Will the Volume-Based Procurement Policy Promote Pharmaceutical Firms’ R&D Investment in China? An Event Study Approach

Abstract

:1. Introduction

2. Theory and Hypothesis

2.1. “4 + 7” Volume-Based Procurement Policy

2.2. R&D Investment and Market Reaction during the Introduction of the “4 + 7” Procurement Policy

3. Research Design

3.1. Sample Selection and Data

3.2. Variables

3.2.1. Dependent Variable

- Firm value

- Event day

- Event window

- Estimation model

- Significance test

3.2.2. Independent Variables

3.2.3. Control Variables

3.2.4. Regression Model

4. Results

4.1. Descriptive Statistics

4.2. Main Effect

4.3. Robustness Check

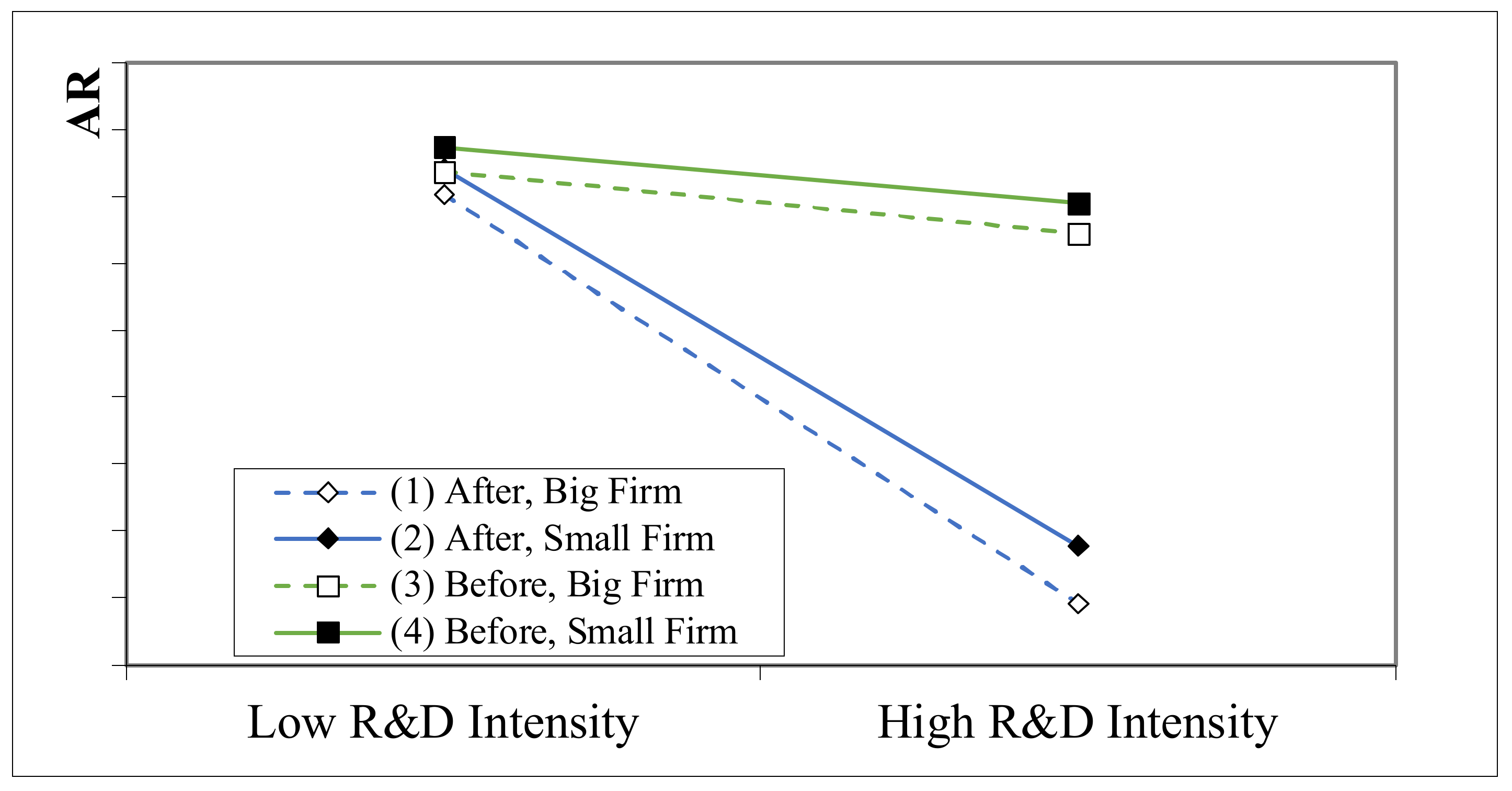

4.4. Further Study

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Askfors, Y.; Fornstedt, H. The Clash of Managerial and Professional Logics in Public Procurement: Implications for Innovation in the Health-Care Sector. Scand. J. Manag. 2018, 34, 78–90. [Google Scholar] [CrossRef]

- Georghiou, L.; Edler, J.; Uyarra, E.; Yeow, J. Policy Instruments for Public Procurement of Innovation: Choice, Design and Assessment. Technol. Forecast. Soc. Chang. 2014, 86, 1–12. [Google Scholar] [CrossRef]

- Meehan, J.; Menzies, L.; Michaelides, R. The Long Shadow of Public Policy; Barriers to a Value-Based Approach in Healthcare Procurement. J. Purch. Supply Manag. 2017, 23, 229–241. [Google Scholar] [CrossRef]

- Miller, F.A.; Lehoux, P. The Innovation Impacts of Public Procurement Offices: The Case of Healthcare Procurement. Res. Policy 2020, 49, 104075. [Google Scholar] [CrossRef]

- Boon, W.; Edler, J. Demand, Challenges, and Innovation. Making Sense of New Trends in Innovation Policy. Sci. Public Policy 2018, 45, 435–447. [Google Scholar] [CrossRef] [Green Version]

- OECD Public Procurement for Innovation: Good Practices and Strategies; OECD Public Governance Reviews; OECD Publishing: Paris, France, 2017.

- Uyarra, E.; Zabala-Iturriagagoitia, J.M.; Flanagan, K.; Magro, E. Public Procurement, Innovation and Industrial Policy: Rationales, Roles, Capabilities and Implementation. Res. Policy 2020, 49, 103844. [Google Scholar] [CrossRef]

- Chen, M.; Cong, L.; He, J.; Yang, Y.; Xu, Y.; Tang, M.; Jin, C. Prospects for Development of Group Purchasing Organizations (GPOs) in China within the Context of National Centralized Drug Procurement. Drug Discov. Ther. 2020, 3, 145–148. [Google Scholar] [CrossRef] [PubMed]

- Li, X. Game among stakeholders in the implementation of centralized drug procurement reform: Challenges and countermeasures. Chin. J. Hosp. Adm. 2016, 32, 518–521. [Google Scholar]

- Meyer, J.C.; Schellack, N.; Stokes, J.; Lancaster, R.; Zeeman, H.; Defty, D.; Godman, B.; Steel, G. Ongoing Initiatives to Improve the Quality and Efficiency of Medicine Use within the Public Healthcare System in South Africa; A Preliminary Study. Front. Pharmacol. 2017, 8, 751. [Google Scholar] [CrossRef] [Green Version]

- Parkinson, B.; Sermet, C.; Clement, F.; Crausaz, S.; Godman, B.; Garner, S.; Choudhury, M.; Pearson, S.-A.; Viney, R.; Lopert, R.; et al. Disinvestment and Value-Based Purchasing Strategies for Pharmaceuticals: An International Review. Pharmacoeconomics 2015, 33, 905–924. [Google Scholar] [CrossRef] [Green Version]

- Bilgin, M.H.; Danis, H.; Demir, E.; Can, U. Eurasian Economic Perspectives: Proceedings of the 22nd Eurasia Business and Economics Society Conference; Springer International Publishing: Cham, Switzerland, 2019; ISBN 978-3-030-11833-4. [Google Scholar]

- Stargardt, T.; Busse, R.; Dauben, H.-P. PPRI Pharma Profile Germany 2008. Pharmaceutical Pricing and Reimbursement Information. 2008. [Google Scholar]

- Weinstein, L. The Role of Group Purchasing Organizations (GPOs) in the U.S. Medical Industry Supply Chain. Estud. De Econ. Apl. 2006, 24, 789–801. [Google Scholar]

- Zhang, Y.; Fang, L. Research on the Development and Reform of Centralized Drug Procurement System. China Pharm. 2020, 31, 2561–2566. [Google Scholar]

- Chen, L.; Yang, Y.; Luo, M.; Hu, B.; Yin, S.; Mao, Z. The Impacts of National Centralized Drug Procurement Policy on Drug Utilization and Drug Expenditures: The Case of Shenzhen, China. Int. J. Environ. Res. Public Health 2020, 17, 9415. [Google Scholar] [CrossRef]

- Tang, M.; He, J.; Chen, M.; Cong, L.; Xu, Y.; Yang, Y.; Hou, Z.; Song, P.; Jin, C. “4 + 7” City Drug Volume-Based Purchasing and Using Pilot Program in China and Its Impact. Drug Discov. Ther. 2019, 13, 365–369. [Google Scholar] [CrossRef] [PubMed]

- Wang, N.; Yang, Y.; Xu, L.; Mao, Z.; Cui, D. Influence of Chinese National Centralized Drug Procurement on the Price of Policy-Related Drugs: An Interrupted Time Series Analysis. Preprints 2021. [Google Scholar] [CrossRef] [PubMed]

- Sunshine Medical Procurement. Available online: http://www.smpaa.cn/gjsdcg/2018/11/15/8511.shtml (accessed on 16 April 2021).

- The State Concil of People’s Republic of China Notice on the Pilot Program of the State-Organized Centralized Procurement and Use of Drugs. Available online: http://www.gov.cn/zhengce/content/2019-01/17/content_5358604.htm (accessed on 22 March 2021).

- Yang, Y.; Chen, L.; Ke, X.; Mao, Z.; Zheng, B. The Impacts of Chinese Drug Volume-Based Procurement Policy on the Use of Policy-Related Antibiotic Drugs in Shenzhen, 2018–2019: An Interrupted Time-Series Analysis. BMC Health Serv. Res. 2021, 21, 668. [Google Scholar] [CrossRef]

- The Joint Procurement Office. Available online: http://www.yyzbsw.sh.cn/gjsdcg/2021/02/08/9889.shtml (accessed on 14 November 2021).

- Lu, J.; Yang, Y.; Wen, X.; Wang, J.; Shen, Y.; Mao, L.; Cui, D.; Mao, Z.; Li, J. Implementation and Impact of National Centralized Drug Procurement Policy in China: Evidence from the National Drug Procurement Database. 2021; in review. [Google Scholar]

- Zimon, G. Influence of Group Purchasing Organizations on Financial Situation of Polish SMEs. Oeconomia Copernic. 2018, 9, 87–104. [Google Scholar] [CrossRef]

- Knutsson, H.; Thomasson, A. Innovation in the Public Procurement Process: A Study of the Creation of Innovation-Friendly Public Procurement. Public Manag. Rev. 2014, 16, 242–255. [Google Scholar] [CrossRef]

- Cai, X. The evolution of the Chinese centralized drug procurement and its logical relationship with medical insurance payment. Chin. J. Health Policy 2017, 10, 6–12. [Google Scholar]

- Wang, J.; Yang, Y.; Xu, L.; Shen, Y.; Wen, X.; Mao, L.; Wang, Q.; Cui, D.; Mao, Z. The Impact of National Centralized Drug Procurement Policy on the Use of Policy-Related Original and Generic Drugs in Public Medical Institutions in China: A Difference-in-Difference Analysis Based on National Database. medRxiv 2021, preprints. [Google Scholar] [CrossRef]

- Zimon, G. The Influence of a Branch Group Purchasing Organization on the Development of Small and Medium-Sized Enterprises. In Eurasian Business Perspectives; Bilgin, M.H., Danis, H., Demir, E., Can, U., Eds.; Springer International Publishing: Cham, Switzerland, 2019; pp. 145–153. [Google Scholar]

- Zimon, G.; Sobolewski, M.; Lew, G. An Influence of Group Purchasing Organizations on Financial Security of SMEs Operating in the Renewable Energy Sector—Case for Poland. Energies 2020, 13, 2926. [Google Scholar] [CrossRef]

- Bruhn, W.E.; Fracica, E.A.; Makary, M.A. Group Purchasing Organizations, Health Care Costs, and Drug Shortages. JAMA 2018, 320, 1859–1860. [Google Scholar] [CrossRef] [PubMed]

- Dalpé, R. Effects of Government Procurement on Industrial Innovation. Technol. Soc. 1994, 16, 65–83. [Google Scholar] [CrossRef]

- Kundu, O.; James, A.D.; Rigby, J. Public Procurement and Innovation: A Systematic Literature Review. Sci. Public Policy 2020, 47, 490–502. [Google Scholar] [CrossRef]

- Baumol, W.J. Contestable Markets: An Uprising in the Theory of Industry Structure. In Microtheory: Applications and Origins; MIT Press: Cambridge, MA, USA, 1986; ISBN 978-0-262-02245-3. [Google Scholar]

- Cui, H.; Mak, Y.T. The Relationship between Managerial Ownership and Firm Performance in High R&D Firms. J. Corp. Financ. 2002, 8, 313–336. [Google Scholar] [CrossRef]

- Honoré, F.; Munari, F.; van Pottelsberghe de La Potterie, B. Corporate Governance Practices and Companies’ R&D Intensity: Evidence from European Countries. Res. Policy 2015, 44, 533–543. [Google Scholar] [CrossRef]

- Chen, D.; Khan, S.; Yu, X.; Zhang, Z. Government Intervention and Investment Comovement: Chinese Evidence. J. Bus. Financ. Account. 2013, 40, 564–587. [Google Scholar] [CrossRef]

- Rao, N. Do Tax Credits Stimulate R&D Spending? The Effect of the R&D Tax Credit in Its First Decade. J. Public Econ. 2016, 140, 1–12. [Google Scholar] [CrossRef]

- Fama, E.F. Market Efficiency, Long-Term Returns, and Behavioral FInance. J. Financ. Econ. 1998, 49, 283–306. [Google Scholar] [CrossRef]

- Castro-Iragorri, C. Does the Market Model Provide a Good Counterfactual for Event Studies in Finance? Financ. Mark Portf Manag. 2019, 33, 71–91. [Google Scholar] [CrossRef]

- Martin, K.D.; Borah, A.; Palmatier, R.W. Data Privacy: Effects on Customer and Firm Performance. J. Mark. 2017, 81, 36–58. [Google Scholar] [CrossRef] [Green Version]

- Fasan, M.; Zaro, E.S.; Zaro, C.S.; Porco, B.; Tiscini, R. An Empirical Analysis: Did Green Supply Chain Management Alleviate the Effects of COVID-19? Bus. Strategy Environ. 2021. [Google Scholar] [CrossRef]

- Zhang, Y.; Wang, H.; Zhou, X. Dare to Be Different? Conformity Versus Differentiation in Corporate Social Activities of Chinese Firms and Market Responses. AMJ 2020, 63, 717–742. [Google Scholar] [CrossRef]

- Sunshine Medical Procurement. Available online: http://www.yyzbsw.sh.cn/gjsdcg/2018/11/14/8508.shtml (accessed on 14 November 2021).

- The Joint Procurement Office. Available online: http://www.yyzbsw.sh.cn/gjsdcg/2018/11/15/8511.shtml (accessed on 14 November 2021).

- The Joint Procurement Office. Available online: http://www.yyzbsw.sh.cn/gjsdcg/2018/12/07/8531.shtml (accessed on 14 November 2021).

- McWilliams, A.; Siegel, D. Event Studies in Management Research: Theoretical and Empirical Issues. AMJ 1997, 40, 626–657. [Google Scholar] [CrossRef]

- Godfrey, P.C.; Merrill, C.B.; Hansen, J.M. The Relationship between Corporate Social Responsibility and Shareholder Value: An Empirical Test of the Risk Management Hypothesis. Strateg. Manag. J. 2009, 30, 425–445. [Google Scholar] [CrossRef]

- Szücs, F. M&A and R&D: Asymmetric Effects on Acquirers and Targets? Res. Policy 2014, 43, 1264–1273. [Google Scholar] [CrossRef] [Green Version]

- Johnson, L.D.; Pazderka, B. Firm Value and Investment in R&D. Manag. Decis. Econ. 1993, 14, 15–24. [Google Scholar] [CrossRef]

- Tyagi, S.; Nauriyal, D.K.; Gulati, R. Firm Level R&D Intensity: Evidence from Indian Drugs and Pharmaceutical Industry. Rev. Manag. Sci. 2018, 12, 167–202. [Google Scholar] [CrossRef]

- Stuart, E.A. Matching Methods for Causal Inference: A Review and a Look Forward. Stat. Sci. 2010, 25, 1–21. [Google Scholar] [CrossRef] [Green Version]

- Chauvin, K.W.; Hirschey, M. Advertising, R&D Expenditures and the Market Value of the Firm. Financ. Manag. 1993, 22, 128–140. [Google Scholar] [CrossRef]

- Aiken, L.S.; West, S.G.; Reno, R.R. Multiple Regression: Testing and Interpreting Interactions; SAGE: Thousand Oaks, CA, USA, 1991; ISBN 978-0-7619-0712-1. [Google Scholar]

{kind=link}

| Event Window | CAR | t-Value |

|---|---|---|

| (−10, 0) | −0.0396 *** | −9.680 |

| (−10, 1) | −0.0478 *** | −10.500 |

| (−10, 2) | −0.0468 *** | −9.750 |

| (−10, 3) | −0.0516 *** | −10.550 |

| (−10, 4) | −0.0566 *** | −11.720 |

| (−10, 5) | −0.0673 *** | −13.010 |

| (−10, 6) | −0.0726 *** | −14.000 |

| (−10, 7) | −0.0672 *** | −13.200 |

| (−10, 8) | −0.0739 *** | −13.980 |

| (−10, 9) | −0.0617 *** | −11.800 |

| (−10, 10) | −0.0578 *** | −10.720 |

| (−5, 0) | −0.0123 ** | −3.540 |

| (−5, 1) | −0.0205 *** | −5.490 |

| (−5, 2) | −0.0196 *** | −4.900 |

| (−5, 3) | −0.0246 *** | −5.910 |

| (−5, 4) | −0.0300 *** | −7.270 |

| (−5, 5) | −0.0405 *** | −9.070 |

| (−2, 0) | −0.0246 *** | −8.350 |

| (−2, 1) | −0.032 *** | −9.920 |

| (−2, 2) | −0.0320 *** | −8.900 |

| (−2, 3) | −0.0371 *** | −9.860 |

| (−2, 4) | −0.0427 *** | −11.430 |

| (−2, 5) | −0.0531 *** | −12.480 |

| (−2, 6) | −0.0586 *** | −13.400 |

| (−2, 7) | −0.0532 *** | −12.440 |

| (−2, 8) | −0.0598 *** | −12.890 |

| (−2, 9) | −0.0476 *** | −10.070 |

| (−2, 10) | −0.0435 *** | −8.560 |

| (−1, 0) | −0.0317 *** | −11.460 |

| (−1, 1) | −0.0400 *** | −12.580 |

| (−1, 2) | −0.0392 *** | −11.420 |

| (−1, 3) | −0.0443 *** | −12.070 |

| (−1, 4) | −0.0499 *** | −13.910 |

| (−1, 5) | −0.0604 *** | −14.650 |

| (−1, 6) | −0.0659 *** | −15.430 |

| (−1, 7) | −0.0606 *** | −14.310 |

| (−1, 8) | −0.0672 *** | −14.410 |

| (−1, 9) | −0.0550 *** | −11.560 |

| (−1, 10) | −0.0509 *** | −9.950 |

| Variable Type | Variables | Variable Name | Description |

|---|---|---|---|

| Dependent Variable | Firm value | AR | The CAR during the event window (−10,10) |

| Independent Variables | Treatment variable | Treat | Dummy variable, coded as 1 if R&D intensity of the firm is above 75% percentile, and 0 otherwise |

| Time variable | Post | Dummy variable, coded as 1 if a firm is observed after 7 December 2018 | |

| R&D intensity | RDI | R&D input/Sales revenue (2017) | |

| Proportion of R&D personnel | RDPI | Number of R&D personnel/total number of employees (2017) | |

| Control Variables | Firm age | AGE | Time since establishment of the company (2017) |

| Tobin’s Q | Tobinsq | Market value/Asset value (2017) | |

| ROA | ROA | Net profit/Total asset (2017) | |

| Debt to asset ratio | Lev | Debt/Asset (2017) | |

| Liquidity ratio | Cash Ratio | Cash and cash equivalents/current liabilities (2017) | |

| Return on fixed asset | ROF | Net profit/fixed asset (2017) | |

| Return on investment | ROI | Investment return/(Long-term equity investment + held-to-maturity investment + transactional financial assets + available-for-sale financial assets + derivative financial assets) (2017) | |

| Bid winner | Target | 1, if the firm won the bid on 7 December 2018; 0 otherwise | |

| Certificated high-tech | Tech | 1, if the firm is certificated high-tech firm according to the government; 0 otherwise (2017) | |

| Generic drug concept stock | AND | 1, if the firm is a generic drug concept stock; 0, otherwise (2017) | |

| Innovative drug concept stock | ID | 1, if the firm is an innovative drug concept stock; 0 otherwise (2017) | |

| Firm ownership | Ownership | 1, if the firm is state-owned; 0, otherwise (2017) | |

| Firm size | SIZE | Natural logarithm of total asset (2017) |

| Panel A: Logit Model Used to Find Propensity Scores | ||||

| Variables | Independent Variable = Treat | |||

| AGE | −0.030 ** (0.015) | |||

| Tobinsq | 484.308 *** (43.716) | |||

| ROA | 1.607 (1.682) | |||

| Lev | 0.112 ** (0.035) | |||

| Cash Ratio | −0.980 *** (0.194) | |||

| ROF | 0.104 *** (0.036) | |||

| ROI | −0.432 *** (0.195) | |||

| Ownership | −0.577 *** (0.186) | |||

| SIZE | 0.777 *** (0.194) | |||

| Constant | −9.331 *** (1.840) | |||

| N | 1550 | |||

| Pseudo R2 | 0.15 | |||

| Panel B: Test of the effectiveness of the propensity score matches | ||||

| Variable | Average, Treated group | Average, Control group | % bias | t-test |

| AGE | 18.5 | −0.000 | −3.4 | −0.66 |

| Tobinsq | 0.003 | 18.421 | −3.3 | −0.60 |

| ROA | 0.088 | 0.003 | −3.4 | 0.48 |

| Lev | 0.275 | 0.082 | 9.0 | 1.71 * |

| Cash Ratio | 1.527 | 3.455 | 9.6 | 1.84 * |

| ROF | 0.564 | 1.579 | −2.3 | −0.47 |

| ROI | 0.745 | 0.101 | 3.1 | 0.57 |

| Ownership | 0.142 | 0.728 | −1.7 | −0.35 |

| SIZE | 9.565 | 0.147 | −6.0 | −1.15 |

| Variables | Full Sample | Treated Group | Control Group | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| N | Mean | SD | Min | Max | N | Mean | SD | Min | Max | N | Mean | SD | Min | Max | |

| AR | 3948 | −0.003 | 0.02 | −0.116 | 0.109 | 739 | −0.004 | 0.023 | −0.101 | 0.098 | 2423 | −0.002 | 0.019 | −0.116 | 0.106 |

| Treat | 3948 | 0.266 | 0.442 | 0 | 1 | 739 | 1 | 0 | 1 | 1 | 2423 | 0 | 0 | 0 | 0 |

| RDI | 3864 | 5.624 | 5.293 | 0.035 | 49.87 | 718 | 11.62 | 8.357 | 6.75 | 49.87 | 2423 | 3.647 | 1.618 | 0.035 | 6.64 |

| AGE | 3906 | 18.76 | 4.7 | 7.699 | 36.48 | 739 | 18.5 | 4.978 | 9.866 | 36.48 | 2423 | 19.28 | 4.471 | 7.953 | 29.85 |

| Tobinsq | 3948 | 0.003 | 0.002 | 0 | 0.017 | 739 | 0.003 | 0.003 | 0 | 0.012 | 2423 | 0.002 | 0.002 | 0 | 0.013 |

| ROA | 3906 | 0.078 | 0.058 | −0.245 | 0.34 | 739 | 0.088 | 0.066 | −0.095 | 0.282 | 2423 | 0.073 | 0.059 | −0.245 | 0.34 |

| Lev | 3906 | 0.281 | 0.158 | 0.042 | 0.886 | 739 | 0.275 | 0.144 | 0.042 | 0.636 | 2423 | 0.3 | 0.166 | 0.045 | 0.886 |

| Cash Ratio | 3906 | 1.299 | 1.955 | 0.017 | 19.04 | 739 | 1.527 | 3.217 | 0.063 | 19.04 | 2423 | 1.073 | 1.253 | 0.017 | 7.058 |

| ROF | 3906 | 0.571 | 0.649 | −0.81 | 4.583 | 739 | 0.564 | 0.535 | −0.645 | 2.176 | 2423 | 0.497 | 0.538 | −0.81 | 3.2 |

| ROI | 3255 | 0.576 | 1.794 | −0.729 | 14.57 | 739 | 0.745 | 2.48 | −0.252 | 14.57 | 2423 | 0.541 | 1.56 | −0.729 | 10.58 |

| Target | 3948 | 0.032 | 0.176 | 0 | 1 | 739 | 0.114 | 0.318 | 0 | 1 | 2423 | 0.017 | 0.131 | 0 | 1 |

| Tech | 3906 | 0.253 | 0.435 | 0 | 1 | 739 | 0.256 | 0.437 | 0 | 1 | 2423 | 0.243 | 0.429 | 0 | 1 |

| AND | 3948 | 0.117 | 0.321 | 0 | 1 | 739 | 0.242 | 0.429 | 0 | 1 | 2423 | 0.078 | 0.268 | 0 | 1 |

| ID | 3948 | 0.277 | 0.447 | 0 | 1 | 739 | 0.441 | 0.497 | 0 | 1 | 2423 | 0.26 | 0.439 | 0 | 1 |

| Ownership | 3906 | 0.188 | 0.391 | 0 | 1 | 739 | 0.142 | 0.349 | 0 | 1 | 2423 | 0.243 | 0.429 | 0 | 1 |

| SIZE | 3906 | 9.519 | 0.435 | 8.787 | 10.79 | 739 | 9.565 | 0.47 | 8.801 | 10.79 | 2423 | 9.609 | 0.413 | 8.787 | 10.55 |

| Variables | 1 | 2 | 3 | 4 | 5 | 6 | 7 | |

|---|---|---|---|---|---|---|---|---|

| 1. AR | 1.000 | |||||||

| 2. Treat | −0.041 * | 1.000 | ||||||

| 3. AGE | 0.003 | −0.072 *** | 1.000 | |||||

| 4. Tobinsq | −0.008 | 0.299 *** | −0.085 *** | 1.000 | ||||

| 5. ROA | −0.011 | 0.103 *** | 0.089 *** | 0.453 *** | 1.000 | |||

| 6. Lev | −0.021 | −0.067 *** | 0.194 *** | −0.417 *** | −0.390 *** | 1.000 | ||

| 7. Cash Ratio | 0.009 | 0.100 *** | −0.079 *** | 0.262 *** | 0.317 *** | −0.429 *** | 1.000 | |

| 8. ROF | 0.006 | 0.052 ** | 0.053 ** | 0.481 *** | 0.768 *** | −0.341 *** | 0.341 *** | |

| 9. ROI | −0.040 * | 0.047 ** | 0.124 *** | 0.033 | 0.393 *** | −0.046 ** | 0.127 *** | |

| 10. Target | −0.022 | 0.208 *** | −0.090 *** | −0.014 | 0.049 ** | 0.035 | −0.027 | |

| 11. Tech | −0.005 | 0.013 | −0.124 *** | 0.116 *** | −0.009 | −0.122 *** | −0.086 *** | |

| 12. AND | -0.033 | 0.217 *** | 0.014 | −0.061 *** | 0.032 | 0.097 *** | −0.069 *** | |

| 13. ID | 0.009 | 0.167 *** | −0.110 *** | −0.063 *** | −0.037* | 0.106 *** | −0.118 *** | |

| 14. Ownership | −0.015 | −0.103 *** | 0.180 *** | −0.127 *** | −0.049 ** | 0.203 *** | 0.001 | |

| 15. SIZE | −0.033 | −0.044 * | 0.163 *** | −0.327 *** | 0.030 | 0.423 *** | −0.218 *** | |

| 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | |

| 8. ROF | 1.000 | |||||||

| 9. ROI | 0.248 *** | 1.000 | ||||||

| 10. Target | 0.051 ** | −0.009 | 1.000 | |||||

| 11. Tech | −0.119 *** | 0.027 | −0.116 *** | 1.000 | ||||

| 12. AND | 0.026 | 0.029 | 0.455 *** | −0.207 *** | 1.000 | |||

| 13. ID | −0.066 *** | −0.019 | 0.088 *** | 0.027 | 0.236 *** | 1.000 | ||

| 14. Ownership | 0.024 | 0.142 *** | −0.108 *** | −0.191 *** | −0.092 *** | −0.174 *** | 1.000 | |

| 15. SIZE | 0.106 *** | 0.059 *** | 0.115 *** | −0.332 *** | 0.274 *** | 0.241 *** | 0.227 *** | 1.000 |

| Variables | VIF | 1/VIF |

|---|---|---|

| ROA | 2.35 | 0.425 |

| ROF | 1.96 | 0.510 |

| Lev | 1.80 | 0.556 |

| SIZE | 1.77 | 0.564 |

| Tobinsq | 1.65 | 0.606 |

| AND | 1.46 | 0.686 |

| Cash Ratio | 1.40 | 0.712 |

| Target | 1.31 | 0.763 |

| Treat | 1.30 | 0.768 |

| ROI | 1.28 | 0.779 |

| ID | 1.24 | 0.803 |

| Ownership | 1.23 | 0.812 |

| Tech | 1.21 | 0.829 |

| AGE | 1.14 | 0.878 |

| Mean VIF | 1.51 | |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| AR | AR | AR | AR | AR | AR | |

| AGE | 0.0045 | 0.0064 | 0.0046 | 0.0022 | 0.0019 | 0.0020 |

| (0.007) | (0.007) | (0.007) | (0.006) | (0.006) | (0.006) | |

| Tobinsq | −44.7663 ** | −29.1016 | −39.7596 * | −39.2848 ** | −29.5914 | −30.3089 |

| (21.427) | (18.280) | (21.694) | (18.664) | (19.289) | (19.329) | |

| ROA | 0.0976 | −0.5764 | 0.0714 | −0.0707 | −0.0498 | −0.0212 |

| (0.777) | (0.746) | (0.783) | (0.683) | (0.687) | (0.683) | |

| Lev | −0.1204 | −0.1511 | −0.1066 | −0.1326 | −0.1255 | −0.1289 |

| (0.211) | (0.177) | (0.213) | (0.181) | (0.181) | (0.180) | |

| Cash Ratio | −0.0121 | 0.0009 | −0.0090 | −0.0079 | −0.0043 | −0.0046 |

| (0.023) | (0.012) | (0.023) | (0.019) | (0.019) | (0.019) | |

| ROF | 0.2279 ** | 0.1733 ** | 0.2255 ** | 0.2036 ** | 0.1888 ** | 0.1875 ** |

| (0.094) | (0.083) | (0.096) | (0.086) | (0.086) | (0.086) | |

| ROI | −0.0630 *** | −0.0432 *** | −0.0618 *** | −0.0609 *** | −0.0595 *** | −0.0593 *** |

| (0.021) | (0.011) | (0.021) | (0.018) | (0.018) | (0.018) | |

| Target | −0.1440 | −0.0611 | −0.1160 | −0.1465 | −0.1048 | −0.1091 |

| (0.199) | (0.099) | (0.197) | (0.156) | (0.157) | (0.156) | |

| Tech | −0.0273 | −0.0857 | −0.0264 | −0.0038 | −0.0031 | −0.0058 |

| (0.073) | (0.064) | (0.073) | (0.059) | (0.059) | (0.059) | |

| AND | −0.0393 | −0.1448 * | −0.0300 | −0.0116 | −0.0043 | −0.0055 |

| (0.107) | (0.086) | (0.105) | (0.083) | (0.082) | (0.082) | |

| ID | 0.1487 ** | 0.1484 *** | 0.1517 ** | 0.1576 *** | 0.1641 *** | 0.1633 *** |

| (0.066) | (0.055) | (0.067) | (0.054) | (0.054) | (0.053) | |

| Ownership | 0.0069 | −0.0388 | 0.0027 | 0.0150 | 0.0171 | 0.0149 |

| (0.071) | (0.058) | (0.071) | (0.059) | (0.059) | (0.059) | |

| SIZE | −0.2304 ** | −0.2273 *** | −0.2342 *** | −0.2066 *** | −0.2025 *** | −0.2005 *** |

| (0.090) | (0.077) | (0.091) | (0.076) | (0.076) | (0.076) | |

| Treat | −0.1579 ** | 0.0628 | −0.1217 * | 0.0265 | ||

| (0.070) | (0.115) | (0.067) | (0.096) | |||

| Post | −0.0918 | 2.4567 *** | ||||

| (0.059) | (0.158) | |||||

| Treat* Post | −0.3596 ** | −0.2978 ** | ||||

| (0.154) | (0.127) | |||||

| _cons | 1.9290 ** | 1.9152 *** | 2.0133 ** | 0.0611 | 0.0231 | −0.0175 |

| (0.861) | (0.733) | (0.868) | (0.740) | (0.738) | (0.736) | |

| time dummies | No | No | No | Yes | Yes | Yes |

| N | 3162 | 3162 | 3162 | 3162 | 3162 | 3162 |

| chi2 | 26.7636 | 93.6968 | 40.6066 | 1.3 × 103 | 1.3 × 103 | 1.3 × 103 |

| Variables | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| CAR [−10,10] | CAR [−5,5] | CAR [−1,1] | CAR [−1,10] | |

| AGE | 0.0014 | 0.0006 | 0.0024 *** | 0.0019 * |

| (0.002) | (0.001) | (0.001) | (0.001) | |

| ROA | −0.1320 | −0.2717 ** | −0.1619 * | −0.4019 ** |

| (0.157) | (0.134) | (0.090) | (0.173) | |

| Lev | −0.0307 | −0.0376 | −0.0337 | −0.0461 |

| (0.042) | (0.035) | (0.027) | (0.043) | |

| Cash Ratio | −0.0005 | −0.0006 | 0.0008 | 0.0002 |

| (0.003) | (0.002) | (0.002) | (0.003) | |

| ROF | 0.0149 | 0.0202 * | 0.0085 | 0.0127 * |

| (0.010) | (0.011) | (0.007) | (0.008) | |

| ROI | −0.0087 *** | −0.0044 | −0.0032 | −0.0027 |

| (0.003) | (0.003) | (0.003) | (0.003) | |

| Target | −0.0276 | −0.0234 * | −0.0094 | −0.0332 |

| (0.027) | (0.013) | (0.017) | (0.026) | |

| Tech | −0.0244 | −0.0170 | −0.0167 | −0.0282 |

| (0.019) | (0.015) | (0.014) | (0.021) | |

| AND | 0.0210 | 0.0118 | −0.0130 * | −0.0058 |

| (0.013) | (0.010) | (0.007) | (0.012) | |

| ID | −0.0041 | 0.0062 | −0.0024 | −0.0019 |

| (0.013) | (0.012) | (0.009) | (0.012) | |

| Ownership | −0.0285 * | −0.0205 | −0.0164 * | −0.0392 *** |

| (0.015) | (0.013) | (0.009) | (0.013) | |

| Treat | −0.0616 ** | −0.0416 * | −0.0271 ** | −0.0649 *** |

| (0.024) | (0.023) | (0.013) | (0.021) | |

| _cons | 0.2070 | 0.1698 | 0.0984 | 0.3348 *** |

| (0.138) | (0.118) | (0.085) | (0.119) | |

| N | 155 | 155 | 155 | 155 |

| R2 | 0.158 | 0.163 | 0.239 | 0.298 |

| adj. R2 | 0.087 | 0.092 | 0.175 | 0.239 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| AR | AR | AR | AR | AR | AR | |

| AGE | 0.0042 | 0.0056 | 0.0040 | 0.0013 | 0.0009 | 0.0010 |

| (0.007) | (0.007) | (0.007) | (0.006) | (0.006) | (0.006) | |

| Tobinsq | −45.6390 *** | −24.5801 * | −40.0337 ** | −45.4149 *** | −37.0687 *** | −37.5037 *** |

| (15.122) | (14.943) | (15.972) | (11.892) | (12.807) | (12.945) | |

| ROA | 0.7377 | −0.1865 | 0.7423 | 0.6058 | 0.6285 | 0.6554 |

| (0.671) | (0.692) | (0.674) | (0.581) | (0.584) | (0.579) | |

| Lev | −0.1874 | −0.1885 | −0.1723 | −0.1939 | −0.1867 | −0.1880 |

| (0.209) | (0.181) | (0.211) | (0.180) | (0.180) | (0.179) | |

| Cash Ratio | −0.0236 | −0.0033 | −0.0203 | −0.0234 | −0.0202 | −0.0198 |

| (0.020) | (0.012) | (0.020) | (0.016) | (0.016) | (0.016) | |

| ROF | 0.1077 * | 0.0775 | 0.0986 * | 0.0851 | 0.0725 | 0.0705 |

| (0.056) | (0.051) | (0.056) | (0.052) | (0.052) | (0.052) | |

| ROI | −0.0602 *** | −0.0407 *** | −0.0589 *** | −0.0581 *** | −0.0567 *** | −0.0565 *** |

| (0.021) | (0.012) | (0.021) | (0.018) | (0.018) | (0.018) | |

| Target | −0.1229 | −0.0712 | −0.0949 | −0.1392 | −0.0989 | −0.1031 |

| (0.200) | (0.105) | (0.197) | (0.157) | (0.158) | (0.156) | |

| Tech | −0.0450 | −0.1027 | −0.0467 | −0.0264 | −0.0259 | −0.0291 |

| (0.071) | (0.063) | (0.071) | (0.057) | (0.057) | (0.057) | |

| AND | −0.0442 | −0.1323 | −0.0374 | −0.0110 | −0.0031 | −0.0063 |

| (0.105) | (0.081) | (0.104) | (0.082) | (0.082) | (0.082) | |

| ID | 0.1384 ** | 0.1335 ** | 0.1414 ** | 0.1460 *** | 0.1519 *** | 0.1514 *** |

| (0.066) | (0.056) | (0.066) | (0.053) | (0.053) | (0.053) | |

| Ownership | 0.0108 | −0.0343 | 0.0082 | 0.0226 | 0.0254 | 0.0228 |

| (0.071) | (0.060) | (0.071) | (0.059) | (0.059) | (0.059) | |

| SIZE | −0.2032 ** | −0.1948 *** | −0.2071 ** | −0.1954 *** | −0.1933 *** | −0.1915 *** |

| (0.083) | (0.074) | (0.084) | (0.072) | (0.072) | (0.072) | |

| Treat | −0.1508 ** | 0.0752 | −0.1166 * | 0.0400 | ||

| (0.071) | (0.114) | (0.067) | (0.095) | |||

| Post | −0.0929 | 2.4606 *** | ||||

| (0.059) | (0.156) | |||||

| Treat* Post | −0.3721 ** | −0.3117 ** | ||||

| (0.149) | (0.123) | |||||

| _cons | 1.7160 ** | 1.6438 ** | 1.8065 ** | 0.0192 | 0.0041 | −0.0373 |

| (0.787) | (0.694) | (0.795) | (0.688) | (0.687) | (0.685) | |

| time dummies | No | No | No | Yes | Yes | Yes |

| N | 3255 | 3255 | 3255 | 3255 | 3255 | 3255 |

| chi2 | 26.8702 | 65.4635 | 42.5369 | 1.3 × 103 | 1.3 × 103 | 1.3 × 103 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| AR | AR | AR | AR | AR | AR | |

| AGE | 0.0042 | 0.0032 | 0.0033 | 0.0013 | 0.0009 | 0.0009 |

| (0.007) | (0.007) | (0.007) | (0.006) | (0.006) | (0.006) | |

| Tobinsq | −45.6390 *** | −44.2223 *** | −45.9828 *** | −45.4149 *** | −43.7701 *** | −44.5657 *** |

| (15.122) | (15.146) | (15.051) | (11.892) | (12.007) | (11.981) | |

| ROA | 0.7377 | 0.6790 | 0.6733 | 0.6058 | 0.5734 | 0.5784 |

| (0.671) | (0.672) | (0.677) | (0.581) | (0.583) | (0.581) | |

| Lev | −0.1874 | −0.1766 | −0.1704 | −0.1939 | −0.1760 | −0.1793 |

| (0.209) | (0.209) | (0.212) | (0.180) | (0.180) | (0.179) | |

| Cash Ratio | −0.0236 | −0.0152 | −0.0145 | −0.0234 | −0.0164 | −0.0158 |

| (0.020) | (0.020) | (0.020) | (0.016) | (0.016) | (0.016) | |

| ROF | 0.1077 * | 0.1097 ** | 0.1121 ** | 0.0851 | 0.0894 * | 0.0906 * |

| (0.056) | (0.056) | (0.056) | (0.052) | (0.052) | (0.052) | |

| ROI | −0.0602 *** | −0.0641 *** | −0.0642 *** | −0.0581 *** | −0.0616 *** | −0.0617 *** |

| (0.021) | (0.021) | (0.021) | (0.018) | (0.018) | (0.018) | |

| Target | −0.1229 | −0.1071 | −0.1124 | −0.1392 | −0.1242 | −0.1248 |

| (0.200) | (0.199) | (0.197) | (0.157) | (0.156) | (0.156) | |

| Tech | −0.0450 | −0.0419 | −0.0422 | −0.0264 | −0.0260 | −0.0264 |

| (0.071) | (0.071) | (0.071) | (0.057) | (0.057) | (0.057) | |

| AND | −0.0442 | −0.0540 | −0.0518 | −0.0110 | −0.0207 | −0.0215 |

| (0.105) | (0.105) | (0.105) | (0.082) | (0.082) | (0.082) | |

| ID | 0.1384 ** | 0.1491 ** | 0.1463 ** | 0.1460 *** | 0.1537 *** | 0.1527 *** |

| (0.066) | (0.066) | (0.067) | (0.053) | (0.053) | (0.053) | |

| Ownership | 0.0108 | 0.0154 | 0.0149 | 0.0226 | 0.0231 | 0.0225 |

| (0.071) | (0.071) | (0.071) | (0.059) | (0.059) | (0.059) | |

| SIZE | −0.2032 ** | −0.2229 *** | −0.2277 *** | −0.1954 *** | −0.2110 *** | −0.2103 *** |

| (0.083) | (0.083) | (0.085) | (0.072) | (0.072) | (0.072) | |

| Treat2 | −0.1602 ** | −0.0314 | −0.1338 ** | −0.0274 | ||

| (0.073) | (0.103) | (0.058) | (0.083) | |||

| Post | −0.1045 * | 2.4640 *** | ||||

| (0.060) | (0.156) | |||||

| Treat2* Post | −0.2499 * | −0.2082 * | ||||

| (0.139) | (0.112) | |||||

| _cons | 1.7160 ** | 1.9406 ** | 2.0411 ** | 0.0192 | 0.1853 | 0.1581 |

| (0.787) | (0.791) | (0.803) | (0.688) | (0.692) | (0.690) | |

| Time dummies | No | No | No | Yes | Yes | Yes |

| N | 3255 | 3255 | 3255 | 3255 | 3255 | 3255 |

| chi2 | 26.8702 | 32.0048 | 42.9573 | 1.3 × 103 | 1.3 × 103 | 1.3 × 103 |

| Variables | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| AR | AR | AR | AR | |

| AGE | 0.0044 | 0.0018 | 0.0047 | 0.0026 |

| (0.007) | (0.006) | (0.007) | (0.006) | |

| Tobinsq | −42.0477 *** | −40.0027 *** | −41.9173 * | −34.1553 * |

| (16.166) | (13.148) | (21.832) | (19.460) | |

| ROA | 0.6925 | 0.5669 | 0.0309 | −0.0930 |

| (0.672) | (0.576) | (0.781) | (0.679) | |

| Lev | −0.1836 | −0.2164 | −0.1166 | −0.1588 |

| (0.212) | (0.179) | (0.214) | (0.180) | |

| Cash Ratio | −0.0247 | −0.0252 | −0.0145 | −0.0113 |

| (0.020) | (0.016) | (0.023) | (0.019) | |

| ROF | 0.1090 * | 0.0862 | 0.2374 ** | 0.2050 ** |

| (0.057) | (0.052) | (0.096) | (0.087) | |

| ROI | −0.0566 *** | −0.0535 *** | −0.0594 *** | −0.0562 *** |

| (0.021) | (0.018) | (0.021) | (0.018) | |

| Target | −0.0616 | −0.0604 | −0.0821 | −0.0647 |

| (0.197) | (0.157) | (0.197) | (0.156) | |

| Tech | −0.0520 | −0.0325 | −0.0359 | −0.0128 |

| (0.071) | (0.057) | (0.073) | (0.059) | |

| AND | −0.0199 | 0.0122 | −0.0124 | 0.0140 |

| (0.104) | (0.081) | (0.105) | (0.082) | |

| ID | 0.1557 ** | 0.1651 *** | 0.1653 ** | 0.1759 *** |

| (0.066) | (0.053) | (0.067) | (0.053) | |

| Ownership | 0.0356 | 0.0303 | 0.0316 | 0.0235 |

| (0.099) | (0.083) | (0.099) | (0.083) | |

| SIZE | −0.1807 ** | −0.1544 ** | −0.2088 ** | −0.1642 ** |

| (0.085) | (0.073) | (0.091) | (0.077) | |

| Treat | 0.0768 | 0.0411 | 0.0654 | 0.0300 |

| (0.114) | (0.094) | (0.115) | (0.095) | |

| Post | −0.0914 | 2.4633 *** | −0.0900 | 2.4612 *** |

| (0.060) | (0.155) | (0.060) | (0.158) | |

| Treat* Post | −0.3709 ** | −0.2972 ** | −0.3543 ** | −0.2843 ** |

| (0.150) | (0.122) | (0.154) | (0.126) | |

| Post* SIZE | −0.0066 | 0.0094 | −0.0079 | 0.0091 |

| (0.049) | (0.041) | (0.049) | (0.041) | |

| Treat*SIZE | −0.0524 | −0.0522 | −0.0529 | −0.0544 |

| (0.082) | (0.063) | (0.081) | (0.063) | |

| Treat* Post*SIZE | −0.2094 ** | −0.2486 *** | −0.2250 ** | −0.2658 *** |

| (0.100) | (0.082) | (0.104) | (0.084) | |

| _cons | 1.5404 * | −0.4011 | 1.7631 ** | −0.3668 |

| (0.808) | (0.696) | (0.876) | (0.744) | |

| time dummies | No | Yes | No | Yes |

| N | 3255 | 3255 | 3162 | 3162 |

| chi2 | 47.0473 | 1.4 × 103 | 45.4735 | 1.3 × 103 |

| Variables | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| AR | AR | AR | AR | |

| AGE | 0.0039 | 0.0010 | 0.0042 | 0.0018 |

| (0.007) | (0.006) | (0.007) | (0.006) | |

| Tobinsq | −36.1370 ** | −33.2386 ** | −37.6759 * | −28.9945 |

| (16.327) | (13.480) | (21.620) | (19.234) | |

| ROA | 0.7462 | 0.6392 | 0.1176 | 0.0041 |

| (0.671) | (0.576) | (0.781) | (0.680) | |

| Lev | −0.1515 | −0.1680 | −0.0969 | −0.1210 |

| (0.211) | (0.179) | (0.213) | (0.180) | |

| Cash Ratio | −0.0233 | −0.0222 | −0.0114 | −0.0063 |

| (0.020) | (0.016) | (0.023) | (0.019) | |

| ROF | 0.1009 * | 0.0740 | 0.2218 ** | 0.1864 ** |

| (0.056) | (0.052) | (0.095) | (0.086) | |

| ROI | −0.0555 *** | −0.0535 *** | −0.0596 *** | −0.0576 *** |

| (0.021) | (0.018) | (0.021) | (0.018) | |

| Target | −0.0594 | −0.0762 | −0.0947 | −0.0958 |

| (0.198) | (0.156) | (0.198) | (0.156) | |

| Tech | −0.0473 | −0.0285 | −0.0283 | −0.0061 |

| (0.071) | (0.057) | (0.073) | (0.059) | |

| AND | −0.0275 | 0.0019 | −0.0193 | 0.0031 |

| (0.104) | (0.082) | (0.105) | (0.082) | |

| ID | 0.1323 | 0.1348 * | 0.1295 | 0.1345 * |

| (0.099) | (0.080) | (0.099) | (0.080) | |

| Ownership | 0.0131 | 0.0247 | 0.0070 | 0.0170 |

| (0.071) | (0.059) | (0.071) | (0.059) | |

| SIZE | −0.1969 ** | −0.1809 ** | −0.2274 ** | −0.1946 ** |

| (0.084) | (0.072) | (0.090) | (0.076) | |

| Treat | 0.0066 | −0.0423 | −0.0370 | −0.0893 |

| (0.134) | (0.112) | (0.134) | (0.113) | |

| Post | −0.1171 * | 2.4432 *** | −0.1164 * | 2.4393 *** |

| (0.069) | (0.158) | (0.070) | (0.160) | |

| Treat* Post | −0.0963 | −0.0381 | −0.0657 | 0.0001 |

| (0.180) | (0.152) | (0.182) | (0.152) | |

| Post* ID | 0.0866 | 0.0849 | 0.0859 | 0.0839 |

| (0.130) | (0.107) | (0.131) | (0.107) | |

| ID*treat | 0.1767 | 0.1839 | 0.3156 | 0.3286 |

| (0.236) | (0.192) | (0.248) | (0.201) | |

| Treat* Post*ID | −0.7885 ** | −0.7136 *** | −0.9164 *** | −0.8594 *** |

| (0.316) | (0.257) | (0.332) | (0.270) | |

| _cons | 1.6960 ** | −0.1510 | 1.9536 ** | −0.0711 |

| (0.800) | (0.688) | (0.867) | (0.734) | |

| time dummies | No | Yes | No | Yes |

| N | 3255 | 3255 | 3162 | 3162 |

| chi2 | 50.4716 | 1.3 × 103 | 49.3844 | 1.3 × 103 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hu, Y.; Chen, S.; Qiu, F.; Chen, P.; Chen, S. Will the Volume-Based Procurement Policy Promote Pharmaceutical Firms’ R&D Investment in China? An Event Study Approach. Int. J. Environ. Res. Public Health 2021, 18, 12037. https://doi.org/10.3390/ijerph182212037

Hu Y, Chen S, Qiu F, Chen P, Chen S. Will the Volume-Based Procurement Policy Promote Pharmaceutical Firms’ R&D Investment in China? An Event Study Approach. International Journal of Environmental Research and Public Health. 2021; 18(22):12037. https://doi.org/10.3390/ijerph182212037

Chicago/Turabian StyleHu, Yuanyuan, Shouming Chen, Fangjun Qiu, Peien Chen, and Shaoxiong Chen. 2021. "Will the Volume-Based Procurement Policy Promote Pharmaceutical Firms’ R&D Investment in China? An Event Study Approach" International Journal of Environmental Research and Public Health 18, no. 22: 12037. https://doi.org/10.3390/ijerph182212037

APA StyleHu, Y., Chen, S., Qiu, F., Chen, P., & Chen, S. (2021). Will the Volume-Based Procurement Policy Promote Pharmaceutical Firms’ R&D Investment in China? An Event Study Approach. International Journal of Environmental Research and Public Health, 18(22), 12037. https://doi.org/10.3390/ijerph182212037