CioSy: A Collaborative Blockchain-Based Insurance System

Abstract

:1. Introduction

- We highlight the benefits of using the blockchain technology and smart contracts to enable peer-to-peer collaborative insurance, where customers rely on each other to meet their insurance needs while eliminating a centralized authority and adopt them in a new scheme, called CioSy. To the best of our knowledge, none of the existing solutions for digitized insurance consider covering all the insurance business process steps (from the insurer teaming up until the claim handling).

- We introduce the machine-readable and self-enforcing insurance policies and claims based on voting mechanisms and external oracles as well as detail the working principles of the proposed blockchain-based insurance system.

- We evaluate CioSy performance and scalability when the number of insurance claims and insurers increases. We analyze the performance of the proposed system in terms of execution time, scalability overhead, and the consumed gas.

2. Related Work

3. Blockchain Technology and Smart Contracts for Insurance

3.1. Blockchain and Smart Contracts

3.2. Blockchain at the Service of Insurance

3.3. System Model Main Goals

3.4. Functional Entities

4. System Model for Blockchain-Based Insurance System

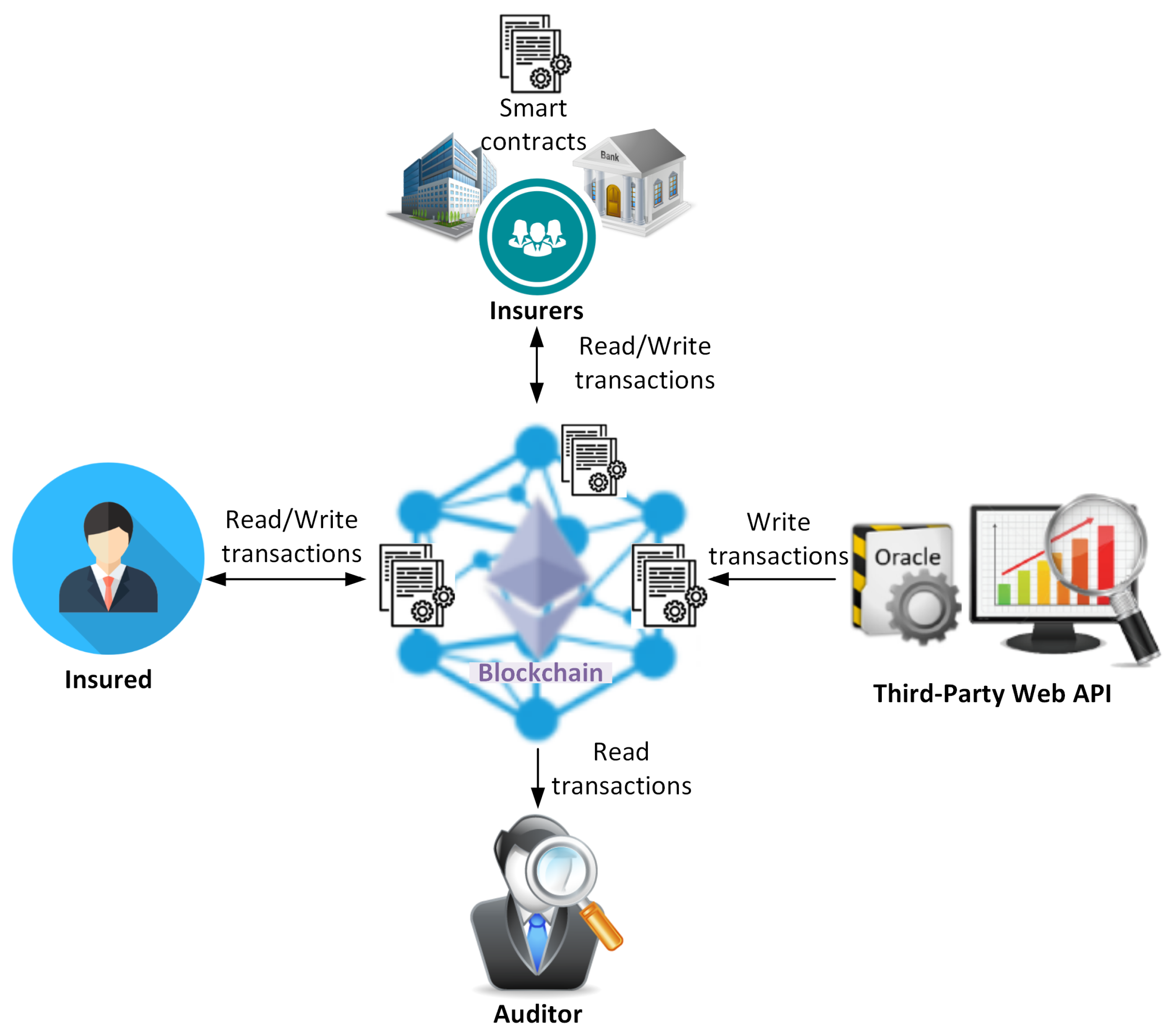

- Insured: This entity is interested in purchasing policies offered by an insurer in order to be covered (depending on the type of insurance). In case of a claim request, the insured can receive refunds from the insurer (subject to verification).

- Insurer: This entity is represented by a smart contract shared among several customers (e.g., people, banks, insurance companies, etc.). These customers collaborate together to pool their contributions/premiums and protect each other by refunding any customer facing a situation that warrants a refund. The refunded entity is then required to contribute to the fund that is used to pay future claims. This smart contract provides insurance for the insured by proposing multiple insurance policy types. Each insurance policy determines the claims that the insurer is legally required to pay. To reduce manual interactions, claim requests are automatically invoked after notifications/warnings are sent by third-party web APIs.

- Third-Party Web APIs: These entities provide specialized services that are useful to invoke claim requests; for instance, an airline’s API that notifies the policy smart contract in case of a flight delay or IoT-equipped vehicles that report near-real time accidents. In case of a dispute between the insurer and the insured, there may be a need for an auditor.

- Auditor: This entity investigates and audits the insurance transactions stored on the blockchain to settle some legal dispute between the insurer and insured. The blockchain-enabled distributed platform facilitates the auditor’s task, thanks to the salient features of blockchain, i.e., transparency, tamper-proof, and the non-repudiation.

5. Blockchain-Based Framework for Insurance

5.1. Proposed Smart Contracts

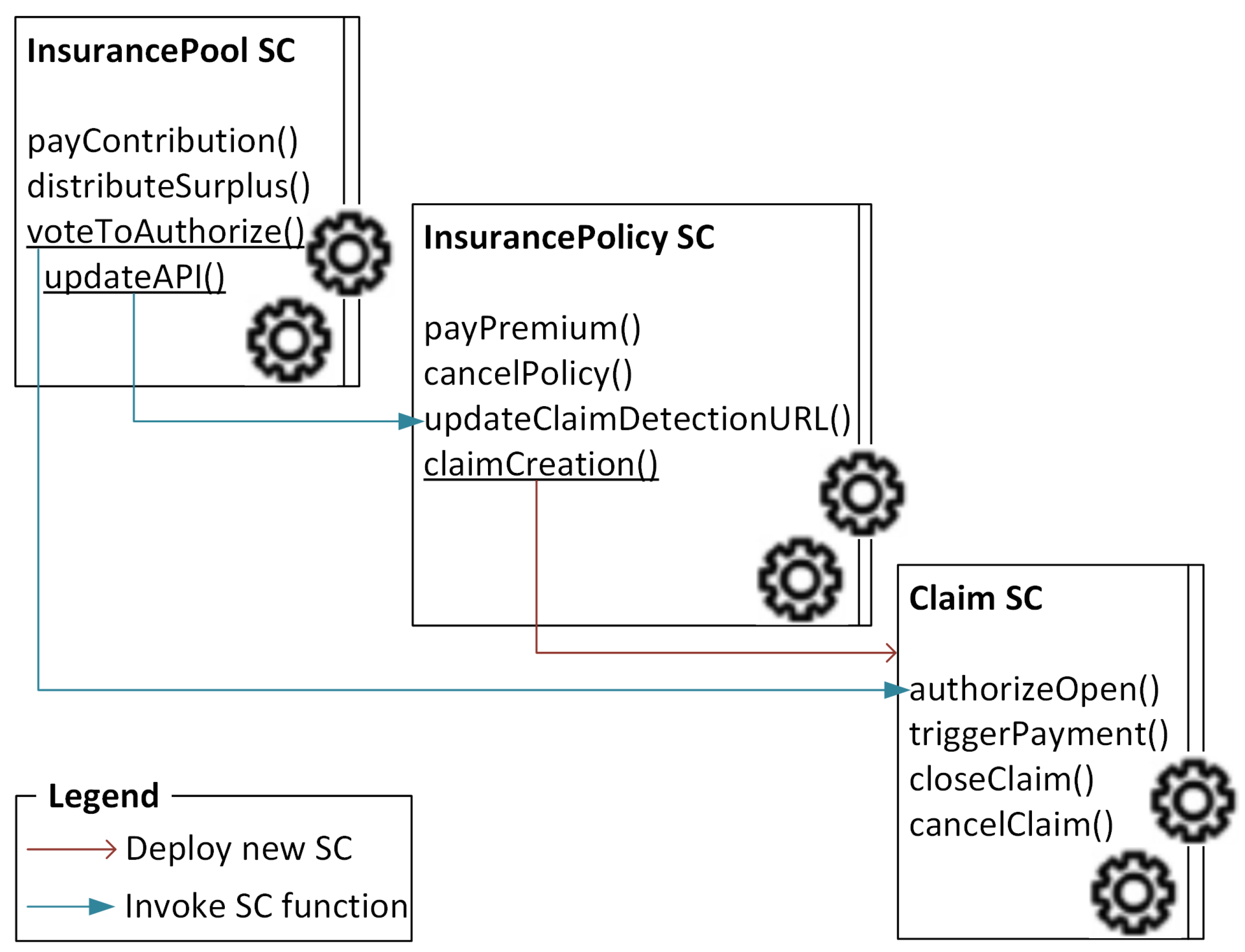

- InsurancePool smart contract: it is hosted on the blockchain and used by multiple clients interested in proposing multiple insurance offers. The InsurancePool smart contract is designed to enable several insurers to collaborate on a common project that offers a collaborative insurance to refund the insured for possible damage(s) during designated incidents. This smart contract defines a set of functions, i.e., a (i) payContribution function that enables each insurer to participate by paying an amount of money to the insurance pool, (ii) updateAPI function that enables the insurers to update the link to the third-party web API, this function invokes automatically one of the Claim smart contract’s functions, (iii) voteToAuthorize function that enables the insurers to decide whether to authorize or not opening a claim, this function also invokes automatically one of the Claim smart contract’s functions, and (iv) distributeSurplus function that is invoked at the end of the year in order to distribute the surplus of the collected money to all insurers who have not had any claims during the last year (each according to its contribution).

- InsurancePolicy smart contract: it is created by the customer interested in purchasing policies offered by the insurer and hosted on the blockchain. The InsurancePolicy smart contract is designed to enable the insured, known as the policyholder, to hold a machine-readable and self-enforcing insurance policy. This smart contract defines a set of functions, namely a (i) payPremium function that enables the policyholder to pay periodically a premium which is a fixed amount of money to the insurer, (ii) cancelPolicy function that enables the policyholder to cancel a purchased insurance policy, thus the insurance policy status is updated to “Canceled” and the insurance policy is canceled, (iii) updateClaimDetectionURL function that is invoked by the updateAPI function defined in the appropriate InsurancePool smart contract instance in order to update the link to the third-party web API, and (iv) claimCreation function that is connected to an external third-party web API, then in case of a received claim notification, this function creates/deploys automatically a new instance of the Claim smart contract. The InsurancePolicy smart contract inherits the usingProvable smart contract [22] which helps to connect our proposed smart contract with the external data provided by the third-party web APIs.

- Claim smart contract: it is created by an InsurancePolicy smart contract and hosted on the blockchain. The Claim smart contract is designed to automate the claim processing, verification, and payment. This smart contract defines a set of functions, namely a (i) authorizeOpen function that enables the insurer to update the status of the claim from “Created” to “Open” or to “Rejected”, this function is invoked by the voteToAuthorize function defined in the InsurancePool smart contract, (ii) triggerPayment function that is automatically invoked in order to refund the claimed amount and ask for closing the claim, (iii) closeClaim function that is automatically invoked once the insured is refunded by updating the claim’s status to “Closed”, and (iv) cancelClaim function that enables the insured to cancel a claim, then the claim status is updated to “Canceled” and the claim is canceled.

5.2. Main Functions and Working Principles of the Proposed Blockchain-Based Insurance

5.2.1. Gathering the Insurers as a Collaborative Community

- Step 1: Create (i.e., write and compile) an InsurancePool smart contract.

- Step 2: Send a transaction to deploy the created smart contract onto the blockchain. Once hosted, the InsurancePool smart contract instance got a unique blockchain address.

- Step 3: Send a transaction to call the payContribution function defined in the created InsurancePool smart contract to pay periodically an amount of money.

5.2.2. Purchasing an Insurance Policy Offered by an Insurance Pool

- Step 1: Create (i.e., write and compile) an InsurancePolicy smart contract.

- Step 2: Send a transaction to deploy the created smart contract onto the blockchain with a precise insurer’s blockchain address (i.e., the blockchain address of the InsurancePool smart contract) and the fixed premium payment amount. The sender of this transaction becomes the owner of the InsurancePolicy smart contract instance, known as the policyholder.

- Step 3: Send a transaction by the defined insurer to call the updateClaimDetectionURL function defined in the InsurancePolicy smart contract to update the link to the third-party web API, which is responsible for claim notifications.

5.2.3. Creating a Claim by the Insurance Policy

- Step 1: Receive a notification from an associated third-party web API that a potential claim has happened.

- Step 2: Call internally the claimCreation function defined in the InsurancePolicy smart contract by the callback function of the usingProvable smart contract [22] in order to deploy a new Claim smart contract instance onto the blockchain. The same InsurancePolicy smart contract instance can create multiple Claim smart contract instances.

5.2.4. Automating Claim Processing and Refund Payment

- Step 1: The insured sends a transaction to call the cancelClaim function defined in the Claim smart contract to cancel the claim and update the claim’s status from “Created” to “Canceled”. One of the most common reasons why the insured might want to cancel a claim is not wanting to pay the deductible, which is the amount of money paid by the insured before the insurer refunds the claimed amount.

- Step 1: Send a transaction by the insurer to call the authorizeOpen function defined in the Claim smart contract to authorize opening the claim or reject it after a claim verification by claim experts and the insured confirmation.

- Step 2: Once the claim is open, call internally the triggerPayment function in order to transfer the deductible amount from the insured account to the insurer account and transfer the claimed amount from the insurer account to the insured account.

- Step 3: Call internally the closeClaim function to update the claim’s status to “Closed”.

6. Performance Evaluation

6.1. Experimental Setup

6.2. Use-Case: Insurance Policy Handling

6.3. Performance Evaluation Metrics

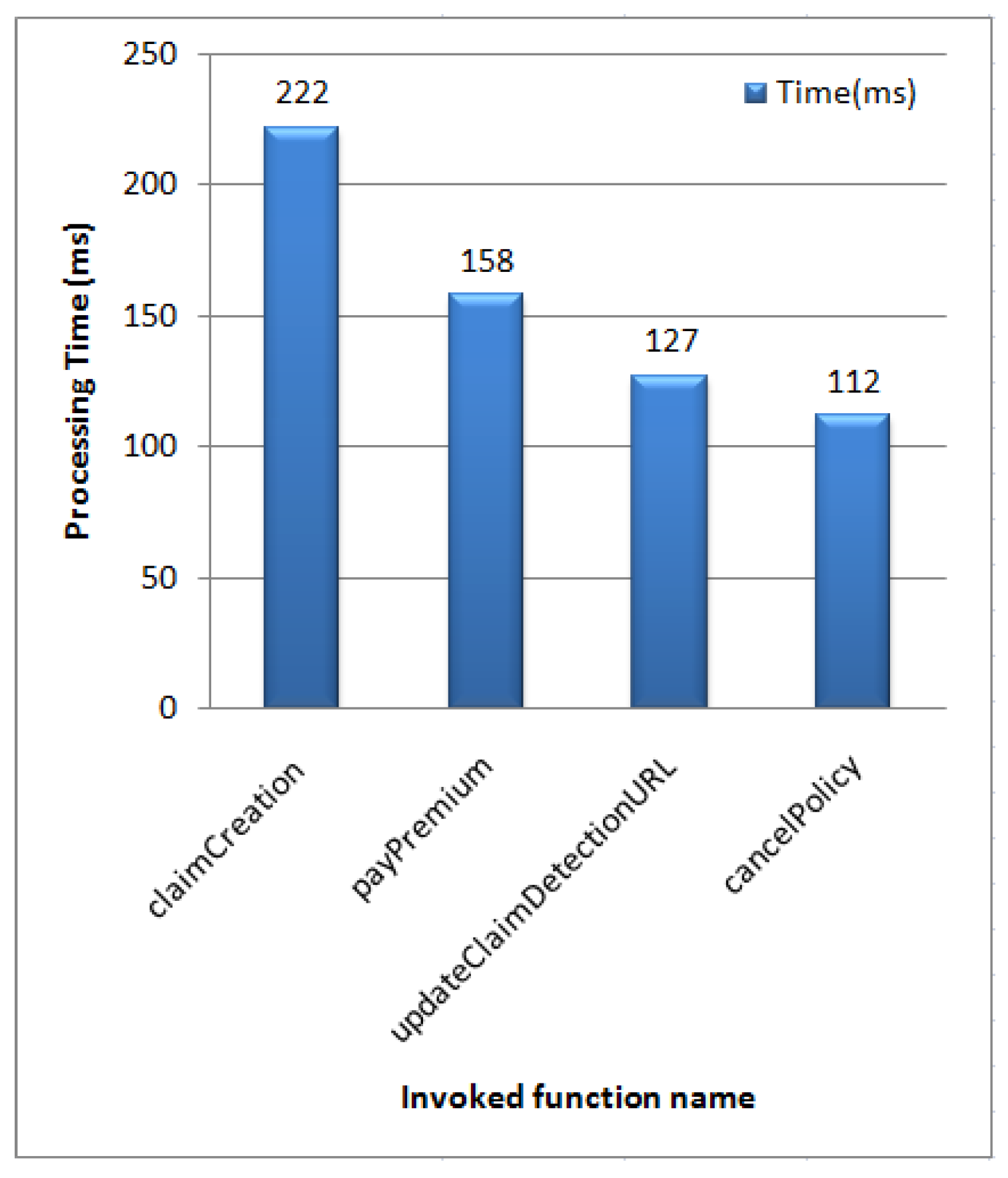

6.3.1. Computation Time Cost

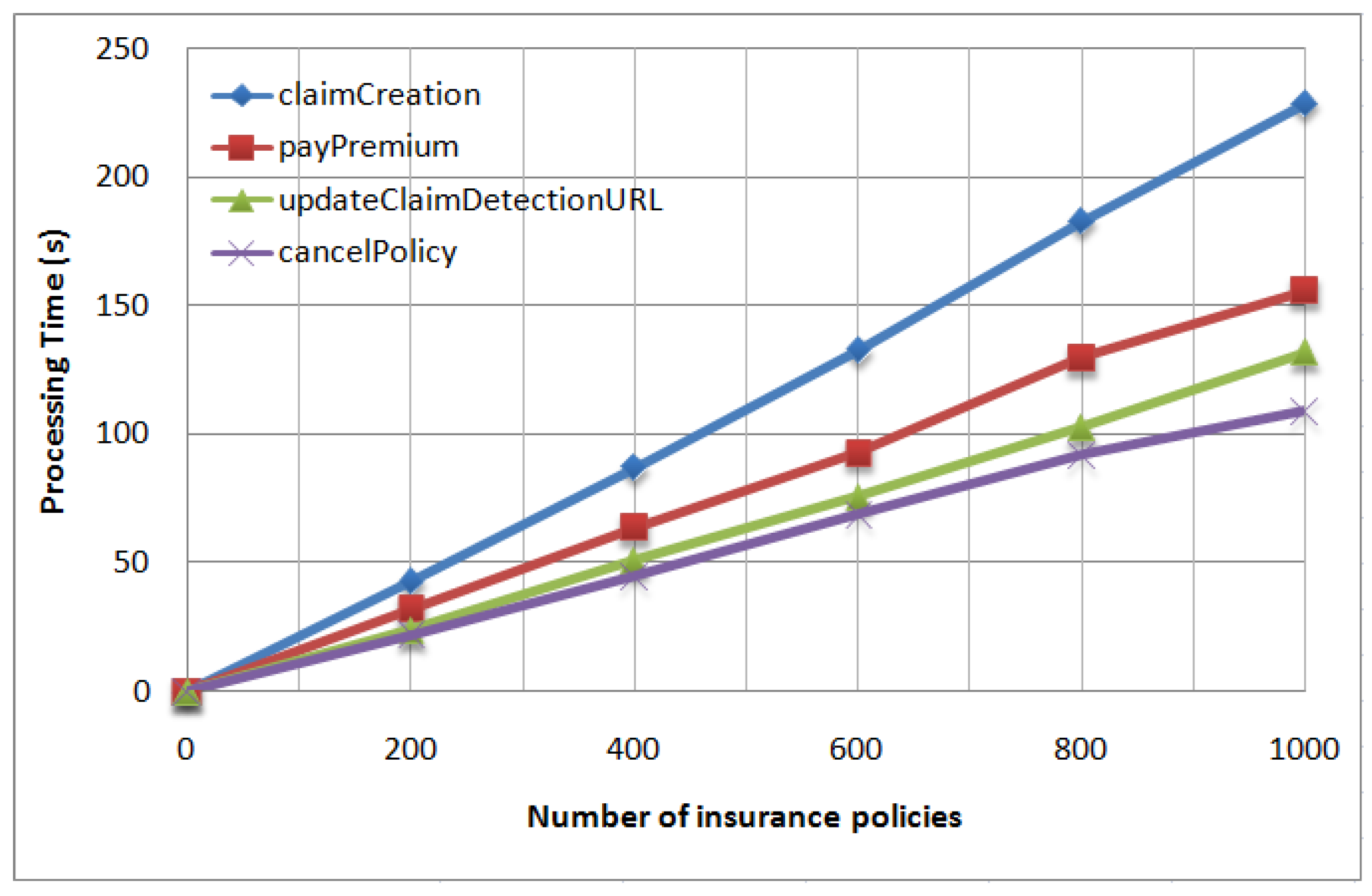

6.3.2. Scalability Overhead

6.3.3. Cost Overhead

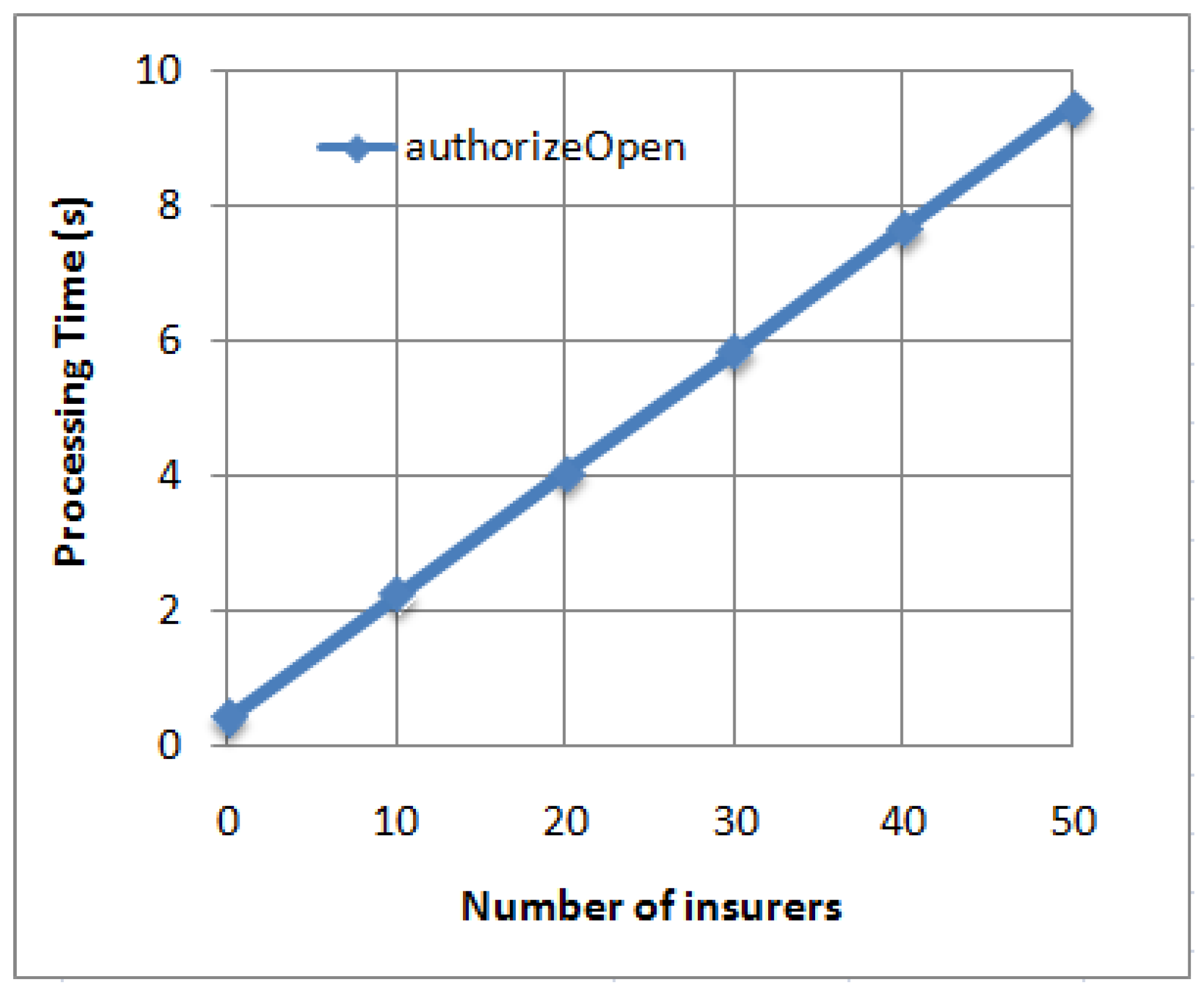

6.3.4. Computational Cost for Claim Authorization

6.4. Discussion

7. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Raikwar, M.; Mazumdar, S.; Ruj, S.; Gupta, S.S.; Chattopadhyay, A.; Lam, K.Y. A blockchain framework for insurance processes. In Proceedings of the 2018 9th IFIP International Conference on New Technologies, Mobility and Security (NTMS), Paris, France, 26–28 February 2018; IEEE: New York, NY, USA, 2018; pp. 1–4. [Google Scholar]

- Gatteschi, V.; Lamberti, F.; Demartini, C.; Pranteda, C.; Santamaría, V. Blockchain and smart contracts for insurance: Is the technology mature enough? Future Internet 2018, 10, 20. [Google Scholar] [CrossRef] [Green Version]

- Lamberti, F.; Gatteschi, V.; Demartini, C.; Pelissier, M.; Gomez, A.; Santamaria, V. Blockchains can work for car insurance: Using smart contracts and sensors to provide on-demand coverage. IEEE Consum. Electron. Mag. 2018, 7, 72–81. [Google Scholar] [CrossRef]

- Vo, H.T.; Mehedy, L.; Mohania, M.; Abebe, E. Blockchain-based data management and analytics for micro-insurance applications. In Proceedings of the 2017 ACM on Conference on Information and Knowledge Management, Singapore, 6–10 November 2017; pp. 2539–2542. [Google Scholar]

- Asquarepartners. Collaborative Insurance: Takeoff Impending? 2019. Available online: https://www.asquarepartners.com/collaborative-insurance-takeoff-impending/ (accessed on 1 April 2021).

- InsurTech. Guevara, ’People to People’ insurance. A Fairer and More Transparent Insurer. 2014. Available online: https://insur-tech.com/Startup/guevara/ (accessed on 1 April 2021).

- Fallucchi, F.; Gerardi, M.; Petito, M.; De Luca, E.W. Blockchain Framework in Digital Government for the Certification of Authenticity, Timestamping and Data Property. In Proceedings of the 54th Hawaii International Conference on System Sciences, Maui, HI, USA, 5–8 January 2021; pp. 2307–2316. [Google Scholar]

- Valls. Valls City Council Open Data Portal. 2019. Available online: https://dadesobertes.valls.cat/en/about (accessed on 15 May 2021).

- Homeland Security. DHS S&T Announces New Collaborative Blockchain Innovation Solution. 2018. Available online: https://www.dhs.gov/science-and-technology/news/2018/12/04/news-release-st-seeks-collaborative-blockchain-innovations (accessed on 15 May 2021).

- Bertini, T.; Butkute, K.; Canessa, F. Smart Flight Insurance—InsurETH. 2015. Available online: http://mkvd.s3.amazonaws.com/apps/InsurEth.pdf (accessed on 1 April 2021).

- Replay. Insure Chain—Blockchain Insurance Management. 2017. Available online: https://www.reply.com/en/content/insurechain (accessed on 1 April 2021).

- Kunde, T.; Herfurth, S.; Meyer-Plath, J. Friendsurance: The P2P Insurance Concept. 2017. Available online: https://www.friendsurance.com/ (accessed on 1 April 2021).

- Joshua, D. Peer to Peer Insurance on an Ethereum Blockchain. 2018. Available online: http://www.dynamisapp.com/whitepaper.pdf (accessed on 1 April 2021).

- Lepoint, T.; Ciocarlie, G.; Eldefrawy, K. BlockCIS—A blockchain-Based Cyber Insurance System. In Proceedings of the IEEE International Conference on Cloud Engineering (IC2E), Orlando, FL, USA, 17–20 April 2018; IEEE: New York, NY, USA, 2018; pp. 378–384. [Google Scholar]

- Aleksieva, V.; Valchanov, H.; Huliyan, A. Implementation of Smart Contracts based on Hyperledger Fabric Blockchain for the Purpose of Insurance Services. In Proceedings of the International Conference on Biomedical Innovations and Applications (BIA), Varna, Bulgaria, 24–27 September 2020; IEEE: New York, NY, USA, 2020; pp. 113–116. [Google Scholar]

- Suciu, G.; Nădrag, C.; Istrate, C.; Vulpe, A.; Ditu, M.-C.; Subea, O. Comparative analysis of distributed ledger technologies. In Proceedings of the 2018 Global Wireless Summit (GWS), Chiang Rai, Thailand, 25–28 November 2018; IEEE: New York, NY, USA, 2018; pp. 370–373. [Google Scholar]

- Buterin, V. Ethereum White Paper: A Next-Generation Smart Contract and Decentralized Application Platform. 2014. Available online: https://blockchainlab.com/pdf/Ethereum_white_paper-a_next_generation_smart_contract_and_decentralized_application_platform-vitalik-buterin.pdf (accessed on 1 June 2021).

- Jiang, S.; Cao, J.; Wu, H.; Yang, Y.; Ma, M.; He, J. Blochie: A blockchain-based platform for healthcare information exchange. In Proceedings of the 2018 IEEE International Conference on Smart Computing (Smartcomp), Taormina, Italy, 18–20 June 2018; IEEE: New York, NY, USA, 2018; pp. 49–56. [Google Scholar]

- Jiang, S.; Cao, J.; Wu, H.; Yang, Y. Fairness-based Packing of Industrial IoT Data in Permissioned Blockchains. IEEE Trans. Ind. Inform. 2020, 1–11. [Google Scholar] [CrossRef]

- Wu, H.; Cao, J.; Yang, Y.; Tung, C.L.; Jiang, S.; Tang, B.; Liu, Y.; Wang, X.; Deng, Y. Data management in supply chain using blockchain: Challenges and a case study. In Proceedings of the 28th International Conference on Computer Communication and Networks (ICCCN), Valencia, Spain, 29 July–1 August 2019; IEEE: New York, NY, USA, 2019; pp. 1–8. [Google Scholar]

- Khan, S.N.; Loukil, F.; Ghedira-Guegan, C.; Benkhelifa, E.; Bani-Hani, A. Blockchain smart contracts: Applications, challenges, and future trends. In Peer-to-Peer Networking and Applications; Springer: Berlin/Heidelberg, Germany, 2021; pp. 1–25. [Google Scholar]

- Ethereum Team. Ethereum API—ProvableAPI 0.5 Smart Contract. 2019. Available online: https://github.com/provable-things/ethereum-api/blob/master/provableAPI_0.5.sol (accessed on 1 April 2021).

- Owyang, J.; Tran, C.; Silva, C. The Collaborative Economy; Altimeter: San Mateo, CA, USA, 2013. [Google Scholar]

- Solidity Team. Solidity Language. 2014. Available online: https://solidity.readthedocs.io/en/develop/ (accessed on 1 April 2021).

- Ganache Team. Ganache: Personal Blockchain for Ethereum Development. 2016. Available online: https://www.trufflesuite.com/ganache (accessed on 1 April 2021).

- Truffle Team. Truffle: Ethereum Development Framework. 2016. Available online: https://github.com/trufflesuite/truffle (accessed on 1 April 2021).

- Web3. Web3.js—Ethereum JavaScript API. 2017. Available online: https://github.com/ethereum/web3.js/ (accessed on 15 May 2021).

- Etherisc. Introduction to Risk Pool Tokens on the Etherisc Protocol. 2018. Available online: https://blog.etherisc.com/introduction-to-risk-pool-tokens-on-the-etherisc-protocol-1744de67a57e (accessed on 26 May 2021).

- Etherisc. Etherisc—Decentralized Insurance Protocol to Collectively Build Insurance Products. 2017. Available online: https://etherisc.com/ (accessed on 26 May 2021).

- Sassano, A. Creating a Symbiotic Relationship. 2020. Available online: https://thedailygwei.substack.com/p/creating-a-symbiotic-relationship (accessed on 15 May 2021).

- Buterin, V. Ethereum Improvement Proposal (EIP) 1559. 2021. Available online: https://github.com/ethereum/EIPs/blob/master/EIPS/eip-1559.md (accessed on 15 May 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

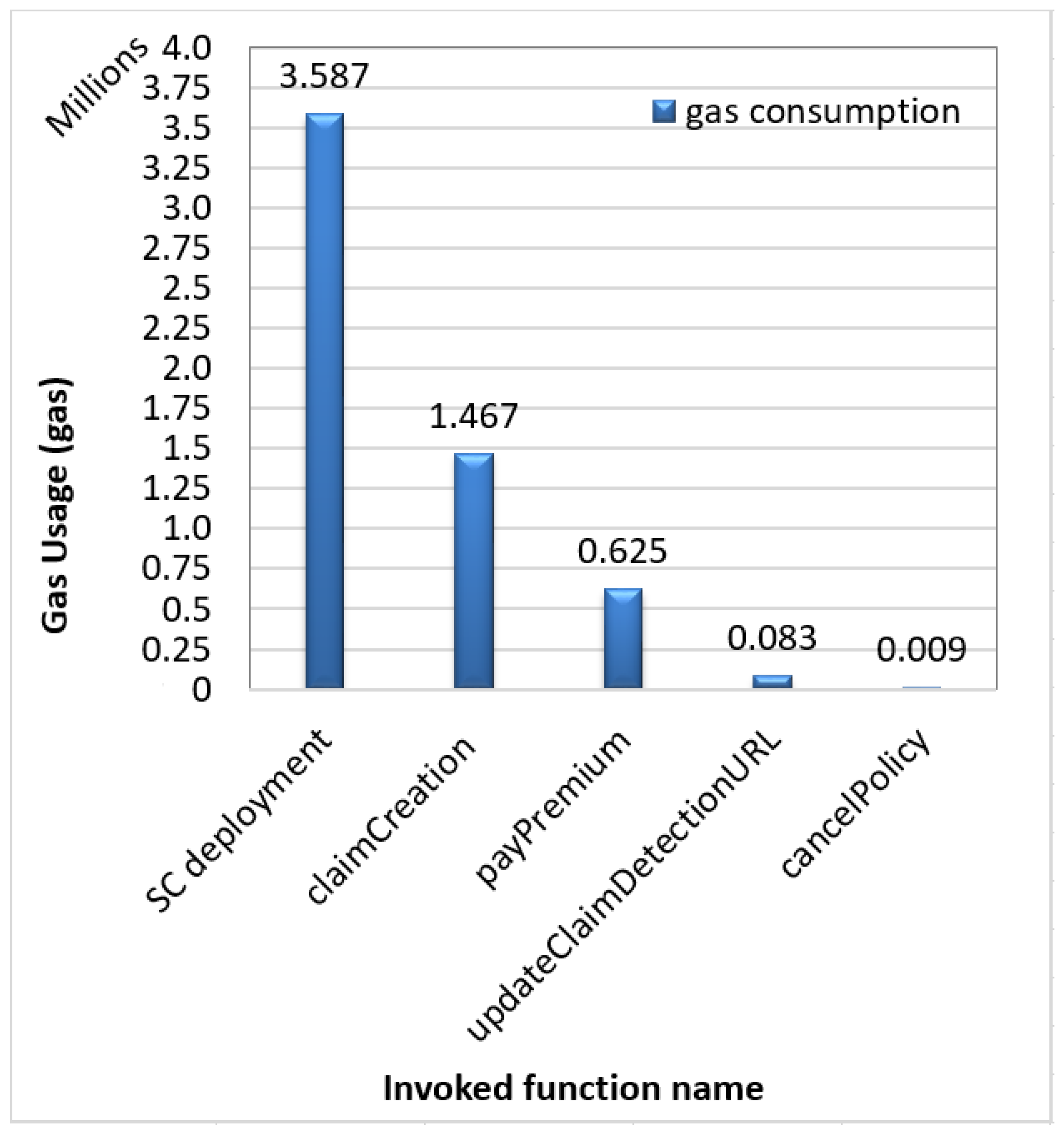

| Invoked Function | Average Gas Usage (Gas) | Average Gas Cost (USD) |

|---|---|---|

| SC Deployment | 3 586 838 | 158.61 |

| claimCreation | 1 467 150 | 64.88 |

| payPremium | 62 4547 | 27.62 |

| updateClaimDetectionURL | 82 882 | 3.66 |

| cancelPolicy | 9 409 | 0.42 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Loukil, F.; Boukadi, K.; Hussain, R.; Abed, M. CioSy: A Collaborative Blockchain-Based Insurance System. Electronics 2021, 10, 1343. https://doi.org/10.3390/electronics10111343

Loukil F, Boukadi K, Hussain R, Abed M. CioSy: A Collaborative Blockchain-Based Insurance System. Electronics. 2021; 10(11):1343. https://doi.org/10.3390/electronics10111343

Chicago/Turabian StyleLoukil, Faiza, Khouloud Boukadi, Rasheed Hussain, and Mourad Abed. 2021. "CioSy: A Collaborative Blockchain-Based Insurance System" Electronics 10, no. 11: 1343. https://doi.org/10.3390/electronics10111343

APA StyleLoukil, F., Boukadi, K., Hussain, R., & Abed, M. (2021). CioSy: A Collaborative Blockchain-Based Insurance System. Electronics, 10(11), 1343. https://doi.org/10.3390/electronics10111343