The sampled 149 branch offices (89 and 60 registered and unregistered, respectively) of MFIs from all parts of Bangladesh were visited to conduct client interviews during the five months from November 2013 to March 2014. A total of 387 clients were interviewed (212 and 175 clients of registered and unregistered NGO-MFIs, respectively), but some clients did not respond to all questions and 342 (88 percent) complete observations for 147 NGO-MFIs were used in the analysis (200 and 142 clients of registered and unregistered MFIs, respectively).

6.1. Descriptive Statistics

In addition to the structured interview questions,

Table 1 reports descriptive statistics for responses to each question and whether or not there is a significant difference in affirmative responses by clients of registered compared with unregistered NGO-MFIs. The Cronbach’s alpha for the 12 questions was 0.878. However, for three questions, no clients of unregistered NGO-MFIs responded “Yes”. These questions relate to Q3—participants’ knowledge of the interest rate (per month) on loans and savings charged by their MFI; Q11—whether or not the service charge is known; and Q12—knowledge of whether or not interest is earned on their savings. Consequently, significant Chi squared values (

p < 0.001) were recorded for the clients of regulated compared with nonregulated MFIs, as shown in

Table 1.

There are also significant Chi squared differences (p < 0.001) for “Yes” responses by clients of registered (47 percent) and unregistered (26 percent) NGO-MFIs to Q1, concerning knowledge of types of loans, Q2, concerning explanations by loan officers (48 and 11 percent, respectively), Q4, concerning maintenance of a savings or passbook (68 and 49 percent, respectively), Q5, concerning receipt of promissory notes (72 and 40 percent, respectively), Q6, concerning accessibility of loan and savings information (96 and 9 percent, respectively), Q7 concerning knowledge of fees, premiums and claims regarding insurance (26 and two percent, respectively), Q8, concerning knowledge of savings (100 and 32 percent, respectively), Q9, concerning knowledge of ability to withdraw savings (100 and 95 percent, respectively), and Q10, concerning knowledge of other, voluntary savings (99 and 32 percent, respectively).

Table 2 reports the Pearson’s correlations between responses to questions 1–12. As was anticipated, some of the Pearson’s correlations were unitary (e.g., Q11 and Q12), with others very high (e.g., 0.879 between Q3 and Q6 and 0.739 between Q3 and Q9) and correlations with the variable registered/unregistered were perfect in some cases, meaning that a singular matrix due to high multicollinearity in the factor analysis will not allow estimation of the Kaiser–Meyer–Olkin (KMO) measure of sampling adequacy. Hence, responses to questions 3, 11, and 12 were omitted. Without these three questions, the Cronbach’s alpha for the remaining nine questions was reduced to 0.720, which is considered adequate.

6.2. Factor Analysis

As mentioned, to reduce the number of variables, the nine questions reported in

Table 1 where responses were not perfectly predictive of MFI registration status were factor analyzed (i.e., questions 1, 2, 4, 5, 6, 7, 8, 9, and 10). Only observations for which all data were present and also met the regression variable requirements are included, resulting in a sample of 342 client observations. The

Table 2 correlations between client responses to these questions reveal that a substantial number are above 0.30 and the inverse correlation matrix reported in

Appendix A—

Table A1 confirm that most correlations among the variables are significant and the negative partial (anti-image) covariances and correlations reported in

Appendix A—

Table A2 reveal only two correlations above 0.70 (Q6 and Q8). Hence, the responses are considered suitable for factor analysis (

Hair et al. 2014, p. 101). The Kaiser–Meyer–Olkin measure of sampling adequacy was 0.651 (

Appendix A—

Table A3, which is low (

Hair et al. 2014, p. 102), but it needs to be remembered that responses to three questions that perfectly predicted NGO-MFI registration status were omitted from the analysis and Bartlett’s test of sphericity, which provides the statistical significance that the correlation matrix has significant correlations among at and a Chi-square of 1106.19 (

p < 0.001) (

Appendix A—

Table A3), enabling the factor analysis to proceed.

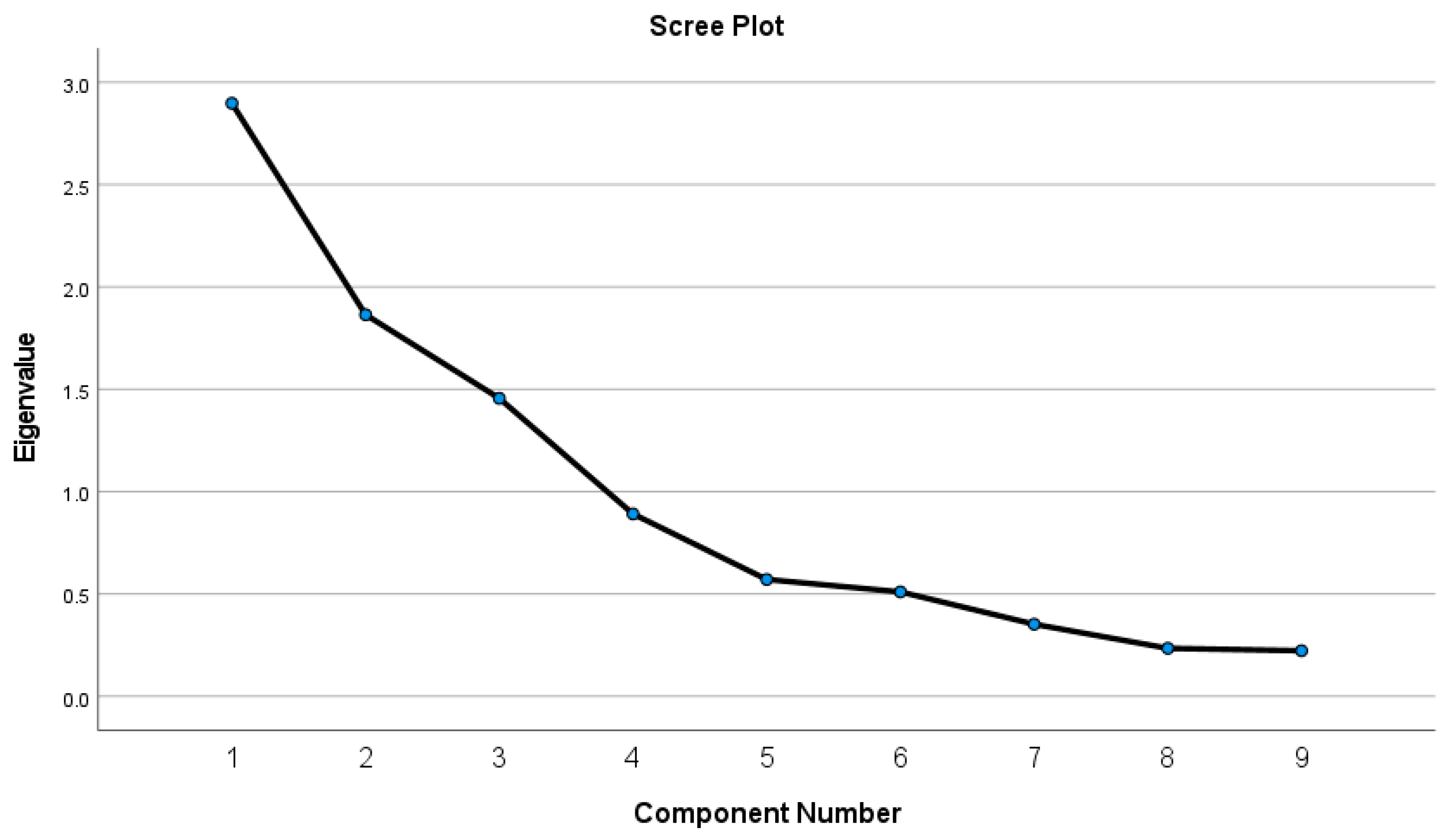

The scree plot (

Appendix A—

Figure A1), communalities (

Appendix A—

Table A4), and eigenvalues greater than one (

Appendix A—

Table A5) (

Hair et al. 2014, p. 107) suggested that three factors capture the variability in the responses best. The lowest communality was 0.495 and the next lowest 0.520 with the rest above 0.6, so the proportion of variance explained for each variable explained by the components was acceptable to proceed. Together, these three factors explained over 69 percent of the variance in the client responses with 32 percent for Factor 1, 21 percent for Factor 2, and 16 percent for Factor 3.

The component matrix (

Appendix A—

Table A6) plus the reproduced correlations (

Appendix A—

Table A7) for the nine questions confirm the earlier outcomes. An oblimin rotation with Kaiser normalization was chosen since the factors were expected to be correlated (

Hair et al. 2014: 114).

Table 3 presents the rotated (oblimin

7) principal components analysis loadings for the client responses to the included questions. The structure matrix is reported in

Appendix A—

Table A8. The loadings are all above 0.50 with at least two questions loading on each component, so a simple structure results, as was the aim. The three components were deemed to represent “Personalized information about savings/loan basics”, “General information about loans”, and “Knowledge of access to savings”.

For the first theme, “Personalized information about savings/loan basics”, the items relate to the client’s knowledge about personal financial information, such as their loan/savings. Client responses to questions consisted of “interest charged on their loans and savings account by respective MFIs”, “access to information from MFIs during business hours”, “having passbook linked with their account”, and providing receipts to clients for financial transactions by respective MFIs.

In the second theme, “General information about Loans”, the items relate to client knowledge about their financial service provider. The questions were focused on the types of loan available, fees premium, settlements of claims for insurance (if any), and whether or not the loan officer explained the terms and conditions of their loan. For the third theme, “Knowledge of access to savings”, the items relate to the clients’ knowledge about their rights to access their savings and their knowledge of the voluntary nature of savings.

Table 4 reports descriptive statistics and tests of difference for demographic variables for clients of registered and unregistered MFIs and the factor scores. The mean annual income was 42,611 taka, with a significant difference (

p < 0.000) between the mean for 200 registered NGO-MFI clients (53,724 taka) and that for 142 clients of unregistered NGO-MFIs (27,592 taka). The factor score for Factor 1 “Knowledge about personalized information about savings/loan basics” for the full sample was −0.018, with a significant difference (

p < 0.000) between the means for registered (0.801) and unregistered (−1.171) NGO-MFI clients. For Factor 2, “General knowledge about savings/loan”, the overall mean was −0.037, with a significant difference (

p < 0.000) between means for registered (0.275) and unregistered MFI clients (−0.475). For Factor 3, “Knowledge of access to savings”, overall, the mean was −0.004, with an insignificant difference between means for registered and unregistered NGO-MFI clients.

The mean age of clients was 39.9 years, with no significant difference for clients of registered versus unregistered NGO-MFIs. The mean number of children was 4.5 overall, with means of 3.7 and 5.7 for registered and unregistered MFI clients, respectively, which is a significant difference (p < 0.000).

For the dichotomous variables, overall 59 percent of clients were married, with a significant difference (p < 0.01) for clients of registered (50 percent) and unregistered (70 percent) NGO-MFIs. In terms of microenterprise ownership, 66 percent overall owned a microenterprise, at 83 and 42 percent for registered and unregistered MFIs, respectively, a difference that is significant (p < 0.000). In terms of education, there was a significant difference (p < 0.000) between clients of the two types of MFI: 77 and 33 percent of clients of registered and unregistered NGO-MFIs, respectively, had some schooling.

6.3. Pearson’s Correlations

Table 5 reports the Pearson’s correlations for the 342 client observations between registered and unregistered NGO-MFI members’ financial literacy as represented by the factor scores, as well as income, age, number of children, and education level. There were significant positive correlations between the three factors [Factor 1 “Knowledge about personalized information about savings/loan basics”, Factor 2, “General knowledge about savings/loan” and Factor 3, “Knowledge of access to savings”] (r = 0.969, r = 0.376, and r = 0.069, respectively) and the status (registered/unregistered) of their NGO-MFIs. It is important to note that Factor 1, “Knowledge of personalized information about loan/savings”, was almost perfectly correlated with registered MFI status, and it is likely that this lack of variability will cause problems with multivariate estimation. None of the correlations between the three factors themselves was higher than 0.240.

Strong positive correlations were noted between NGO-MFI status and clients’ number of children, education, and microenterprise ownership. Client income was significantly correlated with the three factors (r = 0.539, r = 0.266, and r = 0.145, respectively), and also with NGO-MFI status (r = 0.638). In terms of independent variables, client age, as is to be expected, was highly correlated (r = 0.660) with the number of children and with education (r = 0.425). None of the other correlations between the independent variables was higher than 0.400, and so should not present multicollinearity concerns.

6.4. Multivariate Results

OLS Regression results for the test of Hypothesis 1 are reported in

Table 6. This test regressed the hypothesis and control variables on each of the factor scores and the total factor score. The F statistics for all three models were significant, and the R

2 ranged from 75 percent for Factor 1, to 15 percent for Factor 2, and only 3 percent for Factor 3. For the total factor score as the dependent variable, the R

2 was 50 percent. The regressions were robust, controlling for client observations attached to the same NGO-MFI. Notably, MFI status (registered/unregistered) was highly significant (

p < 0.001) and positive for Factors 1 and 2 and the total factor score. That is, client financial literacy and awareness were higher for registered MFIs compared with unregistered MFIs controlling for education and microenterprise ownership. Hence, Hypothesis 1 was supported. Having some schooling (education) was significant (

p < 0.001) only for Factor 2. Client ownership of microenterprises was significant (

p < 0.01) in explaining all three factors and their total (

p < 0.05), but was negatively significant for Factor 2.

For the tests of Hypothesis 2 and Hypothesis 3, robust OLS regression was used, with results reported in

Table 7. Total factor score was used, due to the high correlation between registered NGO-MFI client membership and Factor 1 scores

8. Again, the robust regression fit well, with significant F statistics and with a model R

2 of 45 percent. The total factor score was significant (

p < 0.01), supporting Hypothesis 2, as was belonging to a registered NGO-MFI (

p < 0.001), thus supporting Hypothesis 3. Amongst the control variables, the number of children alone was significant (

p < 0.05) and positive, indicating that children in this setting, on average, add to family income rather than detract from it. Age was negative but not significant, and, hence, this direction needs to be interpreted with caution.

6.5. Robustness Tests

As a robustness test for Hypothesis 1, a financial literacy index comprising the questions listed in

Table 1 with clients’ yes responses were used to create a score between 0–12 and analyzed using truncated regression for the same client sample. That is, instead of factor analyzing, each question was equally weighted and the total of yes responses is used as the dependent variable that is truncated at a maximum score of 12. The mean score for the full sample is 7.01 with that for the regulated MFIs is 9.725 and for unregulated NGO-MFIs is 3.20, a difference that is significant at

p < 0.001. The untabulated truncated regression results based on 342 observations clustered on NGO-MFI identity confirm (refer

Table 6) the factor analysis results. The model fits well with an R

2 of 38.52 per cent. The registered MFI indicator was significant at

p < 0.001, consistent with the total factor score as the dependent variable analysis. The variable representing clients with some schooling was significant at

p < 0.001 and microenterprise ownership was significant at

p < 0.05.

Similarly, the same financial literacy index was used as a robustness test for Hypothesis 2 and Hypothesis 3 with income as the dependent variable. The OLS results confirmed (refer

Table 7) the significance of the financial literacy index (

p < 0.01) and registered NGO-MFI indicator (

p < 0.05) in explaining client income, with an R

2 of 43.33 per cent. No other variables were significant. Both of these results confirm the primary findings.

{kind=link}