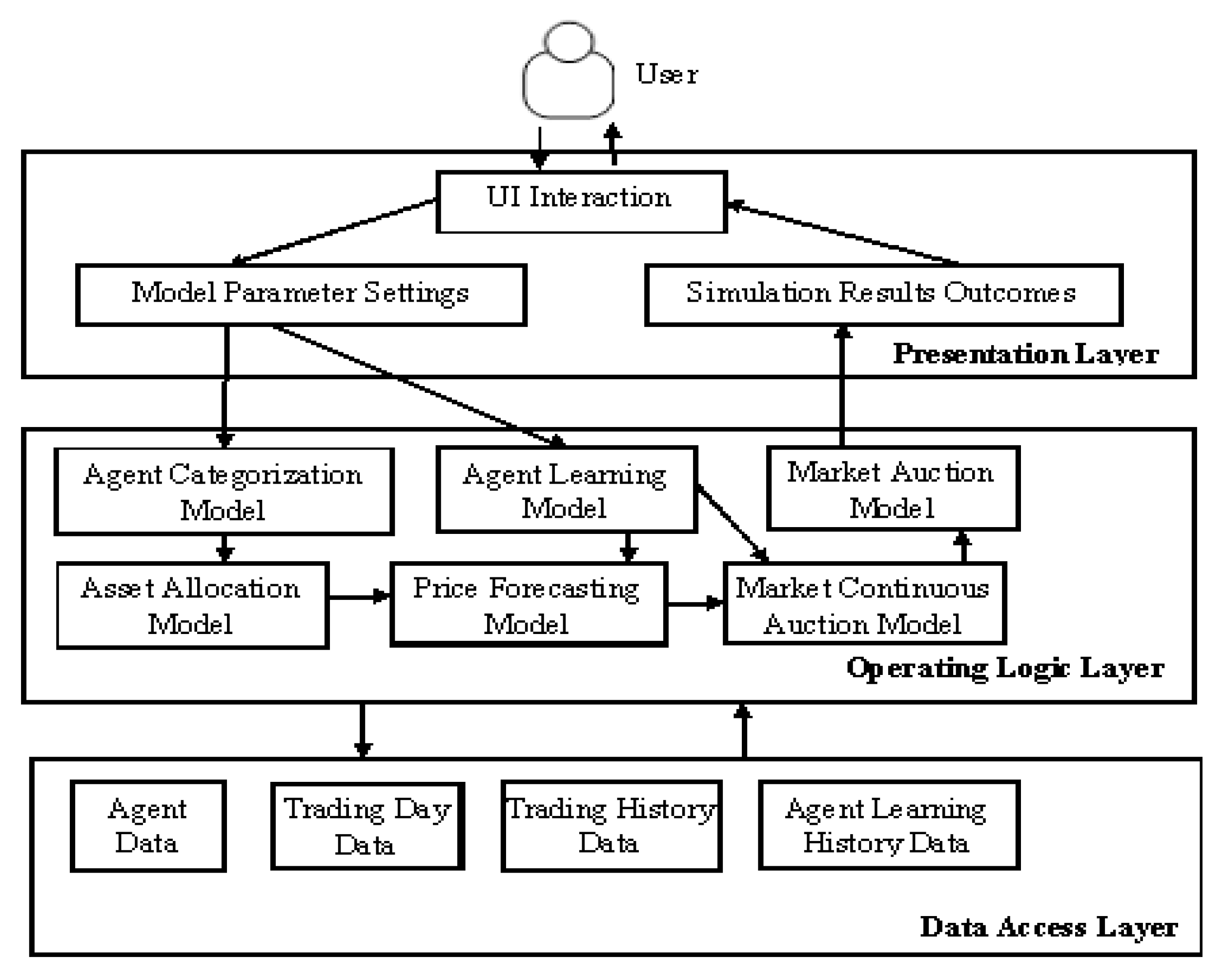

3.1.1. Agent Categorization

Agents adopt different trading strategies in the market. A summary of existing literature and market experiences indicates that the three widely accepted trading strategies employed in China’s stock market are value investing, trend investing, and stochastic investing. These strategies are the top-down approach. The bottom-up categorization method examines the basic attributes influencing agents’ behavioral decisions, such as gender (women/men), age (old/young), and wealth (rich/poor). Further observation of these basic attributes shows that they influence agents’ risk appetite, which consequently affects their investment behaviors. In identical situations, women are less tolerant to risk than men, rich people are less tolerant to risk than poor people, and older people are less tolerant to risk than younger people. Based on these basic attributes, agents can be categorized into eight types: specifically, poor young men, poor old men, rich young men, rich old men, poor young women, poor old women, rich young women, and rich old women. Moreover, an extra type is included in the present study, institution agents. Therefore, agents are categorized into nine types using the bottom-up approach. By combining the two approaches, the nine types of agents each adopt one of three investment strategies, creating 27 agent types.

Let A, B, C, D, E, F, G, H, and I represent poor young men, poor old men, rich young men, rich old men, poor young women, poor old women, rich young women, and rich old women, and institute agent, respectively. Let

k = 1, 2, and 3 represent value investment strategy, trend investment strategy, and stochastic investment strategy, respectively. The market comprises a total of 108 agents. The number of agents in each category is tabulated in

Table A1 of

Appendix B.

3.1.2. Basis of Agent Decision Formulation

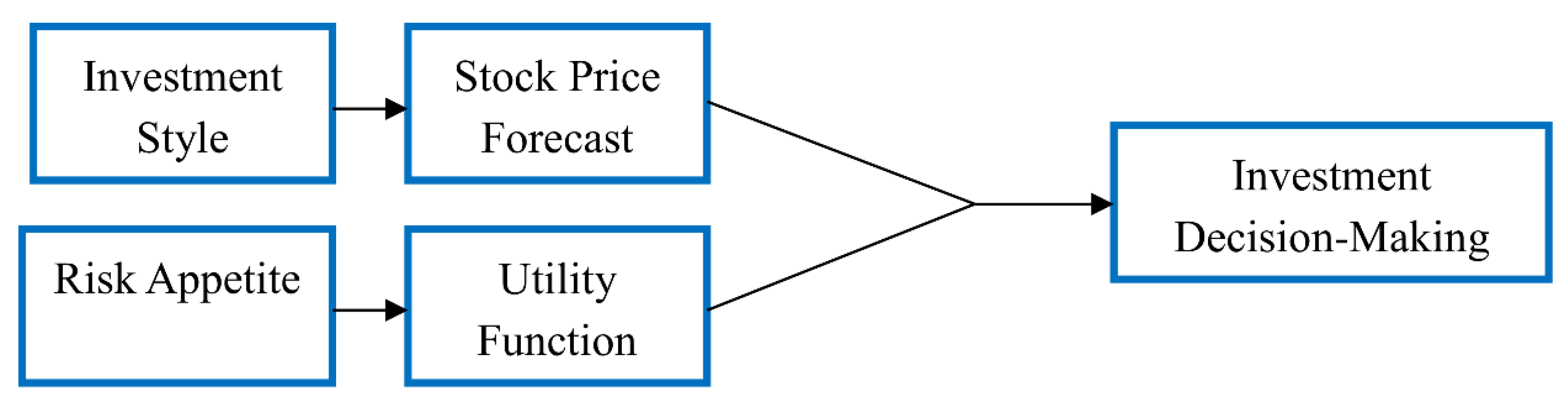

Agents are categorized based on their investment style and risk appetite. Agents’ investment style influences their forecasts of future stock prices. Agents’ risk appetite directly influences their utility function, and their utility function influences their allocation of risk assets. The two factors collectively influence agents’ investment decision behaviors. The influences that agents’ investment styles have on their price forecasting behaviors are first discussed shown as

Figure 1. Then, the influences that agents’ risk appetite has on their asset allocation behaviors are discussed. Finally, how agents combine their investment style and risk appetite to formulate investment decisions is discussed.

(1) Agents’ Investment Strategies

Three types of investment strategies exist in the market: value investment strategy, trend investment strategy, and stochastic investment strategy. The three strategies are evenly adopted by the agents in the market. That is, the three strategies are adopted in all nine agent types to forecast stock prices and formulate investment decisions. The valuation methods for the three strategies are as follows:

(i) Value Investment Strategy

Agents that adopt the value investment strategy believe that the market is efficient and that stock prices fluctuate concurrently with value. They maintain that stock prices constantly trend toward the real stock value. However, agents’ profit expectations vary. Therefore, a stochastic variable is used in the present study to reflect the forecasting differences of different agents, which can be expressed using the following equation:

where,

is the stock estimation of value-investing agent

i in the

t-th period,

is the stock price

j days ago (

j = 1, …, 30),

is the random number that conforms to uniform distribution, and

is the standard deviation of

(

j = 1, 2, …, 30). Let

be the expected rate of return of the value-investing agent in the

t-th period.

(ii) Trend Investment Strategy

Agents that adopt the trend investment strategy believe that certain trends exist in short-term stock prices. Their investment behaviors are based on historical trends. However, different agents value historical data differently. They believe that recent prices have a greater influence on current stock prices. Hence, they weigh the value of historical data according to time.

where,

is the stock estimation of trend investing agent

i in the

t-th period,

is the stock price

j days ago (

j = 1, …, 30),

is the random number that conforms to uniform distribution, and

is the standard deviation

(

j = 1, 2, …, 30). Let

be the expected rate of return of the trend-investing agent in the

t-th period.

(iii) Stochastic Investment Strategy

Agents that adopt the stochastic investment strategy are considered “novice” agents. They do not maintain a fixed determination system. Rather, they adopt the opening price in each period as their forecast price.

(2) Risk Appetite and Utility Function

Agents’ risk appetite determines their utility function. Consequently, their utility function facilitates them in formulating the optimal asset allocation plan. The proposed market comprises a single risk asset (stocks) and a single risk-free asset (case). Agents own both stocks and cash. Short purchasing and short selling are prohibited.

A novel utility function is modeled based on the research objectives and the utility function model presented in cumulative prospect theory [

39] (Bernard and Ghossoub, 2010) to determine the optimal risk asset allocation. In the model proposed by Bernard and Ghossoub, the independent variables for the utility function are the absolute loss values and absolute gain values. These independent variables are appropriate when considering a single agent type because only the monotonicity and marginal diminishment of the utility function must be characterized. By comparison, the utility functions of agents with different financial conditions must be characterized in the proposed model. The initial wealth difference between the agents generates different rates of return in identical gain conditions. Therefore, the absolute gain and absolute loss values adopted in the original model are inadequate for characterizing agents’ different utilities. In the present study, we adopted rate of return as the independent variable for agents’ utility functions. Using rate of return as the independent variable not only accounts for the increase in monotonicity and marginal diminishment of utility functions but also reflects agents’ different financial conditions.

Let be the initial financial condition of agent i in period t. The wealth of agent i comprises a specific amount of stocks (risk asset) and cash (risk-free asset), where represents risk asset, () represents cash, and represents the amount of simulated risk asset (optimal allocation) in the current period.

During the formulation of the optimal asset allocation plan (agent i), let the future rate of stock return be , where . Cash generates risk-free return (). is the expected excess return rate, where . Let , where .

Agents’ expected risk-return can be expressed as follows:

Hence, the expected risk rate of return is

The utility function (

U) can be expressed as follows:

The following criteria must be satisfied:

- (1)

, where

- (2)

- (3)

The total utility of the agent (

) can be expressed as follows:

Formula (7) is explained in

Appendix A. In this section of the calculation, we excluded the probability of distortion mentioned in prospect theory. To include the probability of distortion, please refer to Zhou et al. (2010) [

40]. Let the first-order derivative be 0:

(1) When

If , then = 0. Maximum agent utility is achieved with any risk asset investment ratio.

If , then > 0. The agent invests all assets into risk assets.

If , then < 0. The agent invests all assets into risk-free assets.

Using the aforementioned equations, we obtained the optimal risk allocation proportions in different conditions. We found that the optimal risk asset allocation relies on the , , and values, where is the risk aversion coefficient during gain (risk appetite increases concurrently with an increase in ), is the risk aversion coefficient during loss (risk appetite increases concurrently with an increase in ), is the sensitivity of the agent at gain/loss equilibrium (sensitivity increases concurrently with an increase in ). Therefore, , , and are closely associated with the three basic attributes (gender, wealth, and age) examined in the present study. In a subsequent experiment, we set different coefficient values for different agent types to obtain different utility functions. The optimal risk asset allocation plan in the current period can be determined based on the different rate of returns forecasted by the agents in each period. The allocation plan served as a basis for the subsequent formulation of decisions.

3.1.4. Agent Learning and Evolution

Agents in the proposed ASM are capable of learning and evolving. Agents with learning abilities can collate and reflect personal trading experiences and learn from their own or others’ learning experiences. Agent evolution reflects the evolution of the entire market. Agents that are unsuccessful and lose their wealth are unable to survive in the market and eventually withdraw from the market. These agents are replaced by new agents.

(1) Agents’ Learning Mechanisms

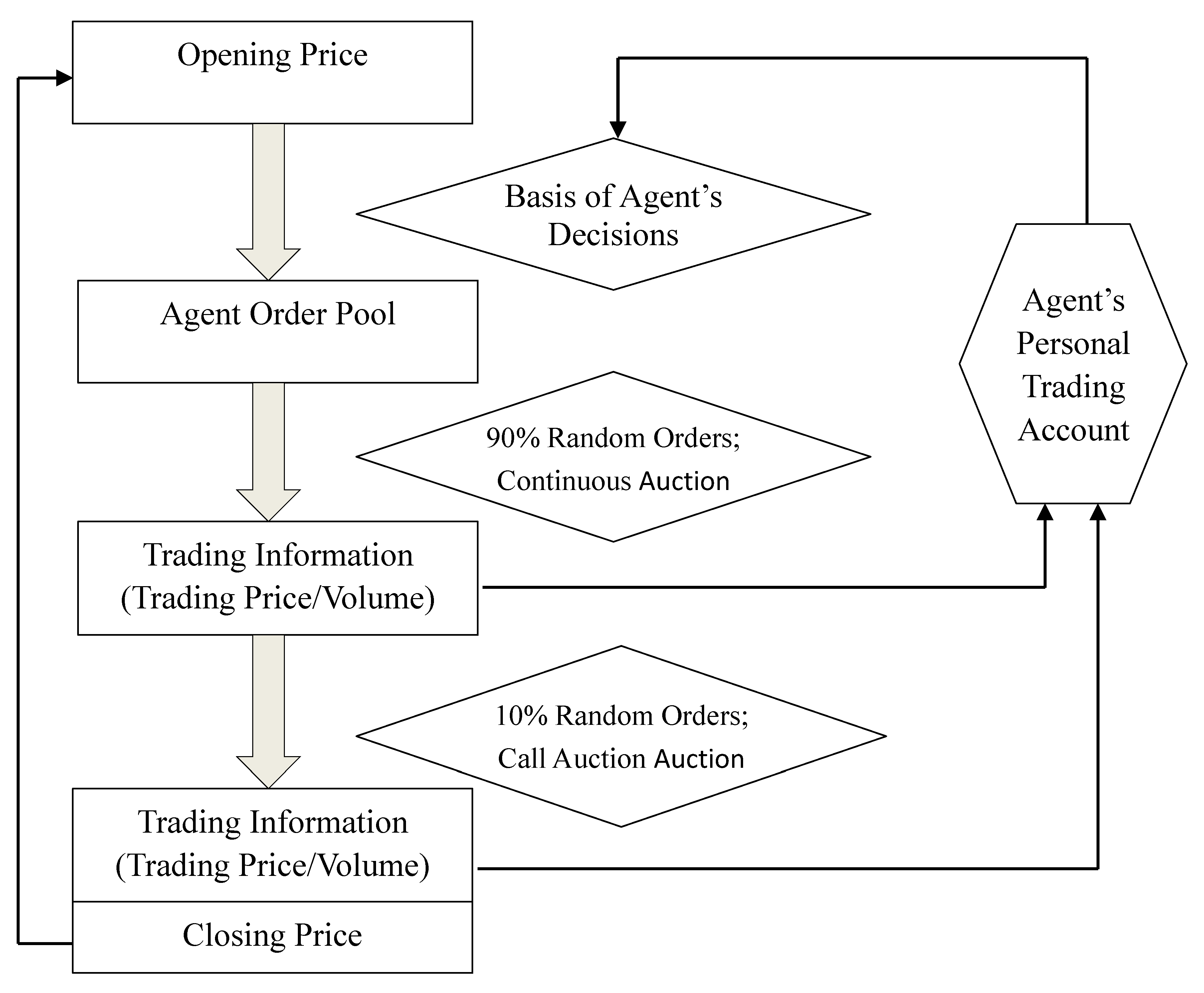

In the proposed ASM, each agent owns a personal account. The trading prices () and trading volume () of every transaction, daily wealth (), and experience account () are recorded in the personal account. The agents experience account, or his/her trading situation (failure/success), is updated in the personal account every 20 days. A successful transaction is recorded with a + 1, a failed transaction is recorded with a − 1, and an even transaction or no transactions are recorded with a + 0.

A successful or failed transaction is determined by comparing the trading price with the closing price in the same period. The transaction is considered successful if or , it is considered a failed transaction if or , and it is considered an even transaction if or . The jth day is set as the “learning day.” First, the agent reviews his/her investment situation in a specific period. That is, the agent compares and to calculate the number of successful and failed transactions in the specified period. The outcomes are then used for learning and improvement. The rules of this process are as follows:

- (i)

If , then the agent’s overall investment condition in the specified period is profitable. The agent is satisfied with his/her current investment strategy.

- (ii)

If

, then the agent’s overall investment condition in the specified period is unprofitable. In this instance, the agent further reviews his/her experience account (

). If

, the failed transactions in the specified period outnumber the successful transactions. Hence, the agent changes his/her investment strategy by referencing the strategies adopted by successful agents in the same category. That is, the agent learns from the profit makers (

) in the same row of

Table 1. When only one profit maker is present in the row, the agent adopts the profit maker as his/her target of learning. When multiple profit makers are present, the system randomly selected one profit maker as the agent’s target of learning. When no profit makers are available, the agent retains his/her investment strategy because he/she considers the failed transaction to be associated with overall market conditions rather than individual strategy.

- (iii)

If

and

, then the agent’s successful transactions outnumber failed transactions in his/her trading history. However, the agent remains unprofitable. In this instance, the agent considers the problem to derive from the poor allocation of assets and opts to change his/her utility function (relevant parameters) by referencing profitable agents in the same category. That is, the agent learns from profitable agents (

) in the same column of

Table 1. When only one profit maker is present in the column, the agent adopts the profit maker as his/her target of learning. When multiple profit makers are present, the system randomly selected one profit maker as the agent’s target of learning. When no profit makers are available, the agent retains his/her investment strategy because he/she considers the failed transaction to be associated with the overall market condition rather than individual strategy.

(2) Agent Evolution

In addition to learning ability, agent renewal and replacement also exist in a normal market. Agents that are unsuccessful eventually withdraw from the market. New agents also enter the market. In the development of the proposed ASM, we assumed that agents enter and withdraw from the market, but that the overall number of agents (n = 108) in the market remains unchanged. When , agent i withdraws from the market and is substituted by a random new agent. The investment strategy and utility function of the new agent are randomly generated.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}