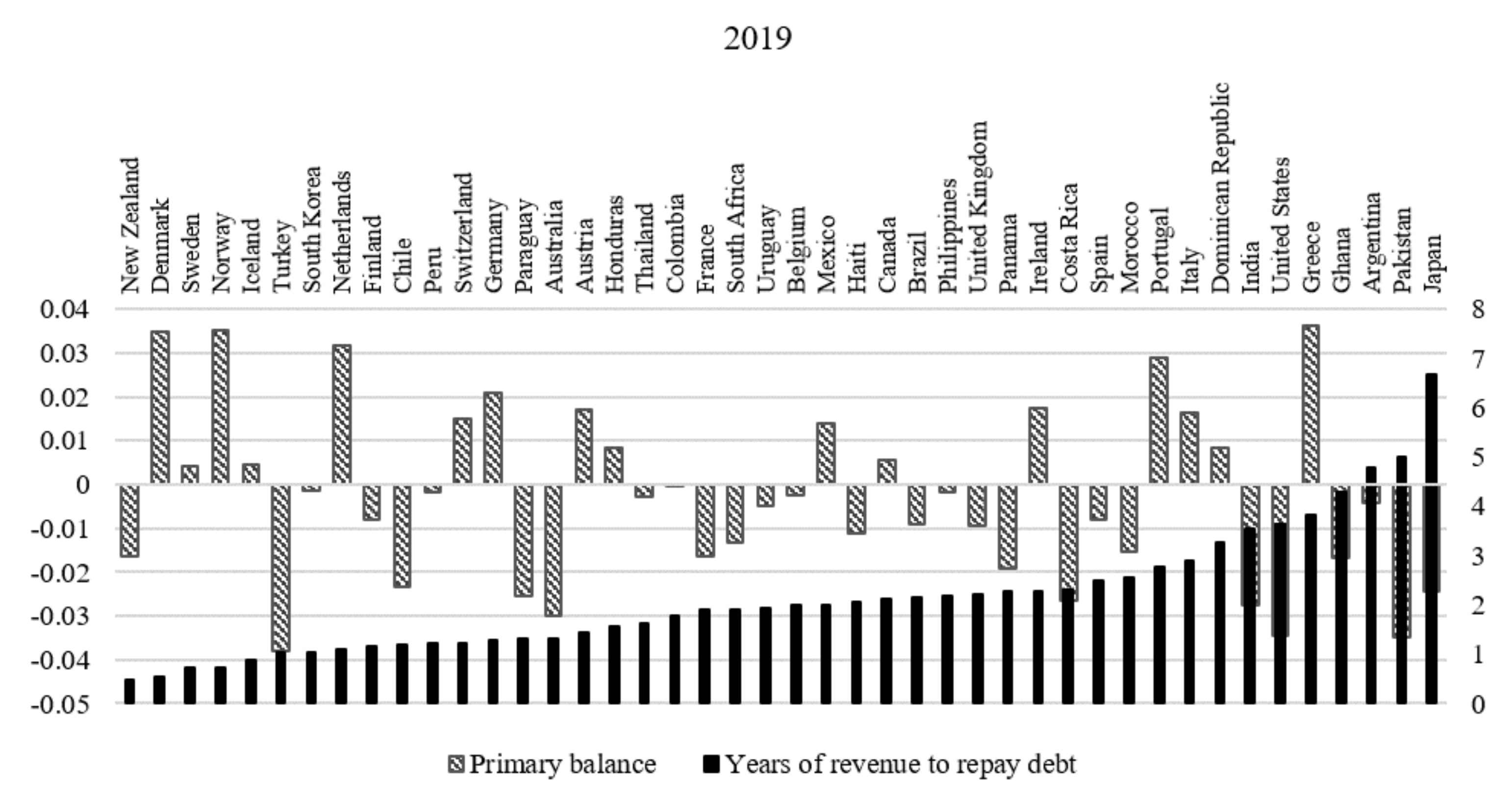

Appendix D. Inverse of Fiscal Space Ratio (in Years): Descriptive Statistics by Country

| 2006 | 2010 | 2019 | 2020 | Average | Min | Max | Stand. Deviation | Number of Observations | |

| Advanced economies | 1.5 | 2.0 | 1.9 | 2.3 | 1.6 | 0.2 | 7.5 | 1.1 | 943 |

| Australia | 0.3 | 0.6 | 1.3 | 1.8 | 0.7 | 0.3 | 1.8 | 0.3 | 41 |

| Austria | 1.3 | 1.5 | 1.4 | 1.7 | 1.3 | 0.8 | 1.7 | 0.2 | 41 |

| Belgium | 1.8 | 1.9 | 2.0 | 2.3 | 2.2 | 1.6 | 2.8 | 0.3 | 41 |

| Canada | 1.7 | 2.1 | 2.1 | 2.8 | 1.9 | 1.2 | 2.8 | 0.3 | 41 |

| Denmark | 0.6 | 0.8 | 0.5 | 0.8 | 0.9 | 0.5 | 1.4 | 0.3 | 41 |

| Finland | 0.8 | 0.9 | 1.2 | 1.3 | 0.8 | 0.2 | 1.3 | 0.3 | 41 |

| France | 1.3 | 1.6 | 1.9 | 2.2 | 1.2 | 0.5 | 2.2 | 0.5 | 41 |

| Germany | 1.6 | 1.9 | 1.3 | 1.5 | 1.3 | 0.7 | 1.9 | 0.3 | 41 |

| Greece | 2.7 | 3.5 | 3.8 | 4.2 | 2.8 | 1.0 | 4.2 | 0.8 | 41 |

| Iceland | 0.6 | 2.3 | 0.9 | 1.9 | 1.2 | 0.6 | 2.5 | 0.5 | 41 |

| Ireland | 0.7 | 2.9 | 2.3 | 2.6 | 2.1 | 0.7 | 3.5 | 0.8 | 41 |

| Italy | 2.4 | 2.6 | 2.9 | 3.3 | 2.5 | 1.7 | 3.3 | 0.3 | 41 |

| Japan | 6.0 | 7.2 | 6.7 | 7.5 | 4.6 | 1.8 | 7.5 | 2.1 | 41 |

| Netherlands | 1.1 | 1.5 | 1.1 | 1.2 | 1.4 | 0.9 | 1.7 | 0.2 | 41 |

| New Zealand | 0.4 | 0.8 | 0.5 | 0.9 | 0.9 | 0.4 | 1.7 | 0.4 | 41 |

| Norway | 1.0 | 1.0 | 0.7 | 0.8 | 0.7 | 0.5 | 1.0 | 0.2 | 41 |

| Portugal | 1.6 | 2.3 | 2.8 | 3.1 | 1.8 | 0.7 | 3.1 | 0.7 | 41 |

| South Korea | 1.0 | 1.0 | 1.0 | 1.9 | 0.8 | 0.3 | 1.9 | 0.3 | 41 |

| Spain | 1.0 | 1.7 | 2.5 | 2.8 | 1.5 | 0.4 | 2.8 | 0.7 | 41 |

| Sweden | 0.8 | 0.8 | 0.7 | 0.8 | 0.9 | 0.6 | 1.3 | 0.2 | 41 |

| Switzerland | 2.0 | 1.6 | 1.2 | 1.3 | 1.5 | 0.8 | 2.2 | 0.4 | 41 |

| United Kingdom | 1.1 | 2.0 | 2.2 | 2.6 | 1.5 | 1.0 | 2.6 | 0.4 | 41 |

| United States | 1.8 | 3.1 | 3.6 | 4.2 | 2.3 | 1.3 | 4.2 | 0.7 | 41 |

| Emerging and Middle- income | 2.1 | 1.9 | 2.3 | 2.8 | 3.1 | 0.2 | 236.1 | 10.8 | 738 |

| Argentina | 2.7 | 1.5 | 4.8 | 3.1 | 2.5 | 0.5 | 8.1 | 1.5 | 41 |

| Brazil | 1.8 | 1.7 | 2.1 | 3.4 | 1.6 | 0.9 | 3.4 | 0.5 | 41 |

| Chile | 0.2 | 0.4 | 1.2 | 1.4 | 1.2 | 0.2 | 4.0 | 1.0 | 41 |

| Colombia | 1.3 | 1.4 | 1.8 | 2.4 | 11.3 | 0.6 | 236.1 | 44.4 | 41 |

| Costa Rica | 2.3 | 2.1 | 2.3 | 1.7 | 4.4 | 1.6 | 8.9 | 2.4 | 41 |

| Dominican Republic | 1.5 | 2.2 | 3.3 | 4.8 | 3.3 | 1.2 | 10.2 | 2.2 | 41 |

| India | 3.0 | 2.7 | 3.6 | 4.4 | 2.8 | 1.4 | 4.4 | 0.9 | 41 |

| Mexico | 1.8 | 1.8 | 2.0 | 1.7 | 2.2 | 1.5 | 3.7 | 0.6 | 41 |

| Morocco | 2.2 | 1.8 | 2.5 | 2.7 | 3.3 | 1.5 | 6.3 | 1.3 | 41 |

| Pakistan | 4.3 | 3.9 | 5.0 | 4.9 | 4.9 | 3.6 | 6.9 | 0.7 | 41 |

| Panama | 2.2 | 1.6 | 2.3 | 3.6 | 2.8 | 1.6 | 5.1 | 0.9 | 41 |

| Paraguay | 1.7 | 0.9 | 1.3 | 1.9 | 2.3 | 0.7 | 5.6 | 1.4 | 41 |

| Peru | 1.8 | 1.3 | 1.2 | 2.0 | 2.6 | 1.0 | 5.5 | 1.2 | 41 |

| Philippines | 3.4 | 3.9 | 2.2 | 3.0 | 3.6 | 2.1 | 6.6 | 1.0 | 41 |

| South Africa | 0.9 | 1.0 | 1.9 | 2.8 | 1.3 | 0.8 | 2.8 | 0.4 | 41 |

| Thailand | 2.0 | 2.1 | 1.6 | 2.4 | 1.8 | 0.2 | 3.4 | 0.8 | 41 |

| Turkey | 1.4 | 1.3 | 1.0 | 1.2 | 1.2 | 0.7 | 2.5 | 0.4 | 41 |

| Uruguay | 2.6 | 1.9 | 1.9 | 2.4 | 2.3 | 0.8 | 5.4 | 1.1 | 41 |

| Low-income developing | 2.2 | 1.5 | 2.6 | 3.3 | 4.8 | 0.8 | 35.0 | 5.0 | 123 |

| Ghana | 1.5 | 2.1 | 4.3 | 6.3 | 4.1 | 1.5 | 10.1 | 2.0 | 41 |

| Haiti | 3.6 | 1.2 | 2.1 | 1.7 | 7.2 | 0.8 | 35.0 | 7.6 | 41 |

| Honduras | 1.3 | 1.1 | 1.6 | 1.8 | 3.0 | 0.8 | 6.8 | 1.6 | 41 |

| Total | 1.8 | 1.9 | 2.2 | 2.6 | 2.4 | 0.2 | 236.1 | 7.1 | 1804 |

| Notes: fiscal space is defined as the sum of total government revenues divided by public debt. The inverse of this measure reflects the number of years of revenue needed to repay the outstanding of public debt at a given date. | |||||||||

Appendix E. Correlation Coefficients between the Primary Balance and the Inverse of the Fiscal Space Ratio (The Number of Years of Revenue Needed to Repay the Debt)

| Inverse of Fiscal Space Ratio (Average in Years) | Correlation Coefficient with Primary Balance | |||||||||

| 1980–2020 | 1980–1989 | 1990–1999 | 2000–2009 | 2010–2020 | 1980–2020 | 1980–1989 | 1990–1999 | 2000–2009 | 2010–2020 | |

| Advanced economies | 1.6 | 1.3 | 1.5 | 1.5 | 2.0 | −61% | 85% | −64% | −96% | −82% |

| Australia | 0.7 | 0.6 | 0.8 | 0.4 | 1.1 | −65% | 74% | −56% | −49% | −50% |

| Austria | 1.3 | 1.1 | 1.3 | 1.3 | 1.6 | −43% | −30% | −86% | −61% | −47% |

| Belgium | 2.2 | 2.3 | 2.6 | 2.0 | 2.0 | 54% | 85% | 49% | 9% | −65% |

| Canada | 1.9 | 1.5 | 2.1 | 1.8 | 2.2 | −27% | 22% | 18% | −36% | −86% |

| Denmark | 0.9 | 1.0 | 1.2 | 0.8 | 0.7 | 31% | 59% | −91% | −39% | −81% |

| Finland | 0.8 | 0.3 | 0.8 | 0.8 | 1.1 | −67% | −48% | −46% | −31% | −34% |

| France | 1.2 | 0.6 | 1.0 | 1.3 | 1.8 | −38% | −32% | 5% | −92% | −16% |

| Germany | 1.3 | 0.9 | 1.2 | 1.5 | 1.6 | −5% | 74% | −4% | −31% | −41% |

| Greece | 2.8 | 1.8 | 2.9 | 2.7 | 3.7 | 3% | −52% | 76% | −88% | 37% |

| Iceland | 1.2 | 0.8 | 1.2 | 1.1 | 1.6 | −61% | −38% | −32% | −78% | −63% |

| Ireland | 2.1 | 2.3 | 2.0 | 1.0 | 2.9 | −37% | 81% | −56% | −85% | −37% |

| Italy | 2.5 | 2.1 | 2.6 | 2.4 | 2.8 | 11% | 21% | −23% | −79% | 1% |

| Japan | 4.6 | 2.2 | 3.0 | 5.8 | 7.1 | −83% | 71% | −91% | −19% | −90% |

| Netherlands | 1.4 | 1.3 | 1.6 | 1.2 | 1.4 | −10% | 70% | −75% | −53% | −62% |

| New Zealand | 0.9 | 1.4 | 1.1 | 0.6 | 0.7 | −23% | −64% | −36% | −24% | −84% |

| Norway | 0.7 | 0.6 | 0.6 | 0.9 | 0.7 | 40% | 0% | −13% | 18% | −4% |

| Portugal | 1.8 | 1.2 | 1.4 | 1.5 | 2.8 | −19% | 82% | −27% | −65% | 52% |

| South Korea | 0.8 | 0.8 | 0.4 | 0.8 | 1.1 | −71% | −70% | −65% | −73% | −44% |

| Spain | 1.5 | 0.7 | 1.4 | 1.2 | 2.4 | −36% | 73% | 7% | −42% | 26% |

| Sweden | 0.9 | 0.9 | 1.1 | 0.9 | 0.8 | 8% | 30% | −20% | −14% | 4% |

| Switzerland | 1.5 | 1.3 | 1.7 | 1.9 | 1.1 | 0% | −69% | −1% | −81% | 27% |

| United Kingdom | 1.5 | 1.3 | 1.3 | 1.2 | 2.2 | −66% | 33% | −31% | −81% | −43% |

| United States | 2.3 | 1.7 | 2.1 | 2.0 | 3.4 | −71% | 1% | −80% | −97% | −60% |

| Emerging and Middle- income | 3.1 | 5.4 | 2.5 | 2.4 | 2.1 | −4% | −37% | 47% | −32% | −38% |

| Argentina | 2.5 | 2.5 | 1.6 | 3.5 | 2.3 | 16% | 14% | −82% | 18% | 6% |

| Brazil | 1.6 | 1.4 | 1.1 | 1.9 | 1.9 | −66% | −31% | 28% | −62% | −34% |

| Chile | 1.2 | 2.3 | 1.3 | 0.5 | 0.8 | 13% | 2% | 56% | −65% | −87% |

| Colombia | 11.3 | 42.0 | 0.8 | 1.5 | 1.7 | −1% | −26% | −50% | −69% | −67% |

| Costa Rica | 4.4 | 7.7 | 5.0 | 2.5 | 2.5 | 62% | 75% | 13% | −31% | 48% |

| Dominican Republic | 3.3 | 5.4 | 3.5 | 1.7 | 2.9 | 21% | 56% | 65% | −75% | −12% |

| India | 2.8 | 1.5 | 2.7 | 3.4 | 3.5 | 24% | −34% | 48% | −61% | −49% |

| Mexico | 2.2 | 2.7 | 2.4 | 2.1 | 1.9 | 66% | 77% | −21% | 57% | 54% |

| Morocco | 3.3 | 4.9 | 3.8 | 2.4 | 2.3 | −29% | 63% | 1% | −76% | 54% |

| Pakistan | 4.9 | 4.6 | 5.7 | 5.1 | 4.5 | 55% | −31% | 91% | 71% | −3% |

| Panama | 2.8 | 3.4 | 3.5 | 2.5 | 2.0 | 12% | −15% | −12% | −65% | −66% |

| Paraguay | 2.3 | 3.0 | 2.6 | 2.6 | 1.1 | 23% | 44% | 34% | −49% | −87% |

| Peru | 2.6 | 3.8 | 3.0 | 2.3 | 1.3 | −24% | −5% | −46% | −63% | −85% |

| Philippines | 3.6 | 4.3 | 3.3 | 4.0 | 3.0 | 31% | 80% | −17% | −18% | −53% |

| South Africa | 1.3 | 1.1 | 1.4 | 1.1 | 1.5 | −37% | 10% | −16% | 12% | −35% |

| Thailand | 1.8 | 1.9 | 0.7 | 2.5 | 1.9 | −44% | −8% | −59% | −57% | −59% |

| Turkey | 1.2 | 1.1 | 1.1 | 1.7 | 1.0 | 48% | −8% | 72% | 8% | −65% |

| Uruguay | 2.3 | 3.2 | 1.5 | 2.7 | 1.7 | 8% | 11% | 54% | 49% | 30% |

| Low-income developing | 4.8 | 5.2 | 8.1 | 3.7 | 2.2 | 33% | 87% | 21% | 39% | 0% |

| Ghana | 4.1 | 3.1 | 5.3 | 4.2 | 3.6 | 5% | 55% | −62% | 46% | 9% |

| Haiti | 7.2 | 9.1 | 13.9 | 4.8 | 1.6 | −7% | 56% | −17% | −5% | −12% |

| Honduras | 3.0 | 3.5 | 5.0 | 2.2 | 1.5 | 41% | 6% | −11% | −4% | −41% |

| Total | 2.4 | 3.2 | 2.4 | 2.0 | 2.1 | −3% | −28% | 10% | −18% | −41% |

References

- Sargent, T.; Wallace, N. Some unpleasant monetarist arithmetic. Fed. Reserve Bank Minneap. Q. Rev. 1981, 5, 1–17. [Google Scholar] [CrossRef]

- Leeper, E. Equilibria under ‘active’ and ‘passive’ monetary and fiscal policies. J. Monet. Econ. 1991, 27, 129–147. [Google Scholar] [CrossRef]

- Catao, L.; Terrones, M. Fiscal deficits and inflation. J. Monet. Econ. 2005, 52, 529–554. [Google Scholar] [CrossRef] [Green Version]

- Fischer, S.; Sahay, R.; Végh, C. Modern hyper-and high inflations. J. Econ. Lit. 2002, 40, 837–880. [Google Scholar] [CrossRef]

- Bohn, H. The behavior of US public debt and deficits. Q. J. Econ. 1998, 113, 949–963. [Google Scholar] [CrossRef]

- Bajo-Rubio, Ó.; Díaz-Roldán, C.; Esteve, V. Deficit sustainability and inflation in EMU: An analysis from the Fiscal Theory of the Price Level. Eur. J. Political Econ. 2009, 25, 525–539. [Google Scholar] [CrossRef] [Green Version]

- Canzoneri, M.; Cumby, R.; Diba, B. Is the price level determined by the needs of fiscal solvency? Am. Econ. Rev. 2001, 91, 1221–1238. [Google Scholar] [CrossRef] [Green Version]

- Creel, J.; Le Bihan, H. Using structural balance data to test the fiscal theory of the price level: Some international evidence. J. Macroecon. 2006, 28, 338–360. [Google Scholar] [CrossRef] [Green Version]

- Sargent, T. Beyond demand and supply curves in macroeconomics. Am. Econ. Rev. 1982, 72, 382–389. [Google Scholar]

- Favero, C.; Monacelli, T. Fiscal Policy Rules and Regime (in) Stability: Evidence from the US; IGIER Working Paper; Bocconi University: Milano, Italy, 2005. [Google Scholar]

- Sims, C. A simple model for study of the determination of the price level and the interaction of monetary and fiscal policy. Econ. Theory 1994, 4, 381–399. [Google Scholar] [CrossRef]

- Woodford, M. Monetary policy and price level determinacy in a cash-in-advance economy. Econ. Theory 1994, 4, 345–380. [Google Scholar] [CrossRef] [Green Version]

- Woodford, M. Price-level determinacy without control of a monetary aggregate. Carnegie-Rochester Conf. Ser. Public Policy 1995, 43, 1–46. [Google Scholar] [CrossRef] [Green Version]

- Cochrane, J. Money as stock. J. Monet. Econ. 2005, 52, 501–528. [Google Scholar] [CrossRef]

- Cochrane, J. Stepping on a rake: The fiscal theory of monetary policy. Eur. Econ. Rev. 2018, 101, 354–375. [Google Scholar] [CrossRef] [Green Version]

- Cochrane, J. The Fiscal Theory of the Price Level. Chicago Booth. 2019. Available online: https://faculty.chicagobooth.edu/john.cochrane/research/papers (accessed on 12 April 2019).

- Loyo, E. Tight Money Paradox on the Loose: A Fiscalist Hyperinflation; Harvard University: Cambridge, MA, USA, 1999. [Google Scholar]

- Tanner, E.; Ramos, A. Fiscal sustainability and monetary versus fiscal dominance: Evidence from Brazil, 1991–2000. Appl. Econ. 2003, 35, 859–873. [Google Scholar] [CrossRef]

- Fan, J.; Minford, P.; Ou, Z. The Fiscal Theory of the Price Level-Identification and Testing for the UK in the 1970s; Cardiff Economics Working Papers; Cardiff University: Cardiff, UK, 2013. [Google Scholar]

- Sims, C. Stepping on a Rake: The Role of Fiscal Policy in the Inflation of the 1970s. Eur. Econ. Rev. 2011, 55, 48–56. [Google Scholar] [CrossRef] [Green Version]

- Cochrane, J. The Fiscal Roots of Inflation. Working Paper. 2019. Available online: https://faculty.chicagobooth.edu/john.cochrane/research/ (accessed on 23 April 2019).

- Hall, G.; Payne, J.; Sargent, T. US Federal Debt 1776–1960: Quantities and Prices; New York University, Leonard N. Stern School of Business, Department of Economics: New York, NY, USA, 2018; Available online: http://www.tomsargent.com/research/US_Federal_Debt_Data.pdf (accessed on 10 October 2021).

- Stockman, A. Anticipated inflation and the capital stock in a cash in-advance economy. J. Monet. Econ. 1981, 8, 387–393. [Google Scholar] [CrossRef]

- Arawatari, R.; Hori, T.; Mino, K. On the nonlinear relationship between inflation and growth: A theoretical exposition. J. Monet. Econ. 2018, 94, 79–93. [Google Scholar] [CrossRef] [Green Version]

- Vaona, A. Inflation and growth in the long run: A New Keynesian theory and further semiparametric evidence. Macroecon. Dyn. 2012, 16, 94–132. [Google Scholar] [CrossRef] [Green Version]

- Kormendi, R.; Meguire, P. Macroeconomic determinants of growth: Cross-country evidence. J. Monet. Econ. 1985, 16, 141–163. [Google Scholar] [CrossRef]

- Fischer, S. The role of macroeconomic factors in growth. J. Monet. Econ. 1993, 32, 485–512. [Google Scholar] [CrossRef] [Green Version]

- Gomme, P. Money and growth revisited: Measuring the costs of inflation in an endogenous growth model. J. Monet. Econ. 1993, 32, 51–77. [Google Scholar] [CrossRef] [Green Version]

- De Gregorio, J. Economic growth in Latin America. J. Dev. Econ. 1992, 39, 59–84. [Google Scholar] [CrossRef]

- Andres, J.; Hernando, I. Inflation and Economic Growth: Some Evidence for the OECD Countries; Monetary Policy and The Inflation Process-BIS Conference Papers; Bank for International Settlements Monetary and Economic Department: Basel, Switzerland, 1997; pp. 364–383. [Google Scholar]

- Cobham, D. A Comprehensive Classification of Monetary Policy Frameworks for Advanced and Emerging Economies. MPRA Paper. 2018. Available online: https://mpra.ub.uni-muenchen.de/id/eprint/90141 (accessed on 14 August 2019).

- Barro, R.; Gordon, D. Rules, discretion and reputation in a model of monetary policy. J. Monet. Econ. 1983, 12, 101–121. [Google Scholar] [CrossRef] [Green Version]

- Rogoff, K. The optimal degree of commitment to an intermediate monetary target. Q. J. Econ. 1985, 100, 1169–1189. [Google Scholar] [CrossRef]

- Ha, J.; Stocker, M.; Yilmazkuday, H. Inflation and exchange rate pass-through. J. Int. Money Financ. 2020, 105, 102187. [Google Scholar] [CrossRef] [Green Version]

- Heller, M. Understanding Fiscal Space; Discussion Paper PDP/05/4; International Monetary Fund: Washington, DC, USA, 2005. [Google Scholar]

- Auerbach, A.; Gale, W. Tempting Fate: The Federal Budget Outlook; Brookings Institution: Washington, DC, USA, 2011; Available online: https://eml.berkeley.edu/~auerbach/temptingfate.pdf (accessed on 24 August 2021).

- Buiter, W. A guide to public sector debt and deficits. Econ. Policy 1985, 1, 13–61. [Google Scholar] [CrossRef]

- Buiter, W.; Corsetti, G.; Roubini, N. Excessive Deficits: Sense and Nonsense in the Treaty of Maastricht. Economic Policy 1993, 8, 57–100. [Google Scholar] [CrossRef] [Green Version]

- Aizenman, J.; Jinjarak, Y. De facto fiscal space and fiscal stimulus: Definition and assessment. Working paper 16539. Natl. Bur. Econ. Res. 2010. [Google Scholar] [CrossRef]

- Sigmund, M.; Ferstl, R. Panel Vector Autoregression in R with the Package Panelvar. SSRN Electron. J. 2017. [Google Scholar] [CrossRef]

- Nickell, S. Biases in dynamic models with fixed effects. Econometrica 1981, 49, 1417–1426. [Google Scholar] [CrossRef]

- Anderson, T.; Hsiao, C. Formulation and estimation of dynamic models using panel data. J. Econom. 1982, 18, 47–82. [Google Scholar] [CrossRef]

- Arellano, M.; Bond, S. Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Rev. Econ. Stud. 1991, 58, 277–297. [Google Scholar] [CrossRef] [Green Version]

- Holtz-Eakin, D.; Newey, W.; Rosen, H. Estimating vector autoregressions with panel data. Econometrica 1988, 56, 1371–1395. [Google Scholar] [CrossRef]

- Blundell, R.; Bond, S. Initial conditions and moment restrictions in dynamic panel data models. J. Econom. 1998, 87, 115–143. [Google Scholar] [CrossRef] [Green Version]

- Pesaran, H.; Shin, Y. Generalized impulse response analysis in linear multivariate models. Econ. Lett. 1998, 58, 17–29. [Google Scholar] [CrossRef]

- Kilian, L.; Lütkepohl, H. Structural Vector Autoregressive Analysis; Cambridge University Press: Cambridge, UK, 2017; Available online: https://ideas.repec.org/b/cup/cbooks/9781107196575.html (accessed on 15 June 2021).

- Kydland, F.; Prescott, E. Rules rather than discretion: The inconsistency of optimal plans. J. Political Econ. 1977, 85, 473–491. [Google Scholar] [CrossRef] [Green Version]

- Carranza, L.; Galdon-Sanchez, J.; Gomez-Biscarri, J. Exchange rate and inflation dynamics in dollarized economies. J. Dev. Econ. 2009, 89, 98–108. [Google Scholar] [CrossRef] [Green Version]

- Reinhart, C.; Rogoff, K.; Savastano, M. Addicted to Dollars; Working Paper 10015; National Bureau of Economic Research Cambridge: Cambridge, MA, USA, 2003. [Google Scholar]

- Devereux, M. Monetary policy, exchange rate flexibility, and exchange rate pass-through. Revisiting The Case For Flexible Exchange Rates. In Proceedings of the Conference Held by the Bank of Canada, Ottawa, ON, Canada, 2–3 November 2000; pp. 47–82. [Google Scholar]

- Calvo, M.; Gramont, M. Currency Substitution in Developing Countries: An Introduction; Working Paper 92/40; International Monetary Fund: Washington, DC, USA, 1992. [Google Scholar]

- Calvo, G.; Végh, C. From currency substitution to dollarization and beyond: Analytical and policy issues. In Money, Exchange Rates, Output by G. Calvo; MIT Press: Cambridge, MA, USA, 1996; pp. 153–175. [Google Scholar]

- Crowe, C.; Meade, E. Central bank independence and transparency: Evolution and effectiveness. Eur. J. Political Econ. 2008, 24, 763–777. [Google Scholar] [CrossRef] [Green Version]

- Garriga, A.; Rodriguez, C. More effective than we thought: Central bank independence and inflation in developing countries. Econ. Model. 2020, 85, 87–105. [Google Scholar] [CrossRef]

- Woolley, J. Political factors in monetary policy. In The Political Economy of Monetary Policy: National and International Aspects; Hodgman, D.R., Ed.; Available online: https://www.bostonfed.org/-/media/Documents/conference/26/conf26.pdf#page=180 (accessed on 15 June 2021).

- Mauro, M.; Romeu, R.; Binder, M.; Zaman, M. A Modern History of Fiscal Prudence and Profligacy; Working Paper 13/5; International Monetary Fund: Washington, DC, USA, 2013. [Google Scholar]

- Reinhart, C.; Rogoff, K. This Time is Different: Eight Centuries of Financial Folly; Princeton University Press: Princeton, NJ, USA, 2009. [Google Scholar]

| i | |||||

| 100% | |||||

| −14% | 100% | ||||

| 2% | −1% | 100% | |||

| i | 6% | −2% | 66% | 100% | |

| 17% | −21% | 3% | 0% | 100% |

| Correlation | Inflation and Interest Rates | Inflation and Primary Balance |

|---|---|---|

| Discretionary regimes | 88% | 23% |

| Inflation targeting (IT) | 40% | 8% |

| Exchange rate targets (ERTs) | 51% | 15% |

| Euro zone countries | 87% | 1% |

| Poorly structured monetary policy | 28% | −15% |

| Mixed targets | 85% | −30% |

| Monetary targets (MTs) | 75% | −16% |

| Correlation | S1 | S2 | Global |

|---|---|---|---|

| Inflation/primary balance | 5% | 2% | 2% |

| Inflation/public debt | −1% | −5% | −1% |

| Inflation/short-term interest rate | 90% | 59% | 66% |

| Reduced-Form VAR | |||||

| i | |||||

| Lag 1 | 0.818 *** | −0.652 *** | 0.241 *** | −0.120 | −0.903 |

| (0.012) | (0.099) | (0.064) | (0.086) | (0.872) | |

| Lag 1 | 0.000 | 0.950 *** | 0.011 *** | −0.007 | −0.017 |

| (0.001) | (0.005) | (0.003) | (0.005) | (0.046) | |

| Lag 1 | −0.004 | −0.121 *** | 0.238 *** | −0.026 | 0.262 |

| (0.004) | (0.030) | (0.020) | (0.026) | (0.268) | |

| Lag 1 i | 0.003 | −0.04 ** | 0.035 *** | 0.879 *** | 1.905 *** |

| (0.002) | (0.017) | (0.011) | (0.014) | (0.147) | |

| Lag 1 | 0.000 | 0.003 | 0.000 | −0.010 *** | 0.313 *** |

| (0.000) | (0.003) | (0.002) | (0.002) | (0.022) | |

| Contemporaneous coefficients | |||||

| i | |||||

| 1 | 1.33 *** | −0.352 *** | −0.506 *** | 1.758 | |

| (0.157) | (0.098) | (0.139) | (1.184) | ||

| 0 | 1 | 0.229*** | −0.043 * | −0.148 | |

| (0.012) | (0.018) | (0.156) | |||

| 0 | 0 | 1 | 0.151 *** | −0.795 *** | |

| (0.028) | (0.239) | ||||

| i | 0 | 0 | 0 | 1 | −5.789 *** |

| (0.168) | |||||

| 0 | 0 | 0 | 0 | 1 | |

| i | |||||

| Lag 1 | 1.7114 | −0.8006 | 0.4023 | −0.4802 | −1.8017 |

| (2.0556) | (0.4349) | (0.3776) | (1.7175) | (1.2941) | |

| Lag 1 | −0.0277 | 0.9658 *** | −0.0108 | 0.0439 | 0.0446 |

| (0.0669) | (0.0272) | (0.0161) | (0.0664) | (0.1062) | |

| Lag 1 | −0.2952 | −0.0748 | 0.4232 * | 0.5708 | 0.5075 |

| (0.5773) | (0.1943) | (0.1873) | (0.7334) | (0.4981) | |

| Lag 1 i | 0.0054 | −0.0394 | 0.0232 | 0.7009 ** | 2.1820 * |

| (0.3989) | (0.0987) | (0.0873) | (0.2465) | (1.0212) | |

| Lag 1 | −0.0155 | 0.0052 | 0.0028 | 0.0197 | 0.3060 *** |

| (0.098) | (0.0169) | (0.0207) | (0.0444) | (0.0867) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bazzaoui, L.; Nagayasu, J. Is Inflation Fiscally Determined? Sustainability 2021, 13, 11306. https://doi.org/10.3390/su132011306

Bazzaoui L, Nagayasu J. Is Inflation Fiscally Determined? Sustainability. 2021; 13(20):11306. https://doi.org/10.3390/su132011306

Chicago/Turabian StyleBazzaoui, Lamia, and Jun Nagayasu. 2021. "Is Inflation Fiscally Determined?" Sustainability 13, no. 20: 11306. https://doi.org/10.3390/su132011306

APA StyleBazzaoui, L., & Nagayasu, J. (2021). Is Inflation Fiscally Determined? Sustainability, 13(20), 11306. https://doi.org/10.3390/su132011306