The Impact of Cigarette Excise Tax Increases on Regular Drinking Behavior: Evidence from China

Abstract

:1. Introduction

2. Materials and Methods

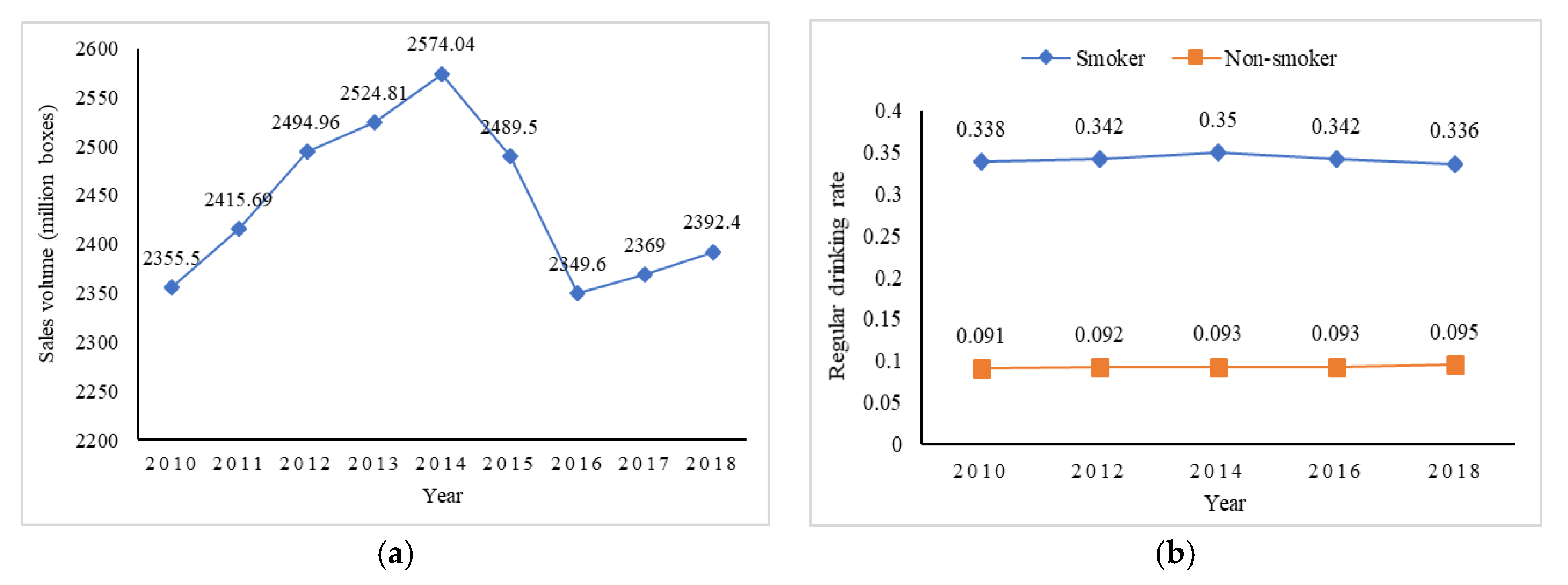

2.1. Background

2.2. Data

2.3. Methods

2.3.1. Theoretical Analysis of the Model Setting

2.3.2. Baseline Model

2.3.3. Model for the Mechanism Test

3. Results

3.1. t-Test for Data before and after the PSM

3.2. Estimation Results of PSM-DID

3.3. Mechanism Analysis

3.4. Heterogeneity Analysis

4. Discussion

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Ali, H.M.; James, S.M.; Donna, F.S.; Julie, L.G. Actual Causes of Death in the United States, 2000. JAMA 2004, 291, 1238–1245. [Google Scholar]

- Harwood, H. Updating Estimates of the Economic Costs of Alcohol Abuse in the United States Estimates, Update Methods, and Data; National Institute on Alcohol Abuse and Alcoholism: Rockville, MD, USA, 2000. [Google Scholar]

- Pelucchi, C.; Gallus, S.; Garavello, W.; Bosetti, C.; La Vecchia, C. Cancer risk associated with alcohol and tobacco use: Focus on upper aero-digestive tract and liver. Alcohol Res. Health 2006, 29, 193–198. [Google Scholar] [PubMed]

- Centers for Disease Control and Prevention. Annual smoking-attributable mortality, years of potential life lost, and economic costs—United States, 1995–1999. MMWR Morb. Mortal Wkly Rep. 2002, 51, 300–302. [Google Scholar]

- Medicine, I.O. Improving the Quality Ofhealth Care for Mental and Substance-Use Conditions; National Academy Press: Washington, DC, USA, 2006. [Google Scholar]

- Goodchild, M.; Zheng, R. Early assessment of China’s 2015 tobacco tax increase. Bull. World Health Organ. 2018, 96, 506–512. [Google Scholar] [CrossRef] [PubMed]

- Bask, M.; Melkersson, M. Rationally addicted to drinking and smoking? Appl. Econ. 2004, 36, 373–381. [Google Scholar] [CrossRef]

- Lisa, C.; Jenny, W. Cannabis, Alcohol and Cigarettes: Substitutes or Complements. Econ. Rec. 2001, 77, 19–34. [Google Scholar]

- Krauss, M.J.; Cavazos-Rehg, P.A.; Plunk, A.D.; Bierut, L.J.; Grucza, R.A. Effects of state cigarette excise taxes and smoke-free air policies on state per capita alcohol consumption in the United States, 1980 to 2009. Alcohol. Clin. Exp. Res. 2014, 38, 2630–2638. [Google Scholar] [CrossRef] [Green Version]

- Lee, J.M. The synergistic effect of cigarette taxes on the consumption of cigarettes, alcohol and betel nuts. BMC Public Health 2007, 121, 1–7. [Google Scholar] [CrossRef] [Green Version]

- Pierpaolo, P.; Silvia, T. Addiction and interaction between alcohol and tobacco consumption. Empir. Econ. 2009, 37, 1–23. [Google Scholar]

- Young-Wolff, K.C.; Hyland, A.J.; Desai, R.; Sindelar, J.; Pilver, C.E.; McKee, S.A. Smoke-free policies in drinking venues predict transitions in alcohol use disorders in a longitudinal U.S. sample. Drug Alcohol Depend. 2013, 128, 214–221. [Google Scholar] [CrossRef] [Green Version]

- Rajeev, K.G.; Mathew, J.M. The Interdependence of Cigarette and Liquor Demand. South. Econ. Assoc. 1995, 62, 9. [Google Scholar]

- Sandra, L.D.; Amy, E.S. Cigarettes and Alcohol: Substitutes or Complements? NBER Working Paper No. 7535; National Bureau of Economic Research: Cambridge, MA, USA, 2000. [Google Scholar]

- Picone, G.A.; Sloan, F.; Trogdon, J.G. The effect of the tobacco settlement and smoking bans on alcohol consumption. Health Econ. 2004, 13, 1063–1080. [Google Scholar] [CrossRef] [PubMed]

- Avram, A.; Nicolescu, A.-C.; Avram, C.D.; Dan, R.L. Financial Communication in the Context of Corporate Social Responsibility Growth. Amfiteatru Econ. 2019, 21, 623. [Google Scholar] [CrossRef]

- Cetin, T. The effect of taxation and regulation on cigarette smoking: Fresh evidence from Turkey. Health Policy 2017, 121, 1288–1295. [Google Scholar] [CrossRef] [PubMed]

- Heckman, J.J.; Ichimura, H.; Todd, P. Matching as an Econometric Evaluation Estimator. Rev. Econ. Stud. 1998, 65, 261–294. [Google Scholar] [CrossRef]

- Beck, T.; Levine, R.; Levkov, A. Big Bad Banks? The Winners and Losers from Bank Deregulation in the United States. J. Financ. 2010, 5, 1637–1667. [Google Scholar] [CrossRef] [Green Version]

- Marianne, B.; Esther, D.; Sendhil, M. How Much Should We Trust Differences-in-Differences Estimates? Q. J. Econ. 2004, 119, 1–27. [Google Scholar]

- James, C.A.; Fernando, E.-W. Epidemiologic analysis of alcohol and tobacco use. Alcohol Res. Health 2000, 24, 1–11. [Google Scholar]

- Lin, H.; Chang, C.; Liu, Z.; Zheng, Y. Subnational smoke-free laws in China. Tob. Induc. Dis. 2019, 17, 1–9. [Google Scholar] [CrossRef]

- Bobo, J.K.; Husten, C. Sociocultural influences on smoking and drinking. Alcohol Res. Health 2000, 24, 1–18. [Google Scholar]

- Grant, B.F.; Hasin, D.S.; Chou, S.P.; Stinson, F.S.; Dawson, D.A. Nicotine Dependence and Psychiatric Disorders in the United States. Arch. Gen. Psychiatry 2004, 61, 1107–1115. [Google Scholar] [CrossRef] [PubMed]

- Chinese Center for Disease Controland Prevention, China Adult Tobacco Survey Report. 2015. Available online: http://www.tcrc.org.cn/UploadFiles/2016-03/318/201603231215175500.pdf (accessed on 28 July 2019).

- Pampel, F.C. Cigarette use and the narrowing sex differential in mortality. Popul. Dev. Rev. 2002, 28, 77–104. [Google Scholar] [CrossRef]

- Silles, M. The causal effect of schooling on smoking behavior. Econ. Educ. Rev. 2015, 48, 102–116. [Google Scholar] [CrossRef]

- Mirowsky, J.; Ross, C.E. Education, learned effectiveness and health1. Lond. Rev. Educ. 2005, 3, 205–220. [Google Scholar] [CrossRef]

- Aristei, D.; Pieroni, L. Addiction, social interactions and gender differences in cigarette consumption. Empirica 2008, 36, 245–272. [Google Scholar] [CrossRef] [Green Version]

- Aristei, D.; Pieroni, L. Habits, Complementarities and Heterogeneity in Alcohol and Tobacco Demand: A Multivariate Dynamic Model. Oxf. Bull. Econ. Stat. 2010, 72, 428–457. [Google Scholar] [CrossRef]

- Ferrer, R.; Orehek, E.; Scheier, M.F.; O’Connell, M.E. Cigarette tax rates, behavioral disengagement, and quit ratios among daily smokers. J. Econ. Psychol. 2018, 66, 13–21. [Google Scholar] [CrossRef]

- Nesson, E. Heterogeneity in Smokers‘ Responses to Tobacco Control Policies. Health Econ. 2017, 26, 206–225. [Google Scholar] [CrossRef]

- Deborah, L.M.; Dominic, H.; Pebbles, F.; Sharon, R.; Constance, M.H. Unintended consequences of cigarette price changes for alcohol drinking behaviors across age groups_ evidence from pooled cross sections. Subst. Abus. Treat. Prev. Policy 2012, 7, 1–10. [Google Scholar]

{kind=link}

| Variables | N | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| Regulardrinker | 71,570 | 0.164 | 0.370 | 0 | 1 |

| Currentsmoker | 71,570 | 0.289 | 0.453 | 0 | 1 |

| Tax | 71,570 | 0.4 | 0.490 | 0 | 1 |

| Daysmokenum | 71,402 | 4.739 | 9.248 | 0 | 100 |

| Smokefree | 71,570 | 0.058 | 0.233 | 0 | 1 |

| Smokeyear | 71,570 | 9.017 | 15.518 | 0 | 76 |

| Male | 71,570 | 0.469 | 0.499 | 0 | 1 |

| Age | 71,570 | 49.752 | 13.769 | 16 | 94 |

| Urban | 71,216 | 0.456 | 0.498 | 0 | 1 |

| Marriage | 71,569 | 0.884 | 0.320 | 0 | 1 |

| Lnincome | 30,590 | 8.902 | 1.827 | 0 | 14.4 |

| Edu | 71,549 | 2.525 | 1.281 | 1 | 7 |

| Chronic | 71,557 | 0.177 | 0.382 | 0 | 1 |

| Part A. Test the Balancing Property for Each Observed Covariate | |||||||

| Variable | Unmatched | Mean | Bias% | t-Test | |||

| Matched | Smoker | Non-Smoker | Bias% | Reductbias% | t-Value | p-Value | |

| Gender | U | 0.965 | 0.247 | 216.9 | 80.47 | 0.000 | |

| M | 0.965 | 0.965 | 0.0 | 100.0 | −0.00 | 1.000 | |

| Age | U | 45.984 | 45.392 | 4.8 | 2.00 | 0.045 | |

| M | 45.987 | 46.116 | −1.0 | 78.2 | −0.38 | 0.706 | |

| Age2 | U | 2259.1 | 2223.1 | 3.2 | 1.32 | 0.187 | |

| M | 2259.8 | 2272.1 | −1.1 | 65.9 | −0.39 | 0.695 | |

| Edu | U | 2.619 | 2.537 | 6.7 | 2.76 | 0.006 | |

| M | 2.619 | 2.631 | −1.0 | 85.3 | −0.36 | 0.715 | |

| Lnincome | U | 8.925 | 8.428 | 33.9 | 13.73 | 0.000 | |

| M | 8.926 | 8.941 | −1.0 | 97.0 | −0.40 | 0.69 | |

| Urban | U | 0.406 | 0.454 | −9.7 | −4.13 | 0.000 | |

| M | 0.406 | 0.420 | −2.9 | 70.0 | −1.04 | 0.300 | |

| Marriage | U | 0.889 | 7.601 | −5.2 | −2.26 | 0.024 | |

| M | 0.889 | 7.671 | 1.2 | 77.2 | 0.40 | 0.686 | |

| Chronic | U | 0.118 | 0.156 | −10.9 | −4.51 | 0.000 | |

| M | 0.118 | 0.100 | 5.4 | 50.6 | 2.09 | 0.037 | |

| Part B. Test the overall balance | |||||||

| Sample | LR χ2 | p > χ2 | Meanbias | Medbias | |||

| Unmatched | 4482.79 | 0.000 | 36.4 | 8.2 | |||

| Matched | 6.27 | 0.617 | 1.7 | 1.1 | |||

| Variable | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Regulardrinker | Regulardrinker | Regulardrinker | Regulardrinker | Regulardrinker | |

| Tax × Currentsmoker | 0.133 ** | −0.00466 | −0.754 ** | −0.746 ** | −0.747 ** |

| (0.0672) | (0.200) | (0.354) | (0.355) | (0.359) | |

| Smokeyear | 0.0478 | 0.0943 * | 0.0903 * | 0.0861 * | |

| (0.0345) | (0.0493) | (0.0495) | (0.0501) | ||

| Smokefree | 0.720 | 1.081 * | 1.059 | 1.032 | |

| (0.455) | (0.654) | (0.654) | (0.661) | ||

| Lnincome | 0.0816 *** | 0.0582 ** | 0.0616 ** | ||

| (0.0287) | (0.0306) | (0.0310) | |||

| Age | 0.0218 | 0.0579 | |||

| (0.437) | (0.443) | ||||

| Age2 | −0.00170 *** | −0.00198 *** | |||

| (0.000601) | (0.000631) | ||||

| Edu | 0.0389 | ||||

| (0.160) | |||||

| Urban | −0.409 | ||||

| (0.266) | |||||

| Marriage | −0.484 * | ||||

| (0.263) | |||||

| Chronic | −0.476 *** | ||||

| (0.147) | |||||

| Individual Fixed | N | Y | Y | Y | Y |

| Time Fixed | N | Y | Y | Y | Y |

| N | 15815 | 6565 | 2549 | 2549 | 2530 |

| LR chi2 | 3.92 | 16.06 | 21.54 | 29.77 | 46.20 |

| Prob > chi2 | 0.0478 | 0.0246 | 0.0058 | 0.0009 | 0.0000 |

| Variable | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Regulardrinker | Regulardrinker | Regulardrinker | Regulardrinker | Regulardrinker | |

| Daysmokenum | 0.0904 *** | 0.0364 *** | 0.0400 *** | 0.0390 *** | 0.0394 *** |

| (0.0027) | (0.0033) | (0.0052) | (0.0053) | (0.0054) | |

| Tax | −0.0443 | −0.0388 | 0.0689 | 0.937 | 0.443 |

| (0.0380) | (0.0661) | (0.108) | (1.416) | (1.469) | |

| Daysmokenum × Tax | 0.0058 * | 0.0041 | −0.0163 ** | −0.0154 ** | −0.0162 ** |

| (0.0031) | (0.0036) | (0.00667) | (0.00670) | (0.0068) | |

| Smokeyear | 0.00362 | 0.0300 | 0.0301 | 0.0296 | |

| (0.0129) | (0.0206) | (0.0207) | (0.0210) | ||

| Smokefree | 0.164 | 0.301 | 0.302 | 0.312 | |

| (0.268) | (0.424) | (0.424) | (0.426) | ||

| Lnincome | 0.0738 *** | 0.0570 ** | 0.0583 ** | ||

| (0.0244) | (0.0255) | (0.0257) | |||

| Age | −0.0266 | 0.0607 | |||

| (0.181) | (0.187) | ||||

| Age2 | −0.000911 ** | −0.00120 *** | |||

| (0.000389) | (0.000411) | ||||

| Edu | −0.00901 | ||||

| (0.100) | |||||

| Urban | −0.418 ** | ||||

| (0.176) | |||||

| Marriage | −0.504 *** | ||||

| (0.174) | |||||

| Chronic | −0.388 *** | ||||

| (0.0924) | |||||

| Individual Fixed | N | Y | Y | Y | Y |

| Time Fixed | N | Y | Y | Y | Y |

| N | 71570 | 18390 | 6083 | 6083 | 5984 |

| LR chi2 | 143 | 90.01 | 89.25 | 95.15 | 125.01 |

| Prob > chi2 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Variable | Gender | Age Groups | |||

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | |

| Male | Female | 16–34 | 35–54 | 55– | |

| Currentsmoker × Tax | −0.780 ** | 0.119 | −0.0808 | −1.143 *** | −0.644 |

| (0.3630) | (0.0869) | (1.000) | (0.024) | (0.744) | |

| Control Variables | Y | Y | Y | Y | Y |

| Individual Fixed | Y | Y | Y | Y | Y |

| Time Fixed | Y | Y | Y | Y | Y |

| N | 2394 | 135 | 398 | 1065 | 594 |

| Wald chi2 | 47.56 | 5.41 | 18.54 | 37.72 | 25.10 |

| Prob > chi2 | 0.0000 | 0.0914 | 0.1832 | 0.0051 | 0.0336 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, Z.; Zheng, R. The Impact of Cigarette Excise Tax Increases on Regular Drinking Behavior: Evidence from China. Int. J. Environ. Res. Public Health 2020, 17, 3327. https://doi.org/10.3390/ijerph17093327

Zhang Z, Zheng R. The Impact of Cigarette Excise Tax Increases on Regular Drinking Behavior: Evidence from China. International Journal of Environmental Research and Public Health. 2020; 17(9):3327. https://doi.org/10.3390/ijerph17093327

Chicago/Turabian StyleZhang, Zili, and Rong Zheng. 2020. "The Impact of Cigarette Excise Tax Increases on Regular Drinking Behavior: Evidence from China" International Journal of Environmental Research and Public Health 17, no. 9: 3327. https://doi.org/10.3390/ijerph17093327

APA StyleZhang, Z., & Zheng, R. (2020). The Impact of Cigarette Excise Tax Increases on Regular Drinking Behavior: Evidence from China. International Journal of Environmental Research and Public Health, 17(9), 3327. https://doi.org/10.3390/ijerph17093327