Exchange Rate Crisis among Inflation Targeting Countries in Sub-Saharan Africa

Abstract

:1. Introduction

2. Literature Review

2.1. Exchange Rate Crisis

2.2. Dealing with Exchange Rate Crisis

2.3. Inflation Targeting (IT) Framework as a Cure to Exchange Rate Crisis

2.4. Measuring Pressure on the Exchange Rate, Possibly Leading to an Exchange Rate Crisis

2.5. Research Gap

3. Materials and Methods

3.1. Materials

3.2. Methodology

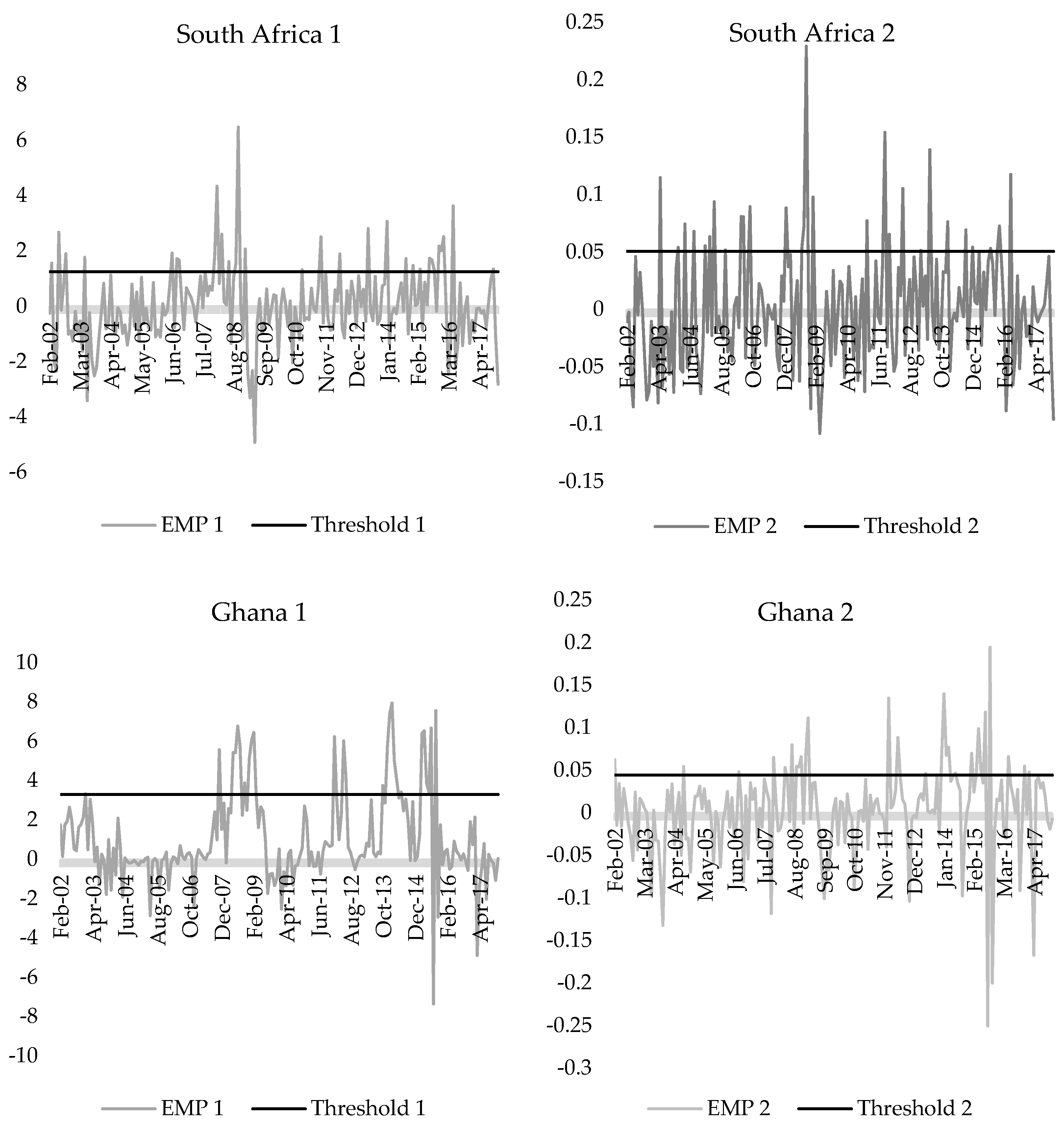

4. Results and Discussion

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| DLNFX | EMP_1 | EMP_2 | EMP_3 | EMP_4 | EMP_5 | |

|---|---|---|---|---|---|---|

| DLNFX | 1 | 0.8501 | 0.9971 | 0.9102 | 0.7268 | 0.7458 |

| EMP_1 | 0.8501 | 1 | 0.8522 | 0.7903 | 0.9264 | 0.6784 |

| EMP_2 | 0.9971 | 0.8522 | 1 | 0.9333 | 0.7346 | 0.7854 |

| EMP_3 | 0.9102 | 0.7903 | 0.9333 | 1 | 0.7133 | 0.9224 |

| EMP_4 | 0.7268 | 0.9264 | 0.7346 | 0.7133 | 1 | 0.6029 |

| EMP_5 | 0.7458 | 0.6784 | 0.7854 | 0.9224 | 0.6029 | 1 |

| DLNFX | EMP_1 | EMP_2 | EMP_3 | EMP_4 | EMP_5 | |

|---|---|---|---|---|---|---|

| DLNFX | 1 | 0.7942 | 0.7233 | 0.5010 | 0.5677 | 0.7821 |

| EMP_1 | 0.7942 | 1 | 0.6139 | 0.4383 | 0.7623 | 0.7970 |

| EMP_2 | 0.7233 | 0.6139 | 1 | 0.9401 | 0.8042 | 0.9326 |

| EMP_3 | 0.5010 | 0.4383 | 0.9401 | 1 | 0.7625 | 0.8328 |

| EMP_4 | 0.5677 | 0.7623 | 0.8042 | 0.7625 | 1 | 0.7974 |

| EMP_5 | 0.7821 | 0.7970 | 0.9326 | 0.8328 | 0.7974 | 1 |

| South Africa | Ghana | |||||

|---|---|---|---|---|---|---|

| AIC | SIC | HQIC | AIC | SIC | HQIC | |

| EMP_1 | −4.4862 | −4.4521 | −4.4724 | −5.3152 | −5.2811 | −5.3014 |

| EMP_2 | −8.3527 | −8.3187 | −8.3389 | −5.0596 | −5.0255 | −5.0458 |

| EMP_3 | −4.9669 | −4.9328 | −4.9531 | −4.6080 | −4.5740 | −4.5942 |

| EMP_4 | −3.9551 | −3.9210 | −3.9413 | −4.7080 | −4.6739 | −4.6942 |

| EMP_5 | −4.0164 | −3.9823 | −4.0026 | −5.2651 | −5.2310 | −5.2513 |

| South Africa | Ghana | |||

|---|---|---|---|---|

| EMP_1 | EMP_2 | EMP_1 | EMP_2 | |

| Variable chosen | EMP_1(-11) | EMP_2(-7) | EMP_1(-5) | EMP_2(-5) |

| Estimated number of thresholds | 5 | 5 | 5 | 5 |

| Threshold value used | 1.245 | 0.051 | 3.292 | 0.044 |

| R-squared | 0.571 | 0.400 | 0.639 | 0.476 |

| Adjusted R-squared | 0.320 | 0.145 | 0.428 | 0.253 |

| Jarque–Bera Normality Test | 1.455 | 0.875 | 154.932 | 173.943 |

| Probability | 0.483 | 0.646 | 0.000 | 0.000 |

| Breusch–Godfrey Serial Correlation LM Test | ||||

| F-statistic (Prob.) | 0.880 | 0.926 | 0.673 | 0.511 |

| Obs*R-squared (Prob) | 0.813 | 0.894 | 0.527 | 0.379 |

| Heteroskedasticity Test: Breusch–Pagan–Godfrey | ||||

| F-statistic (Prob.) | 0.102 | 0.068 | 0.969 | 0.855 |

| Obs*R-squared (Prob) | 0.146 | 0.101 | 0.931 | 0.801 |

References

- Bai, Jushan, and Pierre Perron. 2003. Computation and analysis of multiple structural change models. Journal of Applied Econometrics 18: 1–22. [Google Scholar] [CrossRef] [Green Version]

- Bain, Keith, and Peter Howells. 2003. Monetary Economics—Policy and Its Theoretical Basis. London: Palgrave. [Google Scholar]

- Bank of England, Monetary Policy Committee. 1999. The Transmission Mechanism of Monetary Policy. Available online: http://www.bankofengland.co.uk/publications/other/monetary/montrans.pdf (accessed on 14 September 2021).

- Baqueiro, Armando, Alejandro Diaz, and Alberto Torres. 2003. Fear of floating or fear of inflation? The role of the exchange rate pass-through. BIS Papers 19: 338–54. [Google Scholar]

- Berg, Andrew, Stephen O’Connell, Catherine Pattillo, Rafael Portillo, and Filiz Unsal. 2015. Monetary Policy Issues in Sub-Saharan Africa. Oxford: Oxford University Press, pp. 62–87. [Google Scholar]

- Bertoli, Simone, Giampiero Gallo, and Giorgio Ricchiuti. 2010. Exchange market pressure: Some caveats in empirical applications. Applied Economics 42: 2435–448. [Google Scholar] [CrossRef]

- Calvo, Guillermo Antonio, and Carmen Reinhart. 2002. Fear of floating. The Quarterly Journal of Economics 117: 379–408. [Google Scholar] [CrossRef]

- Cavdar, Seyma Caliskan, and Alev Dilek Aydin. 2015. An empirical analysis for the prediction of a financial crisis in turkey through the use of forecast error measures. Journal of Risk and Financial Management 8: 337–54. [Google Scholar] [CrossRef]

- Devereux, Michael, and Charles Engel. 2003. Monetary policy in the open economy revisited: Price setting and exchange-rate flexibility. The Review of Economic Studies 70: 765–83. [Google Scholar] [CrossRef]

- Devereux, Michael, Philip Richard Lane, and Juanyi Xu. 2006. Exchange rates and monetary policy in emerging market economies. The Economic Journal 116: 478–506. [Google Scholar] [CrossRef] [Green Version]

- Dornbusch, Rudiger. 1976. Expectations and exchange rate dynamics. Journal of political Economy 84: 1161–76. [Google Scholar] [CrossRef]

- Driver, Rebecca, and Peter Westaway. 2004. Concepts of equilibrium exchange rates. Bank of England Working Paper 248: 64. [Google Scholar]

- Eichenbaum, Martin, Benjamin Kramer Johannsen, and Sergio Rebelo. 2017. Monetary Policy and the Predictability of Nominal Exchange Rates (No. w23158). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Eichengreen, Berry, Andrew Kenan Rose, and Charles Wyplosz. 1994. Speculative Attacks on Pegged Exchange Rates: An Empirical Exploration with Special Reference to the European Monetary System (No. w4898). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Eichengreen, Berry, Andrew Kenan Rose, and Charles Wyplosz. 1996. Contagious Currency Crises (No. w5681). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Fiador, Vera Ogeh, and Nicholas Biekpe. 2015. Monetary policy and exchange market pressure–Evidence from sub-Saharan Africa. Applied Economics 47: 3921–37. [Google Scholar] [CrossRef]

- Fischer, Stanley. 2001. Exchange rate regimes: Is the bipolar view correct? Journal of Economic Perspectives 15: 3–24. [Google Scholar] [CrossRef] [Green Version]

- Fratzscher, Marcel. 2009. What explains global exchange rate movements during the financial crisis? Journal of International Money and Finance 28: 1390–407. [Google Scholar] [CrossRef] [Green Version]

- Frenkel, Jacob Aharon, and Richard Levich. 1975. Covered interest arbitrage: Unexploited profits? Journal of Political Economy 83: 325–38. [Google Scholar] [CrossRef]

- Friedman, Milton. 1953. The case for flexible exchange rates. Essays in Positive Economics 157: 203. [Google Scholar]

- Gali, Jordi, and Tommaso Monacelli. 2005. Monetary policy and exchange rate volatility in a small open economy. The Review of Economic Studies 72: 707–34. [Google Scholar] [CrossRef]

- Girton, Lance, and Don Roper. 1977. A monetary model of exchange market pressure applied to the postwar Canadian experience. The American Economic Review 67: 537–48. [Google Scholar]

- Goldfajn, IIan, and Poonam Gupta. 2003. Does monetary policy stabilize the exchange rate following a currency crisis? IMF Staff Papers 50: 90–114. [Google Scholar]

- Győri, Zsuzsanna, and Borbala Benedek. 2021. Stakeholders and opportunities of debt settlement as a values-based banking activity in Hungary. Social Responsibility Journal. [Google Scholar] [CrossRef]

- Hansen, Bruce. 2000. Testing for structural change in conditional models. Journal of Econometrics 97: 93–115. [Google Scholar] [CrossRef] [Green Version]

- Hegerty, Scott. 2018. Exchange market pressure, stock prices, and commodity prices east of the Euro. Journal of Economics & Management 31: 74–94. [Google Scholar]

- Hossfeld, Oliver, and Marcus Pramor. 2018. Global Liquidity and Exchange Market Pressure in Emerging Market Economies (No. 05/2018). Frankfurt: Deutsche Bundesbank. [Google Scholar]

- IMF. 2015. Ghana: First Review under the Extended Credit Facility Arrangement and Request for Waiver and Modifications of Performance Criteria. Washington, DC: Press Release, Staff Report and Statement by the Executive Director for Ghana. [Google Scholar]

- IMF. 2018. Ghana: Fifth and Sixth Reviews Under the Extended Credit Facility, Request for Waivers for Nonobservance of Performance Criteria, and Request for Modification of Performance Criteria. Washington, DC: Press Release, Staff Report and Statement by the Executive Director for Ghana. [Google Scholar]

- IMF. 2021. Annual Report on Exchange Arrangements and Exchange Restrictions 2020. Washington, DC: International Monetary Fund, Available online: https://www.elibrary.imf.org/view/books/012/29310-9781513556567-en/29310-9781513556567-en-book.xml (accessed on 19 October 2021).

- Kaminsky, Graciela Laura, and Carmen Reinhart. 1999. The twin crises: The causes of banking and balance-of-payments problems. American Economic Review 89: 473–500. [Google Scholar] [CrossRef] [Green Version]

- Kim, Soyoung, and Kuntae Lim. 2018. Effects of monetary policy shocks on exchange rate in small open Economies. Journal of Macroeconomics 56: 324–39. [Google Scholar] [CrossRef]

- Knedlik, Tobias. 2006. Signaling Currency Crises in South Africa (No. 19/2006). Toronto: IWH Discussion Papers. [Google Scholar]

- Kouri, Pentti Juka. 1976. The exchange rate and the balance of payments in the short run and in the long run: A monetary approach. Skandinavian Journal of Economics 78: 280–304. [Google Scholar] [CrossRef]

- Krugman, Paul. 1979. A model of balance-of-payments crises. Journal of Money, Credit and Banking 11: 311–25. [Google Scholar] [CrossRef]

- Krušković, Borivoje. 2017. Exchange rate and interest rate in the monetary policy reaction function. Journal of Central Banking Theory and Practice 6: 55–86. [Google Scholar] [CrossRef] [Green Version]

- Latter, Tony. 1996. The Choice of Exchange Rate Regime. Bank of England, Handbooks in Central Banking, No. 2. p. 29. Available online: https://econpapers.repec.org/bookchap/ccbhbooks/2.htm (accessed on 3 February 2022).

- López-Villavicencio, Antonia, and Valerie Mignon. 2017. Exchange rate pass-through in emerging countries: Do the inflation environment, monetary policy regime and central bank behavior matter? Journal of International Money and Finance 79: 20–38. [Google Scholar] [CrossRef]

- Madhou, Ashwin, Tayushma Sewak, Imad Moosa, Vikash Ramiah, and Florian Gerth. 2021. Towards Full-Fledged Inflation Targeting Monetary Policy Regime in Mauritius. Journal of Risk and Financial Management 14: 126. [Google Scholar] [CrossRef]

- Mminele, Daniel. 2013. Note on the Foreign Exchange Market Operations of the South African Reserve Bank. BIS Paper. Reserve Bank, (73x). Available online: https://econpapers.repec.org/bookchap/bisbisbpc/73-24.htm (accessed on 3 February 2022).

- Nakatani, Ryota. 2018. Real and financial shocks, exchange rate regimes and the probability of a currency crisis. Journal of Policy Modeling 40: 60–73. [Google Scholar] [CrossRef] [Green Version]

- Obstfeld, Maurice, and Kenneth Rogoff. 1995. The mirage of fixed exchange rates. Journal of Economic Perspectives 9: 73–96. [Google Scholar] [CrossRef] [Green Version]

- Pentecost, Eric John. 1993. The portfolio balance approach. In Pentecost, E. J. Exchange Rate Dynamics. A Modern Analysis of Exchange Rate Theory and Evidence. Cambridge: Edward Elgar, chp. 7. [Google Scholar]

- Pontines, Victor, and Reza Siregar. 2008. Fundamental pitfalls of exchange market pressure-based approaches to identification of currency crises. International Review of Economics & Finance 17: 345–65. [Google Scholar]

- Sachs, Jeffry, Aaron Tornell, and Andres Velasco. 1996. Financial Crises in Emerging Markets: The Lessons from 1995 (No. w5576). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Saikkonen, Pentti. 1991. Asymptotically efficient estimation of cointegration regressions. Econometric Theory 7: 1–21. [Google Scholar] [CrossRef]

- Salant, Stephen Walter, and Dale William Henderson. 1978. Market anticipations of government policies and the price of gold. Journal of Political Economy 86: 627–48. [Google Scholar] [CrossRef]

- Soe, Than Than, and Makoto Kakinaka. 2018. Inflation targeting and exchange market pressure in developing economies: Some international evidence. Finance Research Letters 24: 263–72. [Google Scholar] [CrossRef]

- Stavarek, Daniel. 2010. Exchange market pressure and de facto exchange rate regime in the euro-candidates. Romanian Journal of Economic Forecasting 13: 119–39. [Google Scholar]

- Stock, James Harold, and Mark Watson. 1993. A simple estimator of cointegrating vectors in higher order integrated systems. Econometrica: Journal of the Econometric Society 61: 783–820. [Google Scholar] [CrossRef]

- Taylor, John Brian. 2001. The role of the exchange rate in monetary-policy rules. American Economic Review 91: 263–67. [Google Scholar] [CrossRef] [Green Version]

| Variables | Data Source | Data Time Period |

|---|---|---|

| Exchange Rates | IFS | 2002–2017 |

| Financial, Interest Rates, Monetary Policy-Related Interest Rate | IFS | 2002–2017 |

| International Reserves, Official Reserve Assets | IFS | 2002–2017 |

| Monetary, Broad Money | IFS | 2002–2017 |

| Monetary, Reserve Money | IFS | 2002–2017 |

| Total Reserves, US Dollars (Gold at Market Price) | IFS | 2002–2017 |

| DOLS Regression | Ridge Regression | |||||

|---|---|---|---|---|---|---|

| S. Africa | Ghana | All | S. Africa | Ghana | All | |

| EMP_1 | 0.004 | 0.012 | −0.001 | 0.005 | 0.008 | 0.006 |

| (0.168) | (1.059) | (−0.318) | (3.899) | (2.287) | (2.559) | |

| EMP_2 | 1.003 | 1.750 | 1.254 | 0.754 | 0.480 | 0.874 |

| (5.703) * | (2.454) ** | (16.646) * | (3.281) | (4.137) | (3.817) | |

| EMP_3 | −0.018 | −0.551 | −0.470 | 0.157 | −0.085 | −0.209 |

| (−0.060) | (−1.339) | (−8.641) * | (3.759) | (3.492) | (3.426) | |

| EMP_4 | −0.085 | −0.398 | 0.014 | −0.037 | −0.155 | −0.037 |

| (−0.254) | (−1.955) *** | (0.439) | (2.971) | (2.800) | (2.518) | |

| EMP_5 | −0.001 | −0.006 | 0.002 | −0.003 | 0.000 | −0.001 |

| (−0.128) | (−0.678) | (1.138) | (2.717) | (3.652) | (3.317) | |

| C | −0.001 | −0.007 | ||||

| (−0.278) | (−1.988) *** | |||||

| R-squared | 0.9999 | 0.9937 | 0.9518 | 0.9916 | 0.8530 | 0.8755 |

| Adjusted R-squared | 0.9991 | 0.9556 | 0.9482 | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Klutse, S.K.; Sági, J.; Kiss, G.D. Exchange Rate Crisis among Inflation Targeting Countries in Sub-Saharan Africa. Risks 2022, 10, 94. https://doi.org/10.3390/risks10050094

Klutse SK, Sági J, Kiss GD. Exchange Rate Crisis among Inflation Targeting Countries in Sub-Saharan Africa. Risks. 2022; 10(5):94. https://doi.org/10.3390/risks10050094

Chicago/Turabian StyleKlutse, Senanu Kwasi, Judit Sági, and Gábor Dávid Kiss. 2022. "Exchange Rate Crisis among Inflation Targeting Countries in Sub-Saharan Africa" Risks 10, no. 5: 94. https://doi.org/10.3390/risks10050094

APA StyleKlutse, S. K., Sági, J., & Kiss, G. D. (2022). Exchange Rate Crisis among Inflation Targeting Countries in Sub-Saharan Africa. Risks, 10(5), 94. https://doi.org/10.3390/risks10050094