ESG Performance and Stock Price Volatility in Public Health Crisis: Evidence from COVID-19 Pandemic

Abstract

:1. Introduction

2. Literature Review

2.1. Corporate Social Responsibility (CSR) and Environmental Social Governance (ESG)

2.2. The Impact of COVID-19 on China’s Stock Market

2.3. Avoid Risk Role of ESG

2.3.1. ESG and Risk

2.3.2. The Avoid Risk Role of ESG in Crisis

3. Study Design

3.1. Data Source

3.2. Variables Selection

3.2.1. Explained Variable: Volatility

3.2.2. Core Explanatory Variable: ESG

3.2.3. Control Variables

3.3. Econometric Model

4. Analysis of Inspection Results

4.1. Descriptive Statistics

4.2. Benchmark Regression

4.2.1. Volatility between ESG and COVID-19

4.2.2. Comparison of Volatility of ESG Performance during COVID-19

4.2.3. The Effect of ESG on Corporate Volatility before and after COVID-19

- (1)

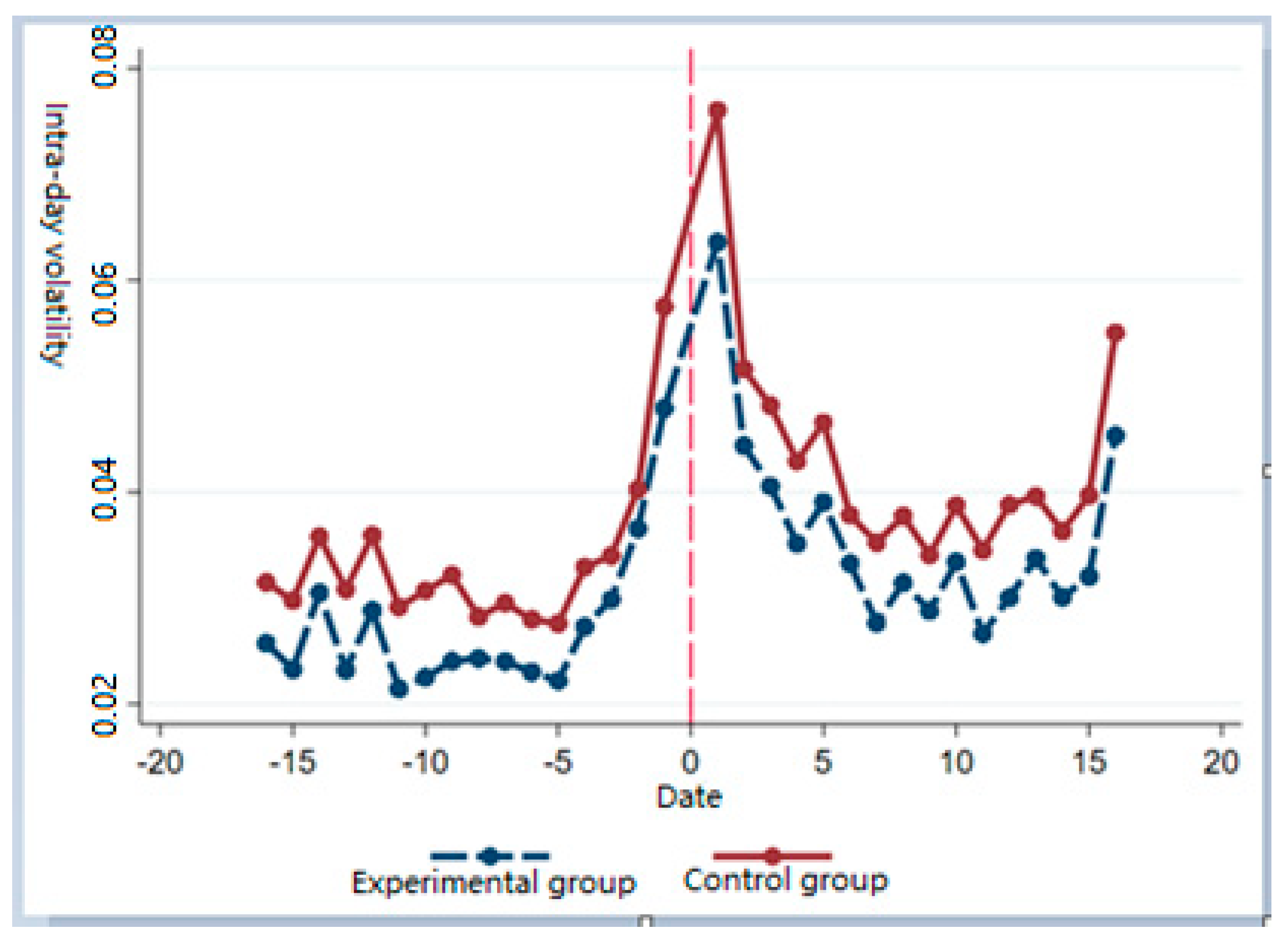

- Parallel trend test

- (2)

- Regression analysis

4.3. Robustness Test

4.3.1. Change the Subsample Selection Method

4.3.2. Change the Time Span

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

References

- Heinkel, R.; Kraus, A.; Zechner, J. The Effect of Green Investing on Corporate Behavior. J. Financ. Quant. Anal. 2001, 36, 431–449. [Google Scholar] [CrossRef]

- Chen, J.; Hong, H.; Stein, J.C. Forecasting Crashes: Trading Volume, Past Returns, and Conditional Skewness in Stock Prices. J. Financ. Econ. 2001, 61, 345–381. [Google Scholar] [CrossRef] [Green Version]

- Mishra, S.; Modi, S.B. Positive and Negative Corporate Social Responsibility, Financial Leverage, and Idiosyncratic Risk. J. Bus. Ethics 2013, 117, 431–448. [Google Scholar] [CrossRef]

- Diemont, D.; Moore, K.; Soppe, A. The Downside of Being Responsible: Corporate Social Responsibility and Tail Risk. J. Bus. Ethics 2016, 137, 213–229. [Google Scholar] [CrossRef]

- Garcia, A.S.; Mendes, W.; Orsato, R.J. Sensitive Industries Produce Better ESG Performance: Evidence from Emerging Markets. J. Clean. Prod. 2017, 150, 135–147. [Google Scholar] [CrossRef]

- Jagannathan, R.; Ravikumar, A.; Sammon, M. Environmental, Social, and Governance Criteria: Why Investors Should Care. J. Invest. Manag. 2018, 16, 18–31. [Google Scholar]

- Lueg, K.; Krastev, B.; Lueg, R. Bidirectional Effects between Organizational Sustainability Disclosure and Risk. J. Clean. Prod. 2019, 229, 268–277. [Google Scholar] [CrossRef]

- Albuquerque, R.; Koskinen, Y.; Zhang, C. Corporate Social Responsibility and Firm Risk: Theory and Empirical Evidence. Manag. Sci. 2019, 65, 4451–4469. [Google Scholar] [CrossRef] [Green Version]

- Broadstock, D.C.; Chan, K.; Cheng, L.T.; Wang, X. The Role of ESG Performance during Times of Financial Crisis: Evidence from COVID-19 in China. Financ. Res. Lett. 2021, 38, 1–11. [Google Scholar] [CrossRef]

- Albuquerque, R.; Koskinen, Y.; Yang, S.; Zhang, C. Resiliency of Environmental and Social Stocks: An Analysis of the Exogenous COVID-19 Market Crash. Rev. Corp. Financ. Stud. 2020, 9, 593–621. [Google Scholar] [CrossRef]

- Takahashi, H.; Yamada, K. When the Japanese stock market meets COVID-19: Impact of ownership, China and US exposure, and ESG channels. Int. Rev. Financ. Anal. 2021, 74, 101670. [Google Scholar] [CrossRef]

- Díaz, V.; Ibrushi, D.; Zhao, J. Reconsidering Systematic Factors during the COVID-19 Pandemic—The Rising Importance of ESG. Financ. Res. Lett. 2021, 38, 1–6. [Google Scholar] [CrossRef]

- Cojoianu, T.F.; Ascui, F.; Clark, G.L.; Hoepner, A.G.; Wójcik, D. Does the Fossil Fuel Divestment Movement Impact New Oil & Hoepner Gas Fundraising. J. Econ. Geogr. 2020, 21, 1–33. [Google Scholar]

- Bowen, H.R. Graduate education in economics. Am. Econ. Rev. 1953, 43, iv-223. [Google Scholar]

- Gillan, S.L.; Koch, A.; Starks, L.T. Firms and Social Responsibility: A Review of ESG and CSR Research in Corporate Finance. J. Corp. Financ. 2021, 66, 1–16. [Google Scholar] [CrossRef]

- Chandan, H.C.; Das, R. Evolution of Responsible and Sustainable Corporate Identity for Chinese Firms. In The China Business Model; Chandos Publishing: Cambridge, UK, 2017; pp. 71–96. [Google Scholar]

- Hou, S.; Li, L. Reasoning and Differences Between CSR Theory and Practice in China, the United States and Europe. J. Int. Bus. Ethics 2014, 7, 19–30. [Google Scholar]

- Baker, S.R.; Bloom, N.; Davis, S.J.; Terry, S.J. COVID-Induced Economic Uncertainty, National Bureau of Economic Research. NBER Working Papers. 2020. No. w26983. Available online: https://www.nber.org/papers/w26983 (accessed on 19 October 2021).

- Zhang, D.; Hu, M.; Ji, Q. Financial markets under the global pandemic of COVID-19. Financ. Res. Lett. 2021, 36, 101528. [Google Scholar] [CrossRef]

- Duan, Y.; Liu, L.; Wang, Z. COVID-19 Sentiment and the Chinese Stock Market: Evidence from the Official News Media and Sina Weibo. Res. Int. Bus. Financ. 2021, 58, 101432. [Google Scholar] [CrossRef]

- Liu, Z.; Huynh, T.L.D.; Dai, P.-F. The Impact of COVID-19 on the Stock Market Crash Risk in China. Res. Int. Bus. Financ. 2021, 57, 1–10. [Google Scholar] [CrossRef] [PubMed]

- Hanif, W.; Mensi, W.; Vo, X.V. Impacts of COVID-19 Outbreak on the Spillovers between US and Chinese Stock Sectors. Financ. Res. Lett. 2021, 7, 1–18. [Google Scholar] [CrossRef]

- Huang, S.; Liu, H. Impact of COVID-19 on stock price crash risk: Evidence from Chinese energy firms. Energy Econ. 2021, 101, 105431. [Google Scholar] [CrossRef]

- Sassen, R.; Hinze, A.K.; Hardeck, I. Impact of ESG Factors on Firm Risk in Europe. J. Bus. Econ. 2016, 86, 867–904. [Google Scholar] [CrossRef]

- Ilhan, E.; Sautner, Z.; Vilkov, G. Carbon Tail Risk. Rev. Financ. Stud. 2019, 34, 1540–1571. [Google Scholar] [CrossRef]

- Shakil, M.H. Environmental, social and governance performance and stock price volatility: A moderating role of firm size. J. Public Aff. 2020, 10, e2574. [Google Scholar] [CrossRef]

- Sabbaghi, O. The impact of news on the volatility of ESG firms. Glob. Financ. J. 2020, 4, 100570. [Google Scholar] [CrossRef]

- James, X.X. The Impact of ESG Risk on Stocks. J. Impact ESG Invest. 2021, 2, 22–42. [Google Scholar]

- Benabou, R.; Tirole, J. Individual and Corporate Social Responsibility. Economica 2010, 77, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Oikonomou, I.; Brooks, C.; Pavelin, S. The Impact of Corporate Social Performance on Financial Risk and Utility: A Longitudinal Analysis. Financ. Manag. 2012, 41, 483–515. [Google Scholar] [CrossRef] [Green Version]

- Krueger, P.; Zacharias, S.; Tang, D.Y.; Rui, Z. The Effects of Mandatory ESG Disclosure Around the World (30 November 2021). European Corporate Governance Institute—Finance Working Paper No. 754/2021, Swiss Finance Institute Research Paper No. 21–44. Available online: http://dx.doi.org/10.2139/ssrn.3832745 (accessed on 19 October 2021).

- Lins, K.V.; Servaes, H.; Tamayo, A. Social Capital, Trust, and Firm Performance: The value of corporate social responsibility during the financial crisis. J. Financ. 2017, 72, 1785–1824. [Google Scholar] [CrossRef] [Green Version]

- Parkinson, M. The Extreme Value Method for Estimating the Variance of the Rate of Return. J. Bus. 1980, 53, 61–65. [Google Scholar] [CrossRef]

- Garman, M.B.; Klass, M.J. On the Estimation of Security Price Volatilities from Historical Data. J. Bus. 1980, 53, 67–78. [Google Scholar] [CrossRef]

- Rogers, L.C.G.; Satchell, S.E. Estimating Variance from High, Low and Closing Prices. Ann. Appl. Probab. 1991, 1, 504–512. [Google Scholar] [CrossRef]

- Yang, D.; Zhang, Q. Drift Independent Volatility Estimation Based on High, Low, Open, and Close Prices. J. Bus. 2000, 73, 477–492. [Google Scholar] [CrossRef] [Green Version]

- Campello, M.; Larrain, M. Enlarging the contracting space: Collateral menus, access to credit, and economic activity. Rev. Financ. Stud. 2016, 29, 349–383. [Google Scholar]

{kind=link}

| Variable Types | Variable Name | Variable Code | Variable Definitions |

|---|---|---|---|

| Explained variable | 5 days before and after the fluctuations | VOL5 | Five (10) days of stock price volatility before and after the window period |

| 10 days before and after the fluctuation | VOL10 | Stock price volatility of 10 days before and after the window period (20 days in total) | |

| Seasonal fluctuations | VOLQ | Stock price volatility for all trading days in the first quarter of 2020 | |

| Intraday volatility | vol | (Intraday high price—intraday low price)/daytime average price | |

| Explanatory variables | ESG performance | ESG | Quantitative scores given by the MSCI ESG index |

| Control variables | The enterprise scale | Size | The natural log of a company’s total annual market value |

| Financial leverage | Lev | Average annual total liabilities/Average annual Total assets ×100 | |

| Tobin Q value | TobinQ | Company market capitalization/total assets | |

| Cash holding ratio | Cash | The company holds cash/total assets |

| Variable Name | Variable Code | Sample Size | Mean Value | Standard Deviation | Min | Max |

|---|---|---|---|---|---|---|

| 5-Day Fluctuation | VOL5 | 1021 | 2.020 | 0.222 | 1.079 | 2.807 |

| Fluctuation In the Last 10 Days | VOL10 | 1021 | 1.818 | 0.219 | 1.002 | 2.714 |

| Quarterly Fluctuation | VOLQ | 1021 | 1.743 | 0.241 | 1.029 | 2.534 |

| Intraday Fluctuation | vol | 38,690 | 0.2294 | 0.4204 | 0 | 1 |

| Esg Performance | ESG | 1021 | 24.80 | 7.650 | 11.21 | 61.72 |

| Tobin Q Value | TobinQ | 1021 | 1.693 | 1.313 | 0.730 | 14.09 |

| Enterprise Scale | Size | 1021 | 23.54 | 1.159 | 20.62 | 28.09 |

| Cash Ratio | Cash | 1021 | 0.0018 | 0.0282 | 0 | 0.876 |

| Financial Leverage | Lev | 1021 | 51.51 | 21.72 | 0.836 | 229.0 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| ESG | −0.099 ** | −0.127 ** | −0.121 *** | −0.145 *** | −0.126 ** | −0.132 ** |

| (0.047) | (0.051) | (0.046) | (0.050) | (0.051) | (0.054) | |

| Size | −0.001 | −0.018 *** | 0.007 | −0.009 * | 0.032 *** | 0.012 ** |

| (0.006) | (0.006) | (0.006) | (0.005) | (0.006) | (0.006) | |

| Lev | −0.002 *** | −0.001 *** | −0.001 *** | −0.000 | −0.000 | 0.001 |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | |

| TobinQ | −0.031 *** | −0.017 *** | −0.034 *** | −0.020 *** | −0.040*** | −0.027 *** |

| (0.006) | (0.007) | (0.006) | (0.006) | (0.007) | (0.007) | |

| Cash | −0.598 ** | −0.493 ** | −0.624 *** | −0.541 ** | −0.790 *** | −0.698 *** |

| (0.237) | (0.224) | (0.235) | (0.221) | (0.258) | (0.238) | |

| Constant term | 2.901 *** | 2.574 *** | 2.725 *** | 2.406 *** | 2.696 *** | 2.383 *** |

| (0.141) | (0.144) | (0.140) | (0.142) | (0.153) | (0.153) | |

| Sample size | 1021 | 1021 | 1021 | 1021 | 1021 | 1021 |

| 0.100 | 0.233 | 0.091 | 0.238 | 0.095 | 0.265 | |

| Fixed effects | YES | YES | YES |

| (1) | (2) | (3) | |

|---|---|---|---|

| ESGf | −0.044 ** | −0.046 ** | −0.067 *** |

| (0.021) | (0.020) | (0.022) | |

| Size | −0.030 *** | −0.033 *** | −0.027 *** |

| (0.009) | (0.009) | (0.009) | |

| Lev | −0.001 * | −0.000 | 0.001 |

| (0.001) | (0.001) | (0.001) | |

| TobinQ | −0.007 | 0.000 | 0.012 |

| (0.008) | (0.008) | (0.009) | |

| Constant term | 2.810 *** | 2.628 *** | 2.349 *** |

| (0.199) | (0.197) | (0.208) | |

| Sample size | 526 | 526 | 526 |

| 0.248 | 0.257 | 0.292 | |

| Fixed effects | YES | YES | YES |

| (1) | (2) | |

|---|---|---|

| Post | 0.011 *** | 0.011 *** |

| (0.001) | (0.001) | |

| ESGf | −0.005 *** | −0.002 *** |

| (0.001) | (0.001) | |

| ESGf*Post | −0.002 *** | −0.002 *** |

| (0.001) | (0.001) | |

| Size | −0.001 *** | |

| (0.000) | ||

| Lev | −0.000 *** | |

| (0.000) | ||

| TobinQ | 0.002 *** | |

| (0.000) | ||

| Cash | −0.025 *** | |

| (0.005) | ||

| Constant term | 0.033 *** | 0.063 *** |

| (0.000) | (0.004) | |

| N | 13,247 | 13,247 |

| R2 | 0.059 | 0.085 |

| (1) | (2) | (3) | |

|---|---|---|---|

| ESGf | −0.028 | −0.040 ** | −0.048 ** |

| (0.020) | (0.020) | (0.021) | |

| Size | −0.029 *** | −0.030 *** | −0.032 *** |

| (0.009) | (0.008) | (0.009) | |

| Lev | −0.000 | 0.001 | 0.002 ** |

| (0.001) | (0.001) | (0.001) | |

| TobinQ | −0.009 | 0.001 | 0.018 * |

| (0.009) | (0.009) | (0.009) | |

| Cash | −0.445 * | −0.494 ** | −0.609 ** |

| (0.237) | (0.230) | (0.244) | |

| Constant term | 2.737 *** | 2.503 *** | 2.388 *** |

| (0.197) | (0.191) | (0.203) | |

| Sample size | 526 | 526 | 526 |

| 0.257 | 0.277 | 0.315 | |

| Fixed effects | YES | YES | YES |

| (1) | (2) | |

|---|---|---|

| Post | 0.015 *** | 0.015 *** |

| (0.000) | (0.000) | |

| ESGf | −0.005 *** | −0.003 *** |

| (0.000) | (0.000) | |

| ESGf*Post | −0.002 *** | −0.002 *** |

| (0.000) | (0.000) | |

| Size | −0.001 *** | |

| (0.000) | ||

| Lev | −0.000 | |

| (0.000) | ||

| TobinQ | 0.002 *** | |

| (0.000) | ||

| Cash | −0.027 *** | |

| (0.003) | ||

| Constant term | 0.030 *** | 0.052 *** |

| (0.000) | (0.002) | |

| N | 38,638 | 38,638 |

| R2 | 0.122 | 0.142 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhou, D.; Zhou, R. ESG Performance and Stock Price Volatility in Public Health Crisis: Evidence from COVID-19 Pandemic. Int. J. Environ. Res. Public Health 2022, 19, 202. https://doi.org/10.3390/ijerph19010202

Zhou D, Zhou R. ESG Performance and Stock Price Volatility in Public Health Crisis: Evidence from COVID-19 Pandemic. International Journal of Environmental Research and Public Health. 2022; 19(1):202. https://doi.org/10.3390/ijerph19010202

Chicago/Turabian StyleZhou, Dongyi, and Rui Zhou. 2022. "ESG Performance and Stock Price Volatility in Public Health Crisis: Evidence from COVID-19 Pandemic" International Journal of Environmental Research and Public Health 19, no. 1: 202. https://doi.org/10.3390/ijerph19010202

APA StyleZhou, D., & Zhou, R. (2022). ESG Performance and Stock Price Volatility in Public Health Crisis: Evidence from COVID-19 Pandemic. International Journal of Environmental Research and Public Health, 19(1), 202. https://doi.org/10.3390/ijerph19010202