Incentive-Driven Information Sharing in Leasing Based on a Consortium Blockchain and Evolutionary Game

Abstract

:1. Introduction

- (1)

- How can the blockchain technically drive information sharing and storage between the SME (the “lessee”) and LF (the “lessor”)?

- (2)

- How to incentivize excellent lessees to share more information while expecting that rational lessees and lessors can both maximally benefit from the leasing business empowered by BCT.

- (3)

- How can the lessee and lessor adjust their behavior strategies to ensure that all parties’ payoffs reach equilibrium through continuous trial-and-error learning?

- (1)

- Our evolutionary game model is developed on the blockchain-based leasing business (specifically the operating lease) in manufacturing, which pays more attention to the SME’s leasing behavior (i.e., making the rental payment, reverting the leased asset, maintenance responsibility, and asset monitoring) dynamically changes with the BCT adoption/non-adoption strategy. This study can mitigate the shortcomings of today’s leasing management.

- (2)

- We provide a more comprehensive analysis demonstrating that the four factors of “information sharing, credit, incentive–penalty, and risk” dynamically impact the lessee’s complying performance on the LC and the lessor’s decision-making on BCT adoption. More importantly, we carefully consider technical barriers faced by the organizational players when implementing BCT, such as on-chain and off-chain storage overheads, leasing transaction verification overheads, and credit assessment in BCT.

- (3)

- Based on the game analysis, our experimental results can support LFs (the “lessor”) in comprehensively understanding how SMEs (the “lessee”) meet the obligations in the LC and give some implications to policymakers when designing a proper incentive mechanism on the lease.

2. Literature Review

2.1. Definition of Leasing

2.2. Blockchain Technology (BCT)

2.3. BCT Application in Leasing

2.4. Evolutionary Game Theory (EGT)

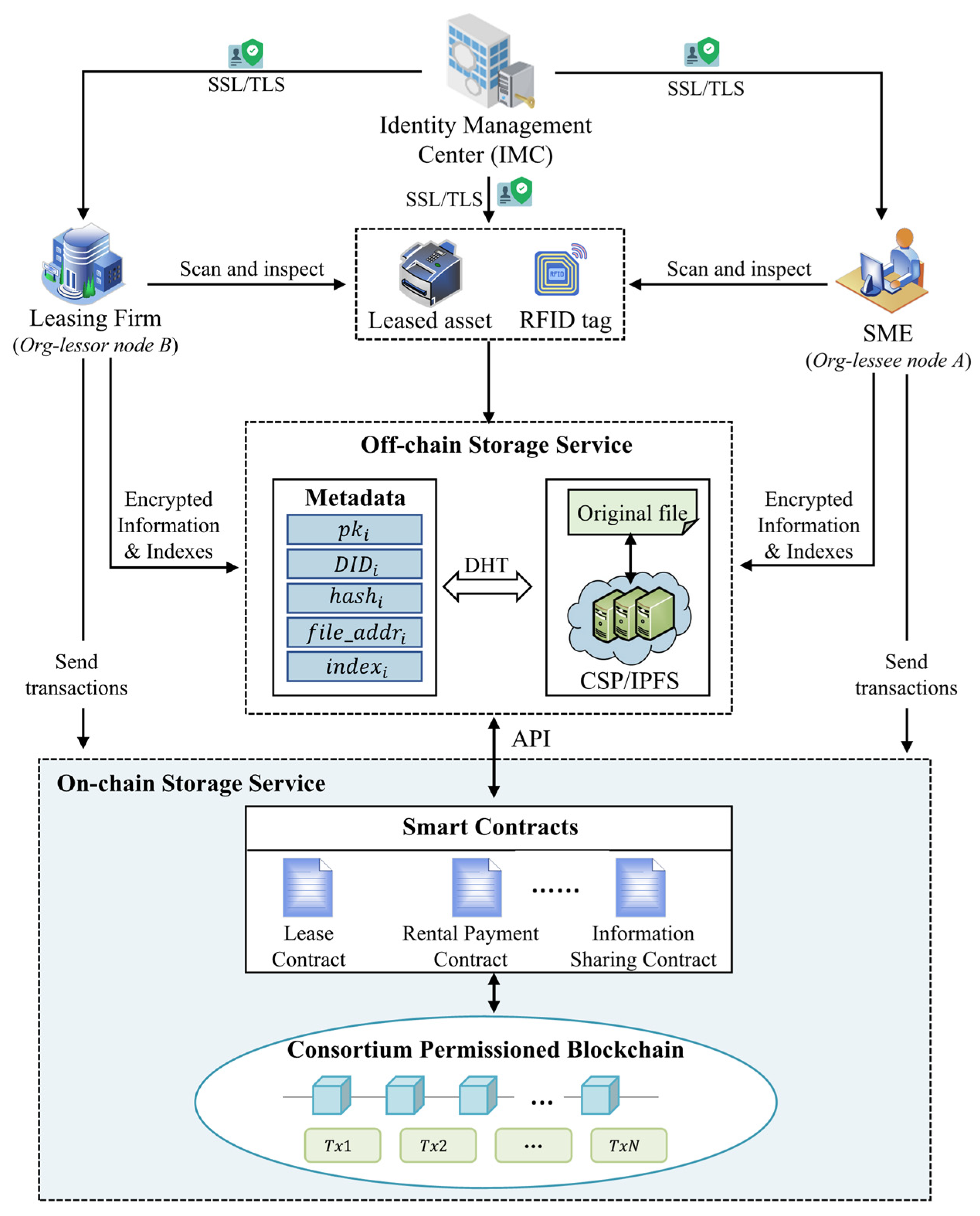

3. Description of Consortium Blockchain-Based Leasing Platform (CBLP)

3.1. Conceptual Architecture of CBLP

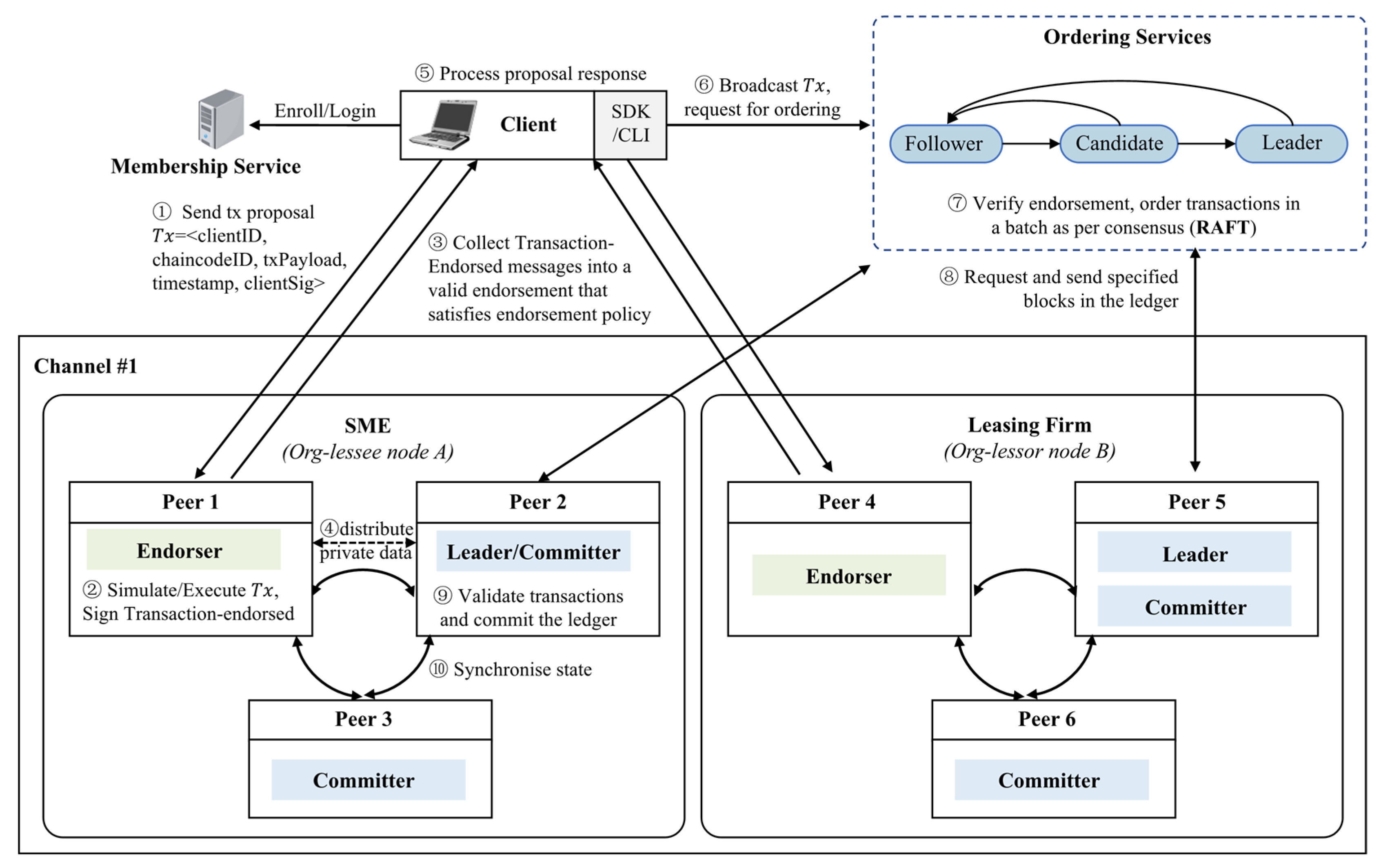

3.2. Raft Consensus Based on Credit

4. Problem Description

4.1. Description of Problem

4.2. Basic Lease Scenarios

4.3. Model Parameters

- (1)

- Return rate (): Return rate refers to the yield that can be earned when completing the investment activity on the lease.

- (2)

- Reinvestment rate (): Reinvestment rate refers to the yield that the lessee expects to earn when it does not pay or defers the full rental price, which can be put into other investments for extra gains.

- (3)

- Maintenance fee (): Maintenance fee refers to the cost of carrying out maintenance actions to ensure that the leased asset is in a proper operating condition. In this study, the LC states that the maintenance service must be provided by MCs and completed until the lease termination—the maintenance fee is not embedded in the rental payment.

- (4)

- Loss rate (): Loss rate refers to the loss that could result from the lessee’s defaulting behavior—for instance, if the lessee defaults by not returning the leased asset at the end of the lease, which cannot be re-leased to the next lessee upon termination of the previous LC.

5. Model Formulation

5.1. Basic Assumptions

5.2. Payoff Matrix

- (1)

- Strategy I: Comply, Access

- (2)

- Strategy II: Default, Access

- (3)

- Strategy III: Comply, Not-access

- (4)

- Strategy IV: Default, Not-access

6. Model Stability Analysis

6.1. Replicator Dynamic System

6.1.1. Replication Dynamic Equation of the SME

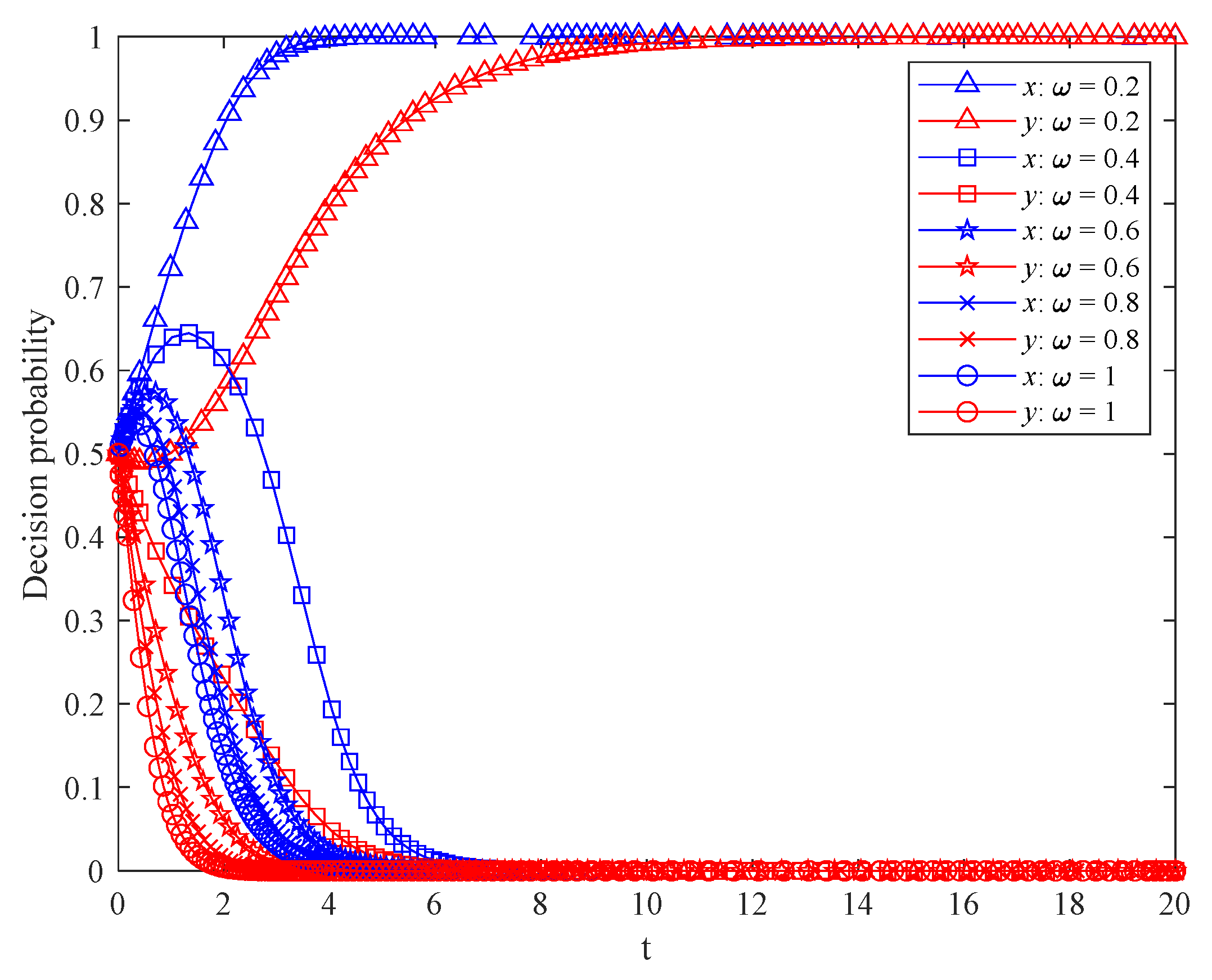

- In the case of , . is an evolutionary stable strategy (ESS). When the probability of the LF accessing the CBLP is larger than , the SME will converge with the equilibrium strategy of “comply with the LC”. The number of SMEs who abide by the contract will gradually increase.

- In the case of , is an evolutionary stable strategy (ESS). It implies that more SMEs will eventually evolve into a stable state of defaulting on the LC, since LFs struggle to distinguish the forgery of credit records without BCT [69].

6.1.2. Replication Dynamic Equation of the LF

- In the case of , . is an evolutionary stable strategy (ESS). When the probability of SME compliance is larger than , the LF converges to the equilibrium strategy of “not accessing the CBLP ”, and thereby the SME does not need to join the consortium blockchain to share information.

- In the case of , . is an evolutionary stable strategy (ESS). When the probability of SME compliance is less than, the LF will converge with the equilibrium strategy of “access the CBLP ” to participate in information sharing on-chain to complete the lease.

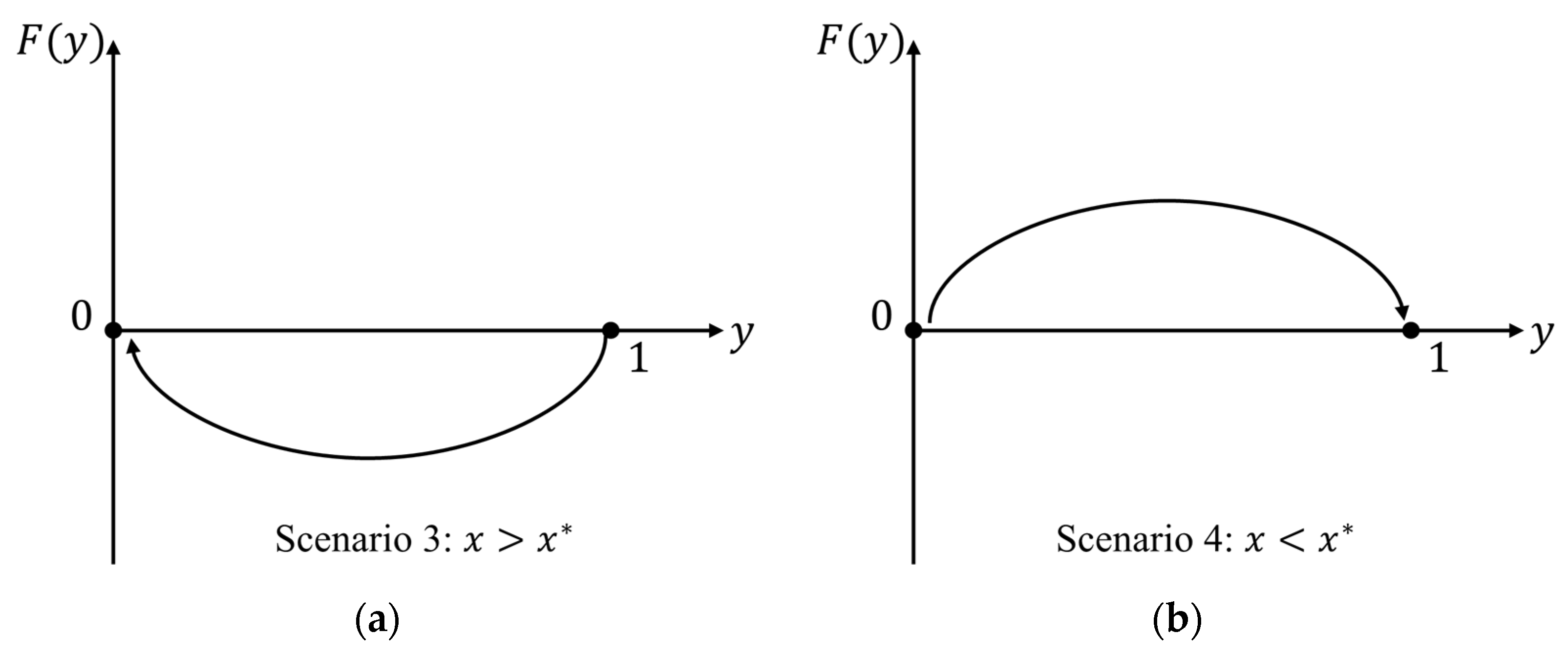

6.2. Analysis of Equilibrium Stability and ESS

6.3. Sensitivity Analysis in the Evolutionary Game

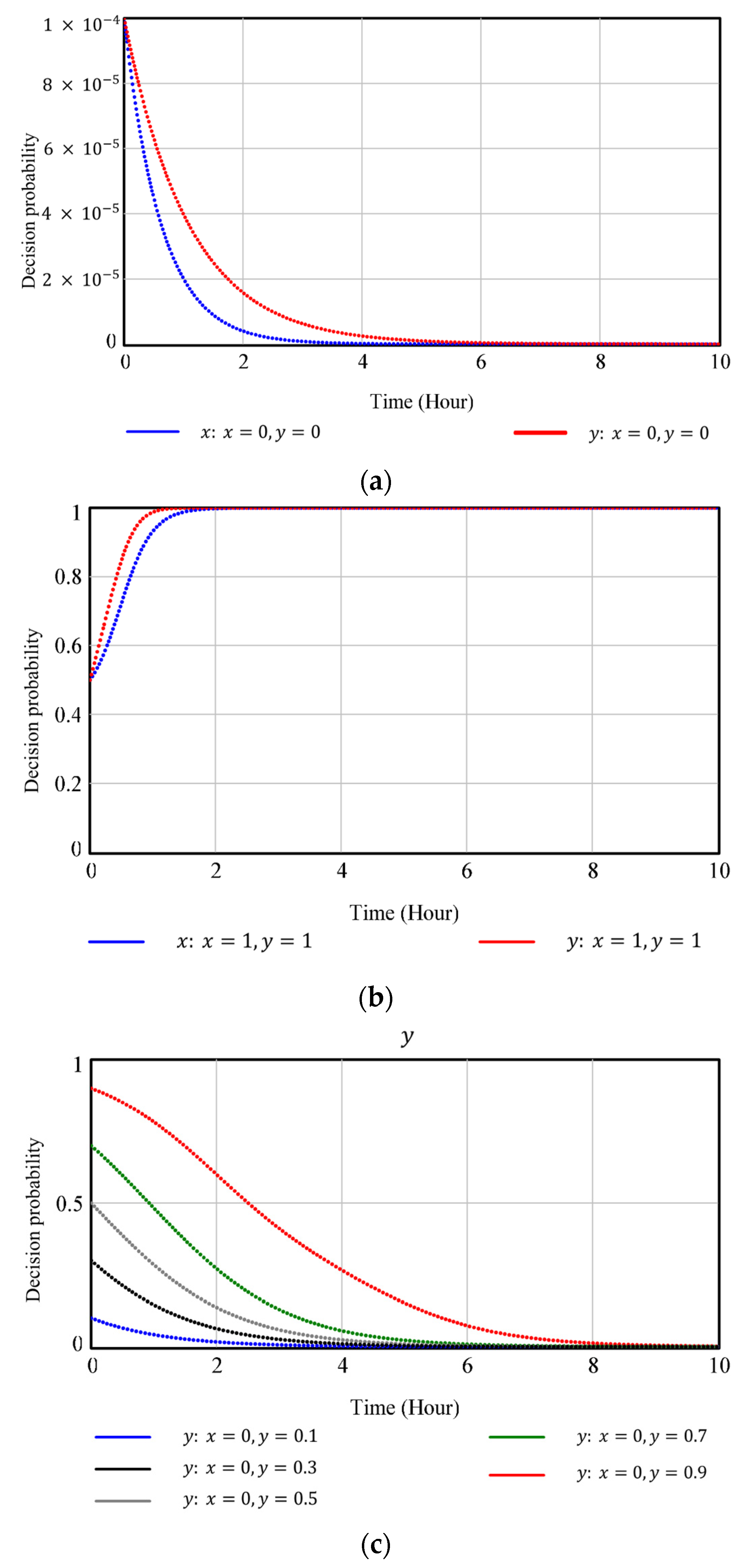

6.3.1. Impact of Information Sharing on

6.3.2. Impact of Credit on

6.3.3. Impact of Incentive–Penalty on

6.3.4. Impact of Risk on

7. Numerical Experiments and Implications

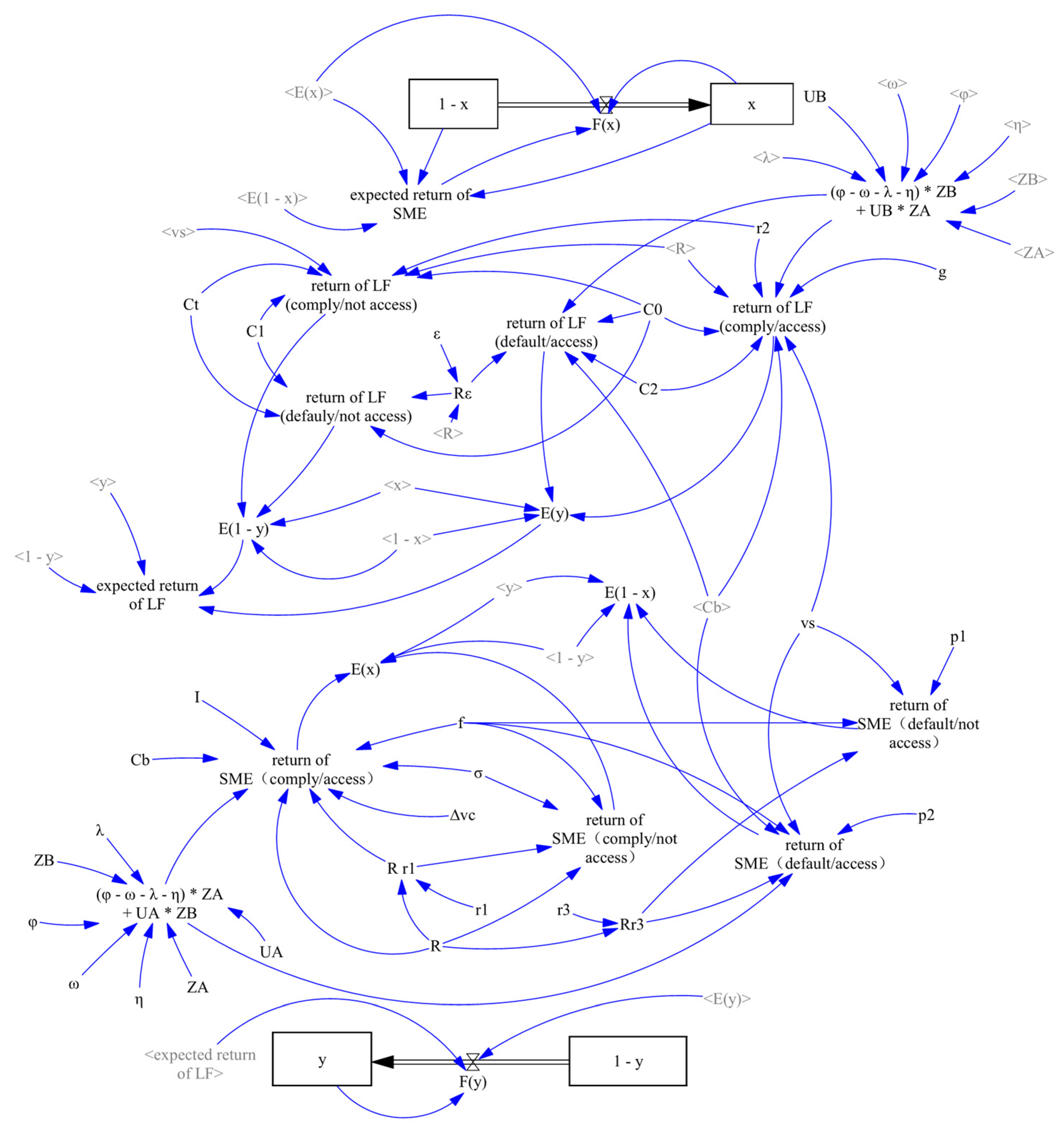

7.1. System Dynamics Model Experiment

7.2. Effect of Parameter Changes on Evolutionary Stable Strategies

7.2.1. Evolution Impacted by Information Sharing

7.2.2. Evolution Impacted by Credit

7.2.3. Evolution Impacted by Incentive-Penalty

7.2.4. Evolution Impacted by Risk

7.3. Implications of the Results

- (1)

- The results reveal that the residual value of the leased asset is a decisive factor supporting the lessor’s access strategy. Before signing the LC, it is necessary to estimate the asset residual value; if the value is relatively large at the termination of the lease, LFs (lessors) have a high probability of actively adopting BCT to efficiently prove their ownership of the leased asset on-chain. Thus, from the perspective of reducing risks of leased asset default, a blockchain-based leasing service provided by the lessor is more beneficial for an operating lease than a capital lease.

- (2)

- Most leasing businesses tend to treat maintenance as a non-core activity and commonly outsource it to a third-party MC [10], as assumed in this study (Section 4). The results indicate that when the maintenance fee is not embedded in the rental payment, the maintenance charge is not a determinant impacting the lessee’s decisions regarding compliance with/defaulting on the LC. Hence, before the lessor decides whether to adopt BCT, it is necessary to take into consideration the in-house or outsourced maintenance problem.

- (3)

- To encourage lessees and lessors to evolve to the ideal equilibrium state, an incentive mechanism should be designed to motivate all parties to cooperatively construct a sustainable and more trustworthy leasing environment. More high-quality information should be shared on-chain, and stakeholders should also improve the capability to effectively utilize the data on- and off-chain [74]. In contrast to the fixed rewards resulting from block mining, the incentive associated with incremental or deductible credit value for consensus action tends to inspire lessees’ willingness to comply with the contract under the BCT-based leasing business. An appropriate default penalty should be set up on-chain that can deter the lessee from defaulting and encourage it to make rental payments on time and return the leased asset as agreed in the LC. When making strategic decisions to join the consortium to share information, participants (particularly lessees) are more sensitive to the technology risk factor to which they are subject. To reduce the cost of building and maintaining the blockchain system to support the leasing business (e.g., on-chain and off-chain storage costs, verification costs, etc.), it is advised and helpful to embed blockchain-as-a-service (BaaS) in our CBLP in the future [75], which will also enhance SMEs’ willingness to share more valuable information on-chain, achieving a win–win outcome in the leasing business.

8. Conclusions and Future Works

8.1. Conclusions

- (1)

- With long-term cooperation, the two parties (lessee and lessor) eventually evolve to adopt strategies in which the lessee is more inclined to conform to the LC and the lessor becomes more proactive in accessing the CBLP as a consortium node to share information on-chain.

- (2)

- According to previous basic lease scenarios that we assumed, two default actions are explored: (i) overdue rental payment; (ii) asset disposal against the LC. For the former default action, we found that the larger proceeds gained resulting from reinvesting the rental payment will cause the lessee to default, and at this time, the lessor will tend to adopt BCT to mitigate the overdue-payment default risk. In addition, the residual value of the leased asset has a positive impact on the exposure at default, and the lessee will be more likely to default by not returning the leased asset to the lessor due to the temptation of the high profit achieved from asset disposal at the end of the lease. Meanwhile, the lessee’s default on asset disposals will result in the lessor being more inclined to adopt BCT to ensure a timely claim of repossession of the leased asset.

- (3)

- Although blockchain can guarantee data reliability (e.g., maintenance events) [76], maintenance cost is not a determinant of the equilibrium state once the maintenance service is outsourced. On the contrary, in-house maintenance provided by the lessor may affect the two parties’ strategic decisions.

- (4)

- When the lessee and lessor have incentives to participate in sharing or utilizing more information on-chain, the lessee will eventually evolve to conform to the LC, which will benefit the lessor and leasing industry. Setting up a changeable credit associated with the lessee’s LC performance to compete for a block accounting right via a consensus mechanism [77] is an effective way to incentivize the lessee to comply with the LC, while this method does not work much to incentive the lessor to adopt BCT. In addition, only when the default penalty on-chain exceeds a critical value can it work to incentivize lessees to correctly fulfill their obligations in the LC [78], once the penalty is lower than a critical value, which will in return increase the default risk. The technology risks and relevant costs concerning CBLP deployment play a vital role in encouraging the consortium to participate in information sharing on-chain, which is consistent with what we expected in reality.

8.2. Limitations and Future Directions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| OEM | Original Equipment Manufacturer |

| SMEs | Small and Medium-Sized Enterprises |

| LFs | Leasing Firms |

| MCs | Maintenance Centers |

| LC | Lease Contract |

| CPL | Capital Lease |

| OPL | Operating Lease |

| EGT | Evolutionary Game Theory |

| ESS | Evolutionary Stable Strategy |

| BCT | Blockchain Technology |

| RDE | Replication Dynamics Equation |

| CBLP | Consortium Blockchain-Based Leasing Platform |

| HLF | Hyperledger Fabric |

| BaaS | Blockchain as a Service |

| CSP | Cloud Storage Provider |

| IPFS | InterPlanetary File System |

References

- Mol-Gómez-Vázquez, A.; Hernández-Cánovas, G.; Köeter-Kant, J. Economic and Institutional Determinants of Lease Financing for European SMEs: An Analysis across Developing and Developed Countries. J. Small Bus. Manag. 2020, 1–22. [Google Scholar] [CrossRef]

- Li, J.; Wang, H.; Deng, Z.; Zhang, W.; Zhang, G. Leasing or Selling? The Channel Choice of Durable Goods Manufacturer Considering Consumers’ Capital Constraint. Flex. Serv. Manuf. J. 2022, 34, 317–350. [Google Scholar] [CrossRef]

- Eisfeldt, A.L.; Rampini, A.A. Leasing, Ability to Repossess, and Debt Capacity. Rev. Financ. Stud. 2009, 22, 1621–1657. [Google Scholar] [CrossRef] [Green Version]

- Van Loon, P.; Delagarde, C.; Van Wassenhove, L.N.; Mihelič, A. Leasing or Buying White Goods: Comparing Manufacturer Profitability versus Cost to Consumer. Int. J. Prod. Res. 2020, 58, 1092–1106. [Google Scholar] [CrossRef]

- Smith, C.W.; Wakeman, L.M. Determinants of Corporate Leasing Policy. J. Financ. 1985, 40, 895–908. [Google Scholar] [CrossRef]

- Zheng, B.-K.; Zhu, L.-H.; Shen, M.; Gao, F.; Zhang, C.; Li, Y.-D.; Yang, J. Scalable and Privacy-Preserving Data Sharing Based on Blockchain. J. Comput. Sci. Technol. 2018, 33, 557–567. [Google Scholar] [CrossRef]

- Dedeoglu, V.; Jurdak, R.; Dorri, A.; Lunardi, R.C.; Michelin, R.A.; Zorzo, A.F.; Kanhere, S.S. Blockchain Technologies for IoT; Springer: Berlin/Heidelberg, Germany, 2020; pp. 55–89. ISBN 9789811387753. [Google Scholar]

- Saberi, S.; Kouhizadeh, M.; Sarkis, J.; Shen, L. Blockchain Technology and Its Relationships to Sustainable Supply Chain Management. Int. J. Prod. Res. 2019, 57, 2117–2135. [Google Scholar] [CrossRef] [Green Version]

- Wang, W.; Feng, L.; Li, Y.; Xu, F.; Deng, Q. Role of Financial Leasing in a Capital-Constrained Service Supply Chain. Transp. Res. Part E Logist. Transp. Rev. 2020, 143, 102097. [Google Scholar] [CrossRef]

- Lease Accounting Framework and the Development of International Accounting Standards|SpringerLink. Available online: https://link.springer.com/chapter/10.1007/978-3-030-71633-2_2 (accessed on 29 November 2022).

- Murthy, D.N.P.; Jack, N. Extended Warranties, Maintenance Service and Lease Contracts; Springer Series in Reliability Engineering; Springer: London, UK, 2014; ISBN 978-1-4471-6439-5. [Google Scholar]

- Kaposty, F.; Klein, P.; Löderbusch, M.; Pfingsten, A. Loss given default in SME leasing. Rev. Manag. Sci. 2022, 16, 1561–1597. [Google Scholar] [CrossRef]

- Kuhle, P. Building A Blockchain-Based Decentralized Digital Asset Management System for Commercial Aircraft Leasing. Comput. Ind. 2021, 21, 103393. [Google Scholar] [CrossRef]

- Altman, E.I.; Brady, B.; Resti, A.; Sironi, A. The Link between Default and Recovery Rates: Theory, Empirical Evidence, and Implications. J. Bus. 2005, 78, 2203–2228. [Google Scholar] [CrossRef]

- Kysucky, V.; Norden, L. The Benefits of Relationship Lending in a Cross-Country Context: A Meta-Analysis. Manag. Sci. 2016, 62, 90–110. [Google Scholar] [CrossRef] [Green Version]

- Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System. Decentralized Bus. Rev. 2008, 21260. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 27 January 2023).

- Politou, E.; Casino, F.; Alepis, E.; Patsakis, C. Blockchain Mutability: Challenges and Proposed Solutions. IEEE Trans. Emerg. Top. Comput. 2021, 9, 1972–1986. [Google Scholar] [CrossRef] [Green Version]

- Viriyasitavat, W.; Hoonsopon, D. Blockchain Characteristics and Consensus in Modern Business Processes. J. Ind. Inf. Integr. 2019, 13, 32–39. [Google Scholar] [CrossRef]

- Yu, Y.; Huang, G.; Guo, X. Financing Strategy Analysis for a Multi-Sided Platform with Blockchain Technology. Int. J. Prod. Res. 2021, 59, 4513–4532. [Google Scholar] [CrossRef]

- Belotti, M.; Božić, N.; Pujolle, G.; Secci, S. A Vademecum on Blockchain Technologies: When, Which, and How. IEEE Commun. Surv. Tutor. 2019, 21, 3796–3838. [Google Scholar] [CrossRef] [Green Version]

- Singh, S.K.; Jenamani, M.; Dasgupta, D.; Das, S. A Conceptual Model for Indian Public Distribution System Using Consortium Blockchain with On-Chain and off-Chain Trusted Data. Inf. Technol. Dev. 2021, 27, 499–523. [Google Scholar] [CrossRef]

- Dutta, P.; Choi, T.-M.; Somani, S.; Butala, R. Blockchain Technology in Supply Chain Operations: Applications, Challenges and Research Opportunities. Transp. Res. Part E Logist. Transp. Rev. 2020, 142, 102067. [Google Scholar] [CrossRef]

- Andoni, M.; Robu, V.; Flynn, D.; Abram, S.; Geach, D.; Jenkins, D.; McCallum, P.; Peacock, A. Blockchain Technology in the Energy Sector: A Systematic Review of Challenges and Opportunities. Renew. Sustain. Energy Rev. 2019, 100, 143–174. [Google Scholar] [CrossRef]

- Tandon, A.; Dhir, A.; Islam, A.K.M.N.; Mäntymäki, M. Blockchain in Healthcare: A Systematic Literature Review, Synthesizing Framework and Future Research Agenda. Comput. Ind. 2020, 122, 103290. [Google Scholar] [CrossRef]

- Leng, J.; Ruan, G.; Jiang, P.; Xu, K.; Liu, Q.; Zhou, X.; Liu, C. Blockchain-Empowered Sustainable Manufacturing and Product Lifecycle Management in Industry 4.0: A Survey. Renew. Sustain. Energy Rev. 2020, 132, 110112. [Google Scholar] [CrossRef]

- Xie, J.; Tang, H.; Huang, T.; Yu, F.R.; Xie, R.; Liu, J.; Liu, Y. A Survey of Blockchain Technology Applied to Smart Cities: Research Issues and Challenges. IEEE Commun. Surv. Tutor. 2019, 21, 2794–2830. [Google Scholar] [CrossRef]

- Loukil, F.; Abed, M.; Boukadi, K. Blockchain Adoption in Education: A Systematic Literature Review. Educ. Inf. Technol. 2021, 26, 5779–5797. [Google Scholar] [CrossRef]

- Wang, J.; Wu, P.; Wang, X.; Shou, W. The Outlook of Blockchain Technology for Construction Engineering Management. Front. Eng. Manag. 2017, 67–75. [Google Scholar] [CrossRef] [Green Version]

- Auer, S.; Nagler, S.; Mazumdar, S.; Mukkamala, R.R. Towards Blockchain-IoT Based Shared Mobility: Car-Sharing and Leasing as a Case Study. J. Netw. Comput. Appl. 2022, 200, 103316. [Google Scholar] [CrossRef]

- Faber, B.; Michelet, G.C.; Weidmann, N.; Mukkamala, R.R.; Vatrapu, R. BPDIMS: A Blockchain-Based Personal Data and Identity Management System. In Proceedings of the 52nd Hawaii International Conference on System Sciences, Maui, HI, USA, 8–11 January 2019; pp. 6855–6864. [Google Scholar]

- Obour Agyekum, K.O.-B.; Xia, Q.; Boateng Sifah, E.; Amofa, S.; Nketia Acheampong, K.; Gao, J.; Chen, R.; Xia, H.; Gee, J.C.; Du, X.; et al. V-Chain: A Blockchain-Based Car Lease Platform. In Proceedings of the 2018 IEEE International Conference on Internet of Things (iThings) and IEEE Green Computing and Communications (GreenCom) and IEEE Cyber, Physical and Social Computing (CPSCom) and IEEE Smart Data (SmartData), HICSS, Halifax, NS, Canada, 30 July–3 August 2018; pp. 1317–1325. [Google Scholar]

- Zheng, K.; Zheng, L.J.; Gauthier, J.; Zhou, L.; Xu, Y.; Behl, A.; Zhang, J.Z. Blockchain Technology for Enterprise Credit Information Sharing in Supply Chain Finance. J. Innov. Knowl. 2022, 7, 100256. [Google Scholar] [CrossRef]

- Fiorentino, S.; Bartolucci, S. Blockchain-Based Smart Contracts as New Governance Tools for the Sharing Economy. Cities 2021, 117, 103325. [Google Scholar] [CrossRef]

- Delle Foglie, A.; Panetta, I.C.; Boukrami, E.; Vento, G. The Impact of the Blockchain Technology on the Global Sukuk Industry: Smart Contracts and Asset Tokenisation. Technol. Anal. Strateg. Manag. 2021, 1–15. [Google Scholar] [CrossRef]

- Wang, J.; Zhou, Z.; Botterud, A. An Evolutionary Game Approach to Analyzing Bidding Strategies in Electricity Markets with Elastic Demand. Energy 2011, 36, 3459–3467. [Google Scholar] [CrossRef]

- Wang, J.; Peng, X.; Du, Y.; Wang, F. A Tripartite Evolutionary Game Research on Information Sharing of the Subjects of Agricultural Product Supply Chain with a Farmer Cooperative as the Core Enterprise. Manag. Decis. Econ. 2022, 43, 159–177. [Google Scholar] [CrossRef]

- Apaloo, J.; Brown, J.S.; Vincent, T.L. Evolutionary Game Theory: ESS, Convergence Stability, and NIS. Evol. Ecol. Res. 2009, 11, 489–515. [Google Scholar]

- Chen, Y.; Zeng, Q.; Zheng, X.; Shao, B.; Jin, L. Safety Supervision of Tower Crane Operation on Construction Sites: An Evolutionary Game Analysis. Saf. Sci. 2022, 152, 105578. [Google Scholar] [CrossRef]

- Su, L.; Cao, Y.; Li, H.; Tan, J. Blockchain-Driven Optimal Strategies for Supply Chain Finance Based on a Tripartite Game Model. J. Theor. Appl. Electron. Commer. Res. 2022, 17, 67. [Google Scholar] [CrossRef]

- Tang, Q.; Zhang, Z.; Yuan, Z.; Li, Z. The Game Analysis of Information Sharing for Supply Chain Enterprises in the Blockchain. Supply Chain 2022, 2, 13. [Google Scholar] [CrossRef]

- Sun, R.; He, D.; Su, H. Evolutionary Game Analysis of Blockchain Technology Preventing Supply Chain Financial Risks. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 155. [Google Scholar] [CrossRef]

- Song, L.; Luo, Y.; Chang, Z.; Jin, C.; Nicolas, M. Blockchain Adoption in Agricultural Supply Chain for Better Sustainability: A Game Theory Perspective. Sustainability 2022, 14, 1470. [Google Scholar] [CrossRef]

- Figueroa-Lorenzo, S.; Añorga, J.; Arrizabalaga, S. Methodological Performance Analysis Applied to a Novel IIoT Access Control System Based on Permissioned Blockchain. Inf. Process. Manag. 2021, 58, 102558. [Google Scholar] [CrossRef]

- Xu, X.; Sun, G.; Luo, L.; Cao, H.; Yu, H.; Vasilakos, A.V. Latency Performance Modeling and Analysis for Hyperledger Fabric Blockchain Network. Inf. Process. Manag. 2021, 58, 102436. [Google Scholar] [CrossRef]

- Androulaki, E.; Barger, A.; Bortnikov, V.; Cachin, C.; Christidis, K.; De Caro, A.; Enyeart, D.; Ferris, C.; Laventman, G.; Manevich, Y. Hyperledger Fabric: A Distributed Operating System for Permissioned Blockchains. arXiv 2018, arXiv:1801.10228. [Google Scholar]

- Rizzardi, A.; Sicari, S.; Miorandi, D.; Coen-Porisini, A. Securing the Access Control Policies to the Internet of Things Resources through Permissioned Blockchain. Concurr. Comput. Pract. Exp. 2022, 34, e6934. [Google Scholar] [CrossRef]

- Steinhoff, S.; Stathakopoulou, C.; Pavlovic, M.; Vukolić, M. BMS: Secure Decentralized Reconfiguration for Blockchain and BFT Systems. arXiv 2021, arXiv:210903913. [Google Scholar]

- Liu, Y.; Lu, Q.; Paik, H.-Y.; Xu, X.; Chen, S.; Zhu, L. Design Pattern as a Service for Blockchain-Based Self-Sovereign Identity. IEEE Softw. 2020, 37, 30–36. [Google Scholar] [CrossRef]

- Viriyasitavat, W.; Xu, L.D.; Sapsomboon, A.; Dhiman, G.; Hoonsopon, D. Building Trust of Blockchain-Based Internet-of-Thing Services Using Public Key Infrastructure. Enterp. Inf. Syst. 2022, 16, 2037162. [Google Scholar] [CrossRef]

- Kuhn, M.; Funk, F.; Zhang, G.; Franke, J. Blockchain-Based Application for the Traceability of Complex Assembly Structures. J. Manuf. Syst. 2021, 59, 617–630. [Google Scholar] [CrossRef]

- Herrera-Joancomartí, J.; Pérez-Solà, C. Privacy in Bitcoin Transactions: New Challenges from Blockchain Scalability Solutions. In Proceedings of the Modeling Decisions for Artificial Intelligence; Springer International Publishing: Cham, Switzerland, 2016; pp. 26–44. [Google Scholar]

- Miyachi, K.; Mackey, T.K. HOCBS: A Privacy-Preserving Blockchain Framework for Healthcare Data Leveraging an on-Chain and off-Chain System Design. Inf. Process. Manag. 2021, 58, 102535. [Google Scholar] [CrossRef]

- Solaiman, E.; Wike, T.; Sfyrakis, I. Implementation and Evaluation of Smart Contracts Using a Hybrid On-and Off-blockchain Architecture. Concurr. Comput. Pract. Exp. 2021, 33, e5811. [Google Scholar] [CrossRef]

- Wu, H.; Peng, Z.; Guo, S.; Yang, Y.; Xiao, B. VQL: Efficient and Verifiable Cloud Query Services for Blockchain Systems. IEEE Trans. Parallel Distrib. Syst. 2021, 33, 1393–1406. [Google Scholar] [CrossRef]

- Udokwu, C.; Norta, A. Deriving and Formalizing Requirements of Decentralized Applications for Inter-Organizational Collaborations on Blockchain. Arab. J. Sci. Eng. 2021, 46, 8397–8414. [Google Scholar] [CrossRef]

- Surjandari, I.; Yusuf, H.; Laoh, E.; Maulida, R. Designing a Permissioned Blockchain Network for the Halal Industry Using Hyperledger Fabric with Multiple Channels and the Raft Consensus Mechanism. J. Big Data. 2021, 8, 10. [Google Scholar] [CrossRef]

- Fu, W.; Wei, X.; Tong, S. An Improved Blockchain Consensus Algorithm Based on Raft. Arab. J. Sci. Eng. 2021, 46, 8137–8149. [Google Scholar] [CrossRef]

- Zhang, Y.; Zhang, L.; Liu, Y.; Luo, X. Proof of Service Power: A Blockchain Consensus for Cloud Manufacturing. J. Manuf. Syst. 2021, 59, 1–11. [Google Scholar] [CrossRef]

- Nechaev, A.S.; Zakharov, S.V.; Barykina, Y.N.; Vel’m, M.V.; Kuznetsova, O.N. Forming Methodologies to Improving the Efficiency of Innovative Companies Based on Leasing Tools. J. Sustain. Financ. Invest. 2022, 12, 536–553. [Google Scholar] [CrossRef]

- Li, Z.; Zhong, R.Y.; Tian, Z.-G.; Dai, H.-N.; Barenji, A.V.; Huang, G.Q. Industrial Blockchain: A State-of-the-Art Survey. Robot. Comput.-Integr. Manuf. 2021, 70, 102124. [Google Scholar] [CrossRef]

- Li, B.; Li, H.; Sun, Q.; Chen, X. Evolutionary Game Analysis between Businesses and Consumers under the Background of Internet Rumors. Concurr. Comput. Pract. Exp. 2022, 34, e5897. [Google Scholar] [CrossRef]

- Weibull, J.W. Evolutionary Game Theory; MIT Press: Cambridge, MA, USA, 1997; ISBN 0-262-73121-5. [Google Scholar]

- Xu, B.; Li, Q. Research on Supervision Mechanism of Big Data Discriminatory Pricing on the Asymmetric Service Platform—Based on SD Evolutionary Game Model. J. Theor. Appl. Electron. Commer. Res. 2022, 17, 63. [Google Scholar] [CrossRef]

- Kang, H.; Dai, T.; Jean-Louis, N.; Tao, S.; Gu, X. Fabzk: Supporting Privacy-Preserving, Auditable Smart Contracts in Hyperledger Fabric; IEEE: Piscataway, NJ, USA, 2019; pp. 543–555. [Google Scholar]

- Bhushan, B.; Sinha, P.; Sagayam, K.M.; Andrew, J. Untangling Blockchain Technology: A Survey on State of the Art, Security Threats, Privacy Services, Applications and Future Research Directions. Comput. Electr. Eng. 2021, 90, 106897. [Google Scholar] [CrossRef]

- Liu, J.; Zhang, H.; Zhen, L. Blockchain Technology in Maritime Supply Chains: Applications, Architecture and Challenges. Int. J. Prod. Res. 2021, 1–17. [Google Scholar] [CrossRef]

- Chang, V.; Baudier, P.; Zhang, H.; Xu, Q.; Zhang, J.; Arami, M. How Blockchain Can Impact Financial Services—The Overview, Challenges and Recommendations from Expert Interviewees. Technol. Forecast. Soc. Chang. 2020, 158, 120166. [Google Scholar] [CrossRef]

- Li, Q.; Wang, Y.; Li, K.; Chen, L.; Wei, Z. Evolutionary Dynamics of the Last Mile Travel Choice. Phys. Stat. Mech. Appl. 2019, 536, 122555. [Google Scholar] [CrossRef]

- Qiao, Y.; Lan, Q.; Zhou, Z.; Ma, C. Privacy-Preserving Credit Evaluation System Based on Blockchain. Expert Syst. Appl. 2022, 188, 115989. [Google Scholar] [CrossRef]

- Friedman, D. On Economic Applications of Evolutionary Game Theory. J. Evol. Econ. 1998, 8, 15–43. [Google Scholar] [CrossRef] [Green Version]

- Nowak, M.A.; Sigmund, K. Evolutionary Dynamics of Biological Games. Science 2004, 303, 793–799. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Ritzberger, K.; Weibull, J.W. Evolutionary Selection in Normal-Form Games. Econom. J. Econom. Soc. 1995, 63, 1371–1399. [Google Scholar] [CrossRef]

- Kang, K.; Zhao, Y.; Zhang, J.; Qiang, C. Evolutionary Game Theoretic Analysis on Low-Carbon Strategy for Supply Chain Enterprises. J. Clean. Prod. 2019, 230, 981–994. [Google Scholar] [CrossRef]

- Yadav, S.; Singh, S.P. Blockchain Critical Success Factors for Sustainable Supply Chain. Resour. Conserv. Recycl. 2020, 152, 104505. [Google Scholar] [CrossRef]

- Jie, S.; Zhang, P.; Alkubati, M.; Yubin, B.; Ge, Y. Research Advances on Blockchain-as-a-Service: Architectures, Applications and Challenges. Digit. Commun. Netw. 2021, 8, 466–475. [Google Scholar]

- Mohril, R.S.; Solanki, B.S.; Lad, B.K.; Kulkarni, M.S. Blockchain Enabled Maintenance Management Framework for Military Equipment. IEEE Trans. Eng. Manag. 2021, 69, 3938–3951. [Google Scholar] [CrossRef]

- Zhu, S.; Cai, Z.; Hu, H.; Li, Y.; Li, W. ZkCrowd: A Hybrid Blockchain-Based Crowdsourcing Platform. IEEE Trans. Ind. Inform. 2019, 16, 4196–4205. [Google Scholar] [CrossRef]

- Holden, R.; Malani, A. Can Blockchain Solve the Hold-up Problem in Contracts? Cambridge University Press: Cambridge, UK, 2021; ISBN 1-00-900479-4. [Google Scholar]

- Natanelov, V.; Cao, S.; Foth, M.; Dulleck, U. Blockchain Smart Contracts for Supply Chain Finance: Mapping the Innovation Potential in Australia-China Beef Supply Chains. J. Ind. Inf. Integr. 2022, 30, 100389. [Google Scholar] [CrossRef]

- Oh, J.; Choi, Y.; In, J. A Conceptual Framework for Designing Blockchain Technology Enabled Supply Chains. Int. J. Logist. Res. Appl. 2022, 1–19. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mode | Party | Notation | Definition |

|---|---|---|---|

| Under the conventional lease mode | SME (Org-lessee node A) | Total rental payments to the LF under the terms of the lease | |

| Return rate of the SME on the lease | |||

| Reinvestment rate of the SME after the contract’s default | |||

| Maintenance fee for the leased asset during the lease period | |||

| Default penalty of the SME under the conventional lease | |||

| Incentives of the SME given by the LFs due to LC compliance | |||

| LF (Org-lessor node B) | Return rate of the LF on the lease | ||

| Marginal credit investigation costs of the LF | |||

| Original acquisition cost of the leased asset | |||

| Monitoring cost of asset’s operation under the conventional lease | |||

| Residual value of the leased asset at the end of the lease | |||

| Loss rate of the LF caused by the contract default | |||

| Under the blockchain-based lease mode | SME (Org-lessee node A) | Membership cost of the SME joining the consortium blockchain | |

| Increased credit value of the SME due to LC compliance on-chain | |||

| I | Fixed reward when mining a block on-chain | ||

| Default penalties of the SME on-chain | |||

| Quantity of information shared by the SME on-chain | |||

| Relative computing power provided by the SME on-chain | |||

| LF (Org-lessor node B) | Synergy gain on the lease business empowered by the blockchain | ||

| Monitoring cost of asset’s operation under the blockchain-based lease | |||

| Quantity of information shared by the LF on-chain | |||

| Relative computing power provided by the LF on-chain | |||

| SME and LF | Coefficient of information transmission efficiency on-chain | ||

| Validation cost coefficient of confirming transaction on-chain | |||

| Storage cost coefficient of information stored off-chain CSP/IPFS | |||

| Security risk coefficient of sharing information on-chain |

| Strategy | LF (Org-Lessor Node B) | ||

|---|---|---|---|

| Access | Not-Access | ||

| SME (Org-lessee node A) | Comply | ||

| Default | |||

| Equilibrium Point | ||

|---|---|---|

| 0 | 1 |

| Judgment | |||

|---|---|---|---|

| <0 | >0 | ESS | |

| >0 | >0 | Unstable point | |

| >0 | >0 | Unstable point | |

| <0 | >0 | ESS | |

| 0 | +/- | Saddle point |

| 8 | 0.2 | 0.25 | 0.3 | 0.05 | 0.8 | 3 | 6 | 4 | 0.08 | 0.6 | 0.4 | 1 |

| / | ||||||||||||

| 1.2 | 5 | 3 | 0.5 | 0.5 | 0.15 | 5 | 1.5 | 0.6 | 0.2 | 0.2 | 0.2 | / |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cheng, H.; Li, J.; Lu, J.; Lo, S.-L.; Xiang, Z. Incentive-Driven Information Sharing in Leasing Based on a Consortium Blockchain and Evolutionary Game. J. Theor. Appl. Electron. Commer. Res. 2023, 18, 206-236. https://doi.org/10.3390/jtaer18010012

Cheng H, Li J, Lu J, Lo S-L, Xiang Z. Incentive-Driven Information Sharing in Leasing Based on a Consortium Blockchain and Evolutionary Game. Journal of Theoretical and Applied Electronic Commerce Research. 2023; 18(1):206-236. https://doi.org/10.3390/jtaer18010012

Chicago/Turabian StyleCheng, Hanlei, Jian Li, Jing Lu, Sio-Long Lo, and Zhiyu Xiang. 2023. "Incentive-Driven Information Sharing in Leasing Based on a Consortium Blockchain and Evolutionary Game" Journal of Theoretical and Applied Electronic Commerce Research 18, no. 1: 206-236. https://doi.org/10.3390/jtaer18010012

APA StyleCheng, H., Li, J., Lu, J., Lo, S.-L., & Xiang, Z. (2023). Incentive-Driven Information Sharing in Leasing Based on a Consortium Blockchain and Evolutionary Game. Journal of Theoretical and Applied Electronic Commerce Research, 18(1), 206-236. https://doi.org/10.3390/jtaer18010012