Enforcing Double Materiality in Global Sustainability Reporting for Developing Economies: Reflection on Ghana’s Oil Exploration and Mining Sectors

Abstract

:1. Introduction

2. Literature Review

2.1. The Paris Agreement as Global Consensus for Climate Policy and the Emerging Green Financial System

2.2. The Essence of Sustainability Reporting: Double Materiality and Recognition of the External Costs

2.3. The Promise of ESG Investing and the Significance of Double Materiality in Practicing Corporate Governance for Sustainability

2.4. The Need for a Global Standard That Protects the Sustainability of Developing Countries

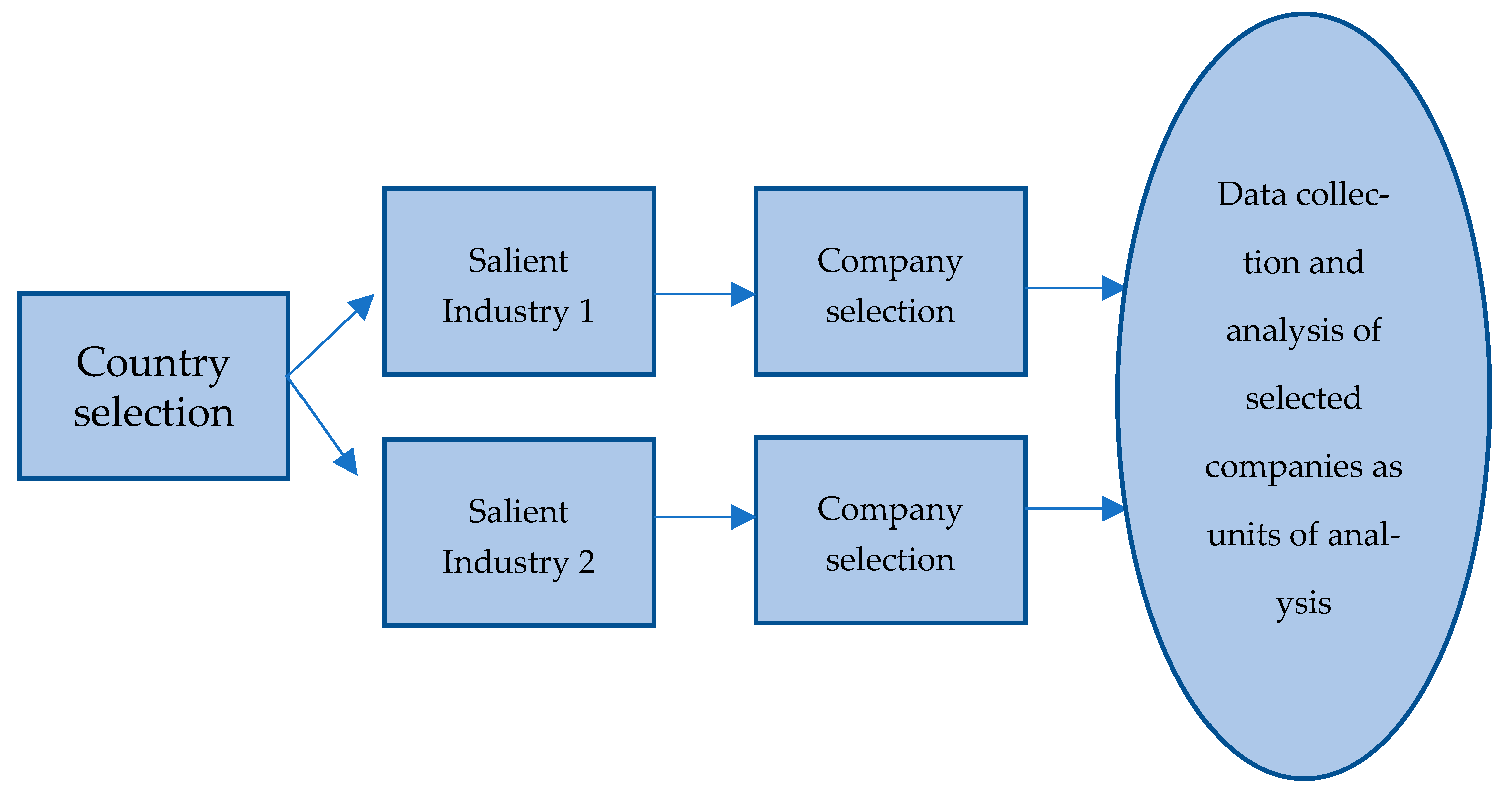

3. Methodology

3.1. Case Study Method

3.2. Industry Background

4. Results:

4.1. Overall Reporting and Governance Approach

4.2. Policy and Standard

4.3. Emission and Energy Disclosure

4.4. Overall Social and Environmental Sustainability Performance

5. Discussion

6. Conclusions

6.1. Concluding Remarks

6.2. Implications

6.3. Limitations and Future Studies

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

References

- Schumacher, K. Green investments need global standards and independent scientific review. Nature 2020, 584, 524–525. [Google Scholar] [CrossRef]

- Hörisch, J. The relation of COVID-19 to the UN sustainable development goals: Implications for sustainability accounting, management and policy research. Sustain. Account. Manag. Policy J. 2021, 12, 877–888. [Google Scholar] [CrossRef]

- Schaltegger, S. Sustainability learnings from the COVID-19 crisis. Opportunities for resilient industry and business development. Sustain. Account. Manag. Policy J. 2021, 12, 889–897. [Google Scholar] [CrossRef]

- IFAC. International Federation of Accountants. 2020. Available online: http://www.ifac.org/system/files/publications/files/2020-IFAC-Financial-Statements.pdf (accessed on 20 February 2022).

- IFRS Foundation. Consultation Paper on Sustainability Reporting. 2020. Available online: https://www.ifrs.org/content/dam/ifrs/project/sustainability-reporting/consultation-paper-on-sustainability-reporting.pdf (accessed on 20 February 2022).

- IFRS Foundation. International Sustainability Standards Board. 2022. Available online: https://www.ifrs.org/groups/international-sustainability-standards-board (accessed on 20 February 2022).

- Deloitte. The Challenge of Double Materiality. 2022. Available online: https://www2.deloitte.com/cn/en/pages/hot-topics/topics/climate-and-sustainability/dcca/thought-leadership/the-challenge-of-double-materiality.html (accessed on 30 June 2022).

- Jørgensen, S.; Mjos, A.; Pedersen, L. Sustainability reporting and approaches to materiality: Tensions and potential resolutions. Sustain. Account. Manag. Policy J. 2022, 13, 341–361. [Google Scholar] [CrossRef]

- Baumüller, J.; Sopp, K. Double materiality and the shift from non-financial to European sustainability reporting: Review, outlook and implications. J. Appl. Account. Res. 2022, 23, 8–28. [Google Scholar] [CrossRef]

- Lin, B.; Agyeman, S. Assessing Ghana’s carbon dioxide emissions through energy consumption structure towards a sustainable development path. J. Clean. Prod. 2019, 238, 117941. [Google Scholar] [CrossRef]

- Bose, S.; Khan, H.Z. Sustainable development goals (SDGs) reporting and the role of country-level institutional factors: An international evidence. J. Clean. Prod. 2022, 335, 130290. [Google Scholar] [CrossRef]

- Erin, O.A.; Bamigboye, O.A.; Oyewo, B. Sustainable development goals (SDG) reporting: An analysis of disclosure. J. Account. Emerg. Econ. 2022. [Google Scholar] [CrossRef]

- Rosati, F.; Faria, L.G.G. Addressing the SDGs in sustainability reports: The relationship with institutional factors. J. Clean. Prod. 2019, 215, 1312–1326. [Google Scholar] [CrossRef]

- Alexander, K.; Dhumale, R.; Eatwell, J. Global Governance of Financial Systems: The International Regulation of Systemic Ris; Oxford University Press: Oxford, NY, USA, 2006. [Google Scholar]

- Perry, J.; Nölke, A. The political economy of International Accounting Standards. Rev. Int. Political Econ. 2006, 13, 559–586. [Google Scholar] [CrossRef]

- Botzem, S.; Quack, S. (No) Limits to Anglo-American accounting? Reconstructing the history of the International Accounting Standards Committee: A review article. Account. Organ. Soc. 2009, 340, 988–998. [Google Scholar] [CrossRef]

- Humphrey, C.; Loft, A.; Woods, M. The global audit profession and the international financial architecture: Understanding regulatory relationships at a time of financial crisis. Account. Organ. Soc. 2009, 34, 810–825. [Google Scholar] [CrossRef]

- Ramanna, K. The International Politics of IFRS Harmonization. Account. Econ. Law. 2013, 3, 1–46. Available online: http://www.tinyurl.com/y453sjex (accessed on 8 February 2022). [CrossRef]

- Stiglitz, J.E. Lessons from the Global Financial Crisis of 2008. Seoul J. Econ. 2010, 23, 321–339. [Google Scholar]

- Stiglitz, J.E. The Globalization of Our Discontent, Chazen Global Insights. 2017. Available online: https://www8.gsb.columbia.edu/articles/chazen-global-insights/globalization-our-discontent (accessed on 2 February 2022).

- UNFCC. The Paris Agreement. United Nations Framework Convention on Climate Change. 2020. Available online: https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement (accessed on 2 February 2022).

- Guterres, A. Carbon Neutrality by 2050: The World’s Most Urgent Mission. 2020. Available online: https://www.un.org/sg/en/content/sg/articles/2020-12-11/carbon-neutrality-2050-theworld%E2%80%99s-most-urgent-mission (accessed on 20 April 2022).

- UNCTAD. Investment Policy Framework for Sustainable Development. 2015. Available online: https://investmentpolicy.unctad.org/investment-policy-framework (accessed on 20 February 2022).

- Carney, M. Building A Private Finance System for Net Zero: Priorities for Private Finance for COP26. 2021. Available online: https://emergingrisks.co.uk/building-a-private-finance-system-for-net-zero/ (accessed on 5 February 2022).

- TCFD. Recommendations of the Task Force on Climate-related Financial Disclosures. Task Force on Climate-Related Financial Disclosures. 2017. Available online: https://www.fsb-tcfd.org/recommendations/ (accessed on 20 February 2022).

- Europe, A. Follow-Up Paper: Interconnected Standards Setting for Corporate Reporting; Accountancy Europe: Brussels, Belgium, 2020. [Google Scholar]

- TCFD. Overview, Task Force on Climate-Related Financial Disclosures. 2021. Available online: https://www.fsb-tcfd.org/about/ (accessed on 20 February 2022).

- Adams, C.; Abhayawansa, S. Connecting the COVID-19 pandemic, environmental, social and governance (ESG) investing and calls for ‘harmonisation’ of sustainability reporting. Crit. Perspect. Account. 2021, 1, 102309. [Google Scholar] [CrossRef]

- Ritchie, H. Sector by Sector: Where Do Global Greenhouse Gas Emissions Come from? Available online: https://ourworldindata.org/ghg-emissions-by-sector (accessed on 5 February 2022).

- Hunt, C.; Weber, O.; Dordi, T. A comparative analysis of the anti-Apartheid and fossil fuel divestment campaign. J. Sustain. Financ. Invest. 2017, 7, 64–81. [Google Scholar] [CrossRef]

- Majoch, A.; Hoepner, A.; Hebb, T. Sources of Stakeholder Salience in the Responsible Investment Movement: Why Do Investors Sign the Principles for Responsible Investment? J. Bus. Ethics. 2017, 140, 723–741. [Google Scholar] [CrossRef]

- Friedman, M. The social responsibility of business is to increase its profits. The New York Times Magazine, 13 September 1970; 122–126. [Google Scholar]

- Ramanna, K. Friedman at 50: Is it still the social responsibility of business to increase profits? Calif. Manag. Rev. 2020, 62, 28–41. [Google Scholar] [CrossRef]

- Gray, R. Accountability, sustainability and the world’s largest corporations: Of CSR, chimeras, oxymorons and tautologies. In Corporate Responsibility: A Research Handbook; Haynes, K., Murray, A., Dillard, J., Eds.; Routledge: London, UK, 2012; pp. 151–166. [Google Scholar]

- Gray, R. Is accounting for sustainability actually accounting for sustainability … and how would we know? An exploration of narratives of organisations and the planet. Account. Organ. Soc. 2010, 35, 47–62. [Google Scholar] [CrossRef]

- Waldman, S. Shell Grappled with Climate Change 20 Years Ago. Documents Show, Scientific America. 2018. Available online: https://www.scientificamerican.com/article/shell-grappled-with-climate-change-20-years-ago-documents-show/ (accessed on 28 May 2021).

- Yuen, P.P.; Ng, A.W. Healthcare Financing and Sustainability In Good Health and Well-Being; Filho, W.L., Wall, T., Azul, A.M., Brandli, L., Özuyar, P.G., Eds.; Encyclopaedia of the UN Sustainable Development Goal; Springer: Cham, Switzerland, 2019; pp. 1–10. [Google Scholar]

- Sovacool, S.; Kim, J.; Yang, M. The hidden costs of energy and mobility: A global meta-analysis and research synthesis of electricity and transport externalities. Energy Res. Soc. Sci. 2021, 72, 101997. [Google Scholar] [CrossRef]

- Katz, D.; McIntosh, L. Corporate Governance Update: “Materiality” in America and Abroad; Harvard Law School Forum on Corporate Governance: Cambridge, MA, USA, May 2021; Available online: https://corpgov.law.harvard.edu/2021/05/01/corporate-governance-update-materiality-in-america-and-abroad/ (accessed on 5 February 2022).

- Adams, C.A.; Alhamood, A.; He, X.; Tian, J.; Wang, L.; Wang, Y. The Double-Materiality Concept: Application and Issue. 2021. Available online: https://dro.dur.ac.uk/33139/ (accessed on 2 January 2022).

- Ashford, N.A.; Hall, R.P. Technology, Globalization, and Sustainable Development: Transforming the Industrial State; Routledge: London, UK, 2019. [Google Scholar]

- Ng, A. Green Investing and Financial Services: ESG Investing for a Sustainable World. In The Palgrave Handbook of Global Sustainability; Springer: Berlin/Heidelberg, Germany, 2021; pp. 1–12. [Google Scholar] [CrossRef]

- Ng, A.; Nathwani, J.; Fu, J.; Zhou, H. Green financing for global energy sustainability: Pro-specting transformational adaptation beyond Industry 4.0. Sustain. Sci. Pract. Policy. 2021, 17, 377–390. [Google Scholar] [CrossRef]

- Tang, Y. Bumpy road leading to internationalization: A review of accounting development in China. Acc. Horiz. 2000, 14, 93–102. Available online: https://upload.news.esnai.com/2013/0509/1368083607642.pdf (accessed on 5 February 2022). [CrossRef]

- Sunder, S. Regulatory competition among accounting standards within and across international boundaries. J. Account. Public Policy 2002, 21, 219–234. [Google Scholar] [CrossRef]

- Bloomberg. Stranded Assets’ Risk Rising with Climate Action and $40 Oil. 2020. Available online: https://www.bloomberg.com/news/articles/2020-08-11/why-climate-action-40-oil-create-stranded-assets-quicktake (accessed on 28 May 2021).

- Shrivastava, P.; Zsolnai, L.; Wasieleski, D.; Stafford-Smith, M.; Walker, T.; Weber, O.; Krosinsky, C.; Oram, D. Finance and Management for the Anthropocene. Organ. Environ. 2019, 2, 26–40. [Google Scholar] [CrossRef]

- Smith, N.; Soonieus, R. How board members really feel about ESG, from deniers to true believers. In Harvard Business Review; Harvard Business Publishing: Cambridge, MA, USA, 2019; Available online: https://hbr.org/2019/04/how-board-members-really-feel-about-esg-from-deniers-to-true-believers (accessed on 5 February 2022).

- Kaplan, R.S.; Ramanna, K. How to fix ESG Reporting. In Harvard Business School Working Paper; Harvard Business Publishing: Cambridge, MA, USA, 2021; No. 22-005. [Google Scholar]

- Malik, A.; Egan, M.; Plessis, M.; Lenzen, M. Managing sustainability using financial accounting data: The value of input-output analysis. J. Clean. Prod. 2021, 293, 126128. [Google Scholar] [CrossRef]

- Serafeim, G. ESG: Hyperboles and reality. In Harvard Business School Working Paper; Harvard Business Publishing: Cambridge, MA, USA, 2021; No. 22-031. [Google Scholar]

- Bebbington, J.; Österblom, H.; Crona, B.; Jouffray, J.-B.; Larrinaga, C.; Russell, S.; Scholtens, B. Accounting and accountability in the Anthropocene. Account. Audit. Account. J. 2020, 33, 152–177. [Google Scholar] [CrossRef]

- Deegan, C. The accountant will have a central role in saving the planet … really? A reflection on ‘green accounting and green eyeshades twenty years later. Crit. Perspect. Account. 2013, 24, 448–458. [Google Scholar] [CrossRef]

- Cho, C.; Mäkelä, H. EAA Accounting Resources Centre, Can Accountants Save the World? Incorporating Sustainability in Accounting Courses and Curricula. Available online: https://arc.eaa-online.org/blog/can-accountants-save-world-incorporating-sustainability-accounting-courses-and-curricula (accessed on 5 February 2022).

- Charnock, R.; Thomson, I. Accounting and Climate Finance: Engaging with the Intergovernmental Panel on Climate Change. Soc. Environ. Account. J. 2020, 42, 1–4. [Google Scholar] [CrossRef]

- Bebbington, J.; Larrinaga, C.; Dwyer, B.; Thomson, I. Routledge Handbook of Environmental Account; Routledge: London, UK, 2021. [Google Scholar]

- Kaplan, R.S.; Ramanna, K. Accounting for climate change: The first rigorous approach to ESG reporting. In Harvard Business Review; Harvard Business Publishing: Cambridge, MA, USA, 2021; Available online: https://hbr.org/2021/11/accounting-for-climate-change (accessed on 20 February 2022).

- Els, F. MINING.COM. Available online: https://www.mining.com/featured-article/top-20-gold-producing-countries/ (accessed on 5 August 2021).

- Braithwaite, J. Responsive regulation and developing economies. World Dev. 2006, 34, 884–898. [Google Scholar] [CrossRef]

- Kumah, A. Sustainability and gold mining in the developing world. J. Clean. Prod. 2006, 14, 315–323. [Google Scholar] [CrossRef]

- Barma, N.; Kaiser, K.; Le, T.M. Rents to Riches? The Political Economy of Natural Resource-Led Development; World Bank Publications: Washington, DC, USA, 2012. [Google Scholar]

- Carroll, A.B.; Brown, J.; Buchholtz, A.K. Business and Society: Ethics, Sustainability, and Stakeholder Management; Cengage Learning: Boston, MA, USA, 2018. [Google Scholar]

- Cheng, Z.; Li, L.; Liu, J. The spatial correlation and interaction between environmental regulation and foreign direct investment. J. Regul. Econ. 2018, 54, 124–146. [Google Scholar] [CrossRef]

- Workman, D. World’s Top Exports. 2021. Available online: https://www.worldstopexports.com/worlds-top-oil-exports-country/ (accessed on 10 May 2021).

- Ravindranath, N.H.; Sathaye, J.A. Climate change and developing countries. In Climate Change and Developing Countries; Springer: Dordrecht, The Netherlands, 2002; pp. 247–265. [Google Scholar]

- Cao, X. Climate change and energy development: Implications for developing countries. Resour. Policy 2003, 29, 61–67. [Google Scholar] [CrossRef]

- Nath, P.K.; Behera, B. A critical review of impact of and adaptation to climate change in developed and developing economies. Environ. Dev. Sustain. 2011, 13, 141–162. [Google Scholar] [CrossRef]

- Impact Management Project. Intergovernmental Panel on Climate Change (IPCC). 2014. Available online: https://www.ipcc.ch/report/ar5/syr/ (accessed on 25 April 2021).

- Ali, W.; Frynas, J.; Mahmood, Z. Determinants of Corporate Social Responsibility (CSR) Disclosure in Developed and Developing Countries: A Literature Review. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 273–294. [Google Scholar] [CrossRef]

- Ali, W.; Frynas, J. The Role of Normative CSR—Promoting Institutions in Stimulating CSR Disclosures in Developing Countries. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 373–390. [Google Scholar] [CrossRef]

- Secretariat, C. Influencing and Meeting International Standards: Challenges for Developing Countries; International Trade Centre UNCTAD/WTO: Geneva, Switzerland, 2003. [Google Scholar]

- ISO. ISO ACTION PLAN for Developing Countries: 2021–2030. 2016. Available online: https://www.iso.org/files/live/sites/isoorg/files/store/en/PUB100374.pdf (accessed on 13 June 2021).

- European Commission. Guidelines on Reporting Climate-related Information. 2019. Available online: https://ec.europa.eu/finance/docs/policy/190618-climate-related-information-reporting-guidelines_en.pdf (accessed on 20 February 2022).

- Yin, R. Case Study Research: Design and Methods; Sage Publications: Thousand Oaks, CA, USA, 2003. [Google Scholar]

- Bryman, A.; Bell, E. Business Research Method; Oxford University Press: Oxford, UK, 2007. [Google Scholar]

- Ng, A.; Nathwani, J. Sustainability performance disclosures: The case of independent power producers. Renew. Sustain. Energy Rev. 2012, 16, 1940–1948. [Google Scholar] [CrossRef]

- Giles, O.; Murphy, D. SLAPPed: The relationship between SLAPP suits and changed ESG reporting by firms. Sustain. Account. Manag. Policy J. 2016, 7, 44–79. [Google Scholar] [CrossRef]

- An, Y.; Davey, H.; Harun, H.; Jin, Z.; Qiao, X.; Yu, Q. Online sustainability reporting at universities: The case of Hong Kong. Sustain. Account. Manag. Policy J. 2020, 11, 887–901. Available online: https://www.emerald.com/insight/2040-8021.htm (accessed on 20 February 2022). [CrossRef]

- Abudu, H.; Sai, R. Examining prospects and challenges of Ghana’s petroleum industry: A systematic review. Energy Rep. 2020, 6, 841–858. [Google Scholar] [CrossRef]

- Ghana Statistical Service. 2020. Available online: https://statsghana.gov.gh/gssmain/storage/img/marqueeupdater/Annual_2013_2019_GDP.pdf (accessed on 5 August 2021).

- US Geological Survey “Gold Data Sheet—Mineral Commodity Summaries”. 2020. Available online: https://pubs.usgs.gov/periodicals/mcs2020/mcs2020-gold.pdf (accessed on 2 June 2021).

- Ghana Chamber of Mines. Performance of The Mining Industry in 2019; Ghana Chamber of Mines: Accra, Ghana, 2019. [Google Scholar]

- GHEITI. Mining Sector Report 2014. Ghana Extractive Industries Transparency Initiative. 2017. Available online: http://www.gheiti.gov.gh (accessed on 20 February 2022).

- Ghana Chamber of Mines. Gold Output from Large-Scale Mining Sector Up Six Percent in 2019. 2020. Available online: https://ghanachamberofmines.org/ (accessed on 5 June 2021).

- Bhattacharya, P.; Sracek, O.; Eldvall, B.; Asklund, R.; Barmen, G.; Jacks, G.; Balfors, B.B. Hydrogeochemical study on the contamination of water resources in a part of Tarkwa mining area, Western Ghana. J. Afr. Earth Sci. 2012, 66–67, 72–84. [Google Scholar] [CrossRef]

- Cuba, N.; Bebbington, A.; Rogan, J.; Millones, M. Extractive industries, livelihoods and natural resource competition: Mapping overlapping claims in Peru and Ghana. Appl. Geogr. 2014, 54, 250–261. [Google Scholar] [CrossRef]

- Gamu, J.; Le Billon, P.; Spiegel, S. Extractive industries and poverty: A review of recent findings and linkage mechanisms. Extr. Ind. Soc. 2015, 2, 162–176. [Google Scholar] [CrossRef]

- Adusah-Karikari, A. Black gold in Ghana: Changing livelihoods for women in communities affected by oil production. Extr. Ind. Soc. 2015, 2, 24–32. [Google Scholar] [CrossRef]

- Rüttinger, L.; Sharma, V. Climate Change and Mining: A Foreign Policy Perspective; University of Queensland: St Lucia, Australia, 2016. [Google Scholar]

- Emmanuel, A.Y.; Jerry, C.S.; Dzigbodi, D.A. Review of environmental and health impacts of mining in Ghana. J. Health Pollut. 2018, 8, 43–52. [Google Scholar] [CrossRef]

- Odell, S.D.; Bebbington, A.; Frey, K.E. Mining and climate change: A review and framework for analysis. Extr. Ind. Soc. 2018, 5, 201–214. [Google Scholar] [CrossRef]

- Environmental Protection Agency of Ghana. 2021. Available online: http://www.epa.gov.gh/epa/ (accessed on 25 May 2021).

- Zalik, A.; Osuoka, I. Beyond transparency: A consideration of extraction’s full costs. Extr. Ind. Soc. 2020, 7, 781–785. [Google Scholar] [CrossRef]

- Pobbi, M.; Anaman, E.A.; Quarm, R.S. Corporate Sustainability Reporting: Empirical Evidence from Ghana. J. Econ. Bus. 2020, 3, 1005–1013. [Google Scholar] [CrossRef]

- Aminu, A.S.; Chiroma, M.A.; Shehu, A.I.O.H.; Abdullahi, A. Possible Roles of Corporate social responsibility (CSR) in promoting sustainable Development in Nigeria. J. Adv. Soc. Sci. Humanit. 2016, 2, 1. [Google Scholar]

- Few, R.; Morchain, D.; Spear, D.; Mensah, A.; Bendapudi, A. Transformation, Adaptation and Development: Relating Concepts to Practice. Palgrave Commun. 2017, 3, 17092. [Google Scholar] [CrossRef]

- European Commission. Industry 5.0: Towards More Sustainable, Resilient and Human-Centric Industry. 2021. Available online: https://ec.europa.eu/info/news/industry-50-towards-more-sustainable-resilient-and-human-centric-industry-2021-jan-07_en (accessed on 20 February 2022).

- Cho, C.H.; Senn, J.; Sobkowiak, M. Sustainability at stake during COVID-19: Exploring the role of accounting in addressing environmental crises. Crit. Perspect. Account. 2021, 82, 102327. [Google Scholar] [CrossRef]

- Ketz, J. The Myth of Auditor Independence: Waking Up to Unconscious Bias. The CPA Journal. 2020. Available online: https://www.cpajournal.com/2020/03/06/the-myth-of-auditor-independence/ (accessed on 5 February 2022).

- Shehadeh, A.; Alshboul, O.; Al Mamlook, R.E.; Hamedat, O. Machine learning models for predicting the residual value of heavy construction equipment: An evaluation of modified decision tree, LightGBM, and XGBoost regression. Autom. Constr. 2021, 129, 103827. [Google Scholar] [CrossRef]

- Alshboul, O.; Shehadeh, A.; Al-Kasasbeh, M.; Al Mamlook, R.E.; Halalsheh, N.; Alkasasbeh, M. Deep and machine learning approaches for forecasting the residual value of heavy construction equipment: A management decision support model. Eng. Constr. Arch. Manag. 2021. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Name of Company (Selected Case) | Industry | Stock Exchanges | Major Type of Investor | Number of Countries Operated in Africa/Total | Corporate Headquarters | No. of Oil Fields/Mines in Ghana | Auditor |

|---|---|---|---|---|---|---|---|

| Tullow Oil (O1) | Oil and Gas exploration | London, Irish and Ghana | Institutional investor | 9/15 | UK | 7 | EY |

| Kosmos Energy (O2) | Oil and Gas exploration | London, and New York | Institutional investor | 5/6 | US | 2 | EY |

| ENI (O3) | Oil and Gas exploration | Milan and New York | Government | 7/42 | Italy | 1 | PWC |

| Anglo Gold Ashanti (M1) | Gold mining | Johannesburg, New York, Australian and Ghana | Institutional investor | 4/7 | South Africa | 2 | EY |

| Newmont (M2) | Gold mining | New York and Toronto | Institutional investor | ¼ | US | 1 | EY |

| Golden Star Resources (M3) | Gold mining | New York, Toronto and Ghana | Institutional investor | 1 | UK | 1 | PWC |

| (a) | ||||||

| Case | Sustainability Committee | Standalone Sustainability Report | Embracing SDGs (Yes/No) | Years of Experience in Sustainability Reporting | Standards Claimed | Assurance |

| Tullow Oil (O1) | Yes | Yes | Yes | 2 (2019–2020) | GRI, IPIECA, TCFD | EY |

| Kosmos Energy (O2) | Yes | Yes | Yes | 1 1 (2019/2020) | GRI, IPIECA, SASB, UNGC, TCFD | Trinity Consultants |

| ENI (O3) | Yes | Yes | Yes | 6 (2015–2020) | GRI, IPIECA, WEF, TCFD | PWC |

| Anglo Gold Ashanti (M1) | Yes | Yes | Yes | 12 (2009–2020) | IIRC, GRI, SASB, AA1000, ICMM | EY |

| Newmont (M2) | Yes | Yes | Yes | 2 (2019–2020) | GRI, SASB, ICMM, AA1000, UNGC, Global Sullivan Principles | Apex Companies |

| Golden Star Resources (M3) | Yes | Yes 2 | Yes | 6 (2006–2011) | GRI, AA1000, SASB, UNGC, LPRM | Perspective Consulting |

| 1 (Kosmos Energy (O2) published one sustainability report for 2019 and 2020) 2 M3 issued standalone Corporate Responsibility report which reports on its sustainability performance | ||||||

| (b) | ||||||

| Case | Scope 1 | Scope 2 | Scope 3 | |||

| Tullow Oil (O1) | 1 | 1 | 0 | |||

| Kosmos Energy (O2) | 1 | 1 | 1 | |||

| ENI (O3) | 1 | 1 | 0 | |||

| Anglo Gold Ashanti (M1) | 1 | 1 | 0 | |||

| Newmont (M2) | 1 | 1 | 1 | |||

| Golden Star Resources (M3) | 1 | 1 | 0 | |||

| Note: 1 = With Disclosure; 0 = No Disclosure | ||||||

| (a) | ||||||

| 2016 | 2017 | 2018 | 2019 | 2020 | ||

| Case | Units | Reported GHG Emission (Global) | ||||

| O1 | million tonnes | 0.77 | 1.62 | 1.24 | 1.28 | 2.36 |

| O2 | million tonnes | 0.09 | 0.22 | 0.11 | 0.04 | NA |

| O3 | million tonnes | 42.86 | 43.80 | 44.02 | 41.89 | 38.49 |

| M1 | million tonnes (metric) | 4.06 | 3.95 | 2.57 | 2.57 | 2.34 |

| M2 | million tonnes | 3.13 | 3.43 | 3.57 | 3.32 | 3.45 |

| M3 | million tonnes | NA | NA | NA | 0.06 | 0.03 |

| Reported Energy Use (Global) | ||||||

| O1 | million GJ | 7.32 | 8.04 | 9.74 | 10.30 | 9.65 |

| O2 | NA | NA | NA | NA | NA | NA |

| O3 | million toe | NA | 13.40 | 13.50 | 13.20 | 12.80 |

| M1 | million GJ | 28.55 | 29.76 | 25.38 | 26.32 | 25.57 |

| M2 | million GJ | 34.84 | 38.50 | 40.59 | 37.90 | 37.39 |

| M3 | million GJ | 0.13 * | 0.14 * | NA | 0.94 | 0.62 |

| Reported Emission Intensity (Global) | ||||||

| O1 | Total Scope 1 and 2 emissions by production (tonnes of CO2e) per thousand tonnes hydrocarbon produced | 142.11 | 185.36 | 139.18 | 134.00 | 220.00 |

| O2 | NA | NA | NA | NA | NA | NA |

| O3 | GHG upstream emissions (Scope 1)/100% operated hydrocarbon gross production (UPS) | 23.56 | 22.75 | 21.44 | 19.58 | 19.98 |

| M1 | Kilograms of GHG per tonne treated | 48.00 | 46.00 | 32.00 | 32.00 | 33.35 |

| M2 | Tonnes of CO2 e/oz of gold produced | 0.57 | 0.47 | 0.61 | 0.58 | 0.63 |

| M3 | Tonnes of CO2 e/oz of gold produced | NA | NA | NA | 0.30 | 0.19 |

| Reported Energy Use Intensity (Global) | ||||||

| O1 | GJ per thousand tonnes of hydrocarbon produced | 1370.03 | 920.08 | 1097.82 | 1081.86 | 1045.20 |

| O2 | NA | NA | NA | NA | NA | NA |

| O3 | Energy consumption from production activities/operated hydrocarbon gross production (upstream) | 1.71 | 1.49 | 1.42 | 1.39 | 1.52 |

| M1 | GJ per metric tonne treated | 0.33 | 0.35 | 0.32 | 0.33 | 0.37 |

| M2 | NA | NA | NA | NA | NA | NA |

| M3 | GJ per oz of gold produced | NA | NA | NA | 4.6 | 3.71 |

| (b) | ||||||

| Units | Reported GHG or CO2 Emissions (Ghana) | |||||

| Case | 2016 | 2017 | 2018 | 2019 | 2020 | |

| O1 | million tonnes | NA | NA | NA | NA | NA |

| O2 | million tonnes | NA | NA | 217 | 202 | NA |

| O3 | million tonnes | NA | NA | NA | NA | NA |

| M1 | million tonnes (metric) | 149 | 160 | 165 | 185 | 238 |

| M2 | million tonnes | NA | NA | NA | 0.32 | 0.34 |

| M3 | million tonnes | NA | NA | NA | 0.061 | 0.033 |

| Reported Energy Use (Ghana) | ||||||

| Case | 2016 | 2017 | 2018 | 2019 | 2020 | |

| O1 | million GJ | NA | NA | NA | NA | NA |

| O2 | NA | NA | NA | NA | NA | NA |

| O3 | million toe | NA | NA | NA | NA | NA |

| M1 | million GJ | 1.32 | 1.72 | 1.84 | 1.99 | 2.45 |

| M2 | million GJ | NA | NA | NA | 4.69 | 4.86 |

| M3 | million GJ | 0.13 * | 0.14 * | NA | 0.94 | 0.62 |

| Reported Emission Intensity (Ghana) | ||||||

| Case | 2016 | 2017 | 2018 | 2019 | 2020 | |

| O1 | Total Scope 1 and 2 emissions by production (tonnes of CO2e) per thousand tonnes hydrocarbon produced | NA | NA | NA | NA | NA |

| O2 | NA | NA | NA | NA | NA | NA |

| O3 | GHG upstream emissions (Scope 1)/100% operated hydrocarbon gross production (UPS) | NA | NA | NA | NA | NA |

| M1 | Kilograms of GHG per tonne treated | 29.00 | 32.00 | 31.00 | 24.00 | 42.28 |

| M2 | Tonnes of CO2 e/oz of gold produced | NA | NA | NA | NA | 0.40 |

| M3 | Tonnes of CO2 e/oz of gold produced | NA | NA | NA | 0.30 | 0.19 |

| Reported Energy Use Intensity (Ghana) | ||||||

| Case | 2016 | 2017 | 2018 | 2019 | 2020 | |

| O1 | GJ per thousand tonnes of hydrocarbon produced | NA | NA | NA | NA | NA |

| O2 | NA | NA | NA | NA | NA | NA |

| O3 | Energy consumption from production activities/operated hydrocarbon gross production (upstream) | NA | NA | NA | NA | NA |

| M1 | GJ per metric tonne treated | 0.26 | 0.34 | 0.3 | 0.28 | 0.44 |

| M2 | NA | NA | NA | NA | NA | NA |

| M3 | GJ per oz of gold produced | NA | NA | NA | 4.6 | 3.71 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ng, A.W.; Yorke, S.M.; Nathwani, J. Enforcing Double Materiality in Global Sustainability Reporting for Developing Economies: Reflection on Ghana’s Oil Exploration and Mining Sectors. Sustainability 2022, 14, 9988. https://doi.org/10.3390/su14169988

Ng AW, Yorke SM, Nathwani J. Enforcing Double Materiality in Global Sustainability Reporting for Developing Economies: Reflection on Ghana’s Oil Exploration and Mining Sectors. Sustainability. 2022; 14(16):9988. https://doi.org/10.3390/su14169988

Chicago/Turabian StyleNg, Artie W., Sally Mingle Yorke, and Jatin Nathwani. 2022. "Enforcing Double Materiality in Global Sustainability Reporting for Developing Economies: Reflection on Ghana’s Oil Exploration and Mining Sectors" Sustainability 14, no. 16: 9988. https://doi.org/10.3390/su14169988

APA StyleNg, A. W., Yorke, S. M., & Nathwani, J. (2022). Enforcing Double Materiality in Global Sustainability Reporting for Developing Economies: Reflection on Ghana’s Oil Exploration and Mining Sectors. Sustainability, 14(16), 9988. https://doi.org/10.3390/su14169988