Examination and Modification of Multi-Factor Model in Explaining Stock Excess Return with Hybrid Approach in Empirical Study of Chinese Stock Market

Abstract

:1. Introduction

2. Literature Review

3. Methodology

3.1. Hypotheses

3.2. Research Design

Factor Selection

3.3. Research Process

3.3.1. Multi-Factor Model Examination with Single Stock Regression Analysis

- Stability Test

- DV: Ri-Rf

- IV: Rm-Rf, SMB, RMW, HML, CMA, CRMHL, AMLH

- CV: Time, Time^2, Season

- OLS Regression

- Ridge Regression

- Robustness Test

3.3.2. Time-Series Analysis for Risk Factors

- Chi-Square Test

- Back-Test for Trading Strategy

3.4. Assumptions for Multi-Factor Examination

- Perfect market: there are no tax and transaction costs.

- People are risk averse or rational.

- People can lend or borrow money at a risk-free rate freely.

- There is a trade-off between risk and return for all securities.

- Everyone can obtain market information equally and freely.

- Investors have the same expectations for this market.

3.5. Models and Variable Definitions

4. Results

4.1. Multi-Factor Model Examination with Single Stock Regression Analysis

4.1.1. Stability Test

- DV: Ri-Rf

- IV: Rm-Rf, SMB, RMW, HML, CMA, CRMHL, AMLH

- CV: Time, Time^2, Season

4.1.2. Regression Models

- OLS Regression

- DV: Ri-Rf

- IV: Rm-Rf, SMB, RMW, HML, CMA

- DV: Ri-Rf

- IV: Rm-Rf, SMB, RMW, HML, CMA, CRMHL, AMLH

- DV: Ri-Rf

- IV: Rm-Rf, RMW, HML, CMA, CRMHL, AMLH

- Ridge Regression

- DV: Ri-Rf

- IV: Rm-Rf, SMB, RMW, HML, CMA, CRMHL, AMLH

4.1.3. Robustness Test: Zero Mean Residual Testing

4.1.4. Industry Analysis

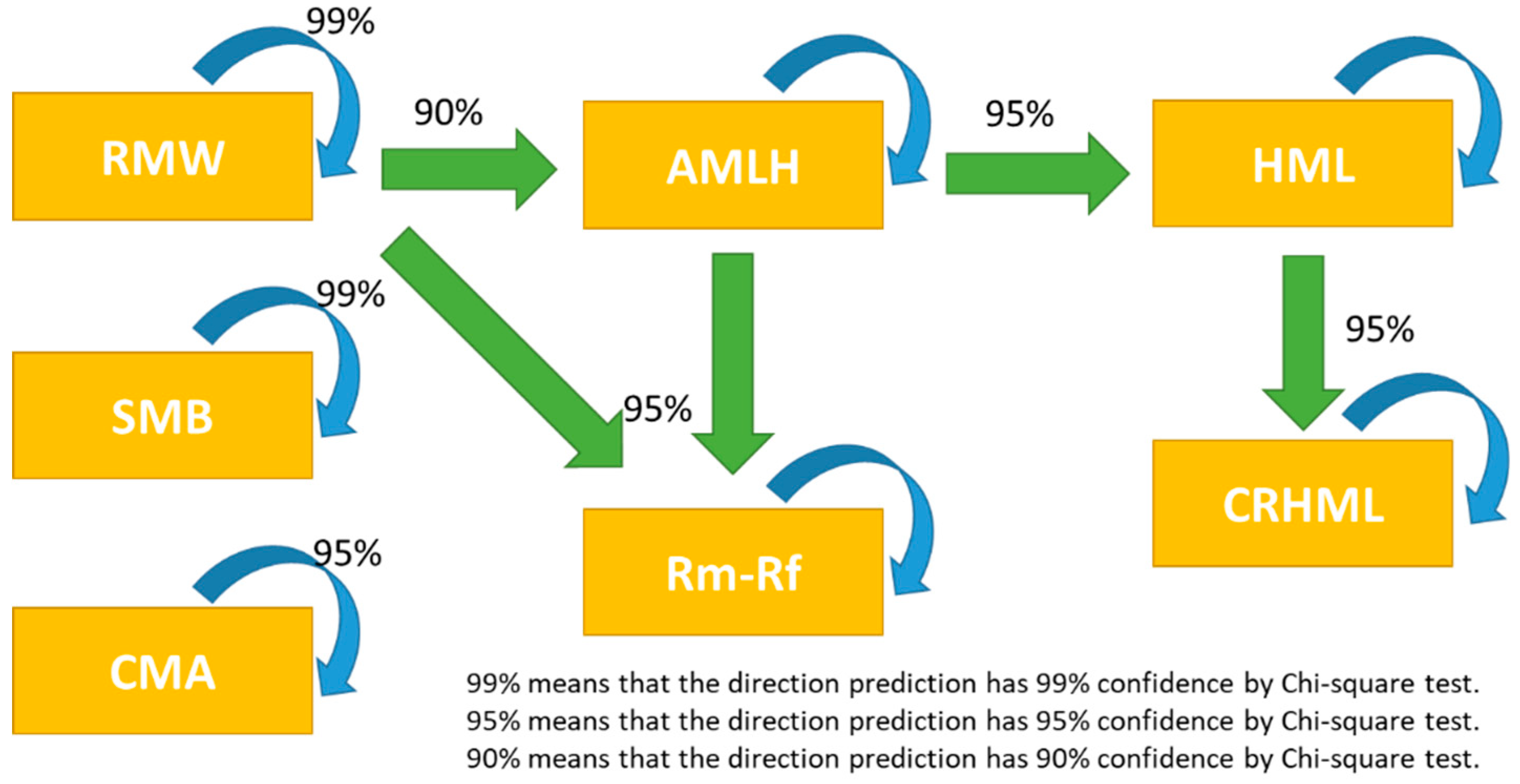

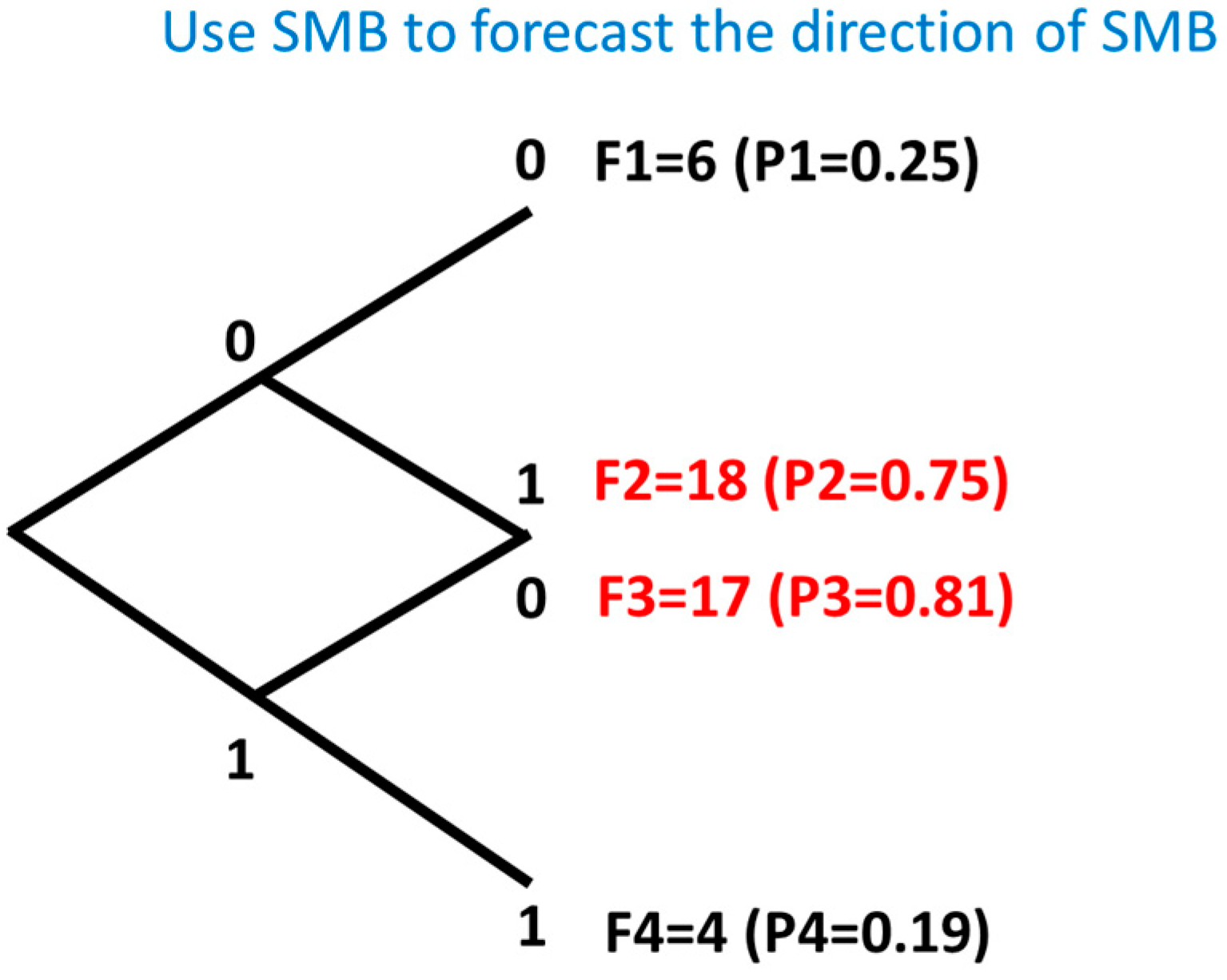

- From analysis of factors’ changing pattern, can we find the reasons or elements to illustrate the fluctuation of seven factors? (if we find out the driving factor which stimulate the moving of other factors, we can explain the most essential ratio that investor may focus on.)

- Can we find an approach to forecast the moving of each factor and apply it to do the back test for trading strategies?

4.2. Time-Series Analysis for Risk Factors

4.2.1. Endogeneity and Exogeneity for Factors’ Cyclical Research

- Endogeneity

- Exogeneity

4.2.2. Trading Strategy with Trend Analysis

4.2.3. Back-Testing

5. Discussion

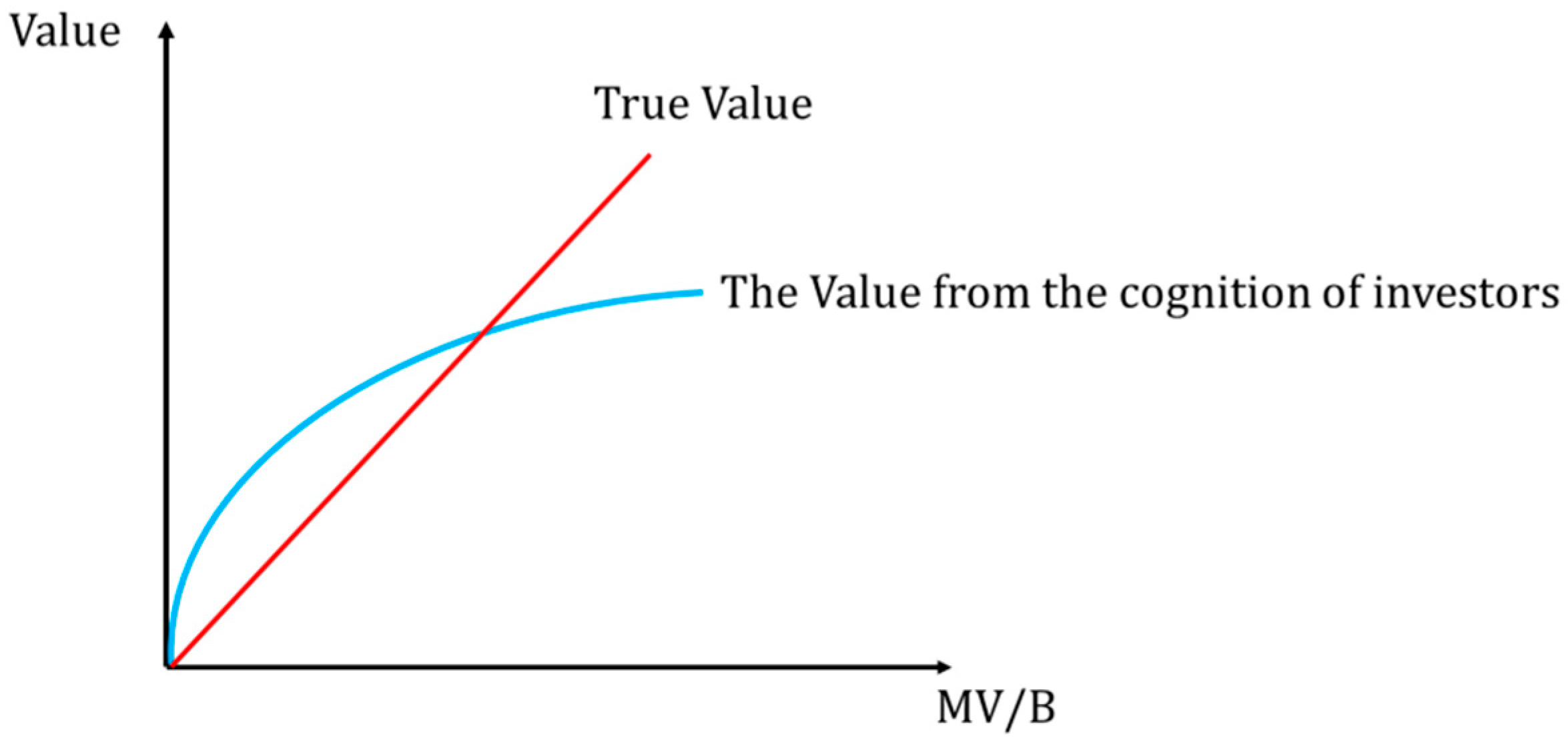

5.1. Analysis of Multi-Factor Model

5.2. Industry Analysis

5.3. Factor Cyclical Research

5.4. Trading Strategy and Back Test

5.5. Significance and Limitations of Research

6. Conclusions and Further Study

Funding

Conflicts of Interest

Appendix A. Intuition and Assumption Behind the Hypotheses

Appendix B. Chi-Square Test of Industry in Different Factors

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Factors | Chi-Square |

|---|---|

| SMB | 97.58155 |

| RMW | 102.9963 |

| HML | 134.683 |

| CMA | 85.7257 |

| Rm-Rf | 38.17769 |

| CRMHL | 66.58794 |

| AMLH | 179.6194 |

Appendix C. Significance Level and Correlation Effect

| Title | SMB | RMW | HML | CMA | CRMHL | AMLH | Rm-Rf |

|---|---|---|---|---|---|---|---|

| Extractive | 0 | −0.76 | −0.8 | −0.72 | 0.72 | −0.72 | 1 |

| Media | 0 | −0.78571 | −1 | 0 | 0 | 0 | 1 |

| Electrical equipment | 0.741935 | −0.80645 | −0.93548 | 0 | 0 | 0 | 1 |

| Electronics | 0.833333 | 0 | −0.875 | 0 | 0.729167 | −0.70833 | 1 |

| Housing | 0 | 0 | −0.72527 | 0 | 0.714286 | 0.791209 | 1 |

| Textiles & garments | 0 | −0.70833 | −0.875 | 0.708333 | 0.916667 | 0 | 1 |

| Non-bank finance | 0 | 0 | 0 | 0 | 0 | 0.714286 | 0.964286 |

| Steel | −0.73684 | −0.94737 | 0.789474 | 0 | 1 | −0.89474 | 1 |

| Utilities | 0 | 0 | 0 | 0.710526 | 0.828947 | 0 | 1 |

| Defense | 0 | −0.8 | −0.72 | 0.8 | 0.8 | −0.84 | 1 |

| Chemistry | 0 | −0.74699 | −0.78313 | 0 | 0.795181 | −0.84337 | 1 |

| Mechanical equipment | 0 | −0.76667 | −0.76667 | 0 | 0.833333 | 0 | 1 |

| Computer | 0.777778 | 0 | −0.92593 | 0 | 0.777778 | 0 | 1 |

| Domestic appliance | 0 | 0 | 0 | 0 | 0.857143 | −0.7619 | 1 |

| Construction material | 0.714286 | −0.7619 | 0 | 0 | 0.904762 | 0 | 1 |

| Construction ornament | 0 | 0 | 0 | 0 | 0.933333 | 0 | 1 |

| Transportation | 0 | −0.81633 | 0 | 0 | 0.857143 | 0 | 1 |

| Animal husbandry and fishery | 0 | 0 | −0.71429 | 0 | 0 | 0 | 1 |

| Automobile | 0 | −0.86364 | −0.75 | 0 | 0.818182 | −0.75 | 1 |

| Light manufacturing | 0 | −0.73077 | −0.76923 | 0.730769 | 0.730769 | −0.80769 | 1 |

| Commercial | 0 | 0 | −0.88525 | 0.754098 | 0 | 0 | 1 |

| Food | 0.794118 | 0 | 0 | 0 | 0.794118 | −0.76471 | 1 |

| Telecommunication | 0.727273 | 0 | −0.77273 | 0 | 0.772727 | −0.77273 | 1 |

| Leisure service | 0.8125 | −0.875 | −0.8125 | 0 | 0.8125 | −0.8125 | 1 |

| Medical | 0 | 0 | −0.80412 | 0 | 0.835052 | −0.74227 | 0.989691 |

| Bank | 0 | 0.714286 | 1 | −0.71429 | 1 | 1 | 1 |

| Nonferrous metal | 0 | −0.88372 | −0.74419 | −0.83721 | 0.790698 | −0.86047 | 1 |

| Comprehensive | 0 | −0.92308 | −0.80769 | 0 | 0 | 0 | 1 |

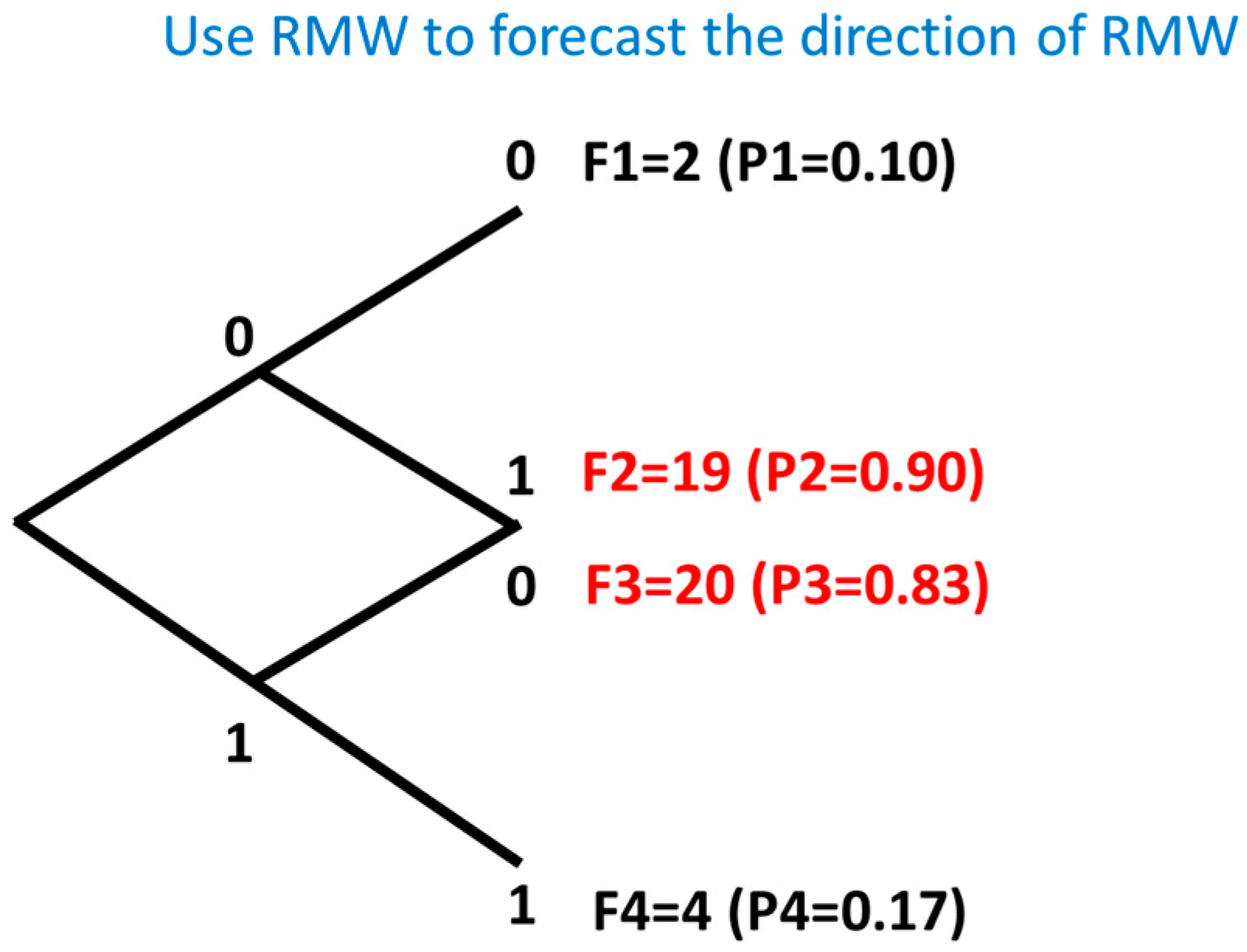

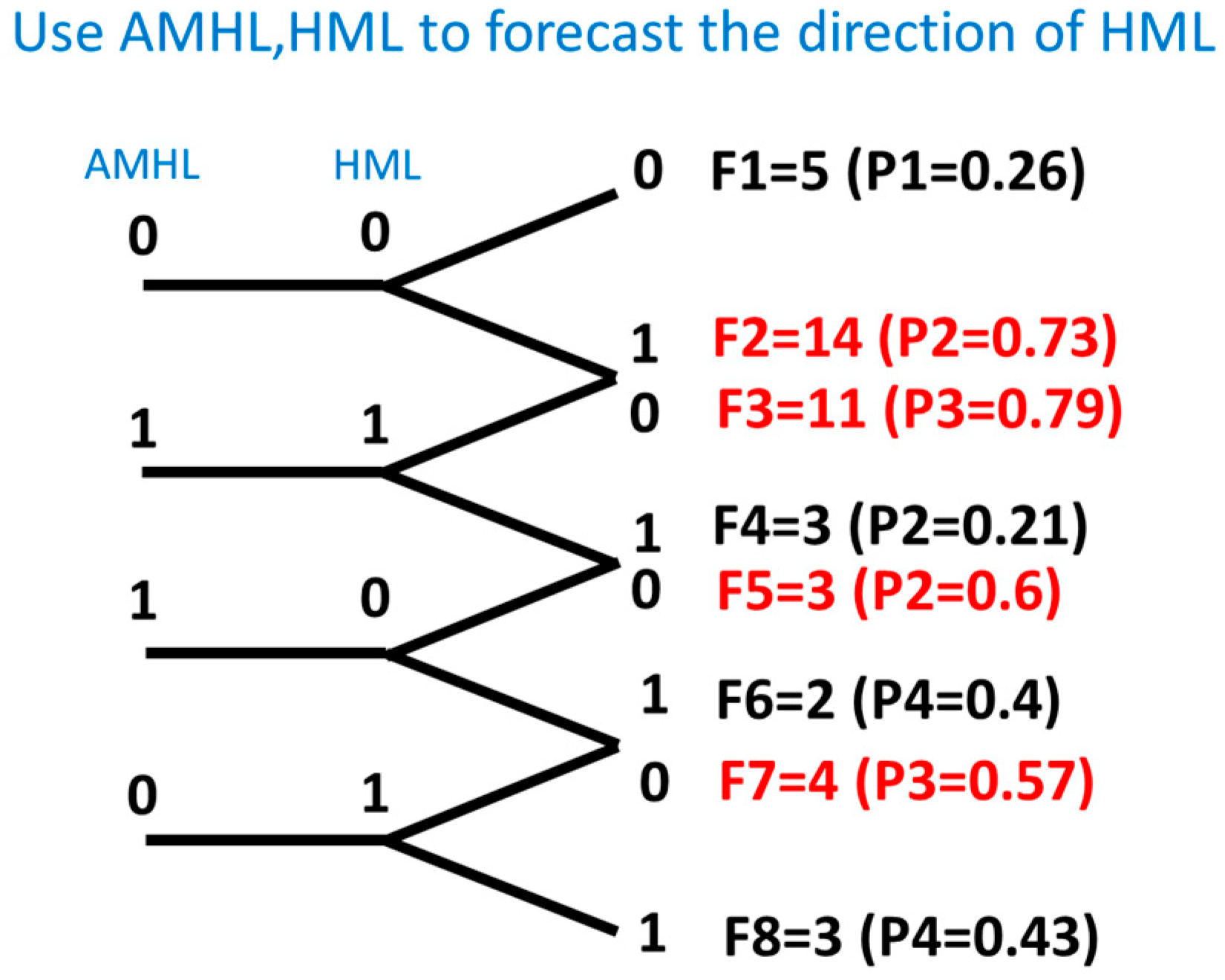

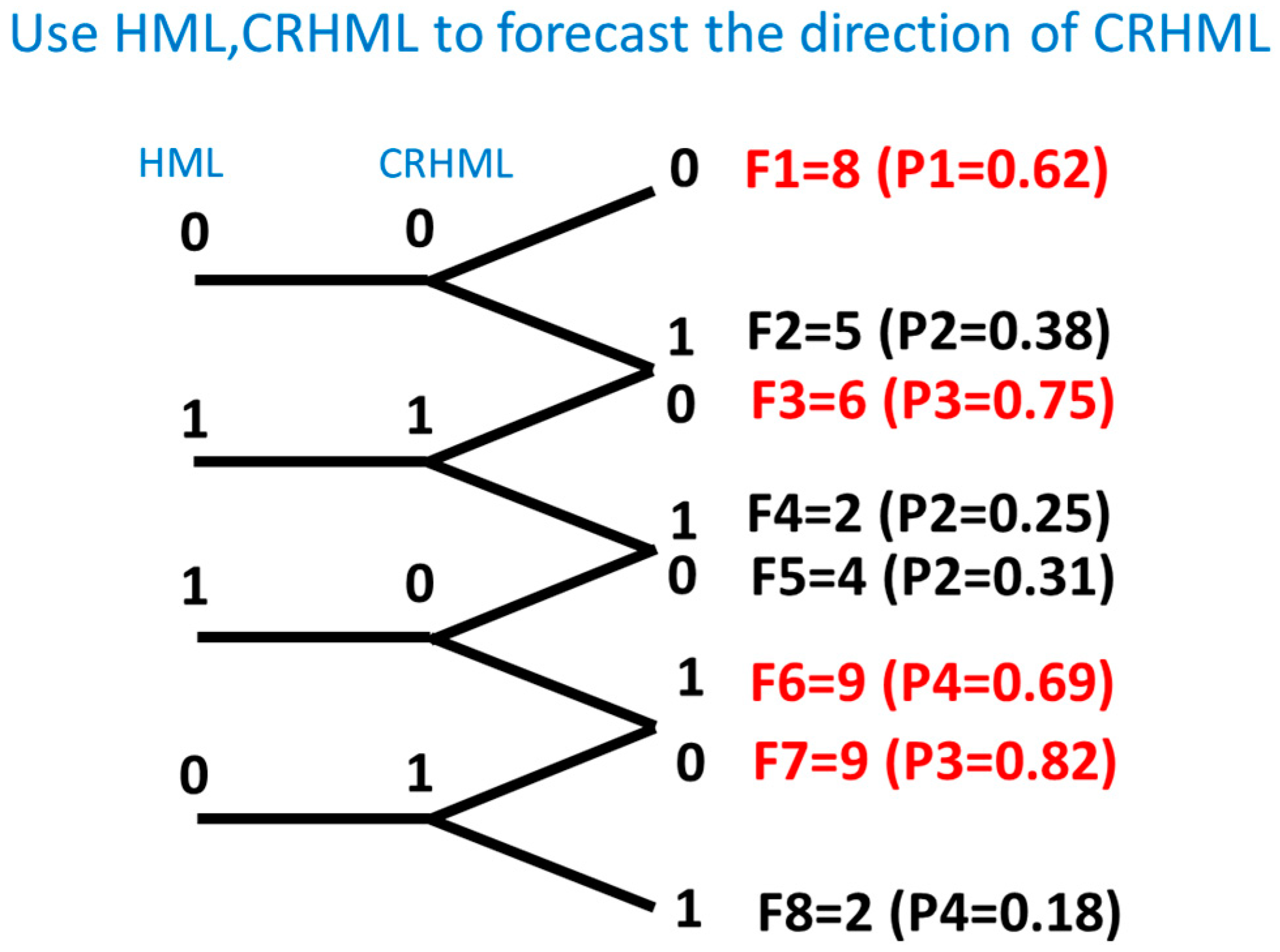

Appendix D. Forecasting the Direction of Factors

Appendix E. Result of Stability Test

References

- Aharoni, Gil, Bruce Grundy, and Qi Zeng. 2013. Stock returns and the miller modigliani valuation formula: Revisiting the fama French analysis. Social Science Electronic Publishing 110: 347–57. [Google Scholar] [CrossRef]

- Akter, Nahida, and Ashadun Nobi. 2018. Investigation of the financial stability of s&p 500 using realized volatility and stock returns distribution. Journal of Risk and Financial Management 11: 22. [Google Scholar]

- Banz, Rolf W. 1981. The relationship between return and market value of common stocks. Journal of Financial Economics 9: 3–18. [Google Scholar] [CrossRef] [Green Version]

- Bhattacharjee, Arnab, and Sudipto Roy. 2019. Abnormal Returns or Mismeasured Risk? Network Effects and Risk Spillover in Stock Returns. Journal of Risk and Financial Management 12: 50. [Google Scholar] [CrossRef]

- Bodie, Zvi, Alex Kane, Alan J. Marcus, and Ravi Jain. 2014. Investments. New York: Mc Graw Hill Education. [Google Scholar]

- Bodie, Zvi, Alex Kane, and Alan J. Marcus. 2017. Essentials of Investments. New York: McGraw-Hill Education. [Google Scholar]

- Carhart, Mark M. 1997. On persistence in mutual fund performance. The Journal of Finance 52: 26. [Google Scholar] [CrossRef]

- Chen, Jieting, and Yuichiro Kawaguchi. 2018. Multi-factor asset-pricing models under markov regime switches: Evidence from the chinese stock market. International Journal of Financial Studies 6: 54. [Google Scholar] [CrossRef]

- Cisse, Mamadou, Mamadou Konte, Mohamed Toure, and Smael A. Assani. 2019. Contribution to the Valuation of BRVM’s Assets: A Conditional CAPM Approach. Journal of Risk and Financial Management 12: 27. [Google Scholar] [CrossRef]

- Fama, Eugene F. 1996. Multifactor portfolio efficiency and multifactor asset pricing. The Journal of Financial and Quantitative Analysis 31: 441–65. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 1993. Common risk factors in the returns on stocks and bonds. Journal of Financial Economics 33: 3–56. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 2015. A five-factor asset pricing model. Journal of Financial Economics 116: 1–22. [Google Scholar] [CrossRef] [Green Version]

- Frazzini, Andrea, David Kabiller, and Lasse H. Pedersen. 2013. Buffett’s alpha. CEPR Discussion Papers 3: 583–90. [Google Scholar]

- Hanke, John E., and Dean W. Wichern. 2014. Business Forecasting. Zug: Pearson Schweiz Ag. [Google Scholar]

- Hsiao, Cheng. 2003. Analysis of Panel Data. Cambridge: Cambridge University Press. [Google Scholar]

- Jegadeesh, Narasimhan, and Sheridan Titman. 1993. Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of Finance 48: 65–91. [Google Scholar] [CrossRef]

- Johnson, Richard Arnold, and Dean W. Wichern. 2008. Applied Multivariate Statistical Analysis. Beijing: Tsinghua University Press. [Google Scholar]

- Lars, Tvede. 2006. Business Cycles: History, Theory and Investment Reality. Hoboken: Wiley. [Google Scholar]

- Lintner, John. 1965. The valuation of risk assets and the Selection of Risky Investments in Stock Portfolios and Capital Budgets. The Review of Economics and Statistics 47: 13–37. [Google Scholar] [CrossRef]

- Markowitz, Harry. 1952. Portfolio selection. Journal of Finance 7: 77–91. [Google Scholar]

- Moinak, Maiti, and A. Balakrishnan. 2018. Is human capital the sixth factor? Journal of Economic Studies 45: 710–37. [Google Scholar]

- Novy-marx, Robert. 2013. The other side of value: The gross profitability premium. Journal of Financial Economics 108: 1–28. [Google Scholar] [CrossRef] [Green Version]

- Peng, Chi-Lu, Kuan-Ling Lai, Maio-Ling Chen, and An-Pin Wei. 2014. Investor sentiment, customer satisfaction and stock returns. Social Science Electronic Publishing 49: 827–50. [Google Scholar] [CrossRef]

- Ronzani, André, Osvaldo Candido, and Wilfredo Maldonado. 2017. Goodness-of-fit versus significance: A capm selection with dynamic betas applied to the brazilian stock market. International Journal of Financial Studies 5: 33. [Google Scholar] [CrossRef]

- Ross, Stephen A. 1976. The arbitrage theory of capital asset pricing. Journal of Economic Theory 13: 341–60. [Google Scholar] [CrossRef]

- Sehgal, Sanjay, and Vibhuti Vasishth. 2015. Past price changes, trading volume and prediction of portfolio returns. Journal of Advances in Management Research 12: 330–56. [Google Scholar] [CrossRef]

- Sharpe, William F. 1964. Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance 19: 18. [Google Scholar]

- Wild, John J. 2016. Fundamental Accounting Principles. New York: McGraw-Hill Education. [Google Scholar]

- Zahedi, Javad, and Mohammad Mahdi Rounaghi. 2015. Application of artificial neural network models and principal component analysis method in predicting stock prices on tehran stock exchange. Physica A: Statistical Mechanics and its Applications 438: 178–87. [Google Scholar] [CrossRef]

| Name | Label | Note |

|---|---|---|

| DV | ||

| Excess return | − | The return of security mines risk-free rate of return |

| IV | ||

| Abnormal return | a | The constant term of formula |

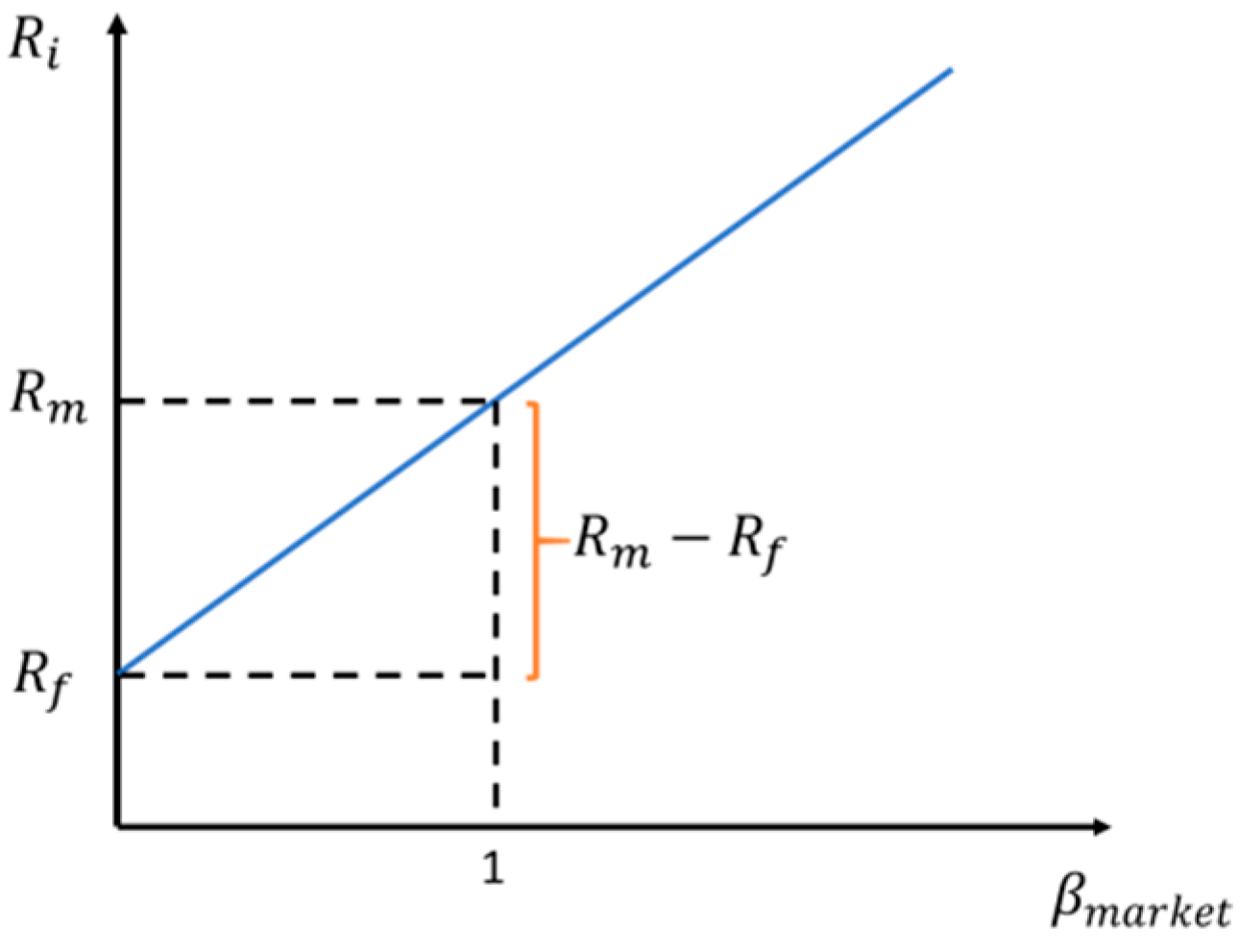

| Market premium | − | The return of market index (in this model, market index is Shanghai stock exchange market index) mines risk-free rate of return |

| Size premium (Small minus Big) | SMB | The return on a diversified set of small stocks minus the return on a diversified set of big stocks. |

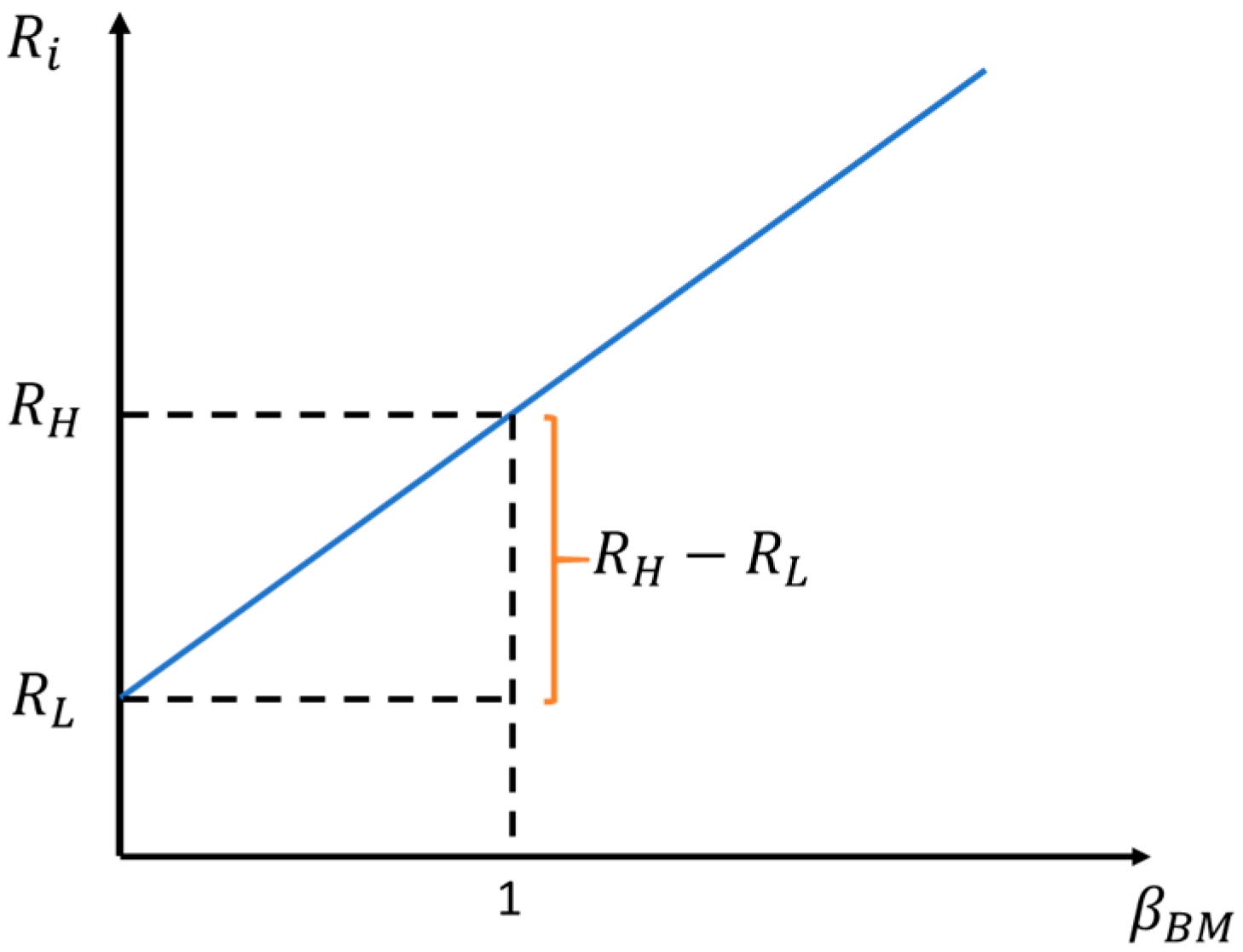

| Book-to-market premium (High minus low) | HML | The difference between the returns on diversified portfolios of high and low B/M stocks. |

| Profitability premium (Robust minus weak) | RMW | The difference between the returns on diversified portfolios of stocks with robust and weak profitability. |

| Investment growth premium (Conservative minus aggressive) | CMA | The difference between the returns on diversified portfolios of the stocks of low and high investment firms, which we label as conservative and aggressive. |

| Momentum premium (High momentum minus low momentum) | CRMHL | The difference between higher momentum (higher accumulated return) companies’ average return and lower momentum (lower accumulated return) companies’ average return in a diversified portfolio or in the market. |

| Asset turnover premium (Low turnover rate minus high turnover rate) | AMLH | The difference between low asset turnover companies’ average return and higher turnover companies’ average return or in the market. |

| OLS | Ridge Regression | ||||

|---|---|---|---|---|---|

| Model 1 | Model 2 | Model 3 | Model 4 | ||

| Mean of R square | 0.5692 | 0.6078 | 0.5911 | 0.6048 | |

| Mean of coefficient (p-level) | Rm-Rf | −0.29 (0.9535)  | 0.29 (0.9991)  | 0.82 (0.9991)  | 0.21 (0.9991)  |

| SMB | −0.29 (0.8669)  | 0.34 (0.1641)  | 0.29 (0.8368)  | ||

| RMW | −0.74 (0.9189)  | 0.24 (0.9891)  | 0.40 (0.9763)  | 0.22 (0.9298)  | |

| HML | 0.13 (0.3874)  | 0.30 (0.9690)  | −0.27 (0.9444)  | 0.22 (0.9681)  | |

| CMA | −0.11 (0.9335)  | 0.58 (0.9900)  | −0.50 (0.9763)  | 0.38 (0.9909)  | |

| CRMHL | −0.14 (0.9617)  | 0.33 (0.9243)  | 0.02 (0.9535)  | ||

| AMLH | −0.04 (0.9991)  | −0.72 (0.9991)  | 0.06 (0.9991)  | ||

| SMB | RMW | HML | CMA | AMLH | CRMHL | Rm-Rf | |

|---|---|---|---|---|---|---|---|

| Positive | 61.0% | 24.2% | 23.0% | 56.2% | 62.4% | 77.8% | 99.8% |

| Negative | 22.7% | 68.7% | 73.8% | 42.8% | 37.5% | 17.6% | 0.1% |

| Uncorrelated | 16.3% | 7.0% | 3.2% | 0.9% | 0.1% | 0.1% | 0.1% |

| OLS t-Value | Ridge Regression t-Value | ||

|---|---|---|---|

| Model 1 | Model 2 | Model 3 | Model 4 |

| 0.5811 | 0.5393 | 0.5416 | 0.5387 |

| Positive Relationships | Negative Relationships | |

|---|---|---|

| SMB | (Group A: 7) Electrical Equipment, Electronics, Computer, Construction Material, Food, Telecommunication, and Leisure Service | (Group B: 1) Steel |

| RMW | (Group C: 1) Banking | (Group D: 16) Extractive, Media, Electrical Equipment, Textiles & Garments, Steel, Defense, Chemistry, Mechanical Equipment, Computer, Construction Material, Transportation, Automobile, Light Manufacturing, Leisure Service, Nonferrous Metal, and Comprehensive Industries. |

| HML | (Group E: 1) Banking | (Group F: 19) Extractive, Media, Electrical Equipment, Electronics, Housing, Textiles & Garments, Steel, Defense, Chemistry, Mechanical equipment, Computer, Animal Husbandry and Fishery, Automobile, Light Manufacturing, Commercial, Telecommunication, Leisure Service, Medical, Nonferrous Metal, and Comprehensive Industries. |

| CMA | (Group G: 5) Textiles & Garments, Utilities, Defense, Light Manufacturing, and Commercial | (Group H: 3) Extractive, Banking, and Nonferrous Metal |

| CRMHL | (Group I: 20) Extractive, Electronics, Housing, Textiles & Garments, Steel, Utilities, Defense, Chemistry, Mechanical Equipment, Computer, Domestic Appliance, Construction material, Transportation, Automobile, Light Manufacturing, Telecommunication, Leisure Service, Medical, Banking, and Nonferrous Metal. | |

| AMLH | (Group J: 3) Housing, Non-Bank Finance, and Banking. | (Group K: 14) Extractive, Electrical Equipment, Electronics, Steel, Defense, Chemistry, Domestic appliance, Automobile, Light Manufacturing, Food, Telecommunication, Leisure Service, Medical and Nonferrous Metal. |

| Rm-Rf | (Group L: 28) All industries |

| Condition | When Factor Is Positive | When Factor Is Negative | ||

|---|---|---|---|---|

| Strategies | BUY | SELL | BUY | SELL |

| SMB | Small MV companies in Group A Big MV companies in Group B | Big MV companies in Group A Small MV companies in Group B | Big MV companies in Group A Small MV companies in Group B | Small MV companies in Group A Big MV companies in Group B |

| RMW | Robust ROE companies in Group C Weak ROE companies in Group D | Weak ROE companies in Group C Robust ROE companies in Group D | Weak ROE companies in Group C Robust ROE companies in Group D | Robust ROE companies in Group C Weak ROE companies in Group D |

| HML | High B/M companies in Group E Low B/M companies in Group F | Low B/M companies in Group E High B/M companies in Group F | Low B/M companies in Group E High B/M companies in Group F | High B/M companies in Group E Low B/M companies in Group F |

| CMA | Conservative (low growth rate of assets) companies in Group G Aggressive (High growth rate of assets) companies in Group H | Aggressive companies in Group G Conservative companies in Group H | Aggressive companies in Group G Conservative companies in Group H | Conservative companies in Group G Aggressive companies in Group H |

| CRMHL | High CR companies in Group I | High CR companies in Group I | ||

| AMLH | Low Asset turnover companies in Group J High Asset turnover companies in Group K | High Asset turnover companies in Group J Low Asset turnover companies in Group K | High Asset turnover companies in Group J Low Asset turnover companies in Group K | Low Asset turnover companies in Group J High Asset turnover companies in Group K |

| Rm-Rf | All companies (Group L) | All companies (Group L) | ||

| Factors | Float Return | Expected Annual Return |

|---|---|---|

| SMB | 165.89% | 15.43% |

| RMW | −6.525% | −0.61% |

| HML | −22.29% | −2.07% |

| CMA | 34.67% | 3.23% |

| CRMHL | 313.09% | 29.13% |

| AMLH | 90.26% | 8.40% |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Huang, J.; Liu, H. Examination and Modification of Multi-Factor Model in Explaining Stock Excess Return with Hybrid Approach in Empirical Study of Chinese Stock Market. J. Risk Financial Manag. 2019, 12, 91. https://doi.org/10.3390/jrfm12020091

Huang J, Liu H. Examination and Modification of Multi-Factor Model in Explaining Stock Excess Return with Hybrid Approach in Empirical Study of Chinese Stock Market. Journal of Risk and Financial Management. 2019; 12(2):91. https://doi.org/10.3390/jrfm12020091

Chicago/Turabian StyleHuang, Jian, and Huazhang Liu. 2019. "Examination and Modification of Multi-Factor Model in Explaining Stock Excess Return with Hybrid Approach in Empirical Study of Chinese Stock Market" Journal of Risk and Financial Management 12, no. 2: 91. https://doi.org/10.3390/jrfm12020091

APA StyleHuang, J., & Liu, H. (2019). Examination and Modification of Multi-Factor Model in Explaining Stock Excess Return with Hybrid Approach in Empirical Study of Chinese Stock Market. Journal of Risk and Financial Management, 12(2), 91. https://doi.org/10.3390/jrfm12020091