Post-Adversities Recovery and Profitability: The Case of Italian Farmers

Abstract

:1. Introduction

2. Literature Review

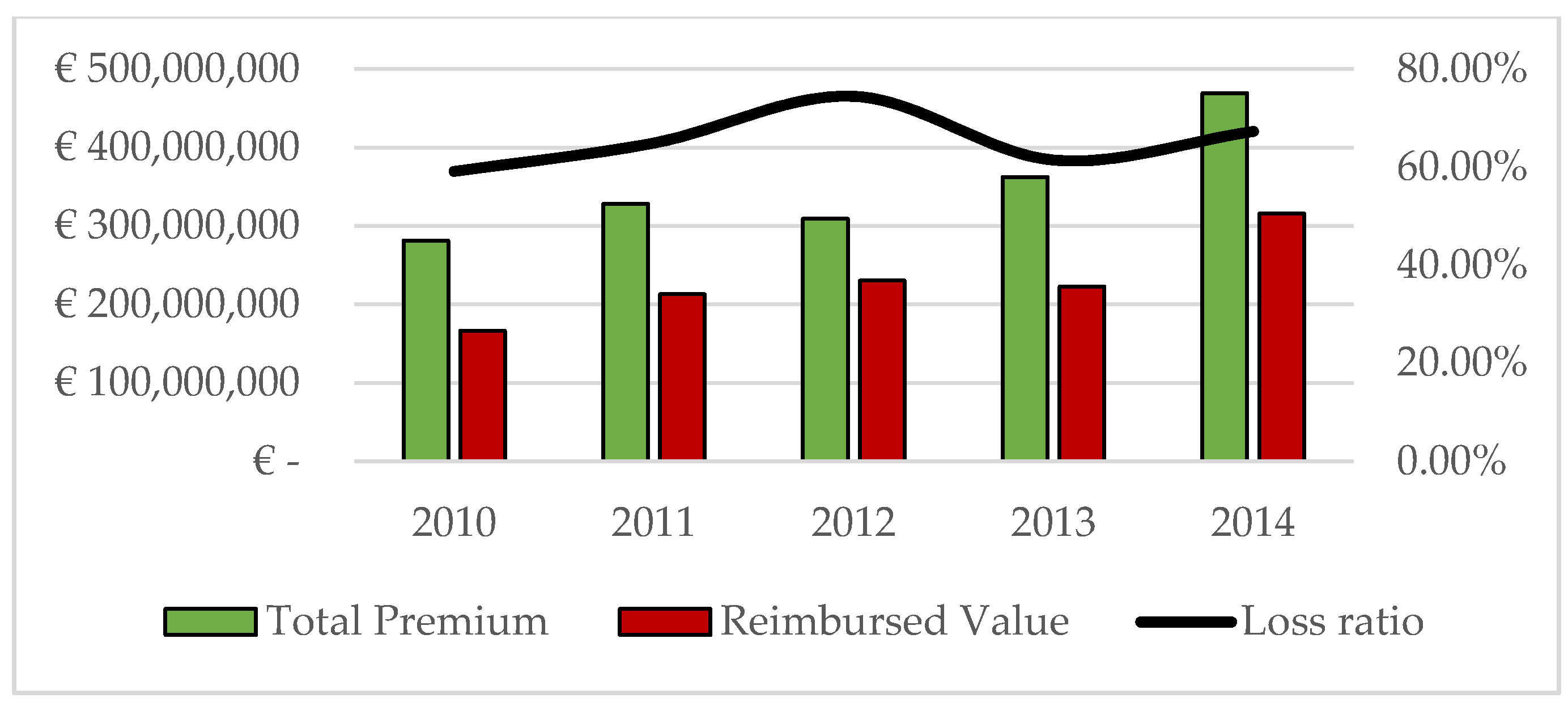

3. Background: The Italian Case

4. Materials and Methods

5. Results and Discussion

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Kunreuther, H.; Michel-Kerjan, E. Economics of Natural Catastrophe Risk Insurance. In Handbook of the Economics of Risk and Uncertainty; Elsevier, B.V.: North-Holland, The Netherlands, 2014. [Google Scholar]

- Smith, V.H.; Glauber, J.W. Agricultural Insurance in Developed Countries: Where Have We Been and Where Are We Going? Appl. Econo. Perspect. Policy 2012, 34, 363–390. [Google Scholar] [CrossRef]

- Raschky, P.A.; Weck-Hannemann, H. Charity hazard—A real hazard to natural disaster insurance? Environ. Hazards 2007, 7, 321–329. [Google Scholar] [CrossRef]

- Miglietta, P.P.; Toma, P.; Fusco, G.; Porrini, D. How to test charity hazard in agricultural insurance systems? In Proceedings of the Annual IAERE Conference (Italian Association of Environmental and Resource Economists), Udine, Italy, 7–8 February 2019. [Google Scholar]

- Santeramo, F.G. Imperfect information and participation in insurance markets: Evidence from Italy. Agric. Financ. Rev. 2018, 78, 183–194. [Google Scholar] [CrossRef]

- Van Asseldonk, M.; van der Meulen, H.; van der Meer, R.; Silvis, H.; Berkhout, P. Does subsidized MPCI crowds out traditional market-Based hail insurance in The Netherlands? Agric. Financ. Rev. 2018, 78, 262–274. [Google Scholar] [CrossRef]

- Url, T.; Sinabell, F.; Heinschink, K. Addressing basis risk in agricultural margin insurances: The case of wheat production in Austria. Agric. Financ. Rev. 2018, 78, 233–245. [Google Scholar] [CrossRef]

- Capitanio, F.; De Pin, A. Measures of Efficiency of Agricultural Insurance in Italy, Economic Evaluations. Risks 2018, 6, 126. [Google Scholar] [CrossRef]

- Zubor-Nemes, A.; Fogarasi, J.; Molnár, A.; Kemény, G. Farmers’ responses to the changes in Hungarian agricultural insurance system. Agric. Financ. Rev. 2018, 78, 275–288. [Google Scholar] [CrossRef]

- Hertel, T.W.; Rosch, S.D. Climate Change, Agriculture and Poverty; The World Bank: Washington DC, USA, 2010. [Google Scholar]

- Dinar, A.; Mendelsohn, R.O. Handbook on Climate Change and Agriculture; Dinar, A., Mendelsohn, R.O., Eds.; Edward Elgar Publishing: Cheltenham, UK, 2011. [Google Scholar]

- Mahul, O.; Stutley, C.J. Government Support to Agricultural Insurance; The World Bank: Washington, DC, USA, 2010. [Google Scholar]

- Morgan, S.L.; Marsden, T.; Morley, A. Agricultural multi-functionality and farmers entrepreneurial skills: A study of Tuscan and Welsh farmers. J. Rural Stud. 2010, 26, 116–129. [Google Scholar] [CrossRef]

- Mario, M.; Vedenov, D.V. Innovations in Agricultural and Natural Disaster Insurance. Am. J. Agric. Econ. 2001, 83, 650–655. [Google Scholar]

- Barnett, B.J.; Mahul, O. Weather index insurance for agriculture and rural areas in lower-Income countries. Am. J. Agric. Econ. 2007, 89, 1241–1247. [Google Scholar] [CrossRef]

- Morton, J.F. The impact of climate change on smallholder and subsistence agriculture. Proc. Natl. Acad. Sci. USA 2007, 104, 19680–19681. [Google Scholar] [CrossRef] [PubMed]

- Mutekwa, V.T. Climate change impacts and adaptation in the Agricultural sector: The case of smallholder farmers in Zimbabwe. J. Sustain. Dev. Afr. 2009, 11, 237–256. [Google Scholar]

- Obermaier, M.; Maroun, M.R.; Kligerman, D.C.; La Rovere, E.L.; Cesano, D.; Corral, T.; Hainc, B. Adaptation to climate change in Brazil: The Pintadas pilot project and multiplication of best practice examples through dissemination and communication networks. In Proceedings of the RIO 9-World Climate & Energy Event, Rio de Janeiro, Brazil, 17–19 March 2009. [Google Scholar]

- Butterworth, M.H.; Semenov, M.A.; Barnes, A.; Moran, D.; West, J.S.; Fitt, B.D. North–South divide: Contrasting impacts of climate change on crop yields in Scotland and England. J. R. Soc. Interface 2010, 7, 123–130. [Google Scholar] [CrossRef] [PubMed]

- Rowhani, P.; Lobell, D.B.; Linderman, M.; Ramankutty, N. Climate variability and crop production in Tanzania. Agric. For. Meteorol. 2011, 151, 449–460. [Google Scholar] [CrossRef]

- Boehlje, M.D.; Trede, L.D. Risk management in agriculture. J. ASFMRA 1977, 41, 20–29. [Google Scholar]

- Ramaswami, R.; Ravi, S.; Chopra, S. Risk management in agriculture. Discuss. Pap. 2008, 3–8, 1–131. [Google Scholar]

- Schaffnit-Chatterjee, C.; Schneider, S.; Peter, M.; Mayer, T. Risk Management in Agriculture. Towards Market Solutions in the EU; Deutsche Bank Reseach: Frankfurt am Mein, Germany, 2010. [Google Scholar]

- Glenk, K.; Fischer, A. Insurance, prevention or just wait and see? Public preferences for water management strategies in the context of climate change. Ecol. Econ. 2010, 69, 2279–2291. [Google Scholar] [CrossRef]

- Arbuckle, J.G.; Morton, L.W.; Hobbs, J. Farmer beliefs and concerns about climate change and attitudes toward adaptation and mitigation: Evidence from Iowa. Clim. Chang. 2013, 118, 551–563. [Google Scholar] [CrossRef] [Green Version]

- Schönhart, M.; Schauppenlehner, T.; Kuttner, M.; Kirchner, M.; Schmid, E. Climate change impacts on farm production, landscape appearance, and the environment: Policy scenario results from an integrated field-Farm-Landscape model in Austria. Agric. Syst. 2016, 145, 39–50. [Google Scholar] [CrossRef]

- Steidl, J.; Schuler, J.; Schubert, U.; Dietrich, O.; Zander, P. Expansion of an existing water management model for the analysis of opportunities and impacts of agricultural irrigation under climate change conditions. Water 2015, 7, 6351–6377. [Google Scholar] [CrossRef]

- Nunes, J.P.; Jacinto, R.; Keizer, J.J. Combined impacts of climate and socio-Economic scenarios on irrigation water availability for a dry Mediterranean reservoir. Sci. Total Environ. 2017, 584, 219–233. [Google Scholar] [CrossRef] [PubMed]

- Tangermann, S. Risk management in agriculture and the future of the EU’s Common Agricultural Policy. Int. Cent. Trade Sustain. Dev. 2011, 34, 1–39. [Google Scholar]

- Cortignani, R.; Dono, G. Agricultural policy and climate change: An integrated assessment of the impacts on an agricultural area of Southern Italy. Environ. Sci. Policy 2018, 81, 26–35. [Google Scholar] [CrossRef]

- Turvey, C.G. Weather derivatives for specific event risks in agriculture. Rev. Agric. Econ. 2001, 23, 333–351. [Google Scholar] [CrossRef]

- Skees, J.R.; Goes, A.; Sullivan, C.; Carpenter, R.; Miranda, M.J.; Barnett, B.J. Index insurance for weather risk in low income countries. In Report prepared for the USAID Microenterprise Development (MD) Office, USAID/DAI Prime Contract LAG-1-00-98-0026-00 BASIS Task Order, 8; Rural Finance Market Development: Washington DC, USA, 2006. [Google Scholar]

- Botzen, W.J.W.; van den Bergh, J.C.J.M.; Bouwer, L.M. Climate change and increased risk for the insurance sector: A global perspective and an assessment for the Netherlands. Nat. Hazards 2010, 52, 577–598. [Google Scholar] [CrossRef]

- Goodwin, B.K.; Smith, V.H. What harm is done by subsidizing crop insurance? Am. J. Agric. Econ. 2013, 95, 489–497. [Google Scholar] [CrossRef]

- Barnett, B. Multiple-Peril crop insurance: Successes and challenges. Agric. Financ. Rev. 2014, 74, 200–216. [Google Scholar] [CrossRef]

- Townsend, R.M. Risk and Insurance in Village India. Econometrica 1994, 62, 539–591. [Google Scholar] [CrossRef]

- Goodwin, B.K. Problems with Market Insurance in Agriculture. Am. J. Agric. Econ. 2001, 83, 643–649. [Google Scholar] [CrossRef]

- Gurenko, E.; Mahul, O. Enabling Productive but Asset-Poor Farmers to Succeed: A Risk Financing Framework; The World Bank: Washington, DC, USA, 2004. [Google Scholar]

- Vavrova, E. The Czech Agricultural Insurance Market and a Prediction of its Development in the Context of the European Union. Agric. Econ-Czech. 2005, 51, 531–538. [Google Scholar] [CrossRef]

- Wenner, M. Agricultural Insurance Revisited: New Development and Perspective in Latin America and the Caribbean; The World Bank: Washington, DC, USA, 2005. [Google Scholar]

- Fusco, G.; Miglietta, P.P.; Porrini, D. How Drought Affects Agricultural Insurance Policies: The Case of Italy. J. Sustain. Dev. 2018, 11, 1–11. [Google Scholar] [CrossRef]

- Lorant, A.; Farkas, M.F. Risk management in the agricultural sector with special attention to insurance. Pol. J. Manag. Stud. 2015, 11, 71–82. [Google Scholar]

- Kostyuchenko, T.N.; Sidorova, D.V.; Eremenko, N.V.; Chernikova, L.I. Insurance as a tool for managing risks in agriculture. Mediterr. J. Soc. Sci. 2015, 6, 220. [Google Scholar] [CrossRef]

- Rey, D.; Garrido, A.; Calatrava, J. Comparison of different water supply risk management tools for irrigators: Option contracts and insurance. Environ. Resour. Econ. 2016, 65, 415–439. [Google Scholar] [CrossRef]

- Müller, B.; Johnson, L.; Kreuer, D. Maladaptive outcomes of climate insurance in agriculture. Glob. Environ. Chang. 2017, 46, 23–33. [Google Scholar] [CrossRef]

- Meuwissen, M.P.M.; de Mey, Y.; Van Asseldonk, M. Prospects for agricultural insurance in Europe. Agric. Financ. Rev. 2018, 78, 174–182. [Google Scholar] [CrossRef]

- Mittenzwei, K.; Persson, T.; Höglind, M.; Kværnø, S. Combined effects of climate change and policy uncertainty on the agricultural sector in Norway. Agric. Syst. 2017, 153, 118–126. [Google Scholar] [CrossRef]

- Kirwan, B. The crowd-out effect of crop insurance on farm survival and profitability. Paper presented at the Agricultural & Applied Economics Associations 2014 AAEA Annual Meeting, Minneapolis, MN, USA, 27–29 July 2014. [Google Scholar]

- Pavlov, A.; Kindaev, A.; Vinnikova, I.; Kuznetsova, E. Crop insurance as a means of increasing efficiency of agricultural production in Russia. Int. J. Environ. Sci. Educ. 2016, 11, 11863–11868. [Google Scholar]

- Cafiero, C.; Capitanio, F.; Cioffi, A.; Coppola, A. Rischio, crisi e intervento pubblico nell’agricoltura europea. Polit. Agricola Intern. 2006, 4, 11–41. [Google Scholar]

- ISMEA. SicurAgro. Banca Dati sui Rischi in Agricoltura. Available online: http://www.ismea.it/flex/cm/pages/ServeBLOB.php/L/IT/IDPagina/4666 (accessed on 31 August 2019).

- FADN [Farm Accountancy Data Network]. FADN Public Database. Available online: https://ec.europa.eu/agriculture/rica/database/database_en.cfm (accessed on 31 August 2019).

- Kelly, E.; Latruffe, L.; Desjeux, Y.; Ryan, M.; Uthes, S.; Diazabakana, A.; Finn, J. Sustainability indicators for improved assessment of the effects of agricultural policy across the EU: Is FADN the answer? Ecol. Indic. 2018, 89, 903–911. [Google Scholar] [CrossRef] [Green Version]

- Tokunaga, S.; Okiyama, M.; Ikegawa, M. Dynamic panel data analysis of the impacts of climate change on agricultural production in Japan. Japan Agric. Res. Q. 2015, 49, 149–157. [Google Scholar] [CrossRef]

- Pappalardo, G.; Scienza, A.; Vindigni, G.; D’Amico, M. Profitability of wine grape growing in the EU member states. J. Wine Res. 2013, 24, 59–76. [Google Scholar] [CrossRef]

- Ovando, P.; Oviedo, J.L.; Campos, P. Measuring total social income of a stone pine afforestation in Huelva (Spain). Land Use Policy 2016, 50, 479–489. [Google Scholar] [CrossRef] [Green Version]

- Eidman, V.T. Quantifying and managing risk in agriculture. Agrekon 1990, 29, 11–23. [Google Scholar] [CrossRef]

- Danso-Abbeam, G.; Addai, K.N.; Ehiakpor, D. Willingness to pay for farm insurance by smallholder cocoa farmers in Ghana. J. Soc. Sci. Policy Implic. 2014, 2, 163–183. [Google Scholar]

- Carter, M.R.; Little, P.D.; Mogues, T.; Negatu, W. Poverty traps and natural disasters in Ethiopia and Honduras. World Dev. 2007, 35, 835–856. [Google Scholar] [CrossRef]

- Wąs, A.; Kobus, P. Factors differentiating the level of crop insurance at Polish farms. Agric. Financ. Rev. 2018, 78, 209–222. [Google Scholar] [CrossRef]

- Park, Y.; Hong, P.; Roh, J.J. Supply chain lessons from the catastrophic natural disaster in Japan. Bus. Horiz. 2013, 56, 75–85. [Google Scholar] [CrossRef]

- Born, P.; Viscusi, W.K. The catastrophic effects of natural disasters on insurance markets. J. Risk Uncertain. 2006, 33, 55–72. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| Source of Data | Code | Data Acquired | Time Period | Unit of Analysis |

|---|---|---|---|---|

| FADN [52] | SE275 | Total intermediate consumption (€) | From 2010 to 2014 | Italian Regions |

| SE420 | Gross Farm Income (€) | |||

| SE360 | Depreciation (€) | |||

| SE025 | Total cultivated surface (ha) | |||

| SE010 | Labor force (1000 annual working units) | |||

| SE135 | Agricultural production (€) | |||

| SE295 | Phytosanitary product (€) | |||

| SICURAGRO [51] | - | Reimbursed Value (1000 €) | ||

| ISTAT | - | Position |

| Variables | Mean | Standard Deviation | Minimum | Maximum |

|---|---|---|---|---|

| Total cultivated surface (ha) | 17.60 | 8.479 | 3.19 | 44.79 |

| Agricultural production (€) | 42,257.28 | 19,272.03 | 18,080.00 | 109,339.00 |

| Total intermediate consumption (€) | 26,808.65 | 17,876.46 | 6237.00 | 92,625.00 |

| Phytosanitary product (€) | 2408.14 | 1054.75 | 900.00 | 6720.00 |

| Labor force (1000 annual working units) | 1.38 | 0.34 | 1.01 | 2.95 |

| Reimbursed Value (1000 €) | 87,302.74 | 229,570.35 | 0.00 | 1,566,012.92 |

| Position | 0.63 | 0.485 | 0.00 | 1.00 |

| Gross Farm Income (€) | 39,009.26 | 17,137.16 | 18,286.00 | 106,522.00 |

| Depreciation (€) | 7300.22 | 3033.50 | 2829.00 | 14,326.00 |

| Variable | Reimbursed Value | Agr Surface | Phyto | Agr Prod | Labor Force | Gross Farmer Income | Total Intermediate Consumption | Depreciation | Position |

|---|---|---|---|---|---|---|---|---|---|

| Reimbursed value | 1 | 0.255 | 0.066 | 0.626 | 0.755 | 0.054 | 0.324 | 0.198 | 0.205 |

| Agr Surface | 1 | 0.191 | 0.250 | 0.237 | 0.210 | 0.184 | 0.133 | 0.159 | |

| Phyto | 1 | 0.504 | 0.113 | 0.792 | 0.747 | 0.480 | 0.429 | ||

| Agr prod | 1 | 0.807 | 0.601 | 0.742 | 0.543 | 0.568 | |||

| Labor force | 1 | 0.332 | 0.512 | 0.408 | 0.358 | ||||

| Gross Farmer Income | 1 | 0.889 | 0.547 | 0.467 | |||||

| Total intermediate consumption | 1 | 0.608 | 0.503 | ||||||

| Depreciation | 1 | 0.579 | |||||||

| Position | 1 |

| Ln Gross Farm Income | Ln Total Intermediate Consumption | Ln Depreciation | |

|---|---|---|---|

| Ln Reimbursed Value | −0.0339896 *** (0.0105740) | 0.0697444 *** (0.0116548) | 0.0266593 (0.0274813) |

| Ln Phyto | 0.155033 (0.14762) | 0.349052 ** (0.133130) | 0.148146 (0.210690) |

| Ln AgrProd | 0.664713 *** (0.163423) | 0.655473 *** (0.142480) | −0.0456099 (0.338077) |

| Ln Labor force | 0.0765265 (0.23467) | 0.339970 * (0.168154) | 0.587118 (0.377879) |

| Ln TotSurf | 0.339613 *** (2.00138) | 0.322562 *** (0.0781898) | 0.175566 (0.126330) |

| Position | 0.0606357 (0.0447147) | 0.106262 * (0.0581844) | 0.397054 *** 0.0803349) |

| Constant | 1.62297 * (0.803597) | −1.33879 * (0.737767) | 6.97767 *** (2.10362) |

| Summary Statistics | |||

| SER | 0.187119 | 0.21127 | 0.323536 |

| Adjusted R2 | 0.821 | 0.901 | 0.558 |

| N. observation | 95 | 95 | 95 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Porrini, D.; Fusco, G.; Miglietta, P.P. Post-Adversities Recovery and Profitability: The Case of Italian Farmers. Int. J. Environ. Res. Public Health 2019, 16, 3189. https://doi.org/10.3390/ijerph16173189

Porrini D, Fusco G, Miglietta PP. Post-Adversities Recovery and Profitability: The Case of Italian Farmers. International Journal of Environmental Research and Public Health. 2019; 16(17):3189. https://doi.org/10.3390/ijerph16173189

Chicago/Turabian StylePorrini, Donatella, Giulio Fusco, and Pier Paolo Miglietta. 2019. "Post-Adversities Recovery and Profitability: The Case of Italian Farmers" International Journal of Environmental Research and Public Health 16, no. 17: 3189. https://doi.org/10.3390/ijerph16173189

APA StylePorrini, D., Fusco, G., & Miglietta, P. P. (2019). Post-Adversities Recovery and Profitability: The Case of Italian Farmers. International Journal of Environmental Research and Public Health, 16(17), 3189. https://doi.org/10.3390/ijerph16173189