Impact of Environmental Regulation on Corporate Green Technological Innovation: The Moderating Role of Corporate Governance and Environmental Information Disclosure

Abstract

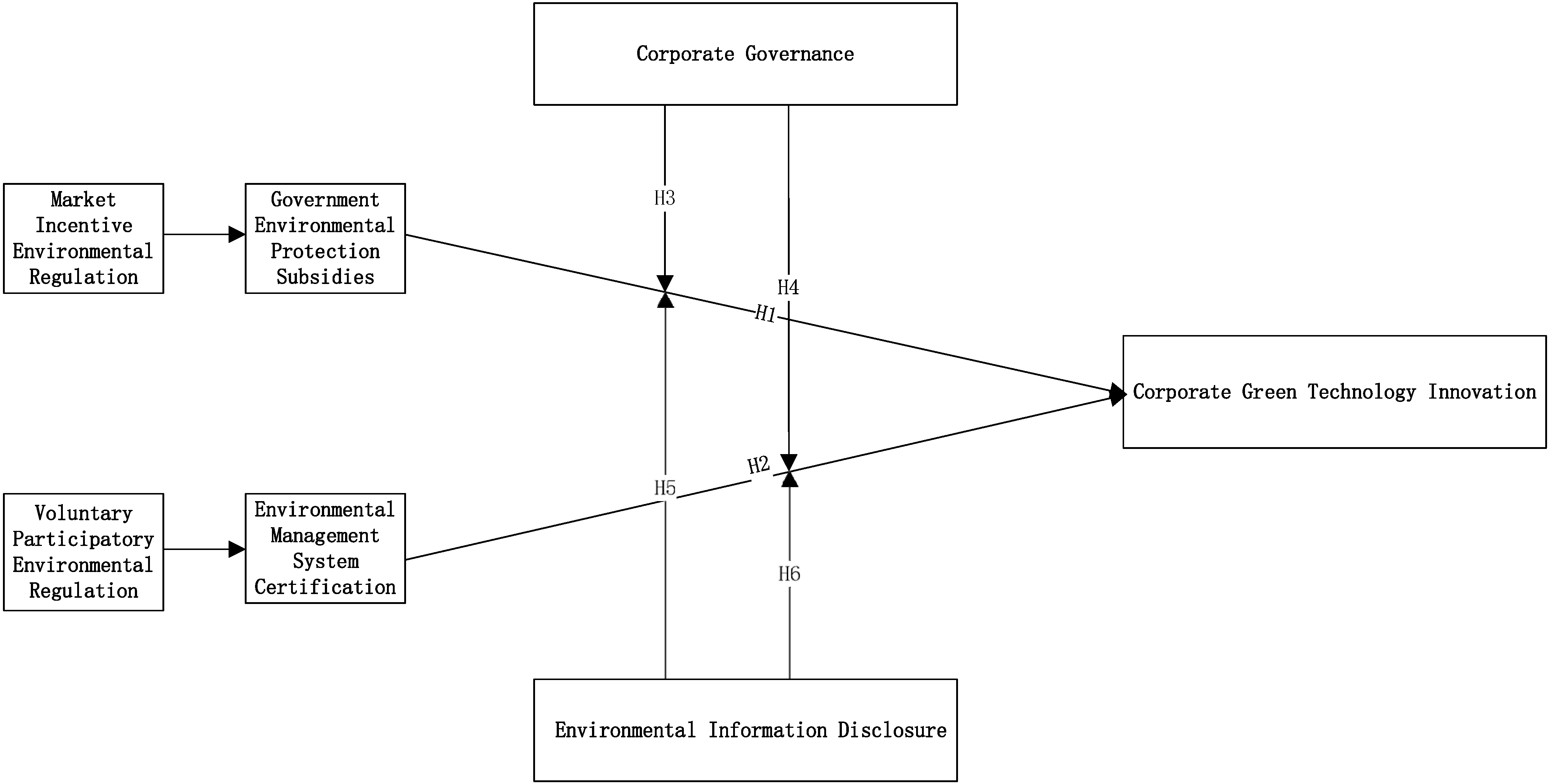

:1. Introduction

2. Theoretical Background and Hypotheses

2.1. Market-Incentive ER and GI

2.2. Voluntary Participatory ER and GI

2.3. Moderating Role of CGL

2.4. Moderating Role of EID

3. Methodology

3.1. Data and Samples

3.2. Variable Definition and Measurement

3.2.1. Dependent Variable

3.2.2. Independent Variables

3.2.3. Moderating Variables

3.2.4. Other Variables

3.3. Models

4. Results

4.1. Descriptive Statistics

4.2. Correlation Analysis

4.3. Regression Results

4.4. Robustness Test

5. Discussion

6. Conclusions and Implications

6.1. Implications

6.1.1. Theoretical Aspect

6.1.2. Practical Aspects

6.2. Conclusions

6.3. Restrictions and Upcoming Studies

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Liu, G.; Sun, W.; Kong, Z.; Dong, X.; Jiang, Q. Did the Pollution Charge System Promote or Inhibit Innovation? Evidence from Chinese Micro-Enterprises. Technol. Forecast. Soc. Chang. 2023, 187, 122207. [Google Scholar] [CrossRef]

- Lin, B.; Chen, X. Environmental Regulation and Energy-Environmental Performance—Empirical Evidence from China’s Non-Ferrous Metals Industry. J. Environ. Manag. 2020, 269, 110722. [Google Scholar] [CrossRef] [PubMed]

- Ruan, H.; Qiu, L.; Chen, J.; Liu, S.; Ma, Z. Government Trust, Environmental Pollution Perception, and Environmental Governance Satisfaction. Int. J. Environ. Res. Public Health 2022, 19, 9929. [Google Scholar] [CrossRef] [PubMed]

- Chen, G.; Wei, B.; Zhu, R. The Impact of Environmental Subsidy on the Performance of Corporate Environmental Responsibility: Evidence from China. Front. Environ. Sci. 2022, 10, 972328. [Google Scholar] [CrossRef]

- Jiang, Y.; Wu, Q.; Brenya, R.; Wang, K. Environmental Decentralization, Environmental Regulation, and Green Technology Innovation: Evidence Based on China. Environ. Sci. Pollut. Res. 2022, 30, 28305–28320. [Google Scholar] [CrossRef] [PubMed]

- Qin, M.; Sun, M.; Li, J. Impact of Environmental Regulation Policy on Ecological Efficiency in Four Major Urban Agglomerations in Eastern China. Ecol. Indic. 2021, 130, 108002. [Google Scholar] [CrossRef]

- Christainsen, G.B.; Haveman, R.H. Public Regulations and the Slowdown in Productivity Growth. Am. Econ. Rev. 2023, 71, 320–325. [Google Scholar]

- Porter, M.E. Towards a Dynamic Theory of Strategy. Strat. Manag. J. 1991, 12, 95–117. [Google Scholar] [CrossRef]

- Du, W.; Li, M.; Wang, Z. The Impact of Environmental Regulation on Firms’ Energy-Environment Efficiency: Concurrent Discussion of Policy Tool Heterogeneity. Ecol. Indic. 2022, 143, 109327. [Google Scholar] [CrossRef]

- Fahad, S.; Bai, D.; Liu, L.; Baloch, Z.A. Heterogeneous Impacts of Environmental Regulation on Foreign Direct Investment: Do Environmental Regulation Affect FDI Decisions? Environ. Sci. Pollut. Res. 2022, 29, 5092–5104. [Google Scholar] [CrossRef] [PubMed]

- Li, Z.; Huang, Z.; Su, Y. New Media Environment, Environmental Regulation and Corporate Green Technology Innovation:Evidence from China. Energy Econ. 2023, 119, 106545. [Google Scholar] [CrossRef]

- Chen, D.; Hu, H.; Chang, C. Green Finance, Environment Regulation, and Industrial Green Transformation for Corporate Social Responsibility. Corp. Soc. Responsib. Environ. Manag. 2023, 30, 2166–2181. [Google Scholar] [CrossRef]

- Xiong, B.; Wang, R. Effect of Environmental Regulation on Industrial Solid Waste Pollution in China: From the Perspective of Formal Environmental Regulation and Informal Environmental Regulation. Int. J. Environ. Res. Public Health 2020, 17, 7798. [Google Scholar] [CrossRef] [PubMed]

- Han, S.; Pan, Y.; Mygrant, M.; Li, M. Differentiated Environmental Regulations and Corporate Environmental Responsibility: The Moderating Role of Institutional Environment. J. Clean. Prod. 2021, 313, 127870. [Google Scholar] [CrossRef]

- Shi, X.; Jiang, Z.; Bai, D.; Fahad, S.; Irfan, M. Assessing the Impact of Green Tax Reforms on Corporate Environmental Performance and Economic Growth: Do Green Reforms Promote the Environmental Performance in Heavily Polluted Enterprises? Environ. Sci. Pollut. Res. 2023, 30, 56054–56072. [Google Scholar] [CrossRef] [PubMed]

- Chen, X.; Sun, L. Analysis of the Research Hotspots and Frontier Issues in Corporate Voluntary Environmental Management. Int. J. Environ. Sci. Technol. 2022, 20, 8127–8140. [Google Scholar] [CrossRef]

- Jiang, F.; Kim, K.A. Corporate Governance in China: A Survey. Rev. Financ. 2020, 24, 733–772. [Google Scholar] [CrossRef]

- Oyewo, B. Corporate Governance and Carbon Emissions Performance: International Evidence on Curvilinear Relationships. J. Environ. Manag. 2023, 334, 117474. [Google Scholar] [CrossRef] [PubMed]

- Chen, W.; Zhang, L.; Shi, L.; Shao, Y.; Zhou, K. Carbon Emissions Trading System and Investment Efficiency: Evidence from China. J. Clean. Prod. 2022, 358, 131782. [Google Scholar] [CrossRef]

- Nirino, N.; Santoro, G.; Miglietta, N.; Quaglia, R. Corporate Controversies and Company’s Financial Performance: Exploring the Moderating Role of ESG Practices. Technol. Forecast. Soc. Chang. 2021, 162, 120341. [Google Scholar] [CrossRef]

- Li, W.; Zheng, M.; Zhang, Y.; Cui, G. Green Governance Structure, Ownership Characteristics, and Corporate Financing Constraints. J. Clean. Prod. 2020, 260, 121008. [Google Scholar] [CrossRef]

- Nirino, N.; Battisti, E.; Ferraris, A.; Dell’Atti, S.; Briamonte, M.F. How and When Corporate Social Performance Reduces Firm Risk? The Moderating Role of Corporate Governance. Corp. Soc. Responsib. Environ. Manag. 2022, 29, 1995–2005. [Google Scholar] [CrossRef]

- Xue, Y.; Jiang, C.; Guo, Y.; Liu, J.; Wu, H.; Hao, Y. Corporate Social Responsibility and High-Quality Development: Do Green Innovation, Environmental Investment and Corporate Governance Matter? Emerg. Mark. Financ. Trade 2022, 58, 3191–3214. [Google Scholar] [CrossRef]

- Elsayih, J.; Datt, R.; Tang, Q. Corporate Governance and Carbon Emissions Performance: Empirical Evidence from Australia. Australas. J. Environ. Manag. 2021, 28, 433–459. [Google Scholar] [CrossRef]

- Zhang, J.; Yang, Y. Can Environmental Disclosure Improve Price Efficiency? The Perspective of Price Delay. Financ. Res. Lett. 2023, 52, 103556. [Google Scholar] [CrossRef]

- Ge, Y.; Chen, Q.; Qiu, S.; Kong, X. Environmental Information Disclosure and Stock Price Crash Risk: Evidence from China. Front. Environ. Sci. 2023, 11, 1108508. [Google Scholar] [CrossRef]

- Li, G.; Xue, Q.; Qin, J. Environmental Information Disclosure and Green Technology Innovation: Empirical Evidence from China. Technol. Forecast. Soc. Chang. 2022, 176, 121453. [Google Scholar] [CrossRef]

- Pan, D.; Fan, W.; Kong, F. Dose Environmental Information Disclosure Raise Public Environmental Concern? Generalized Propensity Score Evidence from China. J. Clean. Prod. 2022, 379, 134640. [Google Scholar] [CrossRef]

- Fan, L.; Yang, K.; Liu, L. New Media Environment, Environmental Information Disclosure and Firm Valuation: Evidence from High-Polluting Enterprises in China. J. Clean. Prod. 2020, 277, 123253. [Google Scholar] [CrossRef]

- Feng, Y.; He, F. The Effect of Environmental Information Disclosure on Environmental Quality: Evidence from Chinese Cities. J. Clean. Prod. 2020, 276, 124027. [Google Scholar] [CrossRef]

- Wang, H.; Zhang, R. Effects of Environmental Regulation on CO2 Emissions: An Empirical Analysis of 282 Cities in China. Sustain. Prod. Consum. 2022, 29, 259–272. [Google Scholar] [CrossRef]

- Zhang, H.; Liu, Z.; Zhang, Y.-J. Assessing the Economic and Environmental Effects of Environmental Regulation in China: The Dynamic and Spatial Perspectives. J. Clean. Prod. 2022, 334, 130256. [Google Scholar] [CrossRef]

- Ji, Y.; Xue, J.; Zhong, K. Does Environmental Regulation Promote Industrial Green Technology Progress? Empirical Evidence from China with a Heterogeneity Analysis. Int. J. Environ. Res. Public Health 2022, 19, 484. [Google Scholar] [CrossRef] [PubMed]

- Huang, X.; Tian, P. How Does Heterogeneous Environmental Regulation Affect Net Carbon Emissions: Spatial and Threshold Analysis for China. J. Environ. Manag. 2023, 330, 117161. [Google Scholar] [CrossRef] [PubMed]

- Wang, Y.; Dong, Y.; Sun, X. Can Environmental Regulations Facilitate Total-Factor Efficiencies in OECD Countries? Energy-Saving Target VS Emission-Reduction Target. Int. J. Green Energy 2023, 20, 1488–1500. [Google Scholar] [CrossRef]

- Guo, X.; Fu, L.; Sun, X. Can Environmental Regulations Promote Greenhouse Gas Abatement in OECD Countries? Command-and-Control vs. Market-Based Policies. Sustainability 2021, 13, 6913. [Google Scholar] [CrossRef]

- Shen, X.; Lin, B. Policy Incentives, R&D Investment, and the Energy Intensity of China’s Manufacturing Sector. J. Clean. Prod. 2020, 255, 120208. [Google Scholar] [CrossRef]

- Qiu, S.; Wang, Z.; Geng, S. How Do Environmental Regulation and Foreign Investment Behavior Affect Green Productivity Growth in the Industrial Sector? An Empirical Test Based on Chinese Provincial Panel Data. J. Environ. Manag. 2021, 287, 112282. [Google Scholar] [CrossRef] [PubMed]

- Zhuge, L.; Freeman, R.B.; Higgins, M.T. Regulation and Innovation: Examining Outcomes in Chinese Pollution Control Policy Areas. Econ. Model. 2020, 89, 19–31. [Google Scholar] [CrossRef]

- Qiu, L.; Hu, D.; Wang, Y. How Do Firms Achieve Sustainability through Green Innovation under External Pressures of Environmental Regulation and Market Turbulence? Bus. Strategy Environ. 2020, 29, 2695–2714. [Google Scholar] [CrossRef]

- Yang, L.; Zhang, J.; Zhang, Y. Environmental Regulations and Corporate Green Innovation in China: The Role of City Leaders’ Promotion Pressure. Int. J. Environ. Res. Public Health 2021, 18, 7774. [Google Scholar] [CrossRef] [PubMed]

- Xie, P.; Xu, Y.; Tan, X.; Tan, Q. How Does Environmental Policy Stringency Influence Green Innovation for Environmental Managements? J. Environ. Manag. 2023, 338, 117766. [Google Scholar] [CrossRef] [PubMed]

- Zhou, P.; Song, F.M.; Huang, X. Environmental Regulations and Firms’ Green Innovations: Transforming Pressure into Incentives. Int. Rev. Financ. Anal. 2023, 86, 102504. [Google Scholar] [CrossRef]

- Yang, Y.; Li, X. Environmental Regulation, Digital Finance, and Technological Innovation: Evidence from Listed Firms in China. Environ. Sci. Pollut. Res. 2023, 30, 44625–44639. [Google Scholar] [CrossRef] [PubMed]

- Luo, Y.; Salman, M.; Lu, Z. Heterogeneous Impacts of Environmental Regulations and Foreign Direct Investment on Green Innovation across Different Regions in China. Sci. Total Environ. 2021, 759, 143744. [Google Scholar] [CrossRef] [PubMed]

- Li, G.; Li, X.; Wang, N. Research on the Influence of Environmental Regulation on Technological Innovation Efficiency of Manufacturing Industry in China. Int. J. Environ. Sci. Technol. 2022, 19, 5239–5252. [Google Scholar] [CrossRef]

- Wang, S.; Wang, H.; Wang, J. Exploring the Effects of Institutional Pressures on the Implementation of Environmental Management Accounting: Do Top Management Support and Perceived Benefit Work? Bus. Strategy Environ. 2019, 28, 233–243. [Google Scholar] [CrossRef]

- Zhang, W.; Li, G.; Guo, F. Does Carbon Emissions Trading Promote Green Technology Innovation in China? Appl. Energy 2022, 315, 119012. [Google Scholar] [CrossRef]

- Chen, J.; Wang, X.; Shen, W.; Tan, Y.; Matac, L.M.; Samad, S. Environmental Uncertainty, Environmental Regulation and Enterprises’ Green Technological Innovation. Int. J. Environ. Res. Public Health 2022, 19, 9781. [Google Scholar] [CrossRef] [PubMed]

- Gao, D.; Li, G.; Li, Y.; Gao, K. Does FDI Improve Green Total Factor Energy Efficiency under Heterogeneous Environmental Regulation? Evidence from China. Environ. Sci. Pollut. Res. 2022, 29, 25665–25678. [Google Scholar] [CrossRef] [PubMed]

- Chen, X.; Li, W.; Chen, Z.; Huang, J. Environmental Regulation and Real Earnings Management—Evidence from the SO2 Emissions Trading System in China. Financ. Res. Lett. 2022, 46, 102418. [Google Scholar] [CrossRef]

- Qu, F.; Xu, L.; Chen, Y. Can Market-Based Environmental Regulation Promote Green Technology Innovation? Evidence from China. Front. Environ. Sci. 2022, 9, 823536. [Google Scholar] [CrossRef]

- Wei, Y.; Xu, D.; Zhang, K.; Cheng, J. Research on the Innovation Incentive Effect and Heterogeneity of the Market-Incentive Environmental Regulation on Mineral Resource Enterprises. Environ. Sci. Pollut. Res. 2021, 28, 58456–58469. [Google Scholar] [CrossRef]

- Shao, Y.; Chen, Z. Can Government Subsidies Promote the Green Technology Innovation Transformation? Evidence from Chinese Listed Companies. Econ. Anal. Policy 2022, 74, 716–727. [Google Scholar] [CrossRef]

- Ren, S.; Sun, H.; Zhang, T. Do Environmental Subsidies Spur Environmental Innovation? Empirical Evidence from Chinese Listed Firms. Technol. Forecast. Soc. Chang. 2021, 173, 121123. [Google Scholar] [CrossRef]

- Chen, L.; Yang, W. R&D Tax Credits and Firm Innovation: Evidence from China. Technol. Forecast. Soc. Chang. 2019, 146, 233–241. [Google Scholar] [CrossRef]

- Lee, S.-H.; Park, C.-H. Environmental Regulations in Private and Mixed Duopolies: Taxes on Emissions versus Green R&D Subsidies. Econ. Syst. 2021, 45, 100852. [Google Scholar] [CrossRef]

- Ma, C.; Yang, H.; Zhang, W.; Huang, S. Low-Carbon Consumption with Government Subsidy under Asymmetric Carbon Emission Information. J. Clean. Prod. 2021, 318, 128423. [Google Scholar] [CrossRef]

- Fang, L.; Zhao, S. On the Green Subsidies in a Differentiated Market. Int. J. Prod. Econ. 2023, 257, 108758. [Google Scholar] [CrossRef]

- Jiang, Z.; Xu, C.; Zhou, J. Government Environmental Protection Subsidies, Environmental Tax Collection, and Green Innovation: Evidence from Listed Enterprises in China. Environ. Sci. Pollut. Res. 2023, 30, 4627–4641. [Google Scholar] [CrossRef] [PubMed]

- Huang, Z.; Liao, G.; Li, Z. Loaning Scale and Government Subsidy for Promoting Green Innovation. Technol. Forecast. Soc. Chang. 2019, 144, 148–156. [Google Scholar] [CrossRef]

- Felício, J.A.; Rodrigues, R.; Caldeirinha, V. Green Shipping Effect on Sustainable Economy and Environmental Performance. Sustainability 2021, 13, 4256. [Google Scholar] [CrossRef]

- Zheng, S.; Jin, S. Can Enterprises in China Achieve Sustainable Development through Green Investment? Int. J. Environ. Res. Public Health 2023, 20, 1787. [Google Scholar] [CrossRef] [PubMed]

- Bu, M.; Qiao, Z.; Liu, B. Voluntary Environmental Regulation and Firm Innovation in China. Econ. Model. 2020, 89, 10–18. [Google Scholar] [CrossRef]

- Jiang, Z.; Wang, Z.; Zeng, Y. Can Voluntary Environmental Regulation Promote Corporate Technological Innovation? Bus. Strategy Environ. 2020, 29, 390–406. [Google Scholar] [CrossRef]

- Sam, A.G.; Song, D. ISO 14001 Certification and Industrial Decarbonization: An Empirical Study. J. Environ. Manag. 2022, 323, 116169. [Google Scholar] [CrossRef] [PubMed]

- Jiang, Z.; Wang, Z.; Lan, X. How Environmental Regulations Affect Corporate Innovation? The Coupling Mechanism of Mandatory Rules and Voluntary Management. Technol. Soc. 2021, 65, 101575. [Google Scholar] [CrossRef]

- Wang, L.; Shang, Y.; Li, C. How to Improve the Initiative and Effectiveness of Enterprises to Implement Environmental Management System Certification? J. Clean. Prod. 2023, 404, 137013. [Google Scholar] [CrossRef]

- Bravi, L.; Santos, G.; Pagano, A.; Murmura, F. Environmental Management System According to ISO 14001:2015 as a Driver to Sustainable Development. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 2599–2614. [Google Scholar] [CrossRef]

- Riaz, H.; Saeed, A. Impact of Environmental Policy on Firm’s Market Performance: The Case of ISO 14001. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 681–693. [Google Scholar] [CrossRef]

- Peng, J.; Song, Y.; Tu, G.; Liu, Y. A study of the dual-target corporate environmental behavior (DTCEB) of heavily polluting enterprises under different environment regulations: Green innovation vs. pollutant emissions. J. Clean. Prod. 2021, 297, 126602. [Google Scholar] [CrossRef]

- Liao, Z.; Liu, P. Market-Based Environmental Policy Instrument Mixes and Firms’ Environmental Innovation: A Fuzzy-Set Qualitative Comparative Analysis. Emerg. Mark. Financ. Trade 2022, 58, 3976–3984. [Google Scholar] [CrossRef]

- Zheng, D.; Yuan, Z.; Ding, S.; Cui, T. Enhancing Environmental Sustainability through Corporate Governance: The Merger and Acquisition Perspective. Energy Sustain. Soc. 2021, 11, 41. [Google Scholar] [CrossRef]

- Naciti, V.; Cesaroni, F.; Pulejo, L. Corporate Governance and Sustainability: A Review of the Existing Literature. J. Manag. Gov. 2022, 26, 55–74. [Google Scholar] [CrossRef]

- Gerged, A.M. Factors Affecting Corporate Environmental Disclosure in Emerging Markets: The Role of Corporate Governance Structures. Bus. Strategy Environ. 2021, 30, 609–629. [Google Scholar] [CrossRef]

- Peng, X.; Zhang, R. Corporate Governance, Environmental Sustainability Performance, and Normative Isomorphic Force of National Culture. Environ. Sci. Pollut. Res. 2022, 29, 33443–33473. [Google Scholar] [CrossRef]

- Yu, Z.; Shen, Y.; Jiang, S. The Effects of Corporate Governance Uncertainty on State-Owned Enterprises’ Green Innovation in China: Perspective from the Participation of Non-State-Owned Shareholders. Energy Econ. 2022, 115, 106402. [Google Scholar] [CrossRef]

- Hu, S.; Wu, H. The Mechanism of Media Pressure on Corporate Green Technology Innovation: The Moderating Effect of Corporate Internal Governance. Technol. Anal. Strateg. Manag. 2022, 1–17. [Google Scholar] [CrossRef]

- Tang, Y.; Yue, S.; Ma, W.; Zhang, L. How Do Environmental Protection Expenditure and Green Technology Innovation Affect Synergistically the Financial Performance of Heavy Polluting Enterprises? Evidence from China. Environ. Sci. Pollut. Res. 2022, 29, 89597–89613. [Google Scholar] [CrossRef] [PubMed]

- Deegan, C.M. Legitimacy Theory: Despite Its Enduring Popularity and Contribution, Time Is Right for a Necessary Makeover. Account. Audit. Account. J. 2019, 32, 2307–2329. [Google Scholar] [CrossRef]

- Dowling, J.; Pfeffer, J. Organizational Legitimacy: Social Values and Organizational Behavior. Pac. Sociol. Rev. 1975, 18, 122–136. [Google Scholar] [CrossRef]

- Huang, C.-L.; Kung, F.-H. Drivers of Environmental Disclosure and Stakeholder Expectation: Evidence from Taiwan. J. Bus. Ethics 2010, 96, 435–451. [Google Scholar] [CrossRef]

- Narsa Goud, N. Corporate Governance: Does It Matter Management of Carbon Emission Performance? An Empirical Analyses of Indian Companies. J. Clean. Prod. 2022, 379, 134485. [Google Scholar] [CrossRef]

- Nicolo, G.; Zampone, G.; Sannino, G.; Tiron-Tudor, A. Worldwide Evidence of Corporate Governance Influence on ESG Disclosure in the Utilities Sector. Util. Policy 2023, 82, 101549. [Google Scholar] [CrossRef]

- Bu, C.; Zhang, K.; Shi, D.; Wang, S. Does Environmental Information Disclosure Improve Energy Efficiency? Energy Policy 2022, 164, 112919. [Google Scholar] [CrossRef]

- Wang, S.; Wang, H.; Wang, J.; Yang, F. Does Environmental Information Disclosure Contribute to Improve Firm Financial Performance? An Examination of the Underlying Mechanism. Sci. Total Environ. 2020, 714, 136855. [Google Scholar] [CrossRef] [PubMed]

- Shi, D.; Bu, C.; Xue, H. Deterrence Effects of Disclosure: The Impact of Environmental Information Disclosure on Emission Reduction of Firms. Energy Econ. 2021, 104, 105680. [Google Scholar] [CrossRef]

- Liu, S.; Liu, C.; Yang, M. The Effects of National Environmental Information Disclosure Program on the Upgradation of Regional Industrial Structure: Evidence from 286 Prefecture-Level Cities in China. Struct. Chang. Econ. Dyn. 2021, 58, 552–561. [Google Scholar] [CrossRef]

- Zhang, X.; Jiang, F.; Liu, H.; Liu, R. Green Finance, Managerial Myopia and Corporate Green Innovation: Evidence from Chinese Manufacturing Listed Companies. Financ. Res. Lett. 2023, 58, 104383. [Google Scholar] [CrossRef]

- Ying, Y.; Jin, S. Digital Transformation and Corporate Sustainability: The Moderating Effect of Ambidextrous Innovation. Systems 2023, 11, 344. [Google Scholar] [CrossRef]

- Tang, M.; Liu, Y.; Hu, F.; Wu, B. Effect of Digital Transformation on Enterprises’ Green Innovation: Empirical Evidence from Listed Companies in China. Energy Econ. 2023, 128, 107135. [Google Scholar] [CrossRef]

- Luo, Y.; Xiong, G.; Mardani, A. Environmental Information Disclosure and Corporate Innovation: The “Inverted U-Shaped” Regulating Effect of Media Attention. J. Bus. Res. 2022, 146, 453–463. [Google Scholar] [CrossRef]

- Li, Q.; Maqsood, U.S.; Zahid, R.M.A.; Anwar, W. Regulating CEO Pay and Green Innovation: Moderating Role of Social Capital and Government Subsidy. Environ. Sci. Pollut. Res. 2023. [Google Scholar] [CrossRef] [PubMed]

- Wang, J.; Ma, M.; Dong, T.; Zhang, Z. Do ESG Ratings Promote Corporate Green Innovation? A Quasi-Natural Experiment Based on SynTao Green Finance’s ESG Ratings. Int. Rev. Financ. Anal. 2023, 87, 102623. [Google Scholar] [CrossRef]

- Wu, J.; Liu, B.; Zeng, Y.; Luo, H. Good for the Firm, Good for the Society? Causal Evidence of the Impact of Equity Incentives on a Firm’s Green Investment. Int. Rev. Econ. Financ. 2022, 77, 435–449. [Google Scholar] [CrossRef]

- Ren, S.; He, D.; Zhang, T.; Chen, X. Symbolic reactions or substantive pro-environmental behaviour? An empirical study of corporate environmental performance under the government’s environmental subsidy scheme. Bus. Strategy Environ. 2019, 28, 1148–1165. [Google Scholar] [CrossRef]

- Wu, J.; Chen, Z. The Asymmetric Influences of Environmental Subsidy and Non-Environmental Subsidy on Corporate Environmental Responsibility: Evidence from China. Environ. Sci. Pollut. Res. 2022, 29, 77057–77070. [Google Scholar] [CrossRef]

- Liao, F.; Hu, Y.; Xu, S. How Do Environmental Subsidies Affect the Environmental Performance of Heavily Polluting Enterprises: Evidence from China. Econ. Res.-Ekon. Istraživanja 2023, 36, 2160777. [Google Scholar] [CrossRef]

- Pei, W.; Pei, W. Empirical Study on the Impact of Government Environmental Subsidies on Environmental Performance of Heavily Polluting Enterprises Based on the Regulating Effect of Internal Control. Int. J. Environ. Res. Public Health 2023, 20, 98. [Google Scholar] [CrossRef]

- Zhang, Y.; Ruan, H.; Tang, G.; Tong, L. Power of Sustainable Development: Does Environmental Management System Certification Affect a Firm’s Access to Finance? Bus. Strategy Environ. 2021, 30, 3772–3788. [Google Scholar] [CrossRef]

- Brown, P.; Beekes, W.; Verhoeven, P. Corporate Governance, Accounting and Finance: A Review. Account. Financ. 2011, 51, 96–172. [Google Scholar] [CrossRef]

- Raithatha, M.; Haldar, A. Are Internal Governance Mechanisms Efficient? The Case of a Developing Economy. IIMB Manag. Rev. 2021, 33, 191–204. [Google Scholar] [CrossRef]

- Addo, K.A.; Hussain, N.; Iqbal, J. Corporate Governance and Banking Systemic Risk: A Test of the Bundling Hypothesis. J. Int. Money Financ. 2021, 115, 102327. [Google Scholar] [CrossRef]

- Tarchouna, A.; Jarraya, B.; Bouri, A. How to Explain Non-Performing Loans by Many Corporate Governance Variables Simultaneously? A Corporate Governance Index Is Built to US Commercial Banks. Res. Int. Bus. Financ. 2017, 42, 645–657. [Google Scholar] [CrossRef]

- Song, X.; Yang, B. Oil Price Uncertainty, Corporate Governance and Firm Performance. Int. Rev. Econ. Financ. 2022, 80, 469–487. [Google Scholar] [CrossRef]

- Hussain, T.; Loureiro, G. Portability of Firm Corporate Governance in Mergers and Acquisitions. Res. Int. Bus. Financ. 2022, 63, 101777. [Google Scholar] [CrossRef]

- Sun, J.; Xue, J.; Qiu, X. Has the Sustainable Energy Transition in China’s Resource-Based Cities Promoted Green Technology Innovation in Firms? Socio-Econ. Plan. Sci. 2022, 87, 101330. [Google Scholar] [CrossRef]

- Desheng, L.; Jiakui, C.; Ning, Z. Political Connections and Green Technology Innovations under an Environmental Regulation. J. Clean. Prod. 2021, 298, 126778. [Google Scholar] [CrossRef]

- Su, X.; Pan, C.; Zhou, S.; Zhong, X. Threshold Effect of Green Credit on Firms’ Green Technology Innovation: Is Environmental Information Disclosure Important? J. Clean. Prod. 2022, 380, 134945. [Google Scholar] [CrossRef]

- Wang, Q.; Sun, T.; Li, R. Does Artificial Intelligence Promote Green Innovation? An Assessment Based on Direct, Indirect, Spillover, and Heterogeneity Effects. Energy Environ. 2023, 0958305X231220520. [Google Scholar] [CrossRef]

- Xu, D.; Abbas, S.; Rafique, K.; Ali, N. The Race to Net-Zero Emissions: Can Green Technological Innovation and Environmental Regulation Be the Potential Pathway to Net-Zero Emissions? Technol. Soc. 2023, 75, 102364. [Google Scholar] [CrossRef]

- Hasan, M.M.; Du, F. Nexus between Green Financial Development, Green Technological Innovation and Environmental Regulation in China. Renew. Energy 2023, 204, 218–228. [Google Scholar] [CrossRef]

- Wu, Y.; Tham, J. The Impact of Environmental Regulation, Environment, Social and Government Performance, and Technological Innovation on Enterprise Resilience under a Green Recovery. Heliyon 2023, 9, e20278. [Google Scholar] [CrossRef] [PubMed]

- Mehmood, S.; Zaman, K.; Khan, S.; Ali, Z.; Khan, H.U.R. The Role of Green Industrial Transformation in Mitigating Carbon Emissions: Exploring the Channels of Technological Innovation and Environmental Regulation. Energy Built Environ. 2024, 5, 464–479. [Google Scholar] [CrossRef]

- Mao, J.; Wu, Q.; Zhu, M.; Lu, C. Effects of Environmental Regulation on Green Total Factor Productivity: An Evidence from the Yellow River Basin, China. Sustainability 2022, 14, 2015. [Google Scholar] [CrossRef]

- Bai, Y.; Song, S.; Jiao, J.; Yang, R. The Impacts of Government R&D Subsidies on Green Innovation: Evidence from Chinese Energy-Intensive Firms. J. Clean. Prod. 2019, 233, 819–829. [Google Scholar] [CrossRef]

- Xia, L.; Gao, S.; Wei, J.; Ding, Q. Government Subsidy and Corporate Green Innovation—Does Board Governance Play a Role? Energy Policy 2022, 161, 112720. [Google Scholar] [CrossRef]

- Han, F.; Mao, X.; Yu, X.; Yang, L. Government Environmental Protection Subsidies and Corporate Green Innovation: Evidence from Chinese Microenterprises. J. Innov. Knowl. 2024, 9, 100458. [Google Scholar] [CrossRef]

- Zhou, D.; Yuan, S.; Xie, D. Voluntary Environmental Regulation and Urban Innovation: Evidence from Low-Carbon Pilot Cities Program in China. Technol. Forecast. Soc. Chang. 2022, 175, 121388. [Google Scholar] [CrossRef]

- Hu, S.; Wang, M.; Wu, M.; Wang, A. Voluntary Environmental Regulations, Greenwashing and Green Innovation: Empirical Study of China’s ISO14001 Certification. Environ. Impact Assess. Rev. 2023, 102, 107224. [Google Scholar] [CrossRef]

- Kurzhals, C.; Graf-Vlachy, L.; König, A. Strategic Leadership and Technological Innovation: A Comprehensive Review and Research Agenda. Corp. Gov. 2020, 28, 437–464. [Google Scholar] [CrossRef]

- Chen, W.; Xie, Y.; He, K. Environmental, Social, and Governance Performance and Corporate Innovation Novelty. Int. J. Innov. Stud. 2024, 8, 109–131. [Google Scholar] [CrossRef]

- Zheng, X.; Shen, J. Corporate Environmental Information Disclosure, Managerial Ownership and the Cost of Debt. Int. Rev. Econ. Financ. 2024, 93, 645–659. [Google Scholar] [CrossRef]

- Aghion, P.; Antonin, C.; Bunel, S. The Power of Creative Destruction: Economic Upheaval and the Wealth of Nations; Harvard University Press: Cambridge, MA, USA, 2021; ISBN 978-0-674-25868-6. [Google Scholar]

- Zhang, C.; Zhou, B.; Wang, Q.; Jian, Y. The Consequences of Environmental Big Data Information Disclosure on Hard-to-Abate Chinese Enterprises’ Green Innovation. J. Innov. Knowl. 2024, 9, 100474. [Google Scholar] [CrossRef]

- Lian, G.; Xu, A.; Zhu, Y. Substantive Green Innovation or Symbolic Green Innovation? The Impact of ER on Enterprise Green Innovation Based on the Dual Moderating Effects. J. Innov. Knowl. 2022, 7, 100203. [Google Scholar] [CrossRef]

{kind=link}

| Variables | Symbol | Definitions |

|---|---|---|

| Green technological innovation | GI | Logarithm of the amount of GI plus 1 |

| Environmental protection subsidy | EPS | Logarithm of the amount of EPS + 1 |

| Environmental management system certification | EMSC | It is 1 for ISO14001 certified and 0 otherwise |

| Level of corporate governance | CGL | It is constructed by the PCA method |

| Environmental information disclosure | EID | It is 1 for disclosing environmental objectives and 0 otherwise |

| Size of enterprise | Size | Logarithm of total assets |

| Asset–liability ratio | Lev | Total liabilities/total assets |

| Net profit margin on total assets | ROA | Net profit/average balance of total assets |

| Cash flow ratio | Cashflow | Net cash flow from operating activities/total assets |

| Year of listing | ListAge | Logarithm of the year of listing plus 1 |

| Dummy variable of industry | Industry | Industry membership is 1 and 0 otherwise. |

| Dummy variable of year | Year | Belonging to the year is 1 and 0 otherwise |

| Variables | N | Mean | SD | Min | Median | Max | Skewness | Kurtosis |

|---|---|---|---|---|---|---|---|---|

| GI | 19425 | 0.44 | 0.702 | 0.000 | 0.000 | 4.094 | 1.5017 | 4.4938 |

| EPS | 19425 | 3.70 | 6.014 | 0.000 | 0.000 | 17.145 | 1.0727 | 2.2798 |

| EMSC | 19425 | 0.21 | 0.404 | 0.000 | 0.000 | 1.000 | 1.4580 | 3.1258 |

| EID | 19425 | 0.82 | 0.385 | 0.000 | 1.000 | 1.000 | −1.6606 | 3.7577 |

| CGL | 19425 | 0.10 | 0.988 | −2.099 | 0.009 | 2.401 | 0.2767 | 2.3975 |

| Size | 19425 | 22.04 | 1.208 | 19.525 | 21.882 | 26.430 | 0.7350 | 3.6194 |

| Lev | 19425 | 0.41 | 0.205 | 0.035 | 0.393 | 0.925 | 0.3049 | 2.2889 |

| ROA | 19425 | 0.04 | 0.055 | −0.117 | 0.041 | 0.182 | −0.2164 | 4.3430 |

| Cashflow | 19425 | 0.04 | 0.068 | −0.197 | 0.045 | 0.257 | −0.0865 | 3.9392 |

| ListAge | 19425 | 2.00 | 0.917 | 0.000 | 2.079 | 3.367 | −0.6147 | 2.4428 |

| GI | EPS | EMSC | EID | CGL | Size | Lev | ROA | Cashflow | ListAge | |

|---|---|---|---|---|---|---|---|---|---|---|

| GI | 1 | |||||||||

| EPS | 0.035 *** | 1 | ||||||||

| EMSC | 0.173 *** | 0.066 *** | 1 | |||||||

| EID | 0.144 *** | 0.081 *** | 0.177 *** | 1 | ||||||

| CGL | 0.059 *** | −0.137 *** | 0.001 | 0.049 *** | 1 | |||||

| Size | 0.112 *** | 0.130 *** | −0.020 *** | 0.047 *** | −0.477 *** | 1 | ||||

| Lev | 0.034 *** | 0.108 *** | −0.047 *** | −0.038 *** | −0.320 *** | 0.518 *** | 1 | |||

| ROA | 0.052 *** | −0.074 *** | 0.029 *** | 0.016 ** | 0.092 *** | −0.064 *** | −0.414 *** | 1 | ||

| Cashflow | 0.00700 | 0.044 *** | 0.060 *** | 0.042 *** | −0.068 *** | 0.056 *** | −0.169 *** | 0.407 *** | 1 | |

| ListAge | −0.141 *** | 0.141 *** | −0.022 *** | −0.042 *** | −0.495 *** | 0.426 *** | 0.389 *** | −0.314 *** | −0.025 *** | 1 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| GI | GI | GI | GI | GI | GI | |

| EPS | 0.0029 *** | 0.0031 *** | 0.0026 *** | |||

| (3.4005) | (3.6180) | (3.1261) | ||||

| EMSC | 0.0547 *** | 0.0556 *** | 0.0423 *** | |||

| (4.0125) | (4.0749) | (2.9080) | ||||

| CGL | 0.0208 ** | 0.0216 ** | ||||

| (2.1149) | (2.1943) | |||||

| EID | 0.0299 ** | 0.0376 *** | ||||

| (2.5270) | (2.8224) | |||||

| EPS × CGL | 0.0016 * | |||||

| (1.8811) | ||||||

| EPS × EID | 0.0051 *** | |||||

| (2.7294) | ||||||

| EMSC × CGL | 0.0248 * | |||||

| (1.8598) | ||||||

| EMSC × EID | 0.0896 ** | |||||

| (2.1364) | ||||||

| Size | 0.0480 *** | 0.0506 *** | 0.0504 *** | 0.0483 *** | 0.0525 *** | 0.0503 *** |

| Lev | −0.0693 | −0.0684 | −0.0680 | −0.0679 | −0.0672 | −0.0670 |

| (−1.5758) | (−1.5544) | (−1.5469) | (−1.5432) | (−1.5278) | (−1.5224) | |

| ROA | 0.0587 | 0.0497 | 0.0717 | 0.0581 | 0.0655 | 0.0555 |

| (0.5647) | (0.4781) | (0.6891) | (0.5592) | (0.6296) | (0.5345) | |

| Cashflow | −0.1259 * | −0.1293 * | −0.1277 * | −0.1245 * | −0.1298 * | −0.1289 * |

| (−1.7915) | (−1.8411) | (−1.8182) | (−1.7731) | (−1.8486) | (−1.8353) | |

| ListAge | −0.0316 ** | −0.0341 ** | −0.0253 | −0.0308 * | −0.0287 * | −0.0335 ** |

| (−1.9731) | (−2.1248) | (−1.5512) | (−1.9248) | (−1.7579) | (−2.0904) | |

| Constant | −0.5856 ** | −0.6396 ** | −0.6510 ** | −0.6145 ** | −0.6914 ** | −0.6656 ** |

| (−2.1038) | (−2.2987) | (−2.3270) | (−2.2073) | (−2.4721) | (−2.3916) | |

| Industry FE | YES | YES | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES | YES | YES |

| Observations | 19,425 | 19,425 | 19,425 | 19,425 | 19,425 | 19,425 |

| R-squared | 0.053 | 0.053 | 0.053 | 0.054 | 0.054 | 0.131 |

| Variables | First Stage | Second Stage | First Stage | Second Stage |

|---|---|---|---|---|

| EPS | GI | EMSC | GI | |

| EPSt−1 | 0.1068 *** | |||

| (11.4147) | ||||

| EPS | 0.0185 ** | |||

| (1.9973) | ||||

| EMSCt−1 | 0.2175 *** | |||

| (23.1490) | ||||

| EMSC | 0.1361 * | |||

| (1.7776) | ||||

| Size | 0.4944 *** | 0.0403 *** | −0.0163 ** | 0.0533 *** |

| (3.8381) | (2.7603) | (−2.1436) | (3.9308) | |

| Lev | −0.3937 | −0.1160 ** | 0.0208 | −0.1261 ** |

| (−0.7879) | (−2.1858) | (0.7043) | (−2.4082) | |

| ROA | −3.7397 *** | 0.0154 | −0.0343 | −0.0546 |

| (−3.2738) | (0.1218) | (−0.5079) | (−0.4564) | |

| Cashflow | 0.5154 | −0.0845 | 0.0532 | −0.0819 |

| (0.6606) | (−1.0211) | (1.1526) | (−1.0009) | |

| Constant | −10.6306 *** | 0.5497 *** | ||

| (−3.4361) | (3.0070) | |||

| Industry FE | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES |

| Observations | 13962 | 13962 | 13962 | 13962 |

| R-squared | 0.040 | 0.025 | 0.057 | 0.045 |

| Cragg–Donald Wald F statistic | 130.295 | 535.877 | ||

| Underidentification test p-value | 0.000 | 0.000 | ||

| Sargan statistic | 0.000 | 0.000 | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ying, Y.; Jin, S. Impact of Environmental Regulation on Corporate Green Technological Innovation: The Moderating Role of Corporate Governance and Environmental Information Disclosure. Sustainability 2024, 16, 3006. https://doi.org/10.3390/su16073006

Ying Y, Jin S. Impact of Environmental Regulation on Corporate Green Technological Innovation: The Moderating Role of Corporate Governance and Environmental Information Disclosure. Sustainability. 2024; 16(7):3006. https://doi.org/10.3390/su16073006

Chicago/Turabian StyleYing, Ying, and Shanyue Jin. 2024. "Impact of Environmental Regulation on Corporate Green Technological Innovation: The Moderating Role of Corporate Governance and Environmental Information Disclosure" Sustainability 16, no. 7: 3006. https://doi.org/10.3390/su16073006

APA StyleYing, Y., & Jin, S. (2024). Impact of Environmental Regulation on Corporate Green Technological Innovation: The Moderating Role of Corporate Governance and Environmental Information Disclosure. Sustainability, 16(7), 3006. https://doi.org/10.3390/su16073006