Comparison of the Technical Efficiency of Construction Industries—A Case Study of Taiwan and Mainland China

,

,  , and

, and

Abstract

:1. Introduction

- What are the respective TE values for various operations aspects as well as the strengths and weaknesses of construction companies on both sides of the Taiwan Strait?

- What is the TE of selected Taiwanese construction companies, and how do they compare to mainland China?

1.1. Approaches to Measuring Efficiency

1.1.1. Stochastic Frontier Analysis

1.1.2. Data Envelope Analysis (DEA)

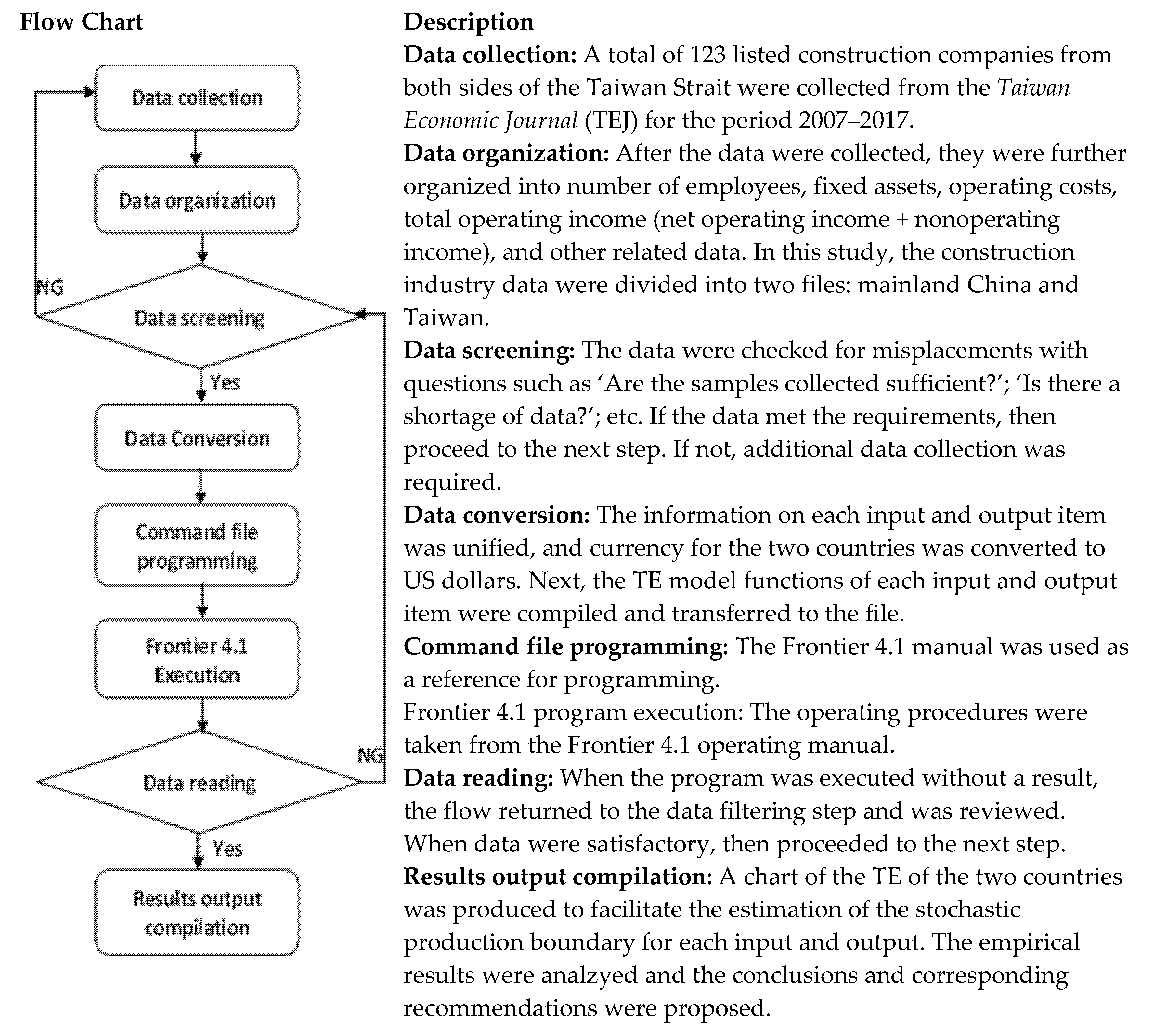

2. Materials and Methods

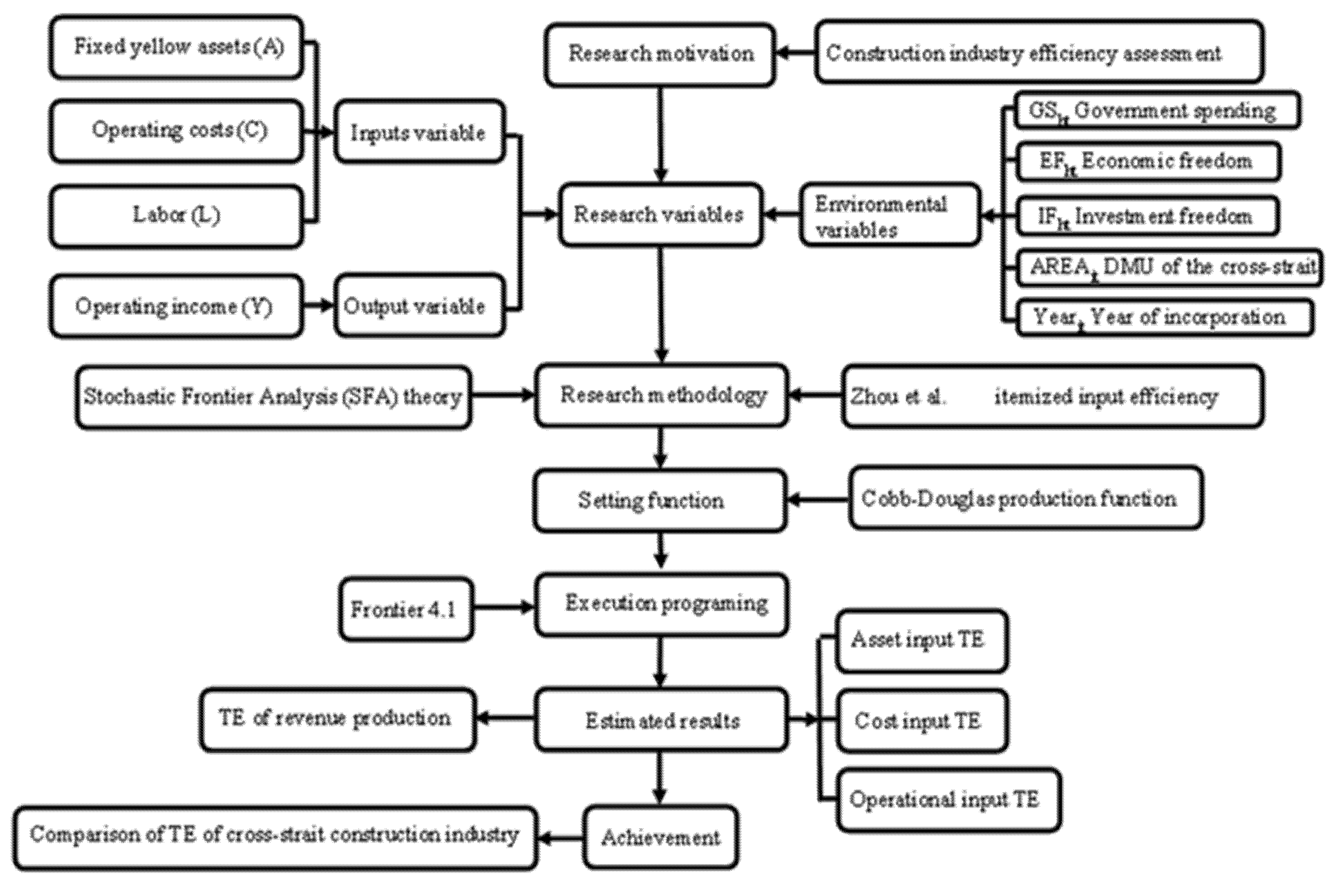

2.1. Research Model

2.2. Data Sources and Variables

3. Results

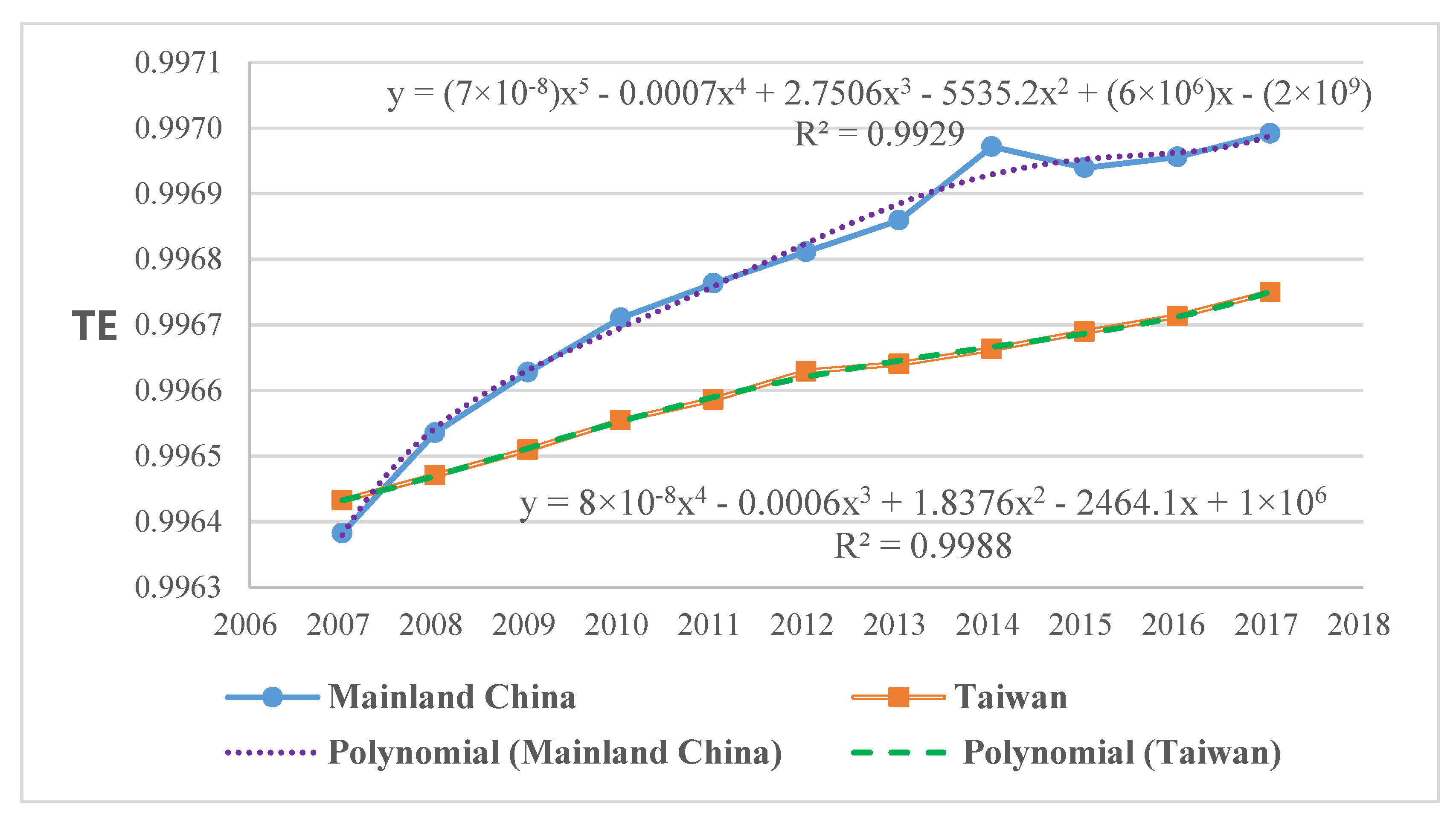

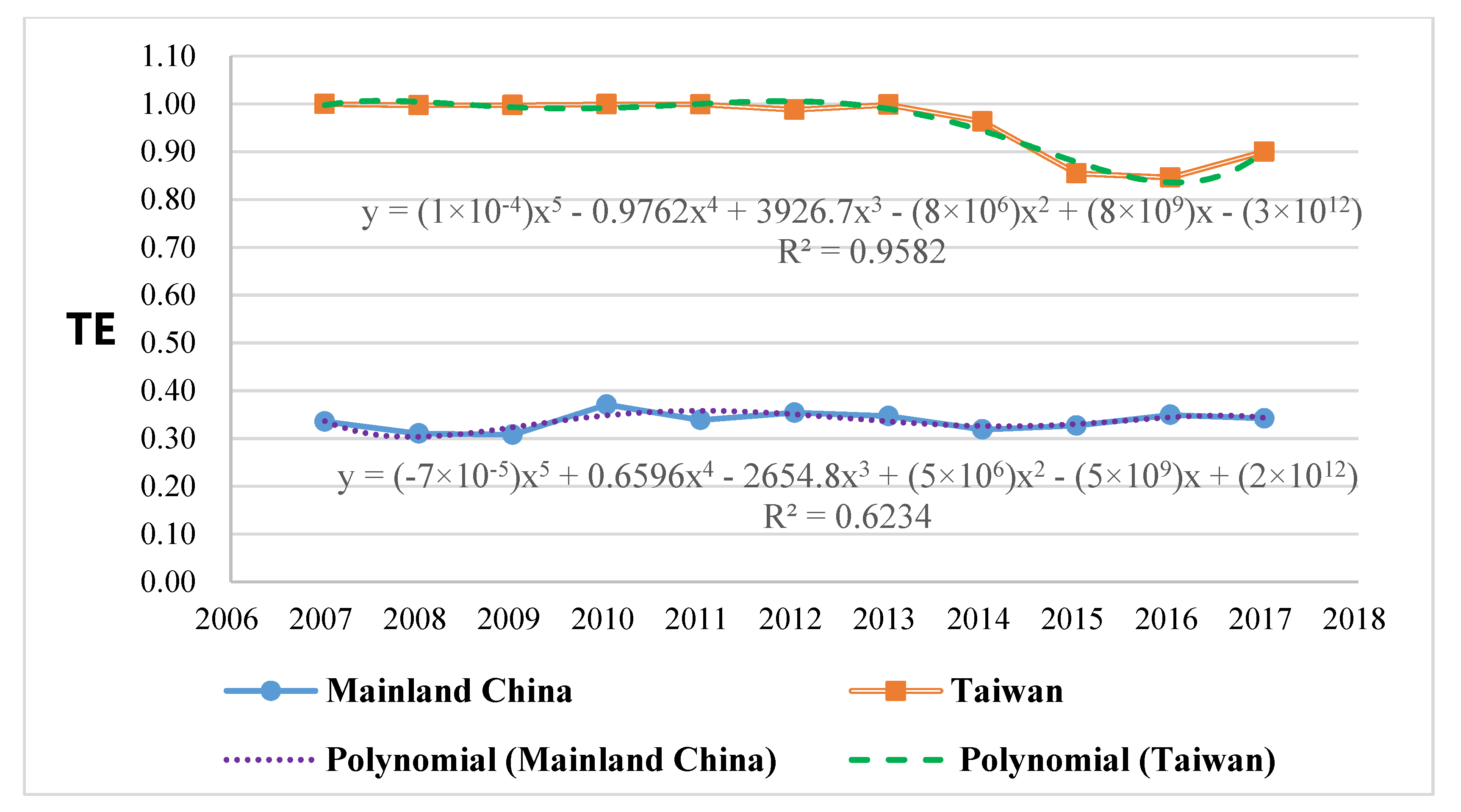

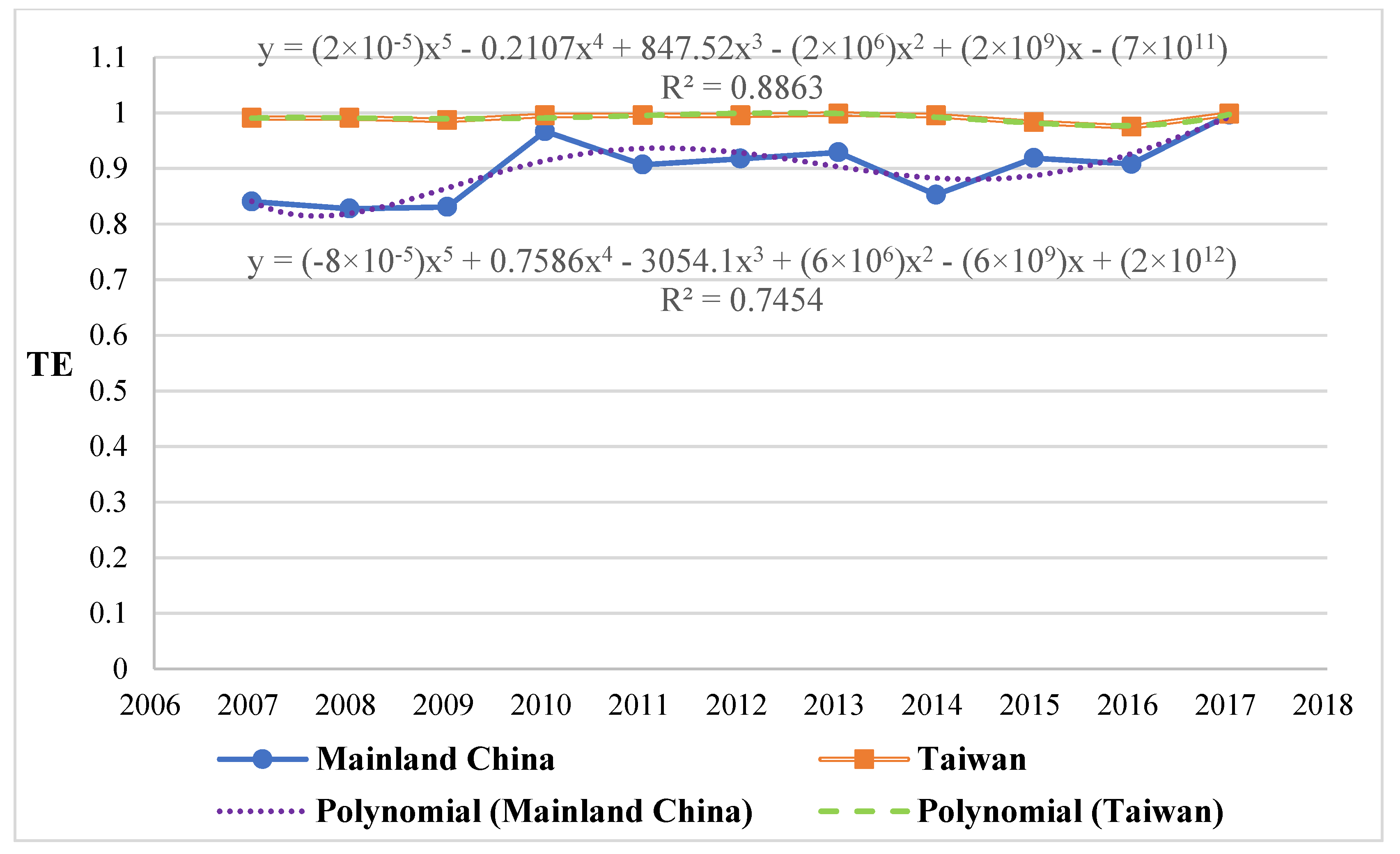

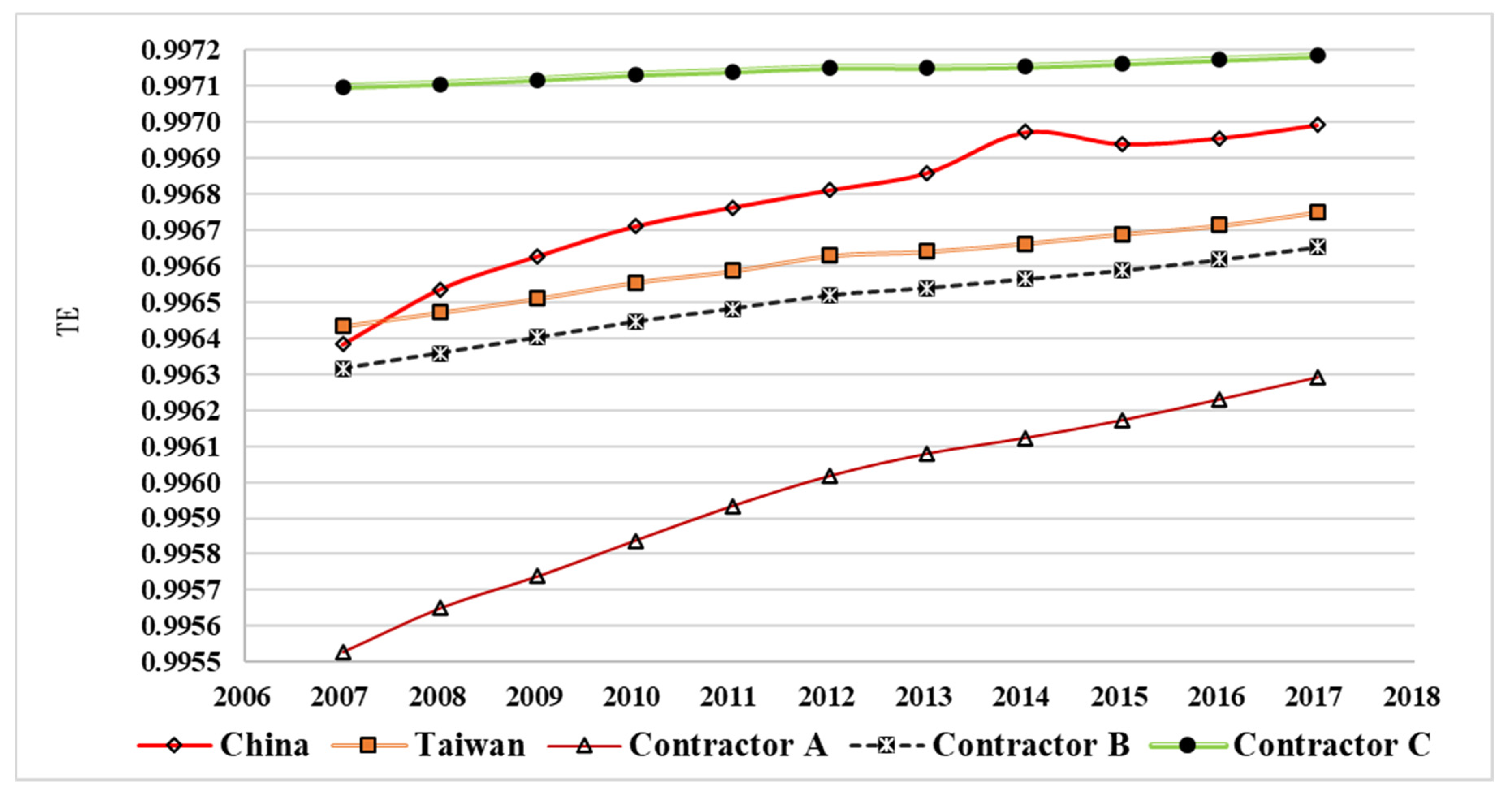

3.1. Technical Efficiency (TE) Analysis of Asset Inputs

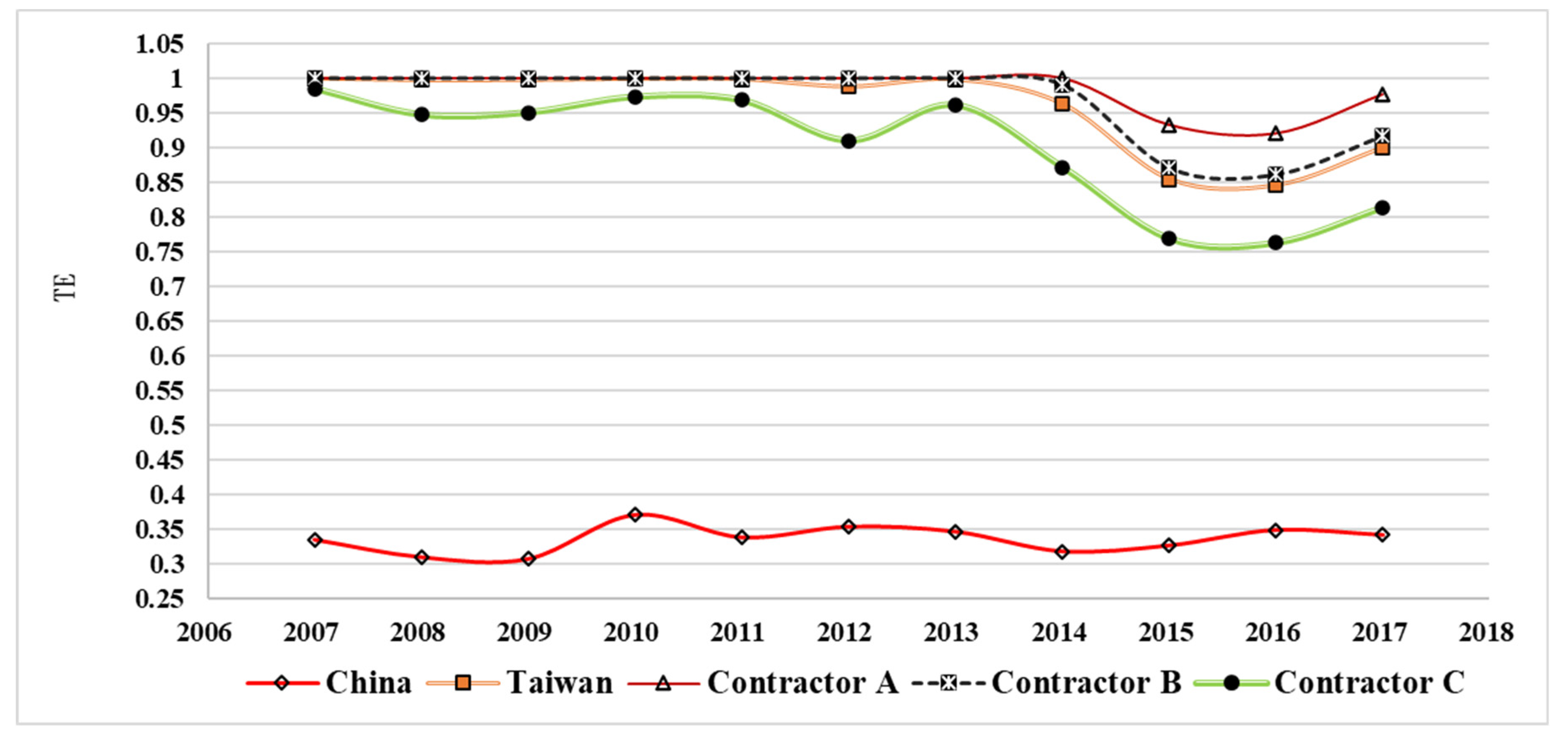

3.2. TE of Cost Inputs

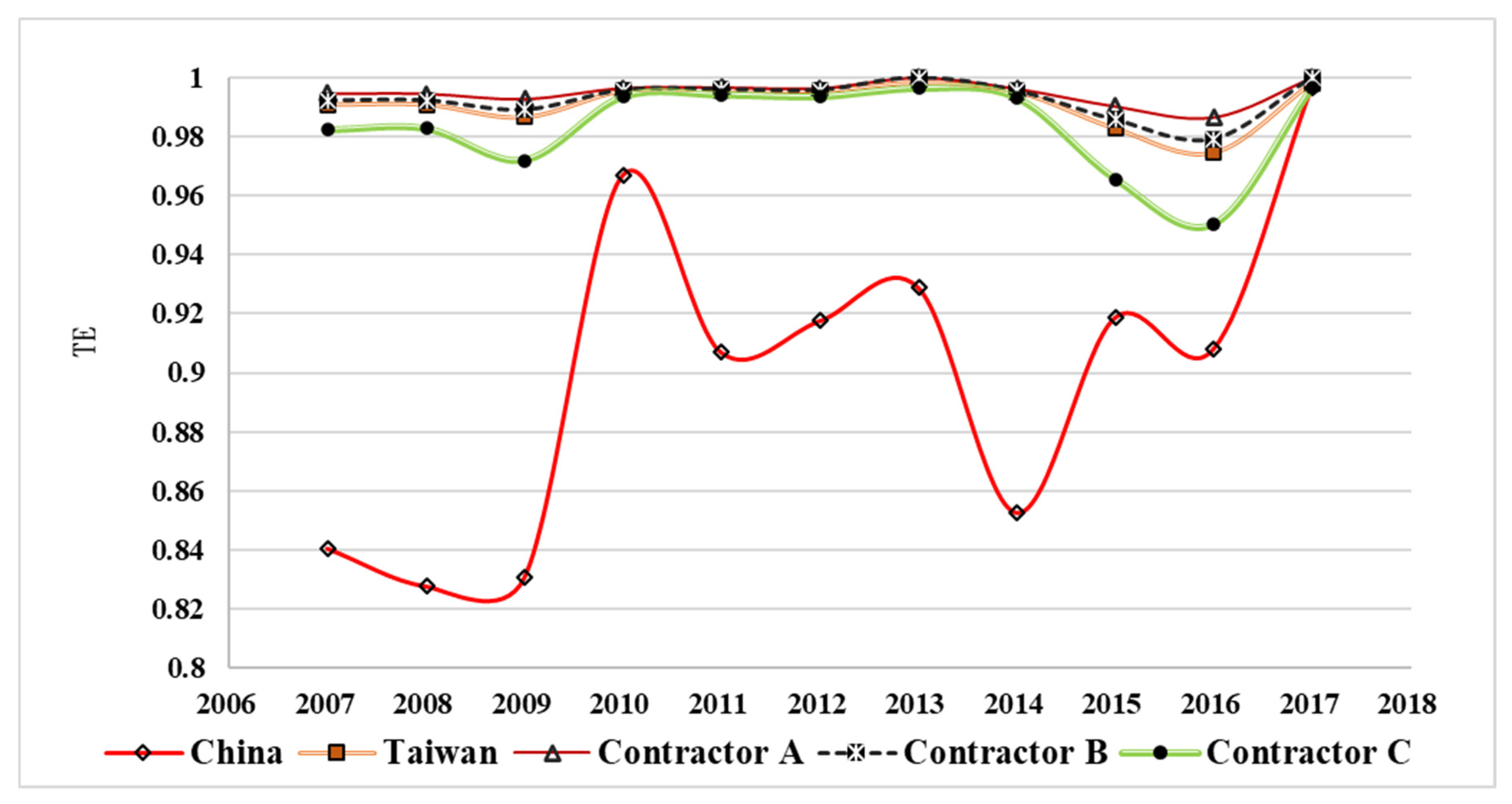

3.3. TE of Labor Inputs

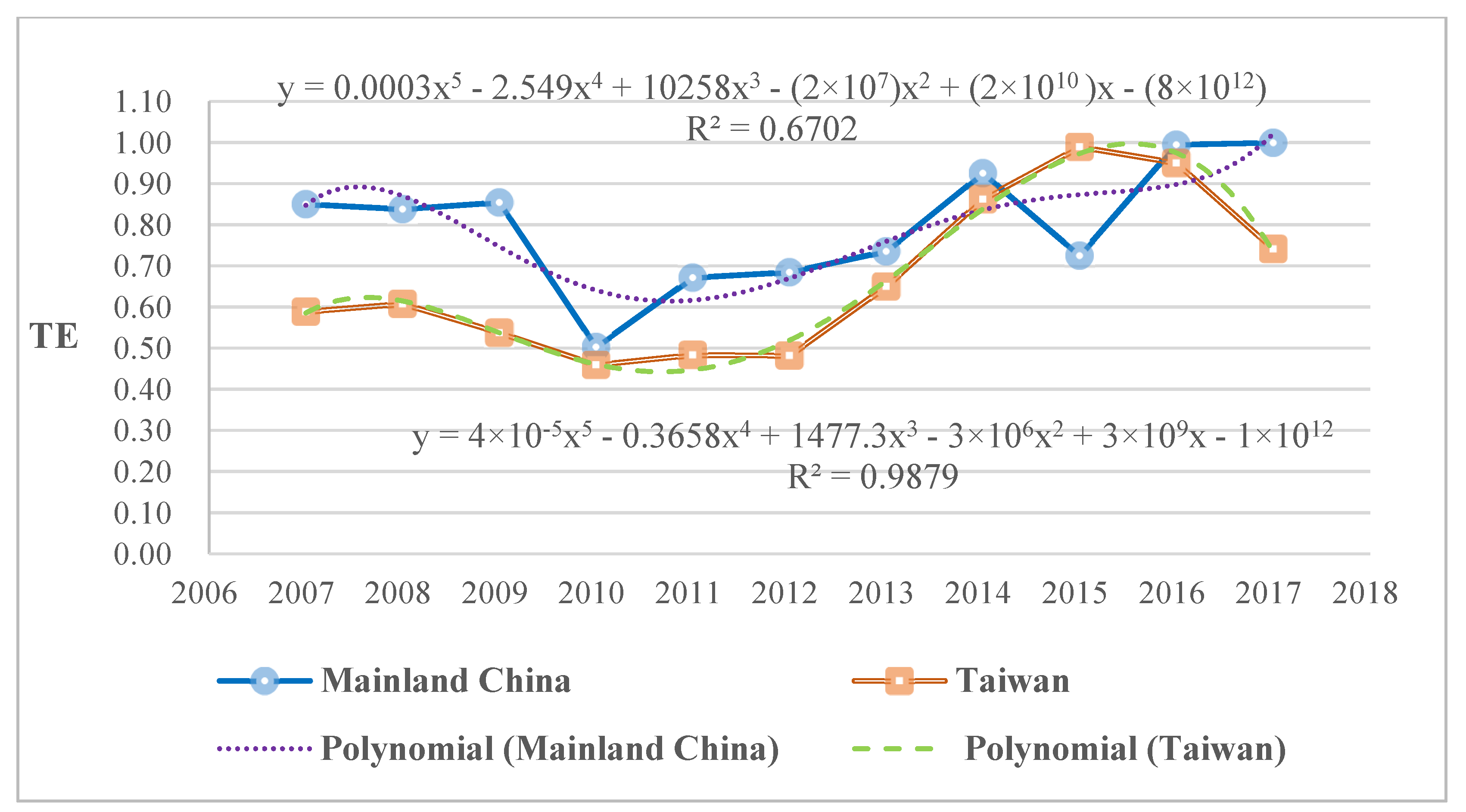

3.4. TE Analysis of Revenue Production

4. Discussion

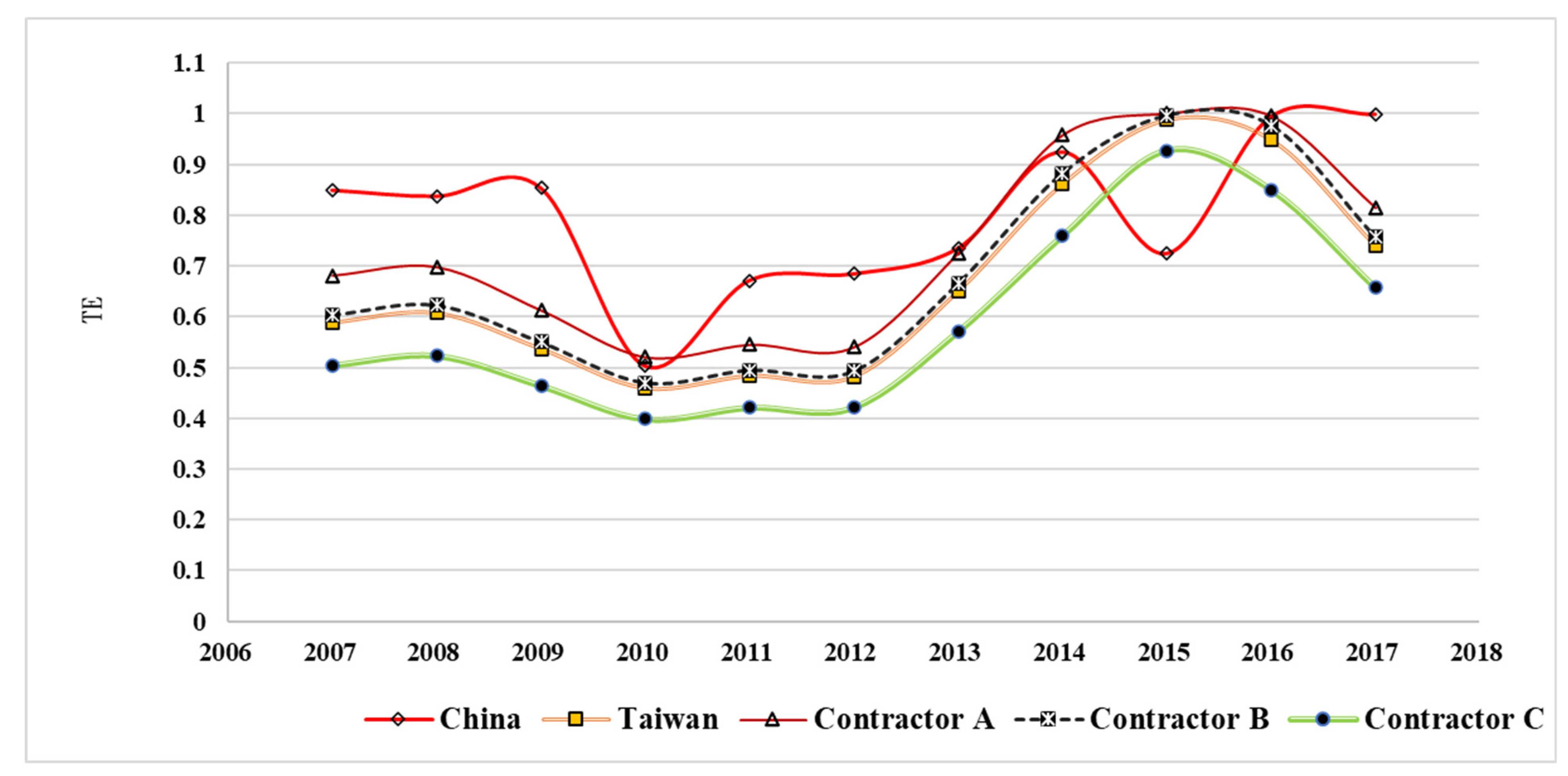

4.1. Company Comparison of Asset Inputs

4.2. Comparison of TE of Cost Inputs

4.3. Comparison of TE of labor inputs

4.4. Comparison of TE of Revenue Production

5. Conclusions

- Prior to the impacts of COVID-19, some Taiwanese companies had the scale and market advantages needed to enter the mainland Chinese market with obvious advantages in terms of labor input factors and revenue output. Further research on establishing cooperative alliances post-COVID-19 may be a practical strategy to consider for Taiwanese companies seeking to enter the mainland Chinese market.

- Changes in government policy are the key factor behind the large fluctuation of the cross-Strait construction industry’s asset investment. Before entering the construction market in mainland China, the policies in place need to allow the freedom and consistency required to effectively support construction companies operating across the Taiwan Strait.

- The impact of macroeconomic input and output variables for each item is not significant in the short term (<1 year). Where the impact becomes more pronounced is in the medium and long term, necessitating careful ongoing evaluation and planning.

- In line with current policies or plans (e.g., Taiwan’s Southbound Policy), these findings provide a useful reference for further exploration and analysis of potential new opportunities for Taiwan’s construction industry throughout the Asian region.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Chen, W.T.; Merrett, H.C.; Huang, Y.H.; Bria, T.A.; Lin, Y.H. Exploring the relationship between safety climate and worker safety behavior on building construction sites in Taiwan. Sustainability 2021, 13, 3326. [Google Scholar] [CrossRef]

- Pan, N.H.; Lee, M.L. Enhancing construction companies’ marketing strategies: The construction industry in Taiwan. Int. J. Organ. Innov. 2017, 10, 143–164. [Google Scholar]

- Chien, H.J.; Barthorpe, S. The current state of information and communication technology usage by small and medium Taiwanese construction companies. J. Inf. Technol. Constr. 2009, 15, 75–85. [Google Scholar]

- Amoah, C.; Bamfo-Agyei, E.; Simpeh, F. The COVID-19 pandemic: The woes of small construction firms in Ghana. Smart Sustain. Built Environ. 2021, 11, 2046–6099. [Google Scholar] [CrossRef]

- Pao, H.W.; Wu, H.I.; Ho, S.P.; Lee, C.Y. From partner selection to trust dynamics: Evidence of the cross-country partnership of Taiwanese construction firms. J. Adv. Manag. Res. 2015, 12, 128–140. [Google Scholar] [CrossRef]

- Chen, T.T.; Wu, F.Y. Exploring critical factors for partnering in the Taiwanese construction industry. In Proceedings of the International Conference on Engineering, Project, and Production Management, Pingtung, Taiwan, 14–15 October 2010. [Google Scholar]

- The Construction and Planning Agent—Ministry of the Interior (CPAMI). Annual Report—2020; Ministry of the Interior: Taipei City, Taiwan, 2021. [Google Scholar]

- Fernandes, D.S.; Joseph, G. Organisational Strategies for Competitive Advantage in the Construction Industry: Chinese Dominance in Southern Africa. J. Constr. Dev. Ctries. 2020, 25, 1–38. [Google Scholar] [CrossRef]

- Lin, C.L.; Fan, C.; Chen, B.K. Hybrid Analytic Hierarchy Process–Artificial Neural Network Model for Predicting the Major Risks and Quality of Taiwanese Construction Projects. Appl. Sci. 2022, 12, 7790. [Google Scholar] [CrossRef]

- Public Construction Commission (PCC). Engineering Industry Globalization Promotion Plan (Policy White Paper)―Phase 2 (2018–2021); Executive Yuan: Taipei City, Taiwan, 2017.

- Public Construction Commission (PCC). Engineering Industry Globalization Promotion Plan (Policy Release)―Phase 3 (2022–2025); Executive Yuan: Taipei City, Taiwan, 2021.

- Chen, J.C. Strengthening the Scientific Research Institutions of the Ministry of Construction and Enhancing the International Competitiveness of the Construction Industry; The Storm Media: Taipei, Taiwan, 2021. [Google Scholar]

- Lin, B.J. The Development Status and Trend of Taiwan Construction Industry. Taiwan Econ. Outlook 2017, 174, 46–48. [Google Scholar]

- Hossain, M.U.; Ng, S.T.; Antwi-Afari, P.; Amor, B. Circular economy and the construction industry: Existing trends, challenges and prospective framework for sustainable construction. Renew. Sustain. Energy Rev. 2020, 130, 109948. [Google Scholar] [CrossRef]

- Dzeng, R.J.; Wu, J.S. Efficiency Measurement of the Construction Industry in Taiwan: A Stochastic Frontier Cost Function Approach. Constr. Manag. Econ. 2013, 31, 335–344. [Google Scholar] [CrossRef]

- Chen, J.H. Evaluation of operating performance of listed construction companies in Taiwan—Application of data envelopment analysis. J. Constr. 2018, 106, 17–29. [Google Scholar]

- Dzeng, R.J.; Wu, J.S. The Cost Efficiency of Construction Industry in Taiwan. Open Constr. Build. Technol. J. 2012, 6, 8–16. [Google Scholar] [CrossRef] [Green Version]

- Fernandez-Lopez, X.L.; Coto-Millan, P. From the boom to the collapse: A technical efficiency analysis of the Spanish construction industry during the financial crisis. Constr. Econ. Build. 2015, 15, 104–117. [Google Scholar] [CrossRef] [Green Version]

- Hendrawan, R.; Utama, P.P. Efficiency Measurement of Building Construction Sector Companies Listed on Indonesia Stock Exchange: Stochastic Frontier Analysis Approach. Asian J. Manag. Sci. Educ. 2020, 9, 1–15. [Google Scholar]

- Yin, T. Research on Spatial Spillover Effect of Total Factor Productivity in Construction Industry: Evidence from Yangtze River Delta Region in China. Am. J. Ind. Bus. Manag. 2021, 11, 1140–1152. [Google Scholar] [CrossRef]

- Boyd, G.A.; Lee, J.M. Measuring plant level energy efficiency and technical change in the U.S. metal-based durable manufacturing sector using stochastic frontier analysis. Energy Econ. 2019, 81, 159–174. [Google Scholar] [CrossRef] [Green Version]

- Wanke, P.; Tan, Y.; Antunes, J.; Hadi-Vencheh, A. Business environment drivers and technical efficiency in the Chinese energy industry: A robust Bayesian stochastic frontier analysis. Comput. Ind. Eng. 2020, 144, 10648. [Google Scholar] [CrossRef]

- Sayavong, V. Technical inefficiency of the manufacturing sector in Laos: A case study of the firm survey. J. Asian Bus. Econ. Stud. 2021; ahead-of-print. [Google Scholar]

- Jian, L.; Peng, L.; Shan, F.; Ping, W. Administrative hierarchy, city size, and urban productivity. Macro-Qual. Res. 2018, 1, 31–43. [Google Scholar]

- Jin, G.; Wu, F.; Li, Z.H.; Guo, B.S.; Zhao, X. Measurement and analysis of land use and ecological efficiency in rapidly urbanizing areas. J. Ecol. 2017, 37, 8048–8057. [Google Scholar]

- Hsieh, H.P. Study on the Operational Efficiency of Japanese Securities Firms. Master’s Thesis, Institute of Business Administration, School of Management, National Chiao Tung University, Hsinchu, Taiwan, 2016. [Google Scholar]

- Chang, T.P.; Hu, J.L.; Chiu, L.H. Application of stochastic common border analysis to explore the efficiency of cross-strait banking inputs. Appl. Econ. Ser. 2016, 100, 149–181. [Google Scholar]

- Chang, W.L. Itemized Input Efficiency of Mutual Funds in Taiwan. Master’s Thesis, Institute of Business Administration, School of Management National Chiao Tung University, Hsinchu, Taiwan, 2013. [Google Scholar]

- Hu, J.L.; Honma, S.; Hsieh, H.P. Input efficiency of Japanese securities firms: An application of Stochastic Frontier Analysis. J. Manag. Res. 2018, 18, 71–89. [Google Scholar]

- Chang, L.C. Study on the Efficiency of Sub-Inputs of Taiwan’s Securities Firms: Application of Stochastic Boundary Analysis. Master’s Thesis, Graduate School of Management, National Chiao Tung University, Hsinchu, Taiwan, 2013. [Google Scholar]

- Charnes, A.; Cooper, W.W.; Rhodes, E. Measuring the efficiency of decision making units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Yang, Z.; Fang, H.; Xue, X. Sustainable efficiency and CO2 reduction potential of China’s construction industry: Application of a three-stage virtual frontier SBM-DEA model. J. Asian Archit. Build. Eng. 2021, 21, 604–617. [Google Scholar] [CrossRef]

- Park, J.L.; Yoo, S.K.; Lee, J.S.; Kim, J.H.; Kim, J.J. Comparing the Efficiency and Productivity of Construction Firms in China, Japan, and Korea Using DEA and DEA-based Malmquist. J. Asian Archit. Build. Eng. 2015, 14, 57–64. [Google Scholar] [CrossRef] [Green Version]

- Wong, W.P.; Gholipour, H.F.; Bazrafshan, E. How Efficient Are Real Estate and Construction Companies in Iran’s Close Economy? Int. J. Strateg. Prop. Manag. 2012, 16, 392–413. [Google Scholar] [CrossRef] [Green Version]

- Al-Malkawi, H.A.N.; Pillai, R. The Impact of Financial Crisis on UAE Real Estate and Construction Sector: Analysis and Implications. Humanomics 2013, 29, 115–135. [Google Scholar] [CrossRef]

- You, T.; Zi, H. The economic crisis and efficiency change: Evidence from the Korean construction industry. Appl. Econ. 2007, 39, 1833–1842. [Google Scholar] [CrossRef]

- Kapelko, M.; Lansink, A.O. Technical efficiency and its determinants in the Spanish construction sector pre- and post-financial crisis. Int. J. Strateg. Prop. Manag. 2015, 19, 96–109. [Google Scholar] [CrossRef]

- Lee, S.M. Competitive Analysis of Taiwan’s Construction Industry. Master’s Thesis, Department of Civil and Disaster Prevention Engineering, National Union University, Miaoli, Taiwan, 2011. [Google Scholar]

- Chen, B.L.; Chou, K.H.; Cheng, Y.J.; Lin, C.C.; Dai, Y.C. Analysis of operating efficiency of listed construction companies in Taiwan. J. Constr. 2010, 1, 25–50. [Google Scholar]

- Huang, T.S.; Chang, P.K. A comparison of technical efficiency of common boundary in our construction industry. Manag. Syst. 2015, 22, 149–174. [Google Scholar]

- Mujaddad, H.G.; Ahmad, H.K. Measuring efficiency of Manufacturing Industries in Pakistan: An Application of DEA Double Bootstrap Technique. Pak. Econ. Soc. Rev. 2007, 54, 363–384. [Google Scholar]

- Erena, O.T.; Kalko, M.M.; Debele, S.A. Technical efficiency, technological progress and productivity growth of large and medium manufacturing industries in Ethiopia: A data envelopment analysis. Cogent Econ. Financ. 2021, 9, 1997160. [Google Scholar] [CrossRef]

- Goncharuk, A.G. Impact of political changes on industrial efficiency: A case of Ukraine. J. Econ. Stud. 2007, 34, 324–340. [Google Scholar] [CrossRef]

- Goncharuk, A.G. Using the DEA in efficiency management in industry. Int. J. Product. Qual. Manag. 2007, 2, 241–262. [Google Scholar] [CrossRef]

- Hu, J.L.; Chang, T.P.; Chu, H.H. Comparison of itemized input efficiency of cross-strait life insurance industry: Application of stochastic boundary analysis. Soochow J. Econ. Bus. 2014, 85, 41–46. [Google Scholar]

- Tsai, Y.Y. Efficiency of Itemized Inputs in Taiwan Regional Funds: An Application of Stochastic Boundary Analysis. Master’s Thesis, Institute of Business Administration, College of Management, National Chiao Tung University, Hsinchu, Taiwan, 2016. [Google Scholar]

- Huang, K.R.; Fu, C.T.; Huang, M.E. Performance Evaluation: Theory and Application of Efficiency and Productivity; Xin Lu Book Co.: Taipei, Taiwan, 2010. [Google Scholar]

- Xie, T.; Zhu, X. Research on the measurement of contribution value of scientific and technological talents in China’s mining industry—Innovative application based on “Cobb Douglas production function method”. In IOP Conference Series: Earth and Environmental Science; IOP Publishing: Bristol, UK, 2022; Volume 1087. [Google Scholar]

- McKenzie, T. Cobb-Douglas Production Function. 2022. Available online: https://inomics.com/terms/cobb-douglas-production-function-1456726 (accessed on 23 July 2022).

- Zhou, P.B.; Ang, W.; Zhou, D.Q. Measuring Economy-Wide Energy Efficiency Performance: A Parametric Frontier Approach. Appl. Energy 2012, 90, 196–200. [Google Scholar] [CrossRef]

- Battese, G.E.; Coelli, T.J. A Model for Technical Inefficiency Effects in a Stochastic Frontier Production Function for Panel Data. J. Product. Anal. 1995, 20, 325–332. [Google Scholar] [CrossRef] [Green Version]

- Coelli, T.J. A Guide to FRONTIER Version 4.1: A Computer Program for Stochastic Frontier Production and Cost Function Estimation; CPEA Working Papers: Armidale, Australia, 1996. [Google Scholar]

- Zhang, B.G.; Huang, T.X.; Guo, J.Y. Analysis of Productivity Changes at the Common Boundary of Listed Construction and Architecture Companies: Application of Input-Oriented Distance Function. Soochow J. Econ. Bus. 2014, 85, 1–40. [Google Scholar]

- Wu, J.H.; Ho, B.J.; Huang, Y.C. The Performances and Management Strategy for Taiwan’s Construction Industries. J. Archit. 2008, 64, 25–48. [Google Scholar]

- Wu, C.H. Application of the Random Boundary Method to the Cost Efficiency and Influence Factors of Construction Companies. Ph.D. Thesis, Department of Civil Engineering, National Chiao Tung University, Hsinchu, Taiwan, 2013. [Google Scholar]

- Wang, K.T. Performance Evaluation of Listed Cabinet-Building Companies in Taiwan-Application of the Random Production Boundary Method. Master’s Thesis, Ling Tung University of Science and Technology, Taichung, Taiwan, 2017. [Google Scholar]

- Zheng, X.; Chau, K.W.; Hui, E.C.M. Efficiency Assessment of Listed Real Estate Companies: An Empirical Study of China. Int. J. Strateg. Prop. Manag. 2011, 15, 91–104. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Items | Inputs and Outputs | Huang & Chang [40] | Zhang et al. [53] | Wong et al. [34] | Wu et al. [54] | Wu [55] | Wang [56] | Dzeng & Wu [17] | Dzeng & Wu [15] | Zheng et al. [57] | Chen [16] |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Inputs | Capital price | ● | |||||||||

| Labor price | ● | ||||||||||

| Equipment cost | ● | ||||||||||

| Equipment cost | ● | ||||||||||

| Total assets | ● | ● | ● | ||||||||

| Total liabilities | ● | ||||||||||

| Shareholders’ equity | ● | ||||||||||

| Capital stock | ● | ● | ● | ● | ● | ||||||

| Fixed assets | ● | ||||||||||

| Net fixed assets | ● | ● | ● | ||||||||

| Operating costs | ● | ● | ● | ● | ● | ● | ● | ||||

| Number of employees | ● | ● | ● | ● | ● | ● | ● | ● | ● | ||

| Outputs | Debt ratio | ● | |||||||||

| Gross profit from operations | ● | ● | |||||||||

| Net income after tax | ● | ||||||||||

| Operating income | ● | ● | ● | ● | |||||||

| Net income from operations | ● | ● | ● | ● | ● | ● | |||||

| Nonoperating income | ● | ● |

| Item | Input/output | Definition |

|---|---|---|

| Inputs | Fixed assets (A) | Cost of fixed assets and net of accumulated depreciation as of the end of the year. |

| Operating cost (C) | The income statement includes operating costs plus operating expenses, net of employment costs. | |

| Number of employees (L) | Total number of employees at the end of the fiscal year. | |

| Output | Operating income (Y) | “Net operating income” is total operating income annually, net of refunds and discounts, and “non-operating income” is total non-operating income in the income statement. Net operating income + nonoperating income is presented in this study. |

| Year | Inputs Variables | Output Variable | ||

|---|---|---|---|---|

| Fixed Assets (A) | Operating Costs (C) | Number of Employees (L) | Operating Income (Y) | |

| 2007 | 150,717 (57,327) | 1,284,813 (593,683) | 11,373 (5596) | 1,444,610 (665,312) |

| 2008 | 207,119 (81,728) | 1,756,323 (814,468) | 11,875 (5735) | 1,974,320 (911,420) |

| 2009 | 267,151 (107,176) | 2,588,635 (1,225,333) | 12,462 (6041) | 2,894,243 (1,360,869) |

| 2010 | 321,762 (130,229) | 3,542,627 (1,687,351) | 13,410 (6403) | 3,954,318 (1,869,421) |

| 2011 | 389,618 (149,902) | 4,034,773 (1,854,236) | 14,464 (6774) | 4,563,122 (2,086,602) |

| 2012 | 440,382 (163,840) | 4,532,648 (2,074,113) | 15,612 (7024) | 5,134,554 (2,339,479) |

| 2013 | 501,888 (183,962) | 5,483,698 (2,520,506) | 16,303 (7233) | 6,196,908 (2,829,566) |

| 2014 | 516,332 (195,272) | 6,072,390 (2,783,455) | 16,886 (7483) | 6,907,099 (3,153,419) |

| 2015 | 558,257 (205,911) | 6,305,863 (2,898,355) | 17,081 (7528) | 7,175,088 (3,286,399) |

| 2016 | 587,839 (206,890) | 6,513,967 (2,966,969) | 17,541 (7620) | 7,265,120 (3,281,260) |

| 2017 | 645,605 (221,718) | 6,969,090 (3,165,771) | 18,352 (7764) | 7,812,648 (3,517,100) |

| Year | Inputs Variables | Outputs Variables | ||

|---|---|---|---|---|

| Fixed Assets (A) | Operating Costs (C) | Number of Employees (L) | Operating Income (Y) | |

| 2007 | 39,679 (8,979) | 96,686 (14,396) | 340 (77) | 124,596 (17,521) |

| 2008 | 47,513 (13,481) | 102,857 (16,936) | 338 (78) | 128,247 (19,796) |

| 2009 | 46,918 (13,470) | 96,016 (14,627) | 334 (78) | 125,336 (18,882) |

| 2010 | 51,545 (14,884) | 109,696 (17,745) | 370 (86) | 148,894 (23,951) |

| 2011 | 57,923 (17,439) | 114,407 (18,452) | 399 (97) | 159,119 (224,531) |

| 2012 | 66,471 (20,403) | 117,536 (18,761) | 379 (94) | 165,057 (23,965) |

| 2013 | 40,004 (13,904) | 140,617 (22,953) | 411 (102) | 200,759 (30,915) |

| 2014 | 39,992 (14,844) | 125,038 (22,768) | 402 (98) | 174,453 (29,844) |

| 2015 | 42,344 (15,077) | 114,432 (20,578) | 401 (98) | 156,252 (27,129) |

| 2016 | 39,507 (12,395) | 118,079 (21,294) | 365 (79) | 156,935 (27,267) |

| 2017 | 36,407 (8490) | 110,001 (15,356) | 359 (78) | 146,805 (20,010) |

| Variable | Mainland China Average | Taiwan Average | t Test (p-Value) |

|---|---|---|---|

| Fixed assets (A) | 416,970 | 46,209 | 7.4926 (p < 0.001) |

| Operating costs (C) | 4,462,256 | 113,215 | 6.4942 (p < 0.001) |

| Number of employees (L) | 15,033 | 372 | 7.1173 (p < 0.001) |

| Operating income (Y) | 5,029,275 | 153,314 | 6.4975 (p < 0.001) |

| Company | Capital (NTD *) | Ratio of the Main Products |

|---|---|---|

| A | 2,085,205 | Construction (99.6%), Engineering (0.4%) |

| B | 1,134,400 | Office Building (32.3%), Civil Engineering (24.6%), Other Projects (20.7%) |

| C | 3,475,274 | Engineering (100%) |

| Parameters | Relationship | Standard Deviation | t-Value |

|---|---|---|---|

| β0 | −1.3646 | 0.3410 | −4.0017 *** |

| lnLit | −0.7965 | 0.0418 | −19.0331 *** |

| lnCit | 0.0782 | 0.0843 | 0.9273 |

| lnYit | −0.3435 | 0.0995 | −3.4533 *** |

| δ0 | 5.2670 | 1.2260 | 4.2963 *** |

| GSht | 3.2661 | 0.6345 | 5.1473 *** |

| EFht | −7.9755 | 1.2780 | −6.2407 *** |

| IFht | −3.7200 | 0.6250 | −5.9521 *** |

| AREAit | −3.1291 | 0.5086 | −6.1527 *** |

| YEARit | 0.1755 | 0.0381 | 4.6025 *** |

| σ² | 2.4375 | 0.1065 | 22.8777 *** |

| γ | 1 × 10−4 | 7 × 10−6 | 21.0489 *** |

| log likelihood function = −2527.15 | |||

| Total obs. 1353 | |||

| Parameters | Relationship | Standard Deviation | t-Value |

|---|---|---|---|

| β0 | 1.2259 | 0.0891 | 13.7631 *** |

| lnAit | 0.0057 | 0.0083 | 0.6882 |

| lnLit | −0.0372 | 0.0141 | −2.6415 *** |

| lnYit | −1.0590 | 0.0122 | −86.8771 *** |

| δ0 | −0.0057 | 0.7377 | −0.0077 |

| GSht | −0.0055 | 0.7771 | −0.0071 |

| EFht | 0.0011 | 0.6788 | 0.0017 |

| IFht | 0.0030 | 0.5854 | 0.0051 |

| AREAit | −0.0214 | 0.4161 | −0.0515 |

| YEARit | −0.0283 | 0.1022 | −0.2765 |

| σ² | 0.2338 | 0.0112 | 20.9461 *** |

| γ | 0.0016 | 0.0015 | 1.0719 *** |

| log likelihood function = | −941.17 | ||

| Total obs. | 1353 | ||

| Parameters | Relationship | Standard Deviation | t-Value |

|---|---|---|---|

| β0 | 3.0478 | 0.1756 | 17.3557 *** |

| lnAit | −0.2472 | 0.0138 | −17.9752 *** |

| lnCit | −0.1185 | 0.0492 | −2.4078 ** |

| lnYit | −0.4043 | 0.0558 | −7.2458 *** |

| δ0 | −4.4145 | 0.9773 | −4.5169 *** |

| GSht | 1.0798 | 0.2985 | 3.6177 *** |

| EFht | 2.8631 | 0.6725 | 4.2571 *** |

| IFht | 1.2688 | 0.2855 | 4.4447 *** |

| AREAit | 2.3278 | 0.2817 | 8.2648 *** |

| YEARit | 0.1500 | 0.0367 | 4.0897 *** |

| σ² | 0.7753 | 0.0291 | 26.6518 *** |

| γ | 2 × 10−5 | 8× 10−6 | 2.1515 ** |

| log likelihood function = | −1747.22 | ||

| Total obs. | 1353 | ||

| Parameters | Relationship | Standard Deviation | t-Value |

|---|---|---|---|

| β0 | 1.7617 | 0.0469 | 37.5761 *** |

| lnAit | 0.0365 | 0.0072 | 5.0947 *** |

| lnCit | 0.8242 | 0.0073 | 112.1341 *** |

| lnLit | 0.0512 | 0.0080 | 6.3601 *** |

| δ0 | −1.4463 | 0.2328 | −6.2112 *** |

| GSht | 0.8719 | 0.3408 | 2.5584 ** |

| EFht | −1.2415 | 0.3051 | −4.0694 *** |

| IFht | 1.8899 | 0.6449 | 2.9308 *** |

| AREAit | 0.8029 | 0.2346 | 3.4227 *** |

| YEARit | 0.0547 | 0.0140 | 3.9140 *** |

| σ² | 0.1879 | 0.0070 | 26.8012 *** |

| γ | 0.0030 | 0.0018 | 1.6731 * |

| log likelihood function = | −747.05 | ||

| Total obs. | 1353 | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, W.T.; Kiani, A.K.; Wu, M.-T.; Merrett, H.C.; Wang, C.-H. Comparison of the Technical Efficiency of Construction Industries—A Case Study of Taiwan and Mainland China. Sustainability 2023, 15, 941. https://doi.org/10.3390/su15020941

Chen WT, Kiani AK, Wu M-T, Merrett HC, Wang C-H. Comparison of the Technical Efficiency of Construction Industries—A Case Study of Taiwan and Mainland China. Sustainability. 2023; 15(2):941. https://doi.org/10.3390/su15020941

Chicago/Turabian StyleChen, Wei Tong, Adiqa Kausar Kiani, Ming-Tsung Wu, Hew Cameron Merrett, and Chih-Hsing Wang. 2023. "Comparison of the Technical Efficiency of Construction Industries—A Case Study of Taiwan and Mainland China" Sustainability 15, no. 2: 941. https://doi.org/10.3390/su15020941

APA StyleChen, W. T., Kiani, A. K., Wu, M. -T., Merrett, H. C., & Wang, C. -H. (2023). Comparison of the Technical Efficiency of Construction Industries—A Case Study of Taiwan and Mainland China. Sustainability, 15(2), 941. https://doi.org/10.3390/su15020941