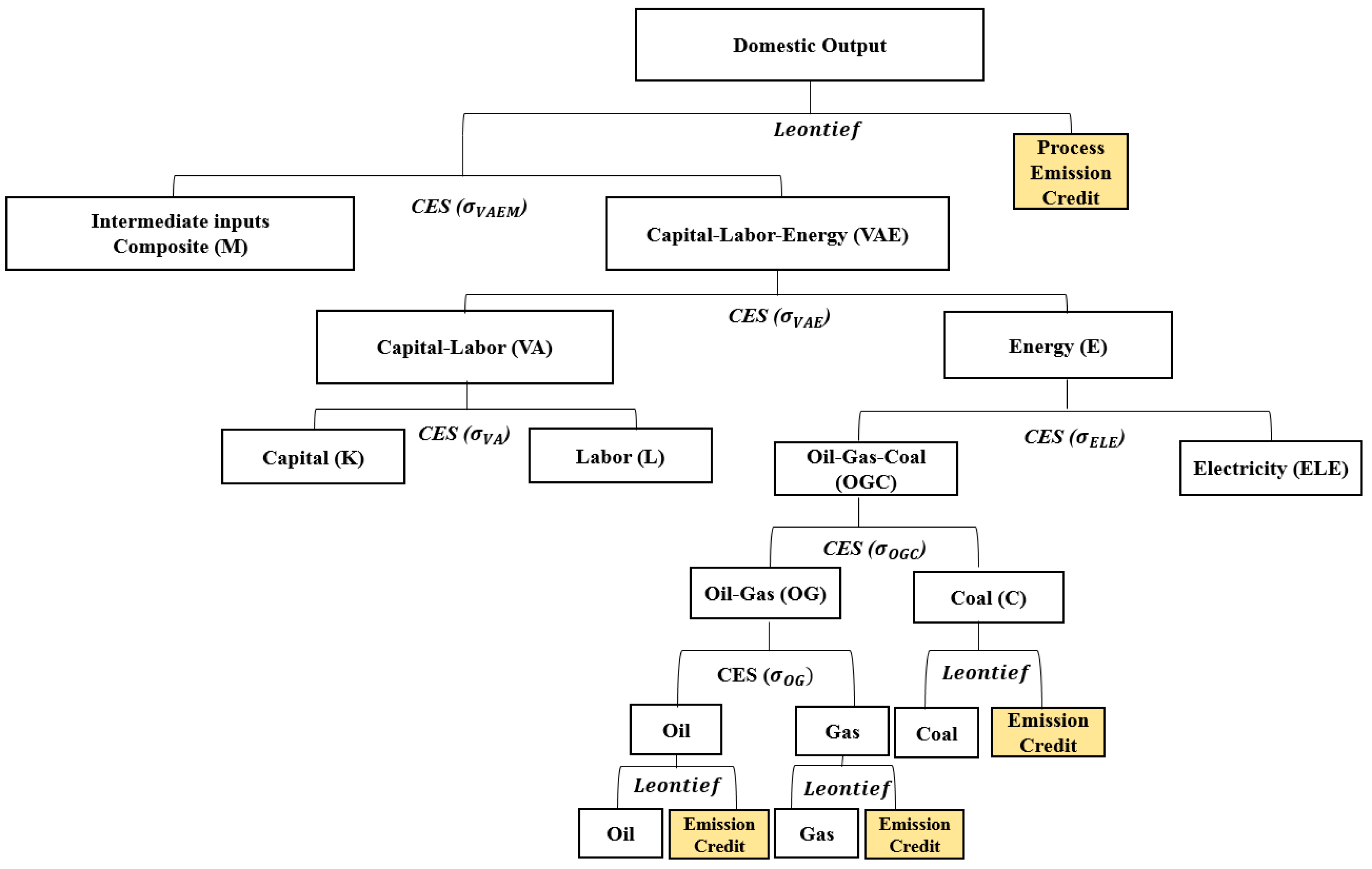

3.1. Scenario Building

Based on the “Comprehensive Measures for Particulate Matter Management” and the “Basic Roadmap Amendment to Achieve National Greenhouse Gas Emission Reduction Targets by 2030,” scenarios are created to examine the economic impacts when particulate matter and GHG reduction targets [

2,

38] are achieved. The target years for investigating the effects of the policies are 2022 and 2030. The year 2022 is the target year for the PM

2.5 reduction measures [

2], and 2030, for the GHG roadmap [

3,

38].

For 2022, the PM

2.5 reduction measures set the target to reduce domestic PM

2.5 emissions by 30%, while the GHG roadmap sets the target to cut domestic GHG emissions by 15.3% compared with the BAU scenario. For 2030, the domestic reduction target for the GHG roadmap is 32.5% compared with the BAU scenario. On the other hand, since there is no quantitative goal set after 2022 for PM

2.5 emissions, the reduction target by 2030 is set at 30%, the same level as that of 2022.

Table 6 shows the scenarios constructed for the analysis.

The reduction targets in the model are met by emissions taxes. It is assumed that a carbon tax is imposed on the unit emissions of GHG, and an air pollution tax is imposed on the unit (primary and secondary) emissions of PM2.5. Thus, targets are achieved through the conversion of fuel mix and restrictions on production, consumption and energy uses by imposing carbon or air pollution taxes.

3.2. 2022 Target Year Scenario

Table 7 shows the results of POL_22 and GHG_22. By 2022, POL_22 reduces PM

2.5 emissions by 30% through an air pollution tax of about

$197 per kilogram of PM

2.5. GHG emissions also reduce by about 22.8% because of the pollution tax and a price increase in fossil fuel and energy-intensive goods. In this case, POL_22 exceeds the GHG reduction target of GHG_22 (set to 15.3%). Thus, by 2022, the auxiliary benefit of exceeding the GHG reduction target was gained through the air pollution reduction policy. On the other hand, air pollution taxes reduce production and consumption activities, decreasing the GDP by 0.62% compared with the BAU. GHG_22 reduces GHG emissions by 15.3% through a carbon tax of approximately

$37 per ton of GHG. As the auxiliary benefit, PM

2.5 emissions are reduced by about 14.8% and the GDP decreases by 0.34% compared with BAU.

Table 8 shows the effects of particulate matter reduction according to POL_22 on total output and labor expenditures. The effects for each of the ten sectors with largest changes are displayed. In terms of total output, the impacts of PM

2.5 reduction policy on the primary metals industry (IRO) and the oil products industry (OIL) are large. In the case of the services industry (SER), as the total amount of output is large, the absolute amount of the impact is also large (

$31.7 billion), even though the rate of change is relatively small (–1.9%). Household consumption (c), including transportation (TRN) and private use, have a substantial impact in terms of the absolute amount. In terms of ratio, the coal products sector (COA) is the largest, with coal consumption declining about 54% compared with the BAU scenario.

The change in labor cost expenditure by sector, which indirectly shows the effect on employment, indicates that the total labor expenditure of the services sector (SER) is decreased by $12.8 billion. In terms of the ratio, it is evident that the labor cost expenditure of air pollution-intensive industries, such as primary metals (IRO), oil products (OIL), transport (TRN), and nonmetallic mineral products (NMP), lowers because of these industries’ reduced output.

Table 9 shows the effects of GHG reductions under GHG_22 on total output by sector and labor cost expenditure. In terms of total output, the negative impact on the primary metals industry (IRO) is the largest due to the GHG reduction. In addition, the negative effects on services (SER), chemical products (CHE), oil products (OIL), and transportation (TRN) are also significant. Household and government consumption are also reduced because of the carbon taxes. In terms of labor cost expenditure, a large decline in labor costs in industries such as services, primary metals, chemical products, and transportation is seen. In terms of ratio, a decline in labor cost is forecast to be large for air pollution-intensive industries, such as primary metals, nonmetallic minerals, and oil products.

3.3. 2030 Target Year Scenario

Table 10 displays the results of the 2030 POL_30 and GHG_30 scenarios. In POL_30, the PM

2.5 reduction target set at 30% compared with the BAU in 2030 is achieved by imposing an air pollution tax of approximately

$211 per kilogram. Due to the impact of air pollution taxes, GDP is about 0.54% lower than in the BAU. Reductions in fossil fuel use due to an air pollution tax result in a 22.6% reduction in GHG emissions.

On the other hand, GHG reduction target (−32.5% below the BAU level) is achieved by imposing a carbon tax of $169 per ton. In this case, the effect on the overall economy is substantial—decreasing GDP by 1.75% compared with the BAU scenario. When GHG emissions falls according to the target, PM2.5 emissions also decrease by 32.8%, thereby exceeding the target for POL_30. Thus, by 2030, the additional benefit of achieving the air pollutant reduction target can be attained through the GHG reduction policy.

Table 11 shows the effects of particulate matter reduction according to POL_30 on total output and labor costs. Primary metals (IRO), a pollution-intensive industry, sustains the largest negative impact. In the services industry (SER), though the rate of change is low, the change in output in absolute terms is not negligible. Like the previous POL_22 scenario, the pollution-intensive industries are heavily affected.

In the case of labor cost expenditure, the labor-intensive services sector (SER), transportation sector (TRN), and primary metals sector (IRO) are heavily affected. The primary metals and oil products industry (OIL) show a large rate of change.

Table 12 shows the effects of GHG reduction according to GHG_30 on total output and labor cost expenditure by sector. For the services sector (SER), the absolute amount of change is large compared with the BAU scenario due to its size. As with the other scenarios above, the GHG-emitting industries show significant reduction in total output. In the case of metal products (MAC) and food and tobacco (FOO), the total output decline is large due to the rise in intermediate materials prices.

The change in the ratio of labor cost expenditure by sector is the largest in the services sector (SER). Large negative effects are also observed in energy-intensive sectors, such as chemical products (CHE), transportation (TRN), primary metals (IRO), and non-metallic mineral products (NMP).

3.4. Comparing Costs and Benefits of Each Scenario

As investigated above, policies to reduce air pollutants or GHGs increase production costs and restrict general production and consumption, thereby reducing the overall GDP. Substantial negative effects on energy-intensive industries and GHG- and air pollution-intensive industries were observed. While the reduction policies involve costs, the air pollutant reduction policy also generates additional benefits, such as reducing GHG emissions (and vice versa).

Prior studies have revealed the calculated external cost per unit of GHG and air pollutant emissions [

22,

39]. Thus the cost and benefit of each scenario can be analyzed by comparing reductions in GDP (that represent a reduction in the aggregated added value for the overall economy) with the environmental benefits of pollutant reduction.

According to a study by the United States Environmental Protection Agency [

39], the estimated external cost per ton of GHG in 2014 was about

$40 (in 2014 price). On the other hand, according to Parry et al. [

22], the external cost per unit of PM

2.5 has had a cost of

$592 per kilogram for the ground-level emissions and

$50 per kilogram for the smokestack emissions (in 2014 prices). In other words, the external cost of PM

2.5 differs greatly depending on the source of the emissions. However, in this study, the unit cost for the smokestack emission is used for comparing the benefit to the cost. This choice is rationalized as follows. First, this study considers the secondary emissions of PM

2.5 which is generated in the atmosphere from precursors. Therefore, the estimation based on PM

2.5 in the atmosphere can be considered appropriate (rather than ground-level emission). Second, this study tries to yield more conservative estimates of benefits of pollution reduction. Future studies can pinpoint the differences in benefits depending on the emission location of the pollutants. For example, it may be desirable to measure primary emissions from vehicles or household heating as PM

2.5 ground-level emissions. Emissions from some small and medium-sized manufacturing firms that are not well equipped with reduction devices can also be considered as ground-level emissions.

Applying the external cost of pollutants per unit would allow us to compare the environmental benefits of reducing GHG and air pollutants with the economic cost (reduction in GDP) for each scenario analyzed in the CGE study. While these comparisons are somewhat different from an accurate cost/benefit analysis, they will help us understand the outcomes of each scenario.

Table 13 shows the amount of GDP reduction, GHG reduction, PM

2.5 reduction, and benefits for each scenario. The ratio of environmental benefits to GDP reduction is calculated. POL_22 shows a decrease in GDP of approximately

$10.9 billion; however, the sum of the benefits from GHG reduction (

$7.3 billion) and PM

2.5 reduction (

$4.9 billion) is about 1.1 times greater than the cost. Under GHG_22, while GDP decreases by

$6.1 billion, the sum of the benefits from GHG reduction (

$4.9 billion) and PM

2.5 reduction (

$2.4 billion) is about 1.2 times greater than the cost.

For POL_30, GDP decreases by about $11.7 billion, which is smaller than the sum of benefits gained from GHG reduction ($7.7 billion) and PM2.5 reduction ($5.3 billion). On the other hand, for GHG_30, the decrease in GDP is substantial—$38.0 billion. In this case, the benefits of GHG and PM2.5 reduction do not compensate for the decrease in GDP, with a multiple of 0.4 compared with GDP reduction.

Winchester and Reilly [

40] estimated the impact of 2030 GHG reduction target of Korea to be around 1% decrease in GDP level, which is smaller than that of 1.75% decrease in GHG_30 scenario in this study (

Table 10). Winchester and Reilly [

40] assumes the use of various reduction technologies such as the increase of various renewable energy sources, the increase of hybrid and electric vehicle, and the purchase of emission rights from the international emission market. With such a reduction technology, the reduction cost can be greatly reduced. Nabernegg et al. [

41] also mentioned the importance of mitigation technology by applying a global CGE model. When the low carbon technologies (such as waste heat recovery) are deployed in developing countries (such as China and India), their global competitiveness increase due to energy saving and GHG reduction, in spite of additional cost of capital investment. Evidently then, to meet Korea’s GHG reduction targets by 2030, the government should introduce reduction technologies and diversify its options to reduce the cost of GHG and PM

2.5 reductions.

{kind=link}