Financial Behavioral Health and Investment Risk Willingness: Implications for the Racial Wealth Gap

Abstract

:1. Introduction

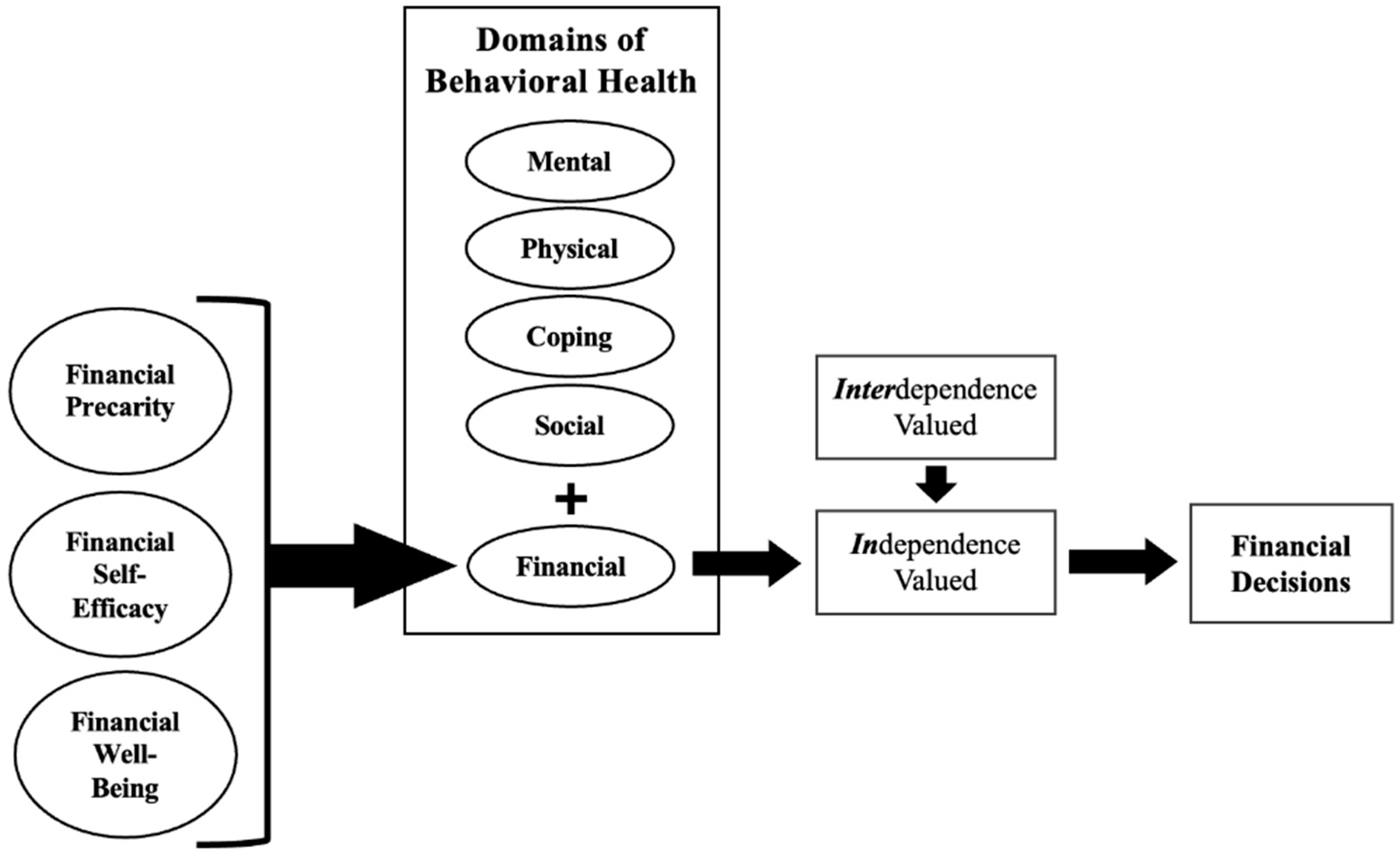

2. Financial Behavioral Health (FBH)

2.1. Financial Precarity (FP)

2.2. Financial Self-Efficacy (FSE)

2.3. Financial Well-Being (FWB)

2.4. Conceptual Model

3. Research Aims

4. Materials and Methods

4.1. Sample and Source of Information

4.2. Measures

4.2.1. Aim 1: FBH Component Development

4.2.2. Aim 2: FBH Construct

4.2.3. Aim 3: FBH Differences by Racial Group Affiliation

4.2.4. Aim 4: FBH on Investment Risk Willingness

4.3. Data Analyses

5. Results

5.1. Sample Description

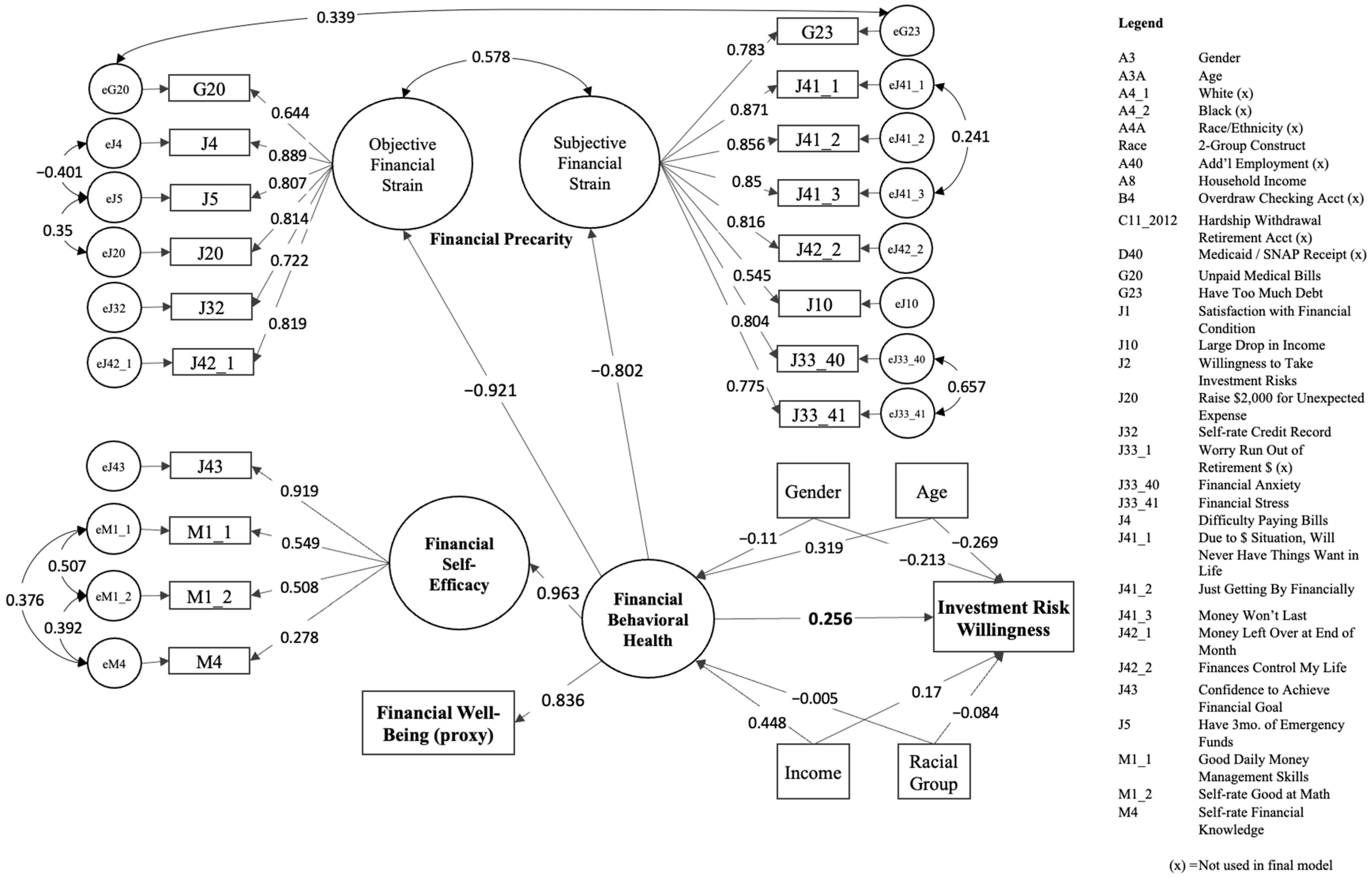

5.2. FBH Model Construction

5.2.1. Financial Precarity (FP)

5.2.2. Financial Self-Efficacy (FP)

5.2.3. Financial Behavioral Health (FBH)

5.3. FBH Model Analysis

5.3.1. Measurement Invariance

5.3.2. FBH Model by Racial Group

5.4. FBH Model Applied to Investment Risk Willingness

6. Discussion

6.1. Strengths and Limitations

6.2. Future Research and Implications

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

Appendix B

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Black Respondent Sub-Sample | White Respondent Sub-Sample | Welch Two Sample t-Test | Chi-Square Test | ||

|---|---|---|---|---|---|---|

| M (SD) | M (SD) | t (df) *** | 95% CI | χ2 (df) | p | |

| Age | 41.026 (15.420) | 49.613 (16.722) | −27.568 (3779) | [−9.197, −7.975] | 855.650 (80) | *** |

| Gender | 0.004 (1) | 0.949 | ||||

| Census Division | 192,992.000 (64) | *** | ||||

| Edu Level Attained | 4.145 | 4.442 | −9.110 (3769) | [−0.361, −0.233] | 152.350 (6) | *** |

| Household Income | 3.766 (2.055) | 4.593 (2.048) | −20.128 (3625) | [−0.907, −0.746] | 460.210 (7) | *** |

| Dependent Children | 2.526 | 2.291 | 7.986 (3419) | [0.177, 0.293] | 314.770 (5) | *** |

| Financial Satisfaction | 5.308 (3.161) | 5.793 (2.842) | −7.676 (3385) | [−0.609, −0.361] | 371.760 (9) | *** |

| Financial Anxiety | 4.725 (2.064) | 4.464 (2.017) | 6.285 (3510) | [0.180, 0.343] | 141.530 (6) | *** |

| Financial Stress | 4.348 (2.162) | 4.052 (2.067) | 6.818 (3479) | [0.211, 0.381] | 119.050 (6) | *** |

| Risk Willingness | 5.361 (3.071) | 4.788 (2.613) | 9.282 (3249) | [0.452, 0.693] | 585.290 (9) | *** |

References

- Asebedo, S.D.; Wilmarth, M.J. Does how we feel about financial strain matter for mental health? J. Financ. Ther. 2017, 8, 62–80. [Google Scholar] [CrossRef]

- Richardson, T.; Elliott, P.; Roberts, R. The relationship between personal unsecured debt and mental and physical health: A systematic review and meta-analysis. Clin. Psychol. Rev. 2013, 33, 1148–1162. [Google Scholar] [CrossRef] [PubMed]

- Compton, M.T.; Shim, R.S. (Eds.) The Social Determinants of Mental Health; American Psychiatric Publishing: Arlington, VA, USA, 2015. [Google Scholar]

- Mancini, M.A. Integrated Behavioral Health Practice; Springer International Publishing: Berlin/Heidelberg, Germany, 2021; ISBN 978-3-030-59658-3. [Google Scholar]

- SAMHSA Glossary of Terms and Acronyms for SAMHSA Grants. Available online: https://www.samhsa.gov/grants/grants-glossary (accessed on 19 April 2022).

- Mitchell, J.; Shan, G. Understanding the economic behavior of the medically uninsured in the United States. Hosp. Top. 2020, 98, 184–194. [Google Scholar] [CrossRef] [PubMed]

- Anvari-Clark, J. Most and Least Stressed States: Ask the Experts. Wallet Hub. 2021. Available online: https://wallethub.com/edu/most-stressful-states/32218#expert=Jeffrey_Anvari-Clark (accessed on 17 September 2021).

- Wolfsohn, R. Financial Behavior Health for You and Your Clients; Center for Financial Social Work: Huntersville, NC, USA, 2021; Available online: https://www.youtube.com/watch?v=KkNgg1yCD2g&t=1s (accessed on 17 September 2021).

- Wolfsohn, R. Financial Behavioral HealthTM a Client Necessity Post-Pandemic; Center for Financial Social Work: Huntersville, NC, USA, 2021; Available online: https://www.youtube.com/watch?v=luUIKw_xm-o&t=2207s (accessed on 17 September 2021).

- Klontz, B.T.; Britt, S.L.; Archuleta, K.L. (Eds.) Financial Therapy: Theory, Research, and Practice; Springer: Berlin/Heidelberg, Germany, 2015. [Google Scholar]

- Hoge, G.L.; Stylianou, A.M.; Hetling, A.; Postmus, J.L. Developing and validating the Scale of Economic Self-Efficacy. J. Interpers. Violence 2020, 35, 3011–3033. [Google Scholar] [CrossRef]

- Consumer Financial Protection Bureau. Financial Well-Being in America; Consumer Financial Protection Bureau: Washington, DC, USA, 2017. Available online: https://www.consumerfinance.gov/data-research/research-reports/financial-well-being-america/ (accessed on 16 January 2023).

- Meuris, J.; Leana, C. The price of financial precarity: Organizational costs of employees’ financial concerns. Organ. Sci. 2017, 29, 398–417. [Google Scholar] [CrossRef]

- Meuris, J.; Leana, C.R. The price of financial precarity: Personal finance as a barrier to work performance. Proceedings 2017, 2017, 12992. [Google Scholar] [CrossRef]

- Gaffney, A.W.; Himmelstein, D.U.; McCormick, D.; Woolhandler, S. Health and social precarity among Americans receiving unemployment benefits during the COVID-19 outbreak. J. Gen. Intern. Med. 2020, 35, 3416–3419. [Google Scholar] [CrossRef]

- Mullainathan, S.; Shafir, E. Scarcity: Why Having Too Little Means So Much; Times Books, Henry Holt: New York, NY, USA, 2013. [Google Scholar]

- Mullainathan, S.; Shafir, E. Freeing up intelligence. Sci. Am. Mind. 2013, 25, 58–63. [Google Scholar] [CrossRef]

- Hoopes, S. ALICE Report; United Way ALICE Project; United Ways of Maryland: Baltimore, MD, USA,, 2019; Available online: https://uwcm.org/alice (accessed on 15 January 2023).

- Beverly, S.G. Measures of material hardship: Rationale and recommendations. J. Poverty 2001, 5, 23–41. [Google Scholar] [CrossRef]

- Corman, H.; Noonan, K.; Reichman, N.E.; Schultz, J. Effects of financial insecurity on social interactions. J. Socio-Econ. 2012, 41, 574–583. [Google Scholar] [CrossRef]

- Hardy, B.; Ziliak, J.P. Decomposing trends in income volatility: The “wild ride” at the top and bottom. Econ. Inq. 2014, 52, 459–476. [Google Scholar] [CrossRef]

- Ziliak, J.P.; Hardy, B.; Bollinger, C. Earnings volatility in America: Evidence from Matched CPS. Labour Econ. 2011, 18, 742–754. [Google Scholar] [CrossRef]

- Friedline, T.; Chen, Z. Digital redlining and the fintech marketplace: Evidence from U.S. zip codes. J. Consum. Aff. 2020, 55, 366–388. [Google Scholar] [CrossRef]

- Karger, H. Shortchanged: Life and Debt in the Fringe Economy; Berrett-Koehler Publishers: San Francisco, CA, USA, 2005. [Google Scholar]

- Mukherjee, K.; Nobles-Knight, D. Assessment of trade-offs made by people due to financial stress from medical care in the USA. J. Pharm. Health Serv. Res. 2013, 4, 95–99. [Google Scholar] [CrossRef]

- Desmond, M.; Gershenson, C.; Kiviat, B. Forced relocation and residential instability among urban renters. Soc. Serv. Rev. 2015, 89, 227–262. [Google Scholar] [CrossRef]

- Desmond, M.; Kimbro, R.T. Eviction’s fallout: Housing, hardship, and health. Soc. Forces 2015, 94, 295–324. [Google Scholar] [CrossRef]

- Ortiz, S.E.; Johannes, B.L. Building the case for housing policy: Understanding public beliefs about housing affordability as a key social determinant of health. SSM -Popul. Health 2018, 6, 63–71. [Google Scholar] [CrossRef]

- Zaloom, C. Indebted: How Families Make College Work at Any Cost; Princeton University Press: Princeton, NJ, USA, 2019. [Google Scholar]

- Zhang, Q.; Kim, H. American young adults’ debt and psychological distress. J. Fam. Econ. Issues 2019, 40, 22–35. [Google Scholar] [CrossRef]

- Sherraden, M. Building blocks of financial capability. In Financial Capability and Asset Development: Research, Education, Policy, and Practice; Birkenmaier, J., Sherraden, M., Curley, J., Eds.; Oxford University Press: New York, NY, USA, 2013; pp. 3–43. [Google Scholar]

- Lown, J.M. Outstanding AFCPE® Conference Paper: Development and validation of a financial self-efficacy scale. J. Financ. Couns. Plan. 2011, 22, 11. [Google Scholar]

- Bandura, A. Self-efficacy: Toward a unifying theory of behavioral change. Psychol. Rev. 1977, 84, 191–215. [Google Scholar] [CrossRef]

- Rosenstock, I.M.; Strecher, V.J.; Becker, M.H. Social learning theory and the health belief model. Health Educ. Q. 1988, 15, 175–183. [Google Scholar] [CrossRef] [PubMed]

- Postmus, J.L. Economic Empowerment of Domestic Violence Survivors; Applied Research Forum, National Resource Center on Domestic Violence: Harrisburg, PA, USA, 2010. Available online: http://www.ncdsv.org/images/VAWnet_EcoEmpowermentDVSurvivors_10-2010.pdf (accessed on 15 January 2023).

- O’Neill, B.; Xiao, J.J.; Ensle, K. Positive health and financial practices: Does budgeting make a difference? J. Fam. Consum. Sci. 2017, 109, 27–36. [Google Scholar] [CrossRef]

- Gross, K.S.M.A.R.T. Financial Goals. Available online: https://www.unitedwaygmwc.org/Speak-United-Blog/SMART-Financial-Goals (accessed on 11 August 2021).

- Sorgente, A.; Totenhagen, C.J.; Lanz, M. The use of the intensive longitudinal methods to study financial well-being: A scoping review and future research agenda. J. Happiness Stud. 2021, 23, 333–358. [Google Scholar] [CrossRef] [PubMed]

- Netemeyer, R.G.; Warmath, D.; Fernandes, D.; Lynch, J.G. How am I doing? Perceived financial well-being, its potential antecedents, and its relation to overall well-being. J. Consum. Res. 2018, 45, 68–89. [Google Scholar] [CrossRef]

- Collins, J.M.; Urban, C. Measuring financial well-being over the lifecourse. Eur. J. Financ. 2019, 26, 341–359. [Google Scholar] [CrossRef]

- Anvari-Clark, J.; Ansong, D. Predicting financial well-being using the financial capability perspective: The roles of financial shocks, income volatility, financial products, and savings behaviors. J. Fam. Econ. Issues 2022, 43, 730–743. [Google Scholar] [CrossRef]

- Sarkisian, N.; Gerstel, N. Kin support among Blacks and Whites: Race and family organization. Am. Sociol. Rev. 2004, 69, 812–837. [Google Scholar] [CrossRef]

- Gerstel, N. Rethinking families and community: The color, class, and centrality of extended kin ties. In Sociological Forum; Blackwell Publishing Ltd.: Oxford, UK, 2011; Volume 26, pp. 1–20. [Google Scholar] [CrossRef]

- Danes, S.M.; Meraz, A.A.; Landers, A.L. Cultural meanings of resource management for Mexican–Americans. J. Fam. Econ. Issue 2016, 37, 607–623. [Google Scholar] [CrossRef]

- Demosthenous, C.; Robertson, B.; Cabraal, A.; Singh, S. Cultural Identity and Financial Literacy: Australian Aboriginal Experiences of Money and Money Management; RMIT University: Melbourne, Australia, 2006. [Google Scholar]

- Morduch, J.; Schneider, R. The Financial Diaries; Princeton University Press: Princeton, NJ, USA, 2017. [Google Scholar]

- Stack, C. All Our Kin; Basic Books: New York, NY, USA, 1974. [Google Scholar]

- Warmath, D.; Chen, P.-J.; Grable, J.; Kwak, E.J. Soft landings: Extending the cushion hypothesis to financial well-being in collectivistic cultures. J. Consum. Aff. 2021, 55, 1563–1590. [Google Scholar] [CrossRef]

- Chiteji, N.S.; Stafford, F.P. Portfolio choices of parents and their children as young adults: Asset accumulation by African-American families. Am. Econ. Rev. 1999, 89, 377–380. [Google Scholar] [CrossRef]

- Grable, J.E. Financial risk tolerance. In Handbook of Consumer Finance Research; Xiao, J.J., Ed.; Springer International Publishing: Berlin/Heidelberg, Germany, 2016; pp. 19–32. ISBN 978-3-319-28885-7. [Google Scholar]

- Hasler, A.; Lusardi, A.; Valdes, O. Financial Anxiety and Stress among U.S. Households: New Evidence from the National Financial Capability Study and Focus Groups; Global Financial Literacy Excellence Center and FINRA Investor Education Foundation: Washington, DC, USA, 2021; Available online: https://gflec.org/wp-content/uploads/2021/04/Anxiety-and-Stress-Report-GFLEC-FINRA-FINAL.pdf?x55020 (accessed on 15 January 2023).

- Gambetti, E.; Giusberti, F. The effect of anger and anxiety traits on investment decisions. J. Econ. Psychol. 2012, 33, 1059–1069. [Google Scholar] [CrossRef]

- Lusardi, A. Financial Well-Being of the Millennial Generation: An In-Depth Analysis of Its Drivers and Implications; Global Financial Literacy Excellence Center: Washington, DC, USA, 2019; Available online: https://gflec.org/wp-content/uploads/2019/12/Financial-Well-Being-of-the-Millennial-Generation-Paper-20191122.pdf?x70470 (accessed on 15 January 2023).

- Jayakody, R. Race differences in intergenerational financial assistance: The needs of children and the resources of parents. J. Fam. Issues 1998, 19, 508–533. [Google Scholar] [CrossRef]

- Taylor, R.J.; Chatters, L.M.; Woodward, A.T.; Brown, E. Racial and ethnic differences in extended family, friendship, fictive kin, and congregational informal support networks. Fam. Relat. 2013, 62, 609–624. [Google Scholar] [CrossRef]

- Rondini, A.C.; Kowalsky, R.H. “First do no harm”: Clinical practice guidelines, mesolevel structural racism, and medicine’s epistemological reckoning. Soc. Sci. Med. 2021, 279, 113968. [Google Scholar] [CrossRef]

- Neal, K. Not by Proxy: Arguments for improving the use of race in biomedical research. Am. J. Bioeth. 2017, 17, 52–54. [Google Scholar] [CrossRef]

- Zuberi, T.; Bonilla-Silva, E. (Eds.) White Logic, White Methods: Racism and Methodology; Rowman & Littlefield Publishers: Lanham, MD, USA, 2008. [Google Scholar]

- Jones, C.P. Levels of racism: A theoretic framework and a gardener’s tale. Am. J. Public Health 2000, 90, 1212–1215. [Google Scholar] [CrossRef]

- Pearson, J.L.; Waa, A.; Siddiqi, K.; Edwards, R.; Nez Henderson, P.; Webb Hooper, M. Naming racism, not race, as a determinant of tobacco-related health disparities. Nicotine Tob. Res. 2021, 23, 885–887. [Google Scholar] [CrossRef]

- Phelan, J.C.; Link, B.G. Is racism a fundamental cause of inequalities in health? Annu. Rev. Sociol. 2015, 41, 311–330. [Google Scholar] [CrossRef]

- Boyd, R.W.; Lindo, E.G.; Weeks, L.D.; McLemore, M.R. On Racism: A New Standard for Publishing on Racial Health Inequities. Available online: http://www.healthaffairs.org/do/10.1377/hblog20200630.939347/full/ (accessed on 5 August 2021).

- Ross, P.T.; Hart-Johnson, T.; Santen, S.A.; Zaidi, N.L.B. Considerations for using race and ethnicity as quantitative variables in medical education research. Perspect. Med. Educ. 2020, 9, 318–323. [Google Scholar] [CrossRef]

- Assari, S.; Curry, T.J. Parental education ain’t enough: A study of race (racism), parental education, and children’s thalamus volume. J. Educ. Cult. Stud. 2021, 5, 1–21. [Google Scholar] [CrossRef]

- Bernaola, D.M.V.; Willows, G.D.; West, D. The relevance of anger, anxiety, gender and race in investment decisions. Mind. Soc. 2021, 20, 1–21. [Google Scholar] [CrossRef]

- Heo, W.; Grable, J.E.; O’Neill, B. Wealth Accumulation inequality: Does investment risk tolerance and equity ownership drive wealth accumulation? Soc. Indic. Res. 2017, 133, 209–225. [Google Scholar] [CrossRef]

- Coleman, S. Risk tolerance and the investment behavior of Black and Hispanic heads of household. J. Financ. Couns. Plan. 2013, 14. [Google Scholar]

- Yao, R.; Gutter, M.; Hanna, S. The financial risk tolerance of Blacks, Hispanics and Whites. Financ. Couns. Plan. 2005, 16, 51–62. [Google Scholar]

- FINRA Investor Education Foundation. National Financial Capability Study: 2018 State-by-State Survey [Data Set]. 2018. Available online: https://www.usfinancialcapability.org/downloads.php (accessed on 15 January 2023).

- ARC Research; FINRA Investor Education Foundation. 2018 National Financial Capability Study: State-by-State Survey Methodology. 2018. Available online: https://finrafoundation.org/sites/finrafoundation/files/NFCS-2018-State-by-State-Methodology.pdf (accessed on 15 January 2023).

- Consumer Financial Protection Bureau. CFPB Financial Well-Being Scale: Scale Development Technical Report. Consumer Financial Protection Bureau: Washington, DC, USA, 2017. Available online: https://www.consumerfinance.gov/data-research/research-reports/financial-well-being-scale/ (accessed on 15 January 2023).

- Chang, M.L. Shortchanged: Why Women Have Less Wealth and What Can Be Done About It; Oxford University Press: New York, NY, USA, 2010. [Google Scholar]

- Chang, M.L. Lifting as We Climb: Women of Color, Wealth, and America’s Future; Insight Center for Community Economic Development: Oakland, CA, USA, 2010; Available online: https://www.mariko-chang.com/s/Lifting_As_We_Climb_InsightCCED_2010.pdf (accessed on 15 January 2023).

- Harrington, D. Confirmatory Factor Analysis; Oxford University Press: Oxford, UK, 2009. [Google Scholar]

- Bowen, N.K.; Guo, S. Structural Equation Modeling; Pocket Guides to Social Work Research Methods; Oxford University Press: Oxford, UK, 2012. [Google Scholar]

- R Core Team. R: A Language and Environment for Statistical Computing, [Software Version 4.0.5]; R Foundation for Statistical Computing: Vienna, Austria, 2021; Available online: https://www.R-project.org (accessed on 15 January 2023).

- Rosseel, Y. Lavaan: An R package for structural equation modeling. J. Stat. Softw. 2012, 48, 1–36. [Google Scholar] [CrossRef]

- Bollen, K. Modeling strategies: In search of the holy grail. Struct. Equ. Model. Multidiscip. J. 2000, 7, 74–81. [Google Scholar] [CrossRef]

- Collins, J.M.; Urban, C. Understanding Financial Well-Being Over the Lifecourse: An Exploration of Measures; 2018, Unpublished Manuscript. Available online: https://www.montana.edu/urban/Draft_FWB_2018%20Anonymous.pdf (accessed on 15 January 2023).

- Knoll, M.A.Z.; Houts, C.R. The Financial Knowledge Scale: An application of item response theory to the assessment of financial literacy. J. Consum. Aff. 2012, 46, 381–410. [Google Scholar] [CrossRef]

- Watkins, M.W. Exploratory factor analysis: A guide to best practice. J. Black Psychol. 2018, 44, 219–246. [Google Scholar] [CrossRef]

- Sass, D.A.; Schmitt, T.A. A comparative investigation of rotation criteria within exploratory factor analysis. Multivar. Behav. Res. 2010, 45, 73–103. [Google Scholar] [CrossRef]

- Rosseel, Y. The Lavaan Tutorial. Available online: https://lavaan.ugent.be/tutorial/index.html (accessed on 24 January 2022).

- Li, C.-H. Confirmatory factor analysis with ordinal data: Comparing robust maximum likelihood and diagonally weighted least squares. Behav. Res. 2016, 48, 936–949. [Google Scholar] [CrossRef]

- Rosseel, Y.; Jorgensen, T.D.; Rockwood, N.; Oberski, D.; Byrnes, J.; Vanbrabant, L.; Savalei, V.; Merkle, E.; Hallquist, M.; Rhemtulla, M.; et al. lavaan: Latent Variable Analysis, [Software Version 0.6-9]. 2021. Available online: https://cran.r-project.org/package=lavaan (accessed on 27 June 2021).

- Schumacker, R.E.; Lomax, R.G. A Beginner’s Guide to Structural Equation Modeling, 3rd ed.; Taylor & Francis: New York, NY, USA, 2010. [Google Scholar]

- Kaiser, H.F. An index of factorial simplicity. Psychometrika 1974, 39, 31–36. [Google Scholar] [CrossRef]

- Tabachnick, B.G.; Fidell, L.S. Using Multivariate Statistics, 6th ed.; Pearson: London, UK, 2014. [Google Scholar]

- Schmitt, T.A. Current methodological considerations in exploratory and confirmatory factor analysis. J. Psychoeduc. Assess. 2011, 29, 304–321. [Google Scholar] [CrossRef]

- Kaiser, T.; Lusardi, A.; Menkhoff, L.; Urban, C.J. Financial Education Affects Financial Knowledge and Downstream Behaviors; NBER Working Paper Series, Number 27057; National Bureau of Economic Research: Cambridge, MA, USA, 2020; Available online: http://www.nber.org/papers/w27057 (accessed on 15 January 2023).

- Wilmarth, M.J. Financial and economic well-being: A decade review from Journal of Family and Economic Issues. J. Fam. Econ. Issue 2020, 42, 124–130. [Google Scholar] [CrossRef]

- Skagerlund, K.; Lind, T.; Strömbäck, C.; Tinghög, G.; Västfjäll, D. Financial literacy and the role of numeracy–How individuals’ attitude and affinity with numbers influence financial literacy. J. Behav. Exp. Econ. 2018, 74, 18–25. [Google Scholar] [CrossRef]

- Gelman, A.; Hill, J.; Vehtari, A. Regression and Other Stories; Cambridge University Press: New York, NY, USA, 2021. [Google Scholar]

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences, 2nd ed.; Lawrence Erlbaum Associates: Mahwah, NJ, USA, 1988. [Google Scholar]

- Consumer Financial Protection Bureau. National Financial Well-Being Survey: Public Use File User Guide; Consumer Financial Protection Bureau: Washington, DC, USA, 2017. Available online: https://www.consumerfinance.gov/documents/5588/cfpb_nfwbs-puf-user-guide.pdf (accessed on 15 January 2023).

- Muruthi, B.; Watkins, K.; McCoy, M.; Muruthi, J.R.; Kiprono, F.J. “I feel happy that I can be useful to others”: Preliminary study of East African women and their remittance behavior. J. Fam. Econ. Issue 2017, 38, 315–326. [Google Scholar] [CrossRef]

- Epstein, J.; Santo, R.M.; Guillemin, F. A review of guidelines for cross-cultural adaptation of questionnaires could not bring out a consensus. J. Clin. Epidemiol. 2015, 68, 435–441. [Google Scholar] [CrossRef]

- Fraser, M.W.; Richman, J.M.; Galinsky, M.J.; Day, S.H. Intervention Research: Developing Social Programs; Pocket Guides to Social Work Research Methods; Oxford University Press: Oxford, UK, 2009. [Google Scholar]

- Cornelius, L.J.; Harrington, D. A Social Justice Approach to Survey Design and Analysis; Pocket Guides to Social Work Research Methods; Oxford University Press: Oxford, UK, 2014. [Google Scholar]

- Asante-Muhammad, D.; Collins, C.; Hoxie, J.; Nieves, E. The Road to Zero Wealth: How the Racial Wealth Divide Is Hollowing out America’s Middle Class; Prosperity Now & Institute for Policy Studies: Washington, DC, USA, 2017. [Google Scholar]

- Gutter, M.S.; Fontes, A. Racial differences in risky asset ownership: A two-stage model of the investment decision-making process. J. Financ. Couns. Plan. 2006, 17, 64–78. [Google Scholar]

- Fergus, D.; Shanks, T.R. The long afterlife of slavery in asset stripping, historical memory, and family burden: Toward a Third Reconstruction. Fam. Soc. 2022, 103, 7–20. [Google Scholar] [CrossRef]

- Ellsworth, S. Death in a Promised Land: The Tulsa Race Riot of 1921; Louisiana State University Press: Baton Rouge, LA, USA, 1992; ISBN 978-0-8071-1767-5. [Google Scholar]

- Association of African American Financial Advisors. Available online: https://www.aaafainc.com (accessed on 20 February 2022).

- Loibl, C.; Hira, T.K. Financial issues of women. In Handbook of Consumer Finance Research; Xiao, J.J., Ed.; Springer International Publishing: Berlin/Heidelberg, Germany, 2016; pp. 195–204. ISBN 978-3-319-28885-7. [Google Scholar]

- Archuleta, K.L.; Dale, A.; Spann, S.M. College students and financial distress: Exploring debt, financial satisfaction, and financial anxiety. J. Financ. Couns. Plan. 2013, 24, 50–62. [Google Scholar]

- García-Garzón, E.; Nieto, M.D.; Garrido, L.E.; Abad, F.J. Bi-factor exploratory structural equation modeling done right: Using the SLiDapp application. Psicothema 2020, 32, 607–614. [Google Scholar] [CrossRef]

- Dahl, M.; DeLeire, T.; Mok, S. Food insufficiency and income volatility in US households: The effects of imputed income in the Survey of Income and Program Participation. Appl. Econ. Perspect. Policy 2014, 36, 416–437. [Google Scholar] [CrossRef]

- Nunley, J.M.; Seals, A. The effects of household income volatility on divorce. Am. J. Econ. Sociol. 2010, 69, 983–1010. [Google Scholar] [CrossRef]

- Mansour, F. Economic insecurity and fertility: Does income volatility impact the decision to remain a one-child family? J. Fam. Econ. Issues 2018, 39, 243–257. [Google Scholar] [CrossRef]

- Compton, M.T.; Shim, R.S. The social determinants of mental health. FOC 2015, 13, 419–425. [Google Scholar] [CrossRef]

- Anvari-Clark, J.; Frey, J.J. Financial capability and behavioral health. In The Routledge Handbook on Financial Social Work: Direct Practice with Vulnerable Populations; Callahan, C., Frey, J.J., Imboden, R., Eds.; Taylor & Francis: New York, NY, USA, 2019; pp. 61–72. [Google Scholar]

- Agency for Healthcare Research and Quality MEPS-HC Panel Design and Collection Process. Available online: https://meps.ahrq.gov/mepsweb/survey_comp/hc_data_collection.jsp (accessed on 16 November 2020).

| Measure | Name | Number (Position) | Scale Score | Reverse Coded | Informed by CFPB FWB Scale |

|---|---|---|---|---|---|

| Financial Precarity | |||||

| Objective Measures | Took on additional employment | A40 (22) | 1 = Yes, 2 = No | R | |

| Difficulty paying bills | J4 (32) | 1 = Very difficult, 2 = Somewhat difficult, 3 = Not at all difficult | R | ||

| Having three months’ worth of emergency funds | J5 (34) | 1 = Yes, 2 = No | |||

| Experienced a large income drop | J10 (38) | 1 = Yes, 2 = No | R | ||

| Confidence to handle a $2000 financial shock | J20 (39) | 1 = I am certain I could come up with the full $2000, 2 = I could probably come up with $2000, 3 = I could probably not come up with $2000, 4 = I am certain I could not come up with $2000 | Yes | ||

| Self-rating of credit | J32 (40) | 1 = Very bad, 2 = Bad, 3 = About average, 4 = Good, 5 = Very good | R | ||

| Frequency of having money left over at the end of the month | J42_1 (47) | 1 = Never, 2 = Rarely, 3 = Sometimes, 4 = Often, 5 = Always | R | Yes | |

| Overdrawing on a checking account | B4 (52) | 1 = Yes, 2 = No | R | ||

| Hardship withdrawal from retirement account | C11_2012 (66) | 1 = Yes, 2 = No | R | ||

| Use of Medicaid/SNAP | D40 (70) | 1 = Yes, 2 = No | R | ||

| Outstanding medical debt | G20 (85) | 1 = Yes, 2 = No | R | ||

| Subjective Measures | Because of my financial situation, I feel like I will never have the things I want in life | J41_1 (44) | 1 = Does not describe me at all, 2 = Describes me very little, 3 = Describes me somewhat, 4 = Describes me very well, 5 = Describes me completely | Yes | |

| I am just getting by financially | J41_2 (45) | 1 = Does not describe me at all, 2 = Describes me very little, 3 = Describes me somewhat, 4 = Describes me very well, 5 = Describes me completely | Yes | ||

| Concerned that money I have or will save won’t last | J41_3 (46) | 1 = Does not describe me at all, 2 = Describes me very little, 3 = Describes me somewhat, 4 = Describes me very well, 5 = Describes me completely | Yes | ||

| My finances control my life | J42_2 (48) | 1 = Never, 2 = Rarely, 3 = Sometimes, 4 = Often, 5 = Always | Yes | ||

| I have too much debt right now | G23 (104) | 1 = Strongly disagree, 2, 3, 4 = Neither agree nor disagree, 5, 6, 7 = Strongly agree | |||

| Financial Self-Efficacy | |||||

| Confidence in ability to achieve a financial goal | J43 (49) | 1 = Not at all confident, 2 = Not very confident, 3 = Somewhat confident, 4 =Very confident | |||

| Worry about running out of money in retirement | J33_1 (41) | 1 = Strongly disagree, 2, 3, 4 = Neither agree nor disagree, 5, 6, 7 = Strongly agree | R | ||

| Good at dealing with day-to-day financial matters, such as checking accounts, credit and debit cards, and tracking expenses; | M1_1 (109) | 1 = Strongly disagree, 2, 3, 4 = Neither agree nor disagree, 5, 6, 7 = Strongly agree | |||

| Self-assessed ability, being pretty good at math | M1_2 (110) | 1 = Strongly disagree, 2, 3, 4 = Neither agree nor disagree, 5, 6, 7 = Strongly agree | |||

| Self-assessed overall financial knowledge. | M4 (111) | 1 =Very low, 2, 3, 4, 5, 6, 7 = Very high |

| Demographic Characteristics | Full Sample | Combined Sub-Sample | White Respondent Sub-Sample | Black Respondent Sub-Sample |

|---|---|---|---|---|

| (N = 27,091) | (n = 24,124) | (n = 21,289) | (n = 2835) | |

| M (SD)/# (%) | M (SD)/# (%) | M (SD)/# (%) | M (SD)/# (%) | |

| Age | 48 (17) | 49 (17) | 50 (17) | 41 (15) |

| Gender | ||||

| Male | 11,956 (44%) | 10,680 (44%) | 9427 (44%) | 1253 (44%) |

| Female | 15,135 (56%) | 13,444 (56%) | 11,862 (56%) | 1582 (56%) |

| Race/Ethnicity | ||||

| White non-Hispanic | 20,099 (74%) | 20,099 (83%) | 20,099 (94%) | 0 (0%) |

| Black non-Hispanic | 2576 (10%) | 2576 (11%) | 0 (0%) | 2576 (91%) |

| Hispanic (any race) | 2338 (9%) | 922 (4%) | 814 (4%) | 108 (4%) |

| Asian non-Hispanic | 1210 (4%) | 0 (0%) | 0 (0%) | 0 (0%) |

| Other, Multiple non-Hispanic Ethnicities | 868 (3%) | 527 (2%) | 376 (2%) | 151 (5%) |

| Edu Level Attained | ||||

| <HS | 697 (3%) | 609 (3%) | 522 (2%) | 87 (3%) |

| High school—Diploma | 4900 (18%) | 4452 (18%) | 3914 (18%) | 538 (19%) |

| High school—GED/Alt | 1919 (7%) | 1699 (7%) | 1480 (7%) | 219 (8%) |

| Some college | 7263 (27%) | 6531 (27%) | 5565 (26%) | 966 (34%) |

| Associate’s Degree | 2864 (11%) | 2528 (10%) | 2220 (10%) | 308 (11%) |

| Bachelor’s Degree | 5905 (22%) | 5192 (22%) | 4700 (22%) | 492 (17%) |

| Post graduate degree | 3543 (13%) | 3113 (13%) | 2888 (14%) | 225 (8%) |

| Household Income | ||||

| <$15,000 | 3041 (11%) | 2632 (11%) | 2053 (10%) | 579 (20%) |

| $15,000–$24,999 | 2804 (10%) | 2509 (10%) | 2139 (10%) | 370 (13%) |

| $25,000–$34,999 | 2934 (11%) | 2590 (11%) | 2246 (11%) | 344 (12%) |

| $35,000–$49,999 | 3917 (14%) | 3497 (14%) | 3099 (15%) | 398 (14%) |

| $50,000–$74,999 | 5259 (19%) | 4694 (19%) | 4198 (20%) | 496 (17%) |

| $75,000–$99,999 | 3856 (14%) | 3472 (14%) | 3106 (15%) | 366 (13%) |

| $100,000–$149,999 | 3439 (13%) | 3099 (13%) | 2901 (14%) | 198 (7%) |

| ≥$150,000 | 1841 (7%) | 1631 (7%) | 1547 (7%) | 84 (3%) |

| No. of Financially Dependent Children | ||||

| Do not have any children | 9006 (33%) | 7823 (32%) | 6832 (32%) | 991 (35%) |

| No financially dependent children | 8471 (31%) | 8004 (33%) | 7438 (35%) | 566 (20%) |

| 1 financially dependent child | 4198 (15%) | 3635 (15%) | 3080 (14%) | 555 (20%) |

| 2 financially dependent children | 3255 (12%) | 2789 (12%) | 2418 (11%) | 371 (13%) |

| 3 financially dependent children | 1355 (5%) | 1186 (5%) | 964 (5%) | 222 (8%) |

| 4 or more financially dependent children | 806 (3%) | 687 (3%) | 557 (3%) | 130 (5%) |

| Financial Satisfaction | 5.72 (2.88) | 5.74 (2.89) | 5.79 (2.84) | 5.31 (3.16) |

| Financial Anxiety | 4.51 (2.02) | 4.49 (2.02) | 4.46 (2.02) | 4.73 (2.06) |

| Financial Stress | 4.12 (2.07) | 4.09 (2.08) | 4.05 (2.07) | 4.35 (2.16) |

| Investment Risk Willingness | 4.91 (2.68) | 4.85 (2.68) | 4.79 (2.61) | 5.36 (3.07) |

| Model Construction | n | χ2 (df) *** | SRMR | CFI | TLI | RMSEA [90% CI] | Δχ2 (df) |

|---|---|---|---|---|---|---|---|

| FP | |||||||

| Original EFA | 12,288 | 3822.4 (89) | 0.049 | 0.993 | 0.991 | 0.058 [0.057, 0.06] | |

| Final EFA | 20,590 | 4879.999 (76) | 0.059 | 0.995 | 0.994 | 0.055 [0.054, 0.057] | (NA—different variables) |

| Original CFA | 22,302 | 6201.99 (53) | 0.057 | 0.994 | 0.993 | 0.072 [0.071, 0.074] | 8582.2 (76) *** |

| Final CFA | 22,302 | 4083.276 (49) | 0.048 | 0.996 | 0.995 | 0.061 [0.059, 0.062] | 3088.2 (4) *** |

| FSE | |||||||

| Original EFA | 24,849 | 3057.167 (5) | 0.081 | 0.955 | 0.91 | 0.157 [0.152, 0.161] | |

| Final EFA | 25,269 | 449.621 (2) | 0.038 | 0.992 | 0.976 | 0.094 [0.087, 0.102] | (NA—different variables) |

| Original CFA | 25,269 | 449.621 (2) | 0.038 | 0.992 | 0.976 | 0.094 [0.087, 0.102] | 0 (0) |

| Final CFA | 25,269 | 159.7976 (1) | 0.021 | 0.997 | 0.983 | 0.079 [0.069, 0.09] | 643.42 (1) *** |

| FBH | |||||||

| Original CFA | 19,232 | 34,696.4 (149) | 0.08 | 0.983 | 0.981 | 0.11 [0.109, 0.111] | |

| CFA w/all way correlations | DNC | ||||||

| Final CFA | 19,232 | 10,311.06 (140) | 0.049 | 0.995 | 0.994 | 0.061 [0.06, 0.062] | 5297.2 (9) *** |

| Model Assessments | |||||||

| Multiple Group Analysis | W = 17,192, B = 2040 | 12,252.39 (280) | 0.049 | 0.994 | 0.993 | 0.067 [0.066, 0.068] | |

| MI: loadings constrained | W = 17,192, B = 2040 | DNC | |||||

| MI: intercepts constrained | W = 17,192, B = 2040 | 13,191.54 (337) | 0.049 | 0.994 | 0.994 | 0.063 [0.062, 0.064] | 543.58 (57) *** |

| MI: intercepts + residual covariances constrained | W = 17,192, B = 2040 | 13,367.8 (345) | 0.049 | 0.994 | 0.994 | 0.063 [0.062, 0.064] | 63.35 (8) *** |

| Partial Invariance (loadings constrained) | DNC for any combination of freed latent factors | ||||||

| Black respondent model fit | 2040 | 5851.964 (140) | 0.127 | 0.952 | 0.941 | 0.141 [0.138, 0.145] | |

| White respondent model fit | 17,192 | 6400.366 (140) | 0.04 | 0.997 | 0.996 | 0.051 [0.05, 0.052] | |

| Applied Model (no covariates) | DNC | ||||||

| Applied Model (with covariates) | 19,031 | 20,746.71 (230) | 0.061 | 0.983 | 0.986 | 0.068 [0.068, 0.069] |

| Component Models | Financial Precarity | Financial Self-Efficacy | |||||

|---|---|---|---|---|---|---|---|

| Objective | Subjective | ||||||

| Item No. | Description | Estimate | p | Estimate | p | Estimate | p |

| A40 | Add’l Employment (x) | ||||||

| J4 | Bill Difficulty | 0.906 | |||||

| J5 | Emergency Funds | 0.812 | *** | ||||

| J10 | Income Drop | 0.592 | |||||

| J20 | Raise $2000 | 0.831 | *** | ||||

| J32 | Self-Rate Credit | 0.754 | *** | ||||

| J42_1 | Money Left Over | 0.786 | *** | ||||

| B4 | Overdraw Checking (x) | ||||||

| D40 | Medicaid/SNAP (x) | ||||||

| G20 | Medical Debt | 0.669 | *** | ||||

| J41_1 | Never Have Wants | 0.861 | *** | ||||

| J41_2 | Just Getting By | 0.875 | *** | ||||

| J41_3 | Money Won’t Last | 0.811 | *** | ||||

| J42_2 | Controls My Life | 0.801 | *** | ||||

| G23 | Too Much Debt | 0.751 | *** | ||||

| J43 | Goal Confidence | 0.473 | |||||

| M1_1 | Management Skills | 0.949 | *** | ||||

| M1_2 | Good at Math | 0.582 | *** | ||||

| M4 | Financial Knowledge | 0.892 | *** | ||||

| Covariances | |||||||

| Obj ⬄ | Subj | 0.872 | *** | ||||

| J41_1 ⬄ | J41_3 | 0.103 | *** | ||||

| J5 ⬄ | J20 | 0.12 | *** | ||||

| J4 ⬄ | J5 | −0.118 | *** | ||||

| G20 ⬄ | G23 | 0.151 | *** | ||||

| M1_1 ⬄ | M4 | −2.031 | *** | ||||

| Latent Variables | CFA FBH Combined Groups | CFA FBH Black Sub-Group | CFA FBH White Sub-Group | SEM Investment Risk | |||||

|---|---|---|---|---|---|---|---|---|---|

| n = 19,232 | n = 2040 | n = 17,192 | n = 19,031 | ||||||

| Item No. | Description | Estimate | p | Estimate | p | Estimate | p | Estimate | p |

| Obj ⇨ | |||||||||

| J4 | Bill Difficulty | 0.889 | *** | 0.786 | *** | 0.904 | *** | 0.889 | *** |

| J5 | Emergency Funds | 0.825 | *** | 0.749 | *** | 0.834 | *** | 0.807 | *** |

| J20 | Raise $2000 | 0.837 | *** | 0.772 | *** | 0.844 | *** | 0.814 | *** |

| J32 | Self-Rate Credit | 0.756 | *** | 0.632 | *** | 0.77 | *** | 0.722 | *** |

| J42_1 | Money Left Over | 0.808 | *** | 0.758 | *** | 0.818 | *** | 0.819 | *** |

| G20 | Medical Debt | 0.649 | *** | 0.435 | *** | 0.674 | *** | 0.644 | *** |

| Sub ⇨ | |||||||||

| J10 | Income Drop | 0.575 | *** | 0.594 | *** | 0.575 | *** | 0.545 | *** |

| J41_1 | Never Have Wants | 0.876 | *** | 0.86 | *** | 0.879 | *** | 0.871 | *** |

| J41_2 | Just Getting By | 0.872 | *** | 0.809 | *** | 0.877 | *** | 0.856 | *** |

| J41_3 | $ Won’t Last | 0.849 | *** | 0.845 | *** | 0.851 | *** | 0.85 | *** |

| J42_2 | Controls My Life | 0.812 | *** | 0.763 | *** | 0.819 | *** | 0.816 | *** |

| G23 | Too Much Debt | 0.763 | *** | 0.682 | *** | 0.77 | *** | 0.783 | *** |

| J33_40 | Financial Anxiety | 0.804 | *** | 0.776 | *** | 0.808 | *** | 0.804 | *** |

| J33_41 | Financial Stress | 0.773 | *** | 0.769 | *** | 0.774 | *** | 0.775 | *** |

| FSE ⇨ | |||||||||

| J43 | Goal Confidence | 0.851 | *** | 0.865 | 0.101 | 0.847 | *** | 0.919 | *** |

| M1_1 | Management Skills | 0.556 | *** | 0.53 | 0.098 | 0.553 | *** | 0.549 | *** |

| M1_2 | Good at Math | 0.322 | *** | 0.306 | 0.098 | 0.326 | *** | 0.508 | *** |

| M4 | Financial Knowledge | 0.518 | *** | 0.603 | 0.1 | 0.517 | *** | 0.278 | *** |

| FBH ⇨ | |||||||||

| Obj | Obj | −0.894 | *** | −0.887 | *** | −0.909 | *** | −0.921 | *** |

| Sub | Sub | −0.78 | *** | −0.313 | *** | −0.84 | *** | −0.802 | *** |

| FSE | FSE | 0.991 | *** | 0.987 | 0.104 | 0.99 | *** | 0.963 | *** |

| J1 | Financial Satisfaction | 0.836 | *** | 0.845 | *** | 0.839 | *** | 0.836 | *** |

| Covariances | |||||||||

| Obj ⬄ | Subj | 0.604 | *** | 0.962 | *** | 0.526 | *** | 0.578 | *** |

| J41_1 ⬄ | J41_3 | 0.237 | *** | 0.235 | *** | 0.234 | *** | 0.241 | *** |

| J5 ⬄ | J20 | 0.361 | *** | 0.473 | *** | 0.34 | *** | 0.35 | *** |

| J4 ⬄ | J5 | −0.44 | *** | −0.77 | *** | −0.389 | *** | −0.401 | *** |

| G20 ⬄ | G23 | 0.356 | *** | 0.465 | *** | 0.321 | *** | 0.339 | *** |

| J33_40 ⬄ | J33_41 | 0.666 | *** | 0.614 | *** | 0.672 | *** | 0.657 | *** |

| M1_2 ⬄ | M4 | 0.408 | *** | 0.393 | *** | 0.41 | *** | 0.392 | *** |

| M1_1 ⬄ | M4 | 0.378 | *** | 0.313 | *** | 0.388 | *** | 0.376 | *** |

| M1_1 ⬄ | M1_2 | 0.5 | *** | 0.431 | *** | 0.51 | *** | 0.507 | *** |

| Regressions | |||||||||

| Inv Risk ⇦ | Gender | −0.213 | *** | ||||||

| Income | 0.17 | *** | |||||||

| Age | −0.269 | *** | |||||||

| Racial Group | −0.084 | *** | |||||||

| FBH ⇦ | Gender | −0.11 | *** | ||||||

| Income | 0.448 | *** | |||||||

| Age | 0.319 | *** | |||||||

| Racial Group | −0.005 | 0.428 | |||||||

| Inv Risk ⇦ | FBH | 0.256 | *** | ||||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Anvari-Clark, J.; Rose, T. Financial Behavioral Health and Investment Risk Willingness: Implications for the Racial Wealth Gap. Int. J. Environ. Res. Public Health 2023, 20, 5835. https://doi.org/10.3390/ijerph20105835

Anvari-Clark J, Rose T. Financial Behavioral Health and Investment Risk Willingness: Implications for the Racial Wealth Gap. International Journal of Environmental Research and Public Health. 2023; 20(10):5835. https://doi.org/10.3390/ijerph20105835

Chicago/Turabian StyleAnvari-Clark, Jeffrey, and Theda Rose. 2023. "Financial Behavioral Health and Investment Risk Willingness: Implications for the Racial Wealth Gap" International Journal of Environmental Research and Public Health 20, no. 10: 5835. https://doi.org/10.3390/ijerph20105835

APA StyleAnvari-Clark, J., & Rose, T. (2023). Financial Behavioral Health and Investment Risk Willingness: Implications for the Racial Wealth Gap. International Journal of Environmental Research and Public Health, 20(10), 5835. https://doi.org/10.3390/ijerph20105835