An Alternative Model to Determine the Financing Structure of PPP-Based Young Graduate Apartments in China: A Case Study of Hangzhou

Abstract

:1. Introduction

2. Research Methodology

{kind=link}

{kind=link}

{kind=link}

| No | Author(s) | Year | Objective | Key Methods |

|---|---|---|---|---|

| 1 | Ngee et al. [33] | 1997 | Concession pricing | Multiple linear regression |

| 2 | Shen et al. [28] | 2002 | Concession period | NPV |

| 3 | Yeo and Tiong [29] | 2003 | Concession period | NPV, Monte Carlo Simulation |

| 4 | Cheng and Tiong [34] | 2005 | Tariff design | NPV, Risk analysis |

| 5 | Shen and Wu [30] | 2005 | Concession period | NPV, Monte Carlo Simulation |

| 6 | Huang and Chou [35] | 2006 | Minimum revenue guarantee | Real option theory |

| 7 | Zhang and AbouRizk [31] | 2006 | Concession period | NPV, Critical path method, Monte Carlo Simulation |

| 8 | Ng et al. [31] | 2007 | Concession price and period | NPV, Monte Carlo Simulation, Fuzzy set theory |

| 9 | Shen et al. [36] | 2007 | Concession period | NPV, Bargaining game theory |

| 10 | Subprasom and Chen [37] | 2007 | Concession price | Genetic algorithm, Case study |

| 11 | Zhang [38] | 2011 | Concession period | Web-based concession period analysis system |

| 12 | Khanzadi et al. [39] | 2012 | Concession period | NPV, Fuzzy set theory, System dynamics |

| 13 | Hanaoka and Palapus [40] | 2012 | Concession period | NPV, Monte Carlo Simulation, Bargaining game theory |

| 14 | Yu and Lam [41] | 2013 | Concession period | NPV, Principal Component Analysis, Monte Carlo Simulation |

| 15 | Bao et al. [42] | 2015 | Concession period | NPV, incomplete information game theory |

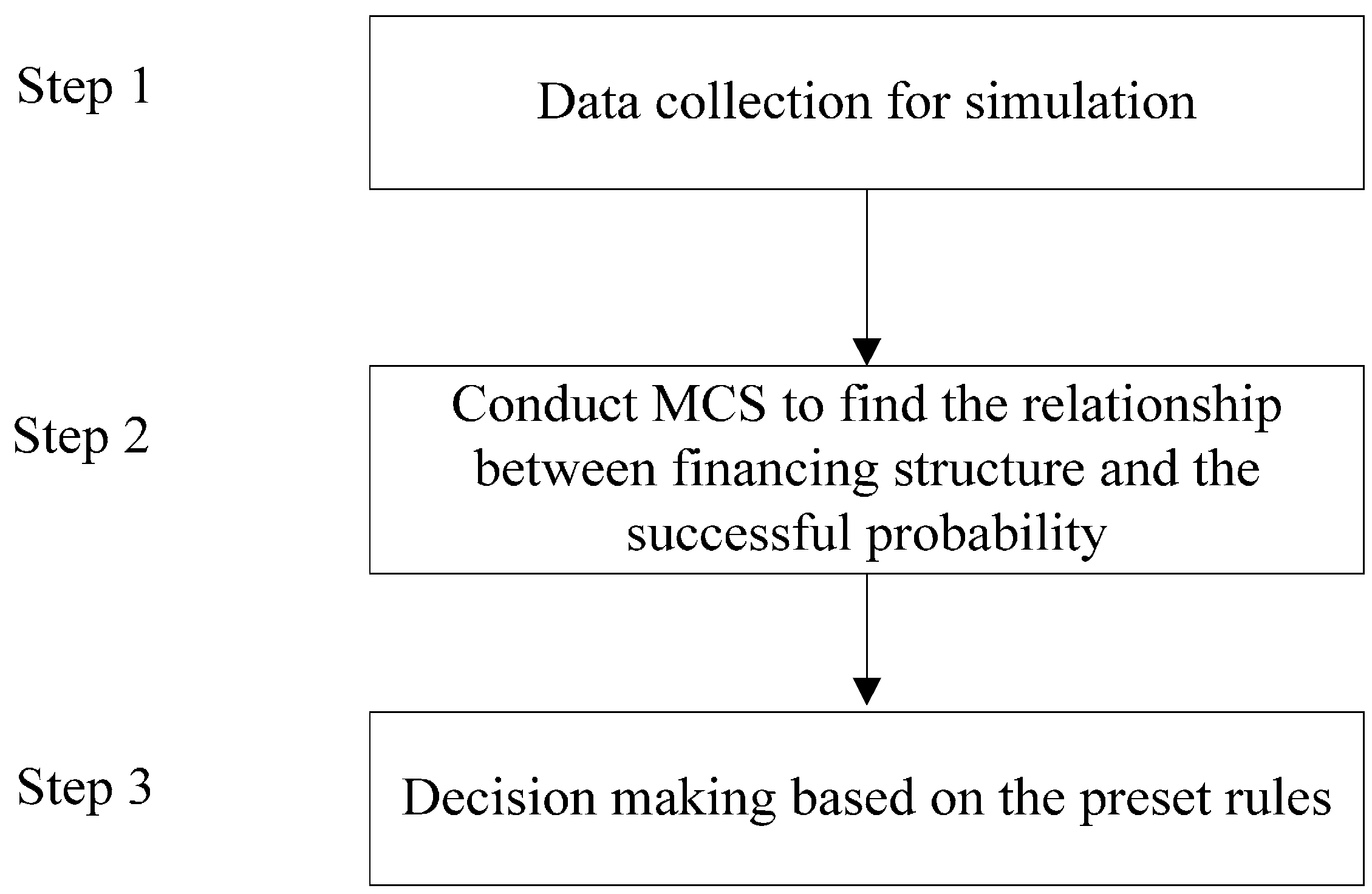

2.1. Step 1 Data Collection for Simulation

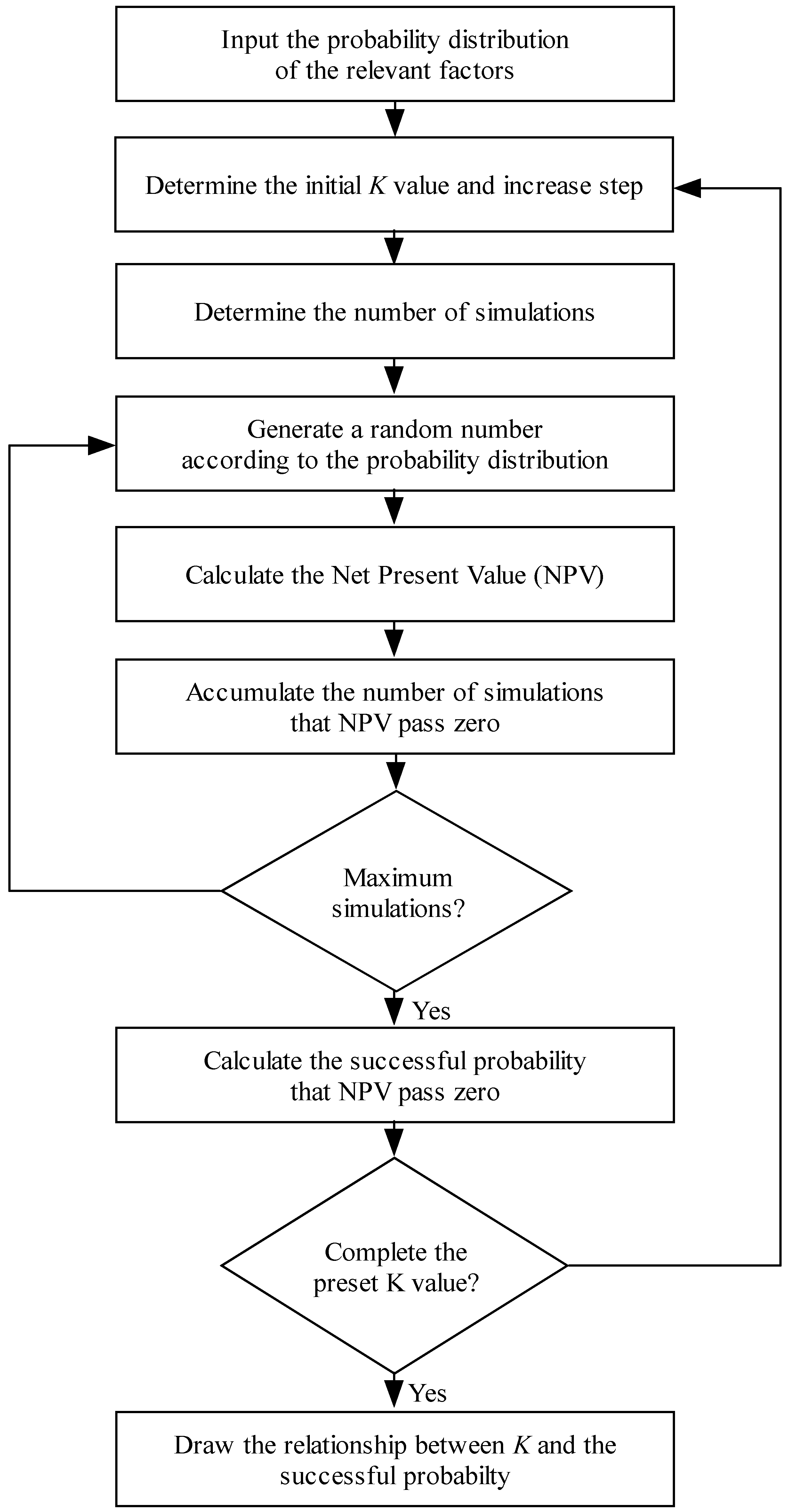

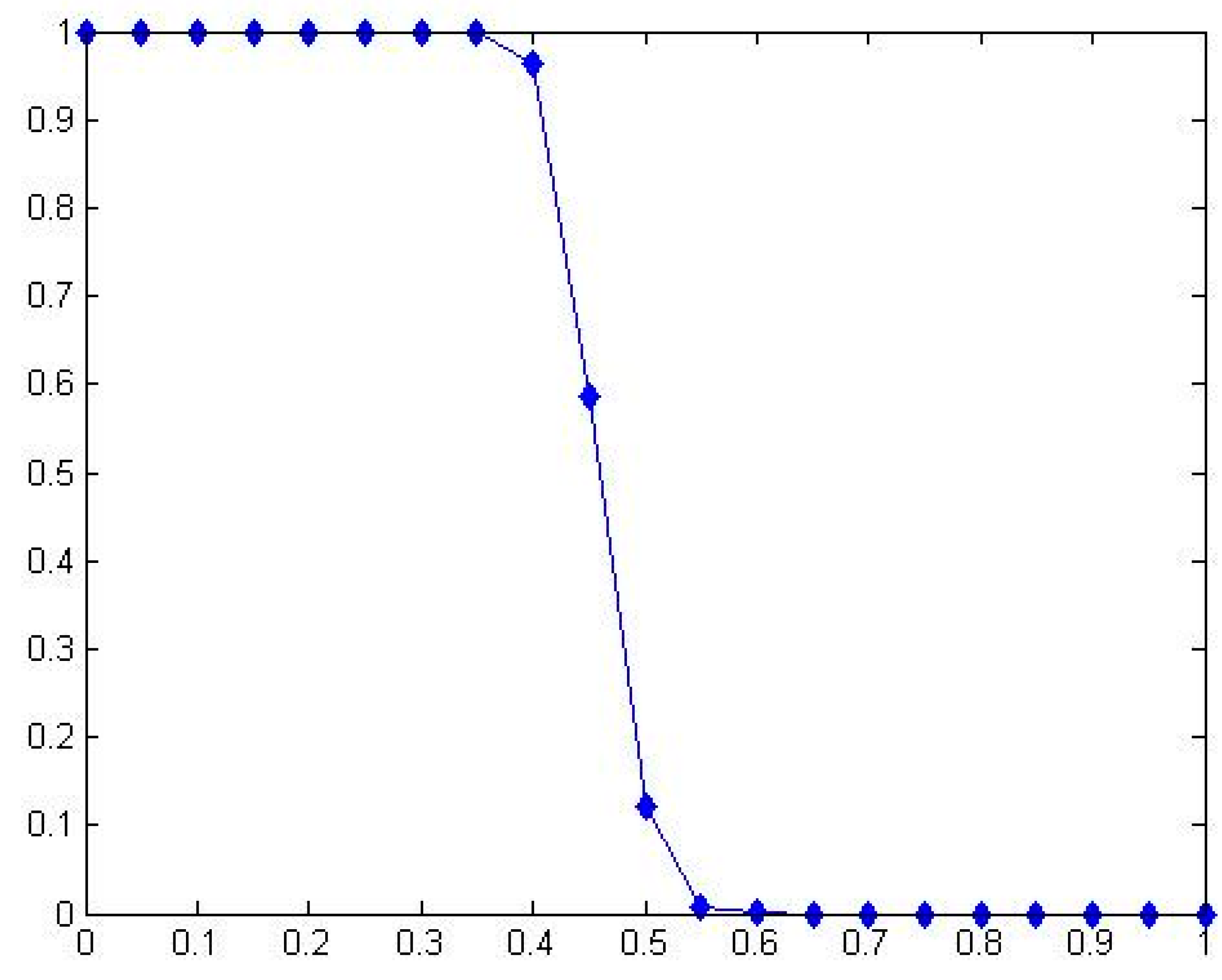

2.2. Conduct MCS to Determine the Relationship between Financing Structure and the Successful Probability

2.3. Step 3 Decision Making Based on the Pre-Set Rules

3. Semi-Hypothetical Case Study

4. Model Validation

| Interviewee | Work Unit | Years of Relevant Work Experience | Education Level | Major Responsibility | Time | Venue |

|---|---|---|---|---|---|---|

| Int 1 | University | 15 | Ph.D. | Research in affordable housing | 13 May 2014 | office |

| Int 2 | University | 8 | Ph.D. | Research in PPP | 13 May 2014 | office |

| Int 3 | University | 4 | Ph.D. | Research in affordable housing | 13 May 2014 | office |

| Int 4 | Government departments | 6 | Ph.D. | Attracting investment | 14 May 2014 | office |

| Int 5 | Government departments | 10 | Master | Policy-making of affordable housing | 14 May 2014 | office |

5. Conclusions

Acknowledgments

Author Contributions

Appendix: Cost and Income Estimation in This Study

- (1)

- The housing maintenance cost is about 20,000 yuan per year, with an annual growth of 10%. The growth rate is assumed to follow normal distribution, with a mean value of 10% and a variance of 5%.

- (2)

- Public rental housing requires four security personnel (2500 yuan/month/person) and six cleaning staff members (1800 yuan/month/person), with an annual growth of about 5%. The growth rate is assumed to follow normal distribution, with a mean value of 5% and a variance of 3%.

- (3)

- The operating cost of the four elevators is 48,000 yuan per year, and the cost for water and electrical appliance replacement is 2000 yuan per year, with an annual growth of 5%. The growth rate is assumed to follow normal distribution with a mean value of 5% and a variance of 3%.

- (4)

- Business tax and surcharges are incorporated in the operating cost according to 5.5% of the business revenue. The tax rate is assumed to be fixed, considering that China may maintain such a rate to promote market economy.

- (1)

- Income from rentals of public rental housing = 1800 apartments × 1012 yuan/apartment/month × 12 months × 85% = 18,580,320 per year. The growth rate is assumed to follow normal distribution with a mean value of 6% and a variance of 3%.

- (2)

- Income from rentals of ancillary housing for business purposes is equal to 200,000 yuan per year. The growth rate is assumed to follow normal distribution with a mean value of 6% and a variance of 3%.

| No. | Items | Definition | Cost |

|---|---|---|---|

| 1 | Land cost |

| 10,157 Yuan/m2 × 50,000 m2 = 507.85 million Yuan |

| 2 | Preliminary project cost |

| 5 million Yuan +10 million Yuan = 15 million Yuan |

| 3 | Construction and installation cost |

| 1600 Yuan/m2 × 50,000 m2 = 80 million Yuan |

| 4 | Public facilities cost |

| 220 Yuan/m2 × 50,000 m2 = 110 million Yuan |

| 1800 Yuan/m2 × 2500 + 80 Yuan/m2× 50,000 = 8.5 million Yuan | |||

| 5 | Management fees |

| 100 Yuan/m2 × 50,000= 5 million Yuan |

| 6 | Reserve fund |

| 100 × 50,000 =5 million Yuan |

| 7 | Financial cost |

| 13.9875 million Yuan |

| Total investment cost | 646.3375 million Yuan | ||

Conflicts of Interest

References

- Wu, Y.Z.; Peng, Y.; Zhang, X.L.; Skitmore, M.; Song, Y. Development priority zoning (DPZ)-led scenario simulation for regional land use change: The case of Suichang County, China. Habitat Int. 2012, 36, 268–277. [Google Scholar] [CrossRef] [Green Version]

- Shen, L.Y.; Peng, Y.; Zhang, X.L.; Wu, Y.Z. An alternative model for evaluating sustainable urbanization. Cities 2012, 29, 32–39. [Google Scholar] [CrossRef]

- Chen, M.; Liu, W.; Tao, X. Evolution and assessment on China’s urbanization 1960–2010: Under-urbanization or over-urbanization? Habitat Int. 2013, 38, 25–33. [Google Scholar] [CrossRef]

- Huang, Y. Low-income housing in Chinese cities: Policies and practices. China Q. 2012, 212, 941–964. [Google Scholar] [CrossRef]

- Wu, J.; Gyourko, J.; Deng, Y.H. Evaluating conditions in major Chinese housing markets. Reg. Sci. Urban Econ. 2012, 42, 531–543. [Google Scholar] [CrossRef]

- Zou, Y.H. Contradictions in China’s affordable housing policy: Goals vs. structure. Habitat Int. 2014, 41, 8–16. [Google Scholar] [CrossRef]

- Li, D.Z.; Chen, H.X.; Hui, E.C.M.; Xiao, C.; Cui, Q.B.; Li, Q.M. A real option-based valuation model for privately-owned public rental housing projects in China. Habitat Int. 2014, 43, 125–132. [Google Scholar] [CrossRef]

- Mak, S.W.; Choy, L.H.; Ho, W.K. Privatization, housing conditions and affordability in the People’s Republic of China. Habitat Int. 2007, 31, 177–192. [Google Scholar] [CrossRef]

- Lian, S. Ant Tribe: Rendezvous of Fresh Graduates; Guangxi Normal University Press: Liuzhou, China, 2009. (In Chinese) [Google Scholar]

- Han, H. Survey on the Read Habitats of Young Ant Tribe Graduates in Beijing, Shanghai and Guangzhou. Available online: http://www.cbbr.com.cn/web/c_000000070001/d_26508.html (accessed on 20 May 2014). (In Chinese)

- Zhang, J.K.; Wang, X.R.; Wu, L.F. PPP model of subsidized house for the “ant tribe” in China. J. Southeast Univ. (Philos. Soc. Sci.) 2012, 14, 41–45. (In Chinese) [Google Scholar]

- People Internet. Understanding the Young Ant Tribe Graduates: The Psychological Condition. Available online: http://book.people.com.cn/GB/69399/107428/178772/10707862.html (accessed on 20 May 2014). (In Chinese)

- Qi, Y.F. Goodbye to Tangjialing. Available online: http://news.ifeng.com/shendu/lwdfzk/detail_2014_02/24/34118488_0.shtml (accessed on 20 May 2014). (In Chinese)

- Jones, C. Private investment in rented housing and the role of REITS. Eur. J. Hous. Policy 2007, 7, 383–400. [Google Scholar] [CrossRef]

- Whitehead, C.M.E. Planning policies and affordable housing: England as a successful case study? Hous. Stud. 2007, 22, 25–44. [Google Scholar] [CrossRef]

- Lawson, J.; Berry, M.; Milligan, V.; Yates, J. Facilitating investment in affordable housing-towards an Australian model. Hous. Financ. Int. 2009, 24, 18–26. [Google Scholar]

- Norris, M.; O’Connell, C. Social housing management, governance and delivery in Ireland: Ten years of reform on seven estates. Hous. Stud. 2010, 25, 317–334. [Google Scholar] [CrossRef]

- Mazouz, B.; Facal, J.; Viola, J.M. Public-private partnership: Elements for a project-based management typology. Proj. Manag. J. 2008, 39, 98–110. [Google Scholar] [CrossRef]

- Xu, Y.L.; Lu, Y.; Chan, A.P.; Skibniewski, M.J.; Yeung, J.F. A computerized risk evaluation model for public-private partnership (PPP) projects and its application. Int. J. Strateg. Prop. Manag. 2012, 16, 277–297. [Google Scholar] [CrossRef]

- Sengupta, U. Government intervention and public-private partnerships in housing delivery in Kolkata. Habitat Int. 2006, 30, 448–461. [Google Scholar] [CrossRef]

- Adegun, O.B.; Taiwo, A.A. Contribution and challenges of the private sector’s participation in housing in Nigeria: Case study of Akure, Ondo state. J. Hous. Built Environ. 2011, 26, 457–467. [Google Scholar] [CrossRef]

- Abdul-Aziz, A.R.; Kassim, J.P.S. Objectives, success and failure factors of housing public-private partnerships in Malaysia. Habitat Int. 2011, 35, 150–157. [Google Scholar] [CrossRef]

- Zhang, Y. Wills and Ways: Policy Dynamics of HOPE VI from 1992–2002. Ph.D. Thesis, Massachusetts Institute of Technology, Cambridge, MA, USA, 1996. [Google Scholar]

- Griffin, L. Creating Affordable Housing in Toronto Using Public-Private Partnerships. Available online: http://fes.yorku.ca/files/outstanding_papers/lara-griffin.pdf (accessed on 20 May 2014).

- Susilawati, C.; Armitage, L. Do Public Private Partnerships Facilitate Affordable Housing Outcome in Queensland? In Proceedings of the 11th European Real Estate Society Conference, Milan, Italy, 2–5 June 2004.

- Wang, Y.P.; Murie, A. The new affordable and social housing provision system in China: implications for comparative housing studies. Int. J. Hous. Policy 2011, 11, 237–254. [Google Scholar] [CrossRef]

- Yuan, J.F.; Guang, M.; Wang, X.X.; Li, Q.M.; Skibniewski, M.J. Quantitative SWOT analysis of public housing delivery by Public-Private Partnerships in China based on the perspective of the public sector. J. Manag. Eng. 2012, 28, 407–420. [Google Scholar] [CrossRef]

- Shen, L.Y.; Li, H.; Li, Q.M. Alternative concession model for build operate transfer contract projects. J. Constr. Eng. Manag. 2002, 128, 326–330. [Google Scholar] [CrossRef]

- Yeo, K.T.; Tiong, R.L.K. Positive management of differences for risk reduction in BOT projects. Int. J. Proj. Manag. 2000, 18, 257–265. [Google Scholar] [CrossRef]

- Shen, L.Y.; Wu, Y.Z. Risk Concession Model for Build/Operate/Transfer Contract Projects. J. Constr. Eng. Manag. 2005, 131, 211–220. [Google Scholar] [CrossRef]

- Zhang, X.Q.; AbouRizk, S.M. Determining a reasonable concession period for private sector provision of public works and services. Can. J. Civil Eng. 2006, 33, 622–631. [Google Scholar] [CrossRef]

- Ng, S.T.; Xie, J.Z.; Skitmore, M.; Cheung, Y.K. A fuzzy simulation model for evaluating the concession items of public-private partnership schemes. Autom. Constr. 2007, 17, 22–29. [Google Scholar] [CrossRef] [Green Version]

- Ngee, L.; Tiong, R.L.K.; Alum, J. Automated approach to negotiation of BOT contracts. J. Comput. Civil Eng. 1997, 11, 121–128. [Google Scholar] [CrossRef]

- Cheng, L.Y.; Tiong, R.L.K. Minimum feasible tariff model for BOT water supply projects in Malaysia. Constr. Manag. Econ. 2005, 23, 255–263. [Google Scholar] [CrossRef]

- Huang, Y.L.; Chou, S.P. Valuation of the minimum revenue guarantee and the option to abandon in BOT infrastructure projects. Constr. Manag. Econ. 2006, 24, 379–389. [Google Scholar] [CrossRef]

- Shen, L.Y.; Bao, H.J.; Wu, Y.Z.; Lu, W.S. Using bargaining-game theory for negotiating concession period for BOT-type contract. J. Constr. Eng. Manag. 2007, 133, 385–392. [Google Scholar] [CrossRef]

- Subprasom, K.; Chen, A. Effects of regulation on highway pricing and capacity choice of a build-operate-transfer scheme. J. Constr. Eng. Manag. 2007, 133, 64–71. [Google Scholar] [CrossRef]

- Zhang, X. Q. Web-based concession period analysis system. Expert Syst. Appl. 2011, 38, 13532–13542. [Google Scholar]

- Khanzadi, M.; Nasirzadeh, F.; Alipour, M. Integrating system dynamics and fuzzy logic modeling to determine concession period in BOT projects. Autom. Constr. 2012, 22, 368–376. [Google Scholar] [CrossRef]

- Hanaoka, S.; Palapus, H. P. Reasonable concession period for build-operate-transfer road projects in the Philippines. Int. J. Proj. Manag. 2012, 30, 938–949. [Google Scholar] [CrossRef]

- Yu, C.Y.; Lam, K.C. A decision support system for the determination of concession period length in transportation project under BOT contract. Autom. Constr. 2013, 31, 114–127. [Google Scholar] [CrossRef]

- Bao, H.J.; Peng, Y.; Ablanedo-Rosas, J.H.; Gao, H.M. An alternative incomplete information bargaining model for identifying the reasonable concession period of a BOT project. J. Proj. Manag. 2015. [Google Scholar] [CrossRef]

- Yuan, Y.B.; Ye, G.W.; Zhang, M.Y. A Study on Optimizing the Financing Structure of PPP Model for Infrastructure. Technoecon. Manag. Res. 2011, 3, 91–95. (In Chinese) [Google Scholar]

- Shen, L.Y.; Lu, W.S.; Peng, Y.; Jiang, S.J. Critical Assessment indicators for measuring benefits of rural infrastructure investment in China. J. Infrastruct. Syst. 2011, 17, 176–183. [Google Scholar] [CrossRef]

© 2015 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xu, Y.; Peng, Y.; Qian, Q.K.; Chan, A.P.C. An Alternative Model to Determine the Financing Structure of PPP-Based Young Graduate Apartments in China: A Case Study of Hangzhou. Sustainability 2015, 7, 5720-5734. https://doi.org/10.3390/su7055720

Xu Y, Peng Y, Qian QK, Chan APC. An Alternative Model to Determine the Financing Structure of PPP-Based Young Graduate Apartments in China: A Case Study of Hangzhou. Sustainability. 2015; 7(5):5720-5734. https://doi.org/10.3390/su7055720

Chicago/Turabian StyleXu, Yelin, Yi Peng, Queena K. Qian, and Albert P. C. Chan. 2015. "An Alternative Model to Determine the Financing Structure of PPP-Based Young Graduate Apartments in China: A Case Study of Hangzhou" Sustainability 7, no. 5: 5720-5734. https://doi.org/10.3390/su7055720

APA StyleXu, Y., Peng, Y., Qian, Q. K., & Chan, A. P. C. (2015). An Alternative Model to Determine the Financing Structure of PPP-Based Young Graduate Apartments in China: A Case Study of Hangzhou. Sustainability, 7(5), 5720-5734. https://doi.org/10.3390/su7055720