Uncertainty in Estimates, Incentives, and Emission Reductions in REDD+ Projects

Abstract

:1. Introduction

The Problem and the Approach to Investigate

2. Literature Review

3. Methods

3.1. Incentive and Profit Functions

3.2. Measuring Uncertainty

3.3. Stakeholder Decision-Making Model in the Scenario without Incentive (BAU Scenario)

3.4. Stakeholder Decision-Making Model in Incentive Scenarios

3.4.1. Incentive Scenario for Landholders (s1 Scenario)

3.4.2. Incentive Scenario for Investors (s2 Scenario)

4. Results

4.1. Numerical Specification

4.2. Numerical Simulation

5. Discussion

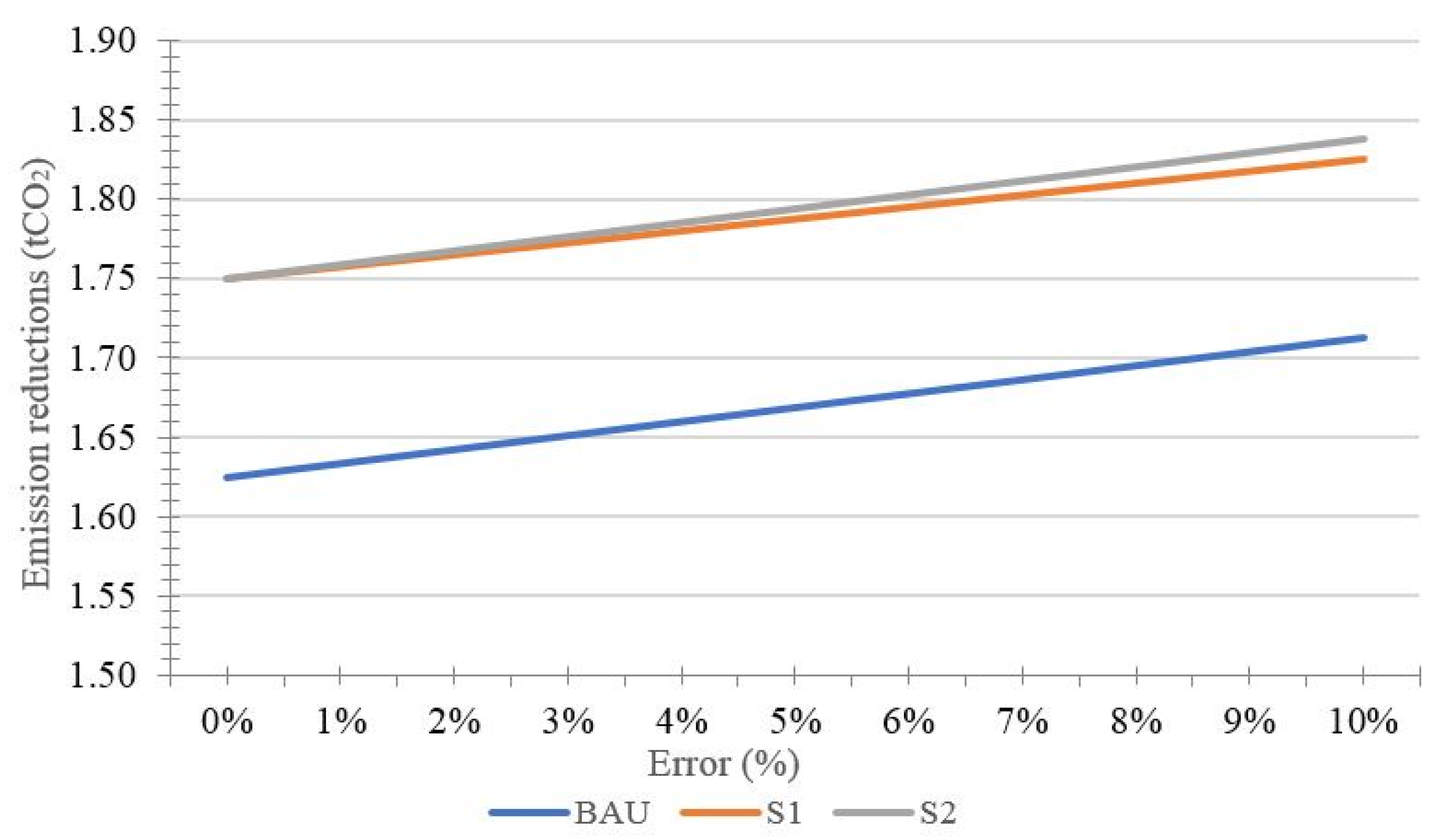

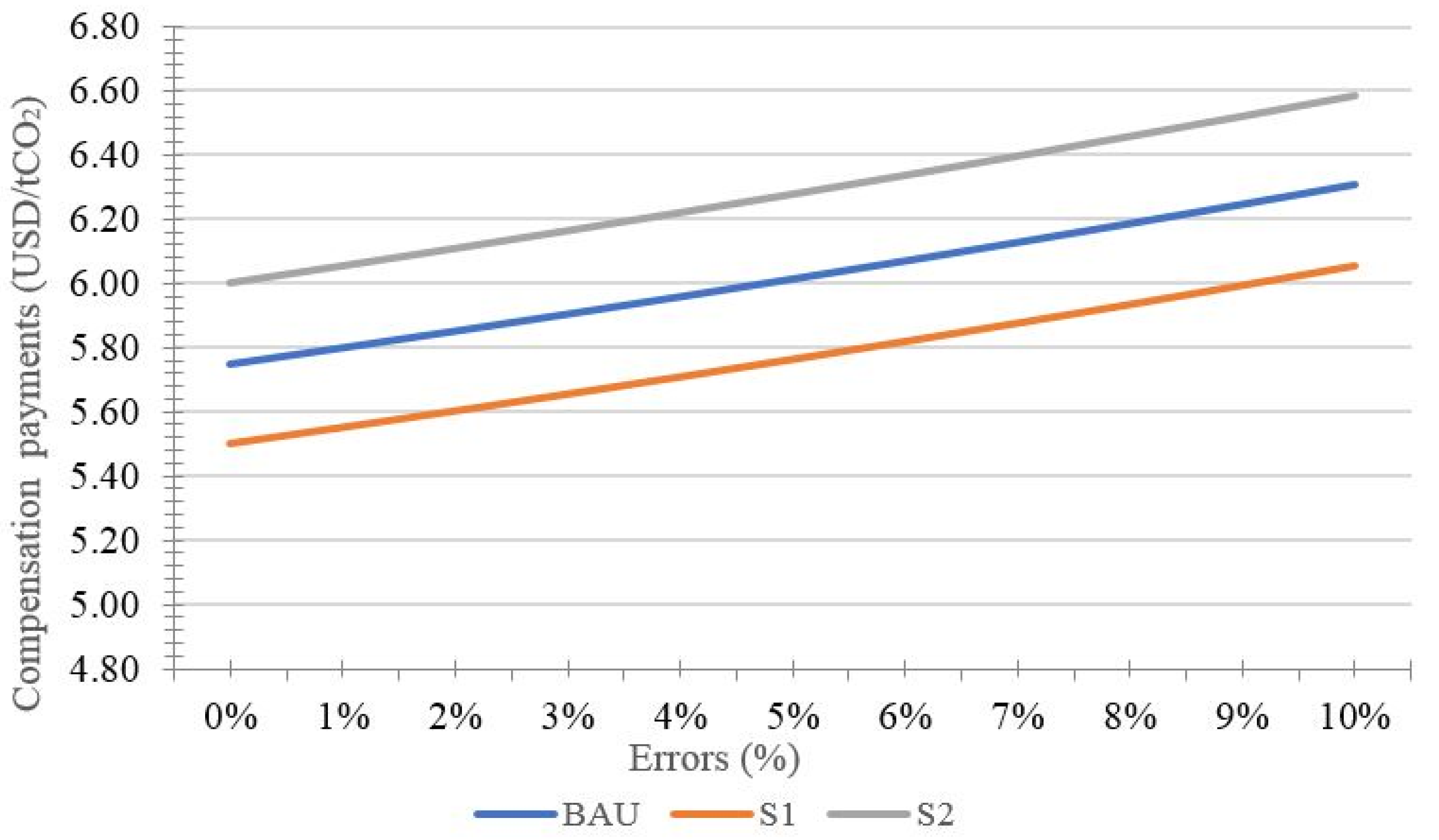

5.1. The Scenarios with Endogenous Errors

5.2. Scenario Comparison

6. Conclusions

- When the incentive is constant, the emission reductions and compensation payments as endogenous variables will increase as errors increase. Eventually, the profits of various stakeholders will also simultaneously increase.

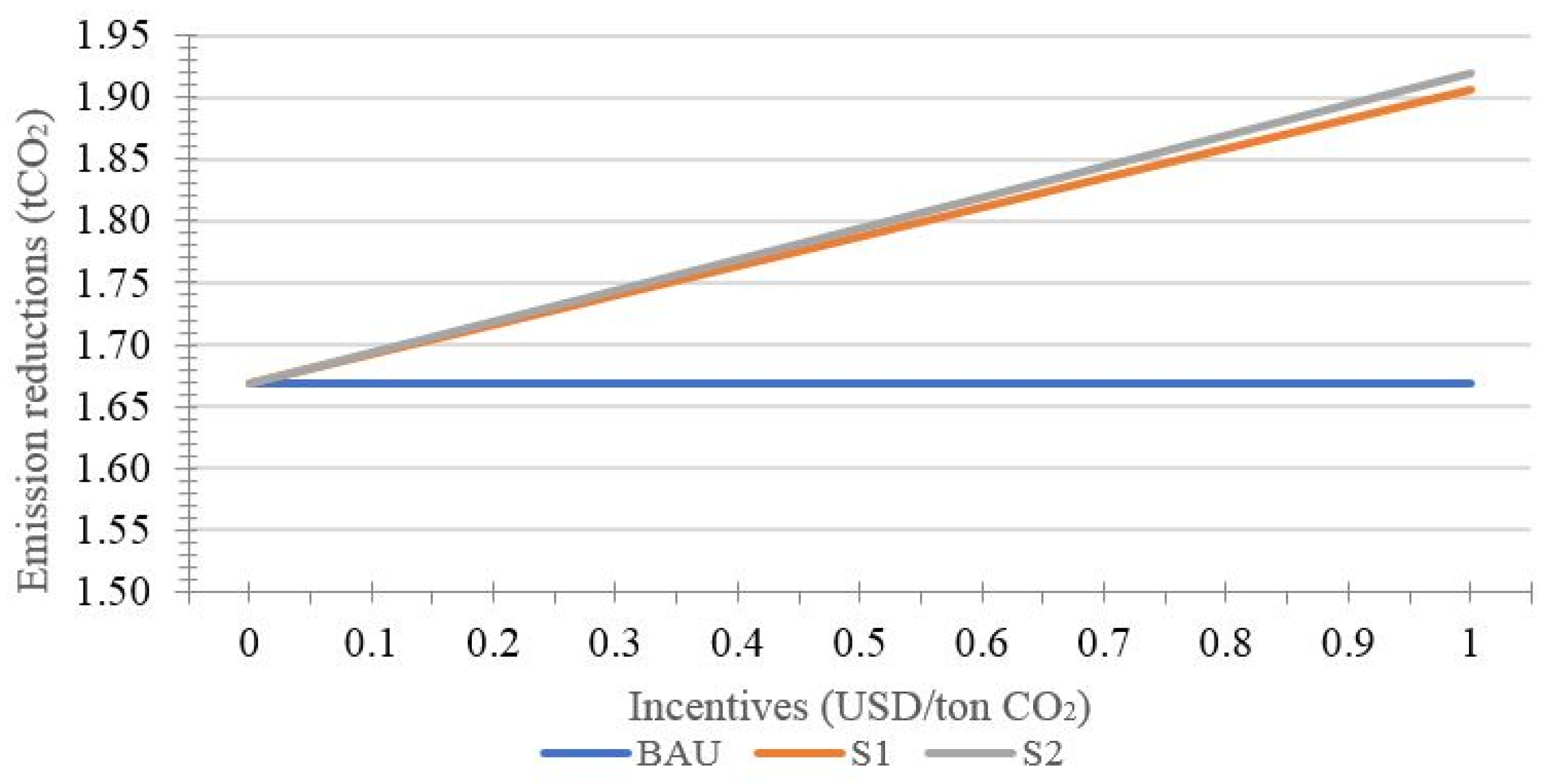

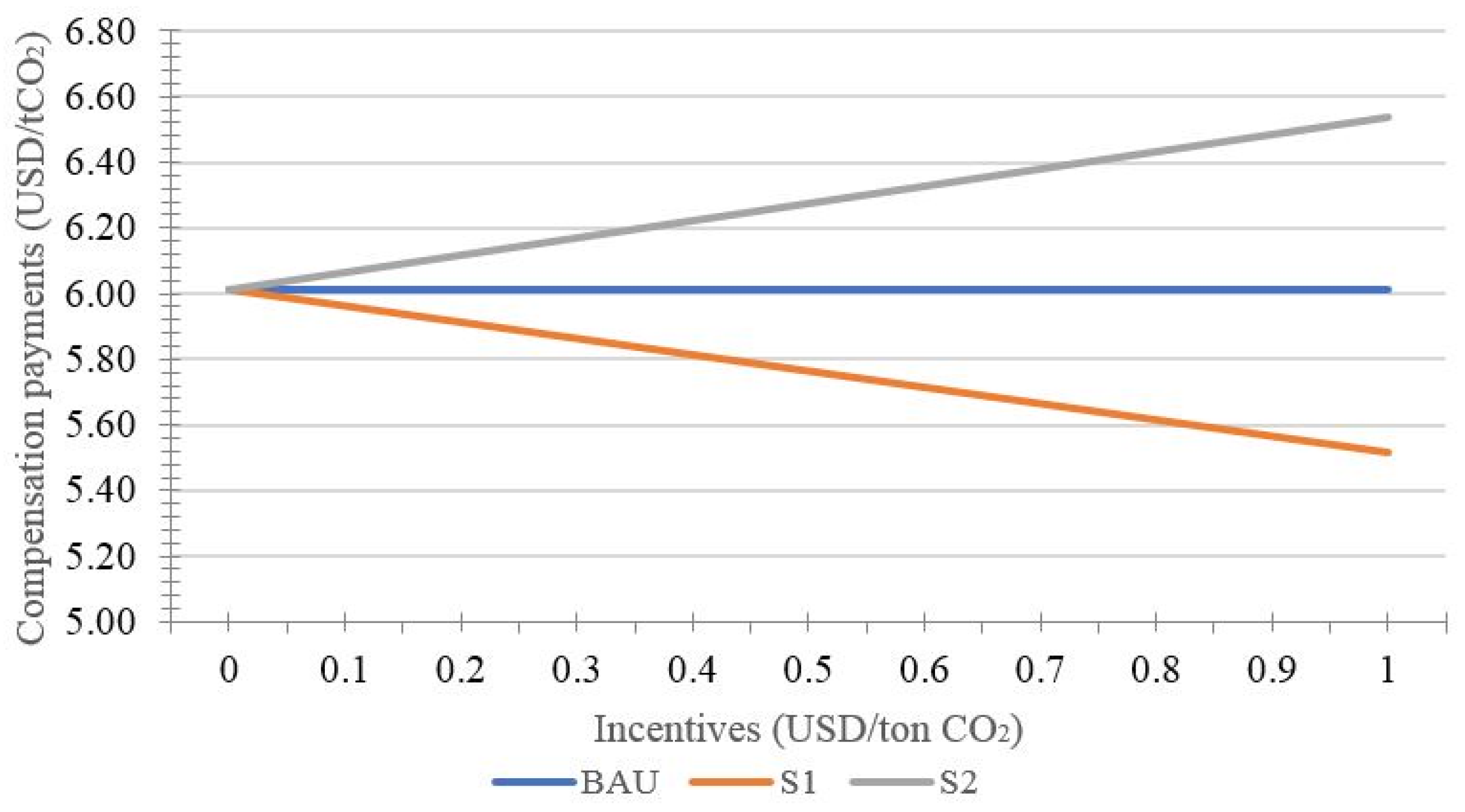

- When errors are unchanged, the emission reductions and stakeholder profits will increase with rising incentive. Meanwhile, the effects of incentive for investors will be better than those for landholders, and the difference is more significant with increased incentive and errors.

- When the emission reductions and errors are endogenous variables, the monitoring error is inversely proportional to the market size, and proportional to the compensation payment and transaction cost. Also, the equilibrium emission reductions are related only to market size.

- The incentive for landholders cannot improve the performance of REDD+ projects, but only increase landholder profits. However, the incentive for investors can reduce error, increase emission reductions, and improve the welfare of all stakeholders.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Bonan, G.B. Forests and climate change: Forcings, feedbacks, and the climate benefits of forests. Science 2008, 320, 1444–1449. [Google Scholar] [CrossRef] [PubMed]

- FAO. Global Forest Resources Assessment 2010; Food and Agriculture Organization of the United Nations Roma: Roma, Italy, 2010. [Google Scholar]

- Sala, O.E.; Chapin, F.S., 3rd; Armesto, J.J.; Berlow, E.; Bloomfield, J.; Dirzo, R.; Huber-Sanwald, E.; Huenneke, L.F.; Jackson, R.B.; Kinzig, A.; et al. Global biodiversity scenarios for the year 2100. Science 2000, 287, 1770–1774. [Google Scholar] [CrossRef] [PubMed]

- UNFCCC. Report of the Conference of the Parties, on Its Thirteenth Session, Held in Bali from 3 to 15 December 2007; UNFCCC: Geneva, Switzerland, 2008. [Google Scholar]

- UNFCCC. Report of the Conference of the Parties on Its Twenty-First Session, Held in Paris from 30 November to 11 December 2015; UNFCCC: Geneva, Switzerland, 2016. [Google Scholar]

- Plugge, D.; Baldauf, T.; Köhl, M. The global climate change mitigation strategy redd: Monitoring costs and uncertainties jeopardize economic benefits. Clim. Chang. 2013, 119, 247–259. [Google Scholar] [CrossRef]

- Lusiana, B.; van Noordwijk, M.; Johana, F.; Galudra, G.; Suyanto, S.; Cadisch, G. Implications of uncertainty and scale in carbon emission estimates on locally appropriate designs to reduce emissions from deforestation and degradation (REDD+). Mitig. Adapt. Strateg. Glob. Chang. 2014, 19, 757–772. [Google Scholar] [CrossRef]

- Skutsch, M.; Vickers, B.; Georgiadou, Y.; McCall, M. Alternative models for carbon payments to communities under REDD+: A comparison using the polis model of actor inducements. Environ. Sci. Policy 2011, 14, 140–151. [Google Scholar] [CrossRef]

- Walker, W.; Baccini, A.; Schwartzman, S.; Ríos, S.; Oliveira-Miranda, M.A.; Augusto, C.; Ruiz, M.R.; Arrasco, C.S.; Ricardo, B.; Smith, R. Forest carbon in amazonia: The unrecognized contribution of indigenous territories and protected natural areas. Carbon Manag. 2014, 5, 479–485. [Google Scholar] [CrossRef]

- Chhatre, A.; Lakhanpal, S.; Larson, A.M.; Nelson, F.; Ojha, H.; Rao, J. Social safeguards and co-benefits in REDD+: A review of the adjacent possible. Curr. Opin. Environ. Sustain. 2012, 4, 654–660. [Google Scholar] [CrossRef]

- Grassi, G.; Monni, S.; Federici, S.; Achard, F.; Mollicone, D. Applying the conservativeness principle to REDD to deal with the uncertainties of the estimates. Environ. Res. Lett. 2008, 3, 035005. [Google Scholar] [CrossRef] [Green Version]

- Fearnside, P.M. Saving tropical forests as a global warming countermeasure: An issue that divides the environmental movement. Ecol. Econ. 2001, 39, 167–184. [Google Scholar] [CrossRef]

- Persson, U.M.; Azar, C. Tropical deforestation in a future international climate policy regime—Lessons from the brazilian amazon. Mitig. Adapt. Strateg. Glob. Chang. 2007, 12, 1277–1304. [Google Scholar] [CrossRef]

- Grassi, G.; Federici, S.; Achard, F. Implementing conservativeness in REDD+ is realistic and useful to address the most uncertain estimates. Clim. Chang. 2013, 119, 269–275. [Google Scholar] [CrossRef] [Green Version]

- Achard, F.; DeFries, R.; Eva, H.; Hansen, M.; Mayaux, P.; Stibig, H. Pan-tropical monitoring of deforestation. Environ. Res. Lett. 2007, 2, 045022. [Google Scholar] [CrossRef] [Green Version]

- Grainger, A.; Obersteiner, M. A framework for structuring the global forest monitoring landscape in the redd plus era. Environ. Sci. Policy 2011, 14, 127–139. [Google Scholar] [CrossRef]

- DeFries, R.S.; Houghton, R.A.; Hansen, M.C.; Field, C.B.; Skole, D.; Townshend, J. Carbon emissions from tropical deforestation and regrowth based on satellite observations for the 1980s and 1990s. Proc. Natl. Acad. Sci. USA 2002, 99, 14256–14261. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Gibbs, H.K.; Brown, S.; Niles, J.O.; Foley, J.A. Monitoring and estimating tropical forest carbon stocks: Making redd a reality. Environ. Res. Lett. 2007, 2, 045023. [Google Scholar] [CrossRef]

- Houghton, R. Aboveground forest biomass and the global carbon balance. Glob. Chang. Biol. 2005, 11, 945–958. [Google Scholar] [CrossRef]

- Pelletier, J.; Kirby, K.R.; Potvin, C. Significance of carbon stock uncertainties on emission reductions from deforestation and forest degradation in developing countries. For. Policy Econ. 2012, 24, 3–11. [Google Scholar] [CrossRef]

- Earles, J.M.; Yeh, S.; Skog, K.E. Timing of carbon emissions from global forest clearance. Nat. Clim. Chang. 2012, 2, 682. [Google Scholar] [CrossRef]

- Pelletier, J.; Martin, D.; Potvin, C. REDD+ emissions estimation and reporting: Dealing with uncertainty. Environ. Res. Lett. 2013, 8, 034009. [Google Scholar] [CrossRef]

- Houghton, R.A. How well do we know the flux of CO2 from land-use change? Tellus B Chem. Phys. Meteorol. 2010, 62, 337–351. [Google Scholar] [CrossRef]

- Ramankutty, N.; Gibbs, H.K.; Achard, F.; Defries, R.; Foley, J.A.; Houghton, R. Challenges to estimating carbon emissions from tropical deforestation. Glob. Chang. Biol. 2007, 13, 51–66. [Google Scholar] [CrossRef]

- Pelletier, J.; Busch, J.; Potvin, C. Addressing uncertainty upstream or downstream of accounting for emissions reductions from deforestation and forest degradation. Clim. Chang. 2015, 130, 635–648. [Google Scholar] [CrossRef]

- Gregersen, H.; El Lakany, H.; Karsenty, A.; White, A. Does the Opportunity Cost Approach Indicate the Real Cost of REDD+? Rights and Realities of Paying for REDD+; Rights and Resources Initiative, CIRAD: Washington, DC, UAS, 2010. [Google Scholar]

- Karky, B.S.; Skutsch, M. The cost of carbon abatement through community forest management in Nepal Himalaya. Ecol. Econ. 2010, 69, 666–672. [Google Scholar] [CrossRef]

- Ghazoul, J.; Butler, R.A.; Mateo-Vega, J.; Koh, L.P. Redd: A reckoning of environment and development implications. Trends Ecol. Evol. 2010, 25, 396–402. [Google Scholar] [CrossRef] [PubMed]

- Groom, B.; Palmer, C. Cost-effective provision of environmental services: The role of relaxing market constraints. Environ. Dev. Econ. 2010, 15, 219–240. [Google Scholar] [CrossRef]

- Borrego, A.; Skutsch, M. Estimating the opportunity costs of activities that cause degradation in tropical dry forest: Implications for redd. Ecol. Econ. 2014, 101, 1–9. [Google Scholar] [CrossRef]

- Sheng, J.; Cao, J.; Han, X.; Miao, Z. Incentive modes and reducing emissions from deforestation and degradation: Who can benefit most? J. Clean. Prod. 2016, 129, 395–409. [Google Scholar] [CrossRef]

- Mahanty, S.; Suich, H.; Tacconi, L. Access and benefits in payments for environmental services and implications for REDD+: Lessons from seven pes schemes. Land Use Policy 2013, 31, 38–47. [Google Scholar] [CrossRef]

- Phelps, J.; Guerrero, M.C.; Dalabajan, D.A.; Young, B.; Webb, E.L. What makes a ‘REDD’ country? Glob. Environ. Chang. 2010, 20, 322–332. [Google Scholar] [CrossRef]

- Cronkleton, P.; Bray, D.B.; Medina, G. Community forest management and the emergence of multi-scale governance institutions: Lessons for redd plus development from Mexico, Brazil and Bolivia. Forests 2011, 2, 451–473. [Google Scholar] [CrossRef]

- Irawan, S.; Tacconi, L.; Ring, I. Stakeholders’ incentives for land-use change and REDD plus: The case of indonesia. Ecol. Econ. 2013, 87, 75–83. [Google Scholar] [CrossRef]

- Pelletier, J.; Ramankutty, N.; Potvin, C. Diagnosing the uncertainty and detectability of emission reductions for REDD+ under current capabilities: An example for panama. Environ. Res. Lett. 2011, 6, 024005. [Google Scholar] [CrossRef]

- Plugge, D.; Köhl, M. Estimating carbon emissions from forest degradation: Implications of uncertainties and area sizes for a REDD+ MRV system. Can. J. For. Res. 2012, 42, 1996–2010. [Google Scholar] [CrossRef]

- Canadell, J.G.; Ciais, P.; Dhakal, S.; Dolman, H.; Friedlingstein, P.; Gurney, K.R.; Held, A.; Jackson, R.B.; Le Quere, C.; Malone, E.L.; et al. Interactions of the carbon cycle, human activity, and the climate system: A research portfolio. Curr. Opin. Environ. Sustain. 2010, 2, 301–311. [Google Scholar] [CrossRef]

- Irawan, S.; Tacconi, L.; Ring, I. Designing intergovernmental fiscal transfers for conservation: The case of REDD+ revenue distribution to local governments in indonesia. Land Use Policy 2014, 36, 47–59. [Google Scholar] [CrossRef]

- Fischer, R.; Hargita, Y.; Günter, S. Insights from the ground level? A content analysis review of multi-national REDD+ studies since 2010. For. Policy Econ. 2016, 66, 47–58. [Google Scholar] [CrossRef]

- Dixon, R.; Challies, E. Making REDD+ pay: Shifting rationales and tactics of private finance and the governance of avoided deforestation in indonesia. Asia Pac. Viewp. 2015, 56, 6–20. [Google Scholar] [CrossRef]

- Well, M.; Carrapatoso, A. Redd+ finance: Policy making in the context of fragmented institutions. Clim. Policy 2016, 17, 687–707. [Google Scholar] [CrossRef]

- McFarland, B.J. International finance for redd plus within the context of conservation financing instruments. J. Sustain. For. 2015, 34, 534–546. [Google Scholar] [CrossRef]

- Minang, P.A.; Van Noordwijk, M.; Duguma, L.A.; Alemagi, D.; Do, T.H.; Bernard, F.; Agung, P.; Robiglio, V.; Catacutan, D.; Suyanto, S. REDD+ readiness progress across countries: Time for reconsideration. Clim. Policy 2014, 14, 685–708. [Google Scholar] [CrossRef]

- Korhonen-Kurki, K.; Sehring, J.; Brockhaus, M.; Di Gregorio, M. Enabling factors for establishing REDD+ in a context of weak governance. Clim. Policy 2014, 14, 167–186. [Google Scholar] [CrossRef]

- Rosendal, G.K.; Andresen, S. Institutional design for improved forest governance through REDD: Lessons from the global environment facility. Ecol. Econ. 2011, 70, 1908–1915. [Google Scholar] [CrossRef]

- Joseph, S.; Herold, M.; Sunderlin, W.D.; Verchot, L.V. Redd plus readiness: Early insights on monitoring, reporting and verification systems of project developers. Environ. Res. Lett. 2013, 8, 034038. [Google Scholar] [CrossRef]

- Romijn, E.; Herold, M.; Kooistra, L.; Murdiyarso, D.; Verchot, L. Assessing capacities of non-annex i countries for national forest monitoring in the context of REDD+. Environ. Sci. Policy 2012, 19–20, 33–48. [Google Scholar] [CrossRef]

- Sharma, S.K.; Deml, K.; Dangal, S.; Rana, E.; Madigan, S. REDD+ framework with integrated measurement, reporting and verification system for community based forest management systems (CBFMS) in Nepal. Curr. Opin. Environ. Sustain. 2015, 14, 17–27. [Google Scholar] [CrossRef]

- Salvini, G.; Herold, M.; De Sy, V.; Kissinger, G.; Brockhaus, M.; Skutsch, M. How countries link REDD+ interventions to drivers in their readiness plans: Implications for monitoring systems. Environ. Res. Lett. 2014, 9, 074004. [Google Scholar] [CrossRef]

- Giessen, L.; Buttoud, G. Defining and assessing forest governance. For. Policy Econ. 2014, 49, 1–3. [Google Scholar] [CrossRef]

- Larson, A.M.; Brockhaus, M.; Sunderlin, W.D.; Duchelle, A.; Babon, A.; Dokken, T.; Pham, T.T.; Resosudarmo, I.; Selaya, G.; Awono, A. Land tenure and REDD+: The good, the bad and the ugly. Glob. Environ. Chang. 2013, 23, 678–689. [Google Scholar] [CrossRef]

- Duchelle, A.E.; Cromberg, M.; Gebara, M.F.; Guerra, R.; Melo, T.; Larson, A.; Cronkleton, P.; Börner, J.; Sills, E.; Wunder, S. Linking forest tenure reform, environmental compliance, and incentives: Lessons from REDD+ initiatives in the brazilian amazon. World Dev. 2014, 55, 53–67. [Google Scholar] [CrossRef]

- Lawlor, K.; Madeira, E.M.; Blockhus, J.; Ganz, D.J. Community participation and benefits in REDD+: A review of initial outcomes and lessons. Forests 2013, 4, 296–318. [Google Scholar] [CrossRef]

- Awono, A.; Somorin, O.A.; Atyi, R.E.; Levang, P. Tenure and participation in local redd plus projects: Insights from southern cameroon. Environ. Sci. Policy 2014, 35, 76–86. [Google Scholar] [CrossRef]

- Shrestha, S.; Shrestha, U.B. Beyond money: Does REDD+ payment enhance household’s participation in forest governance and management in Nepal’s community forests? For. Policy Econ. 2017, 80, 63–70. [Google Scholar] [CrossRef]

- Poudyal, M.; Ramamonjisoa, B.S.; Hockley, N.; Rakotonarivo, O.S.; Gibbons, J.M.; Mandimbiniaina, R.; Rasoamanana, A.; Jones, J.P. Can REDD+ social safeguards reach the ‘right’people? Lessons from madagascar. Glob. Environ. Chang. 2016, 37, 31–42. [Google Scholar] [CrossRef]

- Gebara, M.F. Importance of local participation in achieving equity in benefit-sharing mechanisms for REDD+: A case study from the juma sustainable development reserve. Int. J. Commons 2013, 7, 473–497. [Google Scholar] [CrossRef]

- Luttrell, C.; Loft, L.; Gebara, M.F.; Kweka, D.; Brockhaus, M.; Angelsen, A.; Sunderlin, W.D. Who should benefit from redd plus ? Rationales and realities. Ecol. Soc. 2013, 18, 52. [Google Scholar] [CrossRef]

- Thompson, I.D.; Okabe, K.; Parrotta, J.A.; Brockerhoff, E.; Jactel, H.; Forrester, D.I.; Taki, H. Biodiversity and ecosystem services: Lessons from nature to improve management of planted forests for redd-plus. Biodivers. Conserv. 2014, 23, 2613–2635. [Google Scholar] [CrossRef]

- Bustamante, M.M.; Roitman, I.; Aide, T.M.; Alencar, A.; Anderson, L.O.; Aragao, L.; Asner, G.P.; Barlow, J.; Berenguer, E.; Chambers, J.; et al. Toward an integrated monitoring framework to assess the effects of tropical forest degradation and recovery on carbon stocks and biodiversity. Glob. Chang. Biol. 2016, 22, 92–109. [Google Scholar] [CrossRef] [PubMed]

- Murray, J.P.; Grenyer, R.; Wunder, S.; Raes, N.; Jones, J.P. Spatial patterns of carbon, biodiversity, deforestation threat, and REDD+ projects in indonesia. Conserv. Biol. 2015, 29, 1434–1445. [Google Scholar] [CrossRef] [PubMed]

- Kothke, M.; Schroppel, B.; Elsasser, P. National redd plus reference levels deduced from the global deforestation curve. For. Policy Econ. 2014, 43, 18–28. [Google Scholar] [CrossRef]

- Sheng, J.; Miao, Z.; Ozturk, U.A. A methodology to estimate national REDD+ reference levels using the zero-sum-gains dea approach. Ecol. Indic. 2016, 67, 504–516. [Google Scholar] [CrossRef]

- Romijn, E.; Ainembabazi, J.H.; Wijaya, A.; Herold, M.; Angelsen, A.; Verchot, L.; Murdiyarso, D. Exploring different forest definitions and their impact on developing REDD+ reference emission levels: A case study for indonesia. Environ. Sci. Policy 2013, 33, 246–259. [Google Scholar] [CrossRef]

- Tegegne, Y.T.; Lindner, M.; Fobissie, K.; Kanninen, M. Evolution of drivers of deforestation and forest degradation in the congo basin forests: Exploring possible policy options to address forest loss. Land Use Policy 2016, 51, 312–324. [Google Scholar] [CrossRef]

- Weatherley-Singh, J.; Gupta, A. Drivers of deforestation and REDD+ benefit-sharing: A meta-analysis of the (missing) link. Environ. Sci. Policy 2015, 54, 97–105. [Google Scholar] [CrossRef]

- Wehkamp, J.; Aquino, A.; Fuss, S.; Reed, E.W. Analyzing the perception of deforestation drivers by african policy makers in light of possible REDD+ policy responses. For. Policy Econ. 2015, 59, 7–18. [Google Scholar] [CrossRef]

- Herold, M.; Skutsch, M. Monitoring, reporting and verification for national REDD plus programmes: Two proposals. Environ. Res. Lett. 2011, 6, 014002. [Google Scholar] [CrossRef]

- Joseph, S.; Murthy, M.S.R.; Thomas, A.P. The progress on remote sensing technology in identifying tropical forest degradation: A synthesis of the present knowledge and future perspectives. Environ. Earth Sci. 2011, 64, 731–741. [Google Scholar] [CrossRef]

- Goetz, S.; Dubayah, R. Advances in remote sensing technology and implications for measuring and monitoring forest carbon stocks and change. Carbon Manag. 2011, 2, 231–244. [Google Scholar] [CrossRef] [Green Version]

- De Sy, V.; Herold, M.; Achard, F.; Asner, G.P.; Held, A.; Kellndorfer, J.; Verbesselt, J. Synergies of multiple remote sensing data sources for REDD+ monitoring. Curr. Opin. Environ. Sustain. 2012, 4, 696–706. [Google Scholar] [CrossRef]

- Bottcher, H.; Eisbrenner, K.; Fritz, S.; Kindermann, G.; Kraxner, F.; McCallum, I.; Obersteiner, M. An assessment of monitoring requirements and costs of ‘reduced emissions from deforestation and degradation’. Carbon Balance Manag. 2009, 4, 7. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Pratihast, A.K.; Herold, M.; De Sy, V.; Murdiyarso, D.; Skutsch, M. Linking community-based and national REDD+ monitoring: A review of the potential. Carbon Manag. 2013, 4, 91–104. [Google Scholar] [CrossRef]

- Sunderlin, W.D.; Ekaputri, A.D.; Sills, E.O.; Duchelle, A.E.; Kweka, D.; Diprose, R.; Doggart, N.; Ball, S.; Lima, R.; Enright, A. The Challenge of Establishing REDD+ on the Ground: Insights from 23 Subnational Initiatives in Six Countries; CIFOR: Bogor, Indonesia, 2014; Volume 104. [Google Scholar]

- Bucki, M.; Cuypers, D.; Mayaux, P.; Achard, F.; Estreguil, C.; Grassi, G. Assessing redd plus performance of countries with low monitoring capacities: The matrix approach. Environ. Res. Lett. 2012, 7, 014031. [Google Scholar] [CrossRef]

- Busch, J.; Strassburg, B.; Cattaneo, A.; Lubowski, R.; Bruner, A.; Rice, R.; Creed, A.; Ashton, R.; Boltz, F. Comparing climate and cost impacts of reference levels for reducing emissions from deforestation. Environ. Res. Lett. 2009, 4, 044006. [Google Scholar] [CrossRef] [Green Version]

- Kabiri, N. Public participation, land use and climate change governance in thailand. Land Use Policy 2016, 52, 511–517. [Google Scholar] [CrossRef]

- Petherick, A. Refreshing redd. Nat. Clim. Chang. 2011, 1, 440–441. [Google Scholar] [CrossRef]

- Barron, D.; McDermott, C. Private funder perspectives on local social and environmental impacts in ‘reducing emissions from deforestation and degradation+’. J. Environ. Policy Plan. 2015, 17, 277–293. [Google Scholar] [CrossRef]

- Kossoy, A.; Guigon, P. State and Trends of the Carbon Market 2012; World Bank: Washington, DC, USA, 2010. [Google Scholar]

- Jeong, H. The EU’s REDD+ policy developments and the lessons from the policy implementation in west papua and papua, indonesia. Asian J. Soc. Sci. Stud. 2018, 3, 41. [Google Scholar] [CrossRef]

- World Bank; Ecofys. Carbon Pricing Watch 2017; World Bank: Washington, DC, USA, 2017. [Google Scholar]

- McGregor, A.; Challies, E.; Howson, P.; Astuti, R.; Dixon, R.; Haalboom, B.; Gavin, M.; Tacconi, L.; Afiff, S. Beyond carbon, more than forest? REDD+ governmentality in indonesia. Environ. Plan. A 2015, 47, 138–155. [Google Scholar] [CrossRef]

- Pandey, S.S.; Cockfield, G.; Maraseni, T.N. Assessing the roles of community forestry in climate change mitigation and adaptation: A case study from Nepal. For. Ecol. Manag. 2016, 360, 400–407. [Google Scholar] [CrossRef]

- McDermott, C.L.; Coad, L.; Helfgott, A.; Schroeder, H. Operationalizing social safeguards in REDD+: Actors, interests and ideas. Environ. Sci. Policy 2012, 21, 63–72. [Google Scholar] [CrossRef]

- Krause, T.; Collen, W.; Nicholas, K.A. Evaluating safeguards in a conservation incentive program: participation, consent, and benefit sharing in indigenous communities of the ecuadorian amazon. Ecol. Soc. 2013, 18. [Google Scholar] [CrossRef]

- Corbera, E.; Martin, A.; Springate-Baginski, O.; Villaseñor, A. Sowing the seeds of sustainable rural livelihoods? An assessment of participatory forest management through REDD+ in tanzania. Land Use Policy 2017, in press. [Google Scholar] [CrossRef]

- Savaresi, A. REDD+ and human rights: Addressing synergies between international regimes. Ecol. Soc. 2013, 18. [Google Scholar] [CrossRef]

- Wright, G. Indigenous people and customary land ownership under domestic REDD+ frameworks: A case study of indonesia. Law Environ. Dev. J. 2011, 7, 117. [Google Scholar]

- Muradian, R.; Arsel, M.; Pellegrini, L.; Adaman, F.; Aguilar, B.; Agarwal, B.; Corbera, E.; Ezzine de Blas, D.; Farley, J.; Froger, G. Payments for ecosystem services and the fatal attraction of win-win solutions. Conserv. Lett. 2013, 6, 274–279. [Google Scholar] [CrossRef] [Green Version]

- Pascual, U.; Phelps, J.; Garmendia, E.; Brown, K.; Corbera, E.; Martin, A.; Gomez-Baggethun, E.; Muradian, R. Social equity matters in payments for ecosystem services. Bioscience 2014, 64, 1027–1036. [Google Scholar] [CrossRef]

- Van Hecken, G.; Bastiaensen, J.; Huybrechs, F. What’s in a name? Epistemic perspectives and payments for ecosystem services policies in nicaragua. Geoforum 2015, 63, 55–66. [Google Scholar] [CrossRef]

- Fletcher, R.; Buscher, B. The pes conceit: Revisiting the relationship between payments for environmental services and neoliberal conservation. Ecol. Econ. 2017, 132, 224–231. [Google Scholar] [CrossRef]

- Wunder, S. Payments for Environmental Services: Some Nuts and Bolts; Centre for International Forestry Research: Bogor, Indonesia, 2005. [Google Scholar]

- Merlet, P.; Van Hecken, G.; Rodriguez-Fabilena, R. Playing before paying? A pes simulation game for assessing power inequalities and motivations in the governance of ecosystem services. Ecosyst. Serv. 2018, in press. [Google Scholar] [CrossRef]

- Purnomo, H.; Suyamto, D.; Irawati, R.H. Harnessing the climate commons: An agent-based modelling approach to making reducing emission from deforestation and degradation (REDD)+ work. Mitig. Adapt. Strateg. Glob. Chang. 2013, 18, 471–489. [Google Scholar] [CrossRef]

- Fosci, M. The economic case for prioritizing governance over financial incentives in REDD+. Clim. Policy 2013, 13, 170–190. [Google Scholar] [CrossRef] [Green Version]

- Fletcher, R.; Breitling, J. Market mechanism or subsidy in disguise? Governing payment for environmental services in costa rica. Geoforum 2012, 43, 402–411. [Google Scholar] [CrossRef]

- Isenhour, C. Trading fat for forests: On palm oil, tropical forest conservation, and rational consumption. Conserv. Soc. 2014, 12, 257. [Google Scholar] [CrossRef]

- Boer, H.J. The role of government in operationalising markets for REDD+ in indonesia. For. Policy Econ. 2018, 86, 4–12. [Google Scholar] [CrossRef]

- Henkel, M. Mainstreaming payments for ecosystem services in the global water discourse. Environ. Policy Gov. 2017, 27, 14–27. [Google Scholar] [CrossRef]

- Busch, J.; Lubowski, R.N.; Godoy, F.; Steininger, M.; Yusuf, A.A.; Austin, K.; Hewson, J.; Juhn, D.; Farid, M.; Boltz, F. Structuring economic incentives to reduce emissions from deforestation within indonesia. Proc. Natl. Acad. Sci. USA 2012, 109, 1062–1067. [Google Scholar] [CrossRef] [PubMed]

- Boer, H. Welfare environmentality and REDD+ incentives in Indonesia. J. Environ. Policy Plan. 2017, 19, 795–809. [Google Scholar] [CrossRef]

- Palmer, C. Property rights and liability for deforestation under REDD+: Implications for ‘permanence’ in policy design. Ecol. Econ. 2011, 70, 571–576. [Google Scholar] [CrossRef]

- Loaiza, T.; Nehren, U.; Gerold, G. REDD+ and incentives: An analysis of income generation in forest-dependent communities of the yasuní biosphere reserve, ecuador. Appl. Geogr. 2015, 62, 225–236. [Google Scholar] [CrossRef]

- Salas, P.C.; Roe, B.E.; Sohngen, B. Additionality when redd contracts must be self-enforcing. Environ. Resour. Econ. 2016, 69, 195–215. [Google Scholar] [CrossRef]

- Sheng, J.; Qiu, H. Governmentality within REDD+: Optimizing incentives and efforts to reduce emissions from deforestation and degradation. Land Use Policy 2018, 76, 611–622. [Google Scholar] [CrossRef]

- Guadalupe, V.; Sotta, E.D.; Santos, V.F.; Gonçalves Aguiar, L.J.; Vieira, M.; de Oliveira, C.P.; Nascimento Siqueira, J.V. REDD+ implementation in a high forest low deforestation area: Constraints on monitoring forest carbon emissions. Land Use Policy 2018, 76, 414–421. [Google Scholar] [CrossRef]

- Pandit, R. REDD+ adoption and factors affecting respondents’ knowledge of REDD+ goal: Evidence from household survey of forest users from REDD+ piloting sites in Nepal. For. Policy Econ. 2018, 91, 107–115. [Google Scholar] [CrossRef]

- Albers, H.J.; Lee, K.D.; Robinson, E.J.Z. Economics of reducing emissions from deforestation and forest degradation: Incentives to change forest use behavior. In Encyclopedia of the Anthropocene; Dellasala, D.A., Goldstein, M.I., Eds.; Elsevier: Oxford, UK, 2018; pp. 61–65. [Google Scholar]

- Dean, M. Governmentality: Power and Rule in Modern Society; Sage Publications: London, UK, 2010. [Google Scholar]

- Nasi, R.; Putz, F.; Pacheco, P.; Wunder, S.; Anta, S. Sustainable forest management and carbon in tropical latin america: The case for REDD+. Forests 2011, 2, 200–217. [Google Scholar] [CrossRef]

- Sommerville, M.M.; Milner-Gulland, E.J.; Jones, J.P.G. The challenge of monitoring biodiversity in payment for environmental service interventions. Biol. Conserv. 2011, 144, 2832–2841. [Google Scholar] [CrossRef]

- Ferrer, G.; Swaminathan, J.M. Managing new and remanufactured products. Manag. Sci. 2006, 52, 15–26. [Google Scholar] [CrossRef] [Green Version]

- Tanabe, K.; Wagner, F. Good Practice Guidance for Land Use, Land-Use Change and Forestry; Institute for Global Environmental Strategies: Kanagawa, Japan, 2003; Available online: http://www.ipcc-nggip.iges.or.jp/public/gpglulucf/gpglulucf.htm (accessed on 23 March 2018).

- Kohl, M.; Baldauf, T.; Plugge, D.; Krug, J. Reduced emissions from deforestation and forest degradation (redd): A climate change mitigation strategy on a critical track. Carbon Balance Manag. 2009, 4, 10. [Google Scholar] [CrossRef] [PubMed]

- Boucher, D.H. Out of the Woods: A Realistic Role for Tropical Forests in Curbing Global Warming; Union of Concerned Scientists: Cambridge, MA, USA, 2008. [Google Scholar]

- Antinori, C.; Sathaye, J. Assessing Transaction Costs of Project-Based Greenhouse Gas Emissions Trading; Lawrence Berkeley National Laboratory: Berkeley, CA, USA, 2007. [Google Scholar]

- Nepstad, D.C.; Soares-Filho, B.; Merry, F.; Moutinho, P.; Rodrigues, H.O.; Bowman, M.; Schwartzman, S.; Almeida, O.; Rivero, S. The Costs and Benefits of Reducing Carbon Emissions from Deforestation and Forest Degradation in the Brazilian Amazon; Woods Hole Research Center: Falmouth, MA, USA, 2007. [Google Scholar]

- Delacote, P.; Palmer, C.; Bakkegaard, R.K.; Thorsen, B.J. Unveiling information on opportunity costs in REDD: Who obtains the surplus when policy objectives differ? Resour. Energy Econ. 2014, 36, 508–527. [Google Scholar] [CrossRef] [Green Version]

- Yu, X.; Yu, X.; Lu, Y. Evaluation of an agricultural meteorological disaster based on multiple criterion decision making and evolutionary algorithm. Int. J. Environ. Res. Public Health 2018, 15, 612. [Google Scholar] [CrossRef] [PubMed]

- Cheng, Z.; Li, L.; Liu, J.; Zhang, H. Total-factor carbon emission efficiency of china’s provincial industrial sector and its dynamic evolution. Renew. Sustain. Energy Rev. 2018, 94, 330–339. [Google Scholar] [CrossRef]

- Zhang, M.; Chen, Y.; Wu, X. Resident preferences for augmented rainstorm disasters management strategies: The case of nanjing in china. Environ. Hazards 2018, 1–15. [Google Scholar] [CrossRef]

- Wu, X.; Zhou, L.; Guo, J.; Liu, H. Impacts of typhoons on local labor markets based on gmm: An empirical study of guangdong province, china. Weather Clim. Soc. 2017, 9, 255–266. [Google Scholar] [CrossRef]

- FCPF. Emerging Questions on ER-PD Development—Improving Uncertainty of RLS. In Proceedings of the Carbon Fund Seventeenth Meeting (CF17), Paris, France, 29 January–1 February 2018; Forest Carbon Partnership Facility: Paris, France, 2018. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Stakeholders | Scenarios | Error (%) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1% | 2% | 3% | 4% | 5% | 6% | 7% | 8% | 9% | 10% | ||

| Investors | BAU | 2.64 | 2.67 | 2.70 | 2.73 | 2.76 | 2.78 | 2.81 | 2.84 | 2.87 | 2.90 | 2.93 |

| s1 | 3.06 | 3.09 | 3.12 | 3.14 | 3.17 | 3.20 | 3.22 | 3.25 | 3.28 | 3.30 | 3.33 | |

| s2 | 3.06 | 3.09 | 3.12 | 3.16 | 3.19 | 3.22 | 3.25 | 3.28 | 3.31 | 3.34 | 3.38 | |

| Landholders | BAU | 5.28 | 5.34 | 5.40 | 5.45 | 5.51 | 5.57 | 5.63 | 5.69 | 5.75 | 5.81 | 5.87 |

| s1 | 6.13 | 6.18 | 6.23 | 6.28 | 6.34 | 6.39 | 6.44 | 6.50 | 6.55 | 6.61 | 6.66 | |

| s2 | 6.13 | 6.19 | 6.25 | 6.31 | 6.37 | 6.44 | 6.50 | 6.56 | 6.62 | 6.69 | 6.75 | |

| Stakeholders | Scenarios | Incentive (USD/tCO2) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.00 | 0.10 | 0.20 | 0.30 | 0.40 | 0.50 | 0.60 | 0.70 | 0.80 | 0.90 | 1.00 | ||

| Investors | BAU | 2.78 | 2.78 | 2.78 | 2.78 | 2.78 | 2.78 | 2.78 | 2.78 | 2.78 | 2.78 | 2.78 |

| s1 | 2.78 | 2.86 | 2.95 | 3.03 | 3.11 | 3.20 | 3.28 | 3.37 | 3.45 | 3.54 | 3.63 | |

| s2 | 2.78 | 2.87 | 2.95 | 3.04 | 3.13 | 3.22 | 3.31 | 3.40 | 3.49 | 3.59 | 3.68 | |

| Landholders | BAU | 5.57 | 5.57 | 5.57 | 5.57 | 5.57 | 5.57 | 5.57 | 5.57 | 5.57 | 5.57 | 5.57 |

| s1 | 5.57 | 5.73 | 5.89 | 6.06 | 6.22 | 6.39 | 6.56 | 6.73 | 6.91 | 7.09 | 7.27 | |

| s2 | 5.57 | 5.74 | 5.91 | 6.08 | 6.26 | 6.44 | 6.62 | 6.80 | 6.98 | 7.17 | 7.36 | |

| Equilibrium Solution | Scenario without Incentive (BAU Scenario) | Incentive Scenarios | |

|---|---|---|---|

| Incentive for Landholders (s1 Scenario) | Incentive for Investors (s2 Scenario) | ||

| Monitoring error e | 1−m/[2(r + ct)] | 1−m/[2(r + ct)] | 1− (m + s2)/[2(r + ct)] |

| Emission reductions q | m/4 | m/4 | (m + s2)/4 |

| Players | Scenario without Incentive (BAU Scenario) | Incentive Scenarios | |

|---|---|---|---|

| Incentive for Landholders (s1 Scenario) | Incentive for Investors (s2 Scenario) | ||

| Investors | m2/16 | m2/16 | (m + s2)2/16 |

| Landholders | m2(r − co)/[8(r + ct)] | m2(r−co + s1)/[8(r + ct)] | (m + s2)2(r−co)/[8(r + ct)] |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sheng, J.; Zhou, W.; De Sherbinin, A. Uncertainty in Estimates, Incentives, and Emission Reductions in REDD+ Projects. Int. J. Environ. Res. Public Health 2018, 15, 1544. https://doi.org/10.3390/ijerph15071544

Sheng J, Zhou W, De Sherbinin A. Uncertainty in Estimates, Incentives, and Emission Reductions in REDD+ Projects. International Journal of Environmental Research and Public Health. 2018; 15(7):1544. https://doi.org/10.3390/ijerph15071544

Chicago/Turabian StyleSheng, Jichuan, Weihai Zhou, and Alex De Sherbinin. 2018. "Uncertainty in Estimates, Incentives, and Emission Reductions in REDD+ Projects" International Journal of Environmental Research and Public Health 15, no. 7: 1544. https://doi.org/10.3390/ijerph15071544

APA StyleSheng, J., Zhou, W., & De Sherbinin, A. (2018). Uncertainty in Estimates, Incentives, and Emission Reductions in REDD+ Projects. International Journal of Environmental Research and Public Health, 15(7), 1544. https://doi.org/10.3390/ijerph15071544