The Regime-Switching Structural Default Risk Model

Abstract

:1. Introduction

2. Structural Default Risk Models and Structural Breaks

Comparison of Regime-Switching Models with Competing Models

3. The Regime-Switching Default Risk (RSDR) Model and Its Estimation

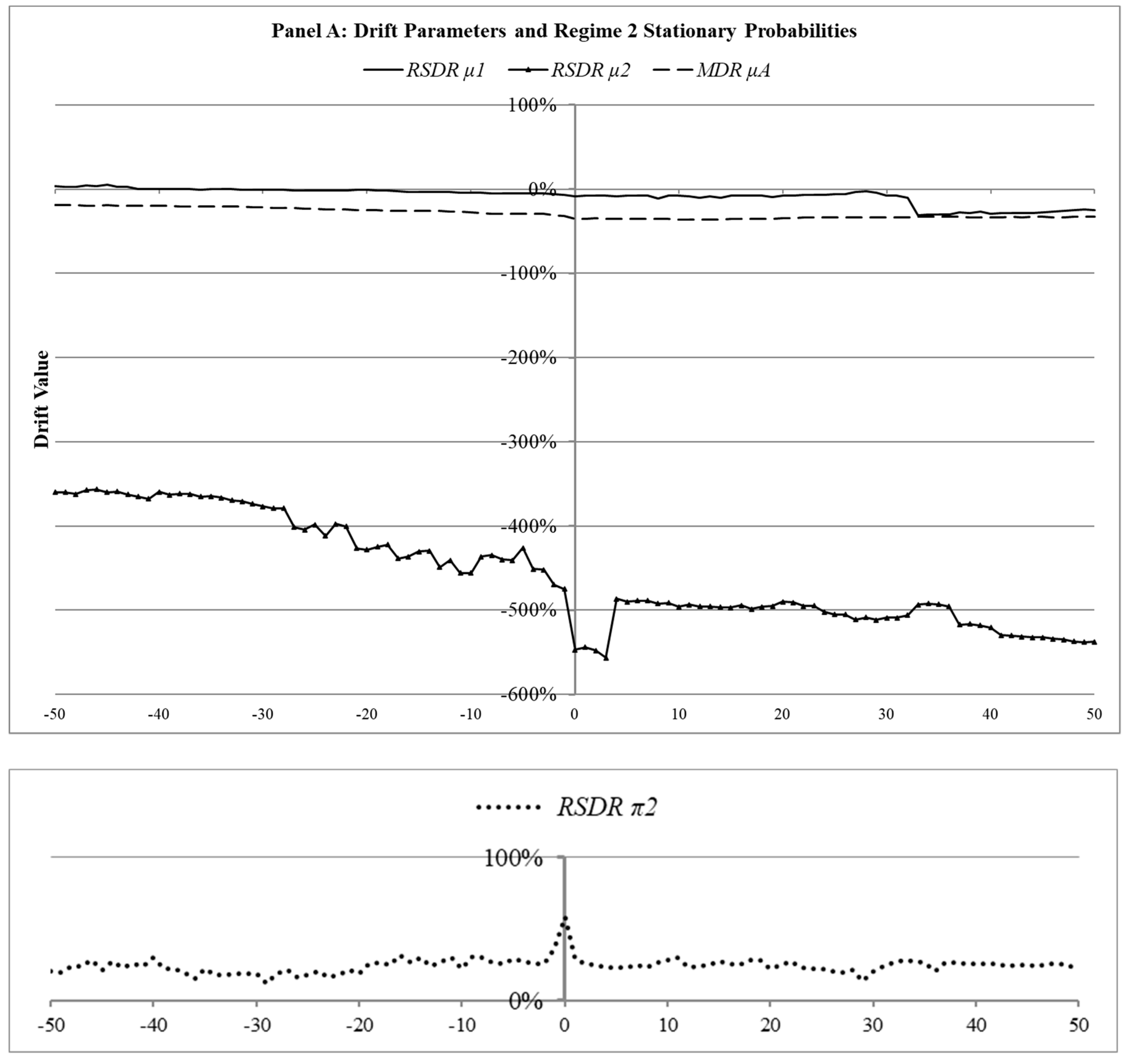

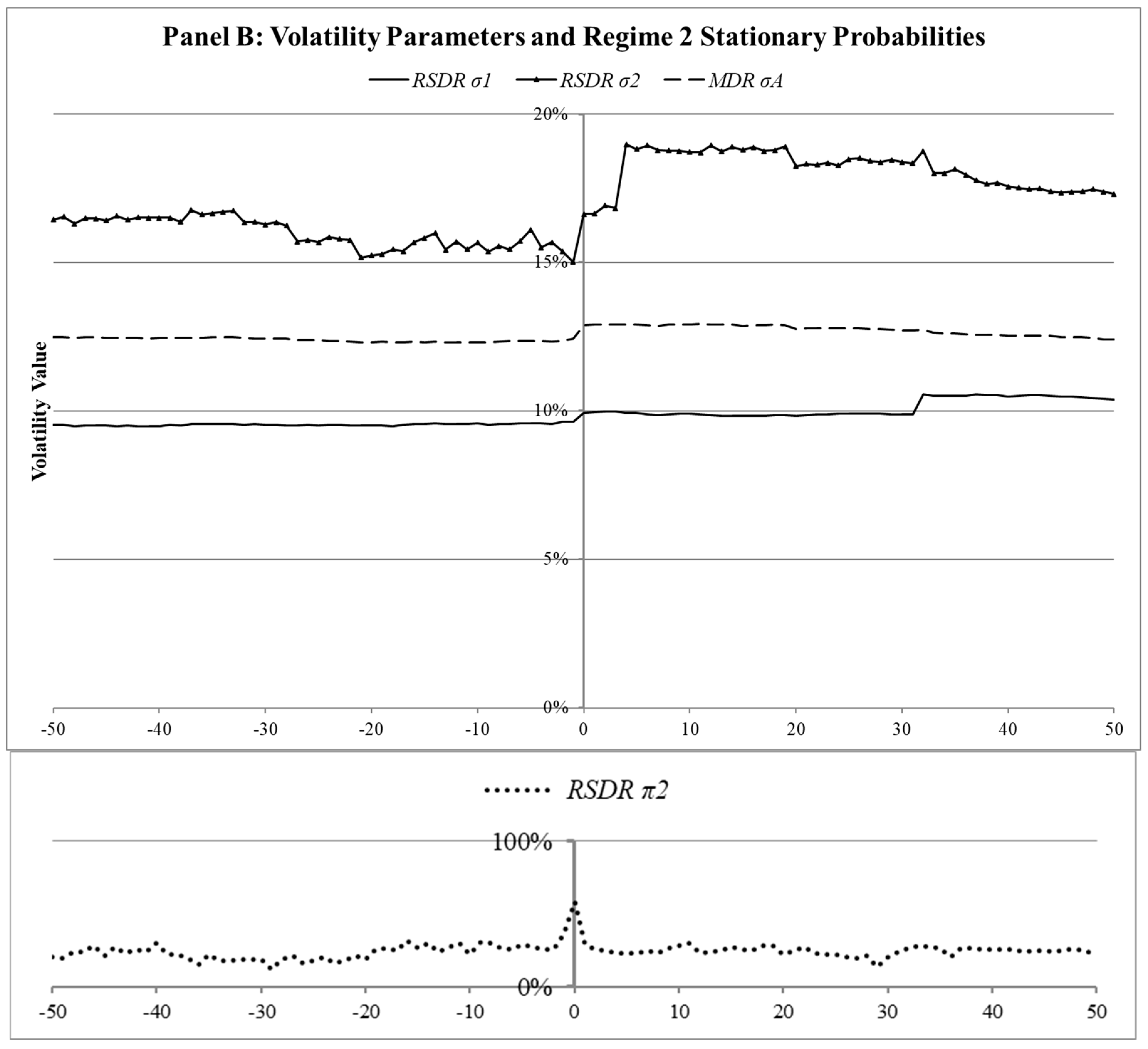

3.1. Lognormal Regime-Switching Asset Price Model

3.2. Estimation

3.3. Sojourn Probability Function

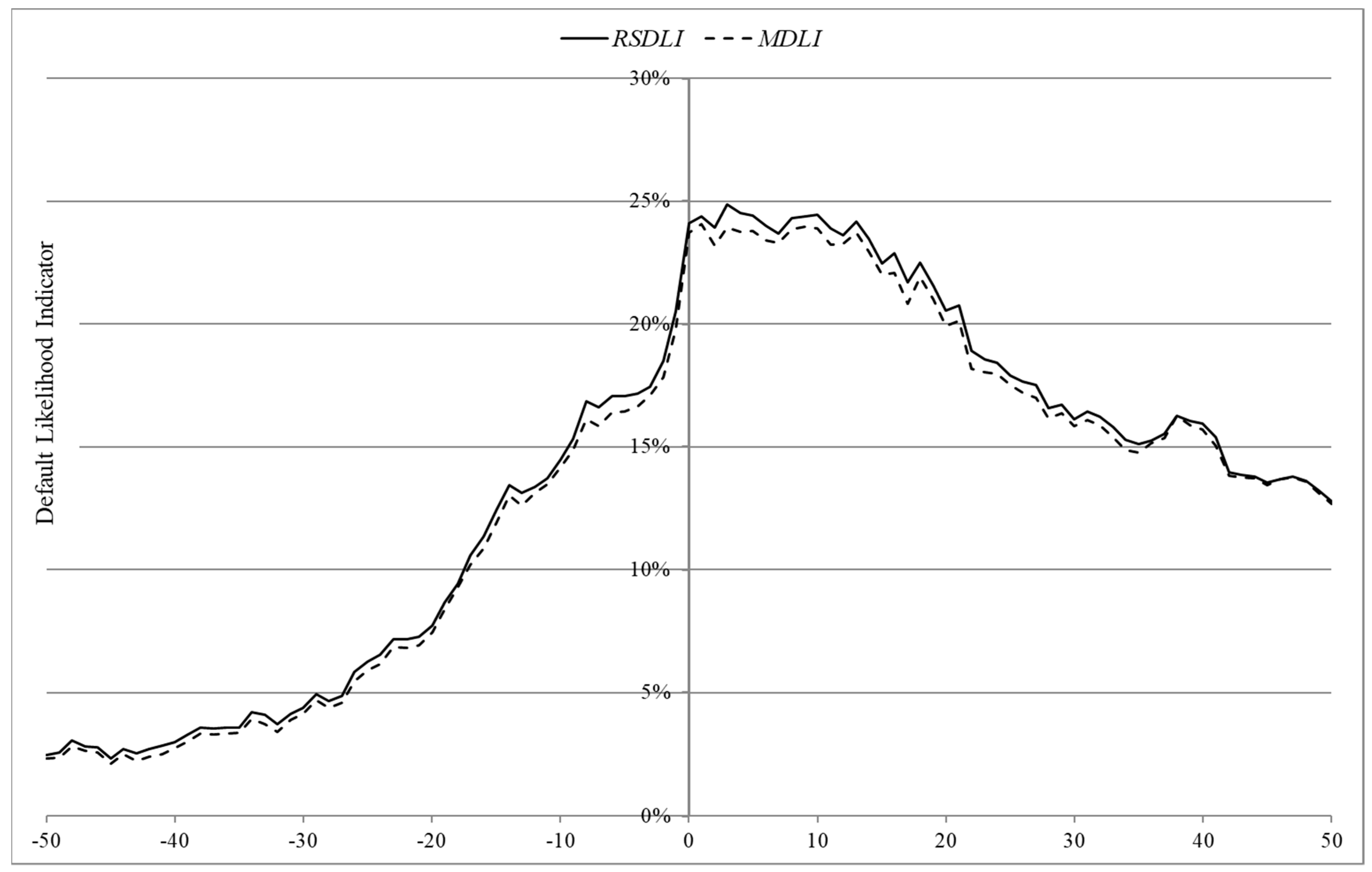

3.4. Asset Values

3.5. Hamilton Filter Modification

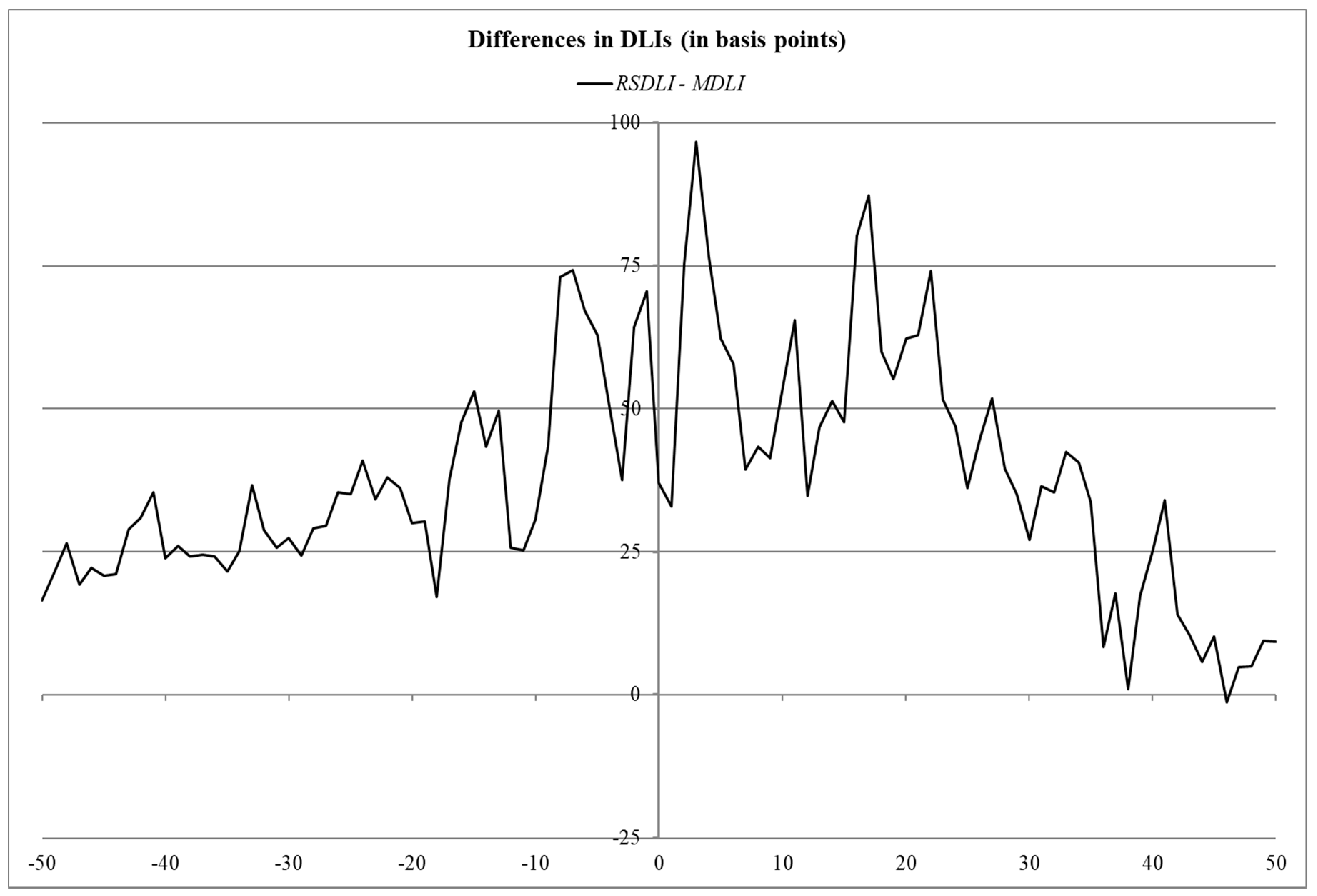

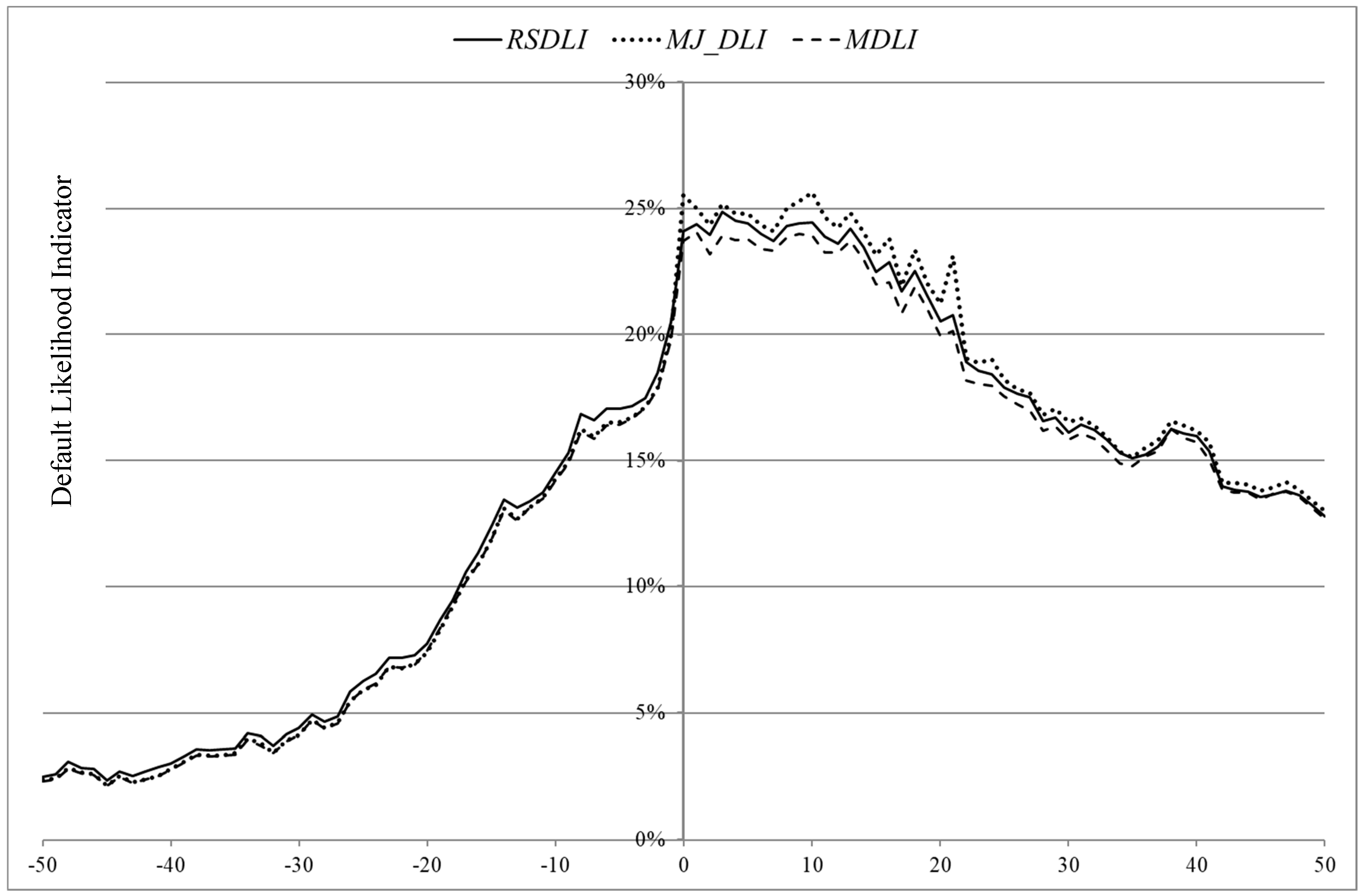

3.6. Forecasting of Return Probability Density Function ()

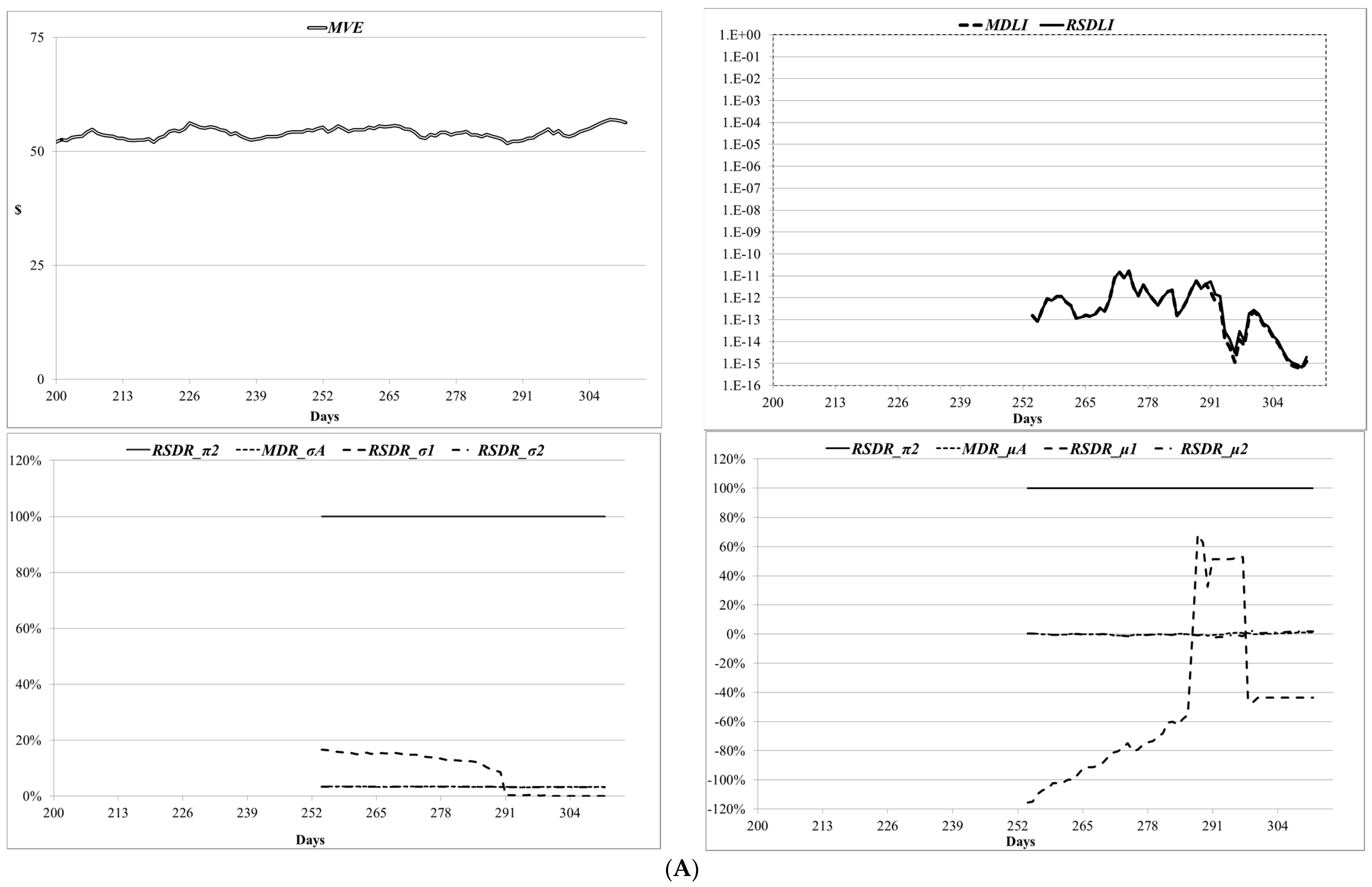

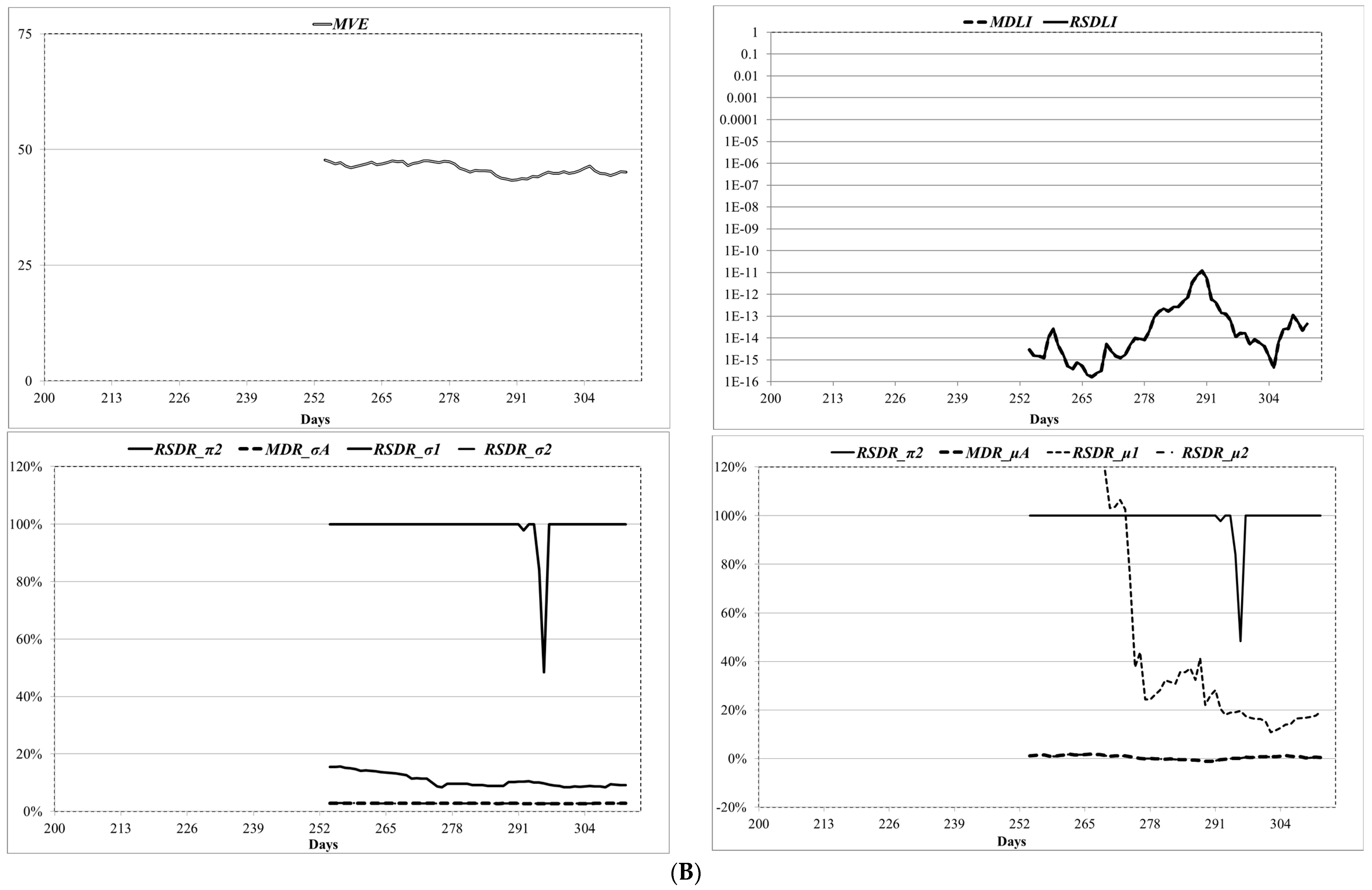

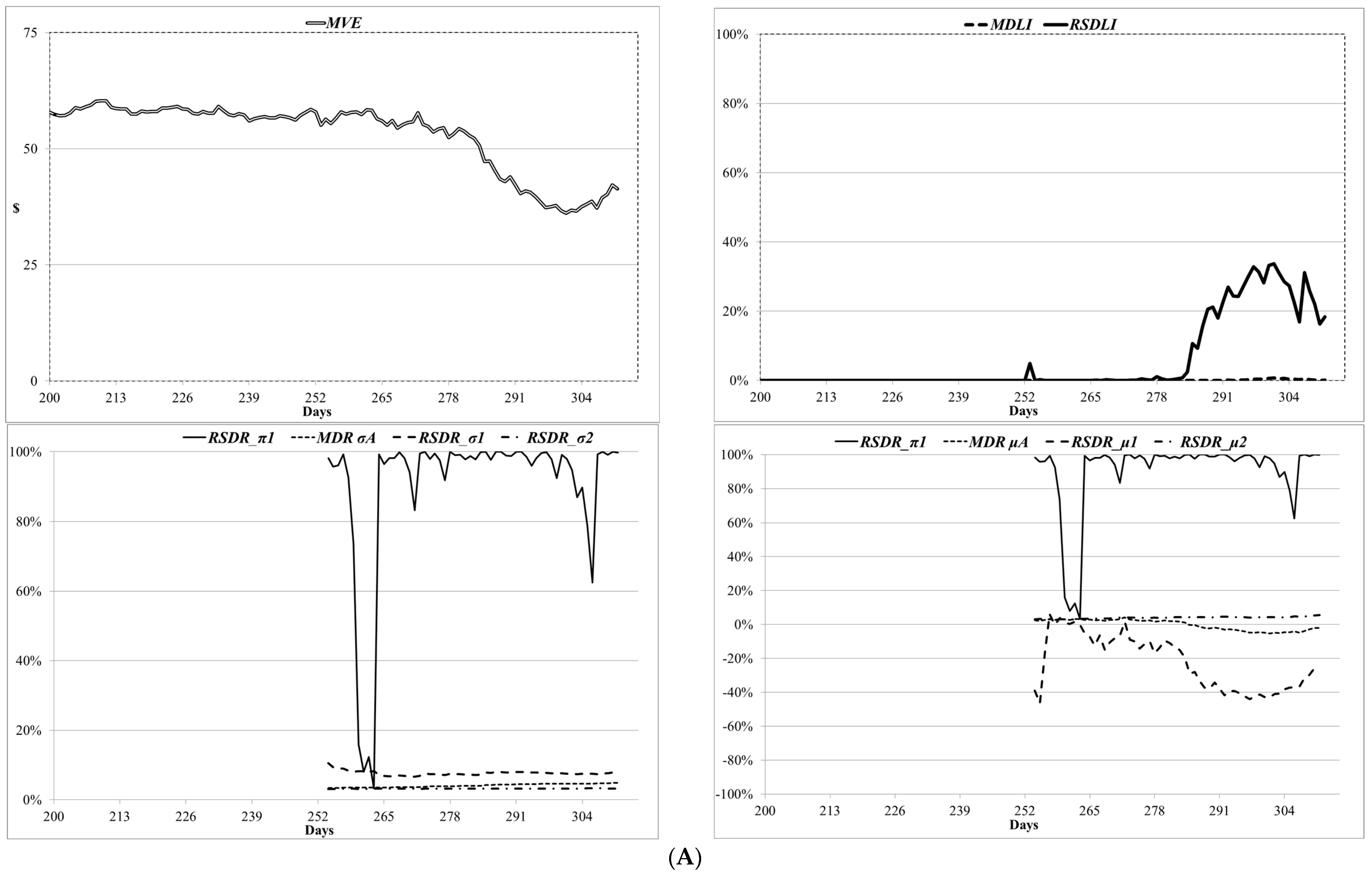

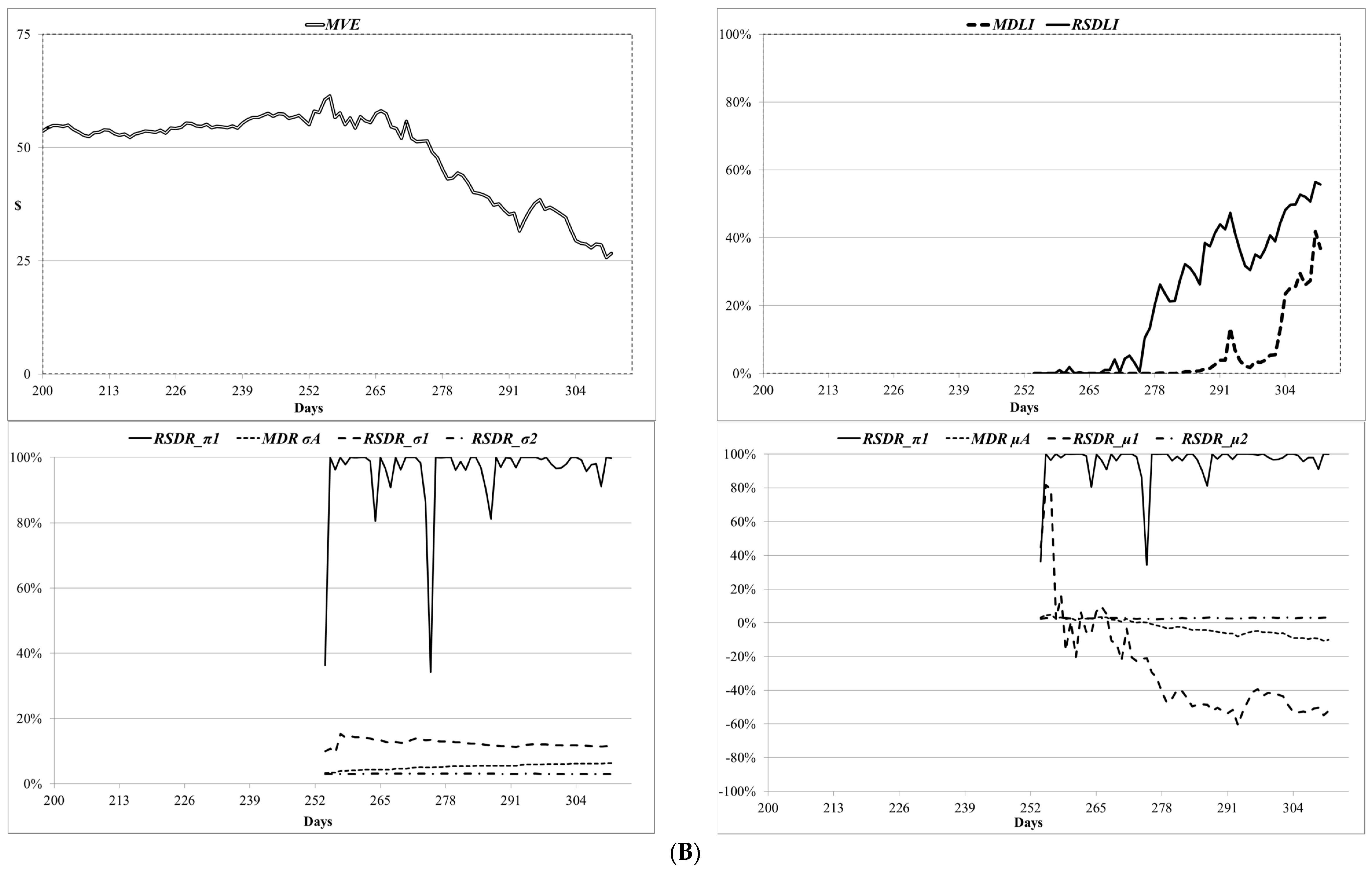

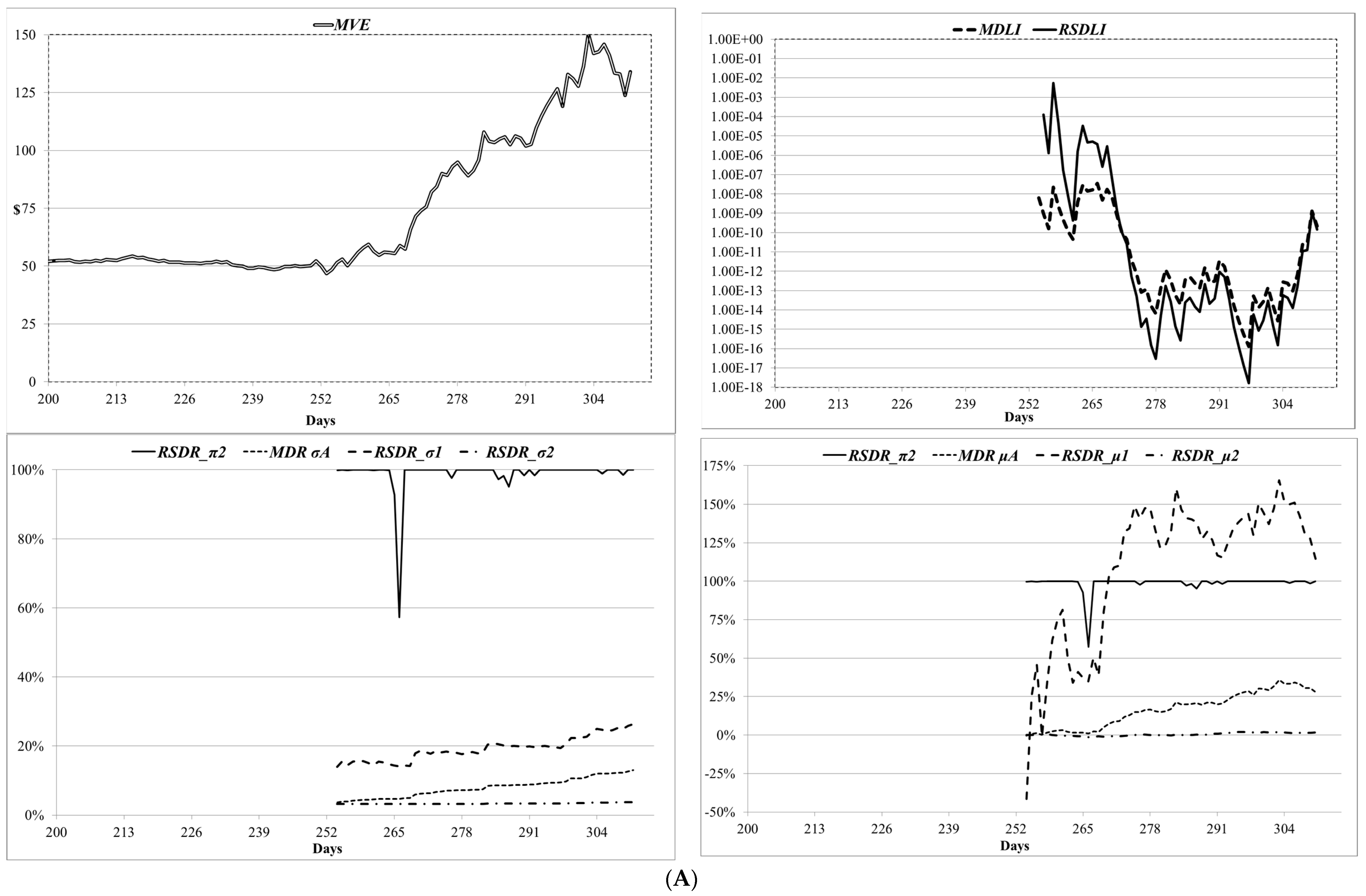

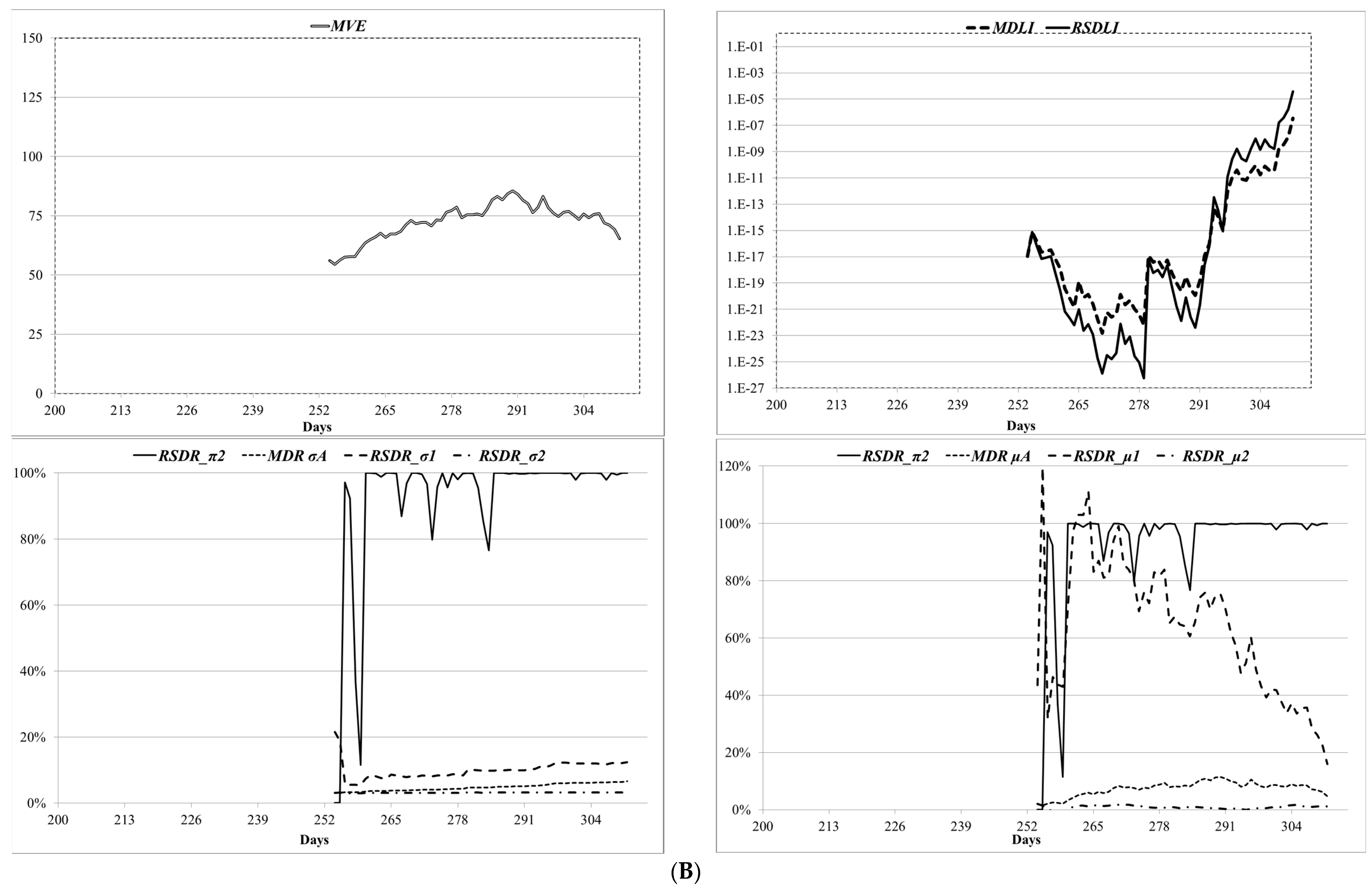

4. RSDR’s Significance and Applications

4.1. Significance of Model

4.2. Simulation Results

4.3. Empirical Results

4.3.1. Why Downgrades by Egan Jones Ratings?

4.3.2. Data

4.3.3. Results

5. Flexibility and Variations of the RSDR Model

6. Future Research

7. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Maximum Likelihood Estimation of the MDR Model

Appendix B. Hamilton’s (1989) Filter

Appendix C. Parameter Covariance Matrix

| 1 | This model is not a jump–diffusion model, but it is a variation of the RSDR model which allows changes in the drift to switch between regimes but not the volatility. We do not claim that this model incorporates the class of jump–diffusion models, but that sudden changes in asset returns can be isolated in a new regime that captures the non-normal changes that are captured by the more frequent regime. |

| 2 | Another strand of literature in modeling default risk comprises the reduced-form models (Artzner and Delbaen 1990, 1992, 1995; Jarrow and Turnbull 1995; Jarrow et al. 1997; Lando 1998; Madan and Unal 1998; Duffie and Singleton 1999). |

| 3 | Hardy (2001) uses a regime-switching model between two lognormal distributions to capture the dynamics of monthly equity returns. She recommends using a “sojourn probability function” to account for the number of months spent in each regime. She then uses the sojourn probability function to derive the distribution of the underlying stock return process. In our case, we use the sojourn probability function to estimate the implied asset values from the observed equity values. |

| 4 | |

| 5 | In Appendix C, we provide details of the calculation of the covariance matrix of . |

| 6 | We expect that the volatility parameters of the RSDR model will almost always behave this way. Estimating the drift parameters of each regime results in noisy estimates sometimes. |

| 7 | Other distributions could be used to simulate equity trajectories, but we choose a distribution that is highly correlated with asset values (i.e., in the case of financially healthy firms, low leverage) and will not introduce major changes in log-returns. |

| 8 | |

| 9 | We find results consistent with these estimates in Section 4.3.3. |

| 10 | We are grateful to Catherine Shakespeare for providing this dataset. |

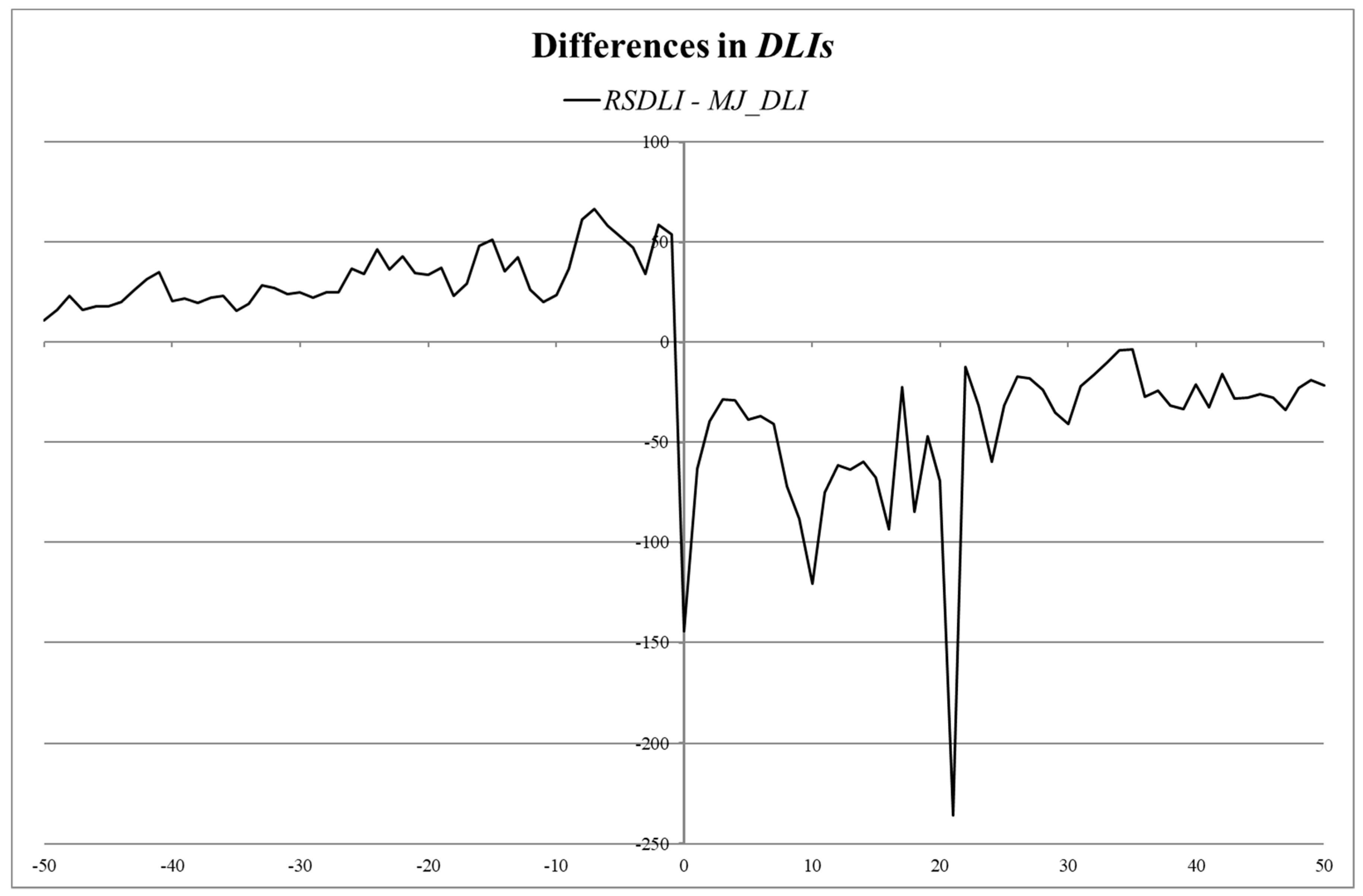

| 11 | The optimization and forecasting procedures for both processes take a significant amount of time on a conventional computer; therefore, we construct indices to produce aggregate measures of default risk in a time-efficient manner. This method is working against us since the aggregation of individual firms’ data allows for diversification, and the default probability for the “aggregate” firm is expected to be lower and less noisy than the respective default probability for an individual firm. Hence, any differences in the probabilities of default from the two models are expected to be lower in the aggregated case. |

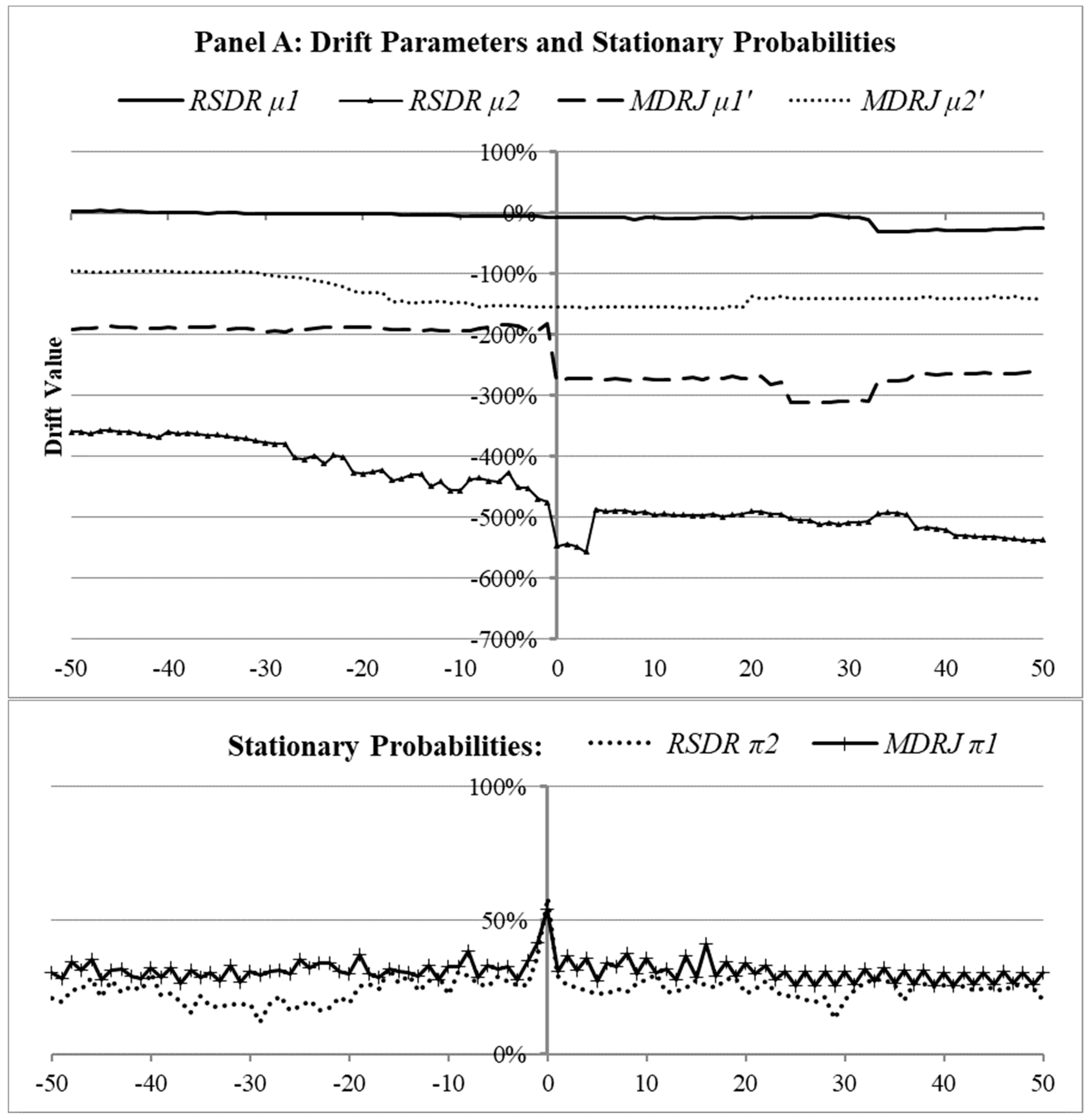

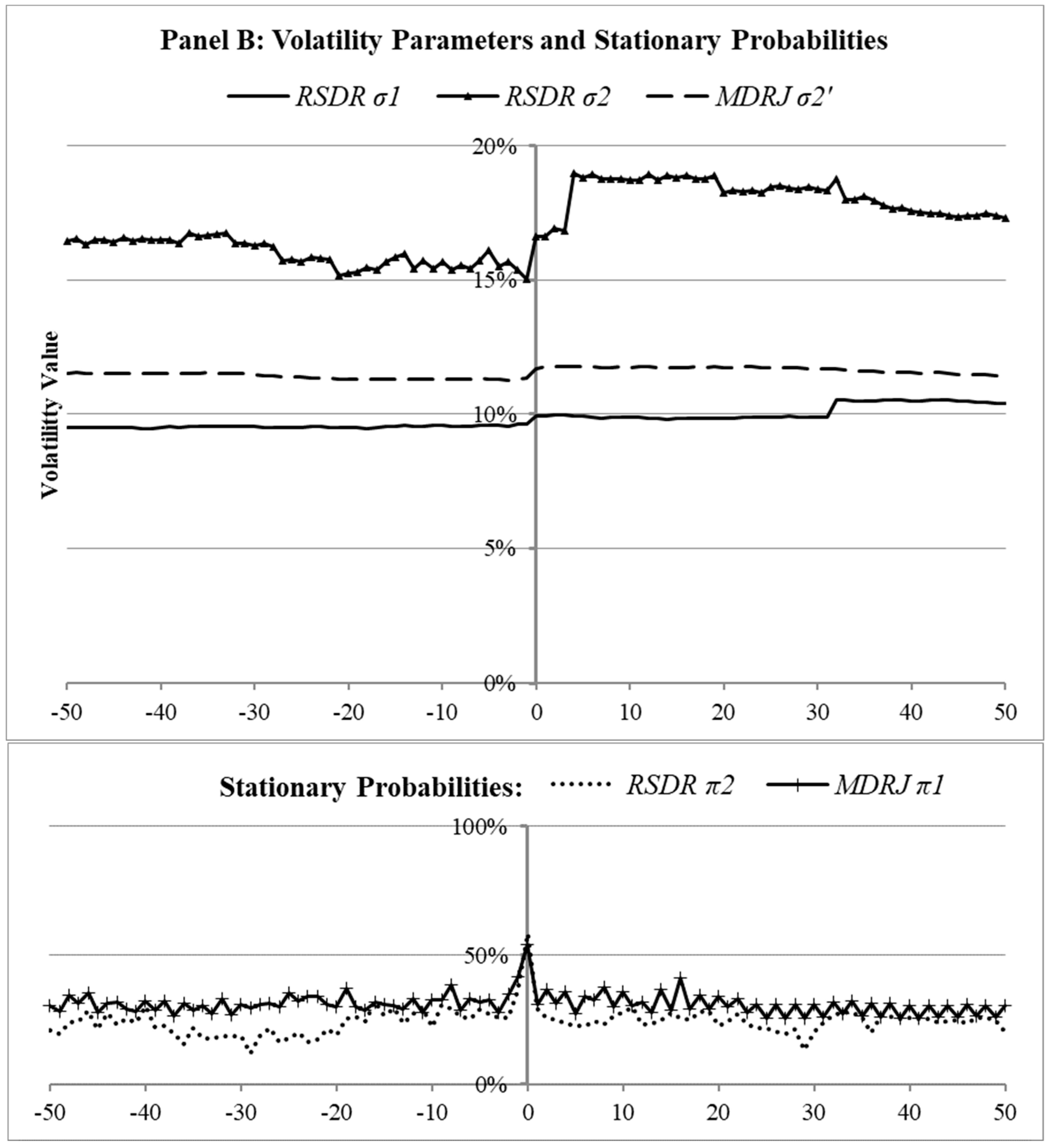

| 12 | In both Panels B and C, we observe that the RSDR drift and volatility parameters serve as outer bounds for the respective parameters of the MDR model. |

| 13 | We have also compared the RSDR model with a variation of the RSDR model that allows volatility parameters to vary in the two regimes but constrains drift parameters to be the same. The results for the constrained drift model are not very different from those of the MDR model. |

References

- Acharya, Viral V., and Jennifer N. Carpenter. 2002. Corporate Bond Valuation and Hedging with Stochastic Interest Rates and Endogenous Bankruptcy. Review of Financial Studies 15: 1355–83. [Google Scholar] [CrossRef]

- Ang, Andrew, and Geert Bekaert. 2002a. Regime Switches in Interest Rates. Journal of Business & Economic Statistics 20: 163–82. [Google Scholar]

- Ang, Andrew, and Geert Bekaert. 2002b. Short rate nonlinearities and regime switches. Journal of Economic Dynamics and Control 26: 1243–74. [Google Scholar] [CrossRef]

- Artzner, Philippe, and Freddy Delbaen. 1990. “Finem Lauda” or the risks in swaps. Insurance: Mathematics and Economics 9: 295–303. [Google Scholar] [CrossRef]

- Artzner, Philippe, and Freddy Delbaen. 1992. Credit Risk and Prepayment Option. ASTIN Bulletin 22: 81–96. [Google Scholar] [CrossRef]

- Artzner, Philippe, and Freddy Delbaen. 1995. Default Risk Insurance And Incomplete Markets. Mathematical Finance 5: 187–95. [Google Scholar] [CrossRef]

- Avellaneda, Marco, Arnon Levy, and Antonio Parás. 1995. Pricing and hedging derivative securities in markets with uncertain volatilities. Applied Mathematical Finance 2: 73–88. [Google Scholar] [CrossRef]

- Beaver, William H., Catherine Shakespeare, and Mark T. Soliman. 2006. Differential properties in the ratings of certified versus non-certified bond-rating agencies. Journal of Accounting and Economics 42: 303–34. [Google Scholar] [CrossRef]

- Berwart, Erik, Massimo Guidolin, and Andreas Milidonis. 2019. An empirical analysis of changes in the relative timeliness of issuer-paid vs. investor-paid ratings. Journal of Corporate Finance 59: 88–118. [Google Scholar] [CrossRef]

- Black, Fischer, and John C. Cox. 1976. Valuing Corporate Securities: Some Effects of Bond Indenture Provisions. Journal of Finance 31: 351–67. [Google Scholar] [CrossRef]

- Black, Fischer, and Myron Scholes. 1973. The Pricing of Options and Corporate Liabilities. Journal of Political Economy 81: 637–54. [Google Scholar] [CrossRef]

- Blume, Marshall E., Felix Lim, and A. Craig MacKinlay. 1998. The Declining Credit Quality of U.S. Corporate Debt: Myth or Reality? Journal of Finance 53: 1389–413. [Google Scholar] [CrossRef]

- Bollen, Nicolas P. B. 1998. Valuing Options in Regime-Switching Models. Journal of Derivatives 6: 38–49. [Google Scholar] [CrossRef]

- Boyle, Phelim, and Thangaraj Draviam. 2007. Pricing exotic options under regime switching. Insurance: Mathematics & Economics 40: 267–82. [Google Scholar]

- Cremers, K. J. Martijn, Joost Driessen, and Pascal Maenhout. 2008. Explaining the Level of Credit Spreads: Option-Implied Jump Risk Premia in a Firm Value Model. Review of Financial Studies 21: 2209–42. [Google Scholar] [CrossRef]

- Duan, Jin-Chuan. 1994. Maximum Likelihood Estimation Using Price Data of the Derivative Contract. Mathematical Finance 4: 155–67. [Google Scholar] [CrossRef]

- Duan, Jin-Chuan. 2000. Correction: Maximum Likelihood Estimation Using Price Data of the Derivative Contract (Mathematical Finance 1994, 4/2, 155–167). Mathematical Finance 10: 461–62. [Google Scholar] [CrossRef]

- Duan, Jin-Chuan, and Chung-Ying Yeh. 2010. Jump and volatility risk premiums implied by VIX. Journal of Economic Dynamics & Control 34: 2232–44. [Google Scholar]

- Duan, Jin-Chuan, and Jean-Guy Simonato. 2002. Maximum likelihood estimation of deposit insurance value with interest rate risk. Journal of Empirical Finance 9: 109–32. [Google Scholar] [CrossRef]

- Duan, Jin-Chuan, and Min-Teh Yu. 1994. Forbearance and Pricing Deposit Insurance in a Multiperiod Framework. The Journal of Risk and Insurance 61: 575–91. [Google Scholar] [CrossRef]

- Duffie, Darrell, and Kenneth J. Singleton. 1999. Modeling term structures of defaultable bonds. Review of Financial Studies 12: 687–720. [Google Scholar] [CrossRef]

- Ederington, Louis H., and Jeremy C. Goh. 1998. Bond Rating Agencies and Stock Analysts: Who Knows What When? Journal of Financial and Quantitative Analysis 33: 569–85. [Google Scholar] [CrossRef]

- Ericsson, Jan, and Joel Reneby. 2004. An Empirical Study of Structural Credit Risk Models Using Stock and Bond Prices. The Journal of Fixed Income 13: 38–49. [Google Scholar] [CrossRef]

- Ericsson, Jan, and Joel Reneby. 2005. Estimating Structural Bond Pricing Models. Journal of Business 78: 707–35. [Google Scholar] [CrossRef]

- Goh, Jeremy C., and Louis H. Ederington. 1993. Is a Bond Rating Downgrade Bad News, Good News, or No News for Stockholders? Journal of Finance 48: 2001–8. [Google Scholar] [CrossRef]

- Goh, Jeremy C., and Louis H. Ederington. 1999. Cross-Sectional Variation in the Stock Market Reaction to Bond Rating Changes. Quarterly Review of Economics & Finance 39: 101–12. [Google Scholar]

- Goldfeld, Stephen M., and Richard E. Quandt. 1973. A Markov model for switching regressions. Journal of Econometrics 1: 3–15. [Google Scholar] [CrossRef]

- Gray, Stephen F. 1996. Modeling the conditional distribution of interest rates as a regime-switching process. Journal of Financial Economics 42: 27–62. [Google Scholar] [CrossRef]

- Güttler, André, and Mark Wahrenburg. 2007. The adjustment of credit ratings in advance of defaults. Journal of Banking & Finance 31: 751–67. [Google Scholar]

- Hamilton, James D. 1989. A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle. Econometrica 57: 357–84. [Google Scholar] [CrossRef]

- Hamilton, James D., and Raul Susmel. 1994. Autoregressive conditional heteroskedasticity and changes in regime. Journal of Econometrics 64: 307–33. [Google Scholar] [CrossRef]

- Hand, John R. M., Robert W. Holthausen, and Richard W. Leftwich. 1992. The Effect of Bond Rating Agency Announcements on Bond and Stock Prices. Journal of Finance 47: 733–52. [Google Scholar] [CrossRef]

- Hardy, Mary R. 2001. A Regime-Switching Model of Long-Term Stock Returns. North American Actuarial Journal 5: 41–53. [Google Scholar] [CrossRef]

- Holthausen, Robert W., and Richard W. Leftwich. 1986. The Effect of Bond Ratings Changes on Common Stock Prices. Journal of Financial Economics 17: 57–89. [Google Scholar] [CrossRef]

- Huang, Jing-Zhi, and Ming Huang. 2012. How much of the corporate-treasury yield spread is due to credit risk? The Review of Asset Pricing Studies 2: 153–202. [Google Scholar] [CrossRef]

- Hull, John, and Alan White. 1987. The Pricing of Options on Assets with Stochastic Volatilities. Journal of Finance 42: 281–300. [Google Scholar] [CrossRef]

- Hull, John, and Alan White. 1988. An Analysis of the Bias in Option Pricing Caused by a Stochastic Volatility. Advances in Futures and Options Research 3: 27–61. [Google Scholar]

- Jarrow, Robert A., and Stuart M. Turnbull. 1995. Pricing Derivatives on Financial Securities Subject to Credit Risk. Journal of Finance 50: 53–85. [Google Scholar] [CrossRef]

- Jarrow, Robert A., David Lando, and Stuart M. Turnbull. 1997. A Markov model for the term structure of credit risk spreads. Review of Financial Studies 10: 481–523. [Google Scholar] [CrossRef]

- Johnson, Richard. 2004. Rating Agency Actions Around the Investment-Grade Boundary. Journal of Fixed Income 13: 25–37. [Google Scholar] [CrossRef]

- Jones, E. Philip, Scott P. Mason, and Eric Rosenfeld. 1984. Contingent Claims Analysis of Corporate Capital Structures: An Empirical Investigation. Journal of Finance 39: 611–25. [Google Scholar] [CrossRef]

- Kalimipalli, Madhu, and Raul Susmel. 2004. Regime-switching stochastic volatility and short-term interest rates. Journal of Empirical Finance 11: 309–29. [Google Scholar] [CrossRef]

- Kealhofer, Stephen. 2003. Credit risk i: Default prediction. Financial Analysts Journal 59: 30–44. [Google Scholar] [CrossRef]

- Kim, Chang-Jin, and Charles R. Nelson. 1999. State-Space Models with Regime Switching: Classical and Gibbs-Sampling Approaches with Applications. MIT Press Books. Cambridge: The MIT Press, vol. 1, p. 0262112388. [Google Scholar]

- Lando, David. 1998. On Cox Processes and Credit Risky Securities. Review of Derivatives Research 2: 99–120. [Google Scholar] [CrossRef]

- Lehar, Alfred. 2005. Measuring systemic risk: A risk management approach. Journal of Banking & Finance 29: 2577–603. [Google Scholar]

- Leland, Hayne E. 1994. Corporate Debt Value, Bond Covenants, and Optimal Capital Structure. (cover story). Journal of Finance 49: 1213–52. [Google Scholar] [CrossRef]

- Leland, Hayne E., and Klaus Bjerre Toft. 1996. Optimal Capital Structure, Endogenous Bankruptcy, and the Term Structure of Credit Spreads. Journal of Finance 51: 987–1019. [Google Scholar] [CrossRef]

- Li, Ka Leung, and Hoi Ying Wong. 2008. Structural models of corporate bond pricing with maximum likelihood estimation. Journal of Empirical Finance 15: 751–77. [Google Scholar] [CrossRef]

- Litterman, Robert B., José Scheinkman, and Laurence Weiss. 1991. Volatility and the Yield Curve. Journal of Fixed Income 1: 49–53. [Google Scholar] [CrossRef]

- Longstaff, Francis A., and Eduardo S. Schwartz. 1995. A Simple Approach to Valuing Risky Fixed and Floating Rate Debt. The Journal of Finance 50: 789–819. [Google Scholar] [CrossRef]

- Lyden, Scott, and David Saraniti. 2001. An Empirical Examination of the Classical Theory of Corporate Security Valuation. Available online: https://www.researchgate.net/publication/228289841_An_Examination_of_the_Classical_Theory_of_Corporate_Security_Valuation (accessed on 15 December 2023).

- Madan, Dilip B., and Haluk Unal. 1998. Pricing the Risks of Default. Review of Derivatives Research 2: 121–60. [Google Scholar] [CrossRef]

- Merton, Robert C. 1974. On the Pricing of Corporate Debt: The Risk Structure of Interest Rates. Journal of Finance 29: 449–70. [Google Scholar]

- Michaelides, Alexander, Andreas Milidonis, and George P. Nishiotis. 2019. Private information in currency markets. Journal of Financial Economics 131: 643–65. [Google Scholar] [CrossRef]

- Michaelides, Alexander, Andreas Milidonis, George P. Nishiotis, and Panayiotis Papakyriakou. 2015. The Adverse Effects of Systematic Leakage Ahead of Official Sovereign Debt Rating Announcements. Journal of Financial Economics 116: 526–47. [Google Scholar] [CrossRef]

- Milidonis, Andreas, and Shaun Wang. 2007. Estimation of Distress Costs Associated with Downgrades Using Regime-Switching Models. North American Actuarial Journal 11: 42–60. [Google Scholar] [CrossRef]

- Naik, Vasanttilak. 1993. Option Valuation and Hedging Strategies with Jumps in the Volatility of Asset Returns. Journal of Finance 48: 1969–84. [Google Scholar] [CrossRef]

- Nelder, John A., and Roger Mead. 1965. A Simplex Method for Function Minimization. The Computer Journal 7: 308–13. [Google Scholar] [CrossRef]

- Ogden, Joseph P. 1987. Determinants of the Ratings and yields on Corporate Bonds: Tests of the Contingent Claims Model. Journal of Financial Research 10: 329–39. [Google Scholar] [CrossRef]

- Poon, Ser-Huang, and Clive W. J. Granger. 2003. Forecasting Volatility in Financial Markets: A Review. Journal of Economic Literature 41: 478–539. [Google Scholar] [CrossRef]

- Quandt, Richard E. 1958. The Estimation of the Parameters of a Linear Regression System Obeying Two Separate Regimes. Journal of the American Statistical Association 53: 873–80. [Google Scholar] [CrossRef]

- Ronn, Ehud I., and Avinash K. Verma. 1986. Pricing Risk-Adjusted Deposit Insurance: An Option-Based Model. Journal of Finance 41: 871–95. [Google Scholar]

- Ronn, Ehud I., and Avinash K. Verma. 1989. Risk-based Capital Adequacy Standards for a Sample of 43 Major Banks. Journal of Banking & Finance 13: 21–29. [Google Scholar]

- Shimko, David C., Naohiko Tejima, and Donald R. Van Deventer. 1993. The pricing of risky debt when interest rates are stochastic. The Journal of Fixed Income 3: 58–65. [Google Scholar]

- Siu, Tak Kuen, Christina Erlwein, and Rogemar S. Mamon. 2008. The Pricing of Credit Default Swaps under a Markov-Modulated Merton’s Structural Model. North American Actuarial Journal 12: 19–46. [Google Scholar] [CrossRef]

- Vassalou, Maria, and Yuhang Xing. 2004. Default Risk in Equity Returns. Journal of Finance 59: 831–68. [Google Scholar] [CrossRef]

- Vassalou, Maria, and Yuhang Xing. 2005. Abnormal Equity Returns following Downgrades Working Paper. Available online: https://www.cicfconf.org/past/cicf2005/paper/20050128043348.PDF (accessed on 15 December 2023).

- Vetterling, William T., Saul A. Teukolsky, William H. Press, and Brian P. Flannery. 2002. Numerical Recipes in C++: The Art of Scientific Computing, 2nd ed. New York: Cambridge University Press. [Google Scholar]

- Zhou, Chunsheng. 2001a. An analysis of default correlations and multiple defaults. Review of Financial Studies 14: 555–76. [Google Scholar] [CrossRef]

- Zhou, Chunsheng. 2001b. The Term Structure of Credit Spreads with Jump Risk. Journal of Banking & Finance 25: 2015–40. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| EJR | Investment | Entire Database | Data Around Event | ||

|---|---|---|---|---|---|

| Rating | Grade? | Downgrade | Upgrade | Downgrade | Upgrade |

| AAA | yes | ||||

| AA+ | yes | 2 | 1 | ||

| AA | yes | 2 | 3 | 1 | |

| AA− | yes | 9 | 11 | 8 | 8 |

| A+ | yes | 28 | 26 | 23 | 23 |

| A | yes | 41 | 26 | 35 | 22 |

| A− | yes | 91 | 37 | 80 | 28 |

| BBB+ | yes | 92 | 63 | 78 | 46 |

| BBB | yes | 129 | 77 | 110 | 54 |

| BBB− | yes | 144 | 56 | 109 | 42 |

| BB+ | no | 115 | 52 | 94 | 38 |

| BB | no | 85 | 60 | 71 | 44 |

| BB− | no | 83 | 47 | 71 | 37 |

| B+ | no | 79 | 26 | 59 | 15 |

| B | no | 66 | 15 | 51 | 11 |

| B− | no | 54 | 3 | 37 | 3 |

| CCC+ | no | 4 | 3 | ||

| CCC | no | 36 | 3 | 21 | 3 |

| CCC− | no | ||||

| CC | no | 30 | 2 | 22 | 2 |

| C | no | 25 | 14 | ||

| D | no | 18 | 6 | ||

| Grand Total | 1133 | 507 | 893 | 377 | |

| Panel A: Market Value of Equity, Default Boundary and Risk-Free Rate by Rating Category | |||||||||||

| Category | Market Value of Equity (MVE) | Default Boundary | Risk-Free Rate | ||||||||

| (USD 1 million) | (USD 1 million) | ||||||||||

| Mean | Std. Dev. | Mean | Std. Dev. | Mean | Std. Dev. | ||||||

| AA− | 458,155 | 38,506 | 142,806 | 8410 | 2.00% | 0.10% | |||||

| A+ | 1,373,105 | 52,918 | 1,468,080 | 32,972 | 1.60% | 0.10% | |||||

| A | 1,428,275 | 110,874 | 795,030 | 13,402 | 1.90% | 0.10% | |||||

| A− | 1,610,407 | 107,046 | 692,493 | 15,849 | 2.00% | 0.10% | |||||

| BBB+ | 1,447,256 | 190,867 | 568,890 | 4531 | 1.80% | 0.10% | |||||

| BBB | 1,453,386 | 64,630 | 674,765 | 6014 | 1.70% | 0.10% | |||||

| BBB− | 1,281,199 | 188,001 | 429,357 | 5882 | 1.70% | 0.10% | |||||

| BB+ | 882,968 | 174,207 | 241,612 | 3411 | 1.60% | 0.20% | |||||

| BB | 555,183 | 181,663 | 114,661 | 1732 | 1.70% | 0.10% | |||||

| BB− | 366,656 | 116,614 | 100,282 | 506 | 1.50% | 0.20% | |||||

| B+ | 75,744 | 12,608 | 53,071 | 2315 | 1.70% | 0.10% | |||||

| B | 143,382 | 25,326 | 87,020 | 1808 | 2.00% | 0.10% | |||||

| B− | 57,374 | 15,759 | 70,393 | 1260 | 1.90% | 0.10% | |||||

| CCC | 25,151 | 7017 | 26,632 | 1159 | 2.00% | 0.10% | |||||

| CC | 36,224 | 3453 | 42,636 | 2924 | 2.30% | 0.10% | |||||

| C | 23,394 | 5299 | 34,462 | 5149 | 2.00% | 0.30% | |||||

| Panel B: Empirical Distribution of Market Value of Equity by Rating Category | |||||||||||

| Downgrade | Market Value of Equity (MVE) Return | ||||||||||

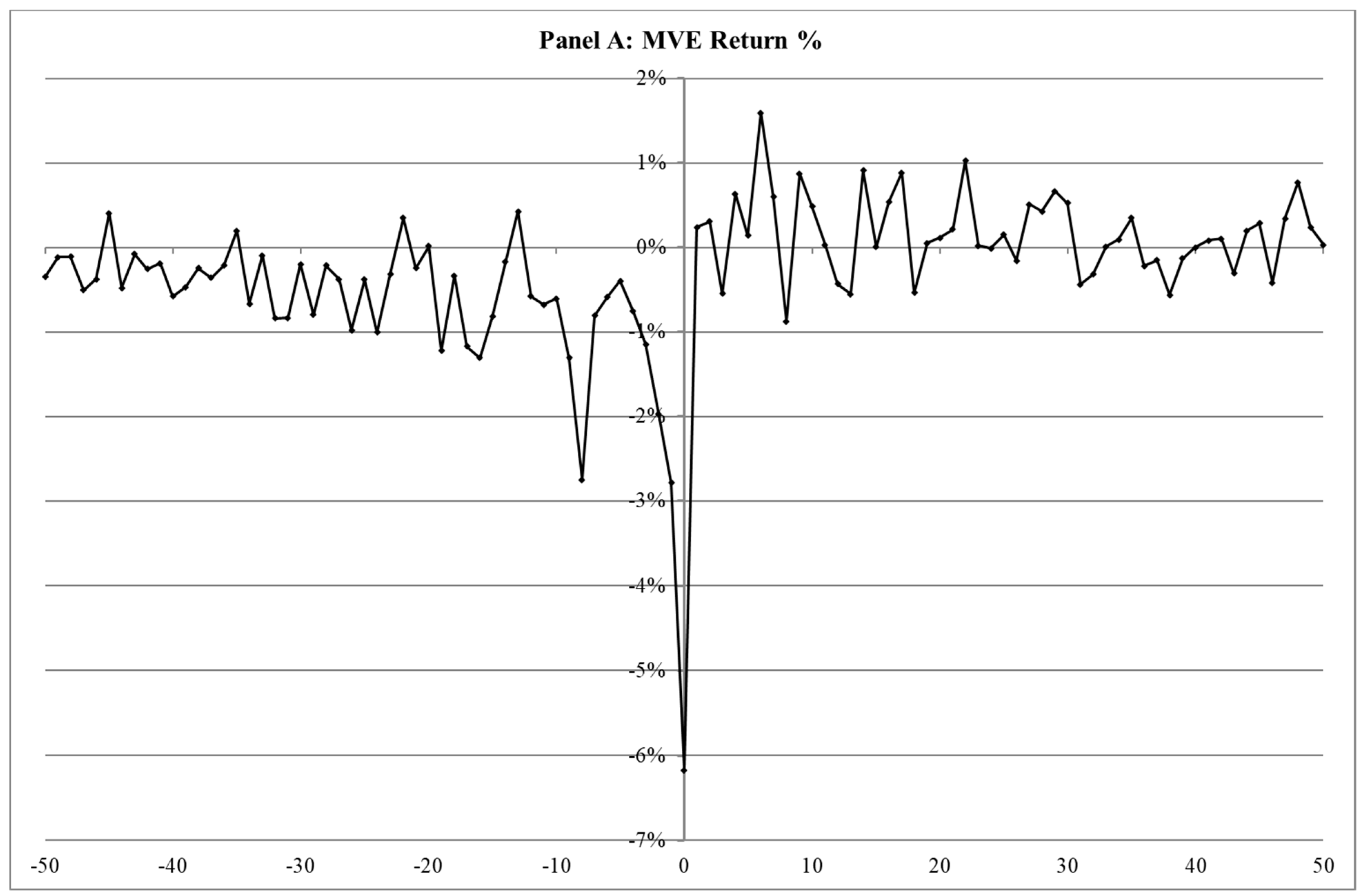

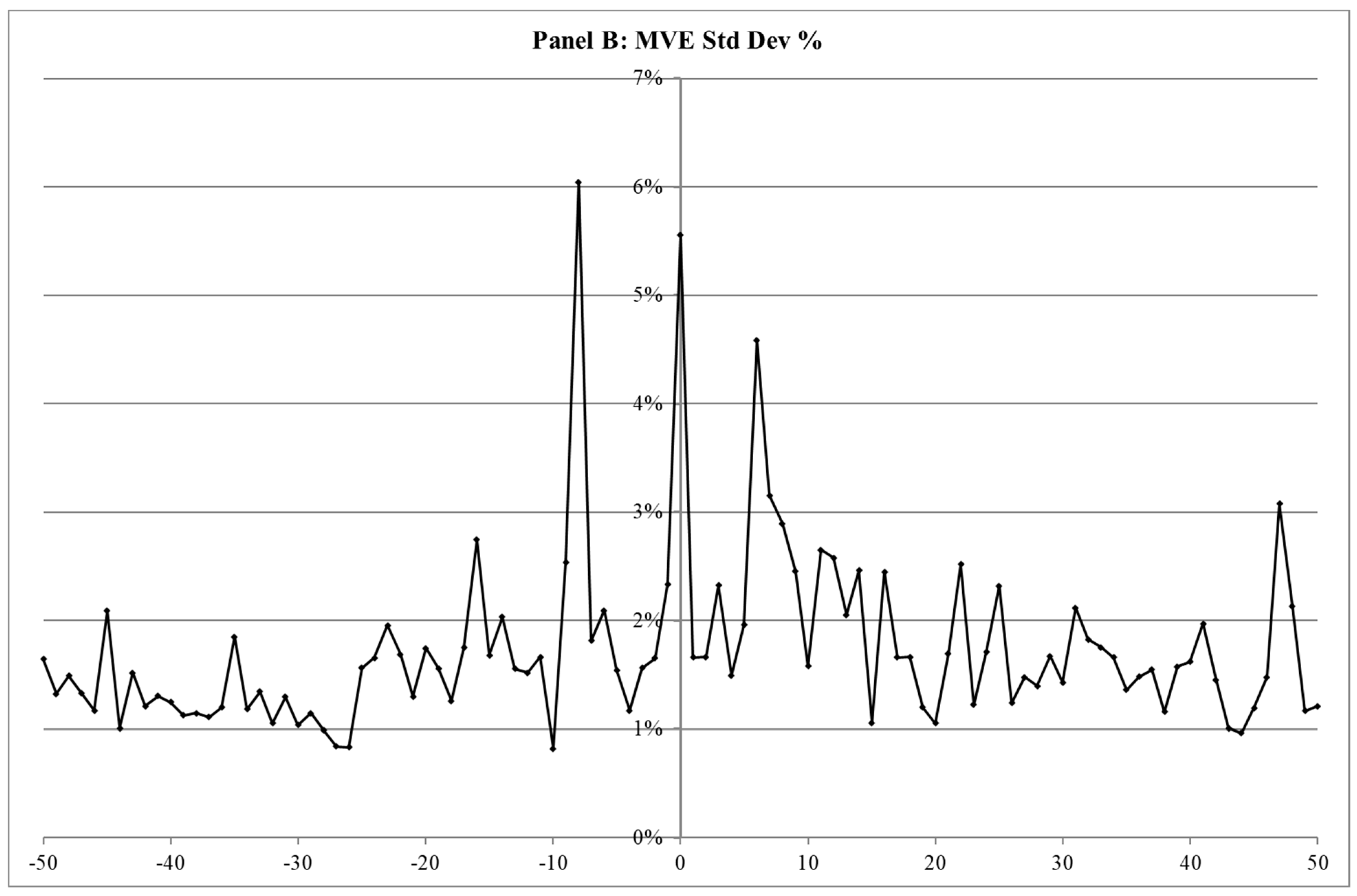

| Average | Std. Dev. | Skew. | Kurt. | pct 0% | pct 1% | pct 5% | pct 50% | pct 95% | pct 99% | pct 100% | |

| Category | Mean | Mean | Mean | Mean | Mean | Mean | Mean | Mean | Mean | Mean | Mean |

| AA− | 0.00% | 1.40% | 4.02 | 41.98 | −4.60% | −2.40% | −1.70% | −0.10% | 1.80% | 2.80% | 13.90% |

| A+ | 0.00% | 0.70% | 0.11 | 2.57 | −2.40% | −1.70% | −1.10% | 0.00% | 1.00% | 1.80% | 2.70% |

| A | 0.00% | 0.90% | 0.29 | 1.19 | −2.40% | −2.00% | −1.40% | 0.00% | 1.40% | 2.10% | 4.10% |

| A− | −0.10% | 0.80% | −0.27 | 0.90 | −3.10% | −2.40% | −1.30% | 0.00% | 1.30% | 1.80% | 2.60% |

| BBB+ | −0.20% | 1.00% | −0.96 | 5.09 | −6.00% | −2.90% | −1.60% | −0.10% | 1.40% | 2.10% | 2.40% |

| BBB | −0.10% | 0.70% | −0.48 | 4.64 | −3.90% | −1.70% | −1.10% | −0.10% | 1.10% | 1.60% | 2.30% |

| BBB− | −0.20% | 0.90% | −0.66 | 2.07 | −4.20% | −3.00% | −1.50% | −0.20% | 1.10% | 1.70% | 2.20% |

| BB+ | −0.30% | 1.10% | −0.80 | 4.41 | −5.90% | −3.40% | −1.80% | −0.20% | 1.40% | 1.90% | 2.80% |

| BB | −0.40% | 1.60% | −0.86 | 3.44 | −8.60% | −5.30% | −2.90% | −0.30% | 2.10% | 2.90% | 3.90% |

| BB− | −0.40% | 1.80% | −1.25 | 5.99 | −10.30% | −6.50% | −2.90% | −0.30% | 2.00% | 3.60% | 4.30% |

| B+ | −0.20% | 1.00% | −0.73 | 2.82 | −4.90% | −3.60% | −1.80% | −0.20% | 1.30% | 2.00% | 2.70% |

| B | −0.30% | 1.40% | −0.24 | 0.29 | −4.70% | −3.70% | −2.70% | −0.20% | 1.80% | 2.50% | 4.00% |

| B− | −0.40% | 1.40% | −0.59 | 8.16 | −8.70% | −4.00% | −2.30% | −0.30% | 1.70% | 3.00% | 6.00% |

| CCC | −0.40% | 1.80% | −1.36 | 11.05 | −12.20% | −4.40% | −3.20% | −0.40% | 2.40% | 3.40% | 4.90% |

| CC | −0.10% | 1.60% | −0.70 | 4.50 | −8.50% | −5.00% | −2.50% | 0.00% | 2.10% | 3.70% | 5.70% |

| C | −0.30% | 2.10% | −0.52 | 6.41 | −11.70% | −5.50% | −3.30% | −0.40% | 2.90% | 4.90% | 7.70% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Milidonis, A.; Chisholm, K. The Regime-Switching Structural Default Risk Model. Risks 2024, 12, 48. https://doi.org/10.3390/risks12030048

Milidonis A, Chisholm K. The Regime-Switching Structural Default Risk Model. Risks. 2024; 12(3):48. https://doi.org/10.3390/risks12030048

Chicago/Turabian StyleMilidonis, Andreas, and Kevin Chisholm. 2024. "The Regime-Switching Structural Default Risk Model" Risks 12, no. 3: 48. https://doi.org/10.3390/risks12030048

APA StyleMilidonis, A., & Chisholm, K. (2024). The Regime-Switching Structural Default Risk Model. Risks, 12(3), 48. https://doi.org/10.3390/risks12030048