Fintechs and Institutions: A Systematic Literature Review and Future Research Agenda

, ,

, ,  ,

,  and

and

Abstract

:1. Introduction

2. Theoretical Background

2.1. Fintechs: Emergence and Conceptual Evolution

2.2. Institutions

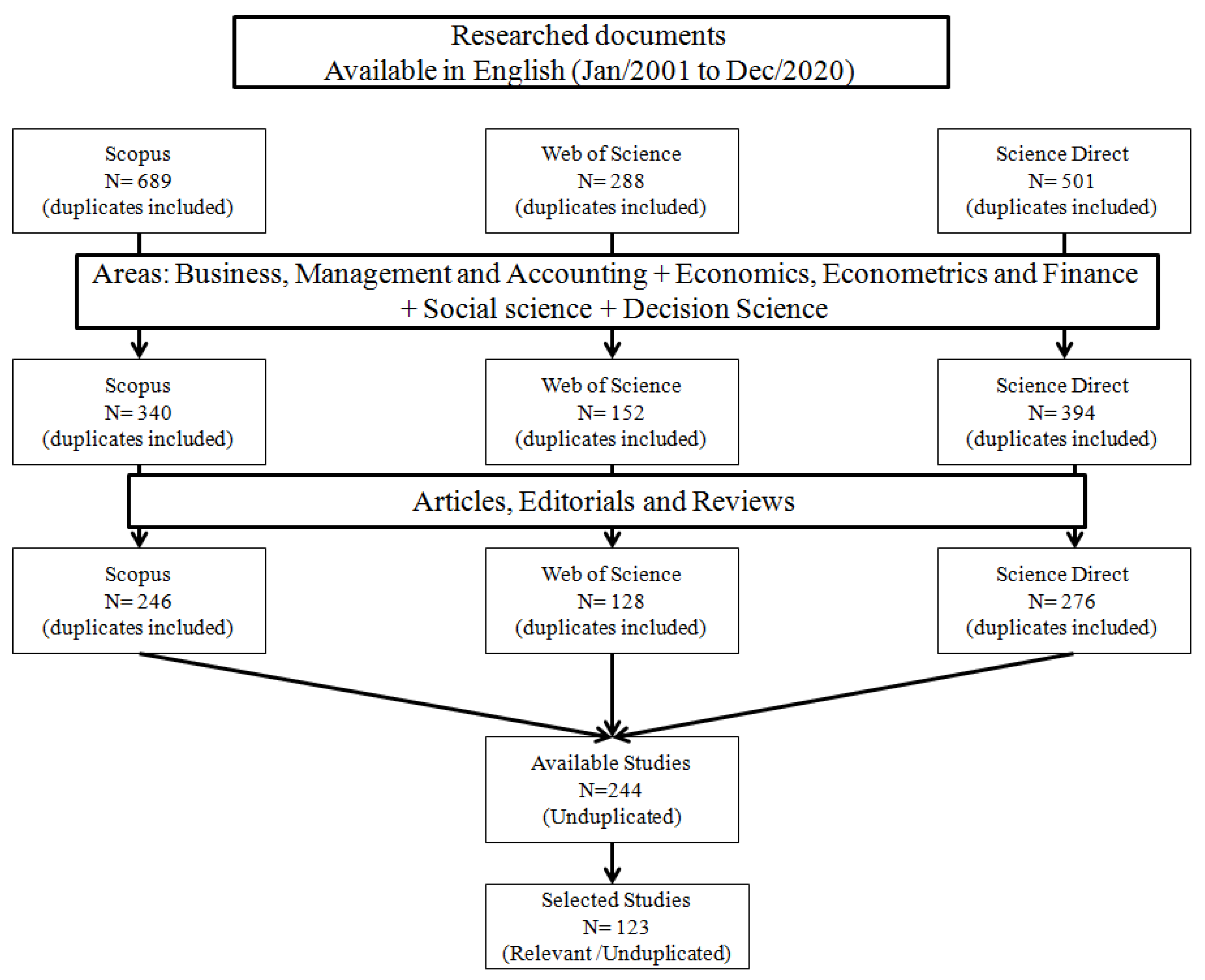

3. Method

4. Results

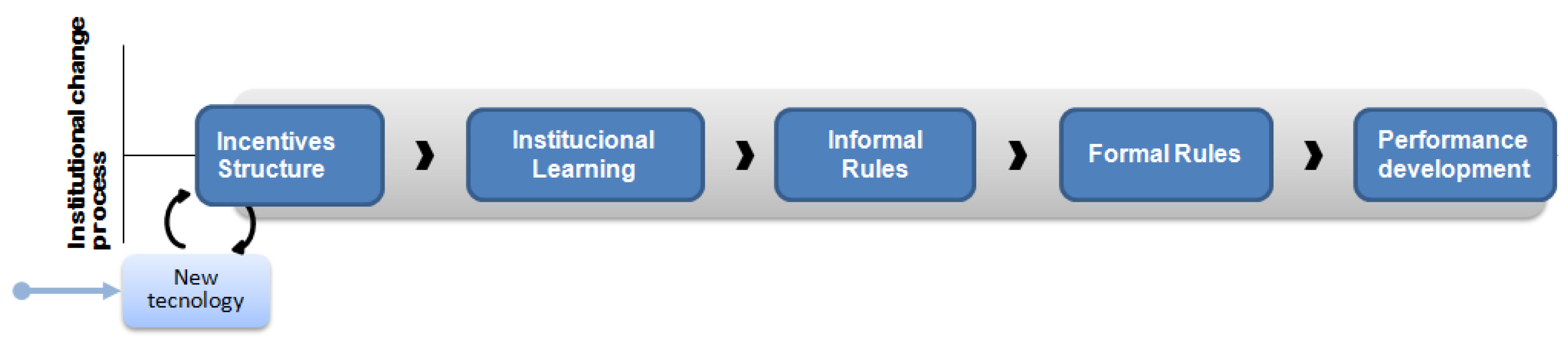

4.1. Stages of Institutional Change

4.2. Dematerialization of Access

4.3. Operational Architecture

4.4. Transactional Regulation

4.5. Transactional Efficiency

5. Analysis of Results

5.1. An Integrative Framework

5.2. Insights about the Dimensions

5.2.1. Dematerialization of Access

5.2.2. Operational Architecture

5.2.3. Transactional Regulation

5.2.4. Transactional Efficiency

5.3. Propositions

5.4. Research Agenda

6. Final Considerations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| N | Title | Authors | Year |

|---|---|---|---|

| 1 | A 2020 perspective on “A fair contract signing protocol with blockchain support” | Josep-Lluis Ferrer-Gomila, Maria Francisca Hinarejos | 2020 |

| 2 | A Tale of Two Markets: How Lower-end Borrowers Are Punished for Bank Regulatory Failures in Nigeria | Philemon Omede | 2020 |

| 3 | A truly future-oriented legal framework for fintech in the EU. | Kapsis, I. | 2020 |

| 4 | Archiving and digitizing of customer records of golden rural bank of the Philippines, Inc. | Princess May Subia, Reynaldo Corpuz | 2020 |

| 5 | Artificial intelligence and automation in financial services: The case of Russian banking sector | Goncharenko, Andrea Miglionico | 2020 |

| 6 | Bank financial capability on MSME lending amid economic change and the growth of Fintech companies in Indonesia | Martino Wibowo, Vesarach Aumeboonsuke | 2020 |

| 7 | Banking and regulatory responses to fintech revisited—Building the sustainable financial service ‘ecosystems’ of tomorrow. | Fenwick, M., & Vermeulen, E. P. | 2020 |

| 8 | Banking goes digital: The adoption of FinTech services by German households | Moritz Jünger, Mark Mietzner | 2020 |

| 9 | Banking on Blockchain: An Evaluation of Innovation Decision Making | Priya Dozier, Troy Montgomery | 2020 |

| 10 | Banking sector earnings management using loan loss provisions in the Fintech era | Peterson Ozili | 2020 |

| 11 | Blockchain and insurance: a review for operations and regulation | Richard Brophy | 2020 |

| 12 | Blockchain disruption and decentralized finance: The rise of decentralized business models | Yan Chen, Cristiano Bellavitis | 2020 |

| 13 | Concealed Risks of FinTech and Goal-Oriented Responsive Regulation: China’s Background and Global Perspective. | Donggen, X. U., & Dawei, X. U. | 2020 |

| 14 | Conventional banks and Fintechs: how digitization has transformed both models | Elisabeth Paulet, Hareesh Mavoori | 2020 |

| 15 | Cooperative financial institutions: A review of the literature | Donal McKillop, Declan French, Barry Quinn, Anna Sobiech, John Wilson | 2020 |

| 16 | Decentralized finance | Dirk Zetzsche, Douglas Arner, Ross Buckley | 2020 |

| 17 | Digital cubic space as a new economic augmented reality | Natalia Kraus, Kateryna Kraus, Andrusiak | 2020 |

| 18 | Emergent role of fintech in financial landscape: A perspective on banking industry | Kumar, Agrawal, Aliza | 2020 |

| 19 | Financial inclusion research around the world: A review | Peterson Ozili | 2020 |

| 20 | Fintech and Financial Stability Potential Influence of FinTech on Financial Stability, Risks and Benefits | Milena Vučinić | 2020 |

| 21 | Fintech in financial reporting and audit for fraud prevention and safeguarding equity investments | Paulina Roszkowska | 2020 |

| 22 | FinTech, blockchain and Islamic finance: An extensive literature review | Mustafa Rabbani, Shahnawaz Khan, Eleftherios Thalassinos | 2020 |

| 23 | Fintech, financial inclusion and income inequality: a quantile regression approach | Ayse Demir, Vanesa Pesqué-Cela, Yener Altunbas, Victor Murinde | 2020 |

| 24 | Fintech: research directions to explore the digital transformation of financial service systems | Christoph Breidbach, Bryon Keating, Chiehyeon Lim | 2020 |

| 25 | From shadow banking to digital financial inclusion: China’s rise and the politics of epistemic contestation within the financial stability board | Peter Knaack, Julian Gruin | 2020 |

| 26 | Governing the gold rush into emerging markets: a case study of Indonesia’s regulatory responses to the expansion of Chinese-backed online P2P lending | Angela Tritto, Yujia He, Victoria Junaedi | 2020 |

| 27 | Granting access to real-time gross settlement systems in the fintech era | Bagio Bossone, Gynedi Srinivas, Holti Banka | 2020 |

| 28 | How individual investors react to negative events in the fintech era? Evidence from China’s peer-to-peer lending market | Xueru Chen, Xiaoji Hu, Shenglin Ben | 2020 |

| 29 | Impact of customers’ digital banking adoption on hidden defection: A combined analytical–empirical approach | Yoonseock Son, Hyeokko Kwon, Giri Tayi, Wonseok Oh | 2020 |

| 30 | Industry 4.0 in finance: the impact of artificial intelligence (ai) on digital financial inclusion | David Mhlanga | 2020 |

| 31 | Initial coin offerings (ICOs): Benefits, risks and success measures | Alfreda Šapkauskienė, Ingrida Višinskaitė | 2020 |

| 32 | Legal Governance on Fintech Risks: Effects and Lessons from Chinae | Yuan, K., & Duoqi, X. U | 2020 |

| 33 | Mobile money adoption and usage and financial inclusion: mediating effect of digital consumer protection | Okello Candiya Bongomin, G.,Ntayi | 2020 |

| 34 | New quality of financial institutions and business management | Nataliia Kraus, Kateryna Kraus, Valerii Osetskyi | 2020 |

| 35 | Not Just Another Shadow Bank: Chinese Authoritarian Capitalism and the ‘Developmental’ Promise of Digital Financial Innovation | Julian Gruin, Peter Knaack | 2020 |

| 36 | Regulating Fintech in the EU: the Case for a Guided Sandbox. | Ringe, W. G., & Christopher, R. U. O. F. | 2020 |

| 37 | Regulation and Recent Trends in High-Interest Credit Markets. | Malone, C., & Skiba, P. M. | 2020 |

| 38 | Regulatory Technology: Replacing Law with Computer Code | Eva Micheler, Anna Whaley | 2020 |

| 39 | Responsible AI-based Credit Scoring–A Legal Framework. | Langenbucher, K | 2020 |

| 40 | Risk spillovers between FinTech and traditional financial institutions: Evidence from the U.S. | Jianping Li, Jingyu Li, Xiaoqian Zhu, Yinhong Yao, Barbara Casu | 2020 |

| 41 | Technology v Technocracy: Fintech as a Regulatory Challenge | Saule Omarova | 2020 |

| 42 | The data sharing paradox: BigTechs in finance | Oscar Borgogno, Giuseppe Colangelo | 2020 |

| 43 | The Development and Regulation of Cryptoassets: Hong Kong Experiences and a Comparative | Robin Huang, Demin Yang, Ferdinand Loo | 2020 |

| 44 | The Disruptive Effect of Distributed Ledger Technology and Blockchain in the over the counter derivatives market. | Paolini, A. | 2020 |

| 45 | The effects of eliminating Riba in foreign currency transactions by introducing global FinTech network | Mohammad Selim | 2020 |

| 46 | The European Union Proposal for a Regulation on Cross-Border Crowdfunding Services: A Solemn or Pie-Crust Promise? | Staikouras, P | 2020 |

| 47 | The impact of the revised payment services directive on the market for payment initiation services | Bruno Yawe, Ibrahim Mukisa | 2020 |

| 48 | The Innovation Research of Contract Farming Financing Mode under the Block Chain Technology | Dehua Zhang | 2020 |

| 49 | The payment systems revolution: India’s story | Narendra Kumar, Abhishek Thakur, Raghuraj, Lalit Mohan | 2020 |

| 50 | The Promise and Perils of Insurtech. | Lin, L., & Chen, C. C. | 2020 |

| 51 | The regulation of crypto-assets in the EU–investment and payment tokens under the radar. | Ferrari, V. | 2020 |

| 52 | The rise and rise of financial technology: The good, the bad, and the verdict | Nofie Iman, N. | 2020 |

| 53 | The Risks of Mobile Payment and Regulatory Responses: A Hong Kong Perspective. | Huang, R. H., Cheung, C. S. W., & Wang, C. M. L | 2020 |

| 54 | The road to RegTech: the (astonishing) example of the European Union | Ross Buckley, Douglas Arner, Dirk Zetzsche, Rolf Weber | 2020 |

| 55 | The small-dollar loan industry: a new era of regulatory reform—and emerging competition? | Thomas Hemphill | 2020 |

| 56 | Transformation needed—report on the 6th international conference on credit risk analysis and management | Simone Westerfeld, Beatrix Wullschleger | 2020 |

| 57 | Twenty-first Century Financial Regulation: P2P Lending, Fintech, and the Argument for a Special Purpose Fintech Charter Approach. | Luther, J. | 2020 |

| 58 | What have we learnt from 10 years of fintech research? a scientometric analysis | Jiajia Liu, Xuerong Li, Shouyang Wang | 2020 |

| 59 | What’s in the “Black Box”? Balancing Financial Inclusion and Privacy in Digital Consumer Lending. | Chou, A. | 2020 |

| 60 | A fair contract signing protocol with blockchain support | Josep-Lluis Ferrer-Gomila, Francisca Hinarejos, Andreu-Pere Isern-Deyà | 2019 |

| 61 | A great leap of faith: the cashless agenda in Digital India. | Athique, A. | 2019 |

| 62 | Competition and stability in modern banking: A post-crisis perspective | Xavier Vives | 2019 |

| 63 | Credit intermediation and the European internal market for mortgage credit | Diederik Bruloot, Evariest Callens, Michiel De Muynck | 2019 |

| 64 | Cross-border regulation and fintech: are transnational cooperation agreements the right way to go? | Ivanova, P. | 2019 |

| 65 | Dematerialization of banking products and services in the digital era | Shahrazad Hadad, Constantin Bratianu | 2019 |

| 66 | Digital Payments: Impact Factors and Mass Adoption in Sub-Saharan Africa | Leigh Soutter, Kenzie Ferguson, Michael Neubert | 2019 |

| 67 | Do digital technologies have the power to disrupt commercial banking? | Golubić, G | 2019 |

| 68 | Encouraging Entrepreneurship and Economic Growth | David Ahlstrom, Amber Chang, Jessie Cheung | 2019 |

| 69 | FinTech on the dark web: The rise of cryptos. | Todorof, M. | 2019 |

| 70 | FinTech sector and banking business: competition or symbiosis? | Mikhail Zveryakov, Sergii Sheludko, Elena Sharah, Victoria Kovalenko | 2019 |

| 71 | Fintechs: A literature review and research agenda | Eduardo Milian, Mauro de Spinola, Marly de Carvalho | 2019 |

| 72 | Following the cyber money trail: Global challenges when investigating ransomware attacks and how regulation can help | Angela Irwin, Caitlin Dawson, | 2019 |

| 73 | Funds sharing regulation in the context of the sharing economy: Understanding the logic of China’s P2P lending regulation | Tao Yu, Wei Shen | 2019 |

| 74 | Global Financial Regulation: Shortcomings and Reform Options | Emily Jones, Peter Knaack | 2019 |

| 75 | Mind the gap: the consideration of financial technologies and blockchain in the reform of the Vertical Agreements Block Exemption Regulation. | Chambers, L. M. | 2019 |

| 76 | Public Financial Law and digital economy. | Tsindeliani, I. | 2019 |

| 77 | Regulatory Fitness: Fintech, Funny Money, and Smart Contracts | Roger Brownsword | 2019 |

| 78 | Regulatory Sandboxes. | Allen, H. J. | 2019 |

| 79 | Success factors in Title III equity crowdfunding in the United States | Stanislav Mamonov, Ross Malaga | 2019 |

| 80 | The influence of financial innovations on eu countries banking systems development | Oleksiy Druhov, Vira Druhova, Olena Pakhnenko | 2019 |

| 81 | Virtual and cryptocurrencies—regulatory and anti-money laundering approaches in the European Union and in Switzerland | Frick, T. A. | 2019 |

| 82 | Complacency, capabilities, and institutional pressure: understanding financial institutions’ participation in the nascent mobile payments ecosystem | Kui Du | 2018 |

| 83 | Cooperative banking and digital transformation: towards a new relationship model with members and clients | Ricardo Palomo Zurdo, Yakira Fernández Torres, Milagros Gutiérrez Fernández | 2018 |

| 84 | Cross-Border Crowdfunding: Towards a Single Crowdlending and Crowdinvesting Market for Europe | Dirk Zetzsche, Christina Preiner | 2018 |

| 85 | Determinants of the financial services market functioning in the era of the informational economy development | Serhiy Shkarlet, Maksym Dubyna, Olena Zhuk | 2018 |

| 86 | Dialectic tensions in the financial markets: a longitudinal study of pre- and postcrisis regulatory technology | Wendy L. Currie, Daniel Gozman, Jonathan Seddon | 2018 |

| 87 | Evolutionary Approaches and the Construction of Technology-Driven Regulations | Dong Yang & Min Li | 2018 |

| 88 | Financial-return Crowdfunding and Regulatory Approaches in the Shadow Banking, FinTech and Collaborative Finance Era | Eugenia Macchiavello | 2018 |

| 89 | Fintech and regtech: Impact on regulators and banks | Ioannis Anagnostopoulos | 2018 |

| 90 | Fintech and the Future of the Payment Landscape: The Mobile Wallet Ecosystem A Challenge for Retail Banks? | Anna Eugenia Omarini | 2018 |

| 91 | Fintech ecosystem and landscape in Russia | Vladimir Soloviev | 2018 |

| 92 | Fintech risk management: A research challenge for artificial intelligence in finance | Paolo Giudici | 2018 |

| 93 | Fintech Venture Capital | Douglas Cumming, Armin Schwienbacher, | 2018 |

| 94 | Fintech: Ecosystem, business models, investment decisions, and challenges | In Lee, Yong Jae Shin | 2018 |

| 95 | From the Institutional to the Platform Economy | Aleksandr Sukhodolov, Yury Beryozkin | 2018 |

| 96 | Impact of digital finance on financial inclusion and stability | Peterson Ozili | 2018 |

| 97 | Information, incentives, and effects of risk-sharing on the real economy | Mark Liu, Wenfeng Wub, Tong Yu | 2018 |

| 98 | Institutional Changes And Ditigalization Of Business Operations In Financial Institutions | Elena Tarkhanova, Elena Chizhevskaya, Natalia Baburina | 2018 |

| 99 | Investor Platform Choice: Herding, Platform Attributes, and Regulations | Yang Jiang, Yi-Chun (Chad) Ho, Xiangbin Yan, Yong Tan | 2018 |

| 100 | Modeling of FinTech market development (on the example of Ukraine | Alina Bukhtiarova, Arsen Hayriyan, Nikol Bort, Andrii Semenog | 2018 |

| 101 | Propensity of contracting loans services from FinTech’s in Brazil | Luis Hernan Contreras-Pinochet, Guilherme Tongnole Diogo, Evandro Luiz Lopes, Eliane Herrero, Ricardo Luiz Pereira Bueno | 2018 |

| 102 | The emergence of the global fintech market: economic and technological determinants | Christian Haddad, Lars Hornuf | 2018 |

| 103 | The emerging Cloud Dilemma: Balancing innovation with cross-border privacy and outsourcing regulations | Daniel Gozman, Leslie Willcocksc | 2018 |

| 104 | The Impact of Selected Regulations on the Development of Payments Systems in Poland | Mateusz Folwarski | 2018 |

| 105 | The influence of financial technologies on the global financial system stability | Galyna Azarenkova, Iryna Shkodina, Borys Samorodov, Maksym Babenko, Iryna Onishchenko | 2018 |

| 106 | The opportunities of engaging FinTech companies into the system of crossborder money transfers in Ukraine | Yuriy Petrushenko, Liudmyla Kozarezenko, Aldona Glinska-Newes, Maryna Tokarenko, Maryna But | 2018 |

| 107 | The Payment Services Directive II and Competitiveness: The Perspective of European Fintech Companies | Inna Romānova, Simon Grima, Jonathan Spiteri, Marina Kudinska | 2018 |

| 108 | The Regulation of Initial Coin Offerings in China: Problems, Prognoses and Prospects | Hui Deng, Robin Hui Huang, Qingran Wu | 2018 |

| 109 | Catching up with Indonesia’s fintech industry | Kevin Davis, Rodney Maddock, Martin Foo | 2017 |

| 110 | Digital Finance and FinTech: current research and future research directions | Peter Gomber, Jascha-Alexander Koch, Michael Siering | 2017 |

| 111 | Fintech as financial innovation—The possibilities and problems of implementation | Svetlana Saksonova, Irina Kuzmina-Merlino | 2017 |

| 112 | FinTech, RegTech, and the Reconceptualization of Financial Regulation | Douglas Arner, Jànos Barberis, Ross Buckley | 2017 |

| 113 | Fintech, Regulatory arbitrage, and the rise of shadow banks | Greg Buchak, Gregor Matvos, Tomasz Piskorski, Amit Seru | 2017 |

| 114 | From digital currencies to digital finance: the case for a smart financial contract standard | Willi Brammertz, Allan I. Mendelowitz | 2017 |

| 115 | Future living framework: Is blockchain the next enabling network? | Maria-Lluïsa, Marsal-Llacuna | 2017 |

| 116 | Payment innovations in Poland: a new approach of the banking sector to introducing payment solutions | Michał Polasik, Dariusz Piotrowski | 2017 |

| 117 | The digital revolution in financial inclusion: international development in the fintech era | Daniela Gabor, Sally Brooks | 2017 |

| 118 | The transition from traditional banking to mobile internet finance: an organizational innovation perspective—a comparative study of Citibank and ICBC | Zhuming Chen, Yushan Li, Yawen Wu, Junjun Luo | 2017 |

| 119 | Entry of FinTech Firms and Competition in the Retail Payments Market | Jooyong Jun, Eunjung Yeo | 2016 |

| 120 | FinTech in China: From Shadow Banking to P2P Lending | Jànos Barberis, Douglas Arner | 2016 |

| 121 | FinTech in Taiwan: a case study of a Bank’s strategic planning for an investment in a FinTech company | Jui-Long Hung, Binjie Luo | 2016 |

| 122 | New factors inducing changes in the retail banking customer relationship management (CRM) and their exploration by the FinTech industry | Marcin Kotarba | 2016 |

| 123 | Payment innovations in poland: the role of payment services in the strategies of commercial banks | Michal Polasik, Dariusz Piotrowski | 2016 |

References

- Lee, I.; Shin, Y.J. Fintech: Ecosystem, business models, investment decisions, and challenges. Bus. Horiz. 2018, 61, 35–46. [Google Scholar] [CrossRef]

- Zavolokina, L.; Dolata, M.; Schwabe, G. The fintech phenomenon: Antecedents of financial innovation perceived by the popular press. Financ. Innov. 2016, 2, 16. [Google Scholar] [CrossRef] [Green Version]

- Soloviev, V.I. Fintech Ecosystem and Landscape in Russia. J. Rev. Glob. Econ. 2018, 7, 377–390. [Google Scholar] [CrossRef]

- Gozman, D.; Willcocks, L. The emerging cloud dilemma: Balancing innovation with cross-border privacy and outsourcing regulations. J. Bus. Res. 2019, 97, 235–256. [Google Scholar] [CrossRef]

- Li, J.P.; Naqvi, B.; Rizvi SK, A.; Chang, H.L. Bitcoin: The biggest financial innovation of fourth industrial revolution and a portfolio’s efficiency booster. Technol. Forecast. Soc. Chang. 2021, 162, 120383. [Google Scholar] [CrossRef]

- Muganyi, T.; Yan, L.; Yin, Y.; Sun, H.; Gong, X.; Taghizadeh-Hesary, F. Fintech, regtech, and financial development: Evidence from China. Financ. Innov. 2022, 8, 29. [Google Scholar] [CrossRef]

- Irwin, A.S.; Dawson, C. Following the cyber money trail: Global challenges when investigating ransomware attacks and how regulation can help. J. Money Laund. Control 2017, 22, 110–131. [Google Scholar] [CrossRef]

- Allen, F.; Gu, X.; Jagtiani, J. Fintech, Cryptocurrencies, and CBDC: Financial Structural Transformation in China. J. Int. Money Financ. 2022, 124, 102625. [Google Scholar] [CrossRef]

- Breidbach, C.F.; Tana, S. Betting on bitcoin: How social collectives shape cryptocurrency markets. J. Bus. Res. 2021, 122, 311–320. [Google Scholar] [CrossRef]

- Senyo, P.K.; Effah, J.; Osabutey, E.L. Digital platformisation as public sector transformation strategy: A case of Ghana’s paperless port. Technol. Forecast. Soc. Chang. 2021, 162, 120387. [Google Scholar] [CrossRef]

- Brophy, R. Blockchain and insurance: A review for operations and regulation. J. Financ. Regul. Compliance 2019, 28, 215–234. [Google Scholar] [CrossRef]

- Akartuna, E.A.; Johnson, S.D.; Thornton, A. Preventing the money laundering and terrorist financing risks of emerging technologies: An international policy Delphi study. Technol. Forecast. Soc. Chang. 2022, 179, 121632. [Google Scholar] [CrossRef]

- Chen, Y.; Bellavitis, C. Blockchain disruption and decentralized finance: The rise of decentralized business models. J. Bus. Ventur. Insights 2020, 13, e00151. [Google Scholar] [CrossRef]

- Deng, H.; Huang, R.H.; Wu, Q. The regulation of initial coin offerings in China: Problems, prognoses and prospects. Eur. Bus. Organ. Law Rev. 2018, 19, 465–502. [Google Scholar] [CrossRef]

- Murinde, V.; Rizopoulos, E.; Zachariadis, M. The impact of the FinTech revolution on the future of banking: Opportunities and risks. Int. Rev. Financ. Anal. 2022, 81, 102103. [Google Scholar] [CrossRef]

- Vives, X. Competition and stability in modern banking: A post-crisis perspective. Int. J. Ind. Organ. 2019, 64, 55–69. [Google Scholar] [CrossRef]

- Arner, D.W.; Barberis, J.; Buckley, R.P. FinTech, regtech, and the reconceptualization of financial regulation. Northwestern J. Int. Law Bus. 2017, 37, 371. [Google Scholar]

- Cao, T.; Cook, W.D.; Kristal, M.M. Has the technological investment been worth it? Assessing the aggregate efficiency of non-homogeneous bank holding companies in the digital age. Technol. Forecast. Soc. Chang. 2022, 178, 121576. [Google Scholar] [CrossRef]

- Kraus, K.; Kraus, N.; Osetskyi, V. New quality of financial institutions and business management. Balt. J. Econ. Stud. 2020, 6, 59–66. [Google Scholar] [CrossRef]

- Gozman, D.; Hedman, J.; Sylvest, K. Open banking: Emergent roles, risks & opportunities. In Proceedings of the 26th European Conference on Information Systems, ECIS 2018, Portsmouth, UK, 23–28 June 2018; Association for Information Systems: Atlanta, Georgia, 2018. [Google Scholar]

- Tarkhanova, E.; Chizhevskaya, E.; Baburina, N. Institutional changes and ditigalization of business operations in financial institutions. J. Inst. Stud. 2018, 4, 145–155. [Google Scholar] [CrossRef]

- Puschmann, T. Fintech. Bus. Inf. Syst. Eng. 2017, 59, 69–76. [Google Scholar] [CrossRef]

- Thakor, A.V. Fintech and banking: What do we know? J. Financ. Intermediation 2019, 41, 100833. [Google Scholar] [CrossRef]

- Yu, T.; Shen, W. Funds sharing regulation in the context of the sharing economy: Understanding the logic of China’s P2P lending regulation. Comput. Law Secur. Rev. 2019, 35, 42–58. [Google Scholar] [CrossRef]

- Zetzsche, D.; Preiner, C. Cross-Border Crowdfunding: Towards a Single Crowdlending and Crowdinvesting Market for Europe. Eur. Bus. Organ. Law Rev. 2018, 19, 217–251. [Google Scholar] [CrossRef]

- Brownsword, R. Regulatory fitness: Fintech, funny money, and smart contracts. Eur. Bus. Organ. Law Rev. 2019, 20, 5–27. [Google Scholar] [CrossRef] [Green Version]

- Zachariadis, M.; Ozcan, P. The API Economy and Digital Transformation in Financial Services: The Case of Open Banking. 2017. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2975199 (accessed on 30 April 2022).

- Uddin, M.H.; Mollah, S.; Ali, M.H. Does cyber tech spending matter for bank stability? Int. Rev. Financ. Anal. 2020, 72, 101587. [Google Scholar] [CrossRef]

- Gomber, P.; Koch, J.A.; Siering, M. Digital finance and fintech: Current research and future research directions. J. Bus. Econ. 2017, 87, 537–580. [Google Scholar] [CrossRef]

- Muthukannan, P.; Tan, B.; Gozman, D.; Johnson, L. The emergence of a Fintech Ecosystem: A case study of the Vizag Fintech Valley in India. Inf. Manag. 2020, 57, 103385. [Google Scholar] [CrossRef]

- Milian, E.Z.; Spinola MD, M.; de Carvalho, M.M. Fintechs: A literature review and research agenda. Electron. Commer. Res. Appl. 2019, 34, 100833. [Google Scholar] [CrossRef]

- Nakashima, T. Creating credit by making use of mobility with FinTech and IoT. IATSS Res. 2018, 42, 61–66. [Google Scholar] [CrossRef]

- Szpringer, W. New Technologies and the Financial Sector: FinTech as an Opportunity and a Threat; Poltext: Warsaw, Poland, 2017; ISBN 9788375617801. [Google Scholar]

- Schueffel, P. The Concise Fintech Compendium; School of Management Fribourg: Fribourg, Switzerland, 2017. [Google Scholar]

- Dorfleitner, G.; Hornuf, L.; Schmitt, M.; Weber, M. Definition of FinTech and Description of the FinTech Industry. In FinTech in Germany; Springer: Cham, Switzerland, 2017; pp. 5–10. [Google Scholar]

- Jun, J.; Yeo, E. Entry of fintech firms and competition in the retail payments market. Asia-Pac. J. Financ. Stud. 2016, 45, 159–184. [Google Scholar] [CrossRef]

- Shen, Y.; Huang, Y. Introduction to the special issue: Internet finance in China. China Econ. J. 2016, 9, 221–224. [Google Scholar] [CrossRef] [Green Version]

- Čižinská, R.; Krabec, T.; Venegas, P. FieldsRank: The Network Value of the Firm. Int. Adv. Econ. Res. 2016, 22, 461–463. [Google Scholar] [CrossRef]

- Kawai, Y. Fintech and the IAIS. In IAIS Newsletter; International Association of Insurance Supervisors: Basel, Switzerland, 2016; p. 1. [Google Scholar]

- Micu, I.; Micu, A. Financial technology (fintech) and its implementation on the Romanian non-banking capital market. SEA-Pract. Appl. Sci. 2016, 11, 379–384. [Google Scholar]

- Maier, E. Supply and demand on crowdlending platforms: Connecting small and medium-sized enterprise borrowers and consumer investors. J. Retail. Consum. Serv. 2016, 33, 143–153. [Google Scholar] [CrossRef]

- Lee, T.H.; Kim, H.W. An exploratory study on fintech industry in Korea: Crowdfunding case. In Proceedings of the 2nd International Conference on Innovative Engineering Technologies (ICIET’2015), Bangkok, Thailand, 7–8 August 2015. [Google Scholar]

- Arner, D.W.; Barberis, J.; Buckley, R.P. The evolution of Fintech: A new post-crisis paradigm. Geo. J. Int’l L. 2015, 47, 1271. [Google Scholar] [CrossRef] [Green Version]

- Lee, D.K.C.; Teo, E.G.S. Emergence of Fintech and the Lasic Principles. J. Financ. Perspect. 2015, 3, 1–26. Available online: https://ink.library.smu.edu.sg/cgi/viewcontent.cgi?article=6071&context=lkcsb_research (accessed on 30 April 2022). [CrossRef] [Green Version]

- Barberis, J. The Rise of Fintech: Getting Hong Kong to Lead the Digital Financial Transition in APAC; Fintech: Hong Kong, 2014. [Google Scholar]

- Langley, P.; Leyshon, A. The platform political economy of fintech: Reintermediation, consolidation and capitalisation. New Political Econ. 2021, 26, 376–388. [Google Scholar] [CrossRef]

- Xie, P.; Zou, C. The Theory of Internet Finance. China Econ. 2013, 8, 1–15. [Google Scholar]

- Liu, J.; Li, X.; Wang, S. What have we learnt from 10 years of fintech research? a scientometric analysis. Technol. Forecast. Soc. Change 2020, 155, 120022. [Google Scholar] [CrossRef]

- Huang, Y.; Zhang, L.; Li, Z.; Qiu, H.; Sun, T.; Wang, X.; Berger, H. Fintech Credit Risk Assessment for SMEs: Evidence from China; IMF Working Papers; International Monetary Fund: Washington, DC, USA, 2020. [Google Scholar]

- Gozman, D.; Liebenau, J.; Mangan, J. The innovation mechanisms of fintech start-ups: Insights from SWIFT’s innotribe competition. J. Manag. Inf. Syst. 2018, 35, 145–179. [Google Scholar] [CrossRef]

- Fuster, A.; Plosser, M.; Schnabl, P.; Vickery, J. The role of technology in mortgage lending. Rev. Financ. Stud. 2019, 32, 1854–1899. [Google Scholar] [CrossRef] [Green Version]

- Chen, Z.; Li, Y.; Wu, Y.; Luo, J. The transition from traditional banking to mobile internet finance: An organizational innovation perspective-a comparative study of Citibank and ICBC. Financ. Innov. 2017, 3, 12. [Google Scholar] [CrossRef]

- Ventura, A.; Koenitzer, M.; Stein, P.; Tufano, P.; Drummer, D. The Future of FinTech: A paradigm shift in small business finance. In Global Agenda Council on the Future of Financing and Capital; World Economic Forum: Cologny, Switzerland, 2015. [Google Scholar]

- Voigt, S. How (not) to measure institutions. J. Inst. Econ. 2013, 9, 35–37. [Google Scholar] [CrossRef] [Green Version]

- DiMaggio, P.J.; Powell, W.W. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef] [Green Version]

- Veblen, T. The Theory of the Leisure Class, an Economic Study in the Evolution of Institutions; Macmillan: New York, NY, USA, 1899; p. 2. [Google Scholar]

- North, D. Institutions, Institutional Change and Economic Performance; Cambridge University Press: Cambridge, UK; New York, NY, USA, 1990. [Google Scholar]

- Hodgson, G.M. What are institutions? J. Econ. Issues 2006, 40, 1–25. [Google Scholar] [CrossRef]

- North, D.C. Institutions. J. Econ. Perspect. 1991, 5, 97–112. [Google Scholar] [CrossRef]

- Tranfield, D.; Denyer, D.; Smart, P. Towards a methodology for developing evidence-informed management knowledge by means of systematic review. Br. J. Manag. 2003, 14, 207–222. [Google Scholar] [CrossRef]

- Liao, Y.; Deschamps, F.; Loures, E.D.F.R.; Ramos, L.F.P. Past, present and future of Industry 4.0-a systematic literature review and research agenda proposal. Int. J. Prod. Res. 2017, 55, 3609–3629. [Google Scholar] [CrossRef]

- Ozili, P.K. Impact of digital finance on financial inclusion and stability. Borsa Istanb. Rev. 2018, 18, 329–340. [Google Scholar] [CrossRef]

- Petrushenko, Y.; Kozarezenko, L.; Glinska-Newes, A.; Tokarenko, M.; But, M. The opportunities of engaging fintech companies into the system of cross-border money transfers in Ukraine. Invest. Manag. Financ. Innov. 2018, 15, 332–344. [Google Scholar] [CrossRef]

- Haddad, C.; Hornuf, L. The emergence of the global fintech market: Economic and technological determinants. Small Bus. Econ. 2019, 53, 81–105. [Google Scholar] [CrossRef] [Green Version]

- Junger, M.; Mietzner, M. Banking goes digital: The adoption of fintech services by German households. Financ. Res. Lett. 2019, 34, 101260. [Google Scholar] [CrossRef]

- Jiang, Y.; Ho, Y.C.; Yan, X.; Tan, Y. Investor platform choice: Herding, platform attributes, and regulations. J. Manag. Inf. Syst. 2018, 35, 86–116. [Google Scholar] [CrossRef]

- Shkarlet, S.; Dubyna, M.; Zhuk, O. Determinants of the financial services market functioning in the era of the informational economy development. Balt. J. Econ. Stud. 2018, 4, 349–357. [Google Scholar] [CrossRef]

- Shkodina, I.; Derid, I.; Zelenko, O. Digital transformation of global banking: Challenges and prospects. Financ. Credit. Act. Probl. Theory Pract. 2019, 3, 45–51. [Google Scholar]

- Bukhtiarova, A.; Hayriyan, A.; Bort, N.; Semenog, A. Modeling of fintech market development (on the Example OF Ukraine). Innov. Mark. 2018, 14, 34–45. [Google Scholar] [CrossRef] [Green Version]

- Saksonova, S.; Kuzmina-Merlino, I. Fintech as financial innovation–The possibilities and problems of implementation. Eur. Res. Stud. 2017, 20, 961–973. [Google Scholar] [CrossRef] [Green Version]

- Langenbucher, K. Responsible AI-based Credit Scoring–A Legal Framework. Eur. Bus. Law Rev. 2020, 31, 527–572. [Google Scholar] [CrossRef]

- Omede, P.I. A tale of two markets: How lower-end borrowers are punished for bank regulatory failures in Nigeria. J. Consum. Policy 2019, 43, 519–542. [Google Scholar] [CrossRef] [Green Version]

- Gabor, D.; Brooks, S. The digital revolution in financial inclusion: International development in the fintech era. New Political Econ. 2017, 22, 423–436. [Google Scholar] [CrossRef]

- Chou, A. What’s in the “Black Box”? Balancing Financial Inclusion and Privacy in Digital Consumer Lending. Duke Law J. 2020, 69, 1183–1217. [Google Scholar]

- Golubić, G. Do digital technologies have the power to disrupt commercial banking? J. Int. Eur. Law Econ. Mark. Integr. 2019, 6, 83–110. [Google Scholar] [CrossRef]

- Kotarba, M. New factors inducing changes in the retail banking customer relationship management (CRM) and their exploration by the fintech industry. Found. Manag. 2016, 8, 69–78. [Google Scholar] [CrossRef] [Green Version]

- Cuttino, N.Q. The rise of “fringetech”: Regulatory risks in earned-wage access. Northwestern Univ. Law Rev. 2021, 115, 1505–1579. [Google Scholar]

- Tsindeliani, I. Public Financial Law and digital economy. Media Cult. Public Relat. 2019, 10, 48–56. [Google Scholar] [CrossRef]

- Fenwick, M.; Vermeulen, E.P. Banking and regulatory responses to fintech revisited—Building the sustainable financial service ‘ecosystems’ of tomorrow. Singap. J. Leg. Stud. 2020, 2020, 165–189. [Google Scholar] [CrossRef]

- Anagnostopoulos, I. Fintech and regtech: Impact on regulators and banks. J. Econ. Bus. 2018, 100, 7–25. [Google Scholar] [CrossRef]

- Omarini, A.E. Fintech and the future of the payment landscape: The mobile wallet ecosystem. A challenge for retail banks? Int. J. Financ. Res. 2018, 9, 97–116. [Google Scholar] [CrossRef]

- Hadad, S.; Bratianu, C. Dematerialization of banking products and services in the digital era. Manag. Mark. Chall. Knowl. Soc. 2019, 14, 318–337. [Google Scholar] [CrossRef] [Green Version]

- Brammertz, W.; Mendelowitz, A.I. From digital currencies to digital finance: The case for a smart financial contract standard. J. Risk Financ. 2018, 19, 76–92. [Google Scholar] [CrossRef]

- Luther, J. Twenty-first Century Financial Regulation: P2P Lending, Fintech, and the Argument for a Special Purpose Fintech Charter Approach. Univ. Pa. Law Rev. 2020, 168, 1013. [Google Scholar]

- Todorof, M. FinTech on the dark web: The rise of cryptos. In Era Forum; Springer: Berlin/Heidelberg, Germany, 2019; Volume 20, pp. 1–20. [Google Scholar]

- Ivanova, P. Cross-border regulation and fintech: Are transnational cooperation agreements the right way to go? Unif. Law Rev. 2019, 24, 367–395. [Google Scholar] [CrossRef]

- Paolini, A. The Disruptive Effect of Distributed Ledger Technology and Blockchain in the over the counter derivatives market. Glob. Jurist 2020, 20. [Google Scholar] [CrossRef]

- Athique, A. A great leap of faith: The cashless agenda in Digital India. New Media Soc. 2019, 21, 1697–1713. [Google Scholar] [CrossRef]

- Liu, M.; Wu, W.; Yu, T. Information, incentives, and effects of risk-sharing on the real economy. Pac.-Basin Financ. J. 2018, 57, 101100. [Google Scholar] [CrossRef]

- Gruin, J.; Knaack, P. Not just another shadow bank: Chinese authoritarian capitalism and the ‘developmental’promise of digital financial innovation. New Political Econ. 2020, 25, 370–387. [Google Scholar] [CrossRef] [Green Version]

- Sukhodolov, A.P.; Beryozkin, Y.M. From the Institutional to the Platform Economy. Upravlenec 2018, 9, 8–13. [Google Scholar] [CrossRef]

- Buckley, R.P.; Arner, D.W.; Zetzsche, D.A.; Selga, E. The dark side of digital financial transformation: The new risks of fintech and the rise of techrisk. UNSW Law Res. Pap. 2019, 19–89. [Google Scholar] [CrossRef]

- Wu, L.; Xu, L. Venture capital certification of small and medium-sized enterprises towards banks: Evidence from China. Account. Financ. 2020, 60, 1601–1633. [Google Scholar] [CrossRef]

- Ringe, W.G.; Christopher, R.U.O.F. Regulating Fintech in the EU: The Case for a Guided Sandbox. Eur. J. Risk Regul. 2020, 11, 604–629. [Google Scholar] [CrossRef]

- Chambers, L.M. Mind the gap: The consideration of financial technologies and blockchain in the reform of the Vertical Agreements Block Exemption Regulation. Compet. Law J. 2019, 18, 116–121. [Google Scholar] [CrossRef]

- Micheler, E.; Whaley, A. Regulatory technology: Replacing law with computer code. Eur. Bus. Organ. Law Rev. 2019, 21, 349–377. [Google Scholar] [CrossRef] [Green Version]

- Ferrari, V. The regulation of crypto-assets in the EU–investment and payment tokens under the radar. Maastricht J. Eur. Comp. Law 2020, 27, 325–342. [Google Scholar] [CrossRef]

- Yang, D.; Li, M. Evolutionary approaches and the construction of technology-driven regulations. Emerg. Mark. Financ. Trade 2018, 54, 3256–3271. [Google Scholar] [CrossRef]

- Hung, J.L.; Luo, B. FinTech in Taiwan: A case study of a Bank’s strategic planning for an investment in a FinTech company. Financ. Innov. 2016, 2, 15. [Google Scholar] [CrossRef] [Green Version]

- Polasik, M.; Piotrowski, D. Payment innovations in Poland: A new approach of the banking sector to introducing payment solutions. Ekon. I Prawo. Econ. Law 2016, 15, 103–131. [Google Scholar] [CrossRef] [Green Version]

- Soutter, L.; Ferguson, K.; Neubert, M. Digital payments: Impact factors and mass adoption in sub-saharan Africa. Technol. Innov. Manag. Rev. 2019, 7, 41–55. [Google Scholar] [CrossRef]

- Druhov, O.; Druhova, V.; Pakhnenko, O.M. The influence of financial innovations on EU countries banking systems development. Mark. Manag. Innov. 2019, 3, 167–177. [Google Scholar] [CrossRef]

- Malone, C.; Skiba, P.M. Regulation and Recent Trends in High-Interest Credit Markets. Annu. Rev. Law Soc. Sci. 2020, 16, 311–326. [Google Scholar] [CrossRef]

- Allen, H.J. Regulatory Sandboxes. Georg. Wash. Law Rev. 2019, 87, 579–645. [Google Scholar]

- Hodson, D. The politics of FinTech: Technology, regulation, and disruption in UK and German retail banking. Public Adm. 2021, 99, 859–872. [Google Scholar] [CrossRef]

- Kumar, M.; Agrawal, S.; Aliza, F. Emergent role of fintech in financial landscape: A perspective on banking industry. Int. J. Sci. Technol. Res. 2020, 9, 4055–4058. [Google Scholar]

- Staikouras, P. The European Union Proposal for a Regulation on Cross-Border Crowdfunding Services: A Solemn or Pie-Crust Promise? Eur. Bus. Law Rev. 2020, 31, 1047–1122. [Google Scholar] [CrossRef]

- Ferrer-Gomila, J.L.; Hinarejos, M.F.; Isern-Deya, A.P. A fair contract signing protocol with blockchain support. Electron. Commer. Res. Appl. 2019, 36, 100869. [Google Scholar] [CrossRef]

- Lin, L.; Chen, C.C. The Promise and Perils of Insurtech. Singap. J. Leg. Stud. 2020, 115–142. Available online: https://ink.library.smu.edu.sg/cgi/viewcontent.cgi?article=5123&context=sol_research (accessed on 30 April 2022). [CrossRef]

- Huang, R.H.; Cheung CS, W.; Wang CM, L. The Risks of Mobile Payment and Regulatory Responses: A Hong Kong Perspective. Asian J. Law Soc. 2020, 7, 325–343. [Google Scholar] [CrossRef]

- Frick, T.A. Virtual and cryptocurrencies—regulatory and anti-money laundering approaches in the European Union and in Switzerland. In Era Forum; Springer: Berlin/Heidelberg, Germany, 2019; Volume 20, pp. 99–112. [Google Scholar]

- Giudici, P. Fintech risk management: A research challenge for artificial intelligence in finance. Front. Artif. Intell. 2018, 1, 1. [Google Scholar] [CrossRef] [Green Version]

- Kapsis, I. A truly future-oriented legal framework for fintech in the EU. Eur. Bus. Law Rev. 2020, 31, 475–514. [Google Scholar] [CrossRef]

- Yuan, K.; Duoqi, X.U. Legal Governance on Fintech Risks: Effects and Lessons from Chinae. Asian J. Law Soc. 2020, 7, 275–304. [Google Scholar] [CrossRef]

- Qureshi, F.; Rea, S.C.; Johnson, K.N. (Dis) Creating Claims of Financial Inclusion: The Integration of Artificial Intelligence in Consumer Credit Markets in the United States and Kenya. J. Int’l Comp. L. 2021, 8, 405. [Google Scholar]

- Nguyen, T.A.N. Does Financial Knowledge Matter in Using Fintech Services? Evidence from an Emerging Economy. Sustainability 2022, 14, 5083. [Google Scholar] [CrossRef]

- Vasenska, I.; Dimitrov, P.; Koyundzhiyska-Davidkova, B.; Krastev, V.; Durana, P.; Poulaki, I. Financial transactions using fintech during the COVID-19 crisis in Bulgaria. Risks 2021, 9, 48. [Google Scholar] [CrossRef]

- Ukwueze, F.O. Cryptocurrency: Towards regulating the unruly Enigma of Fintech in Nigeria and South Africa. Potchefstroom Electron. Law J. (PELJ) 2021, 24, 1–38. [Google Scholar] [CrossRef]

- Bavoso, V. Financial Intermediation in the Age of FinTech: P2P Lending and the Reinvention of Banking. Oxf. J. Leg. Stud. 2022, 42, 48–75. [Google Scholar] [CrossRef]

- Huang, S. Does FinTech improve the investment efficiency of enterprises? Evidence from China’s small and medium-sized enterprises. Econ. Anal. Policy 2022, 74, 571–586. [Google Scholar] [CrossRef]

- Dijmărescu, E. Towards a Fiduciary Digital Currency. Rom. J. Eur. Aff. 2021, 21, 5–18. [Google Scholar]

- Bin-Nashwan, S.A. Toward diffusion of e-Zakat initiatives amid the COVID-19 crisis and beyond. Foresight 2021, 24, 141–158. [Google Scholar] [CrossRef]

- Baumeister, B.M. La pignoración de cuentas de centralización de tesorería y la noción de ‘control’como requisito de aportación de la garantía financiera. Cuad. De Derecho Transnacional 2022, 14, 767–790. [Google Scholar] [CrossRef]

- Tello-Gamarra, J.; Zawislak, P.A. Transactional capability: Innovation’s missing link. J. Econ. Financ. Adm. Sci. 2013, 18, 2–8. [Google Scholar] [CrossRef]

- Hernani-Merino, M.; Tello-Gamarra, J. Evidence of transactional capability in two different countries. Eur. Bus. Rev. 2019, 31, 470–487. [Google Scholar] [CrossRef]

- Popova, Y. Economic Basis of Digital Banking Services Produced by FinTech Company in Smart City. J. Tour. Serv. 2021, 12, 86–104. [Google Scholar] [CrossRef]

- Ionescu, L. Digital Data Aggregation, Analysis, and Infrastructures in FinTech Operations. Rev. Contemp. Philos. 2020, 19, 92–98. [Google Scholar]

- North, D. Understanding the process of economic change. In Understanding the Process of Economic Change; Princeton university press: Princeton, NJ, USA, 2005; pp. 1000–1004. [Google Scholar]

- Zveryakov, M.; Kovalenko, V.; Sheludko, S.; Sharah, E. FinTech sector and banking business: Competition or symbiosis? Econ. Ann.-XXI 2019, 175, 53–57. [Google Scholar] [CrossRef] [Green Version]

- Currie, W.L.; Gozman, D.P.; Seddon, J.J. Dialectic tensions in the financial markets: A longitudinal study of pre-and post-crisis regulatory technology. J. Inf. Technol. 2018, 33, 304–325. [Google Scholar] [CrossRef] [Green Version]

- Jones, E.; Knaack, P. Global financial regulation: Shortcomings and reform options. Global Policy. 2019, 10, 193–206. [Google Scholar] [CrossRef]

- Mamonov, S.; Malaga, R. Success factors in Title III equity crowdfunding in the United States. Electron. Commer. Res. Appl. 2018, 27, 65–73. [Google Scholar] [CrossRef] [Green Version]

| Source | Definition | Perspective | |

|---|---|---|---|

| 1 | [9] | “… are the primary actor to lead, manage, and respond to the formation of markets”. | Agents of the financial system |

| 2 | [30] | “… agents that interact with each other to provide a wide array of financial products and services to end customers”. | Agents of the financial system |

| 3 | [23] | “Fintech is the use of technology to provide new and improved financial services”. | Agents of the financial system |

| 4 | [31] | “innovative companies active in the financial industry making use of the availability of communication, the ubiquity of the internet, and the automated processing of information”. | Firms |

| 5 | [32] | “FinTech is a technology that uses IT in the financial world. FinTech therefore refers to new technological solutions that will even initiate a revolutionary transformation in the world of finance”. | Products and services |

| 6 | [33] | “Fintech are companies that are a new, special category of para-banks”. | Firms |

| 7 | [34] | “… financial industry that applies technology to evolve financial activities”. | Agents of the financial system |

| 8 | [35] | “Fintech” denotes companies or representatives of companies that combine financial services with modern, innovative technologies”. | Firms |

| 9 | [36] | “Recent advances in information and communications technology (ICT) have led to the rapid development and expansion of new and innovative financial services, often termed Fintech”. | Products and services |

| 10 | [37] | “Internet finance, which is often referred to as ‘digital finance’ and ‘fintech’ outside China, was coined by Xie e Zou (2012). | Products and services |

| 11 | [38] | “Fintech is na economic industry composed of companies that use technology to make financial services more efficient”. | Firms |

| 12 | [39] | “Technologically enabled financial innovation. It is giving rise to new business models, applications, processes and products. These could have a material effect on financial markets and institutions and the provision of financial services”. | Products and services |

| 13 | [40] | “Fintech is a new sector in the finance industry that incorporates the whole plethora of technology that is used in finance to facilitate trades, corporate business or interaction and services provided to the retail consumer”. | Agents of the financial system |

| 14 | [41] | “Driven by technological advances, new services models have developed in the financial industry which offer additional opportunities to customers. Under the common denominator ‘fintech’, these new business aim to challenge existing financial institutions by using technology to deliver value to the customer in na alternative way”. | Firms |

| 15 | [42] | “Fintech is conceptually defined as a new type of financial service based on IT companies’ broad types of users, which is combined with IT technology and other financial services like remittance, payment, asset management and so on. Fintech includes all the technical processes from upgrading financial software to programming a new type of financial software which can affect a whole process of finance service. Therefore fintech can improve the performance of financial services and spread the finance service combined with mobile environment”. | Products and services |

| 16 | [43] | “Financial technology” or “FinTech” refers to the use of technology to deliver financial solutions. The term’s origin can be traced to the early 1990s and referred to the “Financial Services Technology Consortium”, a project initiated by Citigroup in order to facilitate technological cooperation efforts. | Products and services |

| 17 | [44] | “FinTech refers to innovative financial services or products delivered via technology”. | Products and services |

| 18 | [45] | “Fintech refers to the application of technology within the financial industry. The sector covers a wide range of activities from payments to financial data and analysis, financial software, digitized processes and payment platforms”. | Products and services |

| 19 | [46] | “Technology applied to financial services has a significant impacto n our daily lives, frim facilitating payments for goods and services to providing the infrastructure essential to the operation of the world’s financial institutions”. | Products and services |

| 20 | [47] | “Beside indirect financing via commercial banks and direct financing through security markets, a third way to conduct financial activities will emerge, which we call ‘internet finance’”. | Agents of the financial system |

| Criterion | Criteria Dimensions |

|---|---|

| Inclusion |

|

| Exclusion |

|

| Dimensions | Definitions | Documents |

|---|---|---|

| Dematerialization of access | Democratic access to financial services, with digital literacy and inclusion | (8) (19) (20) (23) (24) (26) (28)–(30) (46) (59) (65) (66) (83) (96) (99) (101) (111) (115) (117) |

| Operational architecture | Operational routines in the financial system | (5) (6) (7) (9) (11)–(15) (17) (20) (22) (26) (27) (33) (35) (39) (44) (47)–(49) (51) (52) (54) (56)–(58) (60) (62) (67)–(70) (75) (82) (85) (91) (94) (95) (98) (100) (102) (105) (110) (113) (116) (118)–(120) (122) |

| Transactional regulation | Laws and rules that are formalized for the liquidation of financial transactions | (2) (3) (7) (11) (13) (15) (16) (25) (26) (32) (36)–(38) (41)–(43) (46) (47) (54) (55) (64) (72)–(78) (81) (86)–(89) (99) (107)–(109) (112) |

| Transactional efficiency | Improving dematerialized financial operations and using risk management | (1)–(4) (6) (10) (15) (18) (20) (21) (26) (27) (29) (31)–(34) (36) (37) (40) (42) (44) (50) (53) (58) (61) (63) (66) (69) (75) (79)–(81) (84) (87) (90) (92) (93) (97) (103)–(106) (109) (114) (121) (123) |

| Dimensions | Variables | References |

|---|---|---|

| Dematerialization of Access | Digital literacy Democratization of access Financial inclusion | [62,63,64,65] |

| Operational Architecture | Decentralized operations Financial incentives Elimination of intermediaries Creation of smart contracts | [13,26,66,67] |

| Transactional Regulation | Development of regulatory technology Regulatory platforms Integration of regulatory authorities | [7,26,29,69,98] |

| Transactional Efficiency | Shared economy Operation security Technological risk management | [1,19,21] |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tello-Gamarra, J.; Campos-Teixeira, D.; Longaray, A.A.; Reis, J.; Hernani-Merino, M. Fintechs and Institutions: A Systematic Literature Review and Future Research Agenda. J. Theor. Appl. Electron. Commer. Res. 2022, 17, 722-750. https://doi.org/10.3390/jtaer17020038

Tello-Gamarra J, Campos-Teixeira D, Longaray AA, Reis J, Hernani-Merino M. Fintechs and Institutions: A Systematic Literature Review and Future Research Agenda. Journal of Theoretical and Applied Electronic Commerce Research. 2022; 17(2):722-750. https://doi.org/10.3390/jtaer17020038

Chicago/Turabian StyleTello-Gamarra, Jorge, Diogo Campos-Teixeira, André Andrade Longaray, João Reis, and Martin Hernani-Merino. 2022. "Fintechs and Institutions: A Systematic Literature Review and Future Research Agenda" Journal of Theoretical and Applied Electronic Commerce Research 17, no. 2: 722-750. https://doi.org/10.3390/jtaer17020038

APA StyleTello-Gamarra, J., Campos-Teixeira, D., Longaray, A. A., Reis, J., & Hernani-Merino, M. (2022). Fintechs and Institutions: A Systematic Literature Review and Future Research Agenda. Journal of Theoretical and Applied Electronic Commerce Research, 17(2), 722-750. https://doi.org/10.3390/jtaer17020038