A Decade of Cryptocurrency Investment Literature: A Cluster-Based Systematic Analysis

Abstract

:1. Introduction

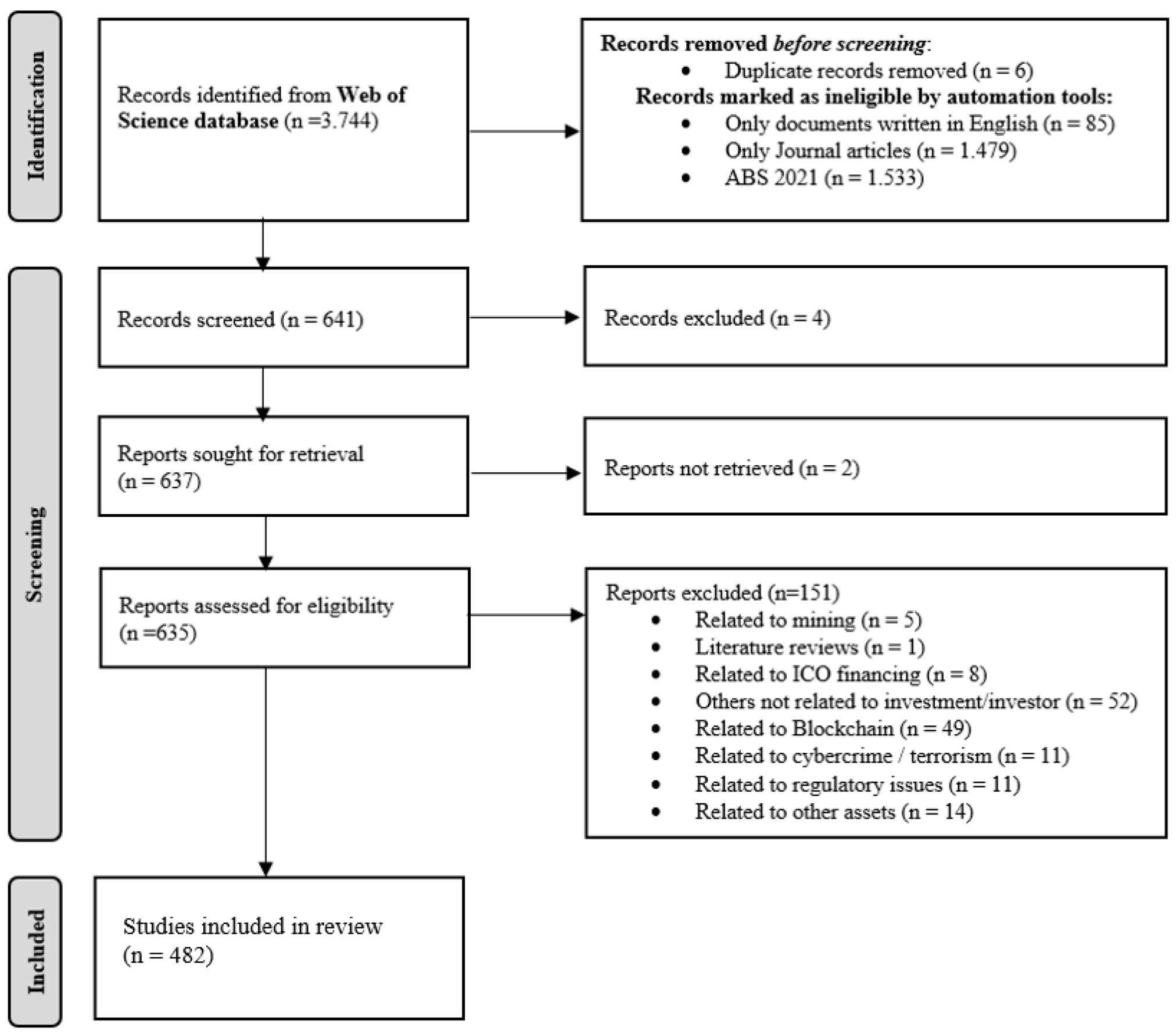

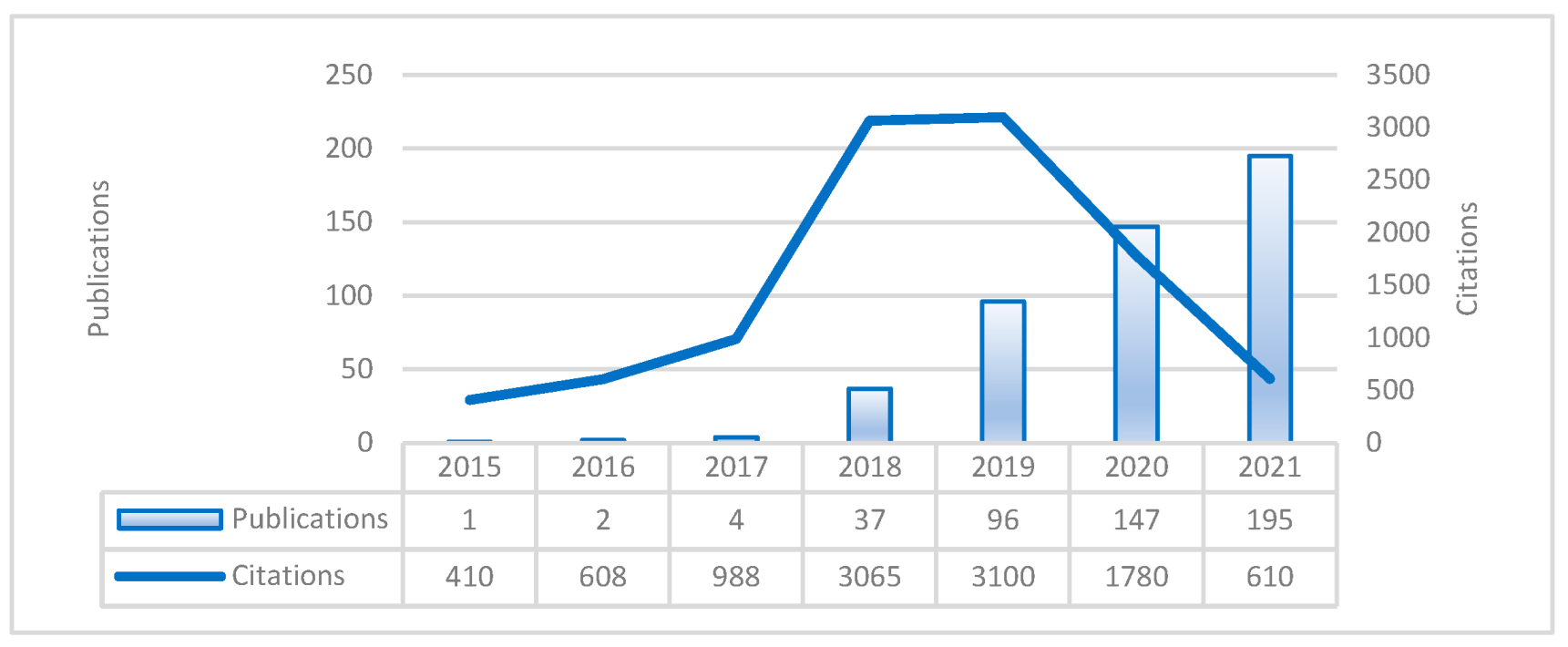

2. Data and Methodology

3. Results

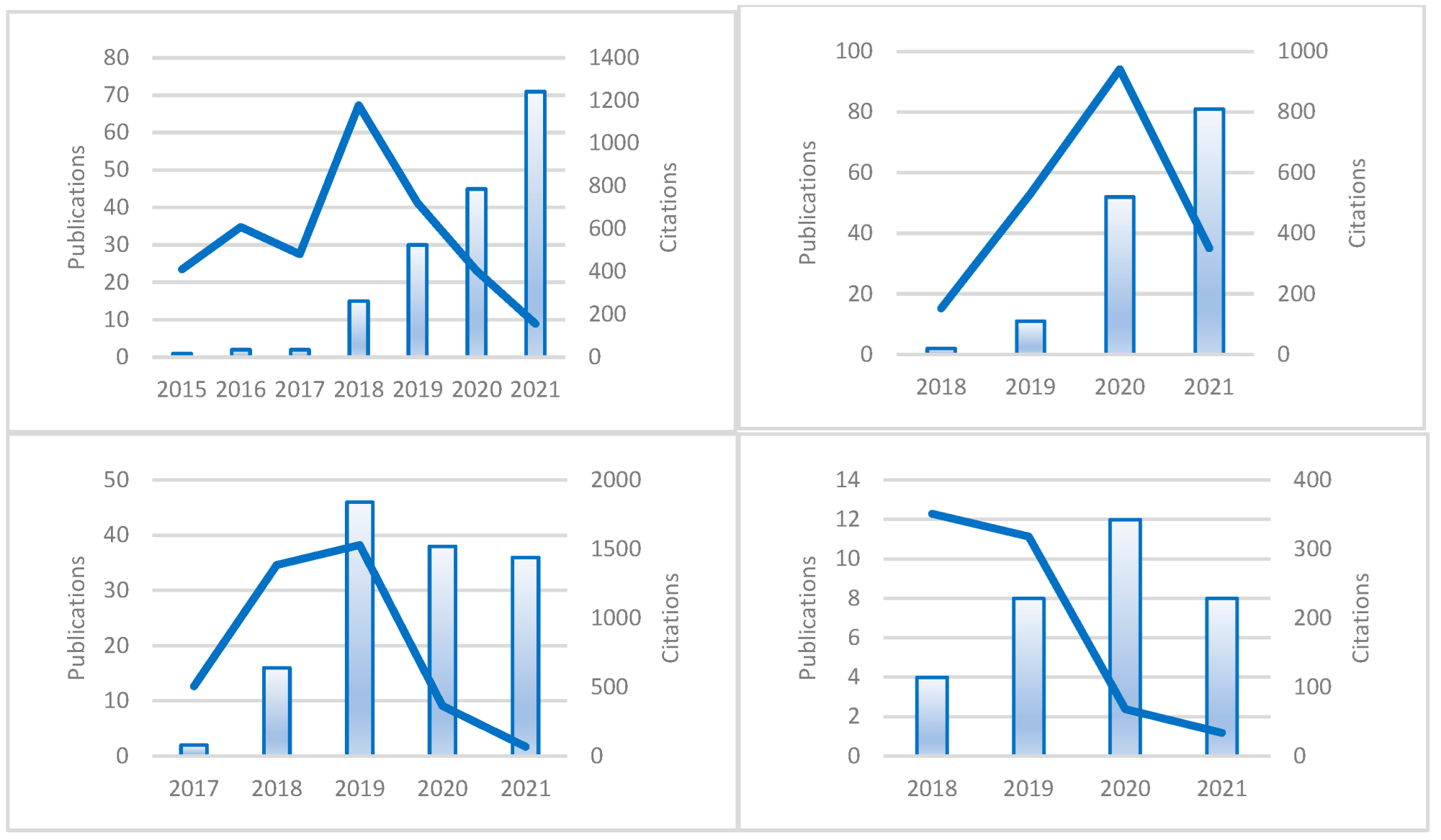

3.1. Cluster Network Analysis

3.2. Cluster’s Top Articles

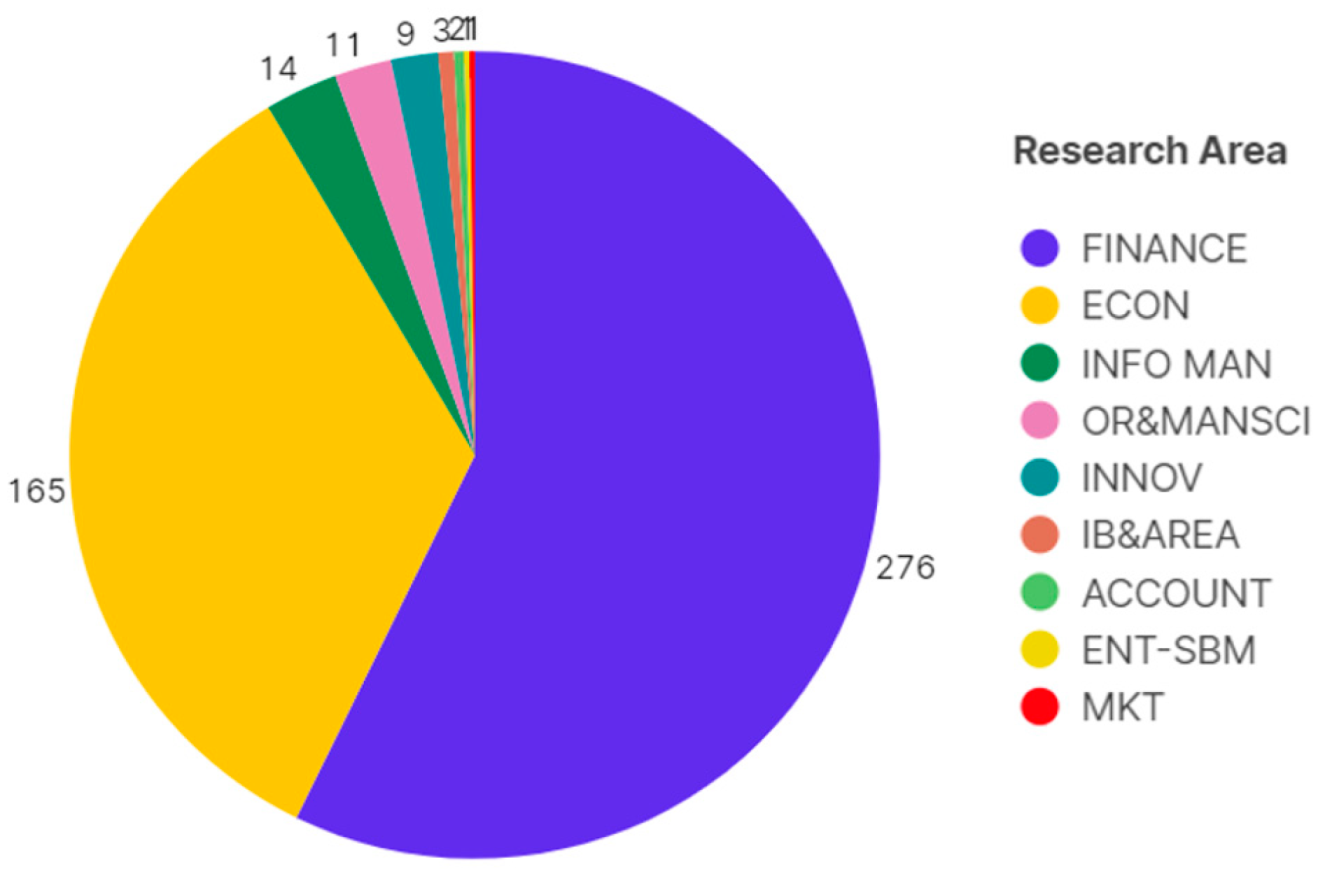

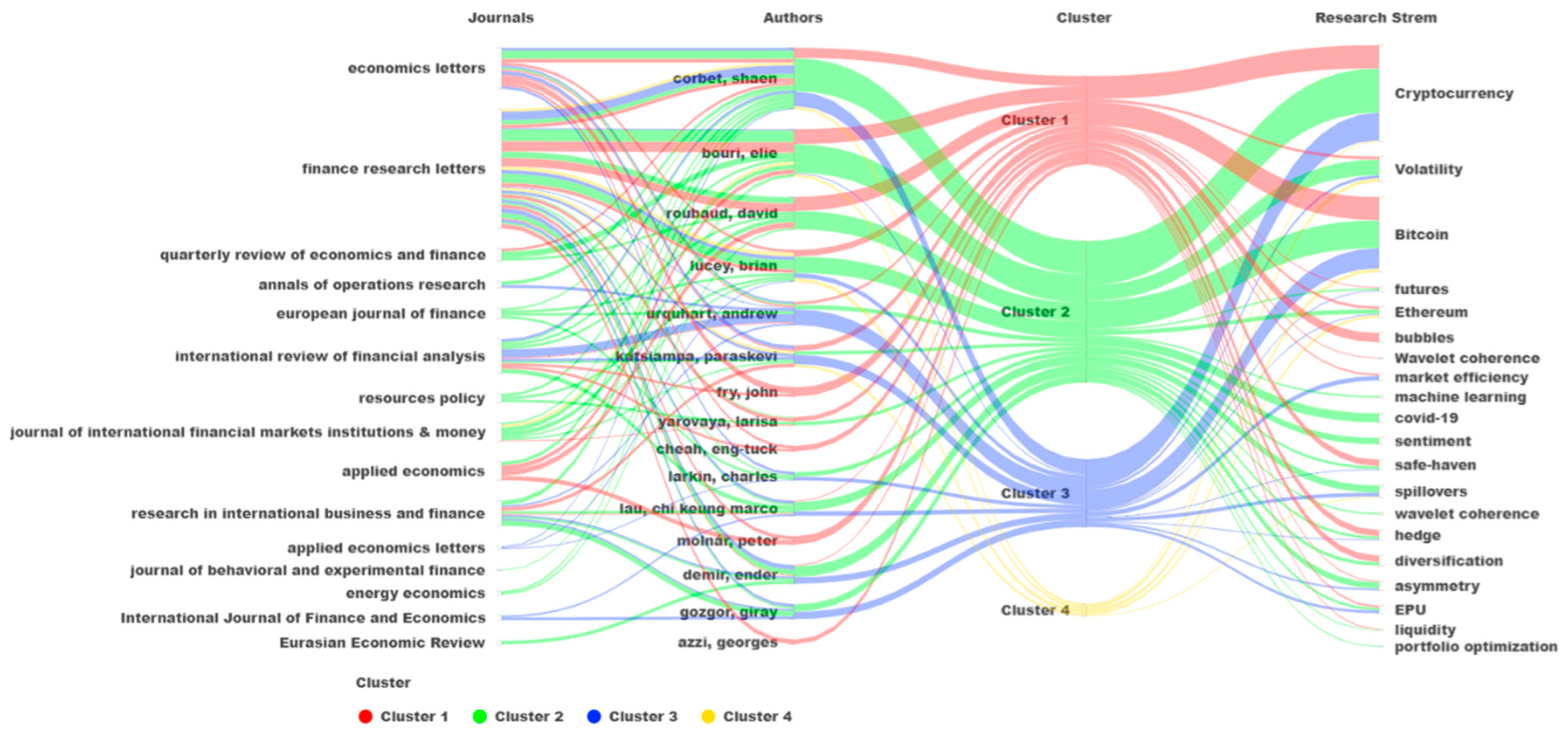

3.3. Journal Cluster Network Analysis

3.4. Country Cluster Network Analysis

3.5. Author Cluster Network Analysis

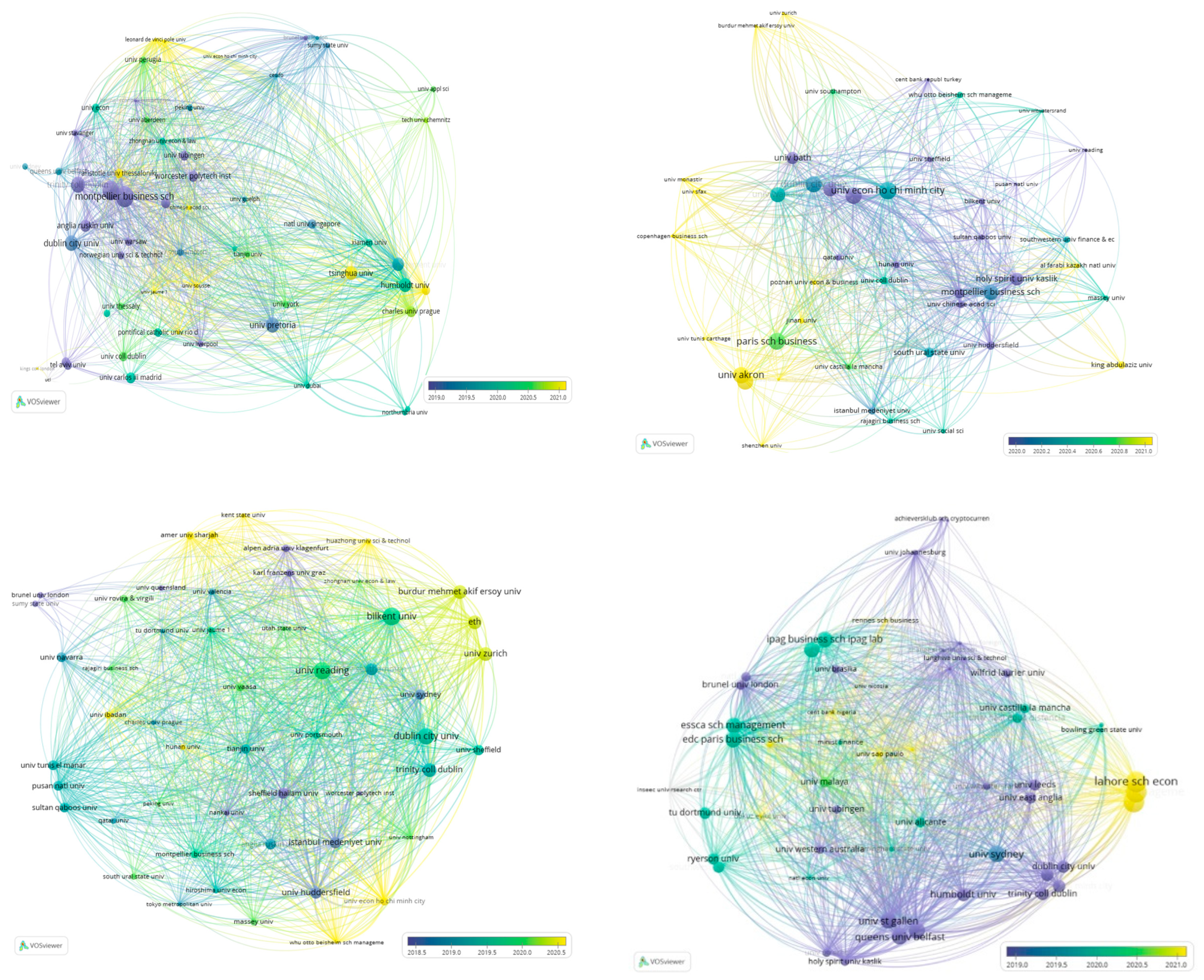

3.6. Institution Cluster Network Analysis

3.7. Identification of Trend Topics

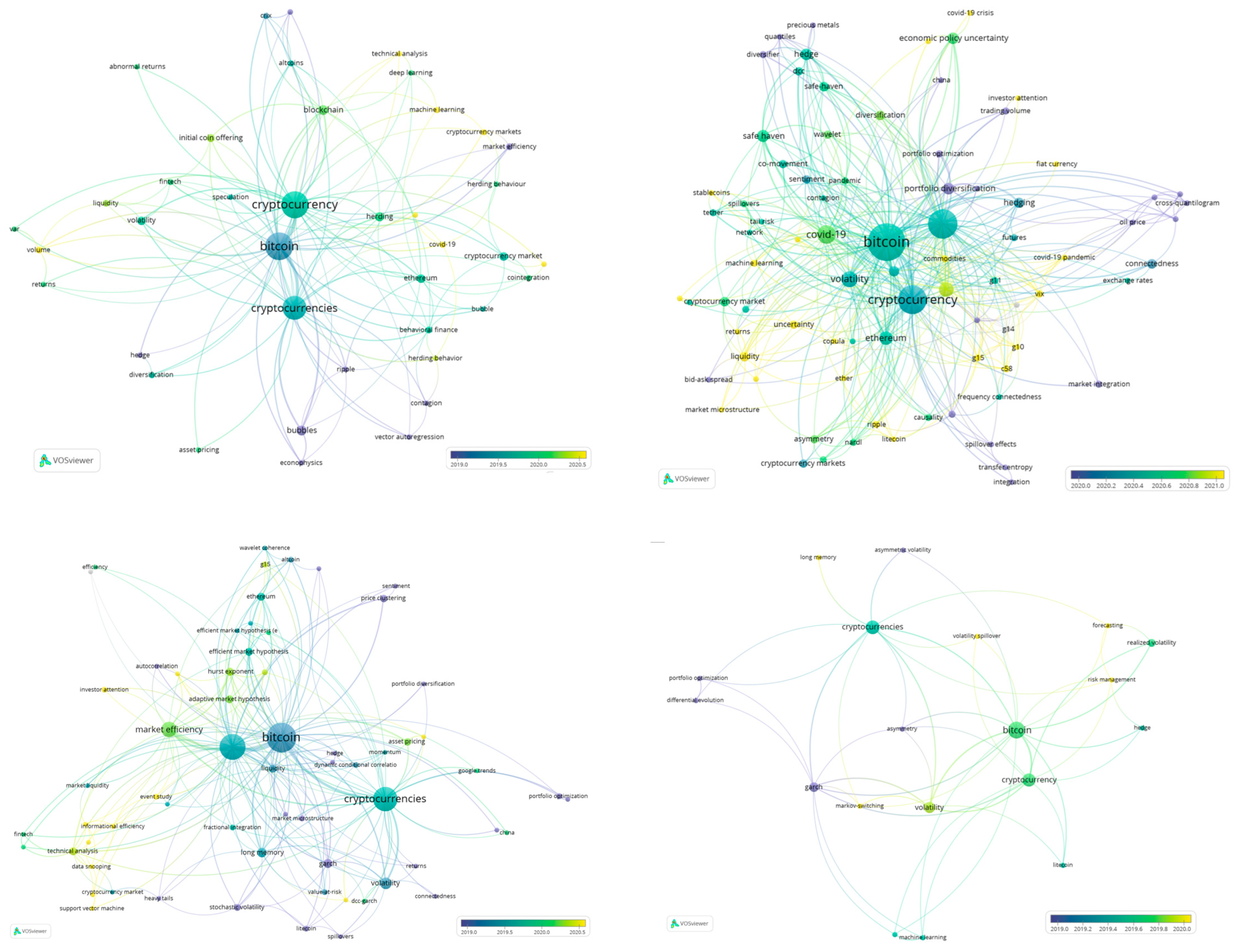

3.7.1. Cluster Keyword Co-Occurrence Analysis

3.7.2. Research Stream Analysis

3.8. Clusters’ Main Contributions to the Literature

3.8.1. Main Conclusions

3.8.2. Main Futures Lines of Research

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Dataset | Ct | Pb | Ct/Pb | Cluster 1 | Ct | Pb | Ct/Pb | Cluster 2 | Ct | Pb | Ct/Pb | Cluster 3 | Ct | Pb | Ct/Pb | Cluster 4 | Ct | Pb | Ct/Pb | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Journals | ||||||||||||||||||||

| 1 | Finance research letters | 3258 | 109 | 29.9 | Finance research letters | 1185 | 21 | 56.4 | Finance research letters | 716 | 34 | 21.1 | Economics letters | 1651 | 21 | 78.6 | International review of financial analysis | 192 | 1 | 192.0 |

| 2 | Economics letters | 2921 | 41 | 71.2 | Economics letters | 1125 | 12 | 93.8 | International review of financial analysis | 345 | 16 | 21.6 | Finance research letters | 1222 | 48 | 25.5 | Research in international business and finance | 145 | 4 | 36.3 |

| 3 | International review of financial analysis | 994 | 30 | 33.1 | Applied economics | 247 | 5 | 49.4 | Research in international business and finance | 178 | 17 | 10.5 | Research in international business and finance | 303 | 9 | 33.7 | Finance research letters | 135 | 6 | 22.5 |

| 4 | Research in international business and finance | 750 | 42 | 17.9 | International review of financial analysis | 205 | 6 | 34.2 | Energy economics | 100 | 2 | 50.0 | International review of financial analysis | 252 | 7 | 36.0 | Economics letters | 92 | 2 | 46.0 |

| 5 | Applied economics | 344 | 18 | 19.1 | Journal of monetary economics | 178 | 1 | 178.0 | Journal of international financial markets institutions & money | 93 | 6 | 15.5 | North American journal of economics and finance | 75 | 5 | 15.0 | Expert systems with applications | 76 | 2 | 38.0 |

| Countries | ||||||||||||||||||||

| 1 | England | 4218 | 101 | 41.8 | England | 1503 | 36 | 41.8 | Peoples R. China | 686 | 35 | 19.6 | England | 1920 | 35 | 54.9 | Germany | 318 | 4 | 79.5 |

| 2 | France | 1474 | 46 | 32.0 | France | 801 | 12 | 66.8 | England | 614 | 27 | 22.7 | Turkey | 554 | 14 | 39.6 | North Ireland | 226 | 2 | 113.0 |

| 3 | Ireland | 1361 | 32 | 42.5 | Lebanon | 754 | 6 | 125.7 | France | 567 | 23 | 24.7 | Ireland | 450 | 7 | 64.3 | Switzerland | 226 | 2 | 113.0 |

| 4 | Australia | 1271 | 35 | 36.3 | USA | 662 | 27 | 24.5 | Ireland | 505 | 16 | 32.6 | Australia | 448 | 11 | 40.7 | Australia | 190 | 6 | 31.7 |

| 5 | Lebanon | 1192 | 19 | 62.7 | Norway | 487 | 4 | 121.8 | Vietnam | 415 | 18 | 23.1 | Spain | 305 | 11 | 27.7 | England | 181 | 3 | 60.3 |

| Authors | ||||||||||||||||||||

| 1 | Corbet, Shaen | 1198 | 22 | 54.5 | Bouri, Elie | 747 | 5 | 149.4 | Bouri, Elie | 404 | 11 | 36.7 | Katsiampa, Paraskevi | 522 | 5 | 104.4 | Klein, Tony | 226 | 2 | 113.0 |

| 2 | Bouri, Elie | 1185 | 18 | 65.8 | Roubaud, David | 747 | 5 | 149.4 | Roubaud, David | 389 | 9 | 43.2 | Corbet, Shaen | 450 | 6 | 75.0 | Walther, Thomas | 226 | 2 | 112.0 |

| 3 | Roubaud, David | 1136 | 14 | 81.1 | Fry, John | 632 | 3 | 210.7 | Corbet, Shaen | 379 | 11 | 34.5 | Lucey, Brian | 420 | 4 | 105.0 | Hien Pham Thu | 192 | 1 | 192.0 |

| 4 | Lucey, Brian | 1121 | 13 | 86.2 | Cheah, Eng-Tuck | 572 | 2 | 286.0 | Lucey, Brian | 346 | 6 | 57.7 | Yarovaya, Larisa | 385 | 3 | 128.3 | Baur, Dirk G. | 81 | 2 | 40.5 |

| 5 | Urquhart, Andrew | 873 | 13 | 67.2 | Molnar, Peter | 481 | 2 | 240.5 | Lau, Chi Keung Marco | 206 | 6 | 34.3 | Urquhart, Andrew | 381 | 8 | 47.6 | Dimpfl, Thomas | 81 | 1 | 81.0 |

| Institutions | ||||||||||||||||||||

| 1 | Dublin City Univ. | 1198 | 22 | 54.5 | Montpellier Business School | 747 | 5 | 149.40 | Trinity College Dublin | 386 | 9 | 42.89 | Sheffield Hallam Univ. | 507 | 4 | 126.75 | Queens Univ. Belfast | 226 | 2 | 113.00 |

| 2 | Trinity College Dublin | 1188 | 18 | 66.0 | Univ. Sheffield | 454 | 3 | 151.33 | Dublin City Univ. | 379 | 11 | 34.45 | Dublin City Univ. | 450 | 6 | 75.00 | Technical Univ.of Dresden | 226 | 2 | 113.00 |

| 3 | Montpellier Business School | 1166 | 20 | 58.3 | Univ. Southampton | 446 | 3 | 148.67 | Montpellier Business School | 372 | 12 | 31.00 | Trinity College Dublin | 420 | 4 | 105.00 | Univ. St Gallen | 226 | 2 | 113.00 |

| 4 | Holy Spirit Univ. | 774 | 13 | 59.4 | Holy Spirit Univ. | 377 | 4 | 94.25 | Holy Spirit Univ. | 363 | 8 | 45.38 | Anglia Ruskin Univ | 368 | 2 | 184.00 | Humboldt Univ. | 192 | 1 | 192.00 |

| 5 | Univ. Southampton | 737 | 13 | 56.7 | Norwegian Univ. Science Technology | 370 | 2 | 185.00 | Univ. Economics Ho Chi Minh City | 361 | 15 | 24.07 | Univ. Huddersfield | 323 | 5 | 64.60 | Univ. Sydney | 108 | 3 | 36.00 |

References

- Almeida, José. 2021. Cryptocurrencies and financial markets–extant literature and future venues. European Journal of Economics, Finance and Administrative Sciences 109: 29–40. [Google Scholar]

- Almeida, José, and Tiago Cruz Gonçalves. 2022. A Systematic Literature Review of Volatility and Risk Management on Cryptocurrency Investment: A Methodological Point of View. Risks 10: 107. [Google Scholar] [CrossRef]

- Almeida, José, and Tiago Cruz Gonçalves. 2023a. A systematic literature review of investor behavior in the cryptocurrency markets. Journal of Behavioral and Experimental Finance 37: 100785. [Google Scholar] [CrossRef]

- Almeida, José, and Tiago Cruz Gonçalves. 2023b. Portfolio Diversification, Hedge and Safe-Haven Properties in Cryptocurrency Investments and Financial Economics: A Systematic Literature Review. Journal of Risk and Financial Management 16: 3. [Google Scholar] [CrossRef]

- Alon, Ilan, John Anderson, Ziaul Haque Munim, and Alice Ho. 2018. A Review of the Internationalization of Chinese Enterprises. Asia Pacific Journal of Management 35: 573–605. [Google Scholar] [CrossRef]

- Alonso, Sergio Luis Náñez, Miguel Ángel Echarte Fernández, David Sanz Bas, and Jarosław Kaczmarek. 2020. Reasons fostering or discouraging the implementation of central bank-backed digital currency: A review. Economies 8: 41. [Google Scholar] [CrossRef]

- Alsmadi, Ayman Abdalmajeed, Najed Alrawashdeh, Ala’a Fouad Al-Dweik, and Mohammed Al-Assaf. 2022. Cryptocurrencies: A bibliometric analysis. International Journal of Data and Network Science 6: 619–28. [Google Scholar] [CrossRef]

- Angerer, Martin, Christian Hugo Hoffmann, Florian Neitzert, and Sascha Kraus. 2020. Objective and subjective risks of investing into cryptocurrencies. Finance Research Letters 40: 101737. [Google Scholar] [CrossRef]

- Aras, Serkan. 2021. Stacking hybrid GARCH models for forecasting Bitcoin volatility. Expert Systems with Applications 174: 114747. [Google Scholar] [CrossRef]

- Aysan, Ahmet Faruk, Hüseyin Bedir Demirtaş, and Mustafa Saraç. 2021. The Ascent of Bitcoin: Bibliometric Analysis of Bitcoin Research. Journal of Risk and Financial Management 14: 427. [Google Scholar] [CrossRef]

- Ballis, Antonis, and Thanos Verousis. 2022. Behavioural finance and cryptocurrencies. Review of Behavioral Finance 14: 545–62. [Google Scholar] [CrossRef]

- Bariviera, Aurelio F., and Ignasi Merediz-Solà. 2021. Where Do We Stand in Cryptocurrencies Economic Research? A Survey Based on Hybrid Analysis. Journal of Economic Surveys 35: 377–407. [Google Scholar] [CrossRef]

- Bartolacci, Francesca, Andrea Caputo, and Michela Soverchia. 2020. Sustainability and financial performance of small and medium sized enterprises: A bibliometric and systematic literature review. Business Strategy and the Environment 29: 1297–309. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Thomas Dimpfl. 2018. Asymmetric volatility in cryptocurrencies. Economics Letters 173: 148–51. [Google Scholar] [CrossRef]

- Baur, Dirk G., Thomas Dimpfl, and Konstantin Kuck. 2018. Bitcoin, gold and the US dollar—A replication and extension. Finance Research Letters 25: 103–10. [Google Scholar] [CrossRef]

- Białkowski, Jędrzej. 2020. Cryptocurrencies in institutional investors’ portfolios: Evidence from industry stop-loss rules. Economics Letters 191: 108834. [Google Scholar] [CrossRef]

- Blau, Benjamin M. 2017. Price dynamics and speculative trading in bitcoin. Research in International Business and Finance 41: 493–99. [Google Scholar] [CrossRef]

- Bouri, Elie, Chi Keung Marco Lau, Brian Lucey, and David Roubaud. 2019a. Trading volume and the predictability of return and volatility in the cryptocurrency market. Finance Research Letters 29: 340–46. [Google Scholar] [CrossRef] [Green Version]

- Bouri, Elie, David Gabauer, Rangan Gupta, and Aviral Kumar Tiwari. 2021. Volatility connectedness of major cryptocurrencies: The role of investor happiness. Journal of Behavioral and Experimental Finance 30: 100463. [Google Scholar] [CrossRef]

- Bouri, Elie, Naji Jalkh, Peter Molnár, and David Roubaud. 2017a. Bitcoin for energy commodities before and after the December 2013 crash: Diversifier, hedge or safe haven? Applied Economics 49: 5063–73. [Google Scholar] [CrossRef]

- Bouri, Elie, Peter Molnár, Georges Azzi, David Roubaud, and Lars Ivar Hagfors. 2017b. On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Finance Research Letters 20: 192–98. [Google Scholar] [CrossRef]

- Bouri, Elie, Rangan Gupta, and David Roubaud. 2019b. Herding behaviour in cryptocurrencies. Finance Research Letters 29: 216–21. [Google Scholar] [CrossRef]

- Bouri, Elie, Syed Jawad Hussain Shahzad, and David Roubaud. 2019c. Co-explosivity in the cryptocurrency market. Finance Research Letters 29: 178–83. [Google Scholar] [CrossRef]

- Brauneis, Alexander, and Roland Mestel. 2018. Price discovery of cryptocurrencies: Bitcoin and beyond. Economics Letters 165: 58–61. [Google Scholar] [CrossRef]

- Briola, Antonio, David Vidal-Tomás, Yuanrong Wang, and Tomaso Aste. 2023. Anatomy of a Stablecoin’s failure: The Terra-Luna case. Finance Research Letters 51: 103358. [Google Scholar] [CrossRef]

- Caporale, Guglielmo Maria, and Timur Zekokh. 2019. Modelling volatility of cryptocurrencies using Markov-Switching GARCH models. Research in International Business and Finance 48: 143–55. [Google Scholar] [CrossRef]

- Caputo, Andrea, Giacomo Marzi, Jane Maley, and Mario Silic. 2019. Ten years of conflict management research 2007–2017: An update on themes, concepts and relationships. International Journal of Conflict Management 30: 87–110. [Google Scholar] [CrossRef]

- Chan, Wing Hong, Minh Le, and Yan Wendy Wu. 2019. Holding Bitcoin longer: The dynamic hedging abilities of Bitcoin. Quarterly Review of Economics and Finance 71: 107–13. [Google Scholar] [CrossRef]

- Charfeddine, Lanouar, and Youcef Maouchi. 2019. Are shocks on the returns and volatility of cryptocurrencies really persistent? Finance Research Letters 28: 423–30. [Google Scholar] [CrossRef]

- Cheah, Eng Tuck, and John Fry. 2015. Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental value of Bitcoin. Economics Letters 130: 32–36. [Google Scholar] [CrossRef] [Green Version]

- Colon, Francisco, Chaehyun Kim, Hana Kim, and Wonjoon Kim. 2020. Are cryptocurrencies a safe haven for equity markets? An international perspective from the COVID-19 pandemic. Research in International Business and Finance 54: 101248. [Google Scholar] [CrossRef] [PubMed]

- Colon, Francisco, Chaehyun Kim, Hana Kim, and Wonjoon Kim. 2021. The effect of political and economic uncertainty on the cryptocurrency market. Finance Research Letters 39: 101621. [Google Scholar] [CrossRef]

- Corbet, Shaen, Andrew Meegan, Charles Larkin, Brian Lucey, and Larisa Yarovaya. 2018a. Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters 165: 28–34. [Google Scholar] [CrossRef] [Green Version]

- Corbet, Shaen, Brian Lucey, and Larisa Yarovaya. 2018b. Datestamping the Bitcoin and Ethereum bubbles. Finance Research Letters 26: 81–88. [Google Scholar] [CrossRef] [Green Version]

- Corbet, Shaen, Brian Lucey, Andrew Urquhart, and Larisa Yarovaya. 2019. Cryptocurrencies as a financial asset: A systematic analysis. International Review of Financial Analysis 62: 182–99. [Google Scholar] [CrossRef] [Green Version]

- Corbet, Shaen, Charles Larkin, and Brian Lucey. 2020. The contagion effects of the COVID-19 pandemic: Evidence from gold and cryptocurrencies. Finance Research Letters 35: 101554. [Google Scholar] [CrossRef]

- Demir, Ender, Giray Gozgor, Chi Keung Marco Lau, and Samuel A. Vigne. 2018. Does economic policy uncertainty predict the Bitcoin returns? An empirical investigation. Finance Research Letters 26: 145–49. [Google Scholar] [CrossRef] [Green Version]

- Ding, Ying, Ronald Rousseau, and Dietmar Wolfram. 2014. Measuring Scholarly Impact. Berlin/Heidelberg: Springer. [Google Scholar] [CrossRef]

- Fang, Fan, Waichung Chung, Carmine Ventre, Michail Basios, Leslie Kanthan, Lingbo Li, and Fan Wu. 2021. Ascertaining price formation in cryptocurrency markets with machine learning. European Journal of Finance, 1–23. [Google Scholar] [CrossRef]

- Flori, Andrea. 2019. News and subjective beliefs: A Bayesian approach to Bitcoin investments. Research in International Business and Finance 50: 336–56. [Google Scholar] [CrossRef]

- Fry, John, and Eng Tuck Cheah. 2016. Negative bubbles and shocks in cryptocurrency markets. International Review of Financial Analysis 47: 343–52. [Google Scholar] [CrossRef] [Green Version]

- Galvao, A., C. Mascarenhas, C. Marques, J. Ferreira, and V. Ratten. 2019. Triple helix and its evolution: A systematic literature review. Journal of Science and Technology Policy Management 10: 812–33. [Google Scholar] [CrossRef]

- Galvao, Anderson, Carla Mascarenhas, Carla Marques, João Ferreira, and Vanessa Ratten. 2018. Price manipulation in the Bitcoin ecosystem. Journal of Monetary Economics 95: 86–96. [Google Scholar] [CrossRef]

- García-Corral, Francisco Javier, José Antonio Cordero-García, Jaime de Pablo-Valenciano, and Juan Uribe-Toril. 2022. A bibliometric review of cryptocurrencies: How have they grown? Financial Innovation 8: 1–31. [Google Scholar] [CrossRef] [PubMed]

- Gemayel, Roland, and Alex Preda. 2021. Performance and learning in an ambiguous environment: A study of cryptocurrency traders. International Review of Financial Analysis 77: 101847. [Google Scholar] [CrossRef]

- Gkillas, Konstantinos, and Paraskevi Katsiampa. 2018. An application of extreme value theory to cryptocurrencies. Economics Letters 164: 109–11. [Google Scholar] [CrossRef] [Green Version]

- Goodell, John W., and Stephane Goutte. 2021. Co-movement of COVID-19 and Bitcoin: Evidence from wavelet coherence analysis. Finance Research Letters 38: 101625. [Google Scholar] [CrossRef]

- Gupta, Swati, Sanjay Gupta, Manoj Mathew, and Hanumantha Rao Sama. 2020. Prioritizing intentions behind investment in cryptocurrency: A fuzzy analytical framework. Journal of Economic Studies 48: 1442–59. [Google Scholar] [CrossRef]

- Hairudin, Aiman, Imtiaz Mohammad Sifat, Azhar Mohamad, and Yusniliyana Yusof. 2020. Cryptocurrencies: A survey on acceptance, governance and market dynamics. International Journal of Finance and Economics 27: 4633–59. [Google Scholar] [CrossRef]

- Haq, Inzamam Ul, Apichit Maneengam, Supat Chupradit, Wanich Suksatan, and Chunhui Huo. 2021. Economic policy uncertainty and cryptocurrency market as a risk management avenue: A systematic review. Risks 9: 163. [Google Scholar] [CrossRef]

- Hattori, Takahiro. 2020. A forecast comparison of volatility models using realized volatility: Evidence from the Bitcoin market. Applied Economics Letters 27: 591–95. [Google Scholar] [CrossRef]

- Hsu, Shu Han, Chwen Sheu, and Jiho Yoon. 2021. Risk spillovers between cryptocurrencies and traditional currencies and gold under different global economic conditions. North American Journal of Economics and Finance 57: 101443. [Google Scholar] [CrossRef]

- Huynh, Toan Luu Duc, Erik Hille, and Muhammad Ali Nasir. 2020. Diversification in the age of the 4th industrial revolution: The role of artificial intelligence, green bonds and cryptocurrencies. Technological Forecasting and Social Change 159: 120188. [Google Scholar] [CrossRef]

- Huynh, Toan Luu Duc. 2021. Does Bitcoin React to Trump’s Tweets? Journal of Behavioral and Experimental Finance 31: 100546. [Google Scholar] [CrossRef]

- Jalal, Raja Nabeel Ud Din, Ilan Alon, and Andrea Paltrinieri. 2021. A bibliometric review of cryptocurrencies as a financial asset. Technology Analysis and Strategic Management, 1–16. [Google Scholar] [CrossRef]

- Ji, Qiang, Elie Bouri, Chi Keung Marco Lau, and David Roubaud. 2019a. Dynamic connectedness and integration in cryptocurrency markets. International Review of Financial Analysis 63: 257–72. [Google Scholar] [CrossRef]

- Ji, Qiang, Elie Bouri, David Roubaud, and Ladislav Kristoufek. 2019b. Information interdependence among energy, cryptocurrency and major commodity markets. Energy Economics 81: 1042–55. [Google Scholar] [CrossRef]

- Jiang, Shangrong, Xuerong Li, and Shouyang Wang. 2021. Exploring evolution trends in cryptocurrency study: From underlying technology to economic applications. Finance Research Letters 38: 101532. [Google Scholar] [CrossRef]

- Kaiser, Lars, and Sebastian Stöckl. 2020. Cryptocurrencies: Herding and the transfer currency. Finance Research Letters 33. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi. 2017. Volatility estimation for Bitcoin: A comparison of GARCH models. Economics Letters 158: 3–6. [Google Scholar] [CrossRef] [Green Version]

- Katsiampa, Paraskevi, Shaen Corbet, and Brian Lucey. 2019a. High frequency volatility co-movements in cryptocurrency markets. Journal of International Financial Markets, Institutions and Money 62: 35–52. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi, Shaen Corbet, and Brian Lucey. 2019b. Volatility spillover effects in leading cryptocurrencies: A BEKK-MGARCH analysis. Finance Research Letters 29: 68–74. [Google Scholar] [CrossRef] [Green Version]

- Klein, Tony, Hien Pham Thu, and Thomas Walther. 2018. Bitcoin is not the New Gold—A comparison of volatility, correlation, and portfolio performance. International Review of Financial Analysis 59: 105–16. [Google Scholar] [CrossRef]

- Koutmos, Dimitrios. 2018. Liquidity uncertainty and Bitcoin’s market microstructure. Economics Letters 172: 97–101. [Google Scholar] [CrossRef]

- Kurka, Josef. 2019. Do cryptocurrencies and traditional asset classes influence each other? Finance Research Letters 31: 38–46. [Google Scholar] [CrossRef] [Green Version]

- Kwon, Ji Ho. 2020. Tail behavior of Bitcoin, the dollar, gold and the stock market index. Journal of International Financial Markets, Institutions and Money 67: 101202. [Google Scholar] [CrossRef]

- Li, Jingming, Nianping Li, Jinqing Peng, Haijiao Cui, and Zhibin Wu. 2019. Energy consumption of cryptocurrency mining: A study of electricity consumption in mining cryptocurrencies. Energy 168: 160–68. [Google Scholar] [CrossRef]

- Li, Rong, Sufang Li, Di Yuan, and Huiming Zhu. 2021. Investor attention and cryptocurrency: Evidence from wavelet-based quantile Granger causality analysis. Research in International Business and Finance 56: 101389. [Google Scholar] [CrossRef]

- Li, Yi, Zhang Wei, Xiong Xiong, and Wang Pengfei. 2020. Does size matter in the cryptocurrency market? Applied Economics Letters 27: 1141–49. [Google Scholar] [CrossRef]

- Liang, Xiaobei, Yibo Yang, and Jiani Wang. 2016. Internet finance: A systematic literature review and bibliometric analysis. Paper Presented at International Conference on Electronic Business (ICEB), Xiamen, China, December 4–8; pp. 386–98. [Google Scholar]

- Matkovskyy, Roman. 2019. Centralized and decentralized bitcoin markets: Euro vs. USD vs. GBP. Quarterly Review of Economics and Finance 71: 270–79. [Google Scholar] [CrossRef]

- Mensi, Walid, Mobeen Ur Rehman, Debasish Maitra, Khamis Hamed Al-Yahyaee, and Ahmet Sensoy. 2020. Does bitcoin co-move and share risk with Sukuk and world and regional Islamic stock markets? Evidence using a time-frequency approach. Research in International Business and Finance 53: 101230. [Google Scholar] [CrossRef]

- Mensi, Walid, Yun Jung Lee, Khamis Hamed Al-Yahyaee, Ahmet Sensoy, and Seong Min Yoon. 2019. Intraday downward/upward multifractality and long memory in Bitcoin and Ethereum markets: An asymmetric multifractal detrended fluctuation analysis. Finance Research Letters 31: 19–25. [Google Scholar] [CrossRef]

- Merediz-Solá, Ignasi, and Aurelio F. Bariviera. 2019. A bibliometric analysis of bitcoin scientific production. Research in International Business and Finance 50: 294–305. [Google Scholar] [CrossRef] [Green Version]

- Milian, Eduardo Z., Mauro de M. Spinola, and Marly M. de Carvalho. 2019. Fintechs: A literature review and research agenda. Electronic Commerce Research and Applications 34: 100833. [Google Scholar] [CrossRef]

- Mnif, Emna, Anis Jarboui, and Khaireddine Mouakhar. 2020. How the cryptocurrency market has performed during COVID 19? A multifractal analysis. Finance Research Letters 36: 101647. [Google Scholar] [CrossRef] [PubMed]

- Nakamoto, Satoshi. 2008. Bitcoin: A Peer-to-Peer Electronic Cash System. Available online: https://bitcoin.org/en/bitcoin-paper (accessed on 10 February 2021).

- Náñez Alonso, Sergio Luis, Javier Jorge-vázquez, Miguel Ángel Echarte Fernández, and Ricardo Francisco Reier Forradellas. 2021. Cryptocurrency mining from an economic and environmental perspective. Analysis of the most and least sustainable countries. Energies 14: 4254. [Google Scholar] [CrossRef]

- Omane-Adjepong, Maurice, and Imhotep Paul Alagidede. 2019. Multiresolution analysis and spillovers of major cryptocurrency markets. Research in International Business and Finance 49: 191–206. [Google Scholar] [CrossRef]

- Page, Matthew J., Joanne E. McKenzie, Patrick M. Bossuyt, Isabelle Boutron, Tammy C. Hoffmann, Cynthia D. Mulrow, Larissa Shamseer, Jennifer M. Tetzlaff, Elie A. Akl, Sue E. Brennan, and et al. 2021. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. Systematic Reviews 10: 89. [Google Scholar] [CrossRef]

- Papadamou, Stephanos, Nikolaos A. Kyriazis, Panayiotis Tzeremes, and Shaen Corbet. 2021. Herding behaviour and price convergence clubs in cryptocurrencies during bull and bear markets. Journal of Behavioral and Experimental Finance 30: 100469. [Google Scholar] [CrossRef]

- Pelster, Matthias, Bastian Breitmayer, and Tim Hasso. 2019. Are cryptocurrency traders pioneers or just risk-seekers? Evidence from brokerage accounts. Economics Letters 182: 98–100. [Google Scholar] [CrossRef] [Green Version]

- Peng, Yaohao, Pedro Henrique Melo Albuquerque, Jader Martins Camboim de Sá, Ana Julia Akaishi Padula, and Mariana Rosa Montenegro. 2018. The best of two worlds: Forecasting high frequency volatility for cryptocurrencies and traditional currencies with Support Vector Regression. Expert Systems with Applications 97: 177–92. [Google Scholar] [CrossRef]

- Phillip, Andrew, Jennifer Chan, and Shelton Peiris. 2018. A new look at Cryptocurrencies. Economics Letters 163: 6–9. [Google Scholar] [CrossRef]

- Phillip, Andrew, Jennifer Chan, and Shelton Peiris. 2019. On long memory effects in the volatility measure of Cryptocurrencies. Finance Research Letters 28: 95–100. [Google Scholar] [CrossRef]

- Qiao, Xingzhi, Huiming Zhu, and Liya Hau. 2020. Time-frequency co-movement of cryptocurrency return and volatility: Evidence from wavelet coherence analysis. International Review of Financial Analysis 71: 101541. [Google Scholar] [CrossRef]

- Raimundo, Júnior, Gerson de Souza, Rafael Baptista Palazzi, Ricardo de Souza Tavares, and Marcelo Cabus Klotzle. 2020. Market Stress and Herding: A New Approach to the Cryptocurrency Market. Journal of Behavioral Finance, 43–57. [Google Scholar] [CrossRef]

- Rialti, Riccardo, Giacomo Marzi, Cristiano Ciappei, and Donatella Busso. 2019. Big data and dynamic capabilities: A bibliometric analysis and systematic literature review. Management Decision 57: 2052–68. [Google Scholar] [CrossRef] [Green Version]

- Sabah, Nasim. 2020. Cryptocurrency accepting venues, investor attention, and volatility. Finance Research Letters 36: 101339. [Google Scholar] [CrossRef]

- Sadeghi Moghadam, Mohammad Reza, Hossein Safari, and Narjes Yousefi. 2021. Clustering quality management models and methods: Systematic literature review and text-mining analysis approach. Total Quality Management and Business Excellence 32: 241–64. [Google Scholar] [CrossRef]

- Sapkota, Niranjan, and Klaus Grobys. 2021. Asset market equilibria in cryptocurrency markets: Evidence from a study of privacy and non-privacy coins. Journal of International Financial Markets, Institutions and Money 74: 101402. [Google Scholar] [CrossRef]

- Sensoy, Ahmet. 2019. The inefficiency of Bitcoin revisited: A high-frequency analysis with alternative currencies. Finance Research Letters 28: 68–73. [Google Scholar] [CrossRef]

- Shonhe, Liah. 2020. Continuous Professional Development (CPD) of Librarians: A Bibliometric Analysis of Research Productivity Viewed Through WoS. Journal of Academic Librarianship 46: 102106. [Google Scholar] [CrossRef]

- Sun, Xiaolei, Mingxi Liu, and Zeqian Sima. 2020. A novel cryptocurrency price trend forecasting model based on LightGBM. Finance Research Letters 32: 101084. [Google Scholar] [CrossRef]

- Symitsi, Efthymia, and Konstantinos J. Chalvatzis. 2019. The economic value of Bitcoin: A portfolio analysis of currencies, gold, oil and stocks. Research in International Business and Finance 48: 97–110. [Google Scholar] [CrossRef] [Green Version]

- Tan, Shay Kee, Jennifer So Kuen Chan, and Kok Haur Ng. 2020. On the speculative nature of cryptocurrencies: A study on Garman and Klass volatility measure. Finance Research Letters 32: 101075. [Google Scholar] [CrossRef]

- Urquhart, Andrew. 2016. The inefficiency of Bitcoin. Economics Letters 148: 80–82. [Google Scholar] [CrossRef]

- Urquhart, Andrew. 2017. Price clustering in Bitcoin. Economics Letters 159: 145–48. [Google Scholar] [CrossRef]

- Urquhart, Andrew, and Hanxiong Zhang. 2019. Is Bitcoin a hedge or safe haven for currencies? An intraday analysis. International Review of Financial Analysis 63: 49–57. [Google Scholar] [CrossRef]

- van Eck, Nees Jan, and Ludo Waltman. 2017. Citation-based clustering of publications using CitNetExplorer and VOSviewer. Scientometrics 111: 1053–70. [Google Scholar] [CrossRef] [Green Version]

- Walther, Thomas, Tony Klein, and Elie Bouri. 2019. Exogenous drivers of Bitcoin and Cryptocurrency volatility—A mixed data sampling approach to forecasting. Journal of International Financial Markets, Institutions and Money 63: 101133. [Google Scholar] [CrossRef]

- Wang, Gang Jin, Chi Xie, Danyan Wen, and Longfeng Zhao. 2019. When Bitcoin meets economic policy uncertainty (EPU): Measuring risk spillover effect from EPU to Bitcoin. Finance Research Letters 31: 489–97. [Google Scholar] [CrossRef]

- Wang, Gang Jin, Xin yu Ma, and Hao yu Wu. 2020. Are stablecoins truly diversifiers, hedges, or safe havens against traditional cryptocurrencies as their name suggests? Research in International Business and Finance 54: 101225. [Google Scholar] [CrossRef]

- Wei, Wang Chun. 2018. Liquidity and market efficiency in cryptocurrencies. Economics Letters 168: 21–24. [Google Scholar] [CrossRef]

- Yi, Shuyue, Zishuang Xu, and Gang Jin Wang. 2018. Volatility connectedness in the cryptocurrency market: Is Bitcoin a dominant cryptocurrency? International Review of Financial Analysis 60: 98–114. [Google Scholar] [CrossRef]

- Yue, Yao, Xuerong Li, Dingxuan Zhang, and Shouyang Wang. 2021. How cryptocurrency affects economy? A network analysis using bibliometric methods. International Review of Financial Analysis 77: 101869. [Google Scholar] [CrossRef]

- Zhang, Shuai, Xinyu Hou, and Shusong Ba. 2021. What determines interest rates for bitcoin lending? Research in International Business and Finance 58: 101443. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Almeida, J.; Gonçalves, T.C. A Decade of Cryptocurrency Investment Literature: A Cluster-Based Systematic Analysis. Int. J. Financial Stud. 2023, 11, 71. https://doi.org/10.3390/ijfs11020071

Almeida J, Gonçalves TC. A Decade of Cryptocurrency Investment Literature: A Cluster-Based Systematic Analysis. International Journal of Financial Studies. 2023; 11(2):71. https://doi.org/10.3390/ijfs11020071

Chicago/Turabian StyleAlmeida, José, and Tiago Cruz Gonçalves. 2023. "A Decade of Cryptocurrency Investment Literature: A Cluster-Based Systematic Analysis" International Journal of Financial Studies 11, no. 2: 71. https://doi.org/10.3390/ijfs11020071

APA StyleAlmeida, J., & Gonçalves, T. C. (2023). A Decade of Cryptocurrency Investment Literature: A Cluster-Based Systematic Analysis. International Journal of Financial Studies, 11(2), 71. https://doi.org/10.3390/ijfs11020071