Green Finance as an Institutional Mechanism to Direct the Belt and Road Initiative towards Sustainability: The Case of China

Abstract

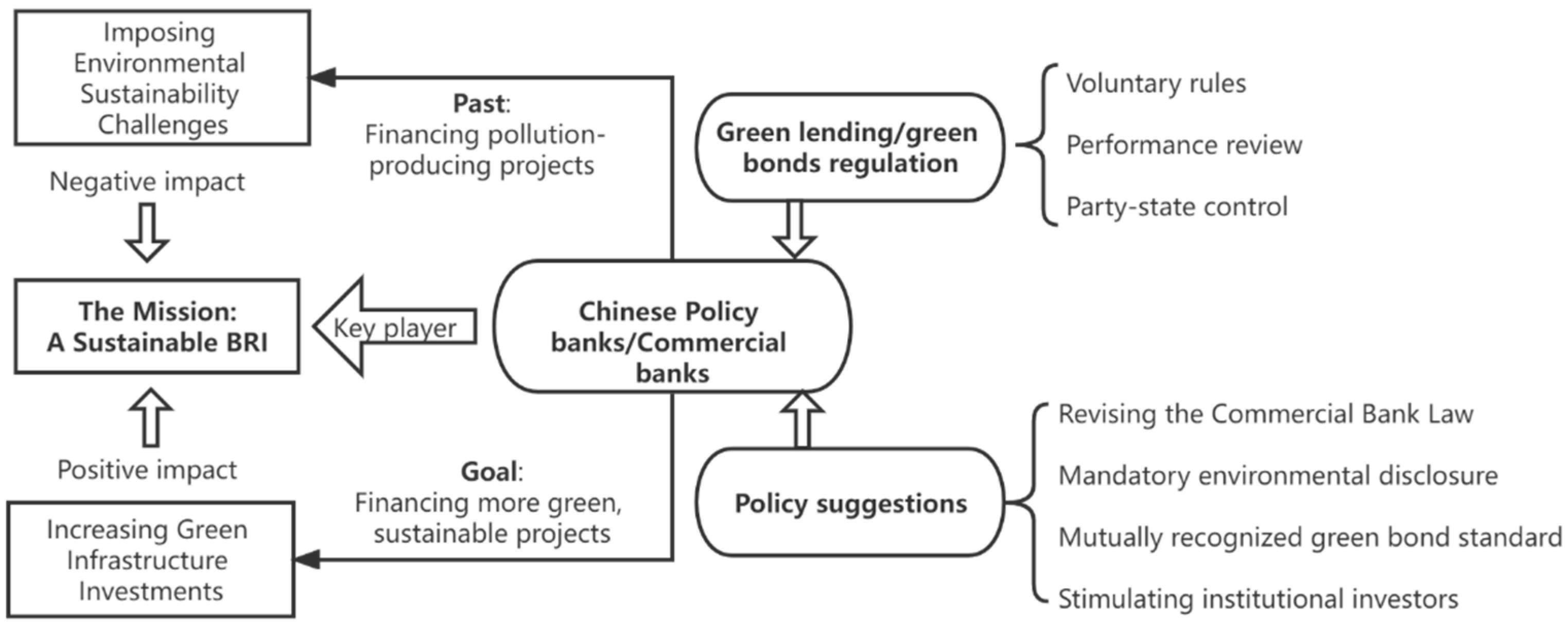

:1. Introduction

2. Materials and Methods

3. Literature Review

3.1. Tools for Facilitating the BRI’s Environmental Sustainability

3.2. Green Finance for Sustainability and Concerns about the ‘Greenness’ of Green Finance

4. Environmental Sustainability Challenges of China’s BRI Investments

- Carbon emission and pollution from fossil fuels: China has funded many coal projects in BRI countries [62]. The construction, operation, and maintenance of infrastructure will increase fossil fuel energy consumption [63]. Industrialization of the BRI countries will result in an increase in energy consumption [8]. Improvement in trade openness has a significantly positive effect on CO2 emissions [64]. Increased emission of greenhouse gases and air pollution could accelerate global warming and related problems such as ocean acidification and permafrost melting [65].

- Exploitation of natural resources: construction of infrastructure will inevitably lead to an increase in the consumption of raw materials such as sand, limestone, and fossil fuels, which are either non-renewable or exceed their natural renewal rate, thus depleting finite resources [31].

- Water pollution and shortage: as the BRI aims to enhance international trade, the increased use of seaborne transportation along the ‘21st Century Maritime Silk Road’ will expose oceans and coastal waters to increased pollution risks [66,67] due to bilge oil and motor fuel leakage, antifouling paint leaching, transfer of harmful aquatic organisms, etc. [68]. Of further concern is increased export-oriented industrialization (such as cement production) and consequent water pollution issues [69,70,71,72]. There has been criticism that China is exporting heavily polluting industries to its neighbors, for instance, after China’s Huaxin Cement invested in two cement plants near Tajikistan’s capital Dushanbe [32].

- Biodiversity loss: BRI projects that build in biodiversity hotspots, wilderness areas, and other critical conservation areas can lead to biological invasion and pose threats to local biodiversity [9,73,74,75]. Research has found that the building of highways in Indonesia’s Bornean forests will have significant negative impacts on rare species [76]. Other consequences include alien species invasion [9], habitat destruction, and overhunting [77].

5. Chinese Banks as Active Players in Facilitating a Green BRI

5.1. Lending Green Credits

5.2. Issuing Green Financial Bonds

5.3. Underwriting Onshore Green Bonds

- Underwriting a Chinese issuer’s onshore green bonds. This is the most common case, in which Chinese banks underwrite domestic enterprises’ green bonds. Typically, the proceeds from the sale of these bonds are invested in domestic green projects [129]. An example is the Exim Bank’s serving as lead underwriter for the State Grid Corp’s RMB 5 billion green mid-term note (a carbon-neutral bond) in 2021, the proceeds of which will be used to construct hydro-power plants on the Yalong and Yangtze Rivers [130].

- Underwriting a non-Chinese issuer’s onshore renminbi-denominated green bonds (‘green panda bonds’). The first mid-term green panda bond for BRI projects was issued in 2017 by China Merchants Port (based in Hong Kong) underwritten by ICBC, and raised RMB 2.5 billion for the construction and operation of ports in BRI countries.

5.4. Financing a Greener BRI in the Pandemic Era

6. Examining Green Finance Rules for Banks on the Green Transition of BRI

6.1. Applicable Laws and Regulations

6.2. Green Credits Lending for Overseas Projects

6.3. Green Financial Bonds Issuance and Reports on Use of Proceeds

6.4. Green Bond Standard

6.4.1. Convergence of Domestic Green Definitions

6.4.2. Alignment with International Green Bonds Standards

6.4.3. A Gap Concerning the Use of Proceeds

6.5. External Review of Green Financial Bonds

6.6. Evaluating Banks’ Green Performance

7. Policy Suggestions for Financing a Greener BRI

7.1. Introducing ‘Green’ Provisions to the Commercial Bank Law

7.2. Mandating Environmental Disclosure for Banks

7.3. Developing a Mutually Recognized Green Bond Standard

7.4. Stimulating Institutional Investors to Buy More Green Bonds

8. Conclusions and Final Remarks

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References and Note

- State Council of China. Action Plan on the Belt and Road Initiative. 30 March 2015. Available online: http://english.www.gov.cn/archive/publications/2015/03/30/content_281475080249035.htm (accessed on 22 January 2022).

- Belt and Road Portal. International Cooperation Profiles. Available online: https://eng.yidaiyilu.gov.cn/info/iList.jsp?cat_id=10076 (accessed on 20 December 2021).

- Ministry of Commerce. Annual Reports on Outward Foreign Direct Investments. Available online: http://www.mofcom.gov.cn/article/tongjiziliao/dgzz/ (accessed on 21 January 2022).

- Belt and Road Initiative. Projects. Available online: https://www.beltroad-initiative.com/projects/ (accessed on 24 December 2021).

- Organisation for Economic Co-Operation and Development. China’s Belt and Road Initiative in the Global Trade, Investment and Finance Landscape. In OECD Business and Finance Outlook 2018; OECD Publishing: Paris, France, 2018. [Google Scholar] [CrossRef]

- United Nations. Sustainability. Available online: https://www.un.org/en/academic-impact/sustainability (accessed on 11 May 2022).

- World Bank. Belt and Road Economics: Opportunities and Risks of Transport Corridors. pp. 111–112. Available online: https://openknowledge.worldbank.org/bitstream/handle/10986/31878/9781464813924.pdf (accessed on 21 January 2022).

- Liu, Y.Y.; Hao, Y. The Dynamic Links Between CO2 Emissions, Energy Consumption and Economic Development in The Countries Along “the Belt and Road”. Sci. Total Environ. 2018, 645, 674–683. [Google Scholar] [CrossRef] [PubMed]

- Liu, X.; Blackburn, T.M.; Song, T.J.; Li, X.P.; Huang, C.; Li, Y.M. Risks of Biological Invasion on The Belt sand Road. Curr. Biol. 2019, 29, 499–505. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Dollar, D. Seven Years into China’s Belt and Road. Available online: https://www.brookings.edu/blog/order-from-chaos/2020/10/01/seven-years-into-chinas-belt-and-road/ (accessed on 24 December 2021).

- Zhai, T.T. Environmental Challenges, Opportunities, and Policy Implications to Materialize China’s Green Belt and Road Initiative. Sustainability 2021, 13, 10428. [Google Scholar] [CrossRef]

- Ministry of Ecology and Environment, Ministry of Foreign Affairs, National Development and Reform Commission, and Ministry of Commerce. The Guidance on Promoting a Green Belt and Road. Available online: https://english.mee.gov.cn/Resources/Policies/policies/Frameworkp1/201706/t20170628_416864.shtml (accessed on 24 December 2021).

- Office of the Leading Group for Promoting the Belt and Road Initiative. The Belt and Road Initiative Progress, Contributions and Prospects. Available online: https://eng.yidaiyilu.gov.cn/zchj/qwfb/86739.htm (accessed on 24 December 2021).

- State Council. Report on the Work of the Government. 2022. Available online: http://english.www.gov.cn/premier/news/202203/12/content_WS622c96d7c6d09c94e48a68ff.html (accessed on 6 April 2022).

- Shen, S.; Chan, W. A comparative study of the Belt and Road Initiative and the Marshall plan. Palgrave Commun. 2018, 4, 32. [Google Scholar] [CrossRef]

- Liu, W.D.; Dunford, M. Inclusive globalization: Unpacking China’s Belt and Road Initiative. Area Dev. Policy 2016, 1, 323–340. [Google Scholar] [CrossRef]

- Zhou, W.F.; Esteban, M. Beyond Balancing: China’s Approach Towards the Belt and Road Initiative. J. Contemp. China 2018, 27, 487–501. [Google Scholar] [CrossRef]

- Gao, M.H.M. Globalization 5.0 Led by China: Powered by Positive Frames for BRI. In China’s Belt and Road Initiative; Zhang, W., Alon, I., Lattemann, C., Eds.; Palgrave Macmillan: London, UK, 2018. [Google Scholar] [CrossRef]

- Nedopil, C. Green finance for soft power: An analysis of China’s green policy signals and investments in the Belt and Road Initiative. Environ. Policy Gov. 2022, 32, 85–97. [Google Scholar] [CrossRef]

- Xiao, H.J.; Cheng, J.J.; Wang, X. Does the Belt and Road Initiative Promote Sustainable Development? Evidence from Countries along the Belt and Road. Sustainability 2018, 10, 4370. [Google Scholar] [CrossRef] [Green Version]

- Wei, Y. Integrating Sustainable Development Goals into the Belt and Road Initiative: Would It Be a New Model for Green and Sustainable Investment? Sustainability 2019, 11, 6991. [Google Scholar] [CrossRef] [Green Version]

- Jin, L. Synergies between the Belt and Road Initiative and the 2030 SDGs: From the perspective of development. Econ. Polit. Stud. 2018, 6, 278–292. [Google Scholar] [CrossRef]

- Boer, B. Greening China’s Belt and Road: Challenges for Environmental Law. Available online: https://ssrn.com/abstract=3420544 (accessed on 24 April 2022).

- Lorenzo, J.A.P. A Path Toward Sustainable Development Along the Belt and Road. J. Int. Econ. Law 2021, 24, 591–608. [Google Scholar] [CrossRef]

- Wang, H.K. Research on the Construction of Green Financial Legal Mechanism of The Belt and Road. J. Contemp. Financ. Res. 2019, 13, 53–63. [Google Scholar]

- Yuan, K. Green Financial Development and its Legal System Protection. Secur. Mark. Her. 2017, 1, 4–11. [Google Scholar]

- Hong, Y.R. International rules and insights on the operation mechanism of green bonds. Faxue 2017, 2, 124–134. [Google Scholar]

- Sun, Q.P.; Zhang, X.D.; Xu, X.Q.; Yang, Q.; Wang, S.J. Does the “Belt and Road Initiative” Promote the Economic Growth of Participating Countries? Sustainability 2019, 11, 5240. [Google Scholar] [CrossRef] [Green Version]

- Li, F.; Su, Y.; Xie, J.P.; Zhu, W.J.; Wang, Y.H. The Impact of High-Speed Rail Opening on City Economics along the Silk Road Economic Belt. Sustainability 2020, 12, 3176. [Google Scholar] [CrossRef] [Green Version]

- Abdulsalam, A.; Xu, H.L.; Ameer, W.; Abdo, A.L.-B.; Xia, J.J. Exploration of the Impact of China’s Outward Foreign Direct Investment (FDI) on Economic Growth in Asia and North Africa along the Belt and Road (B&R) Initiative. Sustainability 2021, 13, 1623. [Google Scholar] [CrossRef]

- Ascensão, F.; Fahrig, L.; Clevenger, A.P.; Corlett, R.T.; Jaeger, J.A.G.; Laurance, W.F.; Pereira, H.M. Environmental Challenges for the Belt and Road Initiative. Nat. Sustain. 2018, 1, 206–209. [Google Scholar] [CrossRef]

- Tracy, E.F.; Shvarts, E.; Simonov, E.; Babenko, M. China’s new Eurasian ambitions: The environmental risks of the Silk Road Economic Belt. Eurasian Geogr. Econ. 2017, 58, 56–88. [Google Scholar] [CrossRef] [Green Version]

- Liu, N.Y. Will China build a green Belt and Road in the Arctic? Rev. Eur. Comp. Int. Environ. Law 2018, 27, 55–62. [Google Scholar] [CrossRef]

- Li, Y.B.; Zhu, X.F. The 2030 Agenda for Sustainable Development and China’s Belt and Road Initiative in Latin America and the Caribbean. Sustainability 2019, 11, 2297. [Google Scholar] [CrossRef] [Green Version]

- Cheng, C.Y.; Ge, C.Z. Green development assessment for countries along the belt and road. J. Environ. Manag. 2020, 263, 110344. [Google Scholar] [CrossRef]

- Gray, K.R. Foreign Direct Investment and Environmental Impacts—Is the Debate Over? Rev. Eur. Community Int. Environ. Law 2003, 11, 306–313. [Google Scholar] [CrossRef]

- Coenen, J.; Bager, S.; Meyfroidt, P.; Newig, J.; Challies, E. Environmental Governance of China’s Belt and Road Initiative. Environ. Policy Gov. 2021, 31, 3–17. [Google Scholar] [CrossRef]

- Harlan, T. Green development or greenwashing? A political ecology perspective on China’s green Belt and Road. Eurasian Geogr. Econ. 2021, 62, 202–226. [Google Scholar] [CrossRef]

- Huang, Y.Y. Environmental risks and opportunities for countries along the Belt and Road: Location choice of China’s investment. J. Clean. Prod. 2019, 211, 14–26. [Google Scholar] [CrossRef]

- Jiang, X.H. Green Belt and Road Initiative Environmental and Social Standards: Will Chinese Companies Conform? IDS Bull. 2019, 50, 68. [Google Scholar] [CrossRef]

- Wang, H. China’s Approach to the Belt and Road Initiative: Scope, Character and Sustainability. J. Int. Econ. Law 2019, 22, 29–55. [Google Scholar] [CrossRef] [Green Version]

- Zhang, D.Y.; Zhang, Z.W.; Managi, S. A bibliometric analysis on green finance: Current status, development, and future directions. Financ. Res. Lett. 2019, 29, 425–430. [Google Scholar] [CrossRef]

- Berrou, R.; Ciampoli, N.; Marini, V. Defining Green Finance: Existing Standards and Main Challenges. In The Rise of Green Finance in Europe: Opportunities and Challenges for Issuers, Investors and Marketplaces; Migliorelli, M., Dessertine., P., Eds.; Palgrave Macmillan: London, UK, 2019; pp. 34–35. [Google Scholar]

- G20 Green Finance Study Group. G20 Green Finance Synthesis Report. 2016. Available online: http://www.g20.utoronto.ca/2016/green-finance-synthesis.pdf (accessed on 26 April 2022).

- Ren, X.D.; Shao, Q.L.; Zhong, R.Y. Nexus between green finance, non-fossil energy use, and carbon intensity: Empirical evidence from China based on a vector error correction model. J. Clean. Prod. 2020, 277, 122844. [Google Scholar] [CrossRef]

- Wang, F.S.; Cai, W.X.; Elahi, E. Do Green Finance and Environmental Regulation Play a Crucial Role in the Reduction of CO2 Emissions? An Empirical Analysis of 126 Chinese Cities. Sustainability 2021, 13, 13014. [Google Scholar] [CrossRef]

- Chen, X.; Chen, Z.G. Can Green Finance Development Reduce Carbon Emissions? Empirical Evidence from 30 Chinese Provinces. Sustainability 2021, 13, 12137. [Google Scholar] [CrossRef]

- Zhang, W.J.; Hong, M.Y.; Li, J.; Li, F.H. An Examination of Green Credit Promoting Carbon Dioxide Emissions Reduction: A Provincial Panel Analysis of China. Sustainability 2021, 13, 7148. [Google Scholar] [CrossRef]

- Fatica, S.; Panzica, R. Green bonds as a tool against climate change? Bus. Strategy Environ. 2021, 30, 2688–2701. Available online: https://op.europa.eu/en/publication-detail/-/publication/c6949012-fed7-11ea-b44f-01aa75ed71a1/language-en (accessed on 26 April 2022). [CrossRef]

- Cui, H.R.; Wang, R.Y.; Wang, H.R. An evolutionary analysis of green finance sustainability based on multi-agent game. J. Clean. Prod. 2020, 269, 121799. [Google Scholar] [CrossRef]

- Falcone, P.M. Environmental regulation and green investments: The role of green finance. Int. J. Green Econ. 2020, 14, 159–173. [Google Scholar] [CrossRef]

- GOH, A. Sustainable Green Finance towards a Green Belt and Road. Asian J. Int. Law 2021, 11, 245–252. [Google Scholar] [CrossRef]

- Jian, J.H.; Fan, X.J.; Zhao, S.Y. The Green Incentives and Green Bonds Financing under the Belt and Road Initiative. Emerg. Mark. Financ. Trade 2022, 58, 1430–1440. [Google Scholar] [CrossRef]

- European Commission. Defining “Green” in the Context of Green Finance. Final Report. 2017. Available online: https://ec.europa.eu/environment/enveco/sustainable_finance/pdf/studies/Defining%20Green%20in%20green%20finance%20-%20final%20report%20published%20on%20eu%20website.pdf (accessed on 26 April 2022).

- Nedopil, C.; Dordi, T.; Weber, O. The Nature of Global Green Finance Standards—Evolution, Differences, and Three Models. Sustainability 2021, 13, 3723. [Google Scholar] [CrossRef]

- Freeburn, L.; Ramsay, I. Green bonds: Legal and Policy Issues. Cap. Mark. Law J. 2020, 15, 418–442. [Google Scholar] [CrossRef]

- Saravade, V.; Chen, X.X.; Weber, O.; Song, X.Z. Impact of regulatory policies on green bond issuances in China: Policy lessons from a top-down approach. Clim. Policy 2022. [Google Scholar] [CrossRef]

- Dorfleitner, G.; Braun, D. Fintech, Digitalization and Blockchain: Possible Applications for Green Finance. In The Rise of Green Finance in Europe: Opportunities and Challenges for Issuers, Investors and Marketplaces; Migliorelli, M., Dessertine, P., Eds.; Palgrave Macmillan: London, UK, 2019; pp. 208–209. [Google Scholar]

- High-Level Expert Group on Sustainable Finance (HLEG). Financing a Sustainable European Economy. 2018. Available online: https://ec.europa.eu/info/sites/default/files/180131-sustainable-finance-final-report_en.pdf (accessed on 26 April 2022).

- Schiereck, D.; Friede, G.; Bassen, A. Financial Performances of Green Securities. In The Rise of Green Finance in Europe: Opportunities and Challenges for Issuers, Investors and Marketplaces; Migliorelli, M., Dessertine, P., Eds.; Palgrave Macmillan: London, UK, 2019; pp. 104–105. [Google Scholar]

- Bachelet, M.J.; Becchetti, L.; Manfredonia, S. The Green Bonds Premium Puzzle: The Role of Issuer Characteristics and Third-Party Verification. Sustainability 2019, 11, 1098. [Google Scholar] [CrossRef] [Green Version]

- Boston University Global Development Policy Center. China’s Global Energy Finance. Available online: https://www.bu.edu/cgef/#/all/EnergySource/Coal (accessed on 24 December 2021).

- Zhang, N.; Liu, Z.; Zheng, X.M.; Xue, J.J. Carbon Footprint of China’s Belt and Road. Science 2017, 357, 1107. [Google Scholar] [CrossRef]

- Chen, F.Z.; Jiang, G.H.; Kitila, G.M. Trade Openness and CO2 Emissions: The Heterogeneous and Mediating Effects for the Belt and Road Countries. Sustainability 2021, 13, 1958. [Google Scholar] [CrossRef]

- Yang, H.; Flower, R.J.; Thompson, J.R. Arctic at Risk from Vast Belt and Road Development. Nature 2019, 570, 446. [Google Scholar] [CrossRef] [PubMed]

- OECD. The Environmental Effects of Freight. 1997. Available online: https://www.oecd.org/environment/envtrade/2386636.pdf (accessed on 24 December 2021).

- Turschwell, M.P.; Brown, C.J.; Pearson, R.M.; Connolly, R.M. China’s Belt and Road Initiative: Conservation opportunities for threatened marine species and habitats. Mar. Policy 2020, 112, 103791. [Google Scholar] [CrossRef]

- Trozzi, C.; Vaccaro, R. Environmental Impact of Port Activities. In Maritime Engineering and Ports II; Brebbia, C.A., Olivella, J., Eds.; WIT Press: Ashurst Lodge, UK, 2000; p. 153. [Google Scholar]

- Ighalo, J.O.; Adeniyi, A.G. A perspective on environmental sustainability in the cement industry. Waste Dispos. Sustain. Energy 2020, 2, 161–164. [Google Scholar] [CrossRef]

- Sesugh, A.; Idowu, O.E.; Titus, A.; Zack, A.; Mavis, O.; Joseph, T. Physicochemical and heavy metal analysis of well water obtained from selected settlements around Dangote cement factory in Gboko, Nigeria. ChemSearch J. 2019, 10, 94–99. [Google Scholar]

- Etim, M.A.; Babaremu, K.; Lazarus, J.; Omole, D. Health Risk and Environmental Assessment of Cement Production in Nigeria. Atmosphere 2021, 12, 1111. [Google Scholar] [CrossRef]

- Alimbaev, T.; Mazhitova, Z.; Beksultanova, C.; Kyzy, N.T. Activities of mining and metallurgical industry enterprises of the Republic of Kazakhstan: Environmental problems and possible solutions. E3S Web Conf. 2020, 175, 14019. [Google Scholar] [CrossRef]

- Lechner, L.A.M.; Chan, F.K.S.; Campos-Arceiz, A. Biodiversity Conservation Should Be a Core Value of China’s Belt and Road Initiative. Nat. Ecol. Evol. 2018, 2, 408–409. [Google Scholar] [CrossRef] [PubMed]

- Hughes, A.C. Understanding and minimizing environmental impacts of the Belt and Road Initiative. Conserv. Biol. 2019, 33, 883–894. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Bohnett, E.; Coulibaly, A.; Hulse, D.; Hoctor, T.; Ahmad, B.; Li, A.; Lewison, R. Corporate responsibility and biodiversity conservation: Challenges and opportunities for companies participating in China’s Belt and Road Initiative. Environ. Conserv. 2022, 49, 42–52. [Google Scholar] [CrossRef]

- Alamgir, M.; Campbell, M.J.; Sloan, S.; Suhardiman, A.; Supriatna, J.; Laurance, W.F. High-risk infrastructure projects pose imminent threats to forests in Indonesian Borneo. Sci. Rep. 2019, 9, 140. [Google Scholar] [CrossRef]

- Clements, G.R.; Lynam, A.J.; Gaveau, D.; Yap, W.L.; Lhota, S.; Goosem, M.; Laurance, S.; Laurance, W.F. Where and How Are Roads Endangering Mammals in Southeast Asia’s Forests? PLoS ONE 2014, 9, 115376. [Google Scholar] [CrossRef] [Green Version]

- Ma, X.Y.; Gallagher, K.P. Who Funds Overseas Coal Plants? The Need for Transparency and Accountability. Available online: https://www.bu.edu/gdp/files/2021/07/GCI_PB_008_FIN-1.pdf (accessed on 24 December 2021).

- Zhou, L.H.; Gilbert, S.; Wang, Y.; Cabré, M.M.; Gallagher, K.P. Moving the Green Belt and Road Initiative: From Words to Actions; Working Paper; World Resources Institute: Washington, DC, USA, 2018; Available online: https://www.bu.edu/gdp/files/2018/11/GDP-and-WRI-BRI-MovingtheGreenbelt.pdf (accessed on 24 December 2021).

- Schonhardt, S. What China’s Coal Phaseout Means for the World. 27 September 2021. Available online: https://www.eenews.net/articles/what-chinas-coal-phaseout-means-for-the-world/ (accessed on 24 December 2021).

- Refinitiv. BRI Connect: An Initiative in Numbers. 2019. Available online: https://www.refinitiv.com/content/dam/marketing/en_us/documents/reports/refinitiv-zawya-belt-and-road-initiative-report-2019.pdf (accessed on 24 December 2021).

- Han, J.Y.; Nedopil Wang, C. China’s Coal Investments Phase-Out in BRI Countries—Bangladesh Case. 2021. Available online: https://greenfdc.org/chinas-coal-investments-phase-out-in-bri-countries-bangladesh-case/?cookie-state-change=1634610748232 (accessed on 24 December 2021).

- Ebrahim, Z.T. Scrapping Imported Coal Projects, Pakistan Fails to Let Go of Local Lignite. 23 December 2020. Available online: https://chinadialogue.net/en/climate/scrapping-imported-coal-projects-pakistan-fails-to-let-go-of-local-lignite/ (accessed on 24 December 2021).

- Nedopil Wang, C. Coal Phase-Out in the Belt and Road Initiative (BRI): An Analysis of Chinese-Backed Coal Power from 2014–2020. June 2021. Available online: https://greenfdc.org/wp-content/uploads/2021/06/Christoph_NEDOPIL_Wang_2021_Coal-phase-out-in-the-Belt-and-Road-Initiative-BRI_Fin.pdf (accessed on 24 December 2021).

- Leandro, F.J.B.S.; Duarte, P.A.B. The Belt and Road Initiative: An Old Archetype of a New Development Model, 1st ed.; Palgrave Macmillan: London, UK, 2020; p. 183. [Google Scholar]

- Putten, F.V.D.; Martin, X.X. China’s Infrastructure Investment & Environmental Sustainability. 24 June 2020. Available online: https://www.clingendael.org/publication/chinas-infrastructure-investment-environmental-sustainability (accessed on 24 December 2021).

- Xi Focus: China to Stop Building New Coal-Fired Power Projects Abroad. Available online: http://www.news.cn/english/2021-09/22/c_1310201218.htm (accessed on 24 December 2021).

- U.S.-China Joint Glasgow Declaration on Enhancing Climate Action in the 2020s. Available online: https://www.state.gov/u-s-china-joint-glasgow-declaration-on-enhancing-climate-action-in-the-2020s/ (accessed on 16 January 2022).

- UNCTAD. From Recovery to Resilience: The Development Dimension. Available online: https://unctad.org/system/files/official-document/tdr2021_part2_en.pdf (accessed on 16 January 2022).

- World Economic Forum. Advancing the Green Development of the Belt and Road Initiative: Harnessing Finance and Technology to Scale Up Low-Carbon Infrastructure. Available online: https://www3.weforum.org/docs/WEF_Advancing_the_Green_Development_of_the_Belt_and_Road_Initiative_2022.pdf (accessed on 16 January 2022).

- National Energy Administration. Qingdao Initiative for BRI Energy Cooperation Was Launched. Available online: http://www.nea.gov.cn/2021-10/19/c_1310254540.htm (accessed on 24 December 2021).

- State Council of China. Action Plan to Peak Carbon Emissions before 2030. Available online: http://english.www.gov.cn/policies/latestreleases/202110/26/content_WS6178023cc6d0df57f98e3d5c.html (accessed on 24 December 2021).

- Yue, M.D.; Nedopil Wang, C. Brief: Public Debt in the Belt and Road Initiative (BRI): How COVID-19 has Accelerated an On-going Problem of China’s Lending. pp. 4–5. Available online: https://greenfdc.org/wp-content/uploads/2020/12/2020_China_Debt_Belt_and_Road_BRI-1.pdf (accessed on 24 December 2021).

- How Much Money Has the Silk Road Fund Contributed to BRI During Six Years? Available online: https://www.sohu.com/a/427216384_731021 (accessed on 24 December 2021).

- ‘Big Four’ Chinese Commercial Banks Are: The Industrial & Commercial Bank of China, the China Construction Bank, the Agricultural Bank of China, and the Bank of China, as Ranked by Asset Size in 2020. Available online: https://corporatefinanceinstitute.com/resources/careers/companies/top-banks-in-china/ (accessed on 16 May 2022).

- ICBC Standard Bank, Oxford Economics. Belt and Road Interim Report: Tracking Evolving Scope, Discovering Expanding Opportunities. pp. 18–19. Available online: https://v.icbc.com.cn/userfiles/Resources/ICBC/haiwai/StandardBank/Download/2019/InauguralWhitepapers3.pdf (accessed on 24 December 2021).

- Yeung, G. Chinese State-Owned Commercial Banks in Reform: Inefficient and Yet Credible and Functional? J. Chin. Gov. 2021, 6, 198–231. [Google Scholar] [CrossRef]

- Harper Ho, V. Sustainable Finance & China’s Green Credit Reforms: A Test Case for Bank Monitoring of Environmental Risk. Cornell Int. Law J. 2018, 51, 609–681. [Google Scholar]

- For Example, in 2017, the Erstwhile China Banking Regulatory Commission Released a ‘Guiding Opinion on Regulating Banking Services for Enterprises Heading Overseas and Strengthening Risk Prevention and Control’, Requiring Banks to Vigorously Implement the BRI Strategy, Provide High-Quality Financial Services to Enterprises Heading Overseas. Available online: http://www.scio.gov.cn/xwfbh/xwbfbh/wqfbh/35861/36645/xgzc36651/Document/1551306/1551306.htm (accessed on 16 May 2022).

- Bank of China. Bank of China’s Action Plan for Carbon Neutrality. Available online: https://www.boc.cn/aboutboc/bi1/202109/t20210924_20085963.html (accessed on 24 December 2021).

- Early, C. How China Shapes the World’s Coal. Available online: https://www.bbc.com/future/article/20211028-how-chinas-climate-decisions-affect-the-world (accessed on 24 May 2021).

- Nedopil Wang, C. China Belt and Road Initiative (BRI) Investment Report H1 2021. Available online: https://greenfdc.org/wp-content/uploads/2021/07/21_07_22_BRI-Investment-Report-H1-2021.pdf (accessed on 21 January 2022).

- The Export-Import Bank of China. White Paper on Green Finance. 2016. Available online: http://english.eximbank.gov.cn/News/WhitePOGF/201807/P020180718416279996548.pdf (accessed on 24 December 2021).

- Jin, J.D.; Ma, X.Y.; Gallagher, K.P. China’s Global Development Finance: A Guidance Note for Global Development Policy Center Databases. 2018, pp. 3–4. Available online: https://www.bu.edu/gdp/files/2018/07/Coding-Manual-.pdf (accessed on 24 December 2021).

- There Is Currently no Official Listing of Those Overseas Projects. For a Non-Official List of Projects, See the Database Compiled by Global Development Policy Center of Boston University. Available online: https://www.bu.edu/gdp/chinas-overseas-development-finance/ (accessed on 24 December 2021).

- The Export-Import Bank of China. White Paper on Green Finance and Social Responsibility. 2019; pp. 19–21. Available online: http://www.eximbank.gov.cn/info/WhitePOGF/202001/P020200115377992690034.pdf (accessed on 24 December 2021).

- Boston University Global Development Policy Center. China’s Global Energy Finance. Hydropower. Available online: https://www.bu.edu/cgef/#/all/EnergySource/Hydropower (accessed on 7 April 2022).

- Chinese Bank to Issue Loans for Hydropower Development on Nam Ou. Available online: https://wle-mekong.cgiar.org/chinese-bank-to-issue-loans-for-hydropower-development-on-nam-ou/# (accessed on 24 December 2021).

- ICBC Lead Arranger to Finance Dubai’s Solar Power Project. Available online: https://www.reuters.com/article/icbc-emirates-power-idUSL8N1RS0OV (accessed on 24 December 2021).

- Clifford Chance Advises Lenders on Project Financing for World’s Largest Solar Power Project. Available online: https://www.cliffordchance.com/news/news/2021/01/clifford-chance-advises-lenders-on-project-financing-for-world-s.html (accessed on 24 December 2021).

- International Capital Market Association. Green Bond Principles-Voluntary Process Guidelines for Issuing Green Bonds. Available online: https://www.icmagroup.org/assets/documents/Regulatory/Green-Bonds/Green-Bonds-Principles-June-2018-270520.pdf (accessed on 24 December 2021).

- Meng, A.X.R.; Xie, W.H.; Shao, H.; Shang, J. China Green Bond Market Report 2020. pp. 4–5. Available online: https://www.climatebonds.net/files/reports/cbi_china_sotm_2021_06c_final_0.pdf (accessed on 24 December 2021).

- Climate Bonds Initiative. China, Green Bonds & Emerging Markets: Leveraging Private Capital; Opportunities Along with the Belt & Road Initiative. Available online: https://www.climatebonds.net/2017/09/china-green-bonds-emerging-markets-leveraging-private-capital-opportunities-along-belt-road (accessed on 24 December 2021).

- Exim Bank Successfully Issued RMB 5 Billion Green Financial Bonds. Available online: https://www.stcn.com/kuaixun/cj/202112/t20211224_4010006.html (accessed on 24 December 2021).

- Data Sources from the Shanghai Stock Exchange (SSE). Available online: http://www.sse.com.cn/assortment/bonds/listing/ (accessed on 24 December 2021).

- European Investment Bank. Climate Awareness Bonds. Available online: https://www.eib.org/en/investor_relations/cab/index.htm# (accessed on 24 December 2021).

- First Green Financial Bond Issued in China. Available online: http://www.gov.cn/xinwen/2016-02/04/content_5039057.htm (accessed on 24 December 2021).

- Exim Bank Issued Its First Bond Connect Green Financial Bond. Available online: https://www.cdmfund.org/19228.html (accessed on 24 December 2021).

- Yiu, E. Bond Connect: Is the Southbound Link the Game-Changing Bonanza That Banks and Investors Have Been Waiting For? 2021. Available online: https://www.scmp.com/business/companies/article/3149051/southbound-link-game-changer-will-boost-hong-kong-bond-market (accessed on 24 December 2021).

- A ‘Reg S’ Offering Refers to the Offering of Debt or Equity Securities Solely in Non-U.S. Countries. The Regulation S Is a Safe Harbor Rule, under Which a Security Offering and Sale Made in Good Faith by an Issuer Outside of the United States Need Not Be Registered under the Securities Act of 1933. Available online: https://www.sec.gov/rules/final/33-7505.htm (accessed on 16 May 2022).

- China Development Bank (HK) Debuts First International Green Bond. Available online: https://www.financeasia.com/article/china-development-bank-hk-debuts-first-international-green-bond/472394 (accessed on 24 December 2021).

- The Economist Corporate Network. BRI beyond 2020 Partnerships for Progress and Sustainability along the Belt and Road. Available online: https://www.bakermckenzie.com/-/media/files/insight/publications/2020/01/bribeyond2020_part_2.pdf (accessed on 24 December 2021).

- ICBC Lists Its Inaugural “Belt and Road” Climate Bond in Luxembourg. Available online: https://www.bourse.lu/pr-icbc-lists-belt-and-road-climate-bond (accessed on 23 December 2021).

- ICBC Successfully Issued the World’s First Green BRBR Bond. 2019. Available online: https://www.icbc.com.cn/icbc/en/newsupdates/icbc%20news/ICBCSuccessfullyIssuedtheWorldsFirstGreenBRBRBond.htm (accessed on 3 August 2021).

- China Construction Bank Celebrates Listing 2 Green Bonds on Nasdaq Dubai. Available online: https://global.chinadaily.com.cn/a/202008/19/WS5f3ce18ba3108348172615e3.html (accessed on 3 August 2021).

- Morgan Davis. BOC Lays Blue Foundation; Now Others Should Follow. Available online: https://www.globalcapital.com/asia/article/28mubssrshvmtp28yv2f4/tuesday-view/boc-lays-blue-foundation-now-others-should-follow (accessed on 23 December 2021).

- Jiang, X.Q. Green Bonds to Lift Industry, Energy. Available online: http://global.chinadaily.com.cn/a/202103/01/WS603c495ba31024ad0baabb9e.html (accessed on 23 December 2021).

- For a Description of the Duties of the Lead Underwriter on the Inter-Bank Market, See, National Association of Financial Market Institutional Investors, Announcement of the NAFMII on Issuing the Rules Governing the Intermediation Services for Debt Financing Instruments of Non-Financial Enterprises in the Inter-Bank Bond Market (2020 Version). Available online: http://nafmii.org.cn/ggtz/gg/202006/t20200612_80139.html (accessed on 16 May 2022).

- Climate Bonds Initiative. China Green Bond Market 2020. 2021, pp. 8–9. Available online: https://www.climatebonds.net/files/reports/cbi_china_sotm_2021_06d.pdf (accessed on 23 December 2021).

- Exim Bank Underwrites First Carbon-Neutral Bond. Available online: https://www.financialnews.com.cn/yh/sd/202103/t20210325_214881.html (accessed on 23 December 2021).

- Asia Securities Industry & Financial Markets Association. Foreign Institutional Investment in China: Various Access Channels. 2021. Available online: https://www.asifma.org/wp-content/uploads/2021/01/accessing-chinas-capital-markets-20-january-2021.pdf (accessed on 23 December 2021).

- Nedopil Wang, C. What is the Future of the Belt and Road Initiative (BRI) After COVID-19 and after the “Two Sessions”? A Health Silk Road? Available online: https://greenfdc.org/what-is-the-future-of-the-belt-and-road-initiative-bri-after-covid-19-and-after-the-two-sessions/ (accessed on 23 December 2021).

- Refinitiv. BRI Connect: An Initiative in Numbers (5th Edition) Fighting COVID-19 with Infrastructure. 2020, p. 5. Available online: https://www.refinitiv.com/content/dam/marketing/en_us/documents/reports/belt-and-road-initiative-in-numbers-issue-5.pdf (accessed on 7 April 2022).

- Hurley, J.; Morris, S.; Portelance, G. Examining the debt implications of the Belt and Road Initiative from a policy perspective. J. Infrastruct. Policy Dev. 2019, 3, 139–175. [Google Scholar] [CrossRef]

- Mouritz, F. Implications of the COVID-19 Pandemic on China’s Belt and Road Initiative. Connect. Q. J. 2020, 19, 115–124. [Google Scholar] [CrossRef]

- Bandiera, L.; Tsiropoulos, V. A Framework to Assess Debt Sustainability under the Belt and Road Initiative. J. Dev. Econ. 2020, 146, 102495. [Google Scholar] [CrossRef]

- Buckley, P.J. China’s Belt and Road Initiative and the COVID-19 Crisis. J. Int. Bus. Policy 2020, 3, 311–314. [Google Scholar] [CrossRef]

- Ogwang, T.; Vanclay, F. Resource-Financed Infrastructure: Thoughts on Four Chinese-Financed Projects in Uganda. Sustainability 2021, 13, 3259. [Google Scholar] [CrossRef]

- Nedopil, C. China’s Investments in the Belt and Road Initiative (BRI) in 2020: A Year of COVID-19. pp. 4–5. Available online: https://greenfdc.org/wp-content/uploads/2021/01/China-BRI-Investment-Report-2020.pdf (accessed on 24 December 2021).

- World Bank. China Economic Update. pp. 13–14. Available online: https://thedocs.worldbank.org/en/doc/7aa7a16968768ccb51f1818654d42561-0070012021/original/CEU-December-2021-ENG.pdf (accessed on 24 December 2021).

- Asian Development Bank. Meeting Asia’s Infrastructure Need. 2017, pp. xiv–xv. Available online: https://www.adb.org/sites/default/files/publication/227496/special-report-infrastructure.pdf (accessed on 24 December 2021).

- How Will the International COVID-19 Outbreak Impact the Belt and Road Initiative? Available online: https://oxfordbusinessgroup.com/news/how-will-international-covid-19-outbreak-impact-belt-and-road-initiative (accessed on 24 December 2021).

- Ding, Y.F.; Xiao, A. China’s Belt and Road Initiative in a Post-Pandemic World. Available online: https://www.invesco.com/invest-china/en/institutional/insights/chinas-belt-and-road-initiative-in-a-post-pandemic-world.html (accessed on 24 December 2021).

- Nedopil Wang, C. China Belt and Road Initiative (BRI) Investment Report 2021. Available online: https://greenfdc.org/wp-content/uploads/2022/02/Nedopil-2022_BRI-Investment-Report-2021.pdf (accessed on 7 April 2022).

- As of January of 2022, There Were Forty-One Financial Institutions Signed Up to the GIP. See, GIP. List of Membership. Available online: https://gipbr.net/Membership.aspx?type=12&m=3 (accessed on 16 January 2021).

- United Nations. The 17 Goals. Available online: https://sdgs.un.org/goals (accessed on 23 December 2021).

- Gip Expects Financial Institutions to Incorporate the Principles into Their Corporate Strategy and Decision-Making Processes, and to Report Regularly on Their Performance to the Gip Secretariat. 23 of the 39 Signatory Members Have Implemented Green Investment Policies That Limit the Financing of Coal Projects. See, Green Finance & Development Center. the Green Investment Principle (gip) for the Belt and Road Initiative. Available online: https://greenfdc.org/green-investment-principle-gip-belt-and-road-initiative/ (accessed on 23 December 2021).

- China Simplifies Bond Issuance in Hong Kong for Domestic Institutions. Available online: https://www.reuters.com/article/china-hongkong-bonds/china-simplifies-bond-issuance-in-hong-kong-for-domestic-institutions-idUKP8N2TB02C (accessed on 23 December 2021).

- NAFMII, Notice on Strengthening Self-Regulation on Information Disclosure of Green Financial Bonds in the Duration. Available online: http://www.nafmii.org.cn/ggtz/tz/202201/P020220117571784117412.pdf (accessed on 19 January 2022).

- Board of the International Organization of Securities Commissions. Sustainable Finance and the Role of Securities Regulators and IOSCO: Final Report. April 2020. Available online: https://www.iosco.org/library/pubdocs/pdf/IOSCOPD652.pdf (accessed on 23 December 2021).

- An Official English Translation of the 2021 Catalogue. Available online: http://www.pbc.gov.cn/goutongjiaoliu/113456/113469/4342400/2021091617180089879.pdf (accessed on 23 December 2021).

- Amstad, M.; He, Z. Chinese Bond Markets and Interbank Market. In The Handbook of China’s Financial System, 1st ed.; Amstad, M., Sun, G., Xiong, W., Eds.; Princeton University Press: Princeton, NJ, USA, 2020; pp. 105–150. [Google Scholar]

- These Include: PBOC. Notice of the PBOC on Revising Green Credit Statistical System, 2019; and CBIRC: Green Financing Statistical System, 2020.

- PBOC; NDRC; CSRC. Green Bond Endorsed Projects Catalogue. 2021. Available online: http://www.csrc.gov.cn/pub/newsite/zjhxwfb/xwdd/202104/t20210421_396410.html (accessed on 8 June 2021).

- Regulation (Eu) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on Sustainability-Related Disclosures in the Financial Services Sector. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A32019R2088 (accessed on 16 May 2022).

- ICMA. Guidance Handbook March 2020. Available online: https://www.icmagroup.org/assets/documents/Regulatory/Green-Bonds/Guidance-Handbook-March-2020-120320.pdf (accessed on 16 January 2022).

- CBI. Climate Bonds Initiative Green Bond Database Methodology. September 2020; p. 4. Available online: https://www.climatebonds.net/files/files/cbi-gb-methodology-061020.pdf (accessed on 16 January 2022).

- European Commission. Questions and Answers: European Green Bonds Regulation. Available online: https://ec.europa.eu/commission/presscorner/detail/en/QANDA_21_3406 (accessed on 16 January 2022).

- PBOC. Announcement on Matters Concerning the Issue of Green Financial Bonds on the Interbank Bond Market. Available online: http://www.gov.cn/xinwen/2015-12/22/content_5026636.htm (accessed on 16 May 2022).

- NAFMII. Guidelines on Non-Financial Enterprises Issuing Green Debt Financing Instruments. Available online: http://www.nafmii.org.cn/ggtz/gg/201703/P020170322639776098176.pdf (accessed on 16 May 2022).

- NDRC. Guidelines on Issuing Green Bonds. Available online: https://www.ndrc.gov.cn/xxgk/zcfb/tz/201601/t20160108_963561.html (accessed on 16 May 2022).

- Shenzhen Stock Exchange. Guidelines No. 1 of the SZSE on the Innovative Types of Corporate Bonds—Green Corporate Bond. 2021. Available online: https://www.amac.org.cn/businessservices_2025/ywfw_esg/esgzc/zczgsc/202112/P020211216596328224172.pdf (accessed on 16 May 2022).

- Shanghai Stock Exchange. Guidelines No. 2 on the Application of the Rules of the SSE Governing the Review of Offering and Listing—Specific Varieties of Corporate Bonds. Available online: http://www.sse.com.cn/lawandrules/sselawsrules/bond/review/c/c_20210713_5520720.shtml (accessed on 16 May 2022).

- CDB Hong Kong Branch Successfully Issued Offshore Green Bonds. Available online: https://www.cdmfund.org/29406.html (accessed on 16 January 2022).

- NAFMII; ICMA. Panda Bonds: Raising Finance in China’ Bond Market-Case Studies. Available online: https://www.icmagroup.org/assets/documents/About-ICMA/APAC/NAFMII-and-ICMA-English-version-PANDA-BONDS-Raising-Finance-in-Chinas-Bond-Market-case-studies-September-2021-230921.pdf (accessed on 16 January 2022).

- SynTao Green Finance. Green Bond Verification in China. 2017. Available online: https://www.cbd.int/financial/greenbonds/china-verification2017.pdf (accessed on 16 January 2022).

- Lin, M.T. China Embarks on Regulatory Reforms for International Green Bond Investors. Available online: https://cleanenergynews.ihsmarkit.com/research-analysis/china-embarks-on-regulatory-reforms-for-international-green-bo.html (accessed on 16 January 2022).

- CBIRC Recently Updated Its Rule Related to Regulatory Rating of Commercial Banks. See, CBIRC. Notice by the CBRC Regarding Issuing the Measures for the Regulatory Rating of Commercial Banks. Available online: http://www.gov.cn/zhengce/zhengceku/2021-09/23/content_5638812.htm (accessed on 16 January 2022).

- Central Bank Assesses Green Finance Performance of 24 Banks, Green Bonds to Expand in Second Half of 2021. Available online: https://finance.sina.com.cn/esg/investment/2021-07-08/doc-ikqcfnca5611534.shtml (accessed on 16 January 2022).

- Huang, T. Green Credit of Commercial Banks: The Implementation Paths and Legal Barriers. J. Zhejiang Univ. (Humanit. Soc. Sci.) 2021, 51, 95–110. [Google Scholar]

- Notice by the PBOC of the Request for Public Comments on the Proposal to Revise the Law of the People’s Republic of China on Commercial Banks (2020). Available online: https://www.financialnews.com.cn/jg/zc/202010/t20201016_203172.html (accessed on 16 May 2022).

- Gallagher, K.S.; Qi, Q. Policies Governing China’s Overseas Development Finance Implications for Climate Change. 2018. Available online: https://sites.tufts.edu/cierp/files/2018/03/CPL_ChinaOverseasDev.pdf (accessed on 27 April 2022).

- Sprinkle, G.B.; Maines, L.A. The benefits and costs of corporate social responsibility. Bus. Horiz. 2010, 53, 445–453. [Google Scholar] [CrossRef]

- European Banking Association. EBA Report on Management and Supervision of ESG Risks for Credit Institutions and Investment Firms. 2021. Available online: https://www.eba.europa.eu/sites/default/documents/files/document_library/Publications/Reports/2021/1015656/EBA%20Report%20on%20ESG%20risks%20management%20and%20supervision.pdf (accessed on 27 April 2022).

- ICBC. Reports on Green Finance. Available online: http://www.icbc-ltd.com/ICBCLtd/%E7%A4%BE%E4%BC%9A%E8%B4%A3%E4%BB%BB/%E7%BB%BF%E8%89%B2%E9%87%91%E8%9E%8D/ (accessed on 20 January 2022).

- Drafters of the Document Explain the First Batch of PBOC’s Green Finance Standards: Mandatory Disclosure for Four Types of Institutions. Available online: https://finance.sina.com.cn/roll/2021-08-20/doc-ikqciyzm2504582.shtml?cref=cj (accessed on 20 January 2022).

- SEC. The Enhancement and Standardization of Climate-Related Disclosures for Investors. SEC Proposed Rule. 2022. Available online: https://www.sec.gov/rules/proposed/2022/33-11042.pdf (accessed on 28 April 2022).

- Azarow, R.C.; Walsh, E.; Grey, S.; Nabhan, P. ESG and Banking: The Disclosure Debate. Bank. Law J. 2021, 138, 554–561. [Google Scholar]

- SEC. SEC Proposes Rules to Enhance and Standardize Climate-Related Disclosures for Investors. Available online: https://www.sec.gov/news/press-release/2022-46 (accessed on 28 April 2022).

- Wang, F.; Yang, S.Y.; Reisner, A.; Liu, N. Does Green Credit Policy Work in China? The Correlation between Green Credit and Corporate Environmental Information Disclosure Quality. Sustainability 2019, 11, 733. [Google Scholar] [CrossRef] [Green Version]

- Zhang, B.; Yang, Y.; Bi, J. Tracking the implementation of green credit policy in China: Top-down perspective and bottom-up reform. J. Environ. Manag. 2011, 92, 1321–1327. [Google Scholar] [CrossRef]

- Giudice, A.D.; Rigamonti, S. Does Audit Improve the Quality of ESG Scores? Evidence from Corporate Misconduct. Sustainability 2020, 12, 5670. [Google Scholar] [CrossRef]

- Gray, R.; Kouhy, R.; Lavers, S. Corporate social and environmental reporting: A review of the literature and a longitudinal study of UK disclosure. Account. Audit. Account. J. 1995, 8, 47–77. [Google Scholar] [CrossRef]

- Ghoul, S.E.; Guedhami, O.; Kwok, C.C.Y.; Mishra, D.R. Does corporate social responsibility affect the cost of capital? J. Bank. Financ. 2011, 35, 2388–2406. [Google Scholar] [CrossRef]

- Aintablian, S.; Mcgraw, P.A.; Roberts, G.S. Bank Monitoring and Environmental Risk. J. Bus. Financ. Account. 2007, 34, 389–401. [Google Scholar] [CrossRef]

- Miles, M.P.; Covin, J.G. Environmental Marketing: A Source of Reputational, Competitive, and Financial Advantage. J. Bus. Ethics 2000, 23, 299–311. [Google Scholar] [CrossRef]

- Jizi, M.I.; Salama, A.; Dixon, R.; Stratling, R. Corporate governance and corporate social responsibility disclosure: Evidence from the US banking sector. J. Bus. Ethics 2014, 125, 601–615. [Google Scholar] [CrossRef] [Green Version]

- Zhu, H. Common Ground Taxonomy: Consolidation of China and EU Green Definitions. Available online: https://www.senecaesg.com/insights/common-ground-taxonomy-consolidation-of-china-and-eu-green-definitions/ (accessed on 16 January 2022).

- CIB Research. Bank Green Finance Performance Evaluation Upgraded Again. Available online: http://pdf.dfcfw.com/pdf/H3_AP202007231393513711_1.pdf (accessed on 20 January 2022).

- Febi, W.; Schäfer, D.; Stephan, A.; Sun, C. The impact of liquidity risk on the yield spread of green bonds. Financ. Res. Lett. 2018, 27, 53–59. [Google Scholar] [CrossRef]

- Antoniuk, Y.; Leirvik, T. Climate Transition Risk and the Impact on Green Bonds. J. Risk Financ. Manag. 2021, 14, 597. [Google Scholar] [CrossRef]

- Annual Net Increase of RMB 750 Billion: Foreign Institutions Hold RMB 4 Trillion Bonds in Interbank Market. Available online: https://www.financialnews.com.cn/sc/zq/202201/t20220113_237326.html (accessed on 20 January 2022).

- State Administration of Foreign Exchange. PBOC & SAFE Remove QFII/RQFII Investment Quotas and Promote Further Opening-Up of China’s Financial Market. Available online: https://www.safe.gov.cn/en/2020/0507/1677.html (accessed on 20 January 2022).

- State Council of China. China to Extend Tax Incentives for Overseas Investors to Attract More Foreign Investment. Available online: http://english.www.gov.cn/premier/news/202110/27/content_WS61796625c6d0df57f98e4009.html (accessed on 20 January 2022).

{kind=link}

| Type | Issuing Authority | Effective Date | Name |

|---|---|---|---|

| Legislation | NPC | October 2018 | Circular Economy Promotion Law (2018 Amendment), art.45 |

| Energy Conservation Law (2018 Amendment), art.65 | |||

| General regulatory framework | CBRC, PBOC, MEP, CRSC, CIRC, NDRC, MOF | August 2016 | Guiding Opinions of Establishing the Green Financial System |

| CBIRC | December 2019 | Guiding Opinions of the CBIRC on Promoting the High-quality Development of Banking and Insurance Industries | |

| MEE, NDRC, PBOC, CBIRC, CSRC | October 2020 | Guiding Opinions of the MEE, the NDRC, the PBOC and Other Departments on Promoting the Investment and Financing in Response to Climate Change | |

| Green credit | CBRC | January 2012 | Green Credit Guidelines |

| July 2013 | Notice of the CBRC on Submission of Green Credit Statistics Form | ||

| June 2014 | Notice of the CBRC on Key Performance Indicators of Green Credit Implementation | ||

| September 2017 | Guiding Opinions of the CBRC on Regulating Banking Services for Enterprises Heading Overseas and Strengthening Risk Prevention and Control | ||

| Green financial bond | PBOC | December 2015 | Announcement on Matters Concerning the Issue of Green Financial Bonds on the Interbank Bond Market |

| March 2018 | Notice by the PBOC of Issues concerning Strengthening the Supervision and Administration of Green Financial Bonds in the Duration | ||

| March 2018 | Guidelines of Information Disclosure of Green Financial Bonds in the Duration | ||

| PBOC, CSRC | October 2017 | Guidelines for the Conduct of Assessment and Certification of Green Bonds (Interim) | |

| PBOC, NDRC, CSRC | April 2021 | Green Bond Endorsed Projects Catalogue (2021 Edition) | |

| Performance evaluation | CBA | December 2018 | Implementation Plan for Green Bank Evaluation in the Banking Sector of China (for Trial Implementation) |

| PBOC | May 2021 | Plan for the Green Finance Evaluation of Banking Financial Institutions |

| Market | Market Regulator | Bond Type | Issuance Regulator | Trading Venue |

|---|---|---|---|---|

| Interbank bond market | PBOC | Green financial bonds | PBOC | CIBM |

| Green enterprise bonds | NDRC | |||

| Green debt financing instruments (e.g., mid-term notes) | NAFMII | |||

| Exchange bond market | CSRC | Green corporate bonds | CSRC | SSE&SZSE |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, M.; Zhang, C.; Li, F.; Liu, Z. Green Finance as an Institutional Mechanism to Direct the Belt and Road Initiative towards Sustainability: The Case of China. Sustainability 2022, 14, 6164. https://doi.org/10.3390/su14106164

Zhang M, Zhang C, Li F, Liu Z. Green Finance as an Institutional Mechanism to Direct the Belt and Road Initiative towards Sustainability: The Case of China. Sustainability. 2022; 14(10):6164. https://doi.org/10.3390/su14106164

Chicago/Turabian StyleZhang, Meihui, Chi Zhang, Fenghua Li, and Ziyu Liu. 2022. "Green Finance as an Institutional Mechanism to Direct the Belt and Road Initiative towards Sustainability: The Case of China" Sustainability 14, no. 10: 6164. https://doi.org/10.3390/su14106164

APA StyleZhang, M., Zhang, C., Li, F., & Liu, Z. (2022). Green Finance as an Institutional Mechanism to Direct the Belt and Road Initiative towards Sustainability: The Case of China. Sustainability, 14(10), 6164. https://doi.org/10.3390/su14106164