Greenhouse Emissions and Productivity Growth

Abstract

:1. Introduction

2. Methodology and Data Sources

2.1. Specification

2.2. Data Sources

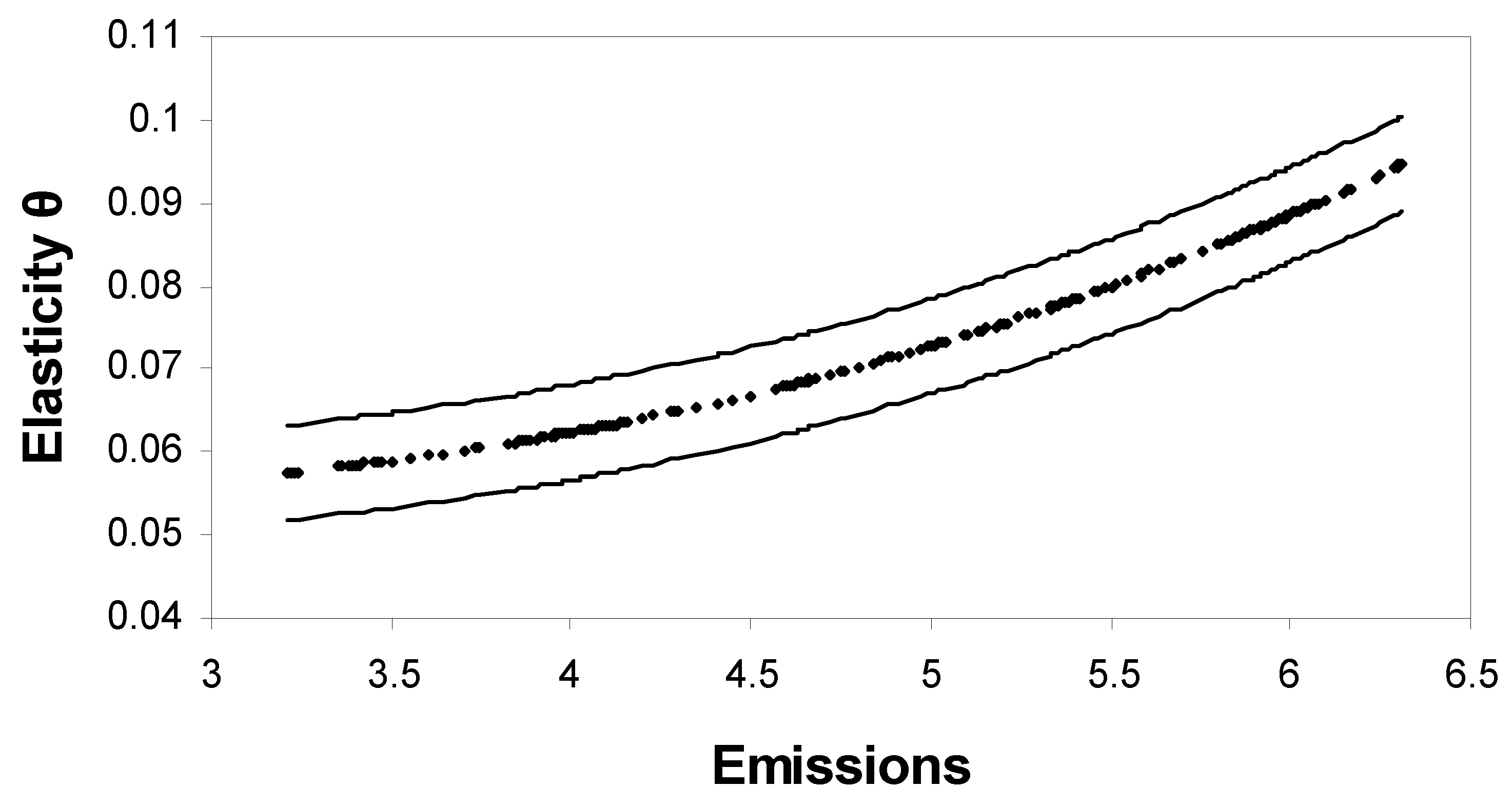

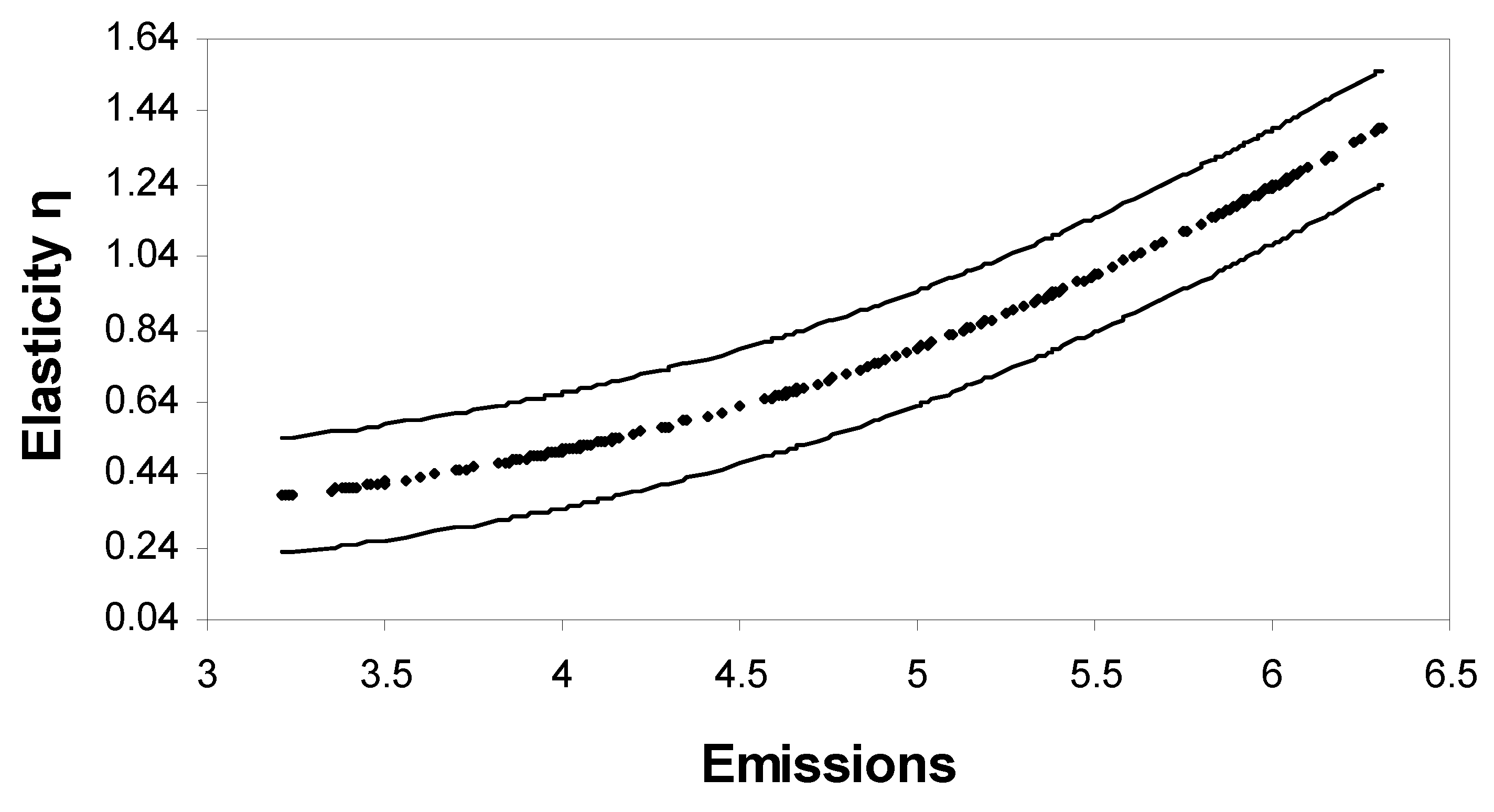

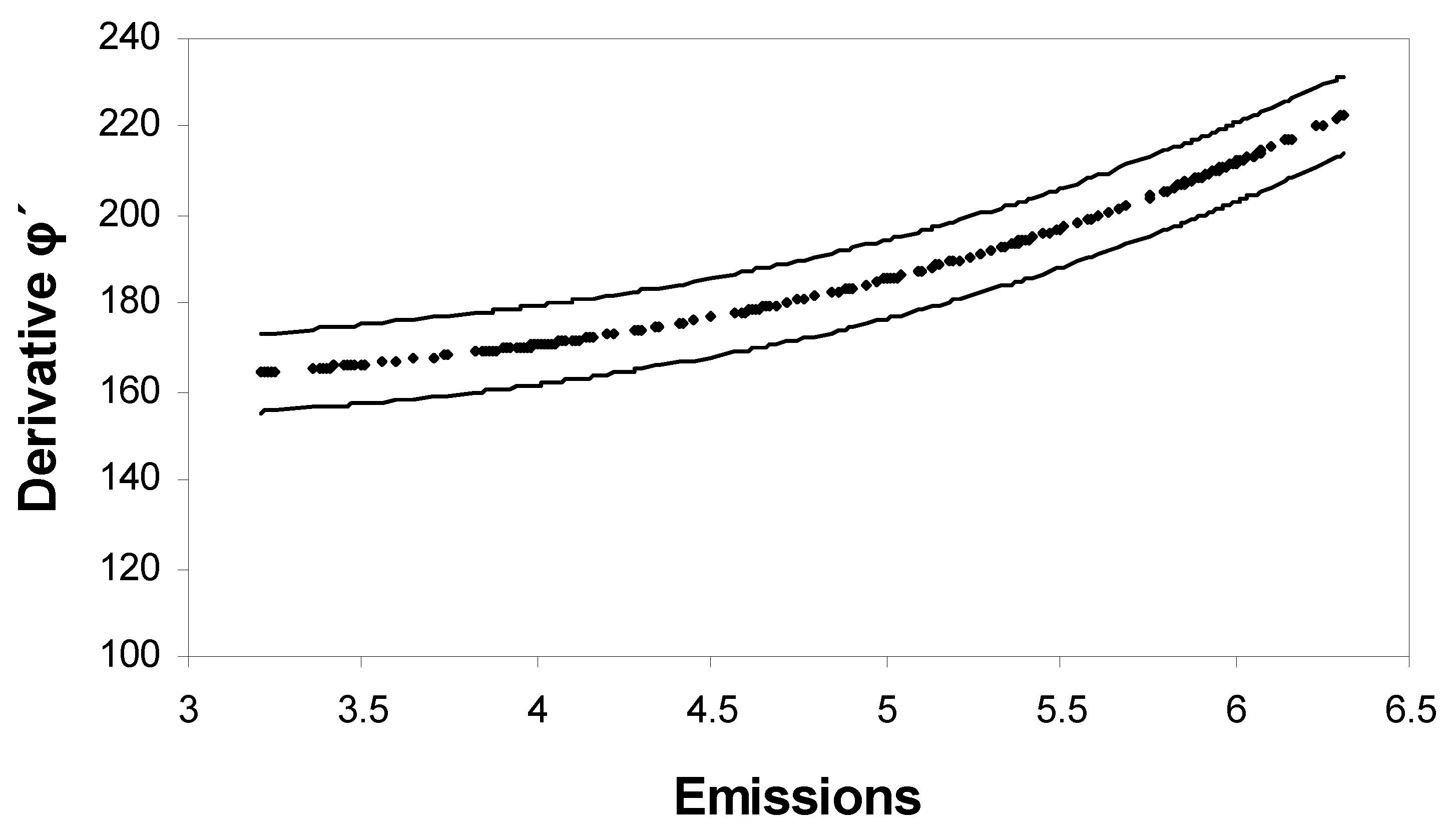

3. Empirical Findings

4. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A. Econometric Estimation: A Smooth Coefficient Semiparametric Approach

Appendix B. Linearity Test

References

- Ahmad, Ibrahim, Sittisak Leelahanon, and Qi Li. 2005. Efficient estimation of a semiparametric partially varying linear model. Annals of Statistics 33: 258–83. [Google Scholar] [CrossRef]

- Anderson, Curt L. 1987. The production process: Inputs and wastes. Journal of Environmental Economics and Management 14: 1–12. [Google Scholar] [CrossRef]

- Ansuategi, Alberto. 2003. Economic growth and transboundary pollution in Europe: An empirical analysis. Environmental and Resource Economics 26: 305–28. [Google Scholar] [CrossRef]

- Ayres, Robert U., and Allen V. Kneese. 1969. Production, Consumption, and Externalities. American Economic Review 59: 282–97. [Google Scholar]

- Azomahou, Theophile, François Laisney, and Phu Nguyen Van. 2006. Economic development and CO2 emissions: A nonparametric panel approach. Journal of Public Economics 90: 1347–63. [Google Scholar] [CrossRef]

- Ball, V. Eldon, Ca Knox Lovell, Richard Nehring, and Agapi Somwaru. 1994. Incorporating Undesirable Outputs into Models of Production: An Application to US Agricultural. Cahiers d’Economique et Sociologie Rurales 31: 59–73. [Google Scholar]

- Barassi, Marco R., Matthew A. Cole, and Robert J. R. Elliott. 2008. Stochastic divergence or convergence of per capita carbon dioxide emissions: Re-examining the evidence. Environmental and Resource Economics 40: 121–37. [Google Scholar] [CrossRef]

- Baumol, William J., and Wallace E. Oates. 1988. The Theory of Environmental Policy, 2nd ed. Cambridge: Cambridge U. Press. [Google Scholar]

- Bertinelli, Luisito, and Eric Strobl. 2005. The Environmental Kuznets Curve semi-parametrically revisited. Economics Letters 88: 350–57. [Google Scholar] [CrossRef]

- Bertinelli, Luisito, Eric Strobl, and Benteng Zou. 2012. Sustainable economic development and the environment: Theory and evidence. Energy Economics 34: 1105–14. [Google Scholar] [CrossRef]

- Bovenberg, A. Lans, and Sjak Smulder. 1995. Environmental quality and pollution-augmenting technological change in a two-sector endogenous growth model. Journal of Public Economics 57: 369–91. [Google Scholar] [CrossRef]

- Brock, William A., and M. Scott Taylor. 821. Economic growth and the environment: A review of theory and empirics. In Handbook of Economic Growth II. Edited by Aghion Philippe and Durlauf Steven. New York: Elsevier, Chp. 28. pp. 369–1749. [Google Scholar]

- Cai, Zongwu, Mitali Das, Huaiyu Xiong, and Xizhi Wu. 2006. Functional coefficient instrumental variable models. Journal of Econometrics 133: 207–41. [Google Scholar] [CrossRef]

- Chimeli, Ariaster B., and John B. Braden. 2005. Total factor productivity and the environmental Kuznets curve. Journal of Environmental Economics and Management 49: 366–80. [Google Scholar] [CrossRef]

- Cropper, Maureen L., and Wallace E. Oates. 1992. Environmental Economics: A survey. Journal of Economic Literature 30: 675–740. [Google Scholar]

- Fan, Jianqing. 1992. Design-adaptive nonparametric regression. Journal of the American Statistical Association 87: 998–1004. [Google Scholar] [CrossRef]

- Fan, Jianqing, and Wenyang Zhang. 1999. Statistical estimation in varying-coefficient models. Annals of Statistics 27: 1491–518. [Google Scholar]

- Fare, Rolf, Shawna Grosskopf, C. A. Knox Lovell, and Suthathip Yaisawarng. 1993. Derivation of shadow prices for undesirable outputs: A distance function approach. Review of Economics and Statistics 75: 375–80. [Google Scholar] [CrossRef]

- Fare, Rolf, Shawna Grosskopf, and Carl A. Pasurka Jr. 2001. Accounting for air pollution emissions in measures of state manufacturing productivity growth. Journal of Regional Science 41: 381–409. [Google Scholar] [CrossRef]

- Fernandez, Carmen, Gary Koop, and Mark F. J. Steel. 2005. Alternative efficiency measures for multiple-output production. Journal of Econometrics 126: 411–44. [Google Scholar] [CrossRef] [Green Version]

- Førsund, Finn R. 2009. Good Modelling of Bad Outputs: Pollution and Multiple-Output Production. International Review of Environmental & Recourse Economics 3: 1–38. [Google Scholar] [Green Version]

- Grossman, Gene M., and Alan B. Krueger. 1995. Economic growth and the environment. Quarterly Journal of Economics 110: 353–77. [Google Scholar] [CrossRef]

- Harbaugh, William T., Arik Levinson, and David Molloy Wilson. 2002. Reexamining the empirical evidence for an environmental Kuznets curve. Review of Economics and Statistics 84: 541–51. [Google Scholar] [CrossRef]

- Heil, Mark T., and Thomas M. Selden. 2001. Carbon emissions and economic development: Future trajectories based on historical experience. Environment and Development Economics 6: 63–83. [Google Scholar] [CrossRef]

- Helland, Eric, and Andrew B. Whitford. 2003. Pollution incidence and political jurisdiction: Evidence from TRI. Journal of Environmental Economics and Management 46: 403–24. [Google Scholar] [CrossRef]

- Holtz-Eakin, Douglas, and Thomas M. Selden. 1995. Stocking the fires? CO2 emissions and economic growth. Journal of Public Economics 57: 85–101. [Google Scholar] [CrossRef]

- Hoover, Donald R., John A. Rice, Colin O. Wu, and Li-Ping Yang. 1998. Nonparametric Smoothing Estimates of Time-Varying Coefficient Models with Longtitudinal Data. Biometrica 85: 809–22. [Google Scholar] [CrossRef]

- IPCC. 2000. IPCC Special Report on Land Use Change and Forestry-Summary for Policymakers. Geneva: Intergovernmental Panel on Climate Change, Available online: https://www.ipcc.ch/pdf/special-reports/spm/srl-en.pdf (accessed on 5 July 2018).

- Koop, Gary. 1998. Carbon Dioxide emissions and economic growth: A structural approach. Journal of Applied Statistics 25: 489–515. [Google Scholar] [CrossRef]

- Laffont, Jean-Jacque. 1988. Fundamentals of Public Economics. Cambridge: MIT Press. [Google Scholar]

- Lauwers, Ludwig. 2009. Justifying the incorporation of the materials balance principle into frontier-based eco-efficiency models. Ecological Economics 68: 1605–14. [Google Scholar] [CrossRef]

- Li, Qi, Cliff J. Huang, Dong Li, and Tsu-Tan Fu. 2002. Semiparametric smooth coefficient models. Journal of Business Econom 20: 412–22. [Google Scholar] [CrossRef]

- Li, Qi, and Suojin Wang. 1998. A Simple Consistent Bootstrap Test for a Parametric Regression Functional Form. Journal of Econometrics 87: 145–65. [Google Scholar] [CrossRef]

- List, John A., and Craig A. Gallet. 1999. The environmental Kuznets curve: Does one size fit all? Ecological Economics 31: 409–23. [Google Scholar] [CrossRef]

- Millimet, Daniel L., John A. List, and Thanasis Stengos. 2003. The environmental Kuznets curve: Real progress or misspecified models? Review of Economics and Statistics 85: 1038–47. [Google Scholar] [CrossRef]

- Maddison, David. 2006. Environmental Kuznets Curves: A spatial econometric approach. Journal of Environmental Economics and Management 51: 218–30. [Google Scholar] [CrossRef]

- Maddison, David. 2007. Modelling sulphur in Europe: A spatial econometric approach. Oxford Economics Paper 59: 726–43. [Google Scholar] [CrossRef]

- Mamuneas, Theofanis P., Andreas Savvides, and Thanasis Stengos. 2006. Economic development and the return to human capital: A smooth coefficient semiparametric approach. Journal of Applied Econometrics 21: 111–32. [Google Scholar] [CrossRef]

- Murdoch, James C., Tod Sandler, and Keith Sargent. 1997. A tale of two collectives: Sulphur versus nitrogen oxide emission reduction in Europe. Economica 64: 281–301. [Google Scholar] [CrossRef]

- Murty, Sushama, and R. Robert Russell. 2002. On Modelling Pollution-Generating Technologies. Riversid: Department of Economics, University of Californiae. [Google Scholar]

- Murty, Sushama, R. Robert Russell, and Steven B. Levkoff. 2011. On Modelling Pollution-Generating Technologies. Discussion Paper 11/1. Exeter: Department of Economics, University of Exeter, ISSN 1473-3307. [Google Scholar]

- Pethig, Rüdiger. 2003. The ‘Materials Balance Approach’ to Pollution: Its Origin, Implications and Acceptance. Economics Discussion Paper No. 105-03. Siegen: University of Siegen. [Google Scholar]

- Pethig, Rüdiger. 2006. Nonlinear Production, Abatement, Pollution and Materials Balance Reconsidered. Journal of Environmental Economics and Management 51: 185–204. [Google Scholar] [CrossRef]

- Pittel, Karen. 2002. Sustainability and Economic Growth. Cheltenham: Edward Elgar. [Google Scholar]

- Reinhard, Stijn, C. A. Knox Lovell, and Geert Thijssen. 1999. Econometric Estimation of Technical and Environmental Efficiency: An Application to Dutch Dairy Farms. American Journal of Agricultural Economics 81: 44–60. [Google Scholar] [CrossRef]

- Rupasingha, Anil, Stephan J. Goetz, David L. Debertin, and Angelos Pagoulatos. 2004. The environmental Kuznets curve for US counties: A spatial econometric analysis with extensions. Papers in Regional Science 83: 407–24. [Google Scholar] [CrossRef]

- Schmalensee, Richard, Thomas M. Stoker, and Ruth A. Judson. 1998. World Carbon Dioxide Emissions: 1950–2050. The Review of Economics and Statistics 80: 15–27. [Google Scholar] [CrossRef]

- Selden, Thomas M., and Daqing Song. 1994. Environmental quality and development: Is there a Kuznets curve for air pollution emission? Journal of Environmental Economics and Management 27: 147–62. [Google Scholar] [CrossRef]

- Sigman, Hilary. 2005. Transboundary spillovers and decentralization of environmental policies. Journal of Environmental Economics and Management 50: 82–101. [Google Scholar] [CrossRef] [Green Version]

- Stern, David I., and Michael S. Common. 2001. Is there an Environmental Kuznets curve for sulphur? Journal of Environmental Economics and Management 41: 162–78. [Google Scholar] [CrossRef]

- Taylor, M. Scott, and William A. Brock. 2004. The Green Solow Model. NBER Working Paper 10557. Calgary, AB, Canada: University of Calgary. [Google Scholar]

- Tzouvelekas, Vangelis, Dimitra Vouvaki, and Anastasios Xepapadeas. 2006. Total Factor Productivity and the Environment: A Case for Green Growth Accounting. Crete: University of Crete. [Google Scholar]

- Vouvaki, Dimitra, and Anastasios Xepapadeas. 2008. Total Factor Productivity Growth when Factors of Production Generate Environmental Externalities. MPRA Paper 10237. Munich: University of Munich. [Google Scholar]

- Westerlund, Joakim, and Syed A. Basher. 2008. Testing the convergence in carbon dioxide emissions using a century of panel data. Environmental and Resource Economics 40: 109–20. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Wenyang, Sik-Yum Lee, and Xinyuan Song. 2002. Local polynomial fitting in semivarying coefficient model. Journal of Multivariate Analysis 82: 166–88. [Google Scholar] [CrossRef]

- Zheng, John Xu. 1996. A Consistent Test of Functional Form via Nonparametric Estimation Techniques. Journal of Econometrics 75: 263–89. [Google Scholar] [CrossRef]

| 1 | Even though as mentioned above, studies that examine the EKC have used different pollutants besides CO, we concentrate on CO as it best captures the use of energy in a production function setting that underlies our TFP approach. |

| 2 | The site for the data is: www.euklems.net/eukdata.shtml. |

| 3 | |

| 4 | In the science of economic growth, it is customary to express variables in a per capita basis. However, in the environmental engineering literature, it is the concentration of pollution that is of interest. In our case, the elasticity of pollution intensity that we estimate is the same as that of pollution concentration, and as such, it is the appropriate concept to use. Another possible standardization, division by total GDP, is likely to introduce endogeneity issues. |

| 5 | However, we should note that our model is more complicated than Cai et al. (2006) as endogeneity enters both the variable in the unknown coefficient function, as well as the regressor. In this case, the asymptotic variance component will be different than theirs. However, deriving the correct asymptotic variance for a functional coefficient of this model goes beyond the scope of the present paper. |

{kind=link}

{kind=link}

{kind=link}

| Contribution to TFP Growth Average 1981–1998 (Stand. Error) | ||

|---|---|---|

| Country | Elasticity | TFP Contribution |

| Australia | 0.0721 (0.0001) | 0.00198 (0.00012) |

| Austria | 0.0553 (0.0001) | 0.00061 (0.00012) |

| Belgium | 0.0607 (0.0001) | −0.00086 (0.00012) |

| Canada | 0.0804 (0.0001) | 0.00047 (0.00011) |

| Denmark | 0.0555 (0.0001) | −0.00051 (0.00011) |

| Finland | 0.0546 (0.0001) | −0.00018 (0.00001) |

| France | 0.0778 (0.0001) | −0.00112 (0.00025) |

| Greece | 0.0568 (0.0001) | 0.00157 (0.00014) |

| Ireland | 0.0515 (0.0001) | 0.00121 (0.00009) |

| Italy | 0.0784 (0.0001) | 0.00048 (0.00008) |

| Korea | 0.0711 (0.0001) | 0.00415 (0.00012) |

| The Netherlands | 0.0642 (0.0001) | 0.00028 (0.00005) |

| Portugal | 0.0529 (0.0001) | 0.00208 (0.00009) |

| Spain | 0.0690 (0.0001) | 0.00084 (0.00006) |

| Sweden | 0.0551 (0.0001) | −0.00116 (0.00007) |

| U.K. | 0.0849 (0.0001) | −0.00032 (0.00003) |

| USA | 0.1266 (0.0001) | 0.00116 (0.00009) |

| Average | 0.0686 (0.0001) | 0.00063 (0.00003) |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kalaitzidakis, P.; Mamuneas, T.P.; Stengos, T. Greenhouse Emissions and Productivity Growth. J. Risk Financial Manag. 2018, 11, 38. https://doi.org/10.3390/jrfm11030038

Kalaitzidakis P, Mamuneas TP, Stengos T. Greenhouse Emissions and Productivity Growth. Journal of Risk and Financial Management. 2018; 11(3):38. https://doi.org/10.3390/jrfm11030038

Chicago/Turabian StyleKalaitzidakis, Pantelis, Theofanis P. Mamuneas, and Thanasis Stengos. 2018. "Greenhouse Emissions and Productivity Growth" Journal of Risk and Financial Management 11, no. 3: 38. https://doi.org/10.3390/jrfm11030038

APA StyleKalaitzidakis, P., Mamuneas, T. P., & Stengos, T. (2018). Greenhouse Emissions and Productivity Growth. Journal of Risk and Financial Management, 11(3), 38. https://doi.org/10.3390/jrfm11030038