Buy Now and Pay (Dearly) Later: Unraveling Consumer Financial Spinning

Abstract

:1. Introduction

1.1. The Research Question

1.2. Article Overview

2. The Analytical Tools

2.1. Modeling—Need and Benefits

2.2. The Data Percolation Methodology

- (1)

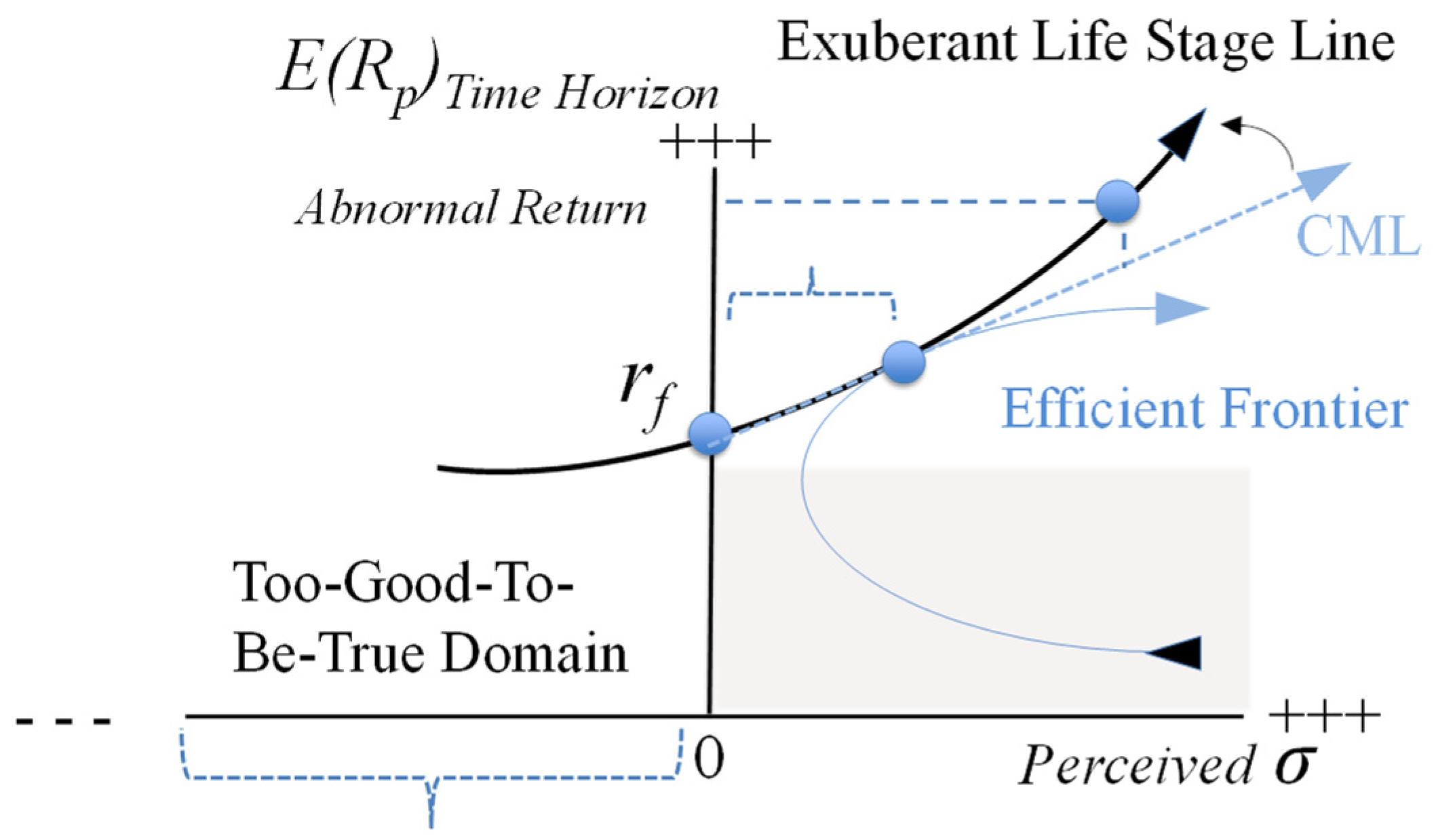

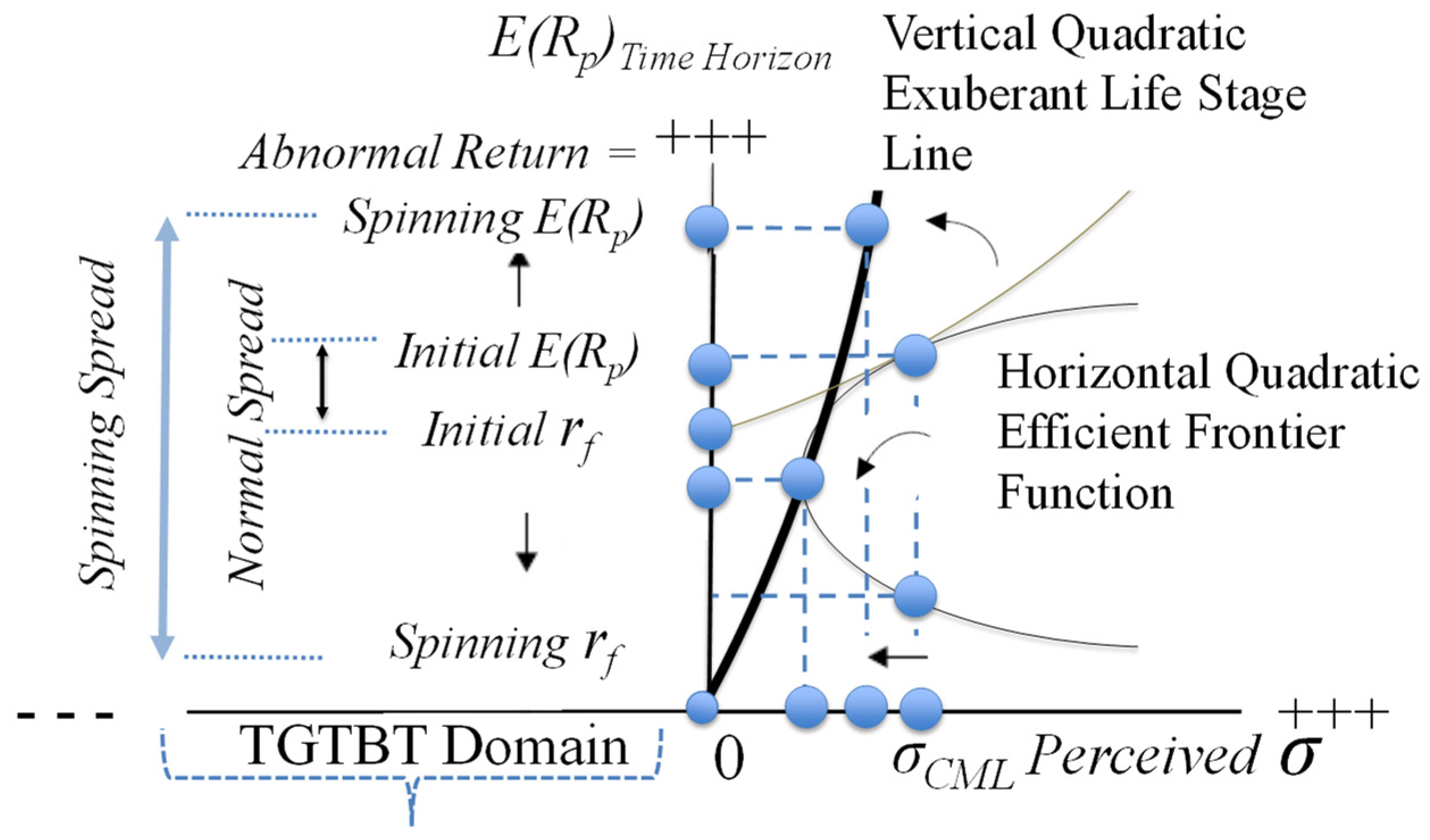

- The framework characterizes the type of construct (beginning, end constructs) and the types of bonds between the variables. We use only the “influence” bond out of the four main types that DPM recommends, in three of its forms: direct influence—positive (I+) or negative (I−)—and indirect—moderating (I±). In the framework presented in Figure 1, rf is the starting point and the “abnormal expected return” the end point;

- (2)

- Constructs are of the same nature. For this reason, we do not refer to risk but to perception of risk;

- (3)

- Symmetry of and among the constructs is of the essence and we assign an equal conceptual weight to each one, until proven otherwise;

- (4)

- Parallelism is paramount: for example, the mathematical functions we use are assumed to be quadratic. We develop our argument on that basis (parallelism outweighs standard assumptions supporting existing models). For this reason, we consider the Capital Market Line (CML) to be a portion of a larger quadratic function, even if this can be strongly debated (see further below). This is because in DPM, all constructs and all of their treatments are assumed upfront to be equal (parallel) until proven otherwise. This assumption is necessary because we are dealing with emerging concepts and do not yet know which constructs take precedence, to what level, and in what order (e.g., precedence, consequence). Hence, we need to keep all options open rather than arbitrarily deciding how to organize the constructs and their characteristics. In the present case, this is because we assume the efficient frontier to be in a quadratic form; by parallelism, we postulate that all other curves of a similar nature are also quadratic. This is not carved in stone; it is merely a technique that DPM suggests to set baselines by studying as yet “unidentified behavioral objects”, namely, emerging concepts;

- (5)

- A multidisciplinary approach allows the researcher to leave no stone unturned and discover “hidden truths”, especially in the context of emerging constructs. In the present case, multidisciplinarity is exposed in Table 1, which compares equivalent constructs across various disciplines. In DPM, these equivalences are considered as possible evidence of the validity of the emerging constructs under investigation.

2.3. The Other Tools

3. Consumer Financial Spinning

3.1. Definition

3.2. Some Key Definitions

4. The Spinning Framework Using the CAPM-Markowitz Models

4.1. The CFS-Markowitz-Modified CAPM Framework

4.2. CAPM Revisited

5. Exploratory Field Study and Results

Results

6. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Proposed Evidence of CFS during the Global Financial Crisis

Appendix B. Excerpts from the Embryonic Questionnaire

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Spinning Debt Latent Variable |

| Debt |

| I very often borrow beyond my means. |

| I tend to be late in paying my debts. |

| I owe a lot of money. |

| Unsustainable |

| I have large debts compared to my capacity to reimburse them. |

| My total income is not enough to cover my total debt. |

| I am unlikely to be able to reimburse all my debts any time soon. |

| Exuberance |

| Despite having to borrow, I cannot resist an investment opportunity. |

| Risky Behavior Latent Variable |

| Speculation |

| I tend to invest with little regard to risk. |

| I like to gamble without paying much attention to my realistic chances of winning. |

| I do not like to take financial risks. (reverse). |

| Narrow |

| I only invest in a narrow range of financial products. |

| I am happy investing in one or very few assets like a house or bonds. |

| I do not have a well-diversified portfolio of financial assets. |

| Horizon |

| When I invest, I look for short-term gains. |

| I expect to earn money quickly when I invest. |

| I am in the financial market for the long run (reverse). |

| Disconnection Latent Variable |

| From Need |

| I am attuned to my financial needs (reverse). |

| I have carefully identified my financial needs (reverse). |

| I understand my financial needs (reverse). |

| From Goal |

| I have identified my financial goals with great care (reverse). |

| I have set my financial goals (reverse). |

| I stick to the financial goals I set (reverse). |

| From Preferences |

| I have determined which financial products I prefer (reverse). |

| I know which attributes I like and do not like in financial products (reverse). |

| I know what I do and do not like about the financial products in which I invest (reverse). |

| Sociodemographics |

| 1 | According to the European Central Bank (2010) systemic risk is a risk “so widespread that it impairs the functioning of a financial system to the point where economic growth and welfare suffer materially”. Accessed 1 September 2021. |

References

- Babiak, Paul. 1995. When psychopaths go to work. Applied Psychology 44: 171–88. [Google Scholar] [CrossRef]

- Baker, Malcolm, and Jeffrey Wurgler. 2007. Investor sentiment in the stock market. Journal of Economic Perspectives 21: 129–51. [Google Scholar] [CrossRef] [Green Version]

- Barberis, Nicholas, and Richard Thaler. 2002. A Survey of Behavioral Finance National Bureau of Economic Research NBER Working Paper No. 9222. Available online: https://www.nber.org/papers/w9222 (accessed on 2 June 2021).

- Benoît, Sylvain, Jean-Edouard Colliard, Christophe Hurlin, and Christophe Pérignon. 2015. Where the Risks Lie: A Survey on Systemic Risk. HEC Paris Research Paper No. FIN-2015–1088. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2577961 (accessed on 23 July 2021).

- Bettman, James R., Mary Frances Luce, and John W. Payne. 1998. Constructive Consumer Choice Processes. Journal of Consumer Research 25: 87–217. [Google Scholar]

- Black, Fischer, Michael C. Jensen, and Myron Scholes. 1972. The Capital Asset Pricing Model: Some Empirical Tests. In @Studies in the Theory of Capital Markets@. Edited by Michael C. Jensen. New York: Praeger, pp. 79–121. [Google Scholar]

- Boush, David M., Marian Friestad, and Peter Wright. 2015. Deception in the Marketplace: The Psychology of Deceptive Persuasion and Consumer Self-Protection. London: Routledge. [Google Scholar]

- Brunnermeier, Markus K., and Martin Oehmke. 2012. Bubbles, Financial Crises, and Systemic Risk NBER Working Paper No. 18398. Available online: https://www.nber.org/papers/w18398 (accessed on 30 May 2020).

- Campbell, John Y., Andrew W. Lo, and A. Craig McKinlay. 1997. The Econometrics of Financial Markets. Princeton: Princeton University Press. [Google Scholar]

- Chakravarti, Ashok. 2017. Imperfect Information and Opportunism. Journal of Economic Issues 51: 1114–36. [Google Scholar] [CrossRef]

- Cleeren, Kathleen, Harald van Heerde, and Mamik G. Dekimpe. 2013. Rising from the ashes: How brands and categories can overcome product-harm crises. Journal of Marketing 77: 58–77. [Google Scholar] [CrossRef]

- Cochrane, John H. 2005. Asset Pricing. revised ed. Princeton: Princeton University Press. [Google Scholar]

- Copes, Heith, and Lynne M. Vieraitis. 2012. Identity Thieves: Motives and Methods. Boston: Northeastern University Press. [Google Scholar]

- Coulibaly, Brahima, and Geng Li. 2009. Choice of mortgage contracts: Evidence from the survey of consumer finances. Real Estate Economics 37: 659–73. [Google Scholar] [CrossRef] [Green Version]

- Cowley, Elizabeth, and Christina I. Anthony. 2005. Consumers tell many lies. Deception Memory: When Will Consumers Remember Their Lies? Journal of Consumer Research 46: 180–99. [Google Scholar] [CrossRef]

- Daunt, Kate L., and Lloyd C. Harris. 2012. Exploring the forms of dysfunctional customer behaviour: A study of differences in servicescape and customer disaffection with service. Journal of Marketing Management 28: 129–53. [Google Scholar] [CrossRef]

- De Bandt, Olivier, and Philipp Hartmann. 2000. Systemic Risk: A Survey. ECB Working Paper, No. 35. Frankfurt: European Central Bank (ECB). Available online: https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp035.pdf (accessed on 5 June 2021).

- De Bondt, Werner F. M., and Richard H. Thaler. 1995. Does the stock market overreact? Journal of Finance 40: 793–805. [Google Scholar] [CrossRef]

- DeLiema, Marguerite, Doug Shadel, and Karla Pak. 2020. Profiling Victims of Investment Fraud: Mindsets and Risky Behaviors. Journal of Consumer Research 46: 904–14. [Google Scholar] [CrossRef]

- DePaulo, Bella M., Deborah Kashy, Susan E. Kirkendol, Melissa M. Wyer, and Jennifer A. Epstein. 1996. Lying in everyday life. Journal of Personality and Social Psychology 70: 979–95. [Google Scholar] [CrossRef] [PubMed]

- Dinica, Irina, and Damian Motteau. 2012. The Market of the Bottom of the Pyramid: Impact on the Marketing-Mix of Companies. Master’s Thesis, Umea School of Business, Umea Univeritet, Umeå, Sweden. [Google Scholar]

- Dow, James. 2000. What Is Systemic Risk? Moral Hazard, Initial Shocks, and Propagation. Monetary and Economic Studies 18: 1–24. [Google Scholar]

- Estelami, Hooman. 2015. Cognitive catalysts for distrust in financial services markets: An integrative review. Journal of Financial Services Marketing 20: 246–57. [Google Scholar] [CrossRef]

- Etkin, Jordan, and Anastasiya Ghosh. 2018. When being in a positive mood increases choice deferral. Journal of Consumer Research 45: 208–25. [Google Scholar] [CrossRef]

- European Central Bank (ECB). 2010. Financial networks and financial stability. Financial Stability Review, 155–60. [Google Scholar]

- Fama, Eugene F. 1970. Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance 25: 383–417. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 1996. Multifactor Explanations of Asset Pricing Anomalies. The Journal of Finance 51: 55–84. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 2004. The Capital Asset Pricing Model: Theory and Evidence. Journal of Economic Perspectives 18: 325–46. [Google Scholar] [CrossRef] [Green Version]

- Fama, Eugene F., and Kenneth R. French. 2015. A five-factor asset pricing model. Journal of Financial Economics 116: 1–22. [Google Scholar] [CrossRef] [Green Version]

- Fehr, Esrnst, and Klaus Schmidt. 1999. A theory of fairness, competition, and cooperation. The Quarterly Journal of Economics 114: 817–68. [Google Scholar] [CrossRef]

- Fenton-O’Creevy, Mark, Nigel Nicholson, Emma Soane, and Paul Willman. 2003. Trading on illusions: Unrealistic perceptions of control and trading performance. Journal of Occupational and Organizational Psychology 76: 53–68. [Google Scholar] [CrossRef]

- Fernbach, Philip, Chrsitina Kan, and John G. Lynch Jr. 2015. Squeezed: Coping with constraint through efficiency and prioritization. Journal of Consumer Research 41: 1204–27. [Google Scholar] [CrossRef]

- Gervais, Simon, and Terrance Odean. 2001. Learning to be overconfident. The Review of Financial Studies 14: 1–27. [Google Scholar] [CrossRef]

- Gilbride, Timothy J., and Greg M. Allenby. 2004. A choice model with conjunctive, disjunctive, and compensatory screening rules. Marketing Science 23: 391–406. [Google Scholar] [CrossRef]

- Griffin, Dale, and Lyle Brenner. 2004. Perspectives on probability judgment calibration. In Blackwell Handbook of Judgment and Decision Making. Edited by Derek J. Koehler and Nigel Harvey. Hoboken, NJ: Wiley-Blackwell, pp. 177–99. [Google Scholar]

- Griffin, Dale, and Amos Tversky. 1992. The weighing of evidence and the determinants of confidence. Cognitive Psychology 24: 411–35. [Google Scholar] [CrossRef]

- Grinblatt, Mark, Matti Keloharju, and Juhani T. Linnainmaa. 2012. IQ, trading behavior, and performance. Journal of Financial Economics 104: 339–62. [Google Scholar] [CrossRef]

- Harris, Lloyd C., and Kate L. Reynolds. 2004. Jay customer behavior: An exploration of types and motives in the hospitality industry. Journal of Services Marketing 18: 339–57. [Google Scholar] [CrossRef]

- Hoch, Stephen J., and George F. Loewenstein. 1991. Time-inconsistent Preferences and Consumer Self-Control. Journal of Consumer Research 17: 492–507. [Google Scholar] [CrossRef] [Green Version]

- Huang, Laura, and Jone L. Pearce. 2015. Managing the unknowable: The effectiveness of early-stage investor gut feel in entrepreneurial investment decisions. Administrative Science Quarterly 60: 634–70. [Google Scholar] [CrossRef] [Green Version]

- Huang, Shiao Yan, Chi-Chen Lin, An-An Chiu, and David C. Yen. 2017. Fraud detection using fraud triangle risk factors. Information Systems Frontiers 19: 1343–56. [Google Scholar] [CrossRef]

- Isen, Alice M., and John M. Reeve. 2005. The influence of positive affect on intrinsic and extrinsic motivation: Facilitating enjoyment of play, responsible work behavior, and self-control. Motivation and Emotion 29: 295–323. [Google Scholar] [CrossRef]

- Jakobwitz, Sharon, and Vincent Egan. 2006. The dark triad and normal personality traits. Personality and Individual Differences 40: 331–39. [Google Scholar] [CrossRef]

- Kahneman, David, and Amos Tversky. 1979. Prospect Theory: An analysis of decision under risk. Econometrica 47: 263–92. [Google Scholar] [CrossRef] [Green Version]

- Kaminsky, Graciela L., and Sergio L. Schmukler. 2003. Short-Run Pain, long-Run Gain: The Effects of Financial Liberalization. National Bureau of Economic Research NBER WP-9787. Available online: http://www.nber.org/papers/w9787 (accessed on 13 July 2021).

- Karlsson, Niklas, George Loewenstein, and Duane Seppi. 2009. The ostrich effect: Selective attention to information. Journal of Risk and Uncertainty 38: 95–115. [Google Scholar] [CrossRef]

- Laran, Juliano. 2010. The influence of information processing goal pursuit on post-decision affect and behavioral intentions. Journal of Personality and Social Psychology 98: 16–28. [Google Scholar] [CrossRef] [Green Version]

- Lavoie, Marc. 2004. Post Keynesian consumer theory: Potential synergies with consumer research and economic psychology. Journal of Economic Psychology 25: 639–49. [Google Scholar] [CrossRef]

- Lesch, William, and Bruce Byars. 2008. Consumer insurance fraud in the US property-casualty industry Consumer insurance fraud. Journal of Financial Crime 15: 411–31. [Google Scholar] [CrossRef]

- Lintner, John. 1965. The Valuation of Risk Assets and the Selection of Risky Investments in Stock Portfolios and Capital Budgets. Review of Economics and Statistics 47: 13–37. [Google Scholar] [CrossRef]

- Loewenstein, Groege F., Elke U. Weber, Christopher K. Hsee, and Ned Welch. 2001. Risk as feelings. Psychological Bulletin 127: 267–86. [Google Scholar] [CrossRef]

- Lusardi, Annamaria, and Olivia S. Mitchelli. 2007. Financial literacy and retirement preparedness: Evidence and implications for financial education. Business Economics 42: 35–44. [Google Scholar] [CrossRef] [Green Version]

- Lusardi, Annamaria, and Olivia S. Mitchelli. 2014. The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature 52: 5–44. [Google Scholar] [CrossRef] [Green Version]

- Mani, Anandi, Sendhil Mullainathan, Eldar Shafir, and Jiaying Zhao. 2013. Poverty impedes cognitive function. Science 341: 976–80. [Google Scholar] [CrossRef] [Green Version]

- Manjit, S. Yadav. 2010. The Decline of Conceptual Articles and Implications for Knowledge Development. Journal of Marketing 74: 1–19. [Google Scholar]

- Markowitz, Harry. 1952. Portfolio Selection. Journal of Finance 7: 77–99. [Google Scholar]

- Mayer, Don, Anita Cava, and Catharine Baird. 2014. Crime and Punishment (or the Lack Thereof) for Financial Fraud in the Subprime Mortgage Meltdown: Reasons and Remedies for Legal and Ethical Lapses. American Business and Law Journal 51: 515–97. [Google Scholar] [CrossRef]

- Mehta, Nitin, Surendra Rajiv, and Kannan Srinivasan. 2004. Role of forgetting in memory-based choice decisions: A structural model. Quantitative Marketing and Economics 2: 107–40. [Google Scholar] [CrossRef]

- Mesly, Olivier. 2010. Voyage au Cœur de la Prédation Entre Vendeurs et Acheteurs—Une Nouvelle Théorie en Vente et Marketing. Sherbrooke: Université de Sherbrooke. [Google Scholar]

- Mesly, Olivier. 2015. Creating Models in Psychological Research. New York: Springer International Publishing. [Google Scholar]

- Mesly, Olivier. 2020. Spinning: Zooming in an atypical consumer behavior. Journal of MacroMarketing 41: 232–50. [Google Scholar] [CrossRef]

- Moore, Don A., and Paul J. Healy. 2008. The trouble with overconfidence. Psychological Review 115: 502–17. [Google Scholar] [CrossRef] [Green Version]

- Netemeyer, Richard G., Dee Warmath, Daniel Fernandes, and John G. Lynch Jr. 2018. How am I doing? Perceived financial well-being, its potential antecedents, and its relation to overall well-being. Journal of Consumer Research 45: 68–89. [Google Scholar] [CrossRef]

- Nicholson, Walter, and Christopher Snyder. 2017. Microeconomic Theory: Basic Principles and Extensions, 12th ed. Boston: Cengage Learning. [Google Scholar]

- Odean, Terrance. 1998. Do investors trade too much? American Economic Review 89: 1279–98. [Google Scholar] [CrossRef]

- Pyone, Jin Seok, and Alice M. Isen. 2011. Positive affect, intertemporal choice, and levels of thinking: Increasing consumers’ willingness to wait. Journal of Marketing Research 48: 532–43. [Google Scholar] [CrossRef] [Green Version]

- Ross, Stephen A. 1976. The Arbitrage Pricing Theory of Capital Asset Pricing. Journal of Economic Theory 13: 341–60. [Google Scholar] [CrossRef]

- Shah, Anuj K., Sendhil Mullainathan, and Eldar Shafir. 2012. Some consequences of having too little. Science 338: 682–85. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Sharpe, William F. 1964. Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk. Journal of Finance 19: 425–42. [Google Scholar]

- Soltani, Baham. 2013. The Anatomy of Corporate Fraud: A Comparative Analysis of High Profile American and European Corporate Scandals. Journal of Business Ethics 120: 251–74. [Google Scholar] [CrossRef]

- Stüttgen, Peter, Peter Boatwright, and Robert T. Monroe. 2012. A satisficing choice model. Marketing Science 31: 878–99. [Google Scholar] [CrossRef] [Green Version]

- Sutherland, Edwin H. 1924. Principles of Criminology. Chicago: University of Chicago Press. [Google Scholar]

- Titus, Ricard M., Fred Heinzelmann, and John M. Boyle. 1995. Victimization of Persons by Fraud. Crime and Delinquency 41: 54–72. [Google Scholar] [CrossRef]

- Van Rooij, Maarten, Annamaria Lusardi, and Rob Alessie. 2011. Financial literacy and stock market participation. Journal of Financial Economics 101: 449–72. [Google Scholar] [CrossRef] [Green Version]

- Von Neumann, John, and Oskar Morgenstern. 1947. Theory of Games and Economic Behavior; Princeton: Princeton University Press, Washington, DC: U.S. Government Printing Office.

- Zwane, Alix P. 2012. Implications of scarcity. Science 338: 617–18. [Google Scholar] [CrossRef]

| Construct | Finance | Marketing | (Neuro)Psychology |

|---|---|---|---|

| Sensitivity | The beta (β) in the CAPM formula | Elasticity | Emotional response to stimuli |

| Perceived Risk | Risk aversion | Fear (e.g., in advertising) | Perceived threat |

| Dysfunctionality | Excessive market frictions, volatility | Cognitive dissonance | Psychopathy |

| Reward | Expected returns on investment | Satisfaction | Pleasure |

| Moral Hazard | Dark Financial Triangle | Attitude | Dark Triad of Psychopathy |

| Needs, Goals, and Preferences | Idem | Idem | Idem |

| Greed | Overconfidence | Customer as king | Ego |

| Definition | In the emotional framing of the commonly used expression “investor sentiment”, overconfidence constitutes an unjustified positive emotional belief about market odds (Baker and Wurgler 2007), resulting in suboptimal performance (Fenton-O’Creevy et al. 2003), the exact opposite of the intended effect. |

| Borrowers’ internal vulnerabilities | Altered price perception and strategic outlook (Loewenstein et al. 2001), belief that the market plays in their favor, harbored biases, investment ground rules ignored (Huang and Pearce 2015), illusion of control (Moore and Healy 2008), reliance on gut feeling (Estelami 2015). |

| Warning signs | Expressing unjustified positive belief about market odds, attempting at predicting the future, blurring product attributes (Etkin and Ghosh 2018), desensitizing to pessimistic news/disregarding negative possibilities, favoring enjoyable situations (Isen and Reeve 2005), narrowing the range of possible choices and actions, opting for poor portfolio diversification (Odean 1998), overestimating stock selection skills, over focusing on prioritizing current tasks and activities, underestimating the market conditions and risks (Coulibaly and Li 2009). |

| Time horizon effect | Absence of due consideration for current market conditions, applying poor statistical weights to the credible variables influencing decision-making (Griffin and Tversky 1992), misaligning intertemporal choice (Pyone and Isen 2011), weak household planning (Lusardi and Mitchelli 2007). |

| Definition | Limiting the disclosure of vital information or providing unnecessary if not misleading information to clients-prey, taking advantage of information asymmetry (predatory) or, from the borrower’s point of view, self-limiting access to crucial information (Mehta et al. 2004; Cleeren et al. 2013). |

| Borrowers’ internal vulnerabilities | Erroneous perception of self-efficacy, judgmental biases, lack or loss of self-control (Laran 2010), limited understanding of basic economic principles (Van Rooij et al. 2011), materialistic values, misaligned cash-flow sensitivity, playing the “ostrich” (Karlsson et al. 2009), poor financial education, prosperous expectations (Stüttgen et al. 2012), worsening of risk. |

| Warning signs | Acting on noise in investment decision-making, avoiding bad news, avoiding long-term planning, confining in limited portfolio diversification, displaying overly positive financial behavior and greater aggressiveness (Zwane 2012), engaging in careless speculation, displaying poor decision making and planning trading behavior (Grinblatt et al. 2012), exerting lower self-control, ignoring voluntarily or not critical information, planning weakened household and retirement strategies (Lusardi and Mitchelli 2014). |

| Time horizon effect | Short-term thinking with no consideration for past experience (Gilbride and Allenby 2004), under time pressure, shifting attention to immediate goals while sacrificing future ones (Shah et al. 2012). |

| Definition | Material false statements or erroneous representations of facts (Titus et al. 1995) by market agents, including customers (Harris and Reynolds 2004; Cowley and Anthony 2005; Boush et al. 2015), while being aware of their falsity or their use to make false claims, characterized in whole or in part by a search for chains of lies, forms of identity concealment, securitization-type processes (risk hiding), the presence of toxic products, the seeking of a financial advantage (DePaulo et al. 1996), the unethical seeking of financial gains (e.g., in the form of financial compensation—(Lesch and Byars 2008). It usually takes place in unsupervised settings/poorly regulated markets. |

| Borrowers’ internal vulnerabilities | Capitalizing on silent second mortgages, double-selling engaging in incomplete disclosure rescue/equity skimming, heightened vigilance for fear of being caught and of retaliation to avoid getting caught, illegal flipping, little self-control; materialistic ambitions. |

| Warning signs | Engaging in growing debt load; (over)stretching resources (Fernbach et al. 2015), procrastinating (Dinica and Motteau 2012), self-justification for abusive behaviors and showing lack of accountability (Huang et al. 2017). |

| Time horizon effect | Use of fraudulent documents constrained by time (Copes and Vieraitis 2012), working “against the clock”. |

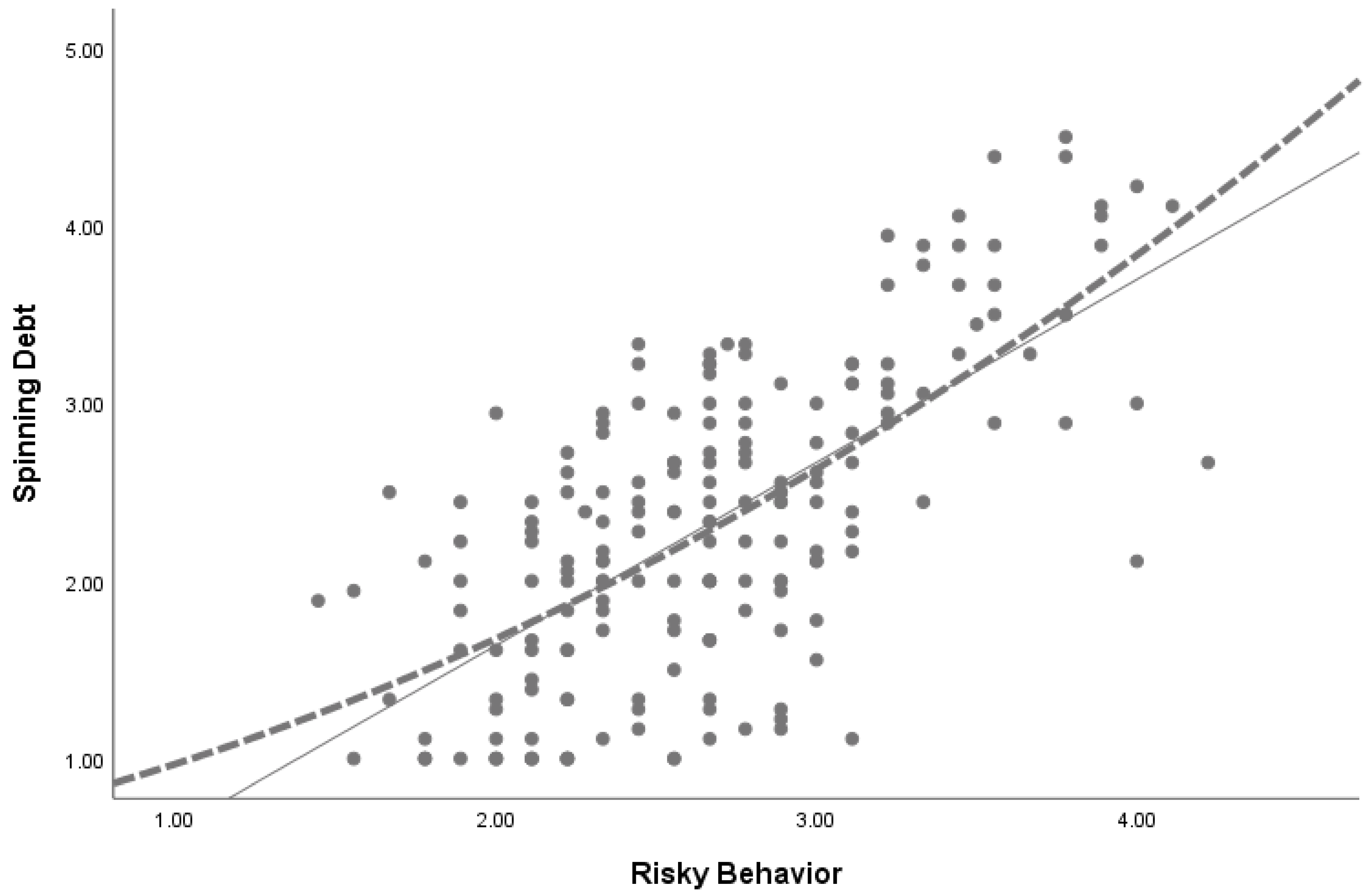

| R | R Square | Adjusted R Square | Std. Error of the Estimate | Durbin-Watson | |

|---|---|---|---|---|---|

| 0.677 | 0.458 | 0.455 | 0.63816 | 2.167 | |

| Sum of Squares | df | Mean Square | F | Sig. | |

| Regression | 66.723 | 1 | 66.723 | 163.840 | 0.000 |

| Residual | 79.006 | 194 | 0.407 | − | − |

| Total | 145.728 | 195 | − | − | − |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mesly, O. Buy Now and Pay (Dearly) Later: Unraveling Consumer Financial Spinning. Int. J. Financial Stud. 2021, 9, 55. https://doi.org/10.3390/ijfs9040055

Mesly O. Buy Now and Pay (Dearly) Later: Unraveling Consumer Financial Spinning. International Journal of Financial Studies. 2021; 9(4):55. https://doi.org/10.3390/ijfs9040055

Chicago/Turabian StyleMesly, Olivier. 2021. "Buy Now and Pay (Dearly) Later: Unraveling Consumer Financial Spinning" International Journal of Financial Studies 9, no. 4: 55. https://doi.org/10.3390/ijfs9040055

APA StyleMesly, O. (2021). Buy Now and Pay (Dearly) Later: Unraveling Consumer Financial Spinning. International Journal of Financial Studies, 9(4), 55. https://doi.org/10.3390/ijfs9040055