Does Innovation Spur Integrated Reporting?

Abstract

:1. Introduction

2. Background and Hypotheses

2.1. Previous Literature

2.2. Country-Level Innovation Performance

2.3. Firm-Level Innovation Commitment

2.3.1. Firm-Level Innovation Commitment: Hypothesis 2

2.3.2. Firm-Level Innovation Commitment: Hypothesis 3

3. Research Design

3.1. Sample and Data

3.2. Research Model

4. Results and Discussion

4.1. Descriptive Statistics

4.2. Logistic Regression Results

4.2.1. Country-Level Innovation Performance: Hypothesis 1

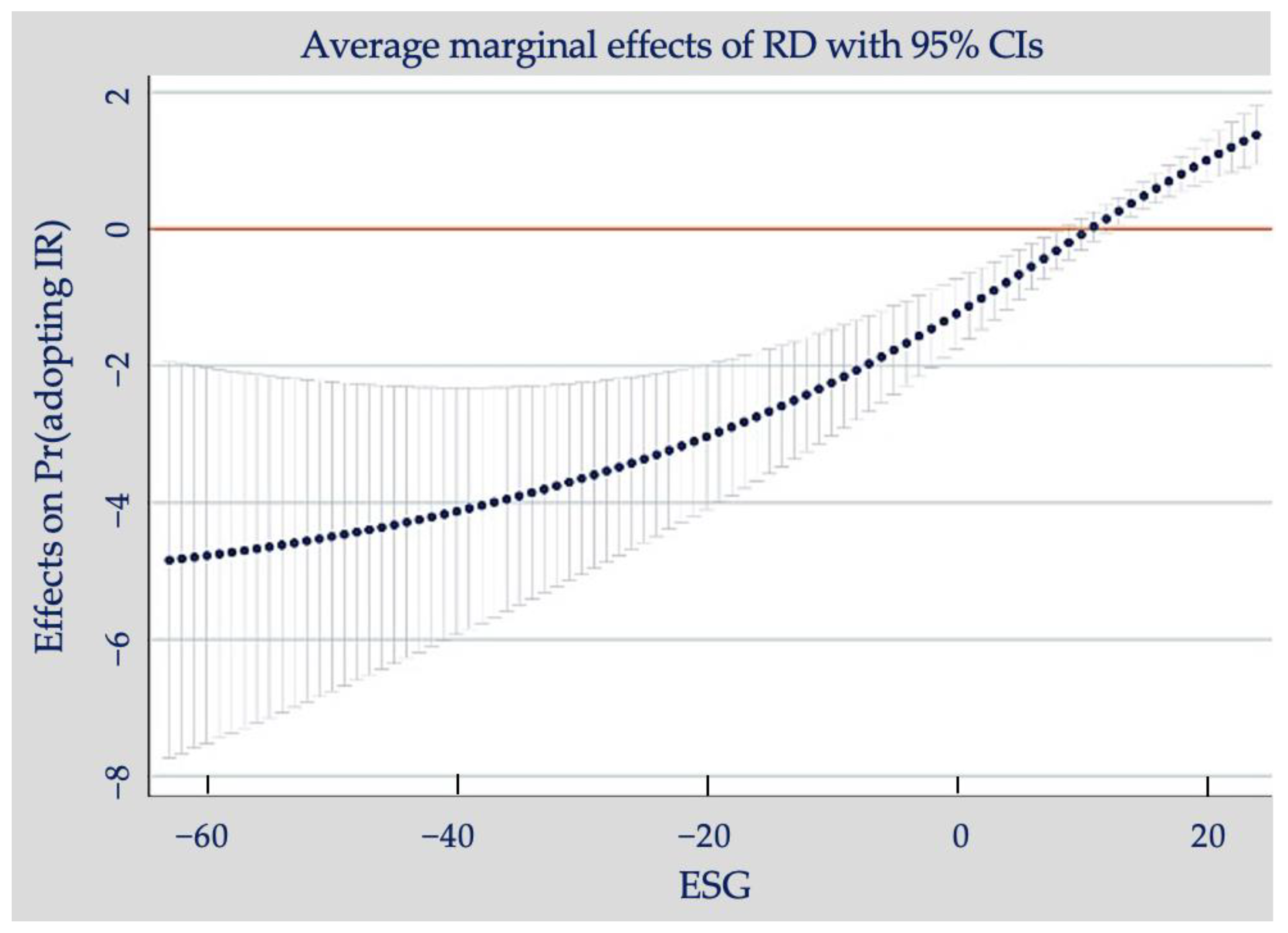

4.2.2. Firm-Level Innovation Commitment: Hypothesis 2 and 3

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Blomme, H. Core & More: Making Reporting Smarter, IFAC. 2017. Available online: https://www.ifac.org/knowledge-gateway/preparing-future-ready-professionals/discussion/core-more-making-reporting-smarter (accessed on 18 May 2022).

- Carraher, S.; Auken, H.V. The use of financial statements for decision making by small firms. J. Small Bus. Entrep. 2013, 26, 323–336. [Google Scholar] [CrossRef]

- Perego, P.; Kennedy, S.; Whiteman, G. A lot of icing but little cake? Taking integrated reporting forward. J. Clean. Prod. 2016, 136A, 53–64. [Google Scholar] [CrossRef] [Green Version]

- Artiach, T.; Lee, D.; Nelson, D.; Walker, J. The determinants of corporate sustainability performance. Account. Financ. 2010, 50, 31–51. [Google Scholar] [CrossRef]

- Baumüller, J.; Sopp, K. Double materiality and the shift from non-financial to European sustainability reporting: Review, outlook and implications. J. Appl. Account. Res. 2022, 23, 8–28. [Google Scholar] [CrossRef]

- Lourenço, I.C.; Branco, M.C. Determinants of corporate sustainability performance in emerging markets: The Brazilian case. J. Clean. Prod. 2013, 57, 134–141. [Google Scholar] [CrossRef]

- Noti, K.; Mucciarelli, F.M.; Angelici, C.; dalla Pozza, V.; Pillinini, M. Corporate Social Responsibility (CSR) and Its Implementation into EU Company Law. 2020. Available online: https://www.europarl.europa.eu/thinktank/en/document/IPOL_STU(2020)658541 (accessed on 25 April 2022).

- White, A.L. New Wine, New Bottles: The Rise of Non-Financial Reporting. A Business Brief by Business for Social Responsibility. 2005. Available online: http://www.bsr.org/reports/200506_BSR_Allen-White_Essay.pdf (accessed on 22 May 2022).

- Siew, R.Y.J. A review of corporate sustainability reporting tools (SRTs). J. Environ. Manag. 2015, 164, 180–195. [Google Scholar] [CrossRef]

- Eccles, R.; Kruzs, M. The Integrated Reporting Movement: Meaning, Momentum, Motives and Materiality; Wiley: Hoboken, NJ, USA, 2015. [Google Scholar]

- Eccles, R.G.; Krzus, M.P. One Report—Integrated Reporting for a Sustainable Strategy, Financial Executive; Wiley & Sons: Hoboken, NJ, USA, 2010. [Google Scholar]

- King, M.; Roberts, L. Integrate Doing Business in the 21st Century; Juta Company Ltd.: Cape Town, South Africa, 2013. [Google Scholar]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate social responsibility and access to finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Howit, R. IIRC Newsletter-Highlights from 2016: Breakthrough Year, International Integrated Reporting Council Newsletter. 2016. Available online: https://integratedreporting.org/news/we-have-made-history-together-thank-you/ (accessed on 18 February 2022).

- IIRC. The International IR Framework, International Integrated Reporting Council. 2021. Available online: https://www.integratedreporting.org/wp-content/uploads/2021/01/InternationalIntegratedReportingFramework.pdf (accessed on 24 February 2022).

- Manes-Rossi, F.; Tiron-Tudor, A.; Nicolò, G.; Zanellato, G. Ensuring more sustainable reporting in Europe using non-financial disclosure-de facto and de jure evidence. Sustainability 2018, 10, 1162. [Google Scholar] [CrossRef] [Green Version]

- Camilleri, M.A. Environmental, social and governance disclosures in Europe. Sustain. Account. Manag. Policy J. 2015, 6, 224–242. [Google Scholar] [CrossRef]

- IIRC. The International IR Framework, International Integrated Reporting Council. 2013. Available online: http://integratedreporting.org/wp-content/uploads/2013/12/13-12-08-THE-INTERNATIONAL-IR-FRAMEWORK-2-1.pdf (accessed on 5 January 2022).

- IIRC. The International IR Framework, International Integrated Reporting Council. Towards Integrated Reporting. Communicating Value in the 21st Century. 2011. Available online: https://integratedreporting.org/wp-content/uploads/2011/09/IR-Discussion-Paper-2011_spreads.pdf (accessed on 4 March 2019).

- Milne, M.J.; Gray, R. W(h)ither Ecology? The Triple Bottom Line, the Global Reporting Initiative, and Corporate Sustainability Reporting. J. Bus. Ethics 2013, 118, 13–29. [Google Scholar] [CrossRef]

- Adams, C.A.; Potter, B.; Singh, P.J.; York, J. Exploring the implications of integrated reporting for social investment (disclosures). Br. Account. Rev. 2016, 48, 283–296. [Google Scholar] [CrossRef] [Green Version]

- Ioannou, I.; Serafeim, G. The Consequences of Mandatory Corporate Sustainability Reporting. In The Oxford Handbook of Corporate Social Responsibility: Psychological and Organizational Perspectives; McWilliams, A., Rupp, D.E., Siegel, D.S., Stahl, G.K., Waldman, D.A., Eds.; Oxford University Press: Oxford, UK, 2019; pp. 452–489. [Google Scholar]

- Rinaldi, L.; Unerman, J.; de Villiers, C. Evaluating the Integrated Reporting journey: Insights, gaps and agendas for future research. Account. J. 2018, 31, 1294–1318. [Google Scholar] [CrossRef] [Green Version]

- de Villiers, C.; Venter, E.R.; Hsiao, P.C.K. Integrated reporting: Background, measurement issues, approaches and an agenda for future research. Account. Financ. 2017, 57, 937–959. [Google Scholar] [CrossRef] [Green Version]

- Frías-Aceituno, J.; Rodriguez-Ariza, L.; Garcia-Sanchez, I.M. Is integrated reporting determined by a country’s legal system? An exploratory study. J. Clean. Prod. 2013, 44, 45–55. [Google Scholar] [CrossRef]

- Frías-Aceituno, J.; Rodriguez-Ariza, L.; Garcia-Sanchez, I.M. The role of the board in the dissemination of integrated corporate social reporting. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 219–233. [Google Scholar] [CrossRef]

- Frías-Aceituno, J.; Rodriguez-Ariza, L.; Garcia-Sanchez, I.M. Explanatory Factors of Integrated Sustainability and Financial Reporting. Bus. Strategy Environ. 2014, 23, 56–72. [Google Scholar] [CrossRef]

- Fuhrmann, S. A multi-theoretical approach on drivers of integrated reporting—Uniting firm-level and country-level associations. Meditari Account. Res. 2020, 28, 168–205. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Rodríguez-Ariza, L.; Frías-Aceituno, J. The cultural system and integrated reporting. Int. Bus. Rev. 2013, 23, 828–838. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Martínez-Ferrero, J.; Garcia-Benau, M.A. Integrated reporting: The mediating role of the board of directors and investor protection on managerial discretion in munificent environments. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 29–45. [Google Scholar] [CrossRef] [Green Version]

- García-Sánchez, I.M.; Noguera-Gámez, L. Institutional Investor Protection Pressures versus Firm Incentives in the Disclosure of Integrated Reporting. Aust. Account. Rev. 2018, 28, 199–219. [Google Scholar] [CrossRef]

- Girella, L.; Rossi, P.; Zambon, S. Exploring the firm and country determinants of the voluntary adoption of integrated reporting. Bus. Strategy Environ. 2019, 28, 1323–1340. [Google Scholar] [CrossRef]

- Jensen, J.C.; Berg, N. Determinants of Traditional Sustainability Reporting Versus Integrated Reporting. An Institutionalist Approach. Bus. Strategy Environ. 2012, 21, 299–316. [Google Scholar] [CrossRef]

- Lai, A.; Melloni, G.; Stacchezzini, R. Corporate Sustainable Development: Is ‘Integrated Reporting’ a Legitimation Strategy? Bus. Strategy Environ. 2016, 25, 165–177. [Google Scholar] [CrossRef]

- Sierra-García, L.; Zorio-Grima, A.; García-Benau, M.A. Stakeholder Engagement, Corporate Social Responsibility and Integrated Reporting: An Exploratory Study. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 286–304. [Google Scholar] [CrossRef]

- Dumay, J.; la Torre, M.; Farneti, F. Developing trust through stewardship: Implications for intellectual capital, integrated reporting, and the EU Directive 2014/95/EU. J. Intellect. Cap. 2019, 20, 11–39. [Google Scholar] [CrossRef]

- la Torre, M.; Sabelfeld, S.; Blomkvist, M.; Dumay, J. Rebuilding trust: Sustainability and non-financial reporting and the European Union regulation. Meditari Account. Res. 2020, 28, 701–725. [Google Scholar] [CrossRef]

- Gallego-Álvarez, I. Assessing corporate environmental issues in international companies: A study of explanatory factors. Bus. Strategy Environ. 2018, 27, 1284–1294. [Google Scholar] [CrossRef]

- Hsueh, L. Opening up the firm: What explains participation and effort in voluntary carbon disclosure by global businesses? An analysis of internal firm factors and dynamics. Bus. Strategy Environ. 2019, 28, 1302–1322. [Google Scholar] [CrossRef]

- Radu, C.; Francoeur, C. Does Innovation Drive Environmental Disclosure? A New Insight into Sustainable Development. Bus. Strategy Environ. 2017, 26, 893–911. [Google Scholar] [CrossRef]

- Saisse, R.D.L.G.; Lima, G.B.A. Similarity modelling with ideal solution for comparative analysis of projects in the context of the additional brics proposal. Braz. J. Oper. Prod. Manag. 2019, 16, 659–671. [Google Scholar] [CrossRef]

- Tziogkidis, P.; Philippas, D.; Leontitsis, A.; Sickles, R.C. A data envelopment analysis and local partial least squares approach for identifying the optimal innovation policy direction. Eur. J. Oper. Res. 2020, 285, 1011–1024. [Google Scholar] [CrossRef]

- Chaminade, C. Innovation for what? Unpacking the role of innovation for weak and strong sustainability. J. Sustain. Res. 2020, 2, e200007. [Google Scholar]

- Fernandes, A.J.C.; Rodrigues, R.G.; Ferreira, J.J. National innovation systems and sustainability: What is the role of the environmental dimension? J. Clean. Prod. 2022, 347, 131164. [Google Scholar] [CrossRef]

- Gonçalves Montenegro, R.L.; Ribeiro, L.C.; Britto, G. The effects of environmental technologies: Evidence of different national innovation systems. J. Clean. Prod. 2021, 284, 124742. [Google Scholar] [CrossRef]

- Crespo, N.F.; Crespo, C.F. Global innovation index: Moving beyond the absolute value of ranking with a fuzzy-set analysis. J. Bus. Res. 2016, 69, 5265–5271. [Google Scholar] [CrossRef]

- Farooq, M.; Noor, A. The impact of corporate social responsibility on financial distress: Evidence from developing economy. Pac. Account. Rev. 2021, 33, 376–396. [Google Scholar] [CrossRef]

- Gogodze, J. Mechanisms and Functions within a National Innovation System. J. Technol. Manag. Innov. 2016, 11, 12–21. [Google Scholar] [CrossRef]

- Jankowska, B.; Matysek-Jȩdrych, A.; Mroczek-Dabrowska, K. Efficiency of National Innovation Systems—Poland and Bulgaria in the Context of the Global Innovation Index. Comp. Econ. Res. 2017, 20, 77–94. [Google Scholar] [CrossRef] [Green Version]

- Tang, D.; Li, Y.; Zheng, H.; Yuan, X. Government R&D spending, fiscal instruments and corporate technological innovation. China J. Account. Res. 2022, 15, 100250. [Google Scholar]

- Lundvall, B.-A. National Systems of Innovation: Towards a Theory of Innovation and Interactive Learning; Pinter: London, UK, 1992. [Google Scholar]

- Lundvall, B.-A. National innovation systems—Analytical concept and development tool. Ind. Innov. 2007, 14, 95–119. [Google Scholar] [CrossRef]

- DiMaggio, P.; Powell, W.W. The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields (translated by G. Yudin). Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef] [Green Version]

- Kothari, S.P.; Laguerre, T.E.; Leone, A.J.; Simon, W.E. Capitalization versus Expensing: Evidence on the Uncertainty of Future Earnings from Capital Expenditures versus R&D Outlays. Rev. Account. Stud. 2002, 7, 355–382. [Google Scholar]

- Rosenberg, N. Exploring the Black Box: Technology, Economics, and History, Technology and Culture, Technology and Culture; Cambridge University Press: Cambridge, UK, 1994. [Google Scholar]

- Eccles, R.G.; Serafeim, G. Corporate and integrated reporting: A functional perspective. In Corporate Stewardship: Achieving Sustainable Effectiveness; Mohrman, S., O’Toole, J., Sheffield, E., Eds.; Greenleaf Publishing: Sheffield, UK, 2015. [Google Scholar]

- Verrecchia, R.E. Discretionary Disclosure. J. Account. Econ. 1983, 5, 179–194. [Google Scholar] [CrossRef]

- Flower, J. The international integrated reporting council: A story of failure. Crit. Perspect. Account. 2015, 27, 1–17. [Google Scholar] [CrossRef]

- WBCSD. Reporting Matters, World Business Council for Sustainable Development. 2020. Available online: https://www.wbcsd.org/contentwbc/download/10460/156310/1 (accessed on 22 March 2022).

- Robertson, F.A.; Samy, M. Factors affecting the diffusion of integrated reporting—A UK FTSE 100 perspective. Sustain. Account. Manag. Policy J. 2015, 6, 190–223. [Google Scholar] [CrossRef]

- Robertson, F.A.; Samy, M. Rationales for integrated reporting adoption and factors impacting on the extent of adoption: A UK perspective. Sustain. Account. Manag. Policy J. 2020, 11, 351–382. [Google Scholar] [CrossRef]

- Freeman, E.R. Strategic Management: A Stakeholder Approach; Pitman Publishing: Boston, MA, USA, 1984. [Google Scholar]

- Gunarathne, N.; Senaratne, S. Diffusion of integrated reporting in an emerging South Asian (SAARC) nation. Manag. Audit. J. 2017, 32, 524–548. [Google Scholar] [CrossRef]

- Kılıç, M.; Uyar, A.; Kuzey, C.; Karaman, A.S. Does institutional theory explain integrated reporting adoption of Fortune 500 companies? J. Appl. Account. Res. 2021, 22, 114–137. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Raimo, N.; Vitolla, F. CEO power and integrated reporting. Meditari Account. Res. 2021, 29, 908–942. [Google Scholar] [CrossRef]

- Girella, L.; Zambon, S.; Rossi, P. Board characteristics and the choice between sustainability and integrated reporting: A European analysis. Meditari Account. Res. 2022, 30, 562–596. [Google Scholar] [CrossRef]

- Hsiao, P.C.K.; de Villiers, C.; Scott, T. Is voluntary International Integrated Reporting Framework adoption a step on the sustainability road and does adoption matter to capital markets? Meditari Account. Res. 2022, 30, 786–818. [Google Scholar] [CrossRef]

- Busco, C.; Malafronte, I.; Pereira, J.; Starita, M.G. The determinants of companies’ levels of integration: Does one size fit all? Br. Account. Rev. 2019, 51, 277–298. [Google Scholar] [CrossRef]

- Vitolla, F.; Raimo, N.; Rubino, M. Appreciations, criticisms, determinants, and effects of integrated reporting: A systematic literature review. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 518–528. [Google Scholar] [CrossRef]

- Edquist, C. Systems of Innovation Approaches—Their Emergence and Characteristics. In Systems of Innovation: Technologies, Institutions and Organisations; Edquist, C., Ed.; Pinter: London, UK, 1997. [Google Scholar]

- Edquist, C.; Johnson, B. Institutions and Organisations in Systems of Innovation. In Systems of Innovation: Technologies, Institutions and Organisations; Edquist, C., Ed.; Pinter: London, UK, 1997. [Google Scholar]

- Sharif, N. Emergence and development of the National Innovation Systems concept. Res. Policy 2006, 35, 745–766. [Google Scholar] [CrossRef] [Green Version]

- Balzat, M.; Hanusch, H. Recent trends in the research on national innovation systems. J. Evol. Econ. 2004, 14, 197–210. [Google Scholar] [CrossRef] [Green Version]

- Watkins, A.; Papaioannou, T.; Mugwagwa, J.; Kale, D. National innovation systems and the intermediary role of industry associations in building institutional capacities for innovation in developing countries: A critical review of the literature. Res. Policy 2015, 44, 1407–1418. [Google Scholar] [CrossRef]

- Campbell, J.L. Institutional Analysis and the Paradox of Corporate Social Responsibility. Am. Behav. Sci. 2006, 49, 925–938. [Google Scholar] [CrossRef]

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Matten, D.; Moon, J. ‘Implicit’ and ‘Explicit’ CSR: A conceptual framework for a comparative understanding of corporate social responsibility. Acad. Manag. Rev. 2008, 33, 404–424. [Google Scholar] [CrossRef] [Green Version]

- Oliver, C. Strategic responses to institutional processes. Acad. Manag. Rev. 1991, 16, 145–179. [Google Scholar] [CrossRef]

- Meyer, J.W.; Rowan, B. Institutionalized Organizations: Formal Structure as Myth and Ceremony. Am. J. Sociol. 1977, 83, 340–363. [Google Scholar] [CrossRef] [Green Version]

- Scott, W.R. Institutions and Organizations: Ideas, Interests and Identities; Sage: Thousand Oaks, CA, USA, 1995. [Google Scholar]

- Spence, M. Job Market Signaling. Q. J. Econ. 1973, 87, 355–374. [Google Scholar] [CrossRef]

- Ross, S.A. The Determination of Financial Structure: The Incentive-Signalling Approach, Source. Bell J. Econ. 1997, 8, 23–40. [Google Scholar] [CrossRef]

- Connelly, B.L.; Certo, S.T.; Ireland, R.D.; Reutzel, C.R. Signalling theory: A review and assessment. J. Manag. 2011, 37, 39–67. [Google Scholar]

- Sun, Y.; Davey, H.; Arunachalam, M.; Cao, Y. Towards a theoretical framework for the innovation in sustainability reporting: An integrated reporting perspective. Front. Environ. Sci. 2022, 10, 1584. [Google Scholar] [CrossRef]

- Dowling, J.; Pfeffer, J. Organizational Legitimacy: Social Values and Organizational Behavior. Pac. Sociol. Rev. 1975, 18, 122–136. [Google Scholar] [CrossRef]

- Cornell, INSEAD and WIPO, The Global Innovation Index 2019: Creating Healthy Lives—The Future of Medical Innovation. World Intellectual Property Organization. 2019. Available online: https://www.wipo.int/publications/en/details.jsp?id=4434 (accessed on 5 June 2022).

- Edquist, C.; Zabala-Iturriagagoitia, J.M.; Barbero, J.; Zofío, J.L. On the meaning of innovation performance: Is the synthetic indicator of the Innovation Union Scoreboard flawed? Res. Eval. 2018, 27, 196–211. [Google Scholar] [CrossRef] [Green Version]

- Gann, D.; Dogson, M. We Need to Measure Innovation Better. Here’s How. World Economic Forum. 2019. Available online: https://www.weforum.org/agenda/2019/05/we-need-to-measure-innovation-better-heres-how-to-do-it/ (accessed on 5 February 2022).

- Romijn, H.; Albaladejo, M. Determinants of innovation capability in small electronics and software firms in southeast England. Res. Policy 2002, 31, 1053–1067. [Google Scholar] [CrossRef]

- Ferreira, A.; Moulang, C.; Hendro, B. Environmental management accounting and innovation: An exploratory analysis, Accounting. Audit. Account. J. 2010, 23, 920–948. [Google Scholar] [CrossRef]

- Dziallas, M.; Blind, K. Innovation indicators throughout the innovation process: An extensive literature analysis. Technovation 2019, 80–81, 3–29. [Google Scholar] [CrossRef]

- Flor, M.L.; Oltra, M.J. Identification of innovating firms through technological innovation indicators: An application to the Spanish ceramic tile industry. Res. Policy 2004, 33, 323–336. [Google Scholar] [CrossRef]

- Cohen, W.M.; Levin, R.C. Empirical studies of innovation and market structure. In Handbook of Industrial Organization; Elsevier: Amsterdam, The Netherlands, 1989; Volume 2, pp. 1059–1107. [Google Scholar]

- Coombs, R.; Narandren, P.; Richards, A. A literature-based innovation output indicator. Res. Policy 1996, 25, 403–413. [Google Scholar] [CrossRef]

- Thomson Reuters. Thomson Reuters ESG Scores; Thomson Reuters: Toronto, ON, Canada, 2019. [Google Scholar]

- Ioannou, I.; Serafeim, G. What Drives Corporate Social Performance? The Role of Nation-level Institutions. J. Int. Bus. Stud. 2012, 43, 834–864. [Google Scholar] [CrossRef] [Green Version]

- Belal, A.R. Environmental reporting in developing countries: Empirical evidence from Bangladesh. Eco-Manag. Audit. 2000, 7, 114–121. [Google Scholar] [CrossRef]

- Hofstede, G. Dimension Data Matrix. 2015. Available online: https://geerthofstede.com/research-and-vsm/dimension-data-matrix/ (accessed on 18 May 2022).

- Buzby, S.L. Company Size, Listed Versus Unlisted Stocks, and the Extent of Financial Disclosure. J. Account. Res. 1975, 13, 16–37. [Google Scholar] [CrossRef]

- Singhvi, S.S.; Desai, H.B. An empirical analysis of the quality of corporate financial disclosure. Account. Rev. 1971, 46, 120–138. [Google Scholar]

- Gujarati, D. Basic Econometrics, 3rd ed.; Mc-Graw Hill International Editions: New York, NY, USA, 1995. [Google Scholar]

- Steyn, M. Organisational benefits and implementation challenges of mandatory integrated reporting: Perspectives of senior executives at South African listed companies. Sustain. Account. Manag. Policy J. 2014, 5, 476–503. [Google Scholar] [CrossRef]

- Birshan, M.; Seth, I.; Sternfels, B. Strategic Courage in an Age of Volatility. 2022. Available online: https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/strategic-courage-in-an-age-of-volatility (accessed on 25 May 2022).

{kind=link}

| Country | IR Adopters (Firm-Year obs.) | Non-IR Adopters (Firm-Year obs.) | Total Firm-Year obs. | % On the Total Firm-Year obs. |

|---|---|---|---|---|

| Belgium | 11 | 11 | 22 | 5.670% |

| France | 60 | 60 | 120 | 30.928% |

| Germany | 16 | 16 | 32 | 8.247% |

| Italy | 12 | 12 | 24 | 6.186% |

| Netherlands | 24 | 24 | 48 | 12.371% |

| Spain | 24 | 24 | 48 | 12.371% |

| Sweden | 15 | 15 | 30 | 7.732% |

| UK | 32 | 32 | 64 | 16.495% |

| Total | 194 | 194 | 388 | 100.000% |

| Industry | IR Adopters (Observations) | Non-IR Adopters (Observations) | Total Industry Observations | Total Industry obs./Total Observations (%) |

|---|---|---|---|---|

| Mining and construction | 13 | 9 | 22 | 5.670% |

| Manufacturing, wholesale trade | 138 | 145 | 283 | 72.938% |

| Services | 13 | 18 | 31 | 7.990% |

| Communications, transportation, electric, gas and sanitary | 30 | 22 | 52 | 13.402% |

| Total | 194 | 194 | 388 | 100.000% |

| Panel A: All Firms (n = 388) | ||||||

|---|---|---|---|---|---|---|

| Mean | Median | SD | Min | Max | ||

| GI | 0.760 | 0.730 | 0.071 | 0.653 | 0.930 | |

| RD | 0.000 | −0.029 | 0.085 | −0.050 | 0.965 | |

| ESG | 0.000 | 3.575 | 16.282 | −64.255 | 24.315 | |

| LAW | 0.711 | - | - | 0.000 | 1.000 | |

| GDP | 10.795 | 10.793 | 0.119 | 10.526 | 11.023 | |

| INDIV | 72.814 | 71.000 | 10.664 | 51.000 | 89.000 | |

| INDC | 0.036 | 0.018 | 0.048 | 0.017 | 0.255 | |

| SIZE | 16.546 | 16.579 | 1.530 | 11.335 | 20.053 | |

| LEV | 0.346 | 0.321 | 1.882 | −35.965 | 2.708 | |

| ROA | 0.082 | 0.075 | 0.056 | −0.144 | 0.290 | |

| CF | 0.139 | 0.128 | 0.114 | −0.516 | 1.022 | |

| Panel B: IR adopters (n = 194) | ||||||

| Mean | Median | SD | Min | Max | ||

| GI | 0.760 | 0.730 | 0.071 | 0.653 | 0.930 | |

| RD | −0.005 | −0.026 | 0.057 | −0.050 | 0.209 | |

| ESG | 3.227 | 6.310 | 15.001 | −64.255 | 24.315 | |

| LAW | 0.711 | - | - | 0.000 | 1.000 | |

| GDP | 10.795 | 10.793 | 0.119 | 10.526 | 11.023 | |

| INDIV | 72.814 | 71.000 | 10.678 | 51.000 | 89.000 | |

| INDC | 0.038 | 0.018 | 0.048 | 0.017 | 0.255 | |

| SIZE | 16.799 | 16.884 | 1.398 | 13.041 | 20.053 | |

| LEV | 0.439 | 0.300 | 0.372 | 0.000 | 1.826 | |

| ROA | 0.088 | 0.082 | 0.050 | −0.018 | 0.290 | |

| CF | 0.158 | 0.139 | 0.115 | −0.003 | 1.022 | |

| Panel C: IR non-adopters (n = 194) | ||||||

| Mean | Median | SD | Min | Max | ||

| GI | 0.760 | 0.730 | 0.071 | 0.653 | 0.930 | |

| RD | 0.005 | −0.031 | 0.106 | −0.050 | 0.965 | |

| ESG | −3.227 | −0.720 | 16.900 | −54.095 | 23.005 | |

| LAW | 0.711 | - | - | 0.000 | 1.000 | |

| GDP | 10.795 | 10.793 | 0.119 | 10.526 | 11.023 | |

| INDIV | 72.814 | 71.000 | 10.678 | 51.000 | 89.000 | |

| INDC | 0.035 | 0.018 | 0.048 | 0.017 | 0.255 | |

| SIZE | 16.292 | 16.231 | 1.616 | 11.335 | 19.528 | |

| LEV | 0.253 | 0.352 | 2.635 | −35.965 | 2.708 | |

| ROA | 0.076 | 0.068 | 0.060 | −0.144 | 0.258 | |

| CF | 0.120 | 0.117 | 0.109 | −0.516 | 0.507 | |

| Panel D | ||||||

| Comparison tests | Test statistics | |||||

| RD | a | −0.626 | ||||

| ESG | a | −4.108 | *** | |||

| INDC | a | 0.732 | ||||

| SIZE | a | −3.281 | *** | |||

| LEV | a | 0.795 | ||||

| ROA | a | 2.136 | ** | |||

| CF | a | 2.869 | *** | |||

| GI | GDP | INDIV | INDC | SIZE | LEV | ROA | CF | ESG | RD | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| GI | 1.000 | ||||||||||||||||||

| GDP | 0.399 | *** | 1.000 | ||||||||||||||||

| INDIV | 0.397 | *** | 0.224 | *** | 1.000 | ||||||||||||||

| INDC | −0.237 | *** | 0.042 | −0.044 | 1.000 | ||||||||||||||

| SIZE | 0.142 | *** | 0.039 | −0.023 | 0.091 | * | 1.000 | ||||||||||||

| LEV | −0.011 | −0.103 | ** | 0.075 | 0.188 | *** | −0.011 | 1.000 | |||||||||||

| ROA | 0.172 | *** | 0.133 | *** | 0.099 | * | −0.160 | *** | −0.091 | * | −0.185 | *** | 1.000 | ||||||

| CF | 0.114 | ** | −0.023 | 0.031 | 0.203 | *** | 0.158 | *** | 0.123 | ** | 0.279 | *** | 1.000 | ||||||

| ESG | 0.007 | 0.028 | −0.058 | 0.013 | 0.541 | *** | −0.033 | 0.023 | 0.118 | ** | 1.000 | ||||||||

| RD | 0.111 | ** | 0.277 | *** | −0.010 | −0.348 | *** | −0.015 | −0.202 | *** | 0.136 | *** | 0.021 | 0.135 | *** | 1.000 |

| C1 | C2 | C3 | C4 | |||||

|---|---|---|---|---|---|---|---|---|

| Coef. | Sig. | Coef. | Sig. | Coef. | Sig. | Coef. | Sig. | |

| constant | −65.348 | *** | −62.082 | *** | −53.308 | *** | −48.261 | *** |

| GI | 1.846 | *** | - | 2.132 | *** | 2.875 | *** | |

| RD | - | −5.339 | *** | −2.254 | *** | −5.424 | *** | |

| ESG | - | 0.036 | *** | 0.029 | *** | 0.037 | *** | |

| RD*ESG | - | 0.502 | *** | - | 0.507 | *** | ||

| Control variables: | ||||||||

| GDP | 4.914 | *** | 5.217 | *** | 4.161 | *** | 3.734 | *** |

| INDIV | 0.066 | *** | 0.040 | *** | 0.049 | *** | 0.036 | *** |

| INDC | −20.094 | *** | −22.497 | *** | −25.786 | *** | −22.537 | *** |

| SIZE | 0.288 | *** | 0.099 | * | 0.122 | ** | 0.100 | * |

| LEV | 0.158 | 0.163 | * | 0.170 | 0.160 | * | ||

| LAW | −0.015 | 0.203 | *** | 0.103 | ** | 0.213 | *** | |

| ROA | 5.818 | *** | 6.462 | ** | 6.185 | *** | 6.512 | ** |

| CF | 2.873 | ** | 2.907 | ** | 2.823 | ** | 2.946 | ** |

| Pseudo R sq. | 0.0661 | 0.1056 | 0.0874 | 0.1061 | ||||

| Nr. Of obs. | 388 | 388 | 388 | 388 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pinto, R.; Lourenço, I.; Simões, A. Does Innovation Spur Integrated Reporting? Sustainability 2023, 15, 657. https://doi.org/10.3390/su15010657

Pinto R, Lourenço I, Simões A. Does Innovation Spur Integrated Reporting? Sustainability. 2023; 15(1):657. https://doi.org/10.3390/su15010657

Chicago/Turabian StylePinto, Ricardo, Isabel Lourenço, and Ana Simões. 2023. "Does Innovation Spur Integrated Reporting?" Sustainability 15, no. 1: 657. https://doi.org/10.3390/su15010657

APA StylePinto, R., Lourenço, I., & Simões, A. (2023). Does Innovation Spur Integrated Reporting? Sustainability, 15(1), 657. https://doi.org/10.3390/su15010657