1. Introduction

Warrants give the holder the right but not the obligation to purchase or sell the underlying assets by a specific date for a certain cost. Be that as it may, this right is not free. The warrant is one sort of exceptional option and it can be ordered in many types. Warrants can be partitioned into American warrants and European warrants as indicated by the distinction of the lapse date. Furthermore, they may be partitioned into call warrants and put warrants as indicated by the distinction of activity method. They may also be partitioned into equity warrants and covered warrants, agreeing with the distinction of the issuer. Covered warrants are as a rule given by sellers, which do not raise the organization’s capital stock after their lapse dates. Valuing for this sort of warrant is like evaluating for normal options and, subsequently, numerous specialists use the Black–Scholes model [

1] to value this sort of warrant. Yet, the value warrants are generally given by the recorded organization and the underlying capital is the given stock of its organization. The value warrants have a weakening impact and, consequently, valuing for this sort of warrant is in contrast to estimating for the standard European options in light of the fact that the organizations’ equity warrants need to give new stock to meet the solicitation of the warrants’ holder at the maturity date. All in all, the estimation cannot totally apply the works of art Black–Scholes model.

Uncertainty strategy was established by Liu [

2] in 2007, and it has turned into a part of obvious mathematics for demonstrating belief degrees. As a part of obvious mathematics to manage belief degrees, the uncertainty hypothesis will assume a significant part in financial hypothesis and practice. Liu [

3] started the pioneering work of uncertain finance in 2009. Thereafter, numerous analysts applied themselves to an investigation of financial issues by utilizing uncertainty strategy. For instance, Chen [

4] explored the American alternative estimating issue and determined the evaluating formulae for Liu’s uncertain stock model, and Chen and Gao [

5] presented an uncertain term structure model of interest rate. Plus, in view of uncertainty strategy, Chen, Liu, and Ralescu [

6] proposed an uncertain stock model with intermittent profits.

Previous studies of pricing equity warrants were mainly carried out with the method of stochastic finance based on the probability theory, and the firm price was usually assumed to follow some stochastic differential equation [

7,

8,

9]. However, many empirical investigations showed that the firm value does not behave randomly, and it is often influenced by the belief degrees of investors since investors usually make their decisions based on the degrees of belief rather than the probabilities. For example, one of the key elements in the Nobel Prize-winning theory of Kahneman and Tversky [

10,

11] is the finding of probability distortion which showed that decision makers usually make their decisions based on a nonlinear transformation of the probability scale rather than the probability itself, and people often overweight small probabilities and underweight large probabilities. Actually, we know that investors’ belief degrees play an important role in decision making for financial practice [

12,

13,

14]. Although a few models have been utilized in an equity warrant pricing, applying an uncertain stock strategy has not been considered. In this paper, inside the system of uncertain hypotheses, we examine the pricing issue of equity warrants. Based on the suspicion that the stock price satisfies an uncertain differential equation, we derive an uncertain model for estimating equity warrants.

The remainder of the paper is organized as follows: Some fundamental ideas of uncertain processes are reviewed in

Section 2. In

Section 3, a short presentation of an uncertain stock model is given. An uncertain value warrants model is proposed in

Section 4. Finally, a concise rundown is given in

Section 5.

3. Uncertain Stock Model

Since the pioneer papers of Black, Scholes, and Merton on option evaluation were distributed in the mid-1970s, as a significant instrument, the Black–Scholes model was broadly utilized for estimating the financial derivatives by numerous specialists in which the stock value measure was portrayed by a stochastic differential equation as follows:

where

is the bond price,

is the stock price,

r is the riskless interest rate,

is the log-drift,

is the log-diffusion, and

is a Wiener process.

Nonetheless, this assumption was tested among others by Liu [

17] who proposed a contradiction showing that utilizing stochastic differential equations to depict stock value processes is not sensible. As an alternate tenet, Liu [

3] generalized an uncertain differential equation to portray the fundamental stock value process and derived an uncertain stock model in which the bond value

and the stock cost

are described by

where

is a Liu process.

It follows from Equation (

2) that the stock price is

whose inverse uncertainty distribution is

4. The Pricing Model

Given an uncertainty space , we will suppose ideal conditions in the market for the firm’s value and for the equity warrants:

- (i)

There are no transaction costs or taxes and all securities are perfectly divisible.

- (ii)

Dividends are not paid during the lifetime of the outstanding warrants, and the sequential exercise of the warrants is not optimal for warrant holders.

- (iii)

The warrant-issuing firm is an equity firm with no outstanding debt.

- (iv)

The total equity value of the firm, during the lifetime of the outstanding warrants,

, satisfies Equation (

2).

In the case of equity warrants, the firm has

N shares of common stock and

M shares of equity warrants outstanding. Each warrant entitles the owner to receive

k shares of stock at time

T upon payment of

J, the payoff of equity warrants is given by

, where

is the value of the firm’s assets at time

T. Considering the time value of money resulting from the bond, the present value of this payoff is

Let

represent the price of the equity warrant. Then, the time-zero net return of the warrant holder is

On the other hand, the time-zero net return of the issuer is

The fair price of this contract should make the holder of the equity warrant and the bank have an identical expected return, i.e.,

Thus, the price of an equity warrant can be defined as follows.

Definition 8. Assume that there is a firm financed by N shares of stock and M shares of equity warrants. Each warrant gives the holder the right to buy k shares of stock at time in exchange for payment of an amount J. Let be the asset value of the firm at time t. Then, the equity warrant price is Theorem 6. Based on all information from Definition (8), the price of an equity warrant at time t is given bywhere the optimal solutions and satisfy the following system of nonlinear equations: Proof. Solving the ordinary differential equation

where

and

is the inverse standard normal uncertainty distribution, we have

That means that the uncertain differential equation

has an

-path

Since

is an increasing function, it follows from Theorem 5 and Definition (8) that the equity warrant price is

It is shown that the warrant pricing formula mentioned above depends on and , which are unobservable. To obtain a pricing formula using observable values, we will make use of the following result.

Let

be the stock’s elasticity, which gives the percentage change in the stock’s value for a percentage change in the firm’s value. Then, from a standard result in option pricing theory, we have

From assumption (iii), we obtain

. Consequently, we have

Now, from (

5) and (

6), it follows that

□

Theorem 7. If . Then, the nonlinear system (4) has a solution . Proof. First, it is clear that for any

, there exists a unique

which satisfies

Define a map

, which is given by an implicit function

The function

is increasing when

since the following inequality holds:

The inequality holds true because the function is an increasing function of .

Second, it is obvious that for any

, there exists a unique

, which satisfies

Define a map

, which is given by an implicit function

Function h is strictly continuous in for all positive . Moreover, for all , and . Thus, we have

- (1)

g is one to one, continuous, and strictly increasing;

- (2)

h is continuous and attains any value in .

Hence, the intersection of g and h exists. This completes the proof. □

Different from a stochastic differential equation, an uncertain differential equation is driven by a Liu process. As a type of differential equation involving an uncertain process, it is very useful to deal with a dynamical process with uncertainty.

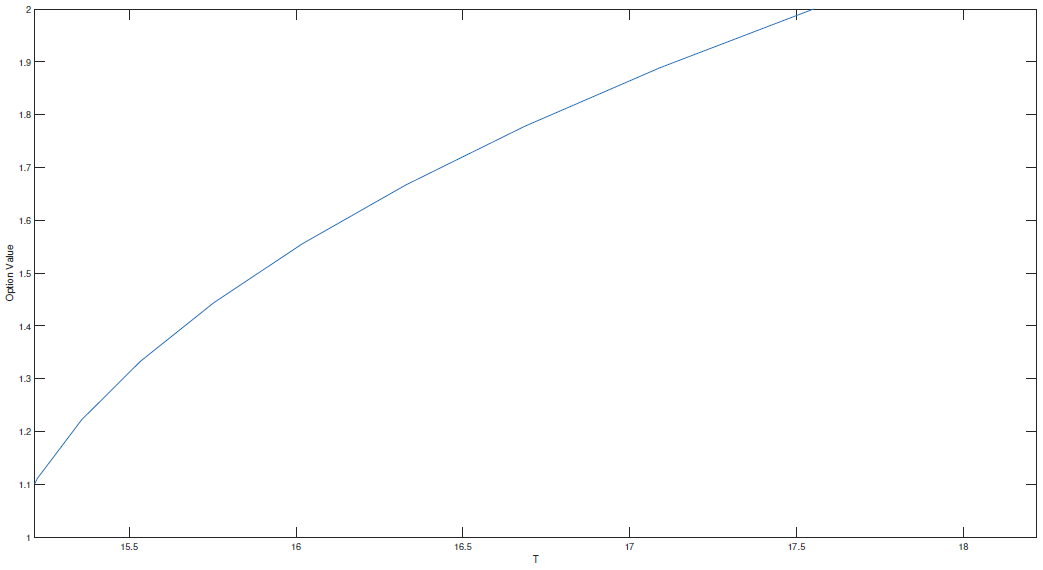

Figure 1 indicates that the equity warrant value is an increasing function with respect to the time

T when other parameters remain unchanged. This is because the longer the time, the more likely it is to be executed and the higher the price of the equity warrant. This law is common sense in the financial markets.

Example 1. Let . Then, based on approximations and , the value of the equity warrant is

{kind=link}