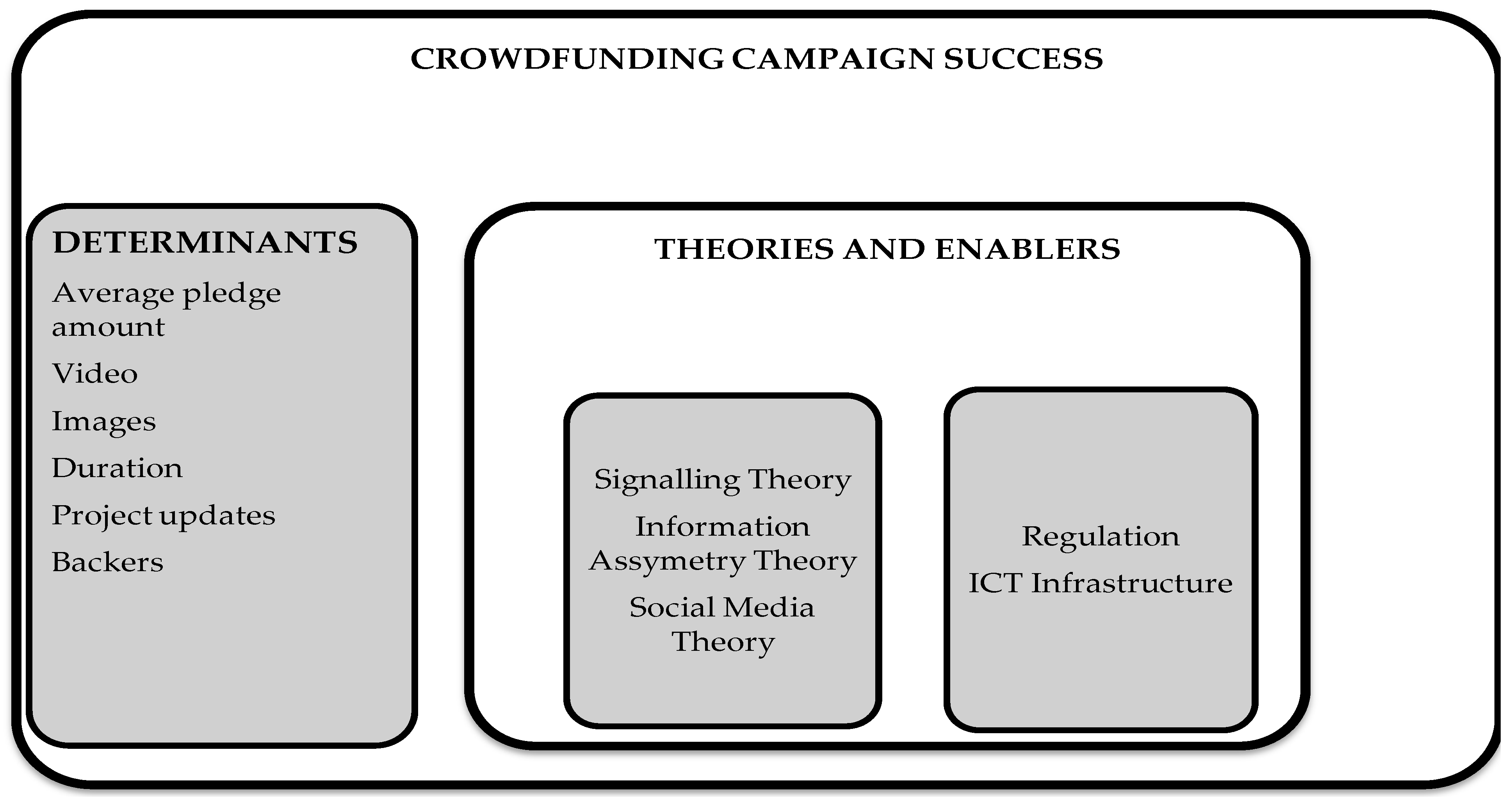

2.1. Theoretical Framework

The theoretical foundations of this study are firmly anchored on the pecking order of information asymmetry and signalling theories. The setting theory agenda also influences crowdfunding success. An additional source of finance, known as crowdfunding, has emerged for entrepreneurs to tap into. Notwithstanding, entrepreneurs mostly rely on internal financing before considering external sources of finance (for example, bank loans or venture capital), which is consistent with the pecking order theory. However, information asymmetries exist between entrepreneurs or fund seekers and external financing [

22]. Regarding crowdfunding, the problem of information asymmetry has the potential to limit the investors or backers from contributing to the project’s initiator. As a result, the worthy crowdfunding project could go unfunded due to the limited information provided to the backers and investors [

23].

More backers for a crowdfunding campaign may send the signal of crowdfunding success. The availability of information may attract the crowd in making decisions, i.e., whether to contribute or not. The signal theory by Ross [

24] and Spence [

25] states that entrepreneurial activities provide or convey worthy information to the investors and backers to enable them to make contributions or invest in a crowdfunding campaign. The theory indicates that between these two parties (the crowd and project creator), one party must examine how to communicate or signal information and the other party must interpret the information provided in order to make informed decisions. The signalling theory has potential to identify all behaviours of individuals when accessing information provided on the crowdfunding platform [

26]. Hence, the theory was adopted to determine factors influencing the crowdfunding performances in the African continent during the COVID-19 crisis. Mainly, the information conveyed influences the crowd to consider the campaign’s initiatives. The crowdfunding platform presents transparency by disclosing the project creator and fund seeker in the process of raising financing. The project creator may provide limited information to the supporters or backers of the project, which creates the problem of information asymmetry.

The common feature amongst all types of crowdfunding campaigns is that, in contrast to more conventional sources of finance, financial means are derived from a range of backers. Funding mechanisms of these crowdfunding platforms are often based on a minimum target amount (or an all-or-nothing principle) and come with a fixed timeframe to attract investors [

4]. According to these crowdfunding principles, projects only receive funding if the raised sum meets the overall targeted investment sum or a lower minimum threshold, which ensures the practicability of the project. If the project cannot reach its target within the given timeframe, the collected sum goes back to the investors. Each project initiator sets a funding goal within the default maximum and a minimum amount given by the platform providers. Another principle used by crowdfunding platforms is the ‘keep-what-you-raise’ approach. In this case, no threshold needs to be reached. The project initiator receives all funds that have been collected within the set timeframe. Typically, the timeframe for projects to raise money ranges from 30 to 90 days.

The agenda setting theory also has a bearing on crowdfunding success as it has an impact on social media policies. According to the social media theory, the social tie involves the interaction between two parties, namely the project creator and backers or the crowd [

27]. The strength of a social bond is determined by a combination of time, emotional intensity, intimacy, and reciprocity, which characterize the bond [

28]. Therefore, social media in relation to crowdfunding remains an important contribution to the success performance. Intimate communication through social media, such as Facebook, Twitter, LinkedIn, is considered to be a strong tie [

29]. As a result, crowdfunding platform provide social interaction accounts and, thus, share their projects statuses with the crowd [

30].

Innovation relies on digital transformational entrepreneurs, which include changes in business settings [

9]. Therefore, crowdfunding is a social change that occurs through entrepreneurial innovative financing activities that occur digitally. Ratten et al. [

31] defined the transformational social entrepreneurship theory as innovative business activities being developed to respond to social issues. Hence, from the vantage point of the transformational entrepreneur social theory, crowdfunding has the potential to overcome problems created by the COVID-19 pandemic in relation to access to finance. A crowdfunding platform alleviates the limited access to financing due to its popularity and growth, especially in Africa [

11].

2.3. Hypotheses Development

In this subsection, we present the hypotheses that underpin this study. We discuss these next.

The presence of images on a crowdfunding platform enables the crowd or backers to decide whether to support the project campaign [

34]. Therefore, the presence of visuals increases the quality and trust concerning the crowdfunding campaign. Hence, the availability of videos and images reduces the information asymmetry between the project creator and backers. The presence of images and videos on the crowdfunding platform signal a creator’s preparedness, which attracts a large number of backers [

35]. Hence, the project creator appears to be more personal and human, decreasing the distance between the backers and project creator (entrepreneur). Therefore, the presence of images and videos signals a strong tie between project creators (SMEs) and backers.

The videos and images appearing on the crowdfunding campaign page attract the backers to invest and contribute to the crowdfunding project [

18]. The presence of images and videos on the project page attracts the backers and supporters to contribute to the project campaign [

36,

37]. The presence of videos is seen as an effective source of information and likely impacts how backers evaluate the project and the success of the project, eliminating confusion concerning the project campaign [

38]. The image and video usage on the crowdfunding campaign has the probability to increase the success of the campaign [

39]. Campaign projects without images and videos have a high probability of unsuccessful performances. The image usage promotes a project campaign and makes it easier for backers, investors, family, and friends to be aware of the campaign [

40]. These views are supported by Huang et al. [

41], who indicated that text messages have limited performances on crowdfunding compared to video and visual images. Contrarily, Butticè et al. [

42] and Petitjean [

34] reported a negative relationship between videos/images and crowdfunding success. As a result, we hypothesise that:

Hypothesis 1 (H1). The presence of videos will have positive and significant influences on the success of a crowdfunding campaign.

Hypothesis 2 (H2). The availability of images on the project page increases the probability of the project’s success.

Consistent updates made between the project creator and backers signal the crowdfunding success [

16]. Updates during a campaign show that the creator is staying in touch with the crowd; it allows creators to present new insights into the project’s progress and communicate further information. Information may include the current status of the project or new features that will be unlocked when a funding threshold is reached. The success of crowdfunding relies on transparency and trustworthiness [

11]. Hence, updates strengthen the relationship between backers and the project creator, and as a result, increase the probability of success. Sharing information and communicating during a campaign in the form of updates decreases the problems concerning information asymmetry, creating a unified consensus [

35]. Continuous updates made on the crowdfunding platform reduce the weak social ties between backers and SMEs.

The more updates made on the crowdfunding page, the more backers will be attracted to it, which will increase the crowdfunding performance. Updates are communicative mechanisms that provide additional information about the business ideas of entrepreneurs to potential investors [

43]. The more updates provided on the crowdfunding campaign project, the more it has the potential to attract more investors or backers, which will ultimately lead to crowdfunding success. Furthermore, the study conducted by de Larrea et al. [

44] showed that the absence of updates decreased crowdfunding success. According to Lagazio et al. [

45], projects with updates increase the involvement of many contributors and backers to invest or donate into the project campaign. In line with the previous findings from the literature, the proposed hypothesis is as follows:

Hypothesis 3 (H3). Project updates will have positive and significant influences on the crowdfunding campaign’s success.

The duration of the crowdfunding campaign is the period in which the project creator or SME attempts to access financing from the backers. However, the period differs based on the crowdfunding platform; for example, Kickstarter ranges from 1 to 60 days and Indiegogo ranges from 1 to 40 days. Mollick [

4] reported that a short duration signals trustworthiness and confidence to backers (or the crowd) in regard to supporting the project campaign. Furthermore, backers may not doubt the crowdfunding’s ability to access finance.

The duration of the project campaign has the probability to influence the performance of a crowdfunding campaign. According to Mollick [

4], a longer duration time has less of a probability of success in crowdfunding because it signals a lack of confidence. These views are supported by Anglin et al. [

46], who contended that a longer duration decreases the confidence of backers or supporters in regard to contributing to the project campaign. A longer duration of the crowdfunding campaign indicates a negative influence on the crowdfunding success. Most backers will perceive that there is a lack of confidence if the project duration is long [

4]. The shorter duration of the project campaign provides backers with quality time and confidence. The longer duration of the crowdfunding project campaign has broader visibility and awareness but it might be perceived as a lack of trust to funders/backers, which will ultimately decrease the probability of success [

47]. Further, Cordova et al. [

48] documented that a longer duration increases the chances of success on the crowdfunding performance with the reward-based model. The expectation of the study is that the visibility of a crowdfunding project that is longer will decrease the probability of success. Hence, we hypothesise that:

Hypothesis 4 (H4). The duration decreases the probability of the crowdfunding project’s success.

Regarding the amount of money raised in millions (USD) from a crowdfunding platform, in later multiple regressions, the natural logarithm (of the actual funding amount plus 1) is used. The actual amount of money raised is used as the control variable and has the probability of success performance. The actual funding amount raised is used as the control variable. The number of funders as well as the average funding amount per funder, as potential mediators, improves the crowdfunding success. On the other hand, a small number of backers decreases the probability of success. The average funding amount of a project increases the probability of the crowdfunding performance [

49]. However, in some instances where there is less risk concerning the project campaign, there is a high probability of success [

50]. Crowdfunding is characterised by less risk and a transparent source of finance. Hence, the research hypothesis put forward is:

Hypothesis 5 (H5). The actual funding amount increases the probability of the crowdfunding project’s success.

The backers are persuaded by the rewards promised after contributions are made on the crowdfunding campaign’s project [

51]. The rewards provided to backers in exchange for money contribute to the campaign’s success. The project creator is responsible for building trust among backers regarding their willingness to contribute to the crowdfunding success [

35]. Furthermore, it signals crowdfunding success due to the higher number of backers willing to support the campaign.

The number of backers supporting the project campaign is influenced by the number of rewards offered [

47]. A larger number of backers supporting the project campaign increases the probability of success [

52]. These findings are supported by the findings by Abdeldayem et al. [

53] and Sum [

54]. However, the results are not in line with the findings by Hobbs [

55]. The backers and creators increase the probability of the crowdfunding success [

17]. It is, therefore, an important indicator of crowdfunding success since it attracts backers to contribute to the project campaign. Hence, the research hypothesis is as follows:

Hypothesis 6 (H6). The larger number of backers increases the probability of the crowdfunding campaign’s success.

{kind=link}