Consideration of ERP Effectiveness: From the Perspective of ERP Implementation Policy and Operational Effectiveness

Abstract

:1. Introduction

2. Literature Review

3. Analysis of Customer Satisfaction Structure

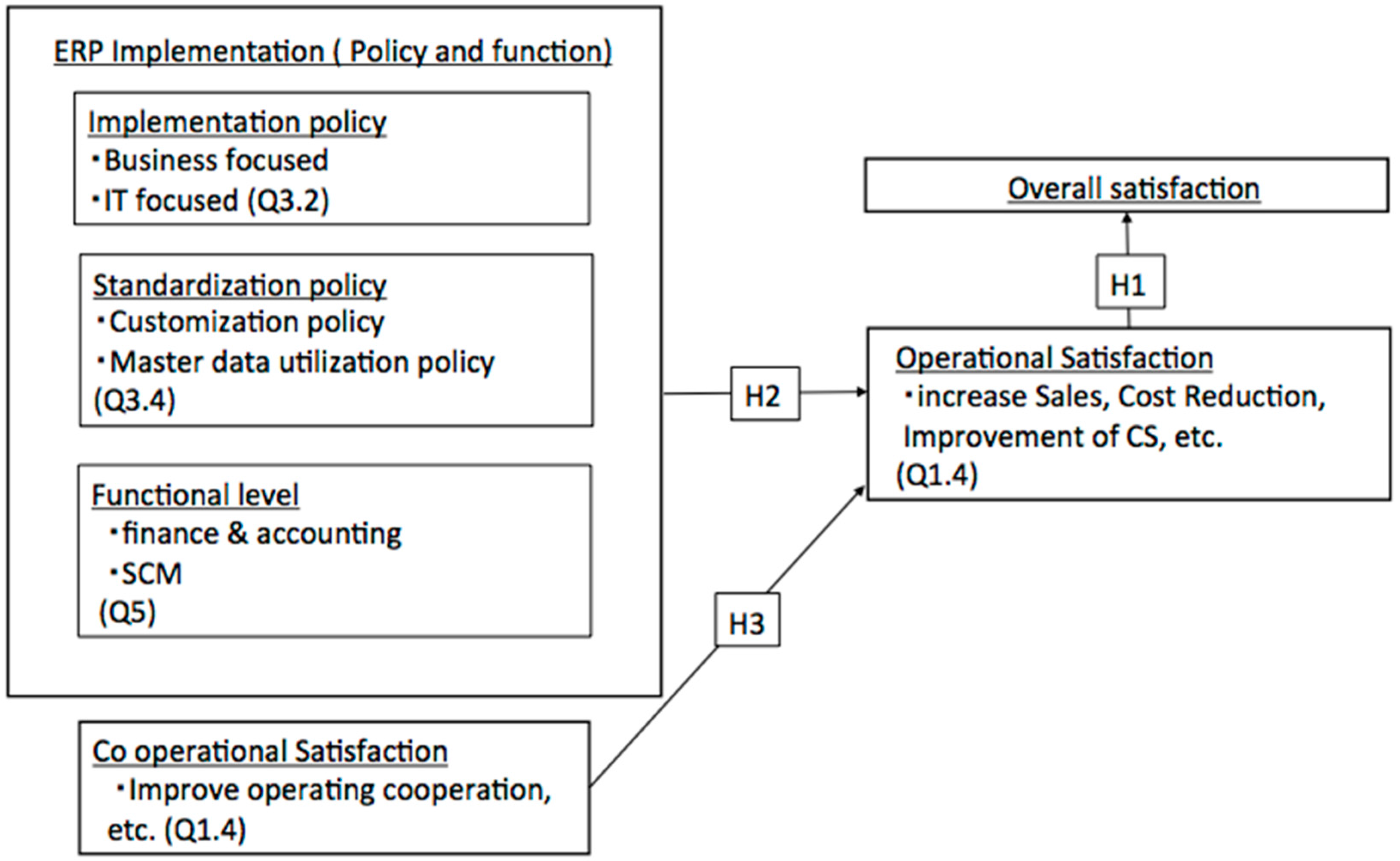

3.1. Conceptual Research Framework and Hypothesis

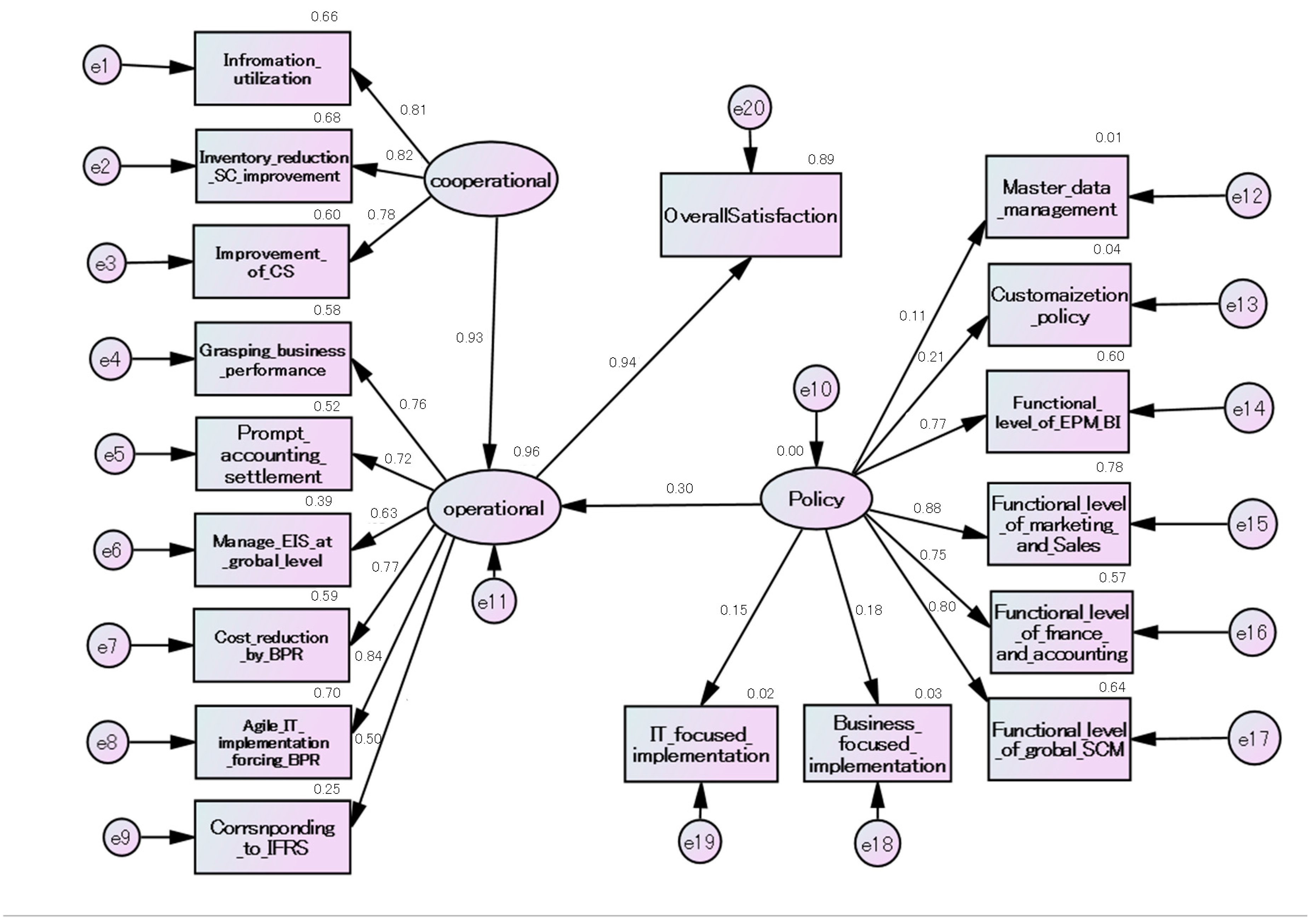

3.2. Research Result

4. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Hammer, M.; Stanton, S.A. The Reengineering Revolution: A Handbook; Harper Collins: New York, NY, USA, 1995. [Google Scholar]

- Hammer, M. Beyond Reengineering; Harper Business: New York, NY, USA, 1996. [Google Scholar]

- Holland, C.P.; Light, B. IEEE Software 16 May/June 1999; Manchester Business School: London, UK, 1999; pp. 30–36. [Google Scholar]

- O’Leary, D.E. Enterprise Resource Planning Systems: Systems, Life Cycle, Electronic Commerce, and Risk; Cambridge University Press: Cambridge, UK, 2000. [Google Scholar]

- ERP Forum. ERP no Saishin Doukou (The Latest Trend of ERP, in Japanese, Annual Research Report); Impress Business Media: Tokyo, Japan, 2014. [Google Scholar]

- Iizuka, K.; Okawada, T.; Tsubone, M.; Iizuka, Y.; Suematsu, C. Issues about Inter-organizational Process Flow Adjustment. In Enterprise and Organizational Modeling and Simulation; Springer: Heidelberg, Germany, 2013; pp. 24–41. [Google Scholar]

- Huang, Z.; Palvia, P. ERP Implementation Issues in Advanced and Developing Countries. Bus. Process Manag. J. 2001, 7, 276–284. [Google Scholar] [CrossRef]

- Higano, T. IT ni Yoru workstyle Henkaku—White color no Seisansei Koujou ni Muketa IT Katsuyo no Arikata (Transformation of the workstyle of IT—Nature of IT utilization towards improving productivity of white-color); IT Solution Frontier: Holland, MI, USA, 2009; pp. 16–19. (In Japanese) [Google Scholar]

- Cusumano, M.A. The Business of Software: What Every Manager, Programmer, and Entrepreneur Must Know to Thrive and Survive in Good Times and Bad; Free Press: New York, NY, USA, 2004. [Google Scholar]

- Iizuka, K.; Tsuda, K. Strategy for software business-from the perspective of customers’ value recognition. Ann. J. Inf. Sci. Lab. Senshu Univ. 2006, 28, 33–56. [Google Scholar]

- Tanaka, T. Software Selection and Productivity of Japanese Companies—Custom Software vs. Packaged Software. In RIETI Discussion Paper Series 10-J-027; The Research of Economy, Trade and Industry: Tokyo, Japan, 2010. [Google Scholar]

- Kumazawa, H. ERP donyu ni yoru kouka to nannido no jissai. Effectiveness and difficulty of ERP implementation. Oper. Res. 2004, 49, 352–358. (In Japanese) [Google Scholar]

- Takei, Y.; Nagase, R.; Iizuka, K. Consideration on Achieving Effectiveness Using ERP System: From the Analysis of Satisfaction Structure. In Proceedings of the 2014 International Symposium on Business and Management (ISBM 2014), Tokyo, Japan, 12–14 November 2014; pp. 1035–1055.

- Jarrar, Y.F.; Mudimigh, A.; Zairi, M. ERP implementation critical success factors-the role and impact of business process management, Management of Innovation and Technology, 2000. ICMIT 2000. In Proceedings of the 2000 IEEE International Conference on Innovation and Technology, Singapore, 2–5 June 2000; pp. 122–127.

- Finney, S.; Corbett, M. ERP implementation: A compilation and analysis of critical success factors. Bus. Process Manag. J. 2007, 13, 329–347. [Google Scholar] [CrossRef]

- Markus, M.L.; Tanis, C. The enterprise systems experience—From adoption to success. In Framing the Domains of IT Management: Projecting the Future through the Past; Zmud, R.W., Ed.; Pinnaflex Educational Resources Inc.: Cincinnati, OH, USA, 2000; pp. 173–207. [Google Scholar]

- Bingi, P.; Sharma, M.K.; Godla, J.K. Critical issues affecting an ERP implementation. Inf. Syst. Manag. 1999, 16, 7–14. [Google Scholar] [CrossRef]

- Ghobakhloo, M.; Hong, T.S.; Sabouri, M.S.; Zulkifli, N. Strategies for Successful Information Technology Adoption in Small and Medium-sized Enterprises. Information 2012, 3, 36–67. [Google Scholar] [CrossRef]

- Albashrawi, M.; Motiwalla, L. Adoption of Mobile ERP in Traditional-ERP Organizations: The Effect of Computer Self-Efficacy. In Proceedings of the Americas Conference on Information Systems (AMCIS), San Diego, CA, USA, 11–14 August 2016.

- Nawaz, S.S.; Pulasinghe, K.; Thelijjagoda, S. Mobile Office and Its Implications for ERP Systems: A Review of Literature. Int. J. Adv. Res. Comput. Sci. Softw. Eng. 2015, 5, 13–16. [Google Scholar]

- ERP Forum. ERP no Saishin Doukou (The Latest Trend of ERP, in Japanese, Annual Research Report); Impress Business Media: Tokyo, Japan, 2013. [Google Scholar]

- Iizuka, K.; Iizuka, Y.; Suematsu, C. Consideration of the Business Process Re-Engineering Effect: Business Flow Notation Structure and the Management Perspective, Business Process Management Workshops, Volume 256 of the Series Lecture Notes in Business Information Processing; Springer International Publishing: Cham, Switzerland, 2016; pp. 323–333. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

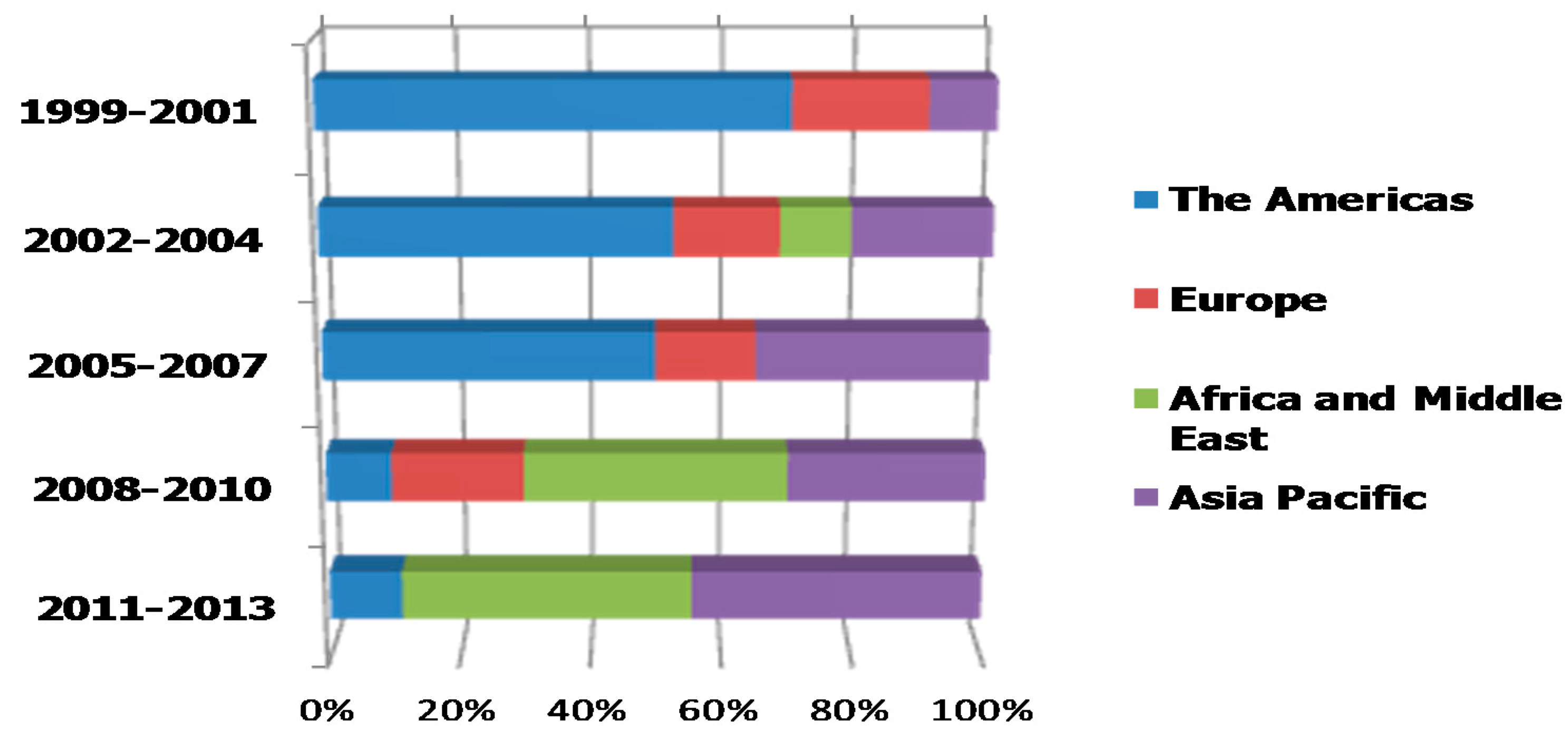

| 1999–2001 | 2002–2004 | 2005–2007 | 2008–2010 | 2011–2013 | |||||

|---|---|---|---|---|---|---|---|---|---|

| USA | 7 | China | 1 | Canada | 1 | Belgium | 1 | China | 2 |

| UK | 2 | Italy | 1 | China | 2 | Egypt | 2 | India | 3 |

| Singapore | 1 | Korea | 2 | India | 1 | India | 1 | Iran | 5 |

| Saudi Arabia | 1 | Malaysia | 3 | Malaysia | 1 | Malaysia | 2 | ||

| Singapore | 1 | Poland | 1 | Pakistan | 1 | Pakistan | 1 | ||

| Netherlands | 1 | Slovenia | 1 | Slovenia | 1 | Saudi Arabia | 1 | ||

| Turkey | 1 | Sweden | 1 | Taiwan | 1 | Taiwan | 1 | ||

| UK | 1 | Taiwan | 1 | UAE | 1 | UAE | 1 | ||

| USA | 10 | USA | 9 | USA | 1 | USA | 2 | ||

| Total | 10 | 19 | 20 | 10 | 18 | ||||

| Before ERP | |||

| Machine’s Name | Purpose | Item of Payment | Expense/Year |

| System-1 | Sales management of SPS. | Machine Lease | 4750 |

| System Charge | 6000 | ||

| Operation Charge | 26,000 | ||

| Maintenance Charge | 20,000 | ||

| System-1 Total | 56,750 | ||

| System-2 | Production of SPS. (inventory, MRP, Purchase) | Machine Lease | 0 |

| System Charge | 0 | ||

| Operation Charge | 24,000 | ||

| Maintenance Charge | 10,000 | ||

| System-2 Total | 34,000 | ||

| System−3 | Production of SPS. (cost, inventory, WIP, Purchase) | Machine Lease | 1980 |

| System Charge | 1200 | ||

| Operation Charge | 0 | ||

| Maintenance Charge | 5000 | ||

| System-3 Total | 8180 | ||

| Outsourcing | Human Resource | Total | 16,800 |

| System-4 | Sales management of SP. Production of SP. All of accounting. | Machine Lease | 22,000 |

| System Charge | 14,000 | ||

| Operation Charge | 30,000 | ||

| Maintenance Charge | 70,000 | ||

| System-4 Total | 136,000 | ||

| Total Running Cost | Machine Lease | 28,730 | |

| System Charge | 21,200 | ||

| Operation Charge | 80,000 | ||

| Maintenance Charge | 105,000 | ||

| Others | 16,800 | ||

| G-Total | 251,730 | ||

| After ERP | |||

| Machine’s Name | Purpose | Item of Payment | Expense/Year |

| Hard Ware | Multi Interface Server | 2,900,000 | 30,332 |

| Human Resource Server | 1,880,000 | ||

| ERP Main Server | 137,500,000 | ||

| ERP Development Server | 7,500,000 | ||

| Multi Report Server | 1,880,000 | ||

| ERP (Annual Supporting Fee) | 19,872 | ||

| Developing Tool (Annual Supporting Fee) | 193 | ||

| MRP Planner (Annual Supporting Fee) | 5904 | ||

| Multi Interface (Annual Supporting Fee) | 1958 | ||

| Multi Report (Annual Supporting Fee) | 1760 | ||

| Human Resource/Salary & Add-on (Annual Supporting Fee) | 1958 | ||

| Fixed Assets (Annual Supporting Fee) | 336 | ||

| System charge | 8000 | ||

| Operation charge | 50,000 | ||

| Total Running Cost | 120,313 | ||

| Estimate of Total Cost Reduction/Year | −131,417 | ||

| Annual Sales | Frequency | Percentage |

| Above 1000T | 18 | 10% |

| Between 300B and 1T | 21 | 12% |

| Between 100B and 300B | 27 | 15% |

| Between 50B and 100B | 23 | 13% |

| Between 30B and 50B | 15 | 8% |

| Between 10B and 30B | 36 | 20% |

| Between 5B and 10B | 13 | 7% |

| Under 5B | 29 | 16% |

| Total | 182 | 100% |

| Industry | Frequency | Percentage |

| Service | 31 | 17% |

| Finance business | 5 | 3% |

| Public corporation | 0 | 0% |

| IT film | 48 | 26% |

| Industry | 82 | 45% |

| Distribution | 16 | 9% |

| Total | 182 | 100% |

| Organization (Department/Section) | Frequency | Percentage |

| Chief Information Officer (CIO) | 5 | 3% |

| IT | 105 | 58% |

| Business planning | 11 | 6% |

| Chief Executive Officer (CEO), Executive team | 9 | 5% |

| System user | 52 | 29% |

| Total | 182 | 100% |

| Path | Estimate | S.E. | C.R. | P | ||

|---|---|---|---|---|---|---|

| Operational_satisfaction | <--- | Cooperational_satisfaction | 0.648 | 0.112 | 5.798 | *** |

| Operational_satisfaction | <--- | Policy and activity | 0.200 | 0.047 | 4.307 | *** |

| Improvement_of_CS | <--- | Cooperational_satisfaction | 1.000 | |||

| Inventory_reduction_SC_improvement | <--- | Cooperational_satisfaction | 1.120 | 0.106 | 10.617 | *** |

| Infromation_utilization | <--- | Cooperational_satisfaction | 1.061 | 0.095 | 11.157 | *** |

| Cost_reduction_by_BPR | <--- | Operational_satisfaction | 1.372 | 0.230 | 5.973 | *** |

| Manage_EIS_at_grobal_level | <--- | Operational_satisfaction | 1.209 | 0.231 | 5.241 | *** |

| Prompt_accounting_settlement | <--- | Operational_satisfaction | 1.335 | 0.229 | 5.838 | *** |

| Grasping_business_performance | <--- | Operational_satisfaction | 1.435 | 0.241 | 5.954 | *** |

| OverallSatisfaction | <--- | Operational_satisfaction | 1.549 | 0.243 | 6.369 | *** |

| Agile_IT_implementation_forcing_BPR | <--- | Operational_satisfaction | 1.530 | 0.249 | 6.148 | *** |

| Corrsnponding_to_IFRS | <--- | Operational_satisfaction | 1.000 | |||

| Function_o_level_of_grobal_SCM | <--- | Impremention_policy | 1.029 | 0.141 | 7.287 | *** |

| Functiona_level_of_fnance_and_accounting | <--- | Impremention_policy | 0.874 | 0.108 | 8.059 | *** |

| Functiona_level_of_marketing_and_Sales | <--- | Impremention_policy | 1.124 | 0.128 | 8.757 | *** |

| Functional_level_of_EPM_BI | <--- | Impremention_policy | 1.000 | |||

| Customaizetion_policy | <--- | Impremention_policy | 0.306 | 0.127 | 2.411 | ** |

| Master_data_management | <--- | Policy_and_activity | 0.145 | 0.110 | 1.312 | 0.190 |

| Business_focused_implementation | <--- | Policy_and_activity | 0.229 | 0.112 | 2.040 | ** |

| IT_focused_implementation | <--- | Policy_and_activity | 0.153 | 0.104 | 1.469 | 0.142 |

| Path | Estimate | ||

|---|---|---|---|

| Operational_satisfaction | <--- | Cooperational_satisfaction | 0.932 |

| Operational_satisfaction | <--- | Impremention_policy | 0.297 |

| Improvement_of_CS | <--- | Cooperational satisfaction | 0.776 |

| Inventory_reduction_SC_improvement | <--- | Cooperational satisfaction | 0.825 |

| Infromation_utilization | <--- | Cooperational satisfaction | 0.814 |

| Cost_reduction_by_BPR | <--- | Operational_satisfaction | 0.769 |

| Manage_EIS_at_grobal_level | <--- | Operational_satisfaction | 0.627 |

| Prompt_accounting_settlement | <--- | Operational_satisfaction | 0.721 |

| Grasping_business_performance | <--- | Operational_satisfaction | 0.759 |

| OverallSatisfaction | <--- | Operational_satisfaction | 0.943 |

| Agile_IT_implementation_forcing_BPR | <--- | Operational_satisfaction | 0.839 |

| Corrsnponding_to_IFRS | <--- | Operational_satisfaction | 0.503 |

| Function_o_level_of_grobal_SCM | <--- | Impremention_policy | 0.800 |

| Functiona_level_of_fnance_and_accounting | <--- | Impremention_policy | 0.754 |

| Functiona_level_of_marketing_and_Sales | <--- | Impremention_policy | 0.882 |

| Functional_level_of_EPM_BI | <--- | Impremention_policy | 0.775 |

| Customaizetion_policy | <--- | Impremention_policy | 0.208 |

| Master_data_management | <--- | Impremention_policy | 0.112 |

| Business_focused_implementation | <--- | Impremention_policy | 0.183 |

| IT_focused_implementation | <--- | Impremention_policy | 0.147 |

| Estimate | S.E. | C.R. | P | Label | |

|---|---|---|---|---|---|

| Cooperational_satisfaction | 0.337 | 0.059 | 5.735 | *** | |

| e10 | 0.356 | 0.076 | 4.720 | *** | |

| e11 | 0.007 | 0.006 | 1.105 | 0.269 | |

| e1 | 0.193 | 0.026 | 7.431 | *** | |

| e2 | 0.198 | 0.031 | 6.493 | *** | |

| e3 | 0.223 | 0.029 | 7.582 | *** | |

| e4 | 0.246 | 0.028 | 8.711 | *** | |

| e5 | 0.268 | 0.030 | 8.861 | *** | |

| e6 | 0.366 | 0.047 | 7.763 | *** | |

| e7 | 0.211 | 0.025 | 8.583 | *** | |

| e8 | 0.160 | 0.020 | 8.000 | *** | |

| e9 | 0.479 | 0.060 | 7.955 | *** | |

| e12 | 0.585 | 0.062 | 9.399 | *** | |

| e13 | 0.737 | 0.080 | 9.231 | *** | |

| e14 | 0.237 | 0.042 | 5.585 | *** | |

| e15 | 0.129 | 0.036 | 3.628 | *** | |

| e16 | 0.207 | 0.034 | 6.168 | *** | |

| e17 | 0.212 | 0.048 | 4.451 | *** | |

| e18 | 0.536 | 0.061 | 8.859 | *** | |

| e19 | 0.380 | 0.048 | 7.959 | *** | |

| e20 | 0.049 | 0.009 | 5.189 | *** |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license ( http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jinno, H.; Abe, H.; Iizuka, K. Consideration of ERP Effectiveness: From the Perspective of ERP Implementation Policy and Operational Effectiveness. Information 2017, 8, 14. https://doi.org/10.3390/info8010014

Jinno H, Abe H, Iizuka K. Consideration of ERP Effectiveness: From the Perspective of ERP Implementation Policy and Operational Effectiveness. Information. 2017; 8(1):14. https://doi.org/10.3390/info8010014

Chicago/Turabian StyleJinno, Haruna, Hiromichi Abe, and Kayo Iizuka. 2017. "Consideration of ERP Effectiveness: From the Perspective of ERP Implementation Policy and Operational Effectiveness" Information 8, no. 1: 14. https://doi.org/10.3390/info8010014

APA StyleJinno, H., Abe, H., & Iizuka, K. (2017). Consideration of ERP Effectiveness: From the Perspective of ERP Implementation Policy and Operational Effectiveness. Information, 8(1), 14. https://doi.org/10.3390/info8010014