1. Introduction

An official statistics program, such as a National Forest Inventory (NFI), is a large and complex interdisciplinary enterprise. It involves three different but closely interconnected disciplinarians: the remote sensing technologist, the resource analyst, and the sample survey statistician. Each discipline has different objectives, perspectives, and technical issues.

The remote sensing technologist produces synoptic geospatial databases that characterize certain conditions of land cover and changes in that cover over time and space. Within an NFI, examples include a few characteristics like land cover, woody biomass, and forest stand conditions. The technologist builds statistical models that use synoptic sensor data to predict those forest attributes for each mapping unit, such as a pixel or polygon. The resource analyst may use those geospatial predictions to gain a better qualitative understanding of the spatial and temporal patterns of major disturbances and land cover changes in the target population. Furthermore, enumeration of predictions for every mapping unit in the study area produces census statistics, such as the proportion of the study area with forest cover, as predicted with sensor data. The statistician may use those census data as auxiliary information to improve accuracy and reduce uncertainty in estimated population statistics for the study area.

The resource analyst studies the status, conditions, and trends within a large study area. An example in a NFI includes the demographic processes of tree populations within the study area, such as total tree growth, mortality, regeneration, and removals; distribution of tree species and tree sizes; supplies of wood fiber by different merchantability categories, including forecasts of future supplies; and indicators of forest health. Other examples include landscape-level changes in the extent and composition of forest stands and plant communities according to detailed classification systems. Major disturbances and changes in land use affect these characteristics of the population, and the remote sensing technologist can detect and quantify the magnitude of certain major changes. However, there are other important driving forces, such as markets for wood fiber, air pollution, climate change, drought, disease, and the ecological processes inherent to forest communities. Compared with major changes in land cover, many demographic and landscape changes evolve slowly over time, with spatial patterns that can be diffuse and fine grained within the landscape.

The NFI resource analyst typically investigates changes in a study area at a detail well beyond the measurement capabilities of synoptic orbital sensors. Much of the information relevant to the resource analyst requires detailed measurements of individual trees and forest stands by field crews. Since it is not feasible to measure every forest stand and every tree in a large study area, those detailed field measurements are made at a sample of sites. With probability sampling, those filed measurements are sufficient to produce unbiased statistical estimates of totals and means for the entire study area. The analyst uses detailed statistical tables that quantify the status and changes within the study area; these tables can require thousands of population estimates. The analyst also uses nonlinear transformations of population statistics to estimate proportions and rates of change in the study area. The thematic maps produced by the remote sensing technologist provide a qualitative spatial context, but such sensor data serve an ancillary role for the analyst’s detailed investigations.

The sample survey statistician produces those thousands of statistical estimates for the study area with detailed field measurements from the probability sample. One important goal for the statistician is maximization of statistical efficiency [

1] (p. 11, p. 65 and p. 227) and estimator accuracy and minimization of uncertainty given the constraints imposed by funding and the logistics of data processing. The statistician can use auxiliary information, primarily inexpensive sensor data, to improve population statistics. This is most often accomplished with conventional univariate sample survey methods, such as post-stratification and regression estimators.

The objective of this manuscript is to provide the remote sensing technologist a means to increase the value of sensor data to resource analysts. The related objective is to demonstrate to the sample survey statistician that multivariate model-assisted regression estimators are feasible in an official statistics program, which involves numerous study variables and numerous remotely sensed auxiliary variables. This statistical approach uses the Kalman filter (KF), which has been applied in navigation and control systems engineering for over 50 years. In the context of a sample survey, the KF is a type of multivariate regression estimator for population statistics. The KF can improve a vector of population statistics for study variables with a vector of population statistics for auxiliary variables.

The KF uses a state space representation of population parameters for the sampled population. In the context of the sample surveys, each state variable in the state vector is considered a “population parameter,” and each estimated state variable is a “population statistic.” The state vector contains all relevant population parameters. In the implementation below, one partition of the state vector contains the full time series of study variables that are important to the analyst, while another partition contains the full time series of auxiliary sensor variables. The KF constrains sample survey estimates for the auxiliary variables to exactly equal their census constants, which are known exactly from GIS enumeration of remotely sensed and other geospatial data for each and every pixel and polygon in the target population. These constraints improve statistical efficiency and reduce uncertainty for every study variable that is well correlated with any auxiliary sensor variable.

2. State Space

The following application of the Kalman filter (KF) uses the state space representation of a sampled population. In this context, state space is a set of statistical values, namely the “state vector,” that sufficiently quantifies all relevant attributes of that population. The state vector is denoted as

x, and each element in the state vector is a “state variable.” Consider the case in which there are

ks state variables that are important to the analyst, termed “study variables,” and

ka remotely sensed state variables, termed “auxiliary variables” [

1]. The latter are primarily intended to reduce uncertainty in estimates of correlated study variables.

In the following implementation of the KF, the state vector has a hierarchical structure. The first

ks-by-1 partition, denoted as vector

xs, includes parameters for the study variables, while the second

ka-by-1 partition, denoted as vector

xa, includes parameters for the auxiliary geospatial and remotely sensed variables. The full state vector

x has dimensions of

k = (

ks +

ka):

In the case of an NFI, some state variables have area as their unit of measure, such as the total hectares for a certain category of land use in the entire study area. Other state variables have different units, such as the number of individuals in a subpopulation or the number of remotely sensed pixels in the population that are classified into a certain category. Assume conventional sample survey methods [

1] make the initial estimate of the

k-by-1 state vector in Equation (1). An example is given in

Section 2.2 (below). The full state vector of population parameters is completely observable with this initial multivariate sample survey estimate.

The initial state vector has an associated

k-by-

k state covariance matrix for random errors that is consistent with the same design based estimator (see

Section 2.2 below). The state covariance matrix quantifies the strength of linear relationships among all statistical estimates in the state vector, including those among the study variables and the auxiliary sensor variables. The

k-by-

k state covariance matrix has conformable partitions with the state vector in Equation (1):

where

Vs is the

ks-by-

ks partition with the covariance matrix for the study variables;

Va is the

ka-by-

ka partition with covariance matrix for the auxiliary sensor variables; and

Vs,a is the

ka-by-

ks matrix partition of covariances between the study variables and the auxiliary sensor variables. The degree to which the KF can improve estimates of the study variables depends upon the absolute magnitude of the covariances in partition

Vs,a.

2.1. Time Series Structure for the State Vector

In a typical engineering application, the “dynamic” KF recursively “updates” estimates of the state vector at each step t in the discrete time series t = 1, 2, …, p. A single “recursion” of the dynamic KF combines a model-based estimate of the state vector for time t with an independent observation vector for the state of that system at time t. This updated KF estimate for time t has less uncertainty (i.e., smaller variance) than either the observation or the initial model based estimate for time t. Next, a linear model predicts the value of the state vector at time t + 1 given the best estimate at time t, and the recursive KF estimation repeats for time t + 1.

Unlike most applications of the KF, the following algorithm is a “static” estimator that uses only one recursion. There is no formal deterministic model that predicts the state of the system at time

t based on the best estimate at time

t − 1. The following algorithm implements a model-assisted estimator, not a model-based method (see [

1] for definitions). However, this algorithm can accommodate dynamic time series. The leading

ks-by-1 partition of the state vector can have sub-partitions for each and every discrete time

t. For example, if there were 11 annual time steps, and estimates for a set of 50 study variables are required for each time step, then the leading partition of the state vector would have

ks = 550 elements. If there is a time series of 30 auxiliary sensor variables at each of those 11 time steps, then in the trailing partition of the state vector would have

ka = 330 elements, and the full state vector would have a total of

k = 880 elements.

Let [

xt=j]

s be the vector of population parameters for all study variables measured at time

t =

j in the time series of

p years, beginning with year

t = 1 and each year thereafter until year

t =

p:

Each temporal partition in the time series can share the same types of study variables, For example, the

ith element of partition [

xt=j]

s might be the area of the sampled population covered by forested lands at time

j, while the

ith element of partition [

xt=j+1]

s might be the area of the sampled population covered by forested lands at time

t = (

j + 1). The corresponding state covariance matrix for estimation errors from the sample survey is:

The partition with the remotely sensed geospatial auxiliary variables xa is treated as time invariant even though there can be time series of sensor data. This is analogous to a photographic image, which does not change even though the subject of that image can change in the future and differed in the past. An image taken at one point in time can be correlated with the state of the subject in the past, present, and future. Most likely, the correlations will be strongest between sensor measurements and field measurements where the differences in measurement times are the smallest. Covariances between the time series of study variables and the time series of auxiliary sensor variables are in the last rows and last columns partitions of the covariance matrix in Equation (4). This structure for the state vector is one of several new features in this application of the KF to time series analyses.

2.2. Initial Estimate for the State Vector

Initialize the application with a design-based sample survey estimate for the full state vector. This estimate serves as the initial input into the KF,

i.e.,

t = 1. For simplicity, assume the special case of a simple random sample in which each sampled unit is measured at each time step. This initial estimate equals the (

ks +

ka)-by-1 vector mean for the random sample of

n units, where each sampled unit

i has a (

ks +

ka)-by-1 vector measurement:

Its estimated (

ks +

ka)-by-(

ks +

ka) covariance matrix is:

2.3. Observation Vector

In addition, the KF uses auxiliary information from an independent “observation vector,” which is referred to as the “measurement vector” by some authors in the KF literature. In the following implementation, elements in this

ka-by-1 vector, with its exact population means for auxiliary sensor variables as enumerated with a GIS, conform to the trailing

ka-by-1 partition of the state vector in Equation (1), with its sample survey estimates for those same auxiliary sensor variables. The population census parameters for all

ka auxiliary sensor variables over all

N pixels or polygons in the statistical population are enumerated with a GIS as:

3. Kalman Filter Estimator

The following application of the KF uses complete census information about remotely sensed auxiliary variables to increase precision in estimated population statistics for the study variables. It does this by constraining the

ka-by-1 partition of the state vector for the auxiliary statistics, which is estimated with the sample survey in Equation (5), to equal its exact true values in the observation vector

ya in Equation (7). This reduces variance of the estimate for any study variable that has a significant nonzero covariance with any auxiliary variable. (If the covariance with a study variable is zero, then the KF has zero effect on that study variable.) The KF applies these constraints as follows [

2].

Let

ka-by-

k matrix constant

H extract the

ka-by-1 partition for the auxiliary variables from the full

k-by-1 estimate of the state vector:

where

H = [

0 |

Ia],

0 is the

ka-by-

ks zero matrix, and

Ia is the

ka-by-

ka identity matrix. In the KF literature,

H is termed the “measurement matrix” or “observation matrix”.

The estimator for the state vector after the KF update [

2] is the matrix-weighted sum of the

k-by-1 vector estimate of

xSRS from the sample survey and the

ka-by-1 observation vector

ya from the GIS enumeration of values for every pixel and polygon in the statistical population:

where

I is the

k-by-

k identity matrix.

W is the

k-by-

ka matrix of Kalman weights, which is defined below in Equation (12). This single recursion with the KF may be considered an application of the multivariate composite estimator. If there were only one study variable, then Equation (9) is algebraically identical to the g-weighted regression estimator. The KF estimator for the state covariance matrix after the Kalman update [

2] in Equation (9) is:

The estimated value of

VSRS in Equation (10) is the

k-by-

k covariance matrix from the sample survey as in Equation (6), and

Va is the

ka-by-

ka covariance matrix for the independent population estimates of auxiliary variables. The vector of population parameters

ya in Equation (9) is a known constant because it is the enumeration of all pixel and polygon values in the statistical population; therefore, its covariance matrix for random sampling errors is

Va =

0, which simplifies Equation (10) to:

The optimal

k-by-

ka KF weight matrix

W is computed [

2] as:

The KF weight matrix

W in Equation (12) yields the Best Linear Unbiased Estimator (BLUE) for the state vector [

2], conditional upon the estimated covariance matrix

from Equation (6). The KF estimator is “optimal” in the sense of a minimum variance or least squares estimator [

2].

Unfortunately, the numerical computation in Equation (12) is notoriously unstable, especially as

Va → 0. Fortunately, the engineering literature offers alternative KF algorithms with superior numerics [

3,

4]. I offer one such algorithm in

Section 4, which assumes the special case in which the observation vector is a known census constant,

i.e.,

Va =

0.

4. Novel Kalman Filter Algorithm

In this section, I present a new algorithm for computations necessary to apply Equations (9)–(12). This algorithm solves numerical problems associated with large state vectors and rank deficient state covariance matrices. It strictly assumes the observation vector is a known constant, namely,

Va =

0 in Equation (10). Like a square root filter [

3,

4], this algorithm sequentially applies one auxiliary sensor variable at a time. In this way, the algorithm replaces the matrix inverse in Equation (12) with the scalar inverse. This simplifies the program code required for inversion of an ill conditioned or singular covariance matrix partition

Va in the estimated state vector; see Equation (6). However, unlike a conventional square root filter, the algorithm does not require prior orthogonalization of that matrix partition [

4] (Chapter 7.4), which reduces the computational burden, especially with a large partition of the covariance matrix.

A single invocation of the algorithm iterates through ka loops in lines 3 to 15, with one iteration for each of the ka auxiliary sensor variables. Within the ith iteration, the KF update uses the ith census constant yi in Equation (7) to improve the KF estimate for the entire state vector. By “improve,” I mean reduce the magnitude of random estimation errors as measured with the covariance matrix for the estimated state vector. Each iteration improves the KF estimate for any study variable that has a nonzero covariance with the ith auxiliary variable after the (i − 1)th loop. Those covariances reside in partitions of the state vector and state covariance matrix having subscripts 1, 2, …, ks. In addition, the ith KF update improves estimates for the remaining auxiliary sensor variables, which reside in partitions with subscripts (ks + 1), (ks + 2), …, (ks + i − 1). If there is zero covariance between any one of these variables and the ith auxiliary variable, then the KF places zero weight on the ith auxiliary variable, meaning the KF has no effect on such these variables during the ith iteration. The KF vector estimate after the ith iteration serves as initial conditions for the KF in the next (i + 1)th iteration.

After the ith iteration, the KF estimate of the (ks + i)th state variable, which is the estimated population mean for the ith auxiliary sensor variable, will exactly equal its corresponding census constant yi, which is computed with the GIS enumeration in Equation (7). This means that the KF “estimate” for that state variable has no random estimation error. Therefore, the (ks + i)th row and column of the state covariance matrix equal the conformable zero vector in Equation (A14), which by definition makes the (ks + i)th state variable orthogonal to all other estimated state variables. In other words, the algorithm performs a sequential orthogonalization of the (ks + i)th state variable within each iteration. This is computationally more efficient, and perhaps numerically more accurate, than a square root filter that requires prior orthogonalization of the full ka-by-ka covariance matrix partition Va. of the estimated state covariance matrix in Equation (6).

Because the algorithm uses a scalar inverse rather than a matrix inverse, it can readily accommodate an ill conditioned or singular covariance matrix. I now explain. The KF weight vector W from Equation (12) is computed in line 11 of the algorithm. This requires the scalar inverse of the variance on the (ks + i) th diagonal element of the estimated state covariance matrix from previous iteration. If that variance is very small (e.g., less than 10−4), then its inverse will be excessively large (e.g., greater than 104). This risks numerical instability. If that variance is nearly zero, then the algorithm omits the KF constraint with the ith auxiliary census constant (see line 5 of Algorithm 1). An estimate of an auxiliary sensor variable with a very small variance typically has very low covariance with the study variables. Therefore, omission of such an auxiliary sensor variable will not notably sacrifice statistical efficiency.

| Algorithm 1 R code that applies sequential Kalman filter (KF) update with known observation constants (measurement vector) and rank deficient state covariance matrix. |

| Input | x is (ks + ka)-by-1 design based initial estimate of state vector |

| V is (ks + ka)-by-(ks + ka) design based initial estimate of covariance matrix |

| y is ka-by-1 conformable vector of auxiliary census constants |

| ks is number of study variables |

| ka is number of auxiliary variablesk = ks + ka |

| 1 | w < − matrix(0,k,1) # initialize with k-by-1 zero vector |

| 2 | I.wh < − diag(k) # initialize with k-by-k identity matrix |

| 3 | for ( i in ka:1 ) { # i = { ka, (ka − 1), ..., 1} |

| 4 | k < − ks + i |

| 5 | if ( V[k,k] < tol ) next # tol near zero (e.g., tol = 0.0001) |

| 6 | c = 2*abs( y[i] − x[k])/V[k,k] |

| 7 | if ( c > 1 ) { # divergence constraint from Equation (A17) |

| 8 | V[1:k,k] < −V[1:k,k]*c |

| 9 | V[k,1:k] < −V[k,1:k]*c |

| 10 | } # end of divergence “if statement” |

| 11 | w[1:k] < −V[1:k,k]/V[k,k] |

| 12 | I.wh[1:k,k] < −(-w[1:k] ) # subtract vector w from k-th column |

| 13 | x[1:k] < − ( I.wh[1:k,1:k] %*% x[1:k] ) + ( w[1:k]*y[i] ) |

| 14 | V[1:k,1:k] < −I.wh[1:k,1:k] %*% V[1:k,1:k] %*% t( I.wh[1:k,1:k] ) |

| 15 | } # end of i-th iteration |

| Definitions | [a:b,c] is the matrix partition, rows a to b, column c |

| <− is the replacement operator |

| abs(z) is the absolute value of scalar z |

| t(A) is the transpose of matrix A |

| %*% is the matrix multiplication operator |

| w is the k-by-1 vector of computed optimal Kalman weights |

| I.wh is the k-by-k matrix of complementary Kalman weights |

| Output | x is (ks + ka)-by-1 state vector after Kalman updates with ka auxiliary variables |

| V is (ks + ka)-by-(ks + ka) covariance matrix with ka auxiliary variables |

Successful applications of the KF require close attention to residual differences between statistical estimates of auxiliary sensor variables and their exact census values. This can be caused by extreme random sampling errors and undetected non-sampling errors, such as database or software errors. If that residual difference is unexpectedly large relative to its estimated variance, then “too much weight” can be assigned to the auxiliary sensor variable, thus causing “divergence.” An estimated variance of the residual that exceeds two standard deviation units (line 6 in the algorithm) is an indication of a significant source of non-sampling error. Whenever this occurs, I assume the

ith row and column of the estimated covariance matrix is “too small.” To mitigate this apparent anomaly, the algorithm inflates the

ith row and column of the estimated covariance matrix (see lines 8 and 9 in algorithm) so that the resulting residual difference is exactly two standard deviations from its estimated expectation. The mathematical statistician should refer to

Appendix A.3 for details.

The above algorithm can potentially process thousands of auxiliary sensor variables to improve estimates for thousands of study variables. But there is a risk. Consider one of many auxiliary sensor variables that truly have zero correlation with certain study variables. The true value of that correlation is unknown; only a statistical estimate of that value is known. That statistical estimate will likely be very close to zero; however, through random sampling error, that estimate will not exactly equal zero. The KF will reduce the estimated variance for every study variable that has a nonzero covariance with an auxiliary sensor variable, even if that covariance is very small. The reduction will be small, but not zero. Assume there are large numbers of auxiliary sensor variables that are truly uncorrelated with a study variable, but they have estimated covariances that are nonzero but very small. Each such auxiliary sensor variable will contribute a small reduction in the variance of the estimated study variables. This can unintentionally accumulate into a notably large reduction. Methods given in

Appendix A.4 (below) mitigate this risk. Those methods identify each off-diagonal element of the state covariance matrix that has a correlation smaller than that expected by chance. Before and after invocation of the algorithm, the estimated covariance for each element that is nearly equal to zero should be changed to exactly zero.

Another risk is a large random sampling error in estimation of the correlation (covariance) between a study variable and an auxiliary sensor variable. If the known estimate substantially differs from its unknown true value, then too much or too little KF weight is placed on the auxiliary variable. Therefore, the KF should only be applied to variables with sufficient sample size.

Section 5 and

Appendix A use the following criterion: every study variable and auxiliary sensor variable must have a nonzero measured value for least 25 sampling units.

5. Case Study

Application of the algorithm is demonstrated with the following case study. It uses NFI data from the Forest Inventory and Analysis (FIA) Program in the USA [

5]. The case study includes two objectives. The first involves estimation of standard official statistics in a forest monitoring program, which is intended to evaluate the capability of the multivariate algorithm to produce large numbers of population statistics. The second objective tests application of the algorithm in the context of a special study, which is often a high priority to the resource analyst. This special study investigates an epidemic of tree mortality in the State of Colorado from mountain pine beetles (

Dendroctonus ponderosae Hopkins), which has swept through the montane forests of the western United States during the past 10 years [

6,

7]. Tree mortality has been most severe in the lodgepole pine (

Pinus contorta) tree population. This phenomenon is highly concentrated into discrete patches of extensive forests, which can be described as tree mortality at the stand scale. Colorado is among the most severely impacted geographic areas in the United States. This case study analyzes the portion of Colorado that contains the vast majority of lodgepole pine forests, regardless of current impacts from mountain pine beetles. The study area covers approximately 30% of Colorado (

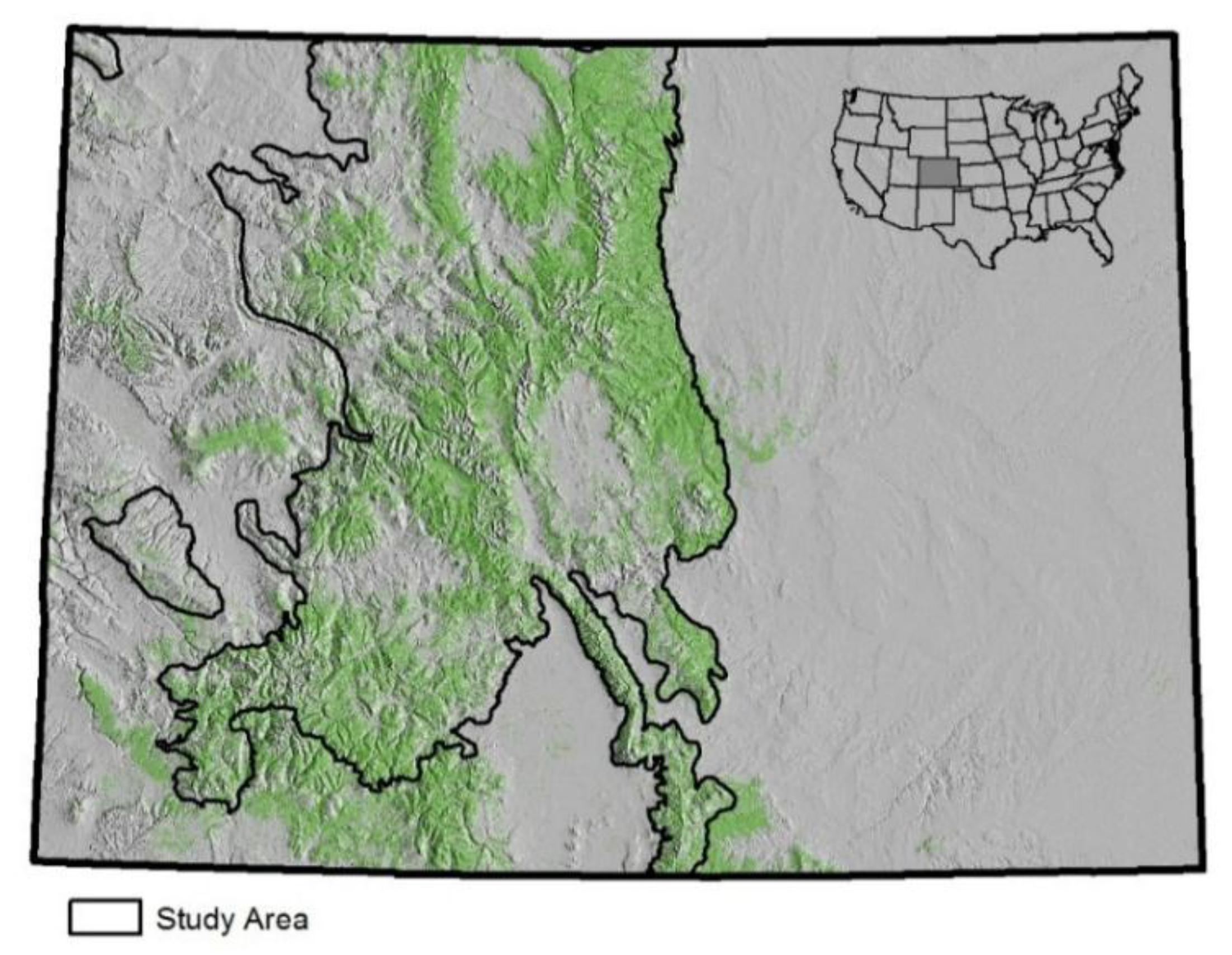

Figure 1). Annual FIA data are available for each of 11 years beginning in 2002.

Figure 1.

Study area (91,976 km2) and spatial distribution of forest cover across the State of Colorado, which covers an area 600 km east to west and 450 km north to south.

Figure 1.

Study area (91,976 km2) and spatial distribution of forest cover across the State of Colorado, which covers an area 600 km east to west and 450 km north to south.

In order to produce standard NFI statistics, there are 3788 FIA plots in this study area, with an average of about 380 sample plots measured each year within an annual panel of primary sampling units, which is a probability sample of the entire study area. An average of 230 of these plots fall within forested conditions each year, of which an average of 60 plots have one or more lodgepole pine tally trees (

Figure 2). Within any single annual panel, 43 to 60 plots had live lodgepole pine tally trees infested with insects; 17 to 30 plots had lodgepole pine mortality trees in the tally.

Figure 2.

Approximate locations of FIA ground (field) plots in study area that are classified as forest with lodgepole pine trees. The figure does not identify locations for the remaining 75% of other FIA sample plots in the study area, which are distributed on an approximate 5 km by 5 km grid; however, all sampled plots in the study area, regardless of forest classification, are used in the sample survey estimators.

Figure 2.

Approximate locations of FIA ground (field) plots in study area that are classified as forest with lodgepole pine trees. The figure does not identify locations for the remaining 75% of other FIA sample plots in the study area, which are distributed on an approximate 5 km by 5 km grid; however, all sampled plots in the study area, regardless of forest classification, are used in the sample survey estimators.

The case study also includes separate estimates for a small analysis area, namely the Arapaho Roosevelt National Forest (ARNF), which covers the 6% study area that is most severely impacted by the mountain pine beetle epidemic. There are 239 FIA plots in this National Forest, with an average of 24 plots measured each year. I use a three-year moving window of remeasured FIA plots to increase sample size from multiple annual FIA panels for this small area. The three-year window is a compromise between augmentation of the sample size and retention of interpretable time series estimates. The ARNF example is typical for special studies conducted by the analyst.

The statistical estimates for study variables include: basal area and numbers of lodgepole pine trees classified by their mortality status; area by forest type; stocking; net tree growth. The result is 212 study variables. However, many of those attributes are rare, even with a three-year moving window. As recommended in

Section 4, any study variable having less than 25 nonzero values in the sample at any of the 11 time steps is omitted; therefore, estimates for only 136 of those 212 study variables are made with the KF.

For remotely sensed and other geospatial auxiliary variables, this case study uses a combination of: polygon data from airborne reconnaissance techniques; digital data from two orbital sensors, each with a different pixel resolution; and independent polygon data from a biogeographical model. The spatial resolution of these auxiliary data range from 0.1-ha pixels to nearly one million-hectare polygons. Each set of spatial data completely tessellates the entire study area so that the exact population parameter value for every auxiliary variable is known through enumeration of all pixels and polygons with a GIS (

Section 2.3).

One set of auxiliary variables uses geographic data from Aerial Detection Surveys (ADS), which are conducted each year by the Forest Health Protection Program. While systematically flying in light aircraft over impacted forests, trained ADS observers visually map broad areas based on visual evidence of episodic tree mortality, where each mapped polygon can represent hundreds of hectares. An ADS “mortality polygon” circumscribes an area that contains obvious concentrations of tree mortality. Each ADS mortality polygon ranges in size from 5 to 500 ha. However, each mortality polygon is a heterogeneous mixture of impacted forest, unaffected forest, and non-forest. Other polygons record areas that were surveyed by ADS observers but contained no remarkable areas of tree mortality. All remaining portions of the study area are classified as unobserved, which typically connotes low impacts from insect damage. There is variability in classifications among observers. These three categories of ADS classifications are available in the GIS for each of the 19 years from 1999 to 2012. After the transformation of these 19 multinomial variables, each with three categories, there are 57 ADS auxiliary variables.

A second set of auxiliary variables comes from multispectral data captured with the MODIS sensor aboard the Terra (EOS AM-1) and Aqua (EOS PM-1) spacecraft, which orbit 705 km above the earth’s surface. MODIS measures 36 different spectral bands, two of which have a nominal spatial resolution of 250-m (6.0-ha) pixels. There are approximately 1.5 million MODIS pixels in my study area. Remote sensing technologists developed statistical models that predict for each MODIS pixel whether or not forest cover is the predominant land cover [

8].

A third set of auxiliary variables originated with the Enhanced Thematic Mapper Plus (ETM+) sensor aboard Landsat satellites, which also orbit 705 km above the earth surface. The EMT+ sensor measures seven different spectral bands, six of which have a nominal spatial resolution of 30 × 30 m (0.1-ha) pixels. There are approximately 90 million EMT+ pixels in my study area. A multiagency consortium of LANDFIRE technologists developed nonparametric statistical models that predict for each ETM+ pixel the predominant category of vegetation [

8,

9]. There are seven categories of vegetation, one of which is “coniferous forest,” for a total of seven binary auxiliary variables.

The ADS protocol is designed to identify “hot spots” of tree mortality each year at the landscape scale; it is not specifically designed to classify episodic tree mortality at the spatial scale of a FIA plot. Therefore, an ADS polygon is relatively large and heterogeneous, with a mixture of many forest stands among which severity of tree mortality varies, and each ADS polygon has non-forest inclusions. I attempt to improve spatial resolution of the ADS data through an intersection of the relatively large ADS polygons with the 30 × 30 m LANDFIRE pixels classified as coniferous forest. This improves agreement between ADS classifications and field observations of tree mortality. However, there are misclassifications of coniferous forest with LANDFIRE pixels, and many forested portions of an ADS mortality polygon are uninfected. Therefore, the agreement is somewhat weak among these auxiliary variables and those study variables related to individual tree mortality. Regardless, this intersection increases the number of binary ADS auxiliary variables from 57 to 114.

A fourth set of auxiliary variables comes from classifications of broad landscapes into different ecoregions based on differences in climate, land form, land management, and ecosystems [

10]. I use the Subsection level in this hierarchical classification system. Subsections completely tessellate the study area into 31 binary auxiliary variables, one for each unique Subsection. The average size of a Subsection polygon is almost 1 million hectares.

Another set of auxiliary variables divides the study area based on administrative units for land management, primarily the six different National Forests in Colorado. This forces the total estimated area for each National Forest to exactly match the official administrative statistics. It also captures certain differences in forests caused by regional epidemiological conditions and land management practices. The Arapaho Roosevelt National Forest is one of those administrative units. This National Forest has experienced the most severe impacts from bark beetle epidemic in Colorado, and additional statistical estimates are made specifically for this small domain.

The final set of auxiliary variables are counties, which are administrative units for local governmental organizations. A county is a spatially contiguous geopolitical subdivision of a state. There are 3007 counties in the USA, and the average size of each is about 3000 km2. The area of each is an administrative census constant. Inclusion of counties as auxiliary variables is intended to assure that the total estimated area of each county agrees with its official census area, which is a common expectation from users of these statistics. The intent is not variance reduction. However, county boundaries also tessellate the study area into contiguous areas, which might capture some of the underlying geospatial patterns in the study variables. Each county is separated into two categories with 6.0-ha MODIS pixels, each of which is classified into forest cover or non-forest cover with sensor data. Since there are 46 counties, this creates 92 binary auxiliary variables in the state vector.

The outcome is a total of 252 remotely sensed and other geospatial auxiliary variables for millions of pixels and polygons. The GIS extracts the values for each of those 252 auxiliary variables for each of those 3788 plots in this case study. The GIS enumerates all pixels and polygons for those 252 auxiliary census values across the entire study area. Therefore, the statistical estimator requires a very small fraction of the spatial data processed by the GIS.

An auxiliary variable can be rare, which in my case means most plots have a measured value of zero for that variable. However, through chance alone, a rare auxiliary variable can be highly correlated with a study variable. Such an auxiliary variable would greatly reduce the estimated variance of the study variable even though there is truly little association with the auxiliary. To mitigate this risk, only those variables with non-zero measurements at 25 or more sampling units are estimated with the KF (see

Appendix A.4 for details). This reduced the number of auxiliary variables from 252 to 164. Furthermore, the algorithm omits auxiliary variables whenever their estimated variance is or becomes nearly zero during each

ith loop iteration within the algorithm. This effectively eliminates redundant information among the auxiliary sensor variables.

The case study compares improvements in the quality of monitoring data with the KF to improvements with the conventional post-stratification estimator. A typical analytical study might use post-stratification with any of the available remotely sensed data. However, the feasible number of strata is limited by the relatively small sample size of FIA plots in each annual sample panel. The stratification is based on intersection of the three different categories used in each of the annual Aerial Detection Surveys (ADS) with the time invariant LANDFIRE ETM+ classification of conifer forest. Therefore, there are six potential strata for each of the 10 FIA panels. Strata change from year to year because the remotely sensed ADS data change each year. I extrapolate the criterion offered by [

11]. If a stratum during one year has fewer than 10 plots, then that stratum is combined with a similar stratum. In most cases, this meant use of a single stratum for ADS mortality polygons rather than an intersection of ADS polygons with the LANDFIRE classification of coniferous forest cover. This process reduced gains from post-stratification, but there is little choice given the limited number of available sample plots.

Post-stratification is compared with two different sets of estimates with the KF. The first set uses only ADS classifications of tree mortality intersected with LANDFIRE predictions of coniferous forest cover for ETM+ pixels. This allows direct comparison of the two post-stratification and Kalman estimators given approximately the same stratification variables and auxiliary variables. The comparison is not exact because the KF uses all 44 ADS auxiliary variables across all years, while the number of plots in each panel restricts post-stratification to ADS data from a single year. The second set of estimates with the KF uses those same 44 ADS variables plus the additional 120 auxiliary variables described above.

Table 1 summarizes the results for this case study. I use the “design effect” to compare statistical efficiency of each set of estimates to the simple random sampling estimator. The design effect [

1] (p. 53) compares the efficiency of each set of estimates with the post-stratification and KF estimators to the simple random sampling estimator. A “design effect” of 10% means a 10% reduction in estimated variance relative to the variance from the simple random sampling estimator. This is an increase in statistical efficiency. A negative design effect for the post-stratification estimator means that it actually degrades estimation accuracy and reduces statistical efficiency. There are 11 estimates for each study variable, one for each year from 2002 to 2012. I present only the minimum and maximum statistics among each of those 11 years to reduce cluttered details.

The post-stratification estimator reduced statistical efficiency in this particular case study; the simple random sampling estimator has less variance in estimation errors than the post-stratification estimator for certain study variables. There are at least three potential causes for this situation in this single case study. First, post-stratification on ADS polygons can increase the “within stratum” variance for some study variables between values at sampling units and their strata means. This might be caused by the coarse spatial resolution of ADS polygons relative to the size of FIA plots, especially for panels with a sample size too small to subdivide large heterogeneous ADS polygons by LANDFIRE classifications of coniferous forest. The most useful auxiliary information from ADS polygons was identification of forests that have no evidence of insect infestations. Second, the estimated stratum mean can have substantial random sampling error, which can inflate the variance of the residual differences between values at sampling units and their estimated strata means [

1] (p. 267). Third, the variance computation for post-stratification contains an adjustment for the random sample size within each stratum, and that approximation might not be sufficiently accurate given the small sample sizes in many strata.

In contrast, the KF always improves accuracy. This mathematical axiom is apparent from Equations (A8) and (A15) in the

Appendix A (below). The improvements are generally greatest in the estimates for the Arapaho Roosevelt National Forest with the study variables for infestation and tree mortality. This National Forest has few FIA plots compared to the entire study area. The KF was especially effective for small domains in this particular case study.

If attention were restricted to those estimation years with the maximum improvement from post-stratification, then improvements from post-stratification are somewhat greater than most improvements with the KF, at least when they share the same post-stratification and auxiliary variables. However, the pattern is reversed with the KF that uses all auxiliary variables, regardless of whether or not they are used for post-stratification. The KF generally produces more precise and reliable estimates than post-stratification in this one case study. However, this does not necessarily mean the KF will be more efficient than post-stratification in other studies.

Table 1.

Change in statistical efficiency with auxiliary sensor data. The minimum and maximum statistics among 11 years are presented. Negative values indicate a loss of statistical efficiency.

Table 1.

Change in statistical efficiency with auxiliary sensor data. The minimum and maximum statistics among 11 years are presented. Negative values indicate a loss of statistical efficiency.

| Small-Area (Arapaho Roosevelt NF) Estimates for Three-Year Moving Window | Minimum Efficiency Gain or Loss | Maximum Efficiency Gain or Loss |

|---|

| Post-Stratification Estimator | Kalman Filter, Post-Stratification Auxiliary Variables Only | Kalman filter, All Auxiliary Variables | Post-Stratification Estimator | Kalman Filter, Post-Stratification Auxiliary Variables Only | Kalman Filter, All Auxiliary Variables |

|---|

| Number of live uninfested lodgepole pine trees | −2.4% | 1.6% | 3.2% | 4.4% | 3.7% | 6.6% |

| Number of live infested lodgepole pine trees | −0.7% | 2.0% | 4.5% | 8.7% | 4.9% | 9.1% |

| Number of first-year morality lodgepole pine trees | −8.0% | 0.5% | 2.5% | 0.2% | 2.0% | 7.8% |

| Area of forest stands dominated by large trees | −42.1% | 1.6% | 6.2% | −29.0% | 4.1% | 11.3% |

| Entire population, estimates for 3-year moving window | | | | | | |

| Number of large live uninfested lodgepole pine trees | −58.3% | 0.2% | 1.6% | 1.3% | 1.4% | 3.4% |

| Number of large live infested lodgepole pine trees | 1.0% | 1.5% | 3.6% | 8.3% | 4.5% | 7.4% |

| Number of large first-year morality lodgepole pine trees | −12.1% | 0.7% | 2.6% | 4.0% | 3.2% | 6.0% |

| Number of small live uninfested lodgepole pine trees | −0.2% | 1.1% | 2.4% | 5.9% | 3.4% | 6.1% |

| Number of small live infested lodgepole pine trees | −2.0% | 1.2% | 2.4% | 9.3% | 3.6% | 5.4% |

| Number of large first-year morality lodgepole trees | −10.5% | 1.0% | 2.7% | 2.6% | 2.9% | 8.3% |

| Area of non-stocked forest stands | −23.9% | 0.4% | 2.6% | −13.8% | 0.7% | 3.5% |

| Entire population, annual estimates | | | | | | |

| Total basal area of lodgepole pine trees | 1.8% | 1.0% | 2.2% | 11.5% | 3.0% | 4.6% |

| Total net tree growth | −1.2% | 0.5% | 2.2% | 5.0% | 2.5% | 4.0% |

| Percent tree stocking of forest stands | 1.2% | 0.9% | 3.5% | 8.6% | 1.8% | 5.3% |

6. Discussion

Increases in statistical efficiency with auxiliary remotely sensed data will vary among different studies. The discussion begins with candidate sources of this variation and methods that improve efficiency. It then covers advantages of multivariate estimators such as the KF. It follows with discussion of methods that improve statistical reliability. It ends with thoughts for future research and development.

First, I extrapolate previous recommendations for stratification by [

12]. The agreement between a categorical auxiliary variable (e.g., forest cover) and its categorical study variable (e.g., forest land use) should generally exceed 90% for common categories and 75% for rare categories [

12]. In detailed classification systems, which have many categories, most categories are relatively rare.

Gains from multispectral remotely sensed auxiliary data depend on the strength of the linear relationships between the auxiliary variables and study variables. However, that relationship can be nonlinear. Exploratory statistical analyses can detect such relationships. A nonlinear or nonparametric statistical model can be built with remotely sensed variables to predict field measurements of study variables. Examples include k-Nearest Neighbor and [

13,

14,

15] and Classification and Regression Trees [

16]. The linear relationship between a study variable and its expected value as predicted with a nonlinear model can be more effective than direct use of remotely sensed variables as predictors. However, predictive models fit with sample survey data for training should be used with caution in estimation applications because they are not independent ancillary data, and this poses challenges akin to endogenous post-stratification [

17,

18].

Categorical auxiliary variables have the values of 0 or 1 for each pixel, polygon, or population unit. This produces relatively large variances around mean prevalence. Unless the distribution is extremely skewed, continuous remotely sensed variables tend to have smaller variances around their expected values. For example, a statistical model that uses remotely sensed data to predict the proportion of crown cover for each predominant tree species in each pixel might increase efficiency more than a model that classifies that pixel into a single forest type. For continuous variables, consider the recommendation by [

1] (p. 224 and p. 250): the absolute value of the linear correlation between an auxiliary variable and a study variable should be 0.5 or higher. An eight-fold gain in statistical efficiency is possible with a correlation of 0.95 [

1].

Because the numerics of the algorithm can accommodate very large sets of auxiliary variables, classification algorithms with remotely sensed data can be specialized for each individual category for a multinomial study variable, such as different types of land cover. For example, a separate binomial thematic map may be optimized for each individual category of land cover (e.g., one for deciduous forest cover, another for coniferous forest, and yet another for cropland). With separate thematic coverage for each individual category, a pixel need not be classified into one and only one category among multiple classification systems. However, inclusion of more auxiliary variables does not necessarily contribute more auxiliary information.

A relatively small number of outlier predictions, or a relatively small proportion of misclassified pixels, can markedly reduce the linear correlations between auxiliary sensor variables and the analyst’s study variables. This would reduce the value of auxiliary sensor data for improvements in statistical monitoring. Therefore, a remotely sensed category should not mix pixels that can be reliably classified with other pixels that are difficult to accurately classify. Following recommendations by [

12], a pixel should not be assigned to a category unless there is relatively high confidence that the remotely sensed classification agrees with the classification field protocol. For example, time series of remotely sensed classifications can identify geographic areas affected by rapid changes in forest cover over time. Remotely sensed data gathered before those changes might be poorly correlated with field observations after those changes. Another example is pixels affected by challenging conditions, such as cloud shadows, steep slopes, sparsely stocked forest, and forest stands with diverse conditions; these pixels do not necessarily need to be classified into any remotely sensed category. Misregistration between the geographic location of a plot and its corresponding pixel or polygon degrades associations among auxiliary sensor variables and field measurements of study variables, especially in heterogeneous, fine-grained landscapes. Methods that might reduce this source of non-sampling error are reviewed by [

2] (p. 100).

The case study includes multivariate vector estimates that improve standard official statistics, such as detailed statistical tables [

19]. The state vector can include a study variable for each and every cell in every statistical table. The row and column margins of each table can be the postestimation sum of estimates for each cell, and the estimated variances for each statistic on the margin computed with the full state covariance matrix [

2]. This would assure that sums of estimated cell values in statistical tables agree with their corresponding row and column totals, including consistency among variance estimates.

The vast majority of sample survey estimators are designed or optimized for a single univariate study variable. Large numbers of estimates produced by official statistics organizations are typically a collection of multiple univariate estimates. Each has an estimated variance for estimation errors, but the sample survey literature rarely considers the covariance matrix for joint estimation errors among numerous population statistics. Off-diagonal covariances serve an important role in variance estimation for transformations of population estimates that are important to analysts. An example is a simple linear transformation of estimates, such as the marginal sum of cells in an estimated statistical table [

1] (p. 399). An example of a nonlinear transformation is the proportion of all live lodgepole pine trees that are heavily infested with bark beetles at time

t. This is the ratio of the estimated number of infested trees divided by the estimated total number of live trees. Yet another example is the mortality rate, which is defined as the number of live infested trees at time

t divided by the number of recent mortality trees at time

t + 1. In a NFI panel design, the same sample tree is never measured at both times

t and (

t + 1) because each NFI plot is measured only once every 5 to 10 years. Therefore, estimates for annual mortality rates are feasible only at the population level. These transformations require linear or nonlinear transformations of elements in the estimated state vector, and variance estimates for these transformations all require estimates for the covariances among study variables.

Transformations of the state vector are known as “synthetic estimators” and “pseudo estimators” in the sample survey literature [

1] (pp. 173−174, pp. 205−207 and p. 399). The associated variance estimators require complementary transformations of the state covariance matrix. For example, [

2] (pp. 68−87) creates a new postestimation state variable for each synthetic and pseudo estimator and develops multivariate linear transformations that appends those to the state vector and state covariance matrix. That covariance matrix has sufficient partitions for all study variables after the Kalman update plus additional partitions for all postestimation synthetic and pseudo estimates. This facilitates additional transformations of synthetic and pseudo estimates; an example is the estimated difference in annual survival rates between large and small trees. Therefore, the analyst may transform multiple time series of statistical estimates for the entire population, small areas or small domains through multiple sequential combinations of the addition, subtraction, multiplication and division operators. Variance estimators for all of these transformations are available in [

2].

A large number of auxiliary variables is analogous to a large number of predictor variables in a multiple regression. There are risks from outliers, chance correlations, numerical errors, estimates for rare variables that are nearly sampling zeroes, and ill-conditioned partitions for auxiliary variables in the state covariance matrix. These risks are mitigated in multiple ways.

Analyze only those study variables and auxiliary variables that have nonzero values for 25 or more sampling units.

The algorithm in

Section 4 (see line 5) uses a scalar inverse, which avoids numerical problems with the matrix inverse in Equation (12).

The algorithm (see lines 6 to 10) uses the constraint from

Appendix A in Equation (A17), which hedges against a suspiciously large residual difference between the populations estimate for an auxiliary variable and its true census value. Such outliers can be a result of non-sampling errors, or rare random sampling errors, or random error in estimates of the covariance between study variables and auxiliary variables, or an auxiliary variable that is highly correlated with other auxiliary variables that were previously processed by the algorithm.

Use statistical tests to identify very small correlations between auxiliary sensor variables and study variables that are likely caused by random chance (

Appendix A.4). Re-estimate those correlations as zero rather than the small nonzero value. This mitigates unintended cumulative consequences with large numbers of auxiliary variables, each of which is well correlated with certain study variables but has nearly zero correlation with other study variables.

To further reduce potential numerical errors, center state space on the zero vector, and subsequently scale state space so that the covariance matrix from the multivariate design based estimator has the unit diagonal. After the KF estimation process is complete, re-transform state space back to its original metrics.

Finally, the analyst must be alert for apparent anomalies among estimates. These can be obvious during careful comparisons of different estimates, as in a time series graph for a study variable. In aggregate, I believe these measures can reasonably assure the algorithm is robust to anomalies in a realized sample, non-sampling errors, and numerical errors.

I urge caution in extrapolating results from the case study in

Section 5. That case study uses a single realization of a single sample from a single geographic area with a single set of auxiliary variables. Different populations with different auxiliary sensor variables might be more, or less, correlated with different study variables. Additional case studies would provide stronger conclusions regarding the post-stratification and Kalman estimators.

{kind=link}

{kind=link}

{kind=link}