Evidence in Asian Food Industry: Intellectual Capital, Corporate Financial Performance, and Corporate Social Responsibility

Abstract

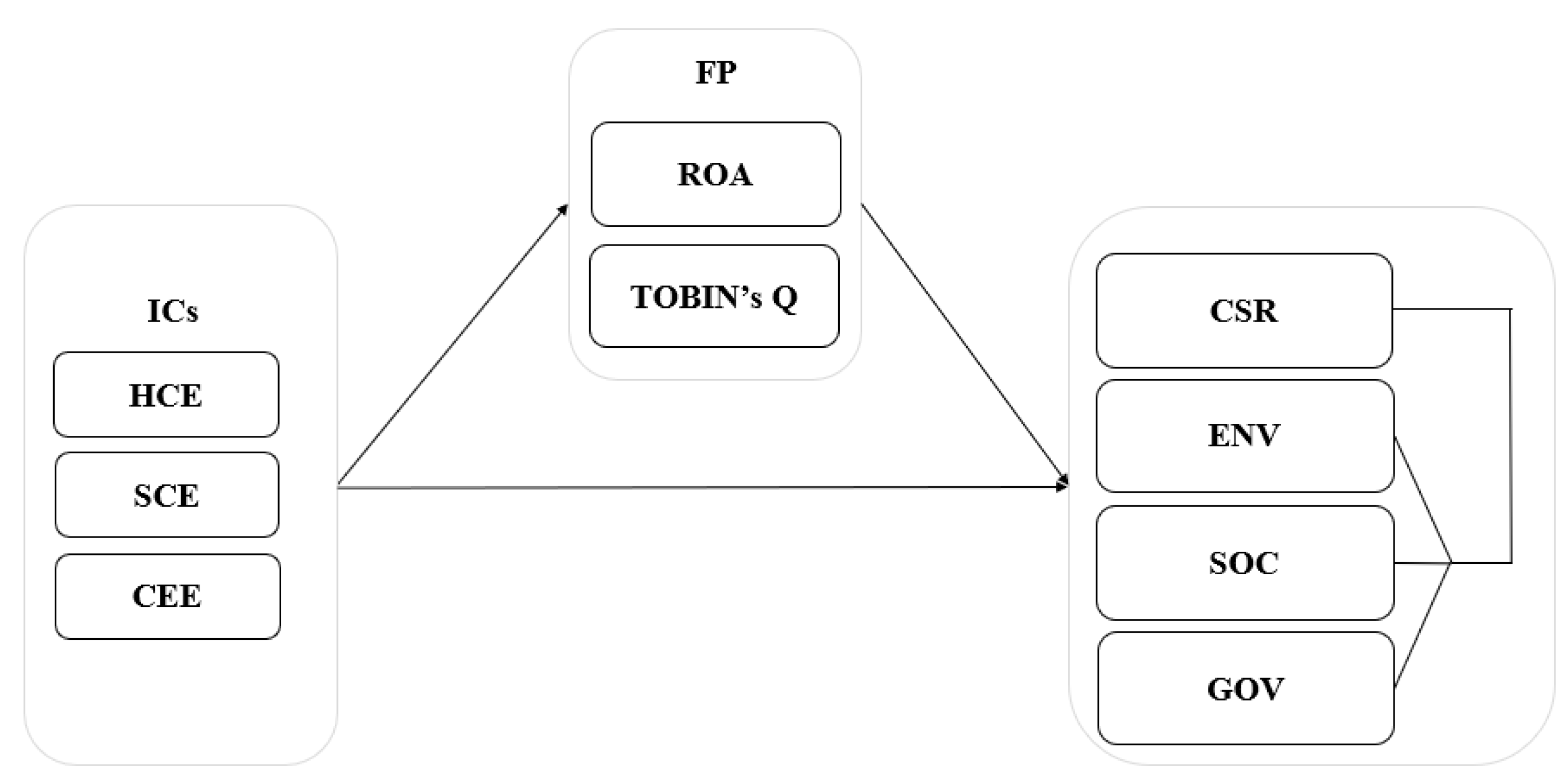

:1. Introduction

2. Literature Review and Hypotheses Development

2.1. Intellectual Capital

2.2. Value-Added Intellectual Capital

2.3. Corporate Social Responsibility

2.4. CSR Pillars

2.5. Intellectual Capital and CSR

2.6. Intellectual Capital and Financial Performance

2.7. Financial Performance and CSR

2.8. IC, Financial Performance, and CSR

3. Research Methodology

3.1. Data and Sample

3.2. CSR Ratings

3.3. Corporate Financial Performance Measures

3.4. Intellectual Capital Measure

3.5. Regression Models

4. Results and Discussions

5. Conclusions

Author Contributions

Conflicts of Interest

References

- Cheung, Y.L.; Tan, W.; Ahn, H.J.; Zhang, Z. Does corporate social responsibility matter in Asian emerging markets? J. Bus. Ethics 2010, 92, 401–413. [Google Scholar] [CrossRef]

- Hopkins, M. Corporate social responsibility and international development: Is business the solution? Earthscan; Taylor & Francis: New York, NY, USA, 2007. [Google Scholar]

- Wang, Y.G. CSR and stock performance—Evidence from Taiwan. Moder. Econ. 2011, 2, 788. [Google Scholar] [CrossRef] [Green Version]

- Lin, C.S.; Chang, R.Y.; Dang, V.T. An integrated model to explain how CSR affects corporate financial performance. Sustainability 2015, 7, 8292–8311. [Google Scholar] [CrossRef] [Green Version]

- Cuganesan, S.; Guthrie, J.; Ward, L. Examining CSR disclosure strategies within the Australian food and beverage industry. In Accounting Forum; Taylor & Francis: Abingdon upon Thames, UK, 2010; Volume 34, pp. 169–183. [Google Scholar]

- Rana, P.; Platts, J.; Gregory, M. Exploration of corporate social responsibility (CSR) in multinational companies within the food industry. In Queen’s Discussion Paper Series on Corporate Responsibility Research; Gueen’s University Belfast: Belfast, UK, 2009. [Google Scholar]

- Maloni, M.J.; Brown, M.E. Corporate social responsibility in the supply chain: An application in the food industry. J. Bus. Ethics 2006, 68, 35–52. [Google Scholar] [CrossRef]

- Kianto, A.; Ritala, P.; Spender, J.C.; Vanhala, M. The interaction of intellectual capital assets and knowledge management practices in organizational value creation. J. Intellect. Cap. 2014, 15, 362–375. [Google Scholar] [CrossRef]

- Ethiraj, S.K.; Kale, P.; Krishnan, M.S.; Singh, J.V. Where do capabilities come from and how do they matter? A study in the software services industry. Strat. Manag. J. 2005, 26, 25–45. [Google Scholar] [CrossRef] [Green Version]

- Haas, M.R.; Hansen, M.T. When using knowledge can hurt performance: The value of organizational capabilities in a management consulting company. Strat. Manag. J. 2005, 26, 1–24. [Google Scholar] [CrossRef] [Green Version]

- Gray, R. Is accounting for sustainability actually accounting for sustainability and how would we know? An exploration of narratives of organizations and the planet. Accoun. Org. Soc. 2010, 35, 47–62. [Google Scholar] [CrossRef]

- Cuganesan, S. Reporting organizational performance in managing human resources: Intellectual capital or stakeholder perspectives? J. Human Res. Cost. Account. 2006, 10, 164–188. [Google Scholar] [CrossRef]

- Arsoy, A.P.; Arabaci, Ö.; Çiftçioğlu, A. Corporate social responsibility and financial performance relationship: The case of Turkey. J. Account. Financ. 2012, 53, 159–176. [Google Scholar]

- Callan, S.J.; Thomas, J.M. Corporate financial performance and corporate social performance: An update and reinvestigation. Corp. Soc. Res. Environ. Manag. 2009, 16, 61–78. [Google Scholar] [CrossRef]

- Ni, N.; Egri, C.; Lo, C.; Lin, C.Y.Y. Patterns of corporate responsibility practices for high financial performance: Evidence from three Chinese societies. J. Bus. Ethics 2015, 126, 169–183. [Google Scholar] [CrossRef]

- Pulic, A. Intellectual capital–does it create or destroy vatue? Meas. Bus. Excel. 2004, 8, 62–68. [Google Scholar] [CrossRef] [Green Version]

- Chen, M.C.; Cheng, S.J.; Hwang, Y. An empirical investigation of the relationship between intellectual capital and firms’ market value and financial performance. J. Intellect. Cap. 2005, 6, 159–176. [Google Scholar] [CrossRef]

- Razafindrambinina, D.; Kariodimedjo, D. Is company intellectual capital linked to corporate social responsibility disclosure? Findings from Indonesia. Commun. IBIMA 2011, 2011, 511442. [Google Scholar] [CrossRef] [Green Version]

- Centre for Liveable Future. Public Support for Food Sustainability. 2016. Available online: https://clf.jhsph.edu/projects/public-support-food-sustainability (accessed on 20 October 2019).

- Morin, I. The rise of the “Food Citizen”. 2017. Available online: https://www.csr-asia.com/newsletter-the-rise-of-the-food-citizen (accessed on 15 October 2019).

- Robertson, R.; Di, H.; Brown, D.K.; Dehejia, R.H. Working Conditions, Work Outcomes, and Policy in Asian Developing Countries; ADB Economics Working Paper Series, No. 497; Asian Development Bank: Mandaluyong City, Philippines, 2016. [Google Scholar]

- Perkowski, J. China’s Growing Food Problem/Opportunity. 2014. Available online: https://www.forbes.com/sites/jackperkowski/2014/09/25/chinas-growing-food-problem-opportunity/#67eb9c624811 (accessed on 17 October 2019).

- Inkinen, H. Review of empirical research on intellectual capital and firm performance. J. Intellect. Cap. 2015, 16, 518–565. [Google Scholar] [CrossRef]

- Wang, Z.; Wang, N.; Cao, J.; Ye, X. The impact of intellectual capital–knowledge management strategy fit on firm performance. Manag. Decis. 2016, 54, 1861–1885. [Google Scholar] [CrossRef]

- Roos, J.; Roos, G.; Dragonetti, N.C.; Edvinsson, L. Intellectual Capital: Navigating in the New Business Landscape; New York University Press: New York, NY, USA, 1997. [Google Scholar]

- Stewart, T.A. Intellectual Capital; Nicholas Brealey Publishing: London, UK, 1997. [Google Scholar]

- Bontis, N. Intellectual capital: An exploratory study that develops measures and models. Manag. Decis. 1998, 36, 63–76. [Google Scholar] [CrossRef] [Green Version]

- Tovstiga, G.; Tulugurova, E. Intellectual capital practices and performance in Russian enterprises. J. Intellect. Cap. 2007, 8, 695–707. [Google Scholar] [CrossRef]

- Hsu, Y.-H.; Fang, W. Intellectual capital and new product development performance: The mediating role of organizational learning capability. Technol. Forecast. Soc. Chang. 2009, 76, 664–677. [Google Scholar] [CrossRef]

- Cabrilo, S. Overview of IC reporting models within Serbian industries. In Intellectual Capital in Organizations; Routledge: Abingdon upon Thames, UK, 2014. [Google Scholar]

- Edvinsson, L.; Malone, M. Intellectual Capital: Realizing Your Company’s True Value by Finding its Hidden Brainpower; Harper Business: New York, NY, USA, 1997. [Google Scholar]

- Subramaniam, M.; Youndt, M.A. The influence of intellectual capital on the types of innovative capabilities. Acad. Manag. J. 2005, 48, 450–463. [Google Scholar] [CrossRef] [Green Version]

- Roos, G.; Roos, J. Measuring your company’s intellectual performance. Long Range Plan. 1997, 30, 413–426. [Google Scholar] [CrossRef]

- Sveiby, K.E. Methods for Measuring Intangible Assets. 2010. Available online: https://www.sveiby.com/files/pdf/intangiblemethods.pdf (accessed on 5 November 2019).

- Pulic, A. Measuring the performance of intellectual potential in knowledge economy. In Proceedings of the 2nd McMaster Word Congress on Measuring and Managing Intellectual Capital by the Austrian Team for Intellectual Potential, Austria, February 1998; pp. 1–20. [Google Scholar]

- Aras, G.; Aybars, A.; Kutlu, O. The interaction between corporate social responsibility and value-added intellectual capital: Empirical evidence from Turkey. Social Responsib. J. 2011, 7, 622–637. [Google Scholar] [CrossRef]

- Abdulsalam, F.; Al-Qaheri, H.; Al-Khayyat, R. The intellectual capital performance of Kuwaiti banks: An application of VAIC model. ÎBusiness 2011, 3, 88–96. [Google Scholar] [CrossRef] [Green Version]

- McWilliams, A.; Siegel, D.S.; Wright, P.M. CSR: Strategic implications. J. Manag. Stud. 2006, 43, 1–18. [Google Scholar] [CrossRef] [Green Version]

- Freeman, R.E. Strategic Management: A Stakeholder Perspective; Cambridge University Press: Cambridge, UK, 1984. [Google Scholar]

- Aguinis, H.; Glavas, A. What we know and don’t know about corporate social responsibility: A review and research agenda. J. Manag. 2012, 38, 932–968. [Google Scholar] [CrossRef] [Green Version]

- Russo, A.; Perrini, F. Investigating stakeholder theory and social capital: CSR in large firms and SMEs. J. Bus. Ethics 2010, 91, 207–221. [Google Scholar] [CrossRef]

- Musibah, A.S.; Alfattani, W.S.B.W.Y. The mediating effect of financial performance on the relationship between Shariah supervisory board effectiveness, intellectual capital and corporate social responsibility, of Islamic banks in Gulf Cooperation Council countries. Asian Soc. Sci. 2014, 10, 139. [Google Scholar] [CrossRef] [Green Version]

- Asiaei, K.; Bontis, N. Using a balanced scorecard to manage corporate social responsibility. Know Process Manag. 2019, 26, 371–379. [Google Scholar] [CrossRef]

- Weber, O. Environmental, social and governance reporting in China. Bus. Strat. Environ. 2014, 23, 303–317. [Google Scholar] [CrossRef]

- Kocmanová, A.; Dočekalová, M. Construction of the economic indicators of performance in relation to environmental, social and corporate governance (ESG) factors. Acta Univ. Agric. Silvic. Mendel. Brun. 2013, 60, 195–206. [Google Scholar] [CrossRef] [Green Version]

- Iamandi, I.E.; Constantin, L.G.; Munteanu, S.M.; Cernat-Gruici, B. Mapping the ESG Behavior of European Companies. A holistic Kohonen approach. Sustainability 2019, 11, 3276. [Google Scholar] [CrossRef] [Green Version]

- Ruf, B.M.; Muralidhar, K.; Brown, R.M.; Janney, J.J.; Paul, K. An empirical investigation of the relationship between change in corporate social performance and financial performance: A stakeholder theory perspective. J. Bus. Ethics 2001, 32, 143–156. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Org. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Bird, R.; Hall, A.D.; Momentè, F.; Reggiani, F. What corporate social responsibility activities are valued by the market? J. Bus. Ethics 2007, 76, 189–206. [Google Scholar] [CrossRef]

- Brown, J.A.; Forster, W.R. CSR and stakeholder theory: A tale of Adam Smith. J. Bus. Ethics 2013, 112, 301–312. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Barnett, M.L. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Acad. Manag. Rev. 2007, 32, 794–816. [Google Scholar] [CrossRef]

- Frey, M.; Melis, M.; Vagnoni, E. Recent Developments in Social and Environmental Reporting among Italian Universities: A Critical Evaluation of Leading-edge Practices. In Civil Economy, Democracy, Transparency and Social and Environmental Accounting Research Role; Baldarelli, M.G., Ed.; McGraw-Hill: Milan, Italy, 2010; pp. 251–272. [Google Scholar]

- Tan, P.H.; Plowman, D.; Hancock, P. Intellectual capital and financial returns of companies. J. Intellect. Cap. 2007, 8, 76–95. [Google Scholar] [CrossRef]

- Ariff, A.H.M.; Islam, A.; Van Zijl, T. Intellectual capital and market performance: The case of multinational R&D firms in the US. J. Dev. Areas 2016, 50, 487–495. [Google Scholar]

- Wu, S.-H.; Lin, L.-Y.; Hsu, M.-Y. Intellectual capital, dynamic capabilities and innovative performance of organizations. Int. J. Technol. Manag. 2007, 39, 279–296. [Google Scholar] [CrossRef]

- Hsu, I.-C.; Sabherwal, R. Relationship between intellectual capital and knowledge management: An empirical investigation. Decis. Sci. 2012, 43, 489–524. [Google Scholar] [CrossRef]

- Holienka, M.; Pilková, A. Impact of intellectual capital and its components on firm performance before and after crisis. Electron. J. Knowl. Manag. 2014, 12, 261. [Google Scholar]

- Maditinos, D.; Šević, Z.; Tsairidis, C. Intellectual capital and business performance: An empirical study for the Greek listed companies. Eur. Res. Stud. J. 2010, 13, 145–167. [Google Scholar] [CrossRef] [Green Version]

- Sharabati, A.-A.A.; Jawad, S.N.; Bontis, N. Intellectual capital and business performance in the pharmaceutical sector of Jordan. Manag. Decis. 2010, 48, 105–131. [Google Scholar] [CrossRef]

- Kim, T.; Kim, W.G.; Park, S.S.S.; Lee, G.; Jee, B. Intellectual capital and business performance: What structural relationships do they have in upper-upscale hotels? Int. J. Tour. Res. 2012, 14, 391–408. [Google Scholar] [CrossRef]

- Firer, S.; Mitchell Williams, S. Intellectual capital and traditional measures of corporate performance. J. Intellect. Cap. 2003, 4, 348–360. [Google Scholar] [CrossRef]

- Carmeli, A.; Tishler, A. The relationships between intangible organizational elements and organizational performance. Strat. Manag. J. 2004, 25, 1257–1278. [Google Scholar] [CrossRef] [Green Version]

- Goh, P.C. Intellectual capital performance of commercial banks in Malaysia. J. Intellect. Cap. 2005, 6, 385–396. [Google Scholar]

- Barathi Kamath, G. The intellectual capital performance of the Indian banking sector. J. Intellect. Cap. 2007, 8, 96–123. [Google Scholar] [CrossRef]

- Ahmed, M.; Ahmed, N.; Luqman, M.; Arshad, A. Intellectual capital efficiency and the performance of mutual funds: A panel data analyses. Sci. Int. 2016, 28, 4867–4872. [Google Scholar]

- Mutuc, E.B.; Lee, J.S. Corporate Social Responsibility and Market-Adjusted Stock Returns: An Asian Perspective. Asia Pac. Soc. Sci. Rev. 2019, 19, 88–107. [Google Scholar]

- Kim, Y.; Park, M.S.; Wier, B. Is earnings quality associated with corporate social responsibility? Account. Rev. 2012, 87, 761–796. [Google Scholar] [CrossRef]

- Jain, P.; Vyas, V.; Roy, A. Exploring the mediating role of intellectual capital and competitive advantage on the relation between CSR and financial performance in SMEs. Soc. Responsib. J. 2017, 13, 1–23. [Google Scholar] [CrossRef]

- Khurshid, M.K.; Shaheer, H.; Nazir, N.; Waqas, M.; Kashif, M. Impact of corporate social responsibility on financial performance: The role of intellectual capital. City Univ. Res. J. 2016, 247–263. [Google Scholar]

- Pedrini, M. Human capital convergences in intellectual capital and sustainability reports. J. Intellect. Cap. 2007, 8, 346–366. [Google Scholar] [CrossRef]

- Janošević, S.; Dženopoljac, V.; Bontis, N. Intellectual capital and financial performance in Serbia. Know. Process. Manag. 2013, 20, 1–11. [Google Scholar] [CrossRef]

- Bontis, N. Assessing knowledge assets: A review of the models used to measure intellectual capital. Int. J. Manag. Rev. 2001, 3, 41–60. [Google Scholar] [CrossRef]

- Thomson Reuters. ESG Methodology. 2018. Available online: https://financial.thomsonreuters/com/content/dam/openweb/documents/pdf/financial/esg-scores-methodology.pdf (accessed on 8 July 2019).

- Chetty, S.; Naidoo, R.; Seetharam, Y. The impact of corporate social responsibility on firms’ financial performance in South Africa. Contemp. Econ. 2015, 9, 193–214. [Google Scholar] [CrossRef] [Green Version]

- Choi, J.S.; Kwak, Y.M.; Choe, C. Corporate social responsibility and corporate financial performance: Evidence from Korea. Austral. J. Manag. 2010, 35, 291–311. [Google Scholar] [CrossRef] [Green Version]

- McWilliams, A.; Siegel, D. Corporate social responsibility and financial performance: Correlation or misspecification? Strat. Manag. J. 2000, 21, 603–609. [Google Scholar] [CrossRef]

- Moore, G. Corporate social and financial performance: An investigation in the UK supermarket industry. J. Bus. Ethics 2001, 34, 299–315. [Google Scholar] [CrossRef]

- Tobin, J. A general equilibrium approach to monetary theory. J. Money Credit Bank. 1969, 1, 15–29. [Google Scholar] [CrossRef]

- Bayraktaroglu, A.E.; Calisir, F.; Baskak, M. Intellectual capital and firm performance: An extended VAIC model. J. Intellect. Cap. 2019, 20, 406–425. [Google Scholar] [CrossRef]

- Muhammad, N.M.N.; Ismail, M.K.A. Intellectual capital efficiency and firm’s performance: Study on Malaysian financial sectors. Int. J. Econ. Financ. 2009, 1, 206–212. [Google Scholar] [CrossRef]

- Zeghal, D.; Maaloul, A. Analyzing value added as an indicator of intellectual capital and its consequences on company performance. J. Intellect. Cap. 2010, 11, 39–60. [Google Scholar] [CrossRef] [Green Version]

- Sardo, F.; Serrasqueiro, Z. Intellectual capital, growth opportunities, and financial performance in European firms: Dynamic panel data analysis. J. Intellect. Cap. 2018, 19, 747–767. [Google Scholar] [CrossRef]

- Nazari, J.A.; Herremans, I.M. Extended VAIC model: Measuring intellectual capital components. J. Intellect. Cap. 2007, 8, 595–609. [Google Scholar] [CrossRef]

- Al-Matari, E.M.; Al-Swidi, A.K.; Fadzil, F.H.B. The moderating effect of board diversity on the relationship between executive committee characteristics and firm performance in Oman: Empirical study. Asian Soc. Sci. 2014, 10, 6–20. [Google Scholar]

- Khatab, H.; Masood, M.; Zaman, K.; Saleem, S.; Saeed, B. Corporate governance and firm performance: A case study of Karachi stock market. Int. J. Trade Econ. Financ. 2011, 2, 39–43. [Google Scholar] [CrossRef]

- Acquaah, M.; Chi, T. A longitudinal analysis of the impact of firm resources and industry characteristics on firm-specific profitability. J. Manag. Gov. 2007, 11, 179–213. [Google Scholar] [CrossRef] [Green Version]

- Kao, E.H.; Yeh, C.C.; Wang, L.H.; Fung, H.G. The relationship between CSR and performance: Evidence in China. Pac. Basin Financ. J. 2018, 51, 155–170. [Google Scholar] [CrossRef]

- Baron, R.M.; Kenny, D.A. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personal. Soc. Psychol. 1986, 51, 1173. [Google Scholar] [CrossRef]

{kind=link}

| Mean | SD | CSR | ENV | SOC | GOV | HCE | SCE | CEE | LEV | SIZE | RDI | ROA | TOBIN’S | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CSR | 47.62 | 11.79 | 1.00 | |||||||||||

| ENV | 53.35 | 16.49 | 0.87 *** | 1.00 | ||||||||||

| SOC | 56.04 | 14.45 | 0.93 *** | 0.82 *** | 1.00 | |||||||||

| GOV | 33.40 | 12.47 | 0.61 *** | 0.20 *** | 0.40 *** | 1.00 | ||||||||

| HCE | 11.23 | 39.56 | −0.04 | −0.08 | −0.05 | 0.06 | 1.00 | |||||||

| SCE | 7.12 × 10−7 | 0.00 | −0.09 | −0.17 *** | −0.13 ** | 0.11 ** | 0.93 *** | 1.00 | ||||||

| CEE | 0.48 | 0.21 | 0.15 *** | 0.19 *** | 0.17 *** | −0.02 | 0.25 *** | 0.16 *** | 1.00 | |||||

| LEV | 64.36 | 88.45 | 0.03 | −0.07 | −0.01 | 0.19 | −0.10 | −0.07 | −0.50 | 1.00 | ||||

| SIZE | 19.39 | 2.09 | 0.06 | 0.29 *** | 0.19 *** | −0.44 *** | −0.14 ** | −0.35 *** | −0.12 ** | 0.17 *** | 1.00 | |||

| RDI | 0.02 | 0.02 | 0.12 ** | 0.02 | 0.11 ** | 0.17 *** | −0.11 | −0.07 | −0.06 | 0.07 | −0.10 | 1.00 | ||

| ROA | 6.35 | 5.04 | 0.14 ** | 0.05 | 0.13 ** | 0.18 *** | 0.01 | 0.03 | 0.47 *** | −0.26 *** | −0.36 *** | 0.09 | 1.00 | |

| TOBIN’S | 1.52 × 10−3 | 1.78 × 10−3 | 0.11 ** | 0.09 | 0.10 | 0.09 | −0.01 | 0.03 | 0.47 *** | −0.35 *** | −0.32 *** | 0.15 ** | 0.75 *** | 1.00 |

| Model 1 | Model 2 | Model 3 | Model 4 | ||||

|---|---|---|---|---|---|---|---|

| (CSR) | (ROA) | (Tobin’s Q) | (CSR) | (CSR) | (CSR) | (CSR) | |

| HCE | −0.20 | −0.30 | −0.46 | −0.22 | −0.34 | ||

| (−0.94) | (−2.05) ** | (−3.17) *** | (−1.01) | (−1.57) | |||

| SCE | 0.18 | 0.19 | 0.41 | 0.19 | 0.30 | ||

| (0.80) | (1.25) | (2.77) *** | (0.84) | (1.35) | |||

| CEE | 0.19 | 0.44 | 0.29 | 0.21 | 0.28 | ||

| (2.67) *** | (8.85) *** | (6.01) *** | (2.65) *** | (3.69) *** | |||

| ROA | 0.05 | −0.05 | |||||

| (0.68) | (−0.62) | ||||||

| TOBIN’S | −0.18 | −0.29 | |||||

| (−2.22) ** | (−3.37) *** | ||||||

| LEV | 0.18 | −0.17 | −0.18 | 0.14 | 0.08 | 0.17 | 0.13 |

| (2.76) *** | (−3.67) *** | (−3.99) *** | (2.16) ** | (1.24) | (2.56) ** | (1.96) * | |

| SIZE | 0.17 | 0.00 | −0.05 | 0.08 | 0.03 | 0.17 | 0.15 |

| (1.73) * | (0.01) | (−0.80) | (1.08) | (0.41) | (1.73) * | (1.60) | |

| RDI | −0.01 | 0.09 | 0.09 | −0.02 | 0.00 | 0.00 | 0.02 |

| (−0.14) | (2.25) ** | (2.24) ** | (−0.28) | (0.05) | (−0.05) | (0.31) | |

| <Fixed effects> | |||||||

| Country | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Adjusted R² | 0.22 | 0.63 | 0.64 | 0.21 | 0.22 | 0.22 | 0.25 |

| Model 1 | Model 2 | Model 3 | Model 4 | ||||

|---|---|---|---|---|---|---|---|

| (ENV) | (ROA) | (Tobin’s Q) | (ENV) | (ENV) | (ENV) | (ENV) | |

| HCE | −0.28 | −0.30 | −0.46 | −0.29 | −0.38 | ||

| (−1.35) | (−2.05) ** | (−3.17) *** | (−1.39) | (−1.83) | |||

| SCE | 0.27 | 0.19 | 0.41 | 0.28 | 0.37 | ||

| (1.30) | (1.25) | (2.77) *** | (1.32) | (1.72) | |||

| CEE | 0.13 | 0.44 | 0.29 | 0.15 | 0.20 | ||

| (1.95) * | (8.85) *** | (6.01) *** | (1.91) * | (2.74) *** | |||

| ROA | 0.03 | −0.03 | |||||

| (0.48) | (−0.40) | ||||||

| TOBIN’S | −0.14 | −0.22 | |||||

| (−1.78) * | (−2.65) *** | ||||||

| LEV | 0.03 | −0.17 | −0.18 | 0.01 | −0.03 | 0.02 | −0.01 |

| (0.47) | (−3.67) *** | (−3.99) *** | (0.18) | (−0.57) | (0.37) | (−0.15) | |

| SIZE | 0.31 | 0.00 | −0.05 | 0.21 | 0.18 | 0.31 | 0.30 |

| (3.35) *** | (0.01) | (−0.80) | (2.97) *** | (2.42) ** | (3.35) *** | (3.26) *** | |

| RDI | −0.07 | 0.09 | 0.09 | (−0.07 | −0.06 | −0.07 | −0.05 |

| (−1.19) | (2.25) ** | (2.24) ** | (−1.22) | (−0.96) | (−1.13) | (−0.85) | |

| <Fixed effects> | |||||||

| Country | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Adjusted R² | 0.28 | 0.63 | 0.64 | 0.28 | 0.28 | 0.28 | 0.30 |

| Model 1 | Model 2 | Model 3 | Model 4 | ||||

|---|---|---|---|---|---|---|---|

| (SOC) | (ROA) | (Tobin’s Q) | (SOC) | (SOC) | (SOC) | (SOC) | |

| HCE | −0.36 | −0.30 | −0.46 | −0.35 | −0.45 | ||

| (−1.74) ** | (−2.05) ** | (−3.17) *** | (−1.68) * | (−2.15) ** | |||

| SCE | 0.33 | 0.19 | 0.41 | 0.33 | 0.41 | ||

| (1.57) | (1.25) | (2.77) *** | (1.53) | (1.94) ** | |||

| CEE | 0.25 | 0.44 | 0.29 | 0.24 | 0.31 | ||

| (3.65) *** | (8.85) *** | (6.01) *** | (3.06) *** | (4.26) *** | |||

| ROA | 0.14 | 0.03 | |||||

| (1.96) * | (0.37) | ||||||

| TOBIN’S | −0.07 | −0.20 | |||||

| (−0.92) | (−2.35) ** | ||||||

| LEV | 0.13 | −0.17 | −0.18 | 0.11 | 0.05 | 0.14 | 0.10 |

| (2.09) ** | (−3.67) *** | (−3.99) *** | (1.73) * | (0.74) | (2.12) ** | (1.51) | |

| SIZE | 0.39 | 0.00 | −0.05 | 0.26 | 0.22 | 0.39 | 0.38 |

| (4.19) *** | (0.01) | (−0.80) | (3.63) *** | (3.01) *** | (4.18) *** | (4.10) *** | |

| RDI | 0.01 | 0.09 | 0.09 | 0.00 | 0.02 | 0.01 | 0.03 |

| (0.26) | (2.25) ** | (2.24) ** | (0.00) | (0.31) | (0.21) | (0.57) | |

| <Fixed effects> | |||||||

| Country | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Adjusted R² | 0.28 | 0.63 | 0.64 | 0.26 | 0.25 | 0.27 | 0.29 |

| Model 1 | Model 2 | Model 3 | Model 4 | ||||

|---|---|---|---|---|---|---|---|

| (GOV) | (ROA) | (Tobin’s Q) | (GOV) | (GOV) | (GOV) | (GOV) | |

| HCE | 0.21 | −0.30 | −0.46 | 0.17 | 0.07 | ||

| (1.21) | (−2.05) ** | (−3.17) *** | (0.97) | (0.41) | |||

| SCE | −0.25 | 0.19 | 0.41 | −0.22 | −0.12 | ||

| (−1.40) | (1.25) | (2.77) *** | (−1.26) | (−0.70) | |||

| CEE | 0.07 | 0.44 | 0.29 | 0.13 | 0.16 | ||

| (1.25) | (8.85) *** | (6.01) *** | (2.02) ** | (2.71) *** | |||

| ROA | −0.06 | −0.13 | |||||

| (−0.98) | (−1.96) ** | ||||||

| TOBIN’S | −0.25 | −0.31 | |||||

| (−3.82) *** | (−4.47) *** | ||||||

| LEV | 0.32 | −0.17 | −0.18 | 0.26 | 0.21 | 0.30 | 0.27 |

| (6.06) *** | (−3.67) *** | (−3.99) *** | (4.96) *** | (4.27) *** | (5.54) *** | (5.06) *** | |

| SIZE | −0.40 | 0.00 | −0.05 | −0.37 | −0.41 | −0.40 | −0.42 |

| (−5.15) *** | (0.01) | (−0.80) | (−6.10) *** | (−6.91) *** | (−5.17) *** | (−5.52) *** | |

| RDI | 0.05 | 0.09 | 0.09 | 0.04 | 0.06 | 0.06 | 0.07 |

| (0.98) | (2.25) ** | (2.24) ** | (0.87) | (1.25) | (1.24) | (1.59) | |

| <Fixed effects> | |||||||

| Country | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Adjusted R² | 0.49 | 0.63 | 0.64 | 0.49 | 0.51 | 0.50 | 0.52 |

| Hypothesis | Results |

|---|---|

| H1a: There is a positive relationship between ICs and CSR. | |

| HCE and CSR, SCE and CSR | Reject |

| CEE and CSR | Accept |

| H1b: There is a positive relationship between ICs and ENV. | |

| HCE and ENV, SCE and ENV | Reject |

| CEE and ENV | Accept |

| H1c: There is a positive relationship between ICs and SOC. | |

| HCE and SOC, SCE and SOC | Reject |

| CEE and SOC | Accept |

| H1d: There is a positive relationship between ICs and GOV. | |

| HCE and GOV, SCE and GOV, CEE and GOV | Reject |

| H2: There is a positive relationship between ICs and financial performance. | |

| HCE and ROA, SCE and ROA | Reject |

| CEE and ROA | Accept |

| HCE and Tobin’s Q, SCE and Tobin’s Q | Reject |

| CEE and Tobin’s Q | Accept |

| H3a: The higher the financial performance, the higher will be the CSR ratings. | Reject |

| H3b: The higher the financial performance, the higher will be the ENV ratings. | Reject |

| H3c: The higher the financial performance, the higher will be the SOC ratings. | |

| ROA and SOC | Accept |

| Tobin’s Q and SOC | Reject |

| H3d: The higher the financial performance, the higher will be the GOV ratings. | Reject |

| H4a: Financial performance mediates the relationship between ICs and CSR. | |

| ROA mediation, HCE and CSR, SCE and CSR, CEE and CSR | Reject |

| Tobin’s Q mediation, HCE and CSR, SCE and CSR | Reject |

| CEE and CSR | Partially |

| H4b: Financial performance mediates the relationship between ICs and ENV. | |

| ROA mediation, HCE and ENV, SCE and ENV, CEE and ENV | Reject |

| Tobin’s Q mediation, HCE and ENV, SCE and ENV | Reject |

| CEE and ENV | Partially |

| H4c: Financial performance mediates the relationship between ICs and SOC. | |

| ROA mediation, HCE and SOC, SCE and SOC, CEE and SOC | Reject |

| Tobin’s Q mediation, HCE and SOC, SCE and SOC, CEE and SOC | Partially |

| H4d: Financial performance mediates the relationship between ICs and GOV. | |

| ROA mediation, HCE and GOV, SCE and GOV | Reject |

| CEE and GOV | Partially |

| Tobin’s Q mediation, HCE and GOV, SCE and GOV | Reject |

| CEE and GOV | Partially |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tsai, C.-H.; Mutuc, E.B. Evidence in Asian Food Industry: Intellectual Capital, Corporate Financial Performance, and Corporate Social Responsibility. Int. J. Environ. Res. Public Health 2020, 17, 663. https://doi.org/10.3390/ijerph17020663

Tsai C-H, Mutuc EB. Evidence in Asian Food Industry: Intellectual Capital, Corporate Financial Performance, and Corporate Social Responsibility. International Journal of Environmental Research and Public Health. 2020; 17(2):663. https://doi.org/10.3390/ijerph17020663

Chicago/Turabian StyleTsai, Cheng-Hung, and Eugene Burgos Mutuc. 2020. "Evidence in Asian Food Industry: Intellectual Capital, Corporate Financial Performance, and Corporate Social Responsibility" International Journal of Environmental Research and Public Health 17, no. 2: 663. https://doi.org/10.3390/ijerph17020663

APA StyleTsai, C. -H., & Mutuc, E. B. (2020). Evidence in Asian Food Industry: Intellectual Capital, Corporate Financial Performance, and Corporate Social Responsibility. International Journal of Environmental Research and Public Health, 17(2), 663. https://doi.org/10.3390/ijerph17020663