1. Introduction

After the climate conference in Copenhagen, carbon reduction policy has been considered a significant mechanism to reduce the greenhouse effect all over the world [

1]. There are many widely used carbon policies, such as carbon cap-and-trade systems, carbon emissions taxes and carbon emissions offset policies [

2]. Before 2008, many developed countries, such as the United Kingdom, Germany, Norway, and Finland, had adopted a carbon tax as their low-carbon policy. In 2008, the European Union formally launched the Emission Trade System, which currently is the largest carbon trading market. Then, a carbon cap-and-trade policy was implemented in many countries, such as the United States (some individual states) and China [

3,

4,

5]. The aim of all these carbon policies was to limit the carbon emissions in the production process.

However, too much attention has been paid to the implementation of low-carbon policies that reduce the impact of production on the environment. Few carbon policies have focused on the production and consumption process at the same time. Approximately 30%–40% of the decline in ecological quality created by global warming is due to the household durable goods consumption [

6]. In real life, many durable goods, such as automobiles, air conditioners, and refrigerators, emit more carbon dioxide during the consumption process [

7]. For example, for the electric automobile, which is currently heavily promoted, the carbon emissions per unit in the production process are approximately 70 g/km, and the carbon emissions per unit in the consumption process are approximately 188 g/km [

8]. This means that even for an electric vehicle, carbon emissions in the consumption process occupied more than 70% of its total carbon emissions in the lifecycle. With the further promotion of future carbon emissions reduction policies, the durable products with high carbon emissions in both production and consumption processes will be restricted by not just one single carbon policy. A mixed carbon policy that limits carbon emissions in both the production and the consumption process should be implemented in the future.

The implementation of a carbon policy has brought great challenges to the high carbon emissions durable goods manufacturer. In the classical durable goods theory, a leasing strategy is always the optimal market strategy for the monopoly manufacturer [

9]. Many scholars have extended this classical durable goods theory finding that many external factors affect the manufacturer’s choice between leasing and selling [

10,

11,

12]. With the implementation of the mixed carbon policy, whether leasing is still the optimal marketing strategy of the monopoly manufacturer is a question worth investigating. A durable goods manufacturer had to regard carbon policy as an important influencing factor in the selection strategy between leasing and selling.

Meanwhile, the leasing strategy is widely regarded as a greener marketing model rather than one based on a selling strategy [

13,

14]. Many enterprises, such as Hewlett-Packard (HP), Bavarian Motor Works (BMW), and GREE Electric Appliances (GREE), have improved their green image through the introduction of leasing programmes. However, whether this conclusion is still valid under the implementation of carbon policy remains to be verified.

Therefore, the authors investigate with respect to a mixed carbon policy, the manufacturer’s selection of an optimal marketing model strategy when choosing between leasing and selling. Furthermore, comparing leasing and selling, this paper determines which strategy is greener. Specifically, the following questions are addressed in this paper:

Main question: Do specific intervals exist for the carbon trading price and carbon tax rate that can achieve a win-win result between the monopoly manufacturer’s profit and a friendly environment?

Other related questions: (1) How do the manufacturer’s production and the consumers’ consumption activities change after the implementation of the mixed carbon policy? (2) What will happen to the optimal leasing and selling profit of the manufacturer under the mixed carbon policy? How do the carbon trading price, the carbon cap, and the carbon tax rate affect the leasing and selling profit? (3) Under a mixed carbon policy, what is the manufacturer’s optimal marketing model selection strategy?

The main contribution of this paper is that it proposes a mixed carbon policy that targets the durable goods’ carbon emissions in both the production and the consumption process. Additionally, this paper provides new analysis results regarding how a manufacturer adjusts its optimal marketing model between leasing and selling. Moreover, by comparing the manufacturer’s profits and total carbon emission volume, this paper also offers some effective policy suggestions that guide manufacturers to choose the marketing model with lower carbon emissions.

To answer the questions above, this paper aims to examine the monopoly manufacturer’s optimum production quantity decisions made under the constraints of a low carbon policy for both production and consumption processes and analyses their effects on the leasing and selling profit. Additionally, this paper, based on the condition that the manufacturer obtains the optimal profits, explores the carbon trading price and the carbon tax rate intervals that enable the manufacturer to choose the more profitable marketing strategy and at the same time to achieve a reduction in carbon emissions to the environment.

The reminder of this paper is structured as follows: The relevant literature is reviewed in

Section 2. In

Section 3, the parameters and decision variables are described and the basic models proposed in this paper are then presented. In

Section 4, the model formulation is described and the optimal solutions is revealed under leasing and selling. In

Section 5, the changing characteristics of consumption behaviour under the mixed carbon policy are discussed. The optimum quantity and marketing model selection strategy for the monopolistic manufacturer are discussed; then, by comparing the actual carbon emissions of leasing and selling, a strategy for obtaining a win-win result is presented. In

Section 6, the numerical analysis and results are described. In

Section 7, the whole paper is summarized, and the implications of this research are discussed.

5. The Mixed Carbon Policy Impact Analysis

This section analyses how the manufacturer’s production quantity, the leasing and selling profits, and the consumer’s behaviour change after the mixed carbon policy is implemented.

5.1. The Impact of the Mixed Carbon Policy on Production

According to the Equations (8) and (18), using the necessary conditions for equilibrium, we can obtain the following results:

Proposition When , whether under leasing or selling, the manufacturer does not produce the durable goods, instead choosing to sell all the carbon quota Q. Only when , the manufacturer will carry on the production activity under leasing and selling. When , depending on the level of the carbon tax rate, the manufacturer only carries on the production activity under one marketing model (leasing or selling).

Proposition 1 shows that the carbon trading price and the carbon tax rate have significant impacts on the manufacturer’s production decision. Different from the general assumption, the high carbon trading price is not always good for the policy-maker. The manufacturer’s incentive to produce decreases as the carbon trading price increases (). When the carbon trading price is too high, the manufacturer has no willingness to produce the durable goods because under this situation, the profit of selling all the carbon quota Q is higher than the profits obtained from leasing or selling the durable goods. Thus, to guarantee the effective implementation of the mixed carbon policy, policy-makers must keep the carbon trading price below the threshold ().

In addition, since the carbon tax is imposed on consumers, when the carbon tax rate is low (), the manufacturer has a higher incentive to resume selling the durable goods, as the price of carbon trading price decreases. Additionally, when the carbon tax rate is high (), the manufacturer has a higher incentive to resume leasing the durable goods, as the price of the carbon trading price decreases. According to our assumptions, carbon cap-and-trade is more effective at controlling total carbon emissions; thus, holding the carbon tax to a high level () would be more beneficial for policymakers in controlling the total amount of carbon emissions.

5.2. The Impact of the Mixed Carbon Policy on Consuming Behaviour

5.2.1. Leasing Situation

At the steady-state equilibrium, under the mixed carbon policy, substituting Equations (9) and (10) into Equations (3) and (4), we can derive the indifference utility value of

as follows:

Before the implementation of the mixed carbon policy,

. Substituting

into Equations (22) and (23), we can derive the indifference utility value of

as follows:

According to Equation (5) and by combining Equations (22–25), we can derive the leasing reduction quantities of new products, used products and total products under the mixed carbon policy as follows:

where

is the reduction in the quantity of the consumers who always rent the new products. Under the mixed carbon policy, this group of consumers turns to renting the used products instead.

is the reduction in the quantity of consumers who always rent the used products; this group of consumers withdraws from the market and no longer rents any of the durable goods. Under the mixed carbon policy,

is the total reduction in the quantity of consumers who rent the durable goods. Hence, the following is proposed:

Proposition 2. The total number of consumers renting durable goods decreases with increases in the carbon trading price. In addition, the number of consumers renting new durable goods is decreasing at the same rate as that of the decrease in the number of consumers renting used durable goods.

Proposition 2 shows that the carbon trading price has a significant impact on the consumers’ consumption behaviour under a leasing strategy. The implementation of the mixed carbon policy has led to a reduction in the number of consumers renting old and new durable goods, and the reduction number is the same. The reduction in the number of consumers renting old and new durable goods increases as the carbon trading price increases. In addition, the higher the carbon emissions of the durable goods in the production and the consumption process are, the greater the reduction in the number of the consumers. In addition, the quality v and the durability δ of the durable goods also affect the consumption behaviours under leasing: the higher the value of v and δ are, the less the reduction in the number of consumers.

5.2.2. Selling Situation

Similar to the leasing situation, we can derive the indifference utility value of

with the mixed carbon policy as follows:

Before the implementation of the mixed carbon policy,

. Substituting

into Equations (26) and (27), we can derive the indifference utility value of

without the carbon cap-and-trade policy and the carbon tax policy as follows:

According to Equation (14) and by combining Equations (26–29), we can derive the selling reduction quantities of the new products, the used products and the total products when the government enacts a carbon cap-and-trade policy and a carbon tax policy as follows:

where

is the reduction in the quantity of consumers who always buy new products. Under the mixed carbon policy, this group of consumers turns to buy used products instead.

is the reduction in the quantity of consumers who always buy used products; this group of consumers withdraws from the market and no longer buys any products. Under the mixed carbon policy,

is the total reduction in the quantity of consumers who buy the durable goods. Hence, the following is proposed:

Proposition 3. The total number of consumers buying durable goods decreases with the increases of the carbon trading price and the carbon tax rate. In addition, the number of consumers buying new durable goods is decreasing at the same rate as the rate of the decrease in the number of consumers buying used durable goods. Compared with the carbon trading price, the carbon tax has a greater impact on consumption behaviours.

Proposition 3 shows that the carbon trading price and the carbon tax rate have significant impacts on the consumers’ consumption behaviours under a selling strategy. The implementation of the mixed carbon policy has led to a reduction in the number of consumers buying old and new durable goods, and the reduction in the numbers is the same. The reduction in the number of consumers buying old and new durable goods increases as the carbon trading price and carbon tax rate increase. In addition, the higher the carbon emissions of the durable goods in the production and the consumption process are, the more the reduction in the number of consumers. In addition, due to the durable goods’ higher carbon emissions in the consumption process, the carbon tax rate has a greater impact on the consumers’ consumption behaviour. Therefore, the carbon tax is a better carbon policy mechanism that the government can employ to regulate and control the consumption behaviours.

Together with the results of Proposition 2 and Proposition 3, we find that the influencing characteristics of the mixed carbon policy on the consumers’ consumption behaviours under leasing and selling are similar. The number of consumers participating in the market both decreases, and the decreasing rate is the same. Moreover, in regulating consumer behaviours, a carbon tax is more effective than a carbon price.

5.3. The Impact of the mixed Carbon Policy on Profits

From

Section 5.2, we know that the number of consumers participating in the market decreases after the government enacts the mixed carbon policy. However, does that mean the manufacturer’s profits also decline? In this section, we study how the mixed carbon policy affects the manufacturer’s leasing and selling profits.

5.3.1. Leasing Situation

Comparing the leasing profits before and after the mixed carbon policy has been enacted, assume the government does not enact the mixed carbon policy, that is, assume that

. Substituting

into Equation (11), without a mixed carbon policy, we can derive the optimal profits of the manufacturer as follows:

where

denotes the optimal leasing profits with no mixed carbon policy.

By comparing the profit difference for the manufacturer between

and

, we have:

Taking the first-order derivatives of

with respect to

, we then have:

Proposition 4. The following result holds:

- (1)

When , we have , : the optimal leasing profit declined after the enactment of the mixed carbon policy. The higher the carbon trading price is, the lower the leasing profit.

- (2)

When , we have , : the optimal leasing profit still declined after the enactment of the mixed carbon policy, but the higher the carbon trading price is, the less the lost leasing profit.

- (3)

When , we have , : the optimal leasing profit under the mixed carbon policy is higher than that without the mixed carbon policy, and the higher the carbon trading price is, the greater the leasing profit.

Note: denotes the total carbon emissions of one durable product in the whole life cycle; thereby, denotes the total carbon emissions of all leased durable goods. We assume that .

Proposition 4 shows that when the government sets the value of the carbon cap Q too low (i.e., lower than the total actual carbon emissions from the manufacturer ), the manufacturer’s leasing profits are badly dented. Additionally, as the carbon trading price increases, the manufacturer’s leasing profits will be further eroded. With the increase of carbon cap Q, the profit level of the manufacturer gradually improves, when ; although the mixed carbon policy still reduces the manufacturer’s leasing profits, the manufacturer can already obtain a benefit by selling excess carbon cap permits. Moreover, the higher the carbon trading price is, the less the leasing profits are reduced. When the carbon cap Q is too high (), the profits than manufacturer can earn by selling excess carbon cap permits is more than the market shrinkage caused by the mixed carbon policy. Thereby, the manufacturer’s leasing profit is higher than it was before the mixed carbon policy was implemented, and the higher the carbon trading price is, the more the manufacturer’s profit will increase.

As seen from the above analysis, a carbon cap Q that is too low will severely decrease the manufacturer’s incentive to produce; however, the government’s goal of controlling carbon emissions will not be achieved if the carbon cap Q is too high. By setting the carbon cap Q on the interval , the manufacturer can be encouraged to reduce the carbon emissions, while not overly affecting the incentives for production.

5.3.2. Selling Situation

Similar to the leasing situation, before the government enacts the mixed carbon policy,

. Substituting

into Equation (21), without the mixed carbon policy, the optimal selling profit of the manufacturer can be derived as follows:

where

denotes the optimal selling profits without the mixed carbon policy.

By comparing the profit difference for the manufacturer between

and

, we have:

Taking the first-order derivatives of

with respect to

and

, then, we have:

Proposition 5. The optimal selling profits of the manufacturer decrease as the carbon tax rate λ increases. Note the following for the carbon cap Q and the carbon trading price :

- (1)

When , we have , : the optimal selling profit declined after the enactment of the mixed carbon policy, and the higher the carbon trading price is, the lower the selling profit.

- (2)

When , we have , : the optimal selling profit still declined after the enactment of the mixed carbon policy, but the higher the carbon trading price is, the less the lost selling profit.

- (3)

When , we have , : the optimal selling profit under the mixed carbon policy is higher than that without the mixed carbon policy, and the higher the carbon trading price is, the more the selling profit.

Note: denotes the carbon emissions of all selling products in the production process. denotes the total carbon tax of all selling products during the consumption process. We assume that .

Compared with the results of Proposition 4, we find that the impact of the carbon cap Q on leasing and selling is very similar. When the carbon cap Q is lower than the total actual carbon emissions from the manufacturer, that is, when , the manufacturer’s selling profits are lower than they were before the mixed carbon policy was implemented, and as the carbon trading price increases, the selling profits fall further. When , the manufacturer’s selling profits are still lower than they were before the mixed carbon policy was implemented, but the higher the carbon trading price is, the less the leasing profits are reduced. When , the manufacturer’s selling profits are higher than they were before the mixed carbon policy was implemented, and the higher the carbon trading price is, the more the selling profits increase. Therefore, similar to the leasing situation, by setting the carbon cap Q on the interval , the manufacturer can be encouraged to reduce the carbon emissions, while not overly affecting the manufacturer’s incentives for production.

Together with the results of Proposition 4 and Proposition 5, we find that the manufacturer’s leasing and selling profits are both affected by the mixed carbon policy. For the carbon tax rate, the higher the carbon tax rate is, the lower the manufacturer’s profits. The carbon cap and carbon trading price combine to affect the manufacturer’s profits. When the carbon cap Q is low, raising the carbon trading price will hurt the manufacturer’s profits; when the carbon cap Q is high, raising the carbon trading price will boost the manufacturer’s profits. Therefore, between the government and the manufacture, for the carbon cap Q, there is an equilibrium interval () in which the government can achieve the aim of controlling carbon emissions, while not overly affecting the manufacturer’s enthusiasm for production.

5.4. Optimal Marketing Model Selection

After the mixed carbon policy was enacted, the manufacturer’s optimal marketing model selection changed. Leasing is no longer the optimal marketing model all the time. In this case, this section studies how the mixed carbon policy affects the manufacturer’s optimal marketing model.

Comparing the leasing and selling profits of the manufacturer under the mixed carbon policy, according to the Equations (11) and (21), we can obtain the following results:

Proposition 6. When the carbon trading price , , i.e., when the manufacturer’s leasing and selling profits are same, there is no difference between the leasing and the selling model; when , ; therefore, leasing is the optimal marketing model; when , ; therefore, selling is the optimal marketing model.

Note: let .

Proposition 6 shows that the carbon tax rate cannot affect the marketing model selection of the manufacturer. In contrast, the carbon trading price has a significant impact on the market model selection of the manufacturer. When the carbon trading price is low, the manufacturer is more inclined to choose leasing as its optimal marketing model; when the carbon trading price is high, the manufacturer is more inclined to choose selling as its optimal marketing model.

Together with the results of Proposition 4 and Proposition 5, we find that when the carbon trading price , the manufacturer will choose the leasing model in order to maximize the profits; under these circumstances, to effectively control the overall carbon emissions, the government should set the carbon cap Q on the interval . When the carbon trading price , the manufacturer will choose the selling model in order to maximize the profits; under the circumstances, to effectively control the overall carbon emissions, the government should set the carbon cap Q on the interval .

5.5. Comparing Total Carbon Emissions under Leasing and Selling

We now compare the total actual carbon emissions of leasing and selling. According to the assumption, we can derive that the total carbon emissions of one durable good during the whole life cycle are always . Therefore, denotes the actual total carbon emissions under leasing, and the actual total carbon emissions of selling are denoted by .

According to the Equations (8) and (18), we can obtain the following results:

Proposition 7. The following result holds:

- (1)

If the carbon tax rate , we have .

- (1)

If the carbon tax rate : When , we have ; when , we have ; and when , we have .

Note: let .

Proposition 7 shows that, when the carbon tax rate λ is low (), the total carbon emissions under leasing are always lower than the total carbon emissions under selling are, regardless of how the carbon trading price changes. Hence, to encourage the manufacturer to choose the leasing model, the government should set the carbon cap Q on the interval and keep the carbon trading price lower than , according to the Proposition 6. When the carbon tax rate λ is high () and the carbon trading price is lower than , the total carbon emissions under leasing are higher than the total carbon emissions under selling. Hence, according to the Proposition 6, to encourage the manufacturer to choose the selling model, the government should set the carbon cap Q on the interval and keep the carbon trading price higher than ; the total carbon emissions under leasing are lower than the total carbon emissions under selling when the carbon trading price is higher than . Hence, to encourage the manufacturer to choose the leasing model, the government should set the carbon cap Q on the interval and keep the carbon trading price lower than , according to the Proposition 6.

5.6. Win-Win Strategy

From the results of

Section 5.3 and

Section 5.4, we know that there exists a threshold value of carbon trading prices that makes the profits and the total actual carbon emissions under leasing the same as those under selling. Therefore, is there a carbon trading price range where the manufacturer gets higher profits and at the same time the total carbon emissions are lower? This section explores the existence of the intervals for the carbon trading price that achieve win-win results for the manufacturer and the environment.

According to the results of Proposition 6 and Proposition 7, we can obtain the following results:

Proposition 8. The following result holds:

- (1)

If the carbon tax rate , we have: .

- (2)

If the carbon tax rate , we have: .

Proposition 8 shows that if the carbon tax rate is low (), then, when the carbon trading price is high (), the profits of the manufacturer under selling are higher than those under leasing, but the total carbon emissions under selling are also higher than those under leasing. When the carbon trading price is low (), the profits of the manufacturer under leasing are higher than the selling profits are, and the total carbon emissions under leasing are meanwhile also lower than those under selling. Thereby, is an optimal equilibrium interval for the carbon trading price and the carbon tax rate that creates a win-win result between the manufacturer’s profits and a friendly environment.

If carbon tax rate is high (), then, when the carbon trading price is too low (), the profits of the manufacturer under leasing are higher than the selling profits, but the total carbon emissions under leasing are also higher than those under selling. When the carbon trading price is too high (), the profits of the manufacturer under selling are higher than the leasing profits, but the total carbon emissions under selling are also higher than those under leasing. Only when the carbon trading price is on the interval , the profits of the manufacturer under leasing are higher than selling profits, and at the same time, the total carbon emissions under leasing are also lower than those under selling. Hence, is another optimal equilibrium interval for the carbon trading price and carbon tax rate that creates a win-win result between the manufacturer’s profits and a friendly environment.

6. Numerical Analysis

To capture qualitative insight regarding how the manufacturer’s production and profits varies as the mixed carbon policy varies, in this section, we use a numerical analysis to further illustrate the impacts of the carbon trading price, carbon cap and carbon tax rate on the production quantities, consumption behaviour, the leasing and selling profits and the total carbon emissions. In our numerical analysis, we use the following values to establish ranges for model parameters: δ = 0.5, v = 1, , , , , , , , , , , , , . We draw the relationships in the following figures.

Figure 1 shows the effect of

(carbon trading price) on the production quantity of the manufacturer under a leasing strategy. It is obvious that if the carbon policy is not implemented, the production quantity of the manufacturer under leasing is a fixed value

.

If the carbon policy is implemented, the optimal production quantity under leasing decreases as increases, and it remains 0 when . Under this circumstance, the manufacturer no longer makes the durable goods but sells the entire carbon emission cap permits.

In

Figure 2, if the mixed carbon policy is not implemented (

), the production quantity of the manufacturer under selling is a fixed value

. If the mixed carbon policy is implemented, the optimal production quantity

under selling decreases as

increases, and the carbon tax rate does not affect the descending slope of the production quantity. The smaller the carbon tax rate

λ is, the closer the production quantity is to 0.31. Whatever the carbon tax rate value is, the manufacturer will no longer make any durable goods when the carbon trading price is large enough.

As shown in

Figure 3, if the mixed carbon policy is not implemented, the utility type value of the consumers who rent new durable goods and used durable goods are 0.7 and 0.4, respectively. If the mixed carbon policy is implemented, the utility type values of both types of consumers increase as the carbon trading price

increases, which means that with the increases of the carbon trading price, both the number of consumers that rent new durable goods and those that rent used durable goods are reduced.

Additionally, the value of is increasing at twice the rate of increase for until when , which means the reduction in the number of consumers who rent new durable goods is half the total reduction in the number of consumers and that the reduction in the number of consumers who rent new durable goods is equal to the reduction in the number of consumers who rent used durable goods. Furthermore, the leasing consumers will all exit the market when .

In

Figure 4, if the mixed carbon policy is not implemented, the utility type value of consumers who buy new durable goods and used durable goods are 0.45 and 0.38, respectively. Similar to the leasing strategy, if the mixed carbon policy is implemented, both types of consumers, i.e., those who buy new durable goods and those that buy used durable goods, are reduced with increases of the carbon trading price

. However, due to the existence of a carbon tax, the utility type value of consumers does not start at the value of the utility type without the carbon policy. Additionally, similar to leasing, the value of

is also increasing at twice the rate of increase of that for

, i.e., the reduction in the number of consumers who buy new durable goods

is half of the total reduction in the number of consumers

. When the carbon trading price

,

, which means the utility value of consumers who buy new durable goods is equal to the utility value of consumers who buy used durable goods. At this point, the consumers in the market all will choose to buy new durable goods.

Figure 5 shows the following: If the mixed carbon policy is not implemented, the manufacturer’s leasing profit is a fixed value

. If the mixed carbon policy is implemented, both the carbon emissions cap

Q and the carbon trading price

affect the manufacturer’s leasing profit. The larger the carbon emission cap

Q is, the higher the manufacturer’s leasing profit. As the

increases, the manufacturer’s leasing profit will decrease at first and then increase, but it will always be lower than 0.225 when

Q = 0.15. In addition, when

Q = 0.25, note the following: the leasing profit

when

. When

, the leasing profit will increase continuously as the carbon trading price

increases. The leasing profit is always higher than

when

Q = 0.35, and as the carbon trading price

increases, the manufacturer’s leasing profit increases at an exponential rate.

As shown in

Figure 6, if the mixed carbon policy is not implemented, the manufacturer’s selling profit is a fixed value

. If the mixed carbon policy is implemented, the higher the carbon cap value is, the faster the manufacturer’s selling profit growth rate. The higher the carbon cap value is, the earlier the selling profit exceeds the fixed value

. Regardless of the value of the carbon emissions cap, with the increase of carbon trading price

, the selling profit will be higher than 0.2 eventually. When the carbon cap value is low (

Q = 0.06), the manufacturer’s selling profit will decrease at first and then increase with the increase of carbon trading price

. When the carbon cap value is high (

Q = 0.1), the selling profit will increase continuously as the carbon trading price

increases.

According to

Figure 7, if the mixed carbon policy is not implemented, the manufacturer’s selling profit is a fixed value

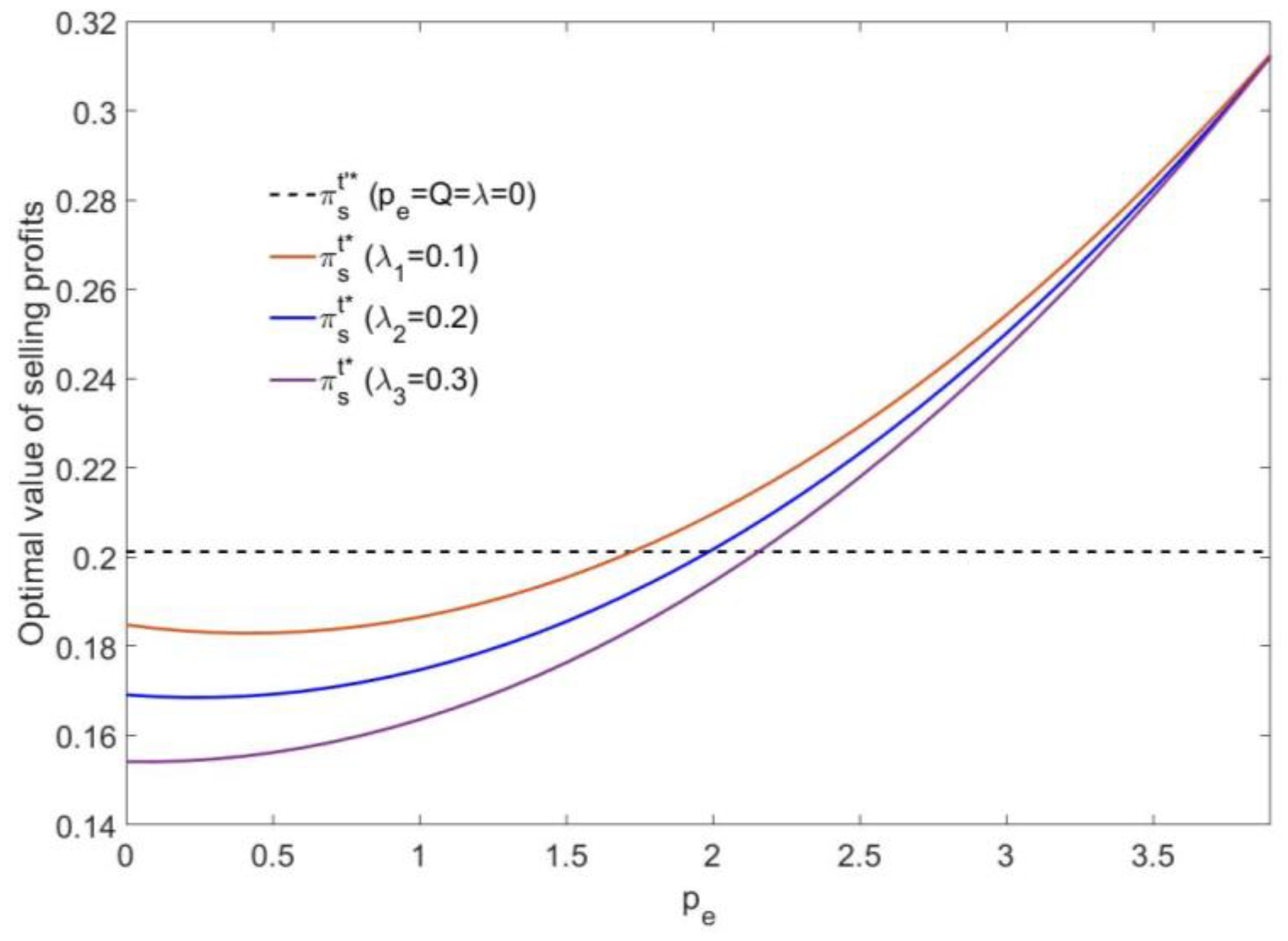

. If the mixed carbon policy is implemented, the increase of the carbon trading price

will lead to an increase in the selling profit of the manufacturer. In addition, the higher the carbon tax rate λ is, the lower the initial selling profit, but with the increase of the carbon trading price

, the growth in the profit is faster than the growth in the profit under a low carbon tax rate.

Moreover, the selling profit is lower than when the carbon trading price is low. Only when the carbon trading price is high the manufacturer can gain more profit than the profit that would have been gained if the mixed carbon policy was not implemented. In addition, the selling profit is growing closer to as the carbon trading price increases.

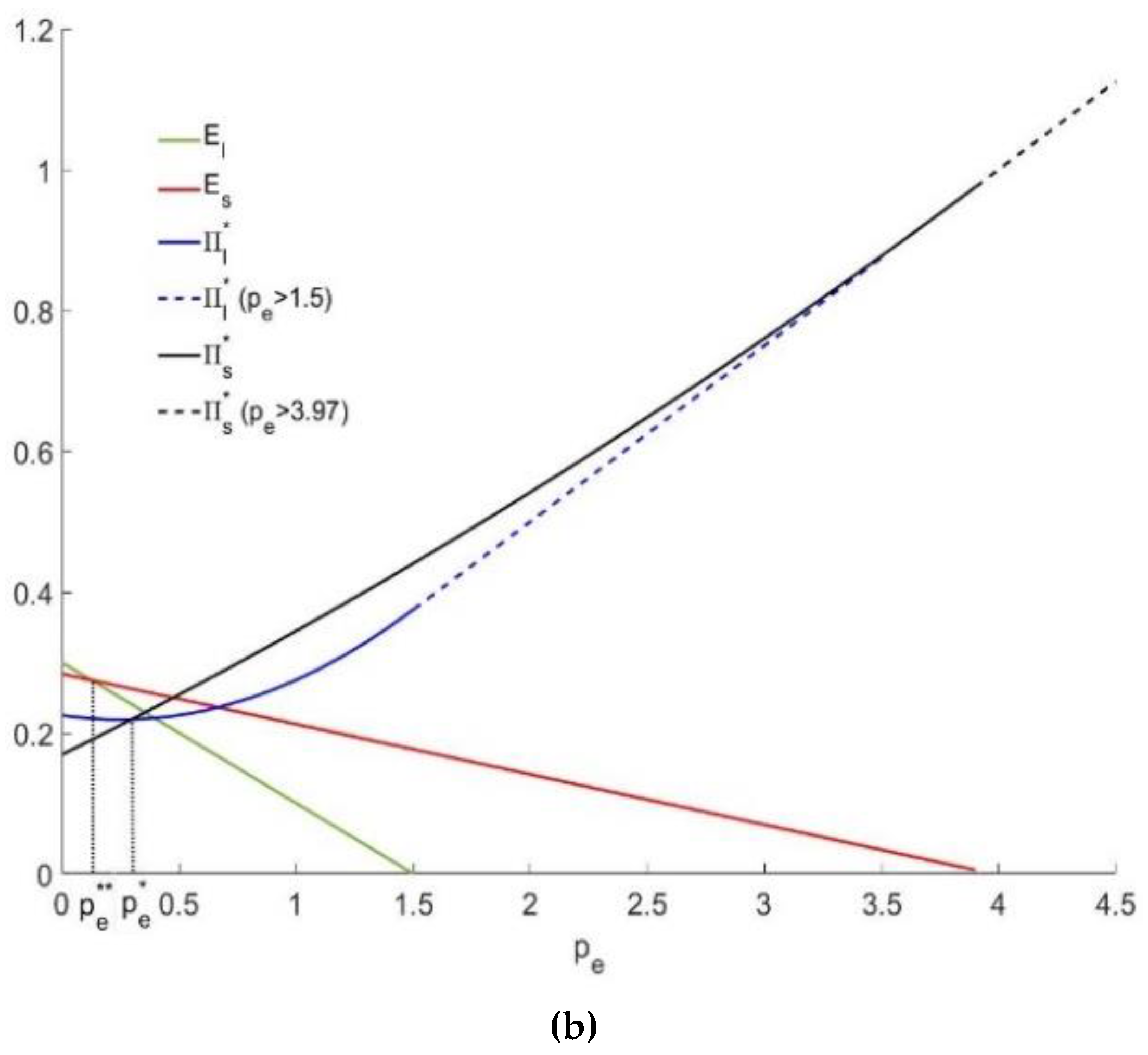

In

Figure 8a,b, whether the carbon emission cap is high or low, we can obtain the following facts: as the carbon trading price increases, the total carbon emissions under leasing and selling will both be reduced, and the carbon emissions under leasing will be reduced faster. When the carbon trading price

, the total carbon emissions under leasing and selling are the same

. When the carbon trading price is low, the profit may decrease at first, but as the carbon trading price increases, the profit under leasing and selling will both eventually increase. The profit under leasing and selling will be equal to

when the carbon trading price is large enough. When the carbon trading price

, the profit under leasing and selling is the same

. Therefore, when

, the leasing profit is higher than the selling profit

, and at the same time, the total carbon emissions under leasing are lower than those under selling

. Thus, we can achieve a win-win result by controlling the carbon trading price within the interval

.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}