1. Introduction

Gender diversity within the board of directors is a topic that has received significant attention from the business world, regulators, and academic researchers within several academic fields, including human resource management, leadership, economics, and even accounting and finance (

Loukil and Yousfi 2016;

Adams and Ferreira 2004;

Carter et al. 2003;

Daily et al. 1999, among others). Theoretical and empirical contributions have examined if and how board gender diversity affects corporate governance, financial decision making, and corporate risk taking (

Adams and Ferreira 2004,

2009). Most of the studies on this topic seem to coincide with the opinion that women are more risk averse (relative to men), and this fact is attributed to biological, social, and even psychological factors (

Saad and Gill 2000;

Meier-Pesti and Penz 2008). This fact leads women executives and board members (especially in developed markets) to avoid risky projects and choose those with more secure payments or increased liquidity.

Faccio et al. (

2016) and

Weber and Zulehner (

2010) suggest that firms with female CEOs are characterized by lower leverage levels, lower earnings volatility, and higher sustainability (especially for start-up firms) (

Loukil and Yousfi 2016;

Boubaker and Nguyen 2012;

Ben-Nasr et al. 2021).

As

Cambrea et al. (

2020) argue, the issue of board gender diversity on liquidity and working capital decisions has been scarcely examined in the literature. As

Chang et al. (

2017),

Deb et al. (

2017), and

Nason and Patel (

2016) have suggested, the recent financial turmoil made clear the huge importance that liquidity and internally generated cash reserves have on the performance and sustainability of firms, while simultaneously the implementation of effective governance mechanisms acts as a safeguard assisting managers to efficiently manage corporate resources. According to

Dimitropoulos (

2020) and

Dimitropoulos and Koronios (

2021), cash-holding decisions are driven by different motives (the precautionary and transactional motives for cash holdings), which differ based on the size of the firm (SMEs versus large firms), the economic sector, and the quality of firms’ corporate governance mechanisms. Following this discussion, the apparent differences between different genders on managerial decision making and risk taking are also relevant for liquidity decisions, thus making the examination of board gender diversity on cash-holding decisions even more significant.

Based on the above discussion, gender diversity within the corporate world has been at the forefront of legislators’ agendas, specifically in the European Union (EU). The “Europe 2020 Strategy” addressed the fact that human capital is the most significant resource on the continent and stressed the balanced representation of women within business decision-making processes (

European Union 2012). EU officials argued that higher gender diversity within boards could contribute towards a more innovative, productive, and highly effective working environment. This position has been supported by several arguments and evidence from the business world that gender diversity could lead to enhanced corporate performance, better market assessment and insight, more efficient decision making, enhanced business ethics and quality of corporate governance, and better utilization of the firms’ talent pool (

European Union 2012).

Therefore, EU officials (even back in 2011) started to call for more representation of women on corporate boards and set a goal to increase the respective percentages from 30% in 2015 to 40% by 2020. Moreover, several EU member countries steadily adopted specific legislative actions for increasing the quotas of women’s representation within corporate boards of both private and state-owned companies (Germany, France, Italy, and Belgium), including specific sanctions in case of non-compliance. The Netherlands adopted similar rules without sanctions for firms failing to achieve specific quotas. Nevertheless, alongside laws and regulations, several voluntary initiatives were launched, including improvement of corporate governance codes, charters, and other firm-specific initiatives (setting voluntary targets, promoting training, networking and mentoring for women executives, etc.), which aimed to firstly recognize the positive impact of gender diversity on the corporate world and secondly to support women’s leadership potential. Efforts to date seem to have prospered since there has been a two-fold increase in the percentages of women presidents, board members, CEOs, and executives within the EU countries over the last ten years.

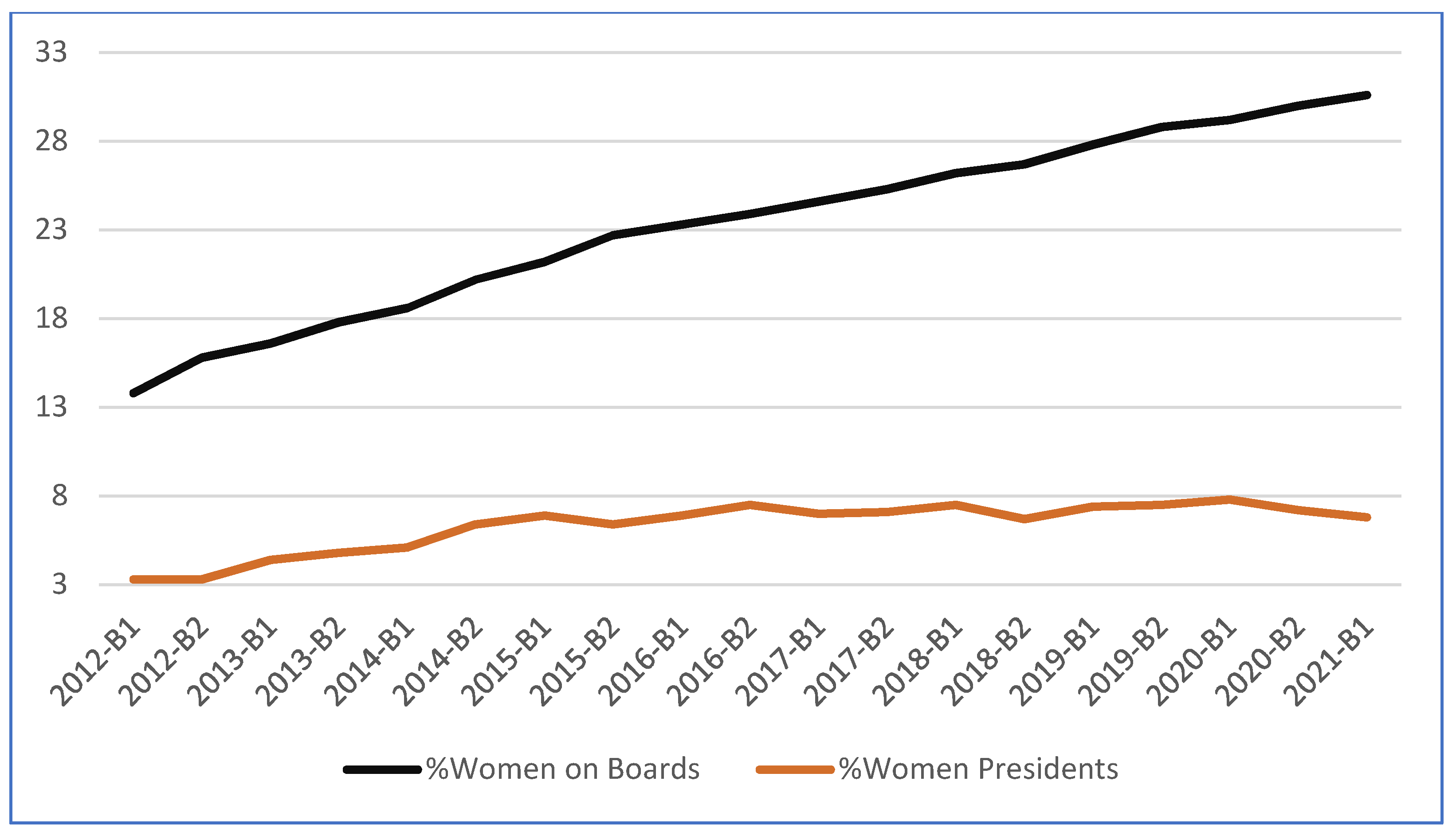

Figure 1 presents the time-series evolution of percentages of women as members on corporate boards and presidents. Data are presented semiannually from 2012 until the first semester of 2021 and are extracted from the Eurostat database. The percentage of board gender diversity has doubled from 13% in 2012 to almost 30% in 2021, suggesting that several countries in the EU have adhered to legislative quotas and replaced their board members with more women. The achieved level is below the goal of 40%; nevertheless, it constitutes a significant improvement over the examined period. Additionally, the percentage of women presidents presented a twofold increase from 3% in 2012 to 7% in 2021, despite the fact that the relative numbers are significantly smaller relative to the percentage of women board members. A similar picture is obtained from

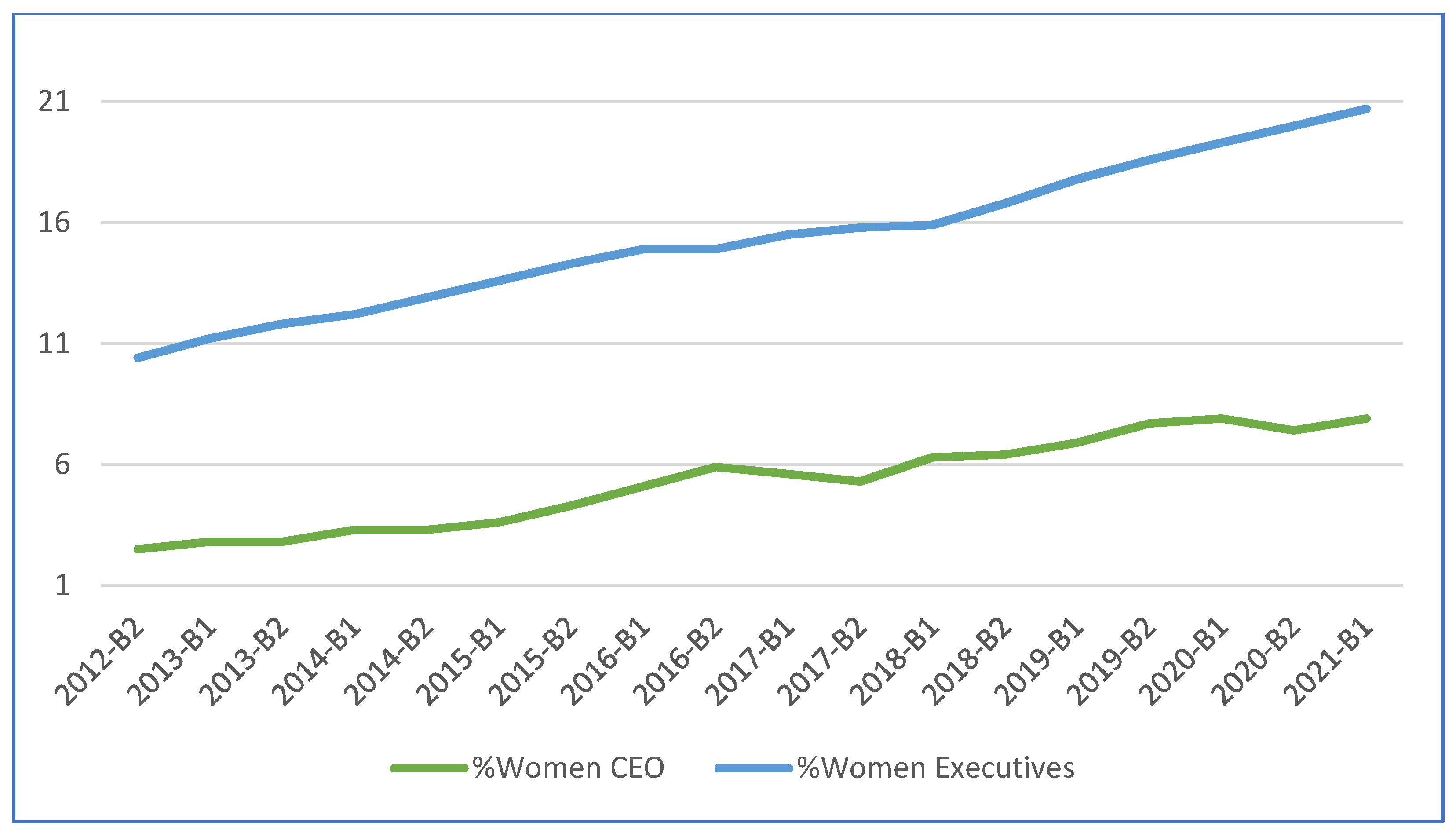

Figure 2, which indicates the evolution of women CEOs and executives in European firms. Women executive numbers are higher relative to CEOs and experienced a twofold increase from 10% to 20% over the last decade. Women CEOs comprised 7% of the population during the first semester of 2021 and still showed a significant increase from 1% back in 2012.

The sport and leisure sector is among the most vibrant and financially sound areas of the EU economy, which managed to generate almost EUR 28 billion in revenues during 2019, experiencing a growth of up to 3% within a single year (

Deloitte 2020). This market growth was attributed to a 2.5% increase in the number of clubs across EU countries and club members increased by 1.5% during the pre-pandemic year. According to

Deloitte (

2020), Europe is the second-largest sport and leisure market globally, being slightly surpassed by the US, which managed to generate EUR 28.6 billion in revenues during 2019.

According to Eurostat sports statistics for 2019, the sport and leisure sector is also a significant job creator. The annual average growth rate of employment within the sport and leisure sector during the 2014–2019 period was up to 3.1%, with the sector contributing 1.3% to the EU’s total employment. In addition, the gender distribution of persons employed in 2019 within the sector was 45.6% women and 54.4% men, indicating an equal representation of both genders.

Despite the importance of the sport and leisure sector in the European economy and the importance of gender diversity as shown by European legislators’ initiatives, the examination of gender diversity within the sport and leisure sector is in its infancy, with only a handful of studies examining this topic. According to

Laine and Vehmas (

2017), the sports economy in Europe has evolved into a significant retail and wholesale business with a crucial contribution to consumption, adding significantly to employment and economic value within the European economy. Nevertheless, this sector has received reduced attention by researchers mainly because European sport was traditionally developed around state contribution and local amateur sports clubs, but simultaneously was a multidimensional sector without being a clearly defined business field (

Laine and Vehmas 2017).

Of course, the private sports sector evolved over the years as more and more people spend a significant portion of their income on sport and recreational activities to improve their well-being and quality of life. However, academic research has left behind several merits, specifically the governance and gender diversity within this sector.

Vega et al. (

2019) examined gender diversity within the steering committees of Spanish sports federations and discovered a gender inequality among them, with only 12% of committee members being women.

Graham et al. (

2020) considered whether the hiring of women executives within NFL teams reduces incidences of employees’ misconduct. They concluded that clubs with a critical mass of women executives experienced a 33% reduction in employee arrests due to off-the-job misconduct, arguing that women in leadership positions bring benefits in terms of ethical and cultural change and decision-making diversity. The scope of this study is to extend the broader understanding of governance and financial decision making within the sport and leisure sector by examining the impact of board gender diversity on corporate cash-holding decisions and test whether a critical mass of women on the board of directors impacts the liquidity of firms within the sport and leisure sector. We respond to more calls for research made by

Laine and Vehmas (

2017) on the importance of rigorous scientific endeavor in the private sports sector, which still remains underresearched. The present study is theoretically grounded on the resource dependence theory (RDT), which postulates that firms’ survival depends on the resources brought by the board of directors, as a crucial mechanism that supports and advises the management team to efficiently utilize firm resources (

Pfeffer and Salancik 1978). According to

Terjesen et al. (

2016) and

Atif et al. (

2019), female presence on the board can create the base for efficient and high-quality decision making manifested into improved performance, fewer occurrences of financial fraud, and managerial entrenchment, facts that can impact corporate policies such as the cash-holding decisions.

This study contributes to the existing literature on gender diversity and working capital management on several merits. First, the study considers the issue of board gender diversity for cash-holding decisions within sports, a sector characterized by material growth, with a significant underrepresentation of women on the management teams (

Fink 2016;

Graham et al. 2020). Additionally, the study adds to the ongoing debate on how women executives might focus on the long-term viability and performance of the firm and so prioritize investments and decisions which can be beneficial for the performance and survival of the firm (

Wu et al. 2019). Finally, the study utilizes a large multicountry sample of European sport and leisure firms over a twelve-year period (2008–2019), thus offering more concrete and up-to-date evidence on the existing literature, contrary to previous studies on the topic that have focused on a single country setting (

Cambrea et al. 2020;

Atif et al. 2019;

Loukil and Yousfi 2016).

After analyzing a sample of 125 corporations over the period 2008–2019, empirical evidence documented that women serving on the board of directors positively impacted the level of cash holdings. This result is attributed to the critical mass theory of governance, suggesting that boards having at least two women directors on their board are associated with higher cash holdings, compared to firms with one or no women directors. Additionally, gender diversity leads to increased cash holdings for firms with lower governance quality, suggesting that women on boards perform a monitoring role within those firms with the most severe agency problems.

Section 2 discusses the theoretical background of the study and develops the research hypotheses.

Section 3 discusses the data selection procedure and the research design.

Section 4 presents the main empirical results along with the sensitivity analysis performed, while

Section 5 concludes the paper by offering useful policy implications and recommendations for future research.

2. Theoretical Background and Testable Hypotheses

Literature on the behavioral, psychological, and biological differences between men and women is quite extensive, and there is a consensus on the fact that men behave differently than women (

Matsa and Miller 2013;

La Rocca et al. 2019). Empirical evidence on the factors that explain the differences in the way men and women make decisions within the economic sphere of human activity is their different interpretations and perceptions of risk and situations involving uncertainty to a small or large extent (

Fujita et al. 1991). Specifically, men tend to be less nervous and afraid of stressful situations, making them less risk averse than women (

Arano et al. 2010;

Booth and Nolen 2012). Evidence by

Loukil and Yousfi (

2016) indicates that firms having women directors (within a sample of listed Tunisian firms) are associated with more risk avoidance, leading to increased cash reserves. Similar conclusions are provided by

Powell and Ansic (

1997), suggesting that women are more risk averse when making financial decisions. Those gender differences (especially within firms with higher levels of board gender diversity) seem to impact several dimensions of firms’ performance, such as lower cash flows, inefficient resource allocation, and profitability, but increase the chances of survival, especially during periods of financial turmoil (

La Rocca et al. 2019), relative to firms with men CEOs or board members.

The abovementioned differences have been considered by academic researchers under different theoretical lenses.

Brammer et al. (

2007) and

Hillman et al. (

2007) examined board gender diversity under the resource dependence theory (RDT) and argued that higher representation of women within corporate boards adds legitimacy to corporate activities and decisions by allowing a more stakeholder-focused managerial environment (including customers, suppliers, creditors, investors, and the general public), and even signaling enhanced career opportunities to potential employees (

Loukil and Yousfi 2016). On the contrary, agency theory stipulates that the separation of ownership and control in modern corporations increases the incidences of managerial entrenchment or conflicts of interests between principals (shareholders) and agents (CEOs and board members) (

Jensen and Meckling 1976). To reduce these agency problems, board gender diversity is considered as a mechanism that can improve monitoring and control by inserting higher diversity in terms of directors’ backgrounds, experiences, and solutions offered to operational problems.

Adams and Ferreira (

2009) documented the benefits of this diversity since female directors are more punctual in their board obligations, have higher attendance rates than men, and are more likely to participate in monitoring committees, thus performing a more effective job of reducing agency conflicts between managers and shareholders.

To be more specific, under the agency theory, the separation of ownership and control within the firm leads to excessive cash holdings because managers have the latitude on when and how to spend, leading to the extraction of private benefits and perks (

Jensen 1986). In other words, managers sustain higher levels of cash reserves so as to safeguard themselves against market frictions at the expense of shareholders (

Atif et al. 2019). One remedy to this problem is the implementation of efficient monitoring and corporate governance mechanisms, which may allow board members to scrutinize managerial behavior and reduce agency problems (

Boubaker et al. 2015). Board gender diversity is one such mechanism for monitoring cash-holding decisions, as women are more active in their roles and open to accountability relative to their male counterparts. As discussed by

Chen et al. (

2017),

Adams and Ferreira (

2009), and

Gul et al. (

2008), women on boards require higher transparency on decision-making processes and audits, making them more efficient monitors of corporate decisions.

Moreover, empirical evidence by

García Lara et al. (

2017) points to the fact that women can voluntarily reduce cash availability to executives, thus mitigating inefficient managerial activities. The positive contribution of board gender diversity on monitoring effectiveness has been corroborated by

Kang et al. (

2007),

Ozkan and Ozkan (

2004),

Srinidhi et al. (

2011), and

Cambrea et al. (

2020), where all provide evidence that women directors are more independent and have lower susceptibility to opportunistic managerial behavior and intent to ensure enhanced financial information transparency. Consequently, within gender-diverse boards, the monitoring and control functions of the board are expected to be more stringent and effective relative to male-dominant boards. Women directors may limit the opportunistic behavior of managers by exercising their power to control and reduce managerial discretion and further mitigate agency problems by limiting the levels of cash available to managers. Thus, higher board gender diversity (under the agency theory) is expected to reduce cash. Thus, based on this discussion, we form the first research hypothesis as follows:

Hypothesis 1a (H1a). Cash holdings decrease with board gender diversity.

On the contrary, considering the strand of literature that posits a different perceived behavior of women and men against risk, the association of board gender diversity and cash-holding decisions may run in the opposite direction. According to

La Rocca et al. (

2019), since risk aversion and overconfidence are determined by gender, those issues could be a determinant factor for cash-holding decisions. Since women are more risk averse relative to men, they will tend to increase cash buffers to cope with the future uncertainty of the economic environment. Thus, under these circumstances, the precautionary motive of cash holdings seems to prevail as a way to sustain the financial performance and survivorship of the firm (

Dimitropoulos et al. 2020), leading to higher cash holdings for corporations with more women serving on their boards.

Pavlia et al. (

2014),

Huang and Kisgen (

2013), and

Bernile et al. (

2018) have documented that female executives carry out less risky investment projects and tend to hold higher levels of liquidity to avoid potential negative outcomes of their decisions and to protect the survivorship of the firm when unexpected situations arise. Therefore, women in decision-making positions can set higher levels of cash reserves, allowing the firm to have the necessary latitude or flexibility to adhere to probable issues of liquidity shortages, and thus safeguard the firm from such negative incidences (

Cambrea et al. 2020;

Boubaker et al. 2014). Therefore, in the case that women on boards are more inclined to avoid risks (relative to their male counterparts), they will be in favor of holding higher levels of cash liquidity to assist the firm with coping with future adversities and even be able to fund growth opportunities during periods of restricted access to financing. Based on the abovementioned discussion, the alternative hypothesis is formed as follows:

Hypothesis 1b (H1b). Cash holdings increase with board gender diversity.

The presence of women on corporate boards was first considered by

Kanter (

1977), who perceived women on boards as a minority group where most executives negatively perceived their presence (as Kanter declares, women were considered as a “token”). This fact led to gender stereotypes, and female directors used to have minimal power and control over managerial decisions. This meant that a single woman on the corporate board had a limited impact on corporate governance quality and monitoring, without considering the negative experiences that women subsumed themselves within this environment (

Goldenhar et al. 1998;

Maass and Clark 1984).

Those initial studies provided the impetus for developing the critical mass theory, which argues that when the size of a minority group (considered as a token) rises above a specific threshold, this group is not considered a minority anymore and starts to gain significance in its role within the firm. As

Atif et al. (

2019) argue, a greater presence of women on corporate boards can contribute to a change in the relationship between the majority and minority groups, making women feel less restricted and uncomfortable to perform their duties (

Bear et al. 2010;

Peillex et al. 2021;

Boubaker et al. 2014;

Benkraiem et al. 2021).

Critical mass within corporate boards has been defined by the number of women directors serving on the board, and several studies have provided some thresholds on this number, ranging from two (2) to four (4) women on the board, depending on the relative board size. For example,

Joecks et al. (

2013) documented that a critical mass of three women on the board (or above) leads to enhanced financial performance.

Atif et al. (

2019) and

Loukil and Yousfi (

2016) found that a critical mass of females on the board is associated with lower levels of cash holdings, while

Bear et al. (

2010) provided evidence of a positive corporate reputation for firms with a critical mass of gender diversity within the board. Finally,

Schwartz-Ziv (

2017) suggested that corporate boards operate more efficiently (thus, firms have enhanced corporate governance quality) if there are at least three directors of a different gender. Consequently, following the abovementioned discussion, we can posit that the impact of board gender diversity on cash-holding decisions will be further exacerbated when a critical mass of gender diversity is achieved within the board. Thus, the final research hypothesis is formed as follows:

Hypothesis 2 (H2). The relationship between gender diversity and cash holdings is more pronounced when a critical mass is achieved.

3. Data Selection and Research Design

The study utilizes a sample of large, listed corporations operating within the sport and leisure services sector and it originates from 32 countries of the European continent over the period 2008–2019. Accounting and corporate governance data have been collected from the Datastream database. We first selected firms included in the discretionary consumer group of firms by Datastream and focused on firms providing sport and leisure services as their main activity. The second phase of the data selection process included sport and leisure firms with full coverage of environmental, social, and governance (ESG) scores provided by Datastream and had available financial data. This procedure produced a sample of 3911 firm-year observations from which we had to exclude firms without sufficient data on board gender diversity and ESG management score. All remaining firms were closing their fiscal year in December and had at least five consecutive years of full data to be included in the sample. Finally, we winsorized the upper and lower one percent of the data distribution to reduce any potential impact of outliers on the empirical analysis. Overall, we ended up with a final unbalanced sample of 793 firm-year observations and 125 unique sport and leisure firms from the Isle of Man, Austria, Bulgaria, Croatia, Cyprus, Denmark, Finland, France, Germany, Gibraltar, Greece, Hungary, Ireland, Italy, Lithuania, Luxembourg, Malta, Monaco, the Netherlands, Norway, Poland, Portugal, Romania, Russia, Slovakia, Slovenia, Spain, Sweden, Switzerland, Turkey, Ukraine, and the United Kingdom.

To test the first research hypotheses, we estimated a panel fixed-effects linear regression model, where the dependent variable was cash holdings, and the main independent variable was the number of women directors serving on the board. (

Atif et al. 2019;

Dimitropoulos 2020;

Dimitropoulos and Koronios 2021). For dealing with potential problems of omitted correlated variables, we utilized a panel fixed-effects regression analysis as in

Dimitropoulos and Koronios (

2021), including year and country fixed effects. To select between the fixed and random effect specifications, we performed the Hausman test. The test was statistically significant (producing a

p-value of 0.034), leading to the conclusion that fixed effects are the proper design for our data. The functional form of the model is provided below, where i denotes the firm, t denotes the year, and e is the error term:

The dependent variable, CASH, is estimated as the ratio of cash and cash equivalents to total assets (

Cambrea et al. 2020;

Atif et al. 2019;

Dimitropoulos and Koronios 2021). DIV_BD captures board gender diversity and is defined as the number of female directors serving on the board, as in

Atif et al. (

2019) and

Cambrea et al. (

2020). If agency theory is valid, we expect a negative and significant coefficient on DIV_BD, while, on the contrary, a positive coefficient will verify the risk-aversion hypothesis and the precautionary motive for cash holdings.

We also included several control variables that previous research has indicated are significant determinants of cash-holding decisions (

Dimitropoulos et al. 2020;

Dimitropoulos and Koronios 2021;

Chang et al. 2019;

Kim et al. 2013). First, the variable SIZE is the natural logarithm of total assets, capturing the firm’s size. Smaller firms have restricted access to financial markets because they are more likely to default. On the contrary, larger firms are expected to hold less cash; thus, a negative coefficient is expected on the SIZE variable. LEV is firm leverage measured as total debt to total assets. Less leveraged firms may face more information asymmetries, leading to reduced opportunities to access capital markets, and thus they need to hold more cash (

Dimitropoulos and Koronios 2021). The following control variable is net working capital (NWC), measured as (inventories + debtors − creditors)/total assets. According to

Dimitropoulos (

2020) and

Dimitropoulos et al. (

2020), firms with fewer liquid assets need more cash. Therefore, firms with higher NWC tend to have less cash on their balance sheet.

Asset tangibility (TANG) is the next control variable, estimated as fixed assets to total assets. Firms with less tangible assets cannot raise funds at a low cost within financial markets because they lack the necessary collateral, which increases their cost of borrowing. In other words, firms with more fixed assets do not need more cash holdings to support their operations. Moreover, firm profitability (ROA) and growth opportunities (GROWTH) are expected to positively impact cash holdings since high-growth and profitable firms are more able to retain earnings and generate higher cash amounts relative to less profitable and slower-growing firms. In addition, firms with a lower ability to create operating cash flows (CFO) are expected to require external financing.

Kim et al. (

2013) and

Dimitropoulos et al. (

2020) document that firms with lower cash flows tend to hold more cash on their balance sheets.

Additionally, we controlled for the existence of golden parachutes (GOLD_PAR) as a mechanism for controlling free cash flow problems in the firm. According to

Subramaniam and Daley (

2000), golden parachutes are contracts that guarantee the continuation of managers’ compensation if a change in the firm control occurs. Firms with free cash flow problems (usually from higher cash holdings) tend to sign such contracts with their executives. Consequently, a positive coefficient is expected on GOLD_PAR, indicating that executives with such guaranteed contracts tend to increase their cash availability, which may further support their overinvestment behavior.

The last control variable is audit committee expertise, measured as the percentage of the audit committee members with CEO expertise (AUD_COM). The literature provides two competing views on the impact of audit committee expertise on cash-holding decisions. The first argues that higher levels of expertise lead to a reduction in free cash flow problems (due to improved monitoring) and thus a higher value for cash holdings. On the contrary, the free cash flow problem may be exacerbated by more experts on the audit committee, as extra members on the committee with CEO expertise do not yield ample benefits for monitoring and control efficiency (

Choi et al. 2020). Thus, based on the contradictory findings in the literature, we cannot infer any expectation regarding the sign of that variable.

Finally, to examine the second research hypothesis (critical mass theory), Model (1) was re-estimated after separating the sample firms among those with a critical mass of female directors on the board and those without such a characteristic. Following

Atif et al. (

2019) and

Loukil and Yousfi (

2016), we distinguished firms with at least two (2) female directors on the board as having a critical mass of gender diversity. The median of the DIV_BD variable was equal to two (2), so we selected this number as the required threshold. The results remained similar after changing the definition of the critical mass of diversity to at least three women directors on the board. Thus, the main findings presented in the following tables refer to at least two female directors as the indicator of a critical mass.

4. Empirical Results

Table 1 presents the descriptive statistics of the sample variables. Cash and cash equivalents comprise ten percent of the firms’ assets, which is somewhat similar to other studies in the US (

Atif et al. 2019) and Europe (

Dimitropoulos and Koronios 2021). Board gender diversity has an average of 2.44 (median equals 2), indicating that, on average, two (2) women serve on the sample firms’ boards, with a minimum value of zero and a maximum value of nine women on the board. This number is higher compared to that in the study by

Atif et al. (

2019) on a sample of S&P 1500 firms, which was 1.29, indicating that European firms exercise board gender diversity to a higher extent compared to US firms. Moreover, sport and leisure firms in Europe are characterized by increased tangibility (average TANG up to fifty-nine percent) and leverage (average debt comprises fifty-seven percent of total assets), while they present negative growth opportunities (−0.78), networking capital (−0.002), and profitability levels, which are close to zero but positive on average. Finally, thirty-eight percent of our sample firms have signed a golden parachute agreement with the CEO, and the majority of the audit committee members (0.85) have CEO expertise, which suggests increased monitoring ability on managerial activities.

Table 2 presents the descriptive statistics of the same variables after separating the sample firms between those with at least two female directors on the board and those with one or no female director as a board member (critical mass theory). The last column presents the difference between the two group averages and the

p-value, indicating whether the difference is statistically significant. As we can see, firms with a critical mass of women on the board (at least two female members) hold more cash on their balance sheets. This is an early indication of the potential impact of a critical mass of gender diversity on cash-holding decisions (corroborating Hypothesis 2). Moreover, firms with at least two women on the board are larger, employ audit committee members with higher expertise, and have lower tangibility and growth opportunities relative to their no-critical mass counterparts.

Table 3 presents the Pearson correlation coefficients of the sample variables. Cash and cash equivalents are positively but statistically insignificantly correlated with boarding gender diversity. CASH_TA presents a negative correlation with SIZE, LEV, TANG, GROWTH, and GOLD_PAR, suggesting that larger, more leveraged firms, with more fixed assets, growth opportunities, and golden parachute contracts, hold less cash on their balance sheet. On the contrary, firms with higher cash flows, profits, and net working capital are positively correlated with the level of cash on their balance sheet. All correlation coefficients are below the threshold of 0.60, and the variance inflation factors (VIFs) for the sample variables were below the threshold of five, verifying that multicollinearity is not present in the data. However, since the correlation does not indicate causation, we proceed with the regression analysis of Model (1).

Table 4 presents the empirical results from the estimation of Model (1) using panel fixed-effects estimation. The regression

F-stat is highly significant, and the overall R

2 (0.296) is satisfactory for this type of analysis considering the variability in our sample firms within several countries. The variable of interest (DIV_BD) produced a positive and highly significant coefficient (0.008), suggesting that firms with an increased number of female directors on the board hold more cash on their balance sheets. This result supports

H1b and suggests that female executives within sport and leisure firms carry out less risky investment projects and hold higher levels of liquidity to avoid potentially negative outcomes of their decisions and protect the survivorship of the firm. Consequently, women in decision-making positions can set higher cash reserve levels, allowing the firm to have the required flexibility to adhere to probable issues of liquidity shortages and safeguard the firm from such negative incidences. This result corroborates previous evidence in the literature (

Cambrea et al. 2020;

Pavlia et al. 2014;

Huang and Kisgen 2013;

Bernile et al. 2018) mentioning the prevalence of the precautionary motive of cash holdings for sustaining the financial performance and survivorship of the firm. For example,

Cambrea et al. (

2020) indicate that firms with female CEOs in Italy are associated with higher cash holdings.

Regarding the rest of the control variables, SIZE produced a negative and significant coefficient as expected, suggesting that larger firms tend to hold less cash on their balance sheet because they have easier access to the financial markets if they need to finance their activities and projects. Additionally, firms with more fixed assets (−0.339), profitability (−0.033), and growth opportunities (−0.001) tend to hold less cash on their balance sheet. Finally, firms with higher net working capital hold more cash on their balance sheet (0.068), suggesting that the precautionary motive of cash holding prevails within the sport and leisure sector.

Table 5 presents the empirical results from the estimation of Model (1) after separating the sample firms between those with at least two women directors on the board and those with one or no women directors. The critical mass theory (according to H2) argues that the enhanced presence of women on corporate boards can contribute to a change in the relationship between the majority and minority groups, making women feel less restricted and uncomfortable to perform their duties (

Bear et al. 2010). Results in

Table 4 verify our second research hypothesis since the coefficient of DIV_BD is only positive and statistically significant (0.008) for the group of firms with at least two women directors on the board. This finding corroborates evidence by

Bear et al. (

2010) and

Schwartz-Ziv (

2017), indicating that a critical mass of gender diversity within the board allows boards to operate more efficiently and be proactive in holding higher cash reserves as a way to supersede financial difficulties and allow the firm to finance daily operations with its own means. Similar results are provided by

Atif et al. (

2019) who examined S&P 1500 listed firms in the US capital market.

The rest of the control variables were similar to

Table 4; operating cash flows (CFO) and golden parachutes (GOLD_PAR) only produced positive and statistically significant coefficients for firms without a critical mass of gender diversity. These results suggest that firms with a higher ability to generate operating cash flows (CFO) are fueling their cash reserves for precautionary reasons. Additionally, sport and leisure firms with golden parachute contracts tend to have free cash flow problems, leading them to increase the level of cash on their balance sheet.

To check the robustness of the main findings, several sensitivity tests were performed. First, the quality of corporate governance was considered as a factor that can impact the association between board gender diversity and cash-holding decisions. As argued by

Atif et al. (

2019) and

Cambrea et al. (

2021), managers can use the cash reserves of the firm in a discretionary manner and even channel funds to negative NPV projects at the expense of the shareholders. In this case, an effective corporate governance structure can help mitigate such behavior and reduce agency conflicts.

Dittmar and Mahrt-Smith (

2007) documented that firms with weak governance mechanisms and increased cash reserves tend to spend cash faster than firms with sufficient governance mechanisms. For this reason, the sample firms were separated based on the median value of Datastream’s ESG Management score. The management score ranges from one (1) to twelve (12) and measures a company’s commitment and effectiveness to implement the best corporate governance principles. The higher the score, the higher the quality of a firm’s corporate governance. Firms with an annual score above the sample median are considered high governance quality firms and vice versa. Model (1) was re-estimated for each sub-group, and the results are presented in

Table 6.

As we can see, the DIV_BD variable only produced a positive and significant coefficient (0.005) for the low governance quality firms. For the high governance quality firms, the coefficient is positive yet insignificant within conventional levels. This result suggests that within firms with more intense agency problems (due to inefficient governance quality), gender diversity enhances the precautionary motive of cash, leading to higher cash reserve levels and allowing the firm to have the required flexibility to adhere to probable issues of liquidity shortages, and thus safeguard the firm from such negative incidences.

Furthermore, we controlled for the potential impact of endogeneity on our data following the work by

Cambrea et al. (

2020) and

Atif et al. (

2019) by utilizing three methods, the 2SLS, GMM, and PSM processes. Since both the number of female directors on the board and the level of cash reserves are endogenously determined by the firm, a 2SLS procedure was employed by using the country level of gender equality index produced by the European Institute for Gender Equality (EIGE) and the ratio of female-to-male participation on the labor force for each country in the sample as the instruments on the first stage regression. Second-stage regression (Model (1)) was re-estimated using the fitted values from the first stage instead of the DIV_BD variable. To check the validity of the instruments, the AR(1) and AR(2) tests were performed, which rejected the null hypothesis, suggesting that the instruments are valid for our research setting. Moreover, the Hansen

J-statistic of overidentifying restrictions was insignificant within conventional levels, suggesting that the instruments were completely exogenous. Furthermore, we utilized the generalized method of moments as an additional instrumental variables approach following

Dimitropoulos and Koronios (

2021) instead of 2SLS. GMM is a more general method allowing us to estimate efficient and consistent estimators in the case of non-identically and independently distributed errors. For GMM, we utilized the same instruments as in the 2SLS procedure. Finally, we implemented propensity score matching (PSM) estimation to examine whether differences in cash levels depend on the presence of women directors on the board. Following

Atif et al. (

2019), we created a dummy variable (D_WOMAN) receiving (1) if one or more women are serving on the board and (0) otherwise; those firms receiving (1) are treated as the treatment group, and firms without female board members are treated as the control group. Firstly, we estimated a logistic regression with D_WOMAN as the dependent variable on the size of the board of directors, the percentage of independent members on the board, and the existence of CEO duality, using the predicted values as the propensity score for every firm-year observation. Secondly, we used the propensity scores to create pairs of D_WOMAN firm-year observations so that any difference in the cash ratio between the two groups could be attributed to differences in the number of female directors on the board and not to independent variables (

Atif et al. 2019).

The results from the estimations of the GMM and 2SLS regression are presented in

Table 7 and indicate that both instruments (EIGE and FEM_RATIO) produced statistically significant coefficients, suggesting that firms operating in countries with a higher gender equality index and female participation in the labor force tend to hire more women directors on the board. Looking at the main variable of interest (DIV_BD

fit), the fitted values of DIV_BD in the second stage regression produced a positive and highly significant coefficient, thus verifying the results presented in

Table 4. We obtained similar results from the PSM estimation provided in

Table 8; thus, there is confidence that the main fixed-effect results in

Table 4 were unaffected by endogeneity.

Furthermore, following previous arguments in the literature regarding the positive or negative impact of cash holdings on firm value, we considered the issue of marginal cash holdings on firms’ stock return and whether board gender diversity moderates that relation. Following

Opler et al. (

1999),

Faulkender and Wang (

2006), and

Choi et al. (

2020), we estimated the impact of gender diversity on the marginal value of cash holdings, and if those two are value relevant, by employing the following panel fixed-effect model:

where R is the portfolio adjusted stock returns based on firm size and book-to-market ratio, ΔC is the annual change in cash and cash equivalents, C is lagged cash, and D_WOMAN is a dummy receiving (1) if there is at least one woman serving on the board and (0) otherwise. All cash variables are deflated by the lagged market value of equity, as in

Choi et al. (

2020). Coefficient β

1 indicates the reaction of the stock market to unexpected changes in cash holdings within the year. Coefficient β

3 indicates the marginal value of cash holdings for firms with at least one woman director on the board. If the board gender diversity improves the monitoring of managerial decisions, etc., and it improves the marginal value of cash, coefficient β

3 will be positive and significant. The results from the estimation of Model (2) are presented in

Table 9.

As we can see, the change in cash (ΔC) has a positive and significant coefficient, suggesting that investors value an extra euro of cash at EUR 0.38. This result is also similar to those presented by

Choi et al. (

2020) and

Faulkender and Wang (

2006), suggesting that cash holdings exert benefits for the firms since they are positively appraised by market participants. The interaction term of D_WOMAN × ΔC produced a positive and statistically significant coefficient, indicating that investors are discounting the value of positive changes of cash holdings for firms having boards with at least one woman director. This means that board gender diversity improves the monitoring ability of the board, corroborating our second research hypothesis and evidence in the literature arguing for the benefits of cash holdings for dealing with market uncertainties.

Furthermore, because the level of cash holdings could incorporate not only cash needs for normal activities but also excess cash beyond that justified by casual operations, we distinguished the level of normal and excess cash holdings and examined the impact of gender diversity on excess cash holdings as in

Opler et al. (

1999) and

Choi et al. (

2020). For this reason, we regressed the natural logarithm of the ratio of cash to non-cash assets on firm size, free cash flow, net working capital, and market-to-book ratio and extracted the residuals of that regression as our measure of excess cash. Then, we replaced the dependent variable of Model (1) with the excess cash measure from the previous process and re-estimated Model (1). The relative results are presented in

Table 10 and indicate a positive and significant coefficient on the DIV_BD variable (0.011, significant at the one percent significance level), corroborating evidence in

Table 4 and verifying the precautionary motive of cash holdings for sport and leisure firms with enhanced board gender diversity.

Moreover, following

Atif et al. (

2019), we controlled for the potential impact of the level of cash holdings relative to the annual average as a flag of potential agency problems. Thus, we separated firms based on the country’s annual average CASH ratio, and those firms with CASH above the country’s annual average were considered as entrenched and vice versa. The results (untabulated) were similar to those in

Table 4 and indicate that the impact of board gender diversity remained positive and significant across the two sub-groups. Finally, following

Dimitropoulos and Koronios (

2021), Model (1) was re-estimated after changing the definitions of some control variables. Specifically, LEV was re-estimated as the ratio of long-term debt to total assets, GROWTH as the ratio of market value to book value of equity (MV/BV), and ROA was replaced by ROE, but the results remained similar after these alterations.

5. Conclusions

Board gender diversity has been at the forefront of regulators and practitioners’ agendas for over two decades. The “Europe 2020 Strategy” addressed the fact that human capital is the most significant resource on the continent and urged the balanced representation of women within business decision-making processes (

European Union 2012). Additionally, securities and exchange commissions within the EU have made proposals for gender quotas within listed firms’ boards and argued that higher gender diversity within boards could contribute towards a more innovative, productive, and highly effective working environment.

Under the resource dependence theory (RDT), the current study aimed to examine the impact of board gender diversity on corporate cash-holding decisions and test whether a critical mass of women on the board of directors impacts the liquidity of firms within the sport and leisure sector. The sport and leisure sector is among the most important areas of the European economy, with a significant contribution to employment and revenue generation (

Deloitte 2020). This study is the first that considers the issue of board gender diversity on working capital management within sports, a sector that is perceived as a growing industry with a significant underrepresentation of women on the management teams (

Fink 2016;

Graham et al. 2020).

The empirical analysis included data selected from 125 unique firms from 2008 to 2019 and was performed using panel fixed-effects regressions. Empirical evidence documented a positive association between the number of women serving on the board of directors and the level of cash holdings. This result is attributed to the critical mass theory of governance, suggesting that boards having at least two women directors are associated with higher cash holdings compared to firms with one or no women directors on the board. Additionally, gender diversity leads to increased cash holdings for firms with lower governance quality, suggesting that women on boards mitigate agency issues within those firms with the lowest monitoring quality and improve corporate monitoring and control. This fact is also positively valued by market participants since firms with higher representation of women on the board are associated with higher stock returns if they hold more cash on their balance sheets. The results remain robust after several sensitivity tests controlling for potential endogeneity among the variables and the functional form of the main model.

This study has important implications for managers, investors, and regulators. First, we contribute to the ongoing discussion on the association between female presence in the boardroom and cash policies by establishing a significant association of gender diversity on cash reserves under different levels of governance quality. Consequently, increased female representation on the board can lead to the efficient decision-making ability of the firm. This can further contribute to enhanced managerial decisions contributing towards reduced liquidity risk and improving firms’ survival. This fact is also useful for regulators to communicate further the benefits of gender diversity in modern corporations and offer leadership courses and guidance for women wanting to excel within managerial and executive positions. The recent legislative efforts made by the EU to insert quotas on the participation of female directors on corporate boards (mainly for listed corporations) is an initial process for enhancing the representation of women, but we must move beyond that stage and develop alternative paths (beyond legislation) which can be more participative and voluntary (not mandatorily enforceable), and thus more efficient at achieving the goal of enhanced diversity within the boardroom.

Additionally, this study provides useful implications for managers and practitioners since the board’s composition can have important implications for decision-making efficiency. This study can provide the impetus to managers for considering board structure and diversity as an additional feature that can improve the monitoring role of the board and enhance its managerial decision ability, with positive repercussions on firms’ stock returns and valuation. Finally, the findings of this study could prove useful to investors and creditors. Since improved liquidity is a valuable feature for sustaining the ability of the firm to pay overdue liabilities and finance daily activities, investing within firms with higher gender diversity on the board can provide additional guarantees to key stakeholders (creditors, customers, lenders, and even the state). In turn, this will allow the firm to remain viable and even expand in the future.

Nevertheless, the study does not come without shortcomings, which, of course, create opportunities for future research. The study is focused on a single sector, making the generalizability of the main findings to other sectors of the economy difficult. Thus, the extension of this study to other sectors (especially services sectors) can provide more concrete evidence on the impact of gender diversity on cash-holding decisions. Even though we controlled for the quality of governance (via the management score), we did not consider other governance mechanisms, including CEO compensation schemes and ownership structure characteristics which can also moderate the relationship among cash reserves and gender diversity. Future research can provide answers to those issues. Finally, the sample (even though it comprised several European countries) was focused on large, listed corporations. Future research can examine gender diversity and working capital management within small and medium-sized firms within the sport and leisure sector, as SMEs need to efficiently manage their cash reserves because they face more restrictions in accessing financing sources (

Dimitropoulos et al. 2020).

{kind=link}

{kind=link}