Can Mobile Payment Increase Household Income and Mitigate the Lower Income Condition Caused by Health Risks? Evidence from Rural China

Abstract

:1. Introduction

2. Background, Literature Review, and Theoretical Analysis

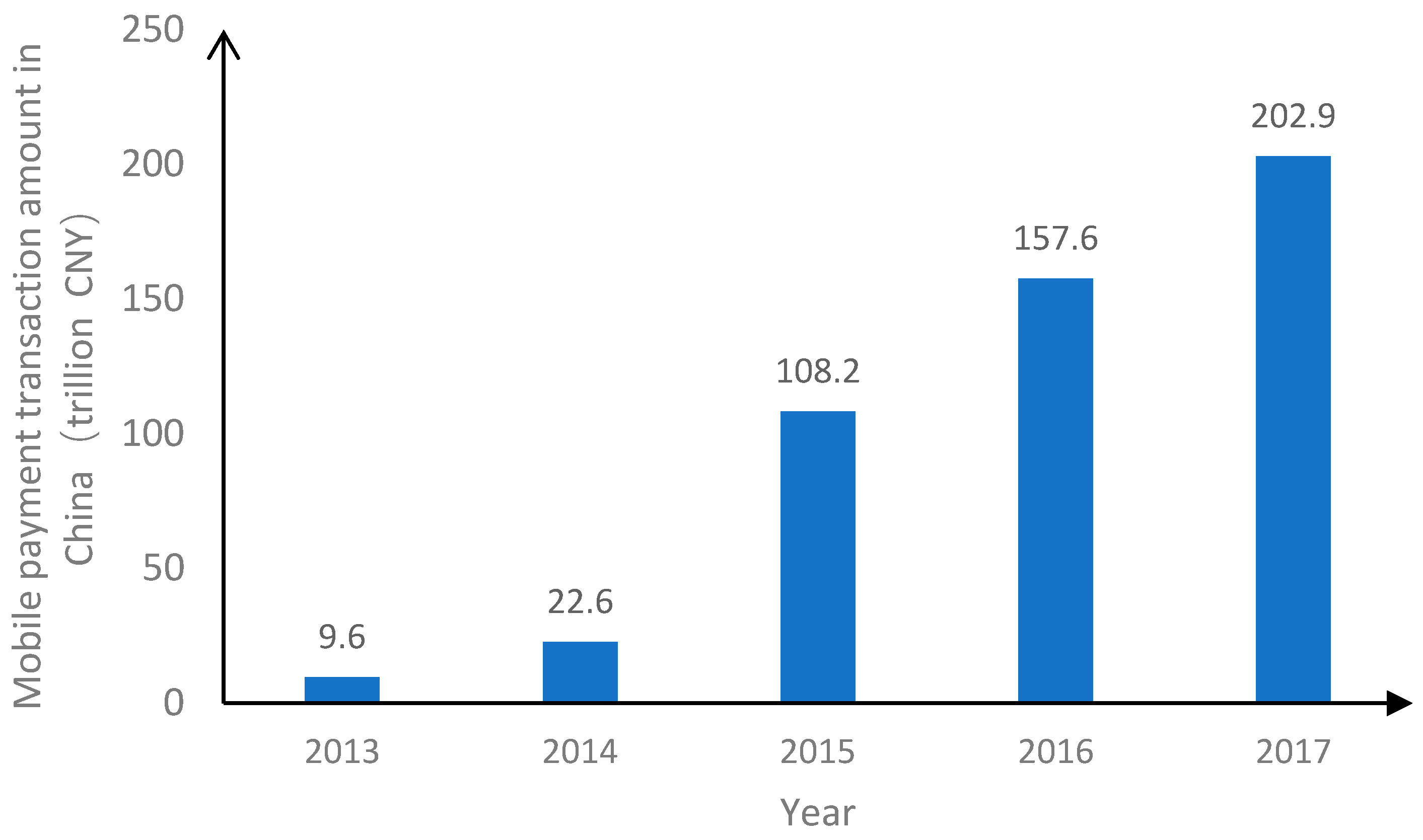

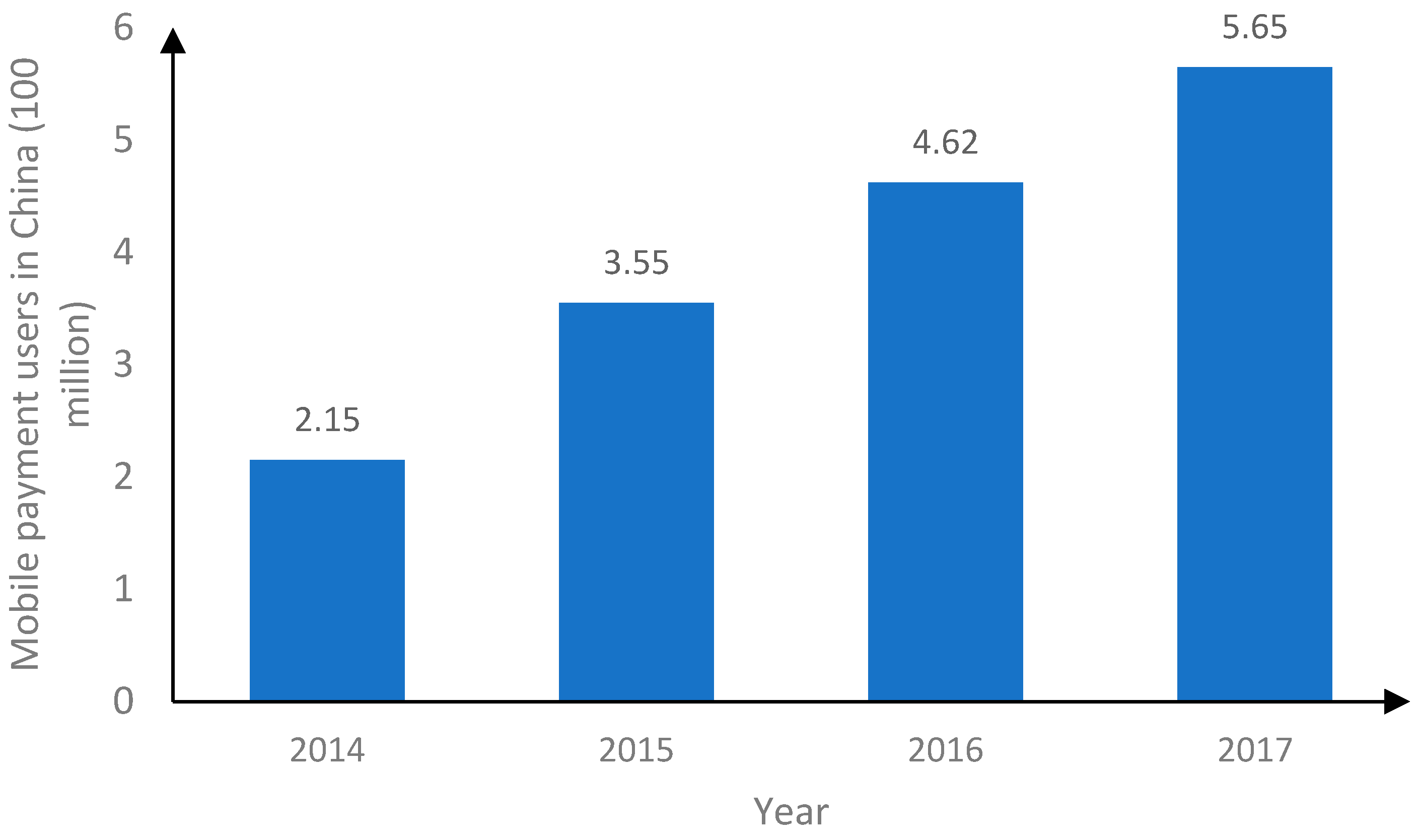

2.1. Background

2.2. Literature Review

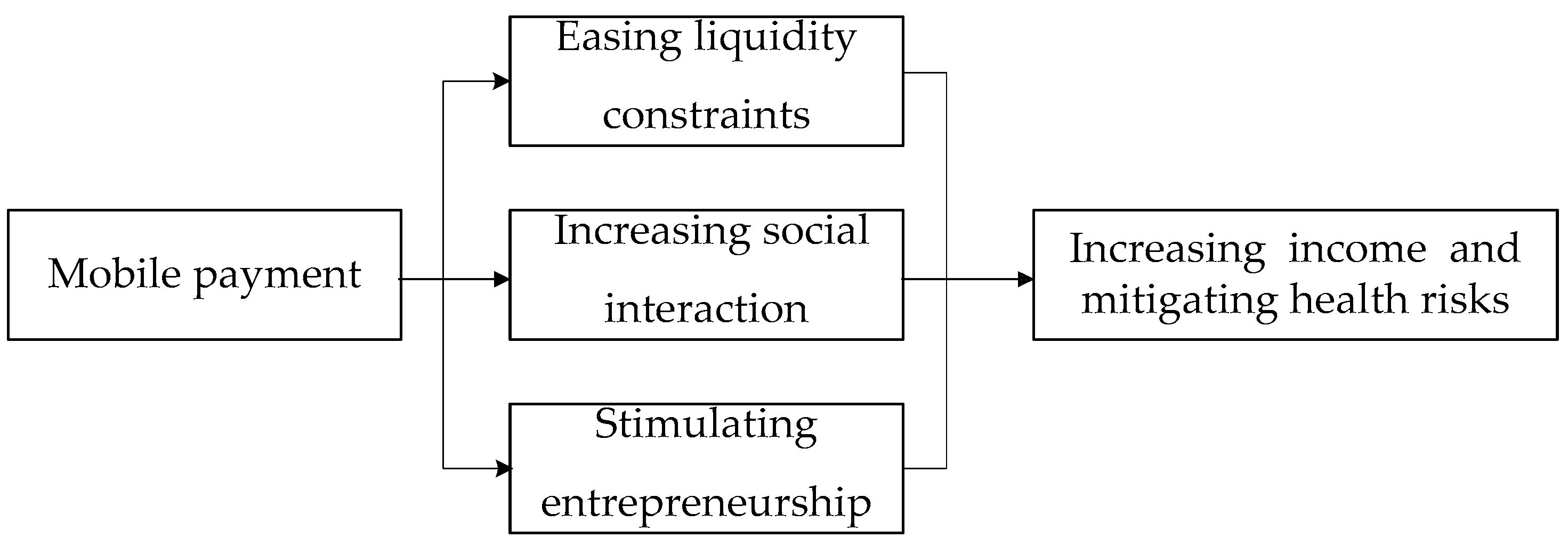

2.3. Theoretical Analysis

3. Research Design

3.1. Data

3.2. Methods

3.3. Variables

3.4. Descriptive Statistics

4. Results

4.1. Baseline Analysis

4.2. Robustness Check

4.3. Mitigated Effects of Mobile Payment on Households with Health Risks

4.4. Mechanism Analysis

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Wang, X.; Zhang, X. An explanation of China’s experience in eliminating absolute poverty and the orientation of relative poverty governance in the post-2020 era. Chin. Rural Econ. 2021, 2, 2–18. [Google Scholar]

- Wang, W.; Luo, X.; Zhang, C.; Song, J.; Xu, D. Can land transfer alleviate the poverty of the elderly? Evidence from rural China. Int. J. Environ. Res. Public Health 2021, 18, 11288. [Google Scholar] [CrossRef]

- He, Y.; Ahmed, T. Farmers’ Livelihood Capital and Its Impact on Sustainable Livelihood Strategies: Evidence from the Poverty-Stricken Areas of Southwest China. Sustainability 2022, 14, 4955. [Google Scholar] [CrossRef]

- Bull, C.N.; Krout, J.A.; Rathbone-McCuan, E.; Shreffler, M.J. Access and issues of equity in remote/rural areas. J. Rural Health 2001, 17, 356–359. [Google Scholar] [CrossRef]

- Chu, K.; Liu, D.; Duan, W. The mechanism of household smoothing consumption in rural areas under health impact—Also on the relationship between external security and family self-security. Nankai Econ. Res. 2018, 2, 39–55. [Google Scholar] [CrossRef]

- Alam, K.; Mahal, A. Economic impacts of health shocks on households in low and middle income countries: A review of the literature. Glob. Health 2014, 10, 1–18. [Google Scholar] [CrossRef]

- Zhang, J.; Gan, L.; Xu, L.C.; Yao, Y. Health shocks, village elections, and household income: Evidence from rural China. China Econ. Rev. 2014, 30, 155–168. [Google Scholar] [CrossRef]

- Islam, A.; Maitra, P. Health shocks and consumption smoothing in rural households: Does microcredit have a role to play? J. Dev. Econ. 2012, 97, 232–243. [Google Scholar] [CrossRef]

- Li, W.; Yuan, K.; Yue, M.; Zhang, L.; Huang, F. Climate change risk perceptions, facilitating conditions and health risk management intentions: Evidence from farmers in rural China. Clim. Risk Manag. 2021, 32, 100283. [Google Scholar] [CrossRef]

- Man, X.; Xue, Z.; Liu, J. The impact of long-term and short-term health shock on the labour supply and labour income of migrant workers in China: The mediating role of medical insurance. Appl. Econ. Lett. 2022, 2022, 1–5. [Google Scholar] [CrossRef]

- Baker, S.R.; Farrokhnia, R.A.; Meyer, S.; Pagel, M.; Yannelis, C. How does household spending respond to an epidemic? Consumption during the 2020 COVID-19 pandemic. Rev. Asset Pricing Stud. 2020, 10, 834–862. [Google Scholar] [CrossRef]

- Bao, R.; Zhang, A. Does lockdown reduce air pollution? Evidence from 44 cities in northern China. Sci. Total Environ. 2020, 731, 139052. [Google Scholar] [CrossRef]

- Haroon, O.; Rizvi, S.A.R. COVID-19: Media coverage and financial markets behavior—A sectoral inquiry. J. Behav. Exp. Financ. 2020, 27, 100343. [Google Scholar] [CrossRef]

- Oo, T.K.; Arunrat, N.; Kongsurakan, P.; Sereenonchai, S.; Wang, C. Nitrogen dioxide (NO2) level changes during the control of COVID-19 pandemic in Thailand. Aerosol Air Qual. Res. 2021, 21, 200440. [Google Scholar] [CrossRef]

- He, M.Z.; Kinney, P.L.; Li, T.; Chen, C.; Sun, Q.; Ban, J.; Wang, J.; Liu, S.; Goldsmith, J.; Kioumourtzoglou, M.-A. Short-and intermediate-term exposure to NO2 and mortality: A multi-county analysis in China. Environ. Pollut. 2020, 261, 114165. [Google Scholar] [CrossRef]

- Fredriksson, P.G.; Mohanty, A. COVID-19 regulations, political institutions, and the environment. Environ. Resour. Econ. 2022, 81, 323–353. [Google Scholar] [CrossRef]

- Wang, Q.; Su, M. A preliminary assessment of the impact of COVID-19 on environment—A case study of China. Sci. Total Environ. 2020, 728, 138915. [Google Scholar] [CrossRef]

- Gong, B.; Zhang, S.; Yuan, L.; Chen, K.Z. A balance act: Minimizing economic loss while controlling novel coronavirus pneumonia. J. Chin. Gov. 2020, 5, 249–268. [Google Scholar] [CrossRef]

- Han, J.; Meyer, B.D.; Sullivan, J.X. Income and Poverty in the COVID-19 Pandemic. Brook. Pap. Econ. Act. 2020, 2020, 85–118. [Google Scholar] [CrossRef]

- Decerf, B.; Ferreira, F.H.G.; Mahler, D.G.; Sterck, O. Lives and livelihoods: Estimates of the global mortality and poverty effects of the Covid-19 pandemic. World Dev. 2021, 146, 105561. [Google Scholar] [CrossRef]

- Long, W.; Zeng, J.; Sun, T. Who Lost Most Wages and Household Income during the COVID-19 Pandemic in Poor Rural China? China World Econ. 2021, 29, 95–116. [Google Scholar] [CrossRef]

- Nie, P.; Ding, L.; Chen, Z.; Liu, S.; Zhang, Q.; Shi, Z.; Wang, L.; Xue, H.; Liu, G.G.; Wang, Y. Income-related health inequality among Chinese adults during the COVID-19 pandemic: Evidence based on an online survey. Int. J. Equity Health 2021, 20, 1–13. [Google Scholar] [CrossRef]

- Qian, Y.; Fan, W. Who loses income during the COVID-19 outbreak? Evidence from China. Res. Soc. Strat. Mobil. 2020, 68, 100522. [Google Scholar] [CrossRef]

- Huang, Y.; Wang, X.; Wang, X. Mobile payment in China: Practice and its effects. Asian Econ. Pap. 2020, 19, 1–18. [Google Scholar] [CrossRef]

- Lin, W.R.; Lin, C.Y.; Ding, Y.H. Factors affecting the behavioral intention to adopt mobile payment: An empirical study in Taiwan. Mathematics 2020, 8, 1851. [Google Scholar] [CrossRef]

- Wei, M.F.; Luh, Y.H.; Huang, Y.H.; Chang, Y.C. Young generation’s mobile payment adoption behavior: Analysis based on an extended UTAUT model. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 618–637. [Google Scholar] [CrossRef]

- Tang, B.; Bragazzi, N.L.; Li, Q.; Tang, S.; Xiao, Y.; Wu, J.H. An updated estimation of the risk of transmission of the novel coronavirus (2019-nCov). Infect. Dis. Model. 2020, 5, 248–255. [Google Scholar] [CrossRef]

- Zhao, Y.; Bacao, F. How does the pandemic facilitate mobile payment? An investigation on users’ perspective under the COVID-19 pandemic. Int. J. Environ. Res. Public Health 2021, 18, 1016. [Google Scholar] [CrossRef]

- Aker, J.C.; Boumnijel, R.; McClelland, A.; Tierney, N. Payment mechanisms and antipoverty programs: Evidence from a mobile money cash transfer experiment in Niger. Econ. Dev. Cult. Change 2016, 65, 1–37. [Google Scholar] [CrossRef]

- Jack, W.; Suri, T. Risk sharing and transactions costs: Evidence from Kenya’s mobile money revolution. Am. Econ. Rev. 2014, 104, 183–223. [Google Scholar] [CrossRef]

- Suri, T.; Jack, W. The long-run poverty and gender impacts of mobile money. Science 2016, 354, 1288–1292. [Google Scholar] [CrossRef]

- Kingiri, A.N.; Fu, X. Understanding the diffusion and adoption of digital finance innovation in emerging economies: M-Pesa money mobile transfer service in Kenya. Innov. Dev. 2019, 10, 67–87. [Google Scholar] [CrossRef]

- Kikulwe, E.M.; Fischer, E.; Qaim, M. Mobile money, smallholder farmers, and household welfare in Kenya. PLoS ONE 2014, 9, e109804. [Google Scholar] [CrossRef]

- Zhao, C.; Wu, Y.; Guo, J. Mobile payment and Chinese rural household consumption. China Econ. Rev. 2022, 71, 101719. [Google Scholar] [CrossRef]

- Zhao, C.; Li, X.; Yan, J. The effect of digital finance on Residents’ happiness: The case of mobile payments in China. Electron. Commer. Res. 2022, 2022, 1–36. [Google Scholar] [CrossRef]

- Ma, Y.; Xiang, Q.; Yan, C.; Liao, H.; Wang, J. Poverty Vulnerability and Health Risk Action Path of Families of Rural Elderly With Chronic Diseases: Empirical Analysis of 1852 Families in Central and Western China. Front. Public Health 2022, 10, 776901. [Google Scholar] [CrossRef]

- Hong, Q.; Chang, X. An analysis of the interaction between disease and poverty among rural residents in China. J. Agric. Econ. 2010, 31, 85–94. [Google Scholar] [CrossRef]

- Bonfrer, I.; Gustafsson-Wright, E. Health shocks, coping strategies and foregone healthcare among agricultural households in Kenya. Glob. Public Health 2017, 12, 1369–1390. [Google Scholar] [CrossRef]

- Mitra, S.; Palmer, M.; Mont, D.; Groce, N. Can households cope with health shocks in Vietnam? Health Econ. 2016, 25, 888–907. [Google Scholar] [CrossRef]

- Liu, K. Insuring against health shocks: Health insurance and household choices. J. Health Econ. 2016, 46, 16–32. [Google Scholar] [CrossRef]

- Morudu, P.; Kollamparambil, U. Health shocks, medical insurance and household vulnerability: Evidence from South Africa. PLoS ONE 2020, 15, e0228034. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Suri, T.; Bharadwaj, P.; Jack, W. Fintech and household resilience to shocks: Evidence from digital loans in Kenya. J. Dev. Econ. 2021, 153, 102697. [Google Scholar] [CrossRef]

- Aker, J.C.; Mbiti, I.M. Mobile phones and economic development in Africa. J. Econ. Perspect. 2010, 24, 207–232. [Google Scholar] [CrossRef]

- Siano, A.; Raimi, L.; Palazzo, M.; Panait, M.C. Mobile banking: An innovative solution for increasing financial inclusion in Sub-Saharan African Countries: Evidence from Nigeria. Sustainability 2020, 12, 10130. [Google Scholar] [CrossRef]

- Li, R.; Li, Q.; Huang, S.; Zhu, X. The credit rationing of Chinese rural households and its welfare loss: An investigation based on panel data. China Econ. Rev. 2013, 26, 17–27. [Google Scholar] [CrossRef]

- Yeung, G.; He, C.; Zhang, P. Rural banking in China: Geographically accessible but still financially excluded? Reg. Stud. 2017, 51, 297–312. [Google Scholar] [CrossRef]

- Lai, J.T.; Yan, I.K.M.; Yi, X.; Zhang, H. Digital financial inclusion and consumption smoothing in China. China World Econ. 2020, 28, 64–93. [Google Scholar] [CrossRef]

- Costello, A.M. The value of collateral in trade finance. J. Financ. Econ. 2019, 134, 70–90. [Google Scholar] [CrossRef]

- Johny, J.; Wichmann, B.; Swallow, B.M. Characterizing social networks and their effects on income diversification in rural Kerala, India. World Dev. 2017, 94, 375–392. [Google Scholar] [CrossRef]

- Jack, W.; Ray, A.; Suri, T. Transaction networks: Evidence from mobile money in Kenya. Am. Econ. Rev. 2013, 103, 356–361. [Google Scholar] [CrossRef]

- Yin, Z.; Gong, X.; Guo, P.; Wu, T. What drives entrepreneurship in digital economy? Evidence from China. Econ. Model. 2019, 82, 66–73. [Google Scholar] [CrossRef]

- Galindo-Martin, M.A.; Méndez-Picazo, M.T.; Alfaro-Navarro, J.L. Entrepreneurship, income distribution and economic growth. Int. Entrep. Manag. J. 2010, 6, 131–141. [Google Scholar] [CrossRef]

- Halvarsson, D.; Korpi, M.; Wennberg, K. Entrepreneurship and income inequality. J. Econ. Behav. Organ. 2018, 145, 275–293. [Google Scholar] [CrossRef]

- Lecuna, A. Income inequality and entrepreneurship. Econ. Res.-Ekon. Istraz. 2020, 33, 2269–2285. [Google Scholar] [CrossRef]

- Wang, X. Mobile payment and informal business: Evidence from China’s household panel data. China World Econ. 2020, 28, 90–115. [Google Scholar] [CrossRef]

- Evans, W.N.; Oates, W.E.; Schwab, R.M. Measuring peer group effects: A study of teenage behavior. J. Polit. Econ. 1992, 100, 966–991. [Google Scholar] [CrossRef]

- Heckman, J.J. Sample Selection Bias as a Specification Error. Econometrica 1979, 47, 153–161. [Google Scholar] [CrossRef]

- He, C.; Li, A.; Li, D.; Yu, J. Does Digital Inclusive Finance Mitigate the Negative Effect of Climate Variation on Rural Residents’ Income Growth in China? Int. J. Environ. Res. Public Health 2022, 19, 8280. [Google Scholar] [CrossRef]

- Wang, W.; Zhang, C.; Guo, Y.; Xu, D. Impact of Environmental and Health Risks on Rural Households’ Sustainable Livelihoods: Evidence from China. Int. J. Environ. Res. Public Health 2021, 18, 10955. [Google Scholar] [CrossRef]

- Kalmijn, M.; Loeve, A.; Manting, D. Income dynamics in couples and the dissolution of marriage and cohabitation. Demography 2007, 44, 159–179. [Google Scholar] [CrossRef]

- Teulings, C.; Van-Rens, T. Education, growth, and income inequality. Rev. Econ. Stat. 2008, 90, 89–104. [Google Scholar] [CrossRef] [Green Version]

- Liang, P.; Guo, S. Social interaction, Internet access and stock market participation—An empirical study in China. J. Comp. Econ. 2015, 43, 883–901. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Variable | Definition |

|---|---|

| Dependent Variable | |

| Income (RMB) | Ln (household annual total income) |

| Income_p (RMB) | Ln (household annual total income/the total number of family members) |

| Core Independent Variable | |

| Mobile payment | =1 if the household uses mobile terminal payment when shopping |

| Health risks | Number of unhealthy family members |

| Other Independent Variable | |

| Age | The age of the head of the household |

| Male | =1 if the head of the household is male |

| Married | =1 if the head of the household is married |

| Edu years | Years of education of the head of the household |

| Work | =1 if the head of the household is employed or self-employed |

| Asset (RMB) | Ln (household asset) |

| Household size | Household size measured by the total number of family members |

| Labor num | Number of family members between 16 and 60 years old |

| Entrepreneurship | =1 if the household is engaged in business |

| Per GDP (RMB) | Ln (GDP per capita) |

| Mechanism Variable | |

| Bank loan | =1 if the household has bank loan |

| Credit card | =1 if the household has credit card |

| Transfer expenditure (RMB) | Ln (Transfer expenditure) |

| Communication cost (RMB) | Ln (Communication cost) |

| Formal entrepreneurship | =1 if the household is engaged in formal business |

| Informal entrepreneurship | =1 if the household is engaged in informal business |

| Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| Income | 12,318 | 9.96 | 1.50 | 0.26 | 17.22 |

| Income_p | 12,318 | 8.68 | 1.42 | 0.05 | 16.52 |

| Mobile payment | 12,318 | 0.11 | 0.31 | 0.00 | 1.00 |

| Age | 12,318 | 57.02 | 12.27 | 18.00 | 97.00 |

| Male | 12,318 | 0.89 | 0.31 | 0.00 | 1.00 |

| Edu years | 12,318 | 7.01 | 3.45 | 0.00 | 19.00 |

| Married | 12,318 | 0.87 | 0.33 | 0.00 | 1.00 |

| Work | 12,318 | 0.74 | 0.44 | 0.00 | 1.00 |

| Household size | 12,318 | 4.12 | 2.06 | 1.00 | 17.00 |

| Labor num | 12,318 | 2.09 | 1.53 | 0.00 | 12.00 |

| Asset | 12,318 | 11.64 | 1.76 | 0.69 | 18.43 |

| Entrepreneurship | 12,318 | 0.10 | 0.30 | 0.00 | 1.00 |

| Per gdp | 12,318 | 10.84 | 0.34 | 10.23 | 11.68 |

| Bank loan | 12,318 | 0.13 | 0.34 | 0.00 | 1.00 |

| Credit card | 12,318 | 0.08 | 0.27 | 0.00 | 1.00 |

| Transfer expenditure | 12,318 | 5.06 | 3.68 | 0.00 | 12.21 |

| Communication cost | 12,318 | 6.74 | 1.63 | 0.00 | 11.00 |

| Formal entrepreneurship | 12,318 | 0.01 | 0.09 | 0.00 | 1.00 |

| Informal entrepreneurship | 12,318 | 0.14 | 0.34 | 0.00 | 1.00 |

| The Use of Mobile Payment | Income | Income_p |

|---|---|---|

| YES | 11.00 | 9.48 |

| NO | 9.83 | 8.58 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Income | Income | Income_p | Income_p | |

| Mobile payment | 1.118 *** (0.038) | 0.306 *** (0.036) | 0.832 *** (0.038) | 0.305 *** (0.036) |

| Age | 0.004 *** (0.001) | 0.007 *** (0.001) | ||

| Male | −0.009 (0.042) | −0.023 (0.043) | ||

| Married | 0.040 *** (0.004) | 0.040 *** (0.004) | ||

| Edu years | 0.151 *** (0.039) | 0.007 (0.039) | ||

| Work | 0.208 *** (0.029) | 0.196 *** (0.029) | ||

| Asset | 0.026 *** (0.007) | −0.197 *** (0.007) | ||

| Household size | 0.272 *** (0.011) | 0.248 *** (0.011) | ||

| Labor num | 0.252 *** (0.008) | 0.244 *** (0.008) | ||

| Entrepreneurship | 0.298 *** (0.038) | 0.314 *** (0.038) | ||

| Per GDP | 0.396 *** (0.139) | 0.389 *** (0.139) | ||

| Province | Yes | Yes | Yes | Yes |

| Observations | 12,318 | 12,318 | 12,318 | 12,318 |

| Adj. R2 | 0.078 | 0.347 | 0.081 | 0.276 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Mobile Payment | Income | Income_p | |

| Mobile payment | 2.383 *** (0.348) | 2.410 *** (0.346) | |

| Mobile payment usage rate | 0.382 *** (0.032) | ||

| Controls | Yes | Yes | Yes |

| Province | Yes | Yes | Yes |

| Observations | 12,311 | 12,311 | 12,311 |

| Adj. R2 | 0.151 | 0.190 | 0.095 |

| F Value | 40.51 | ||

| DWH Test | 50.543 | 53.146 |

| Matching Method | Dependent | Income | Income_p |

|---|---|---|---|

| Variables | |||

| Nearest neighbor matching (k = 1) | ATT | 0.248 | 0.250 |

| T-stat | 4.22 | 4.24 | |

| Nearest neighbor matching (k = 4) | ATT | 0.226 | 0.230 |

| T-stat | 4.92 | 4.92 | |

| Radius matching (r = 0.01) | ATT | 0.980 | 0.780 |

| T-stat | 9.82 | 7.96 |

| (1) | (2) | |

|---|---|---|

| Income | Income_p | |

| Health risks | −0.117 *** (0.013) | −0.125 *** (0.013) |

| Controls | Yes | Yes |

| Province | Yes | Yes |

| Observations | 12,318 | 12,318 |

| Adj. R2 | 0.078 | 0.347 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Health Risks Group | No Health Risks Group | Health Risks Group | No Health Risks Group | |

| Income | Income | Income_p | Income_p | |

| Mobile payment | 0.293 *** (0.045) | 0.244 *** (0.064) | 0.290 *** (0.044) | 0.248 *** (0.063) |

| Controls | Yes | Yes | Yes | Yes |

| Province | Yes | Yes | Yes | Yes |

| Observations | 6311 | 6007 | 6311 | 6007 |

| Adj. R2 | 0.361 | 0.302 | 0.294 | 0.209 |

| (1) Bank Loan | (2) Credit Card | |

|---|---|---|

| Mobile payment | 0.027 ** (0.012) | 0.158 *** (0.013) |

| Controls | Yes | Yes |

| Province | Yes | Yes |

| Observations | 12,318 | 12,318 |

| Adj. R2 | 0.109 | 0.086 |

| (1) Transfer Expenditure | (2) Communication Cost | |

|---|---|---|

| Mobile payment | 0.670 *** (0.101) | 0.301 *** (0.027) |

| Controls | Yes | Yes |

| Province | Yes | Yes |

| Observations | 12,318 | 12,318 |

| Adj. R2 | 0.131 | 0.341 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Entrepreneurship | Formal Entrepreneurship | Informal Entrepreneurship | |

| Mobile payment | 0.122 *** (0.013) | 0.016 *** (0.005) | 0.141 *** (0.014) |

| Controls | Yes | Yes | Yes |

| Province | Yes | Yes | Yes |

| Observations | 12,318 | 12,318 | 12,318 |

| Adj. R2 | 0.109 | 0.016 | 0.105 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Qiu, W.; Wu, T.; Xue, P. Can Mobile Payment Increase Household Income and Mitigate the Lower Income Condition Caused by Health Risks? Evidence from Rural China. Int. J. Environ. Res. Public Health 2022, 19, 11739. https://doi.org/10.3390/ijerph191811739

Qiu W, Wu T, Xue P. Can Mobile Payment Increase Household Income and Mitigate the Lower Income Condition Caused by Health Risks? Evidence from Rural China. International Journal of Environmental Research and Public Health. 2022; 19(18):11739. https://doi.org/10.3390/ijerph191811739

Chicago/Turabian StyleQiu, Weisong, Tieqi Wu, and Peng Xue. 2022. "Can Mobile Payment Increase Household Income and Mitigate the Lower Income Condition Caused by Health Risks? Evidence from Rural China" International Journal of Environmental Research and Public Health 19, no. 18: 11739. https://doi.org/10.3390/ijerph191811739

APA StyleQiu, W., Wu, T., & Xue, P. (2022). Can Mobile Payment Increase Household Income and Mitigate the Lower Income Condition Caused by Health Risks? Evidence from Rural China. International Journal of Environmental Research and Public Health, 19(18), 11739. https://doi.org/10.3390/ijerph191811739