What Coins Lead in the Cryptocurrency Market: Using Copula and Neural Networks Models

Abstract

:1. Introduction

2. Methods

2.1. Neural Network Autoregression Model

2.2. Copula and Directional Dependence

- For all , if at least one coordinate of is 0;

- , , for and

- C is 2-increasing (see Nelsen 2006).

2.3. Gaussian Copula Marginal Beta Regression

3. Data Analysis

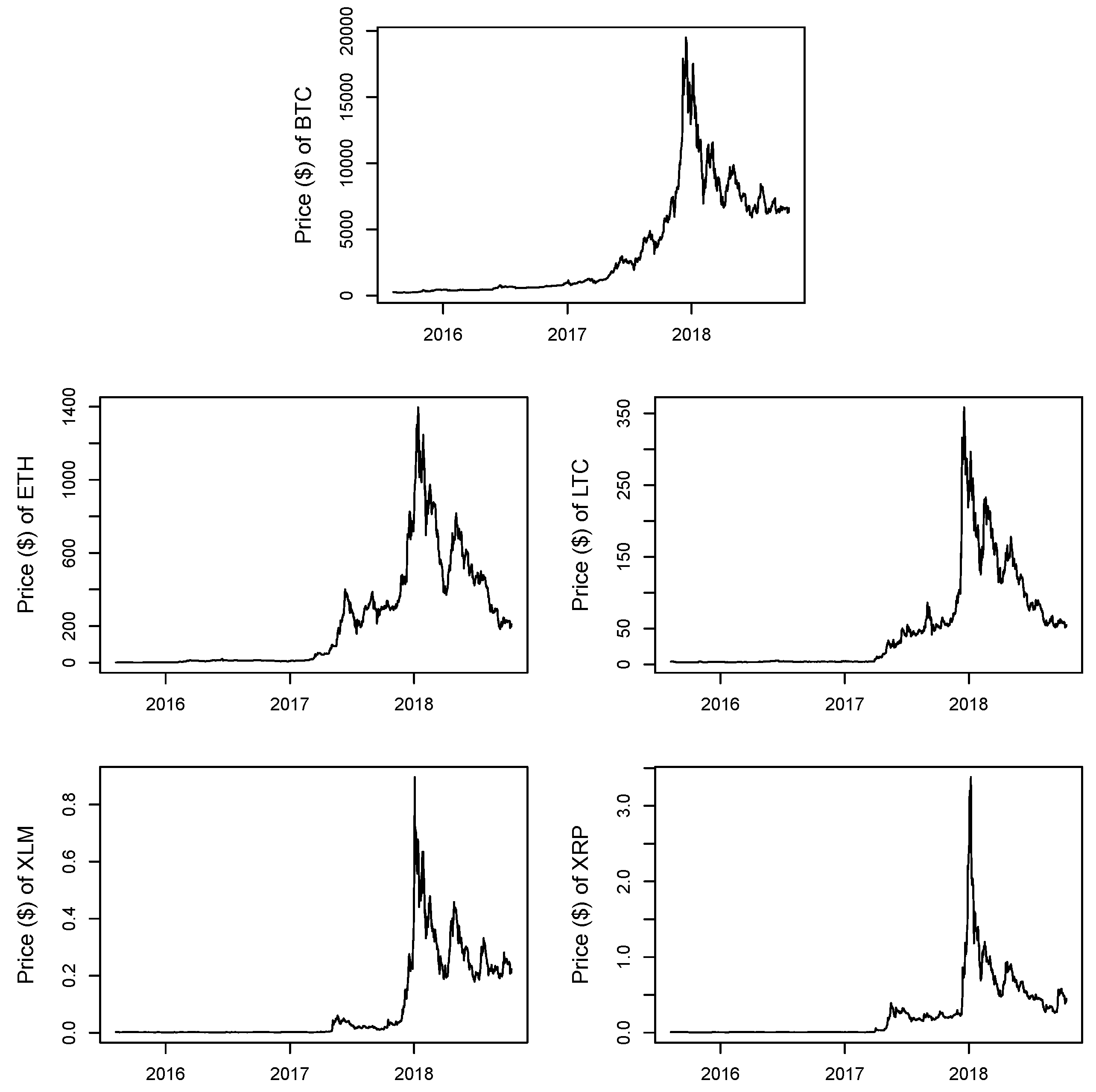

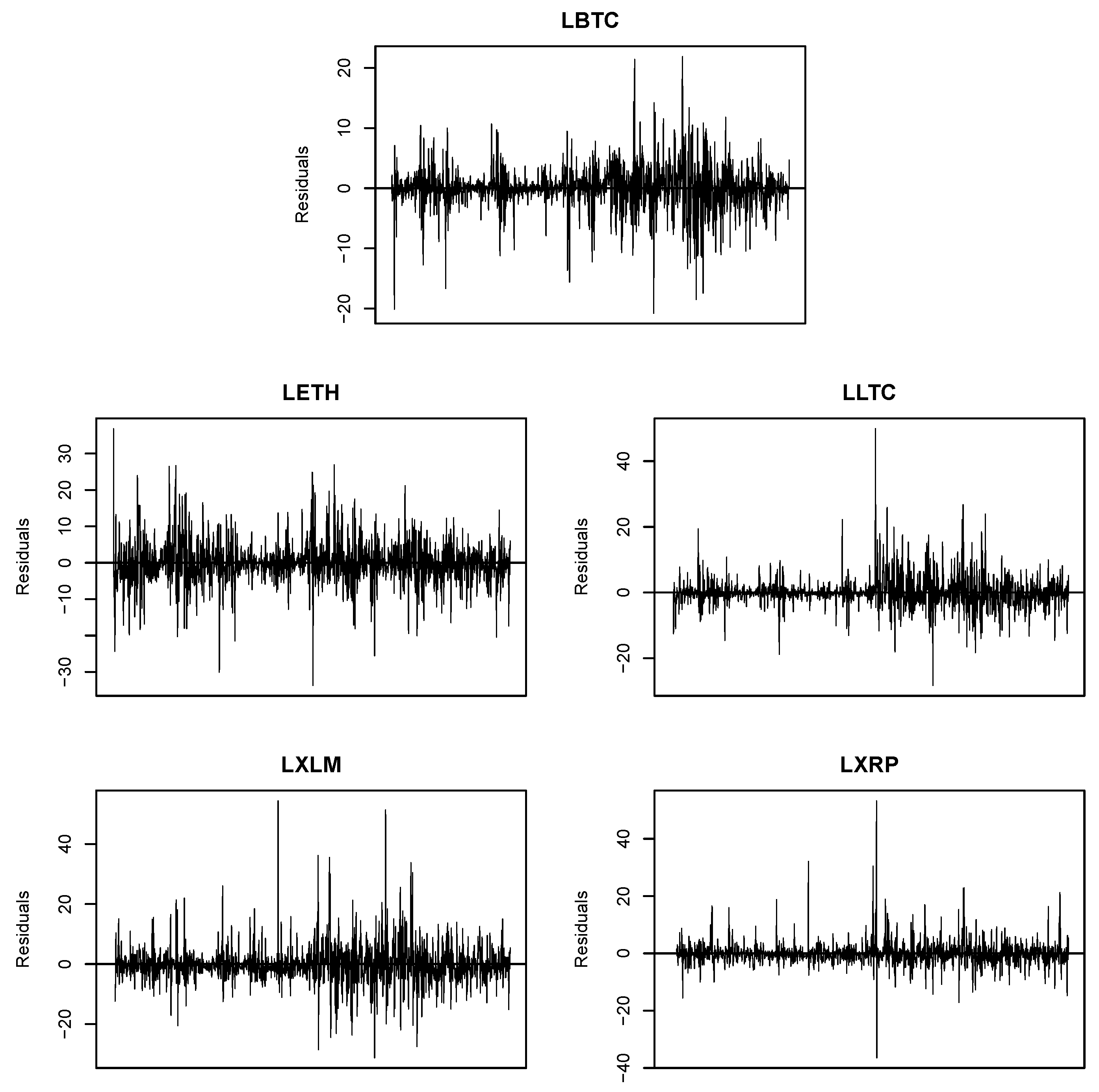

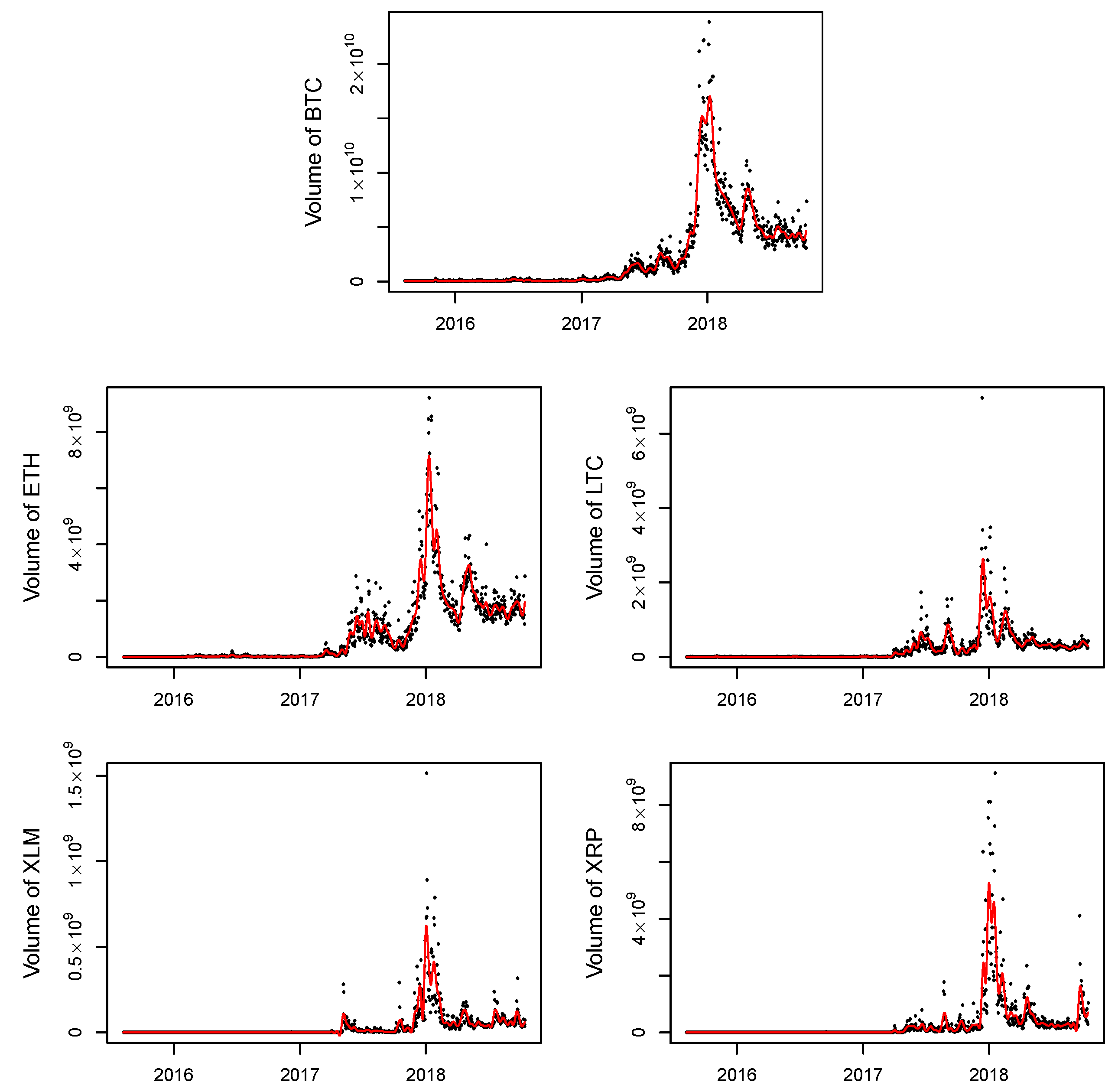

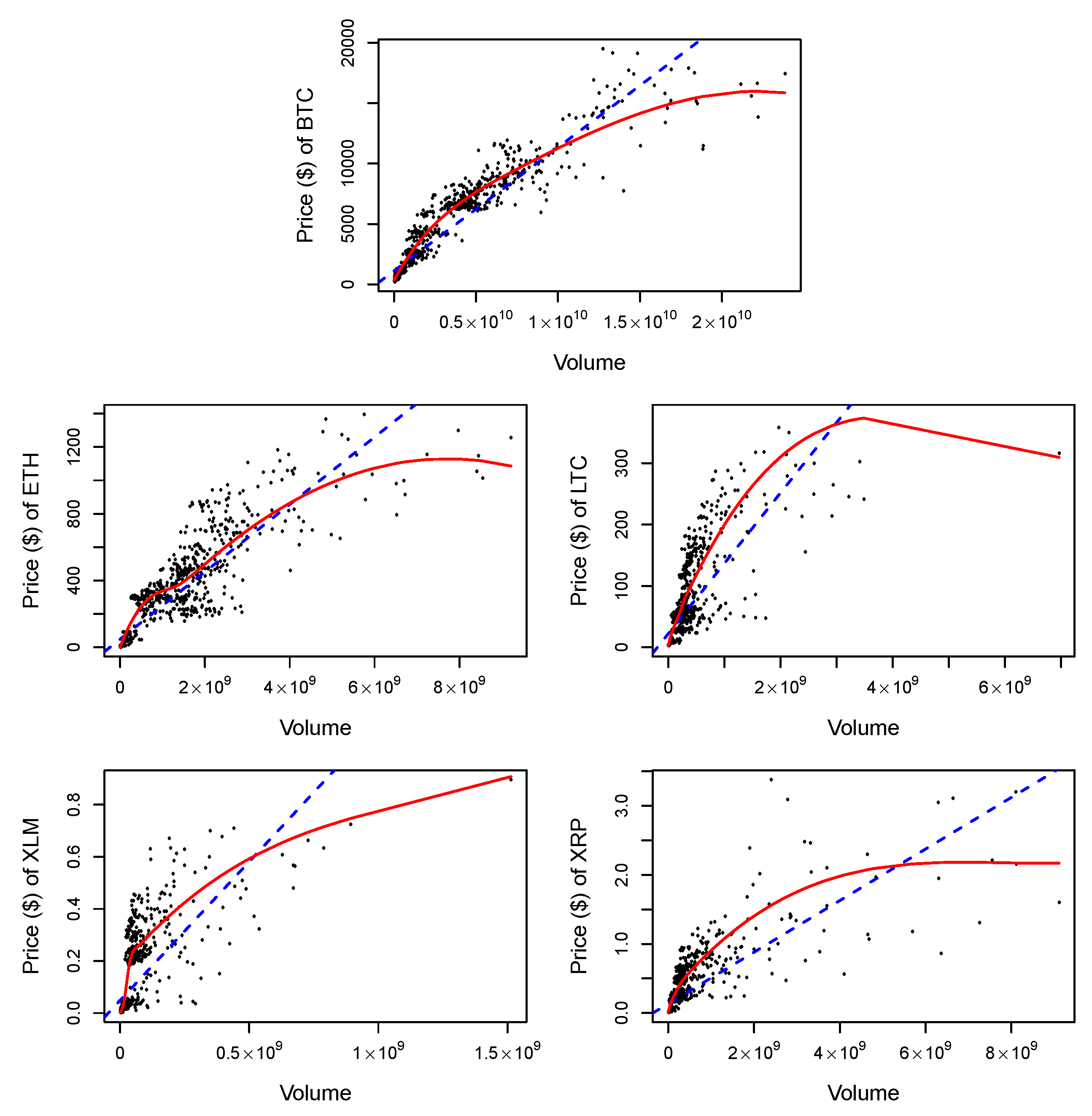

3.1. Data and Summary Statistics

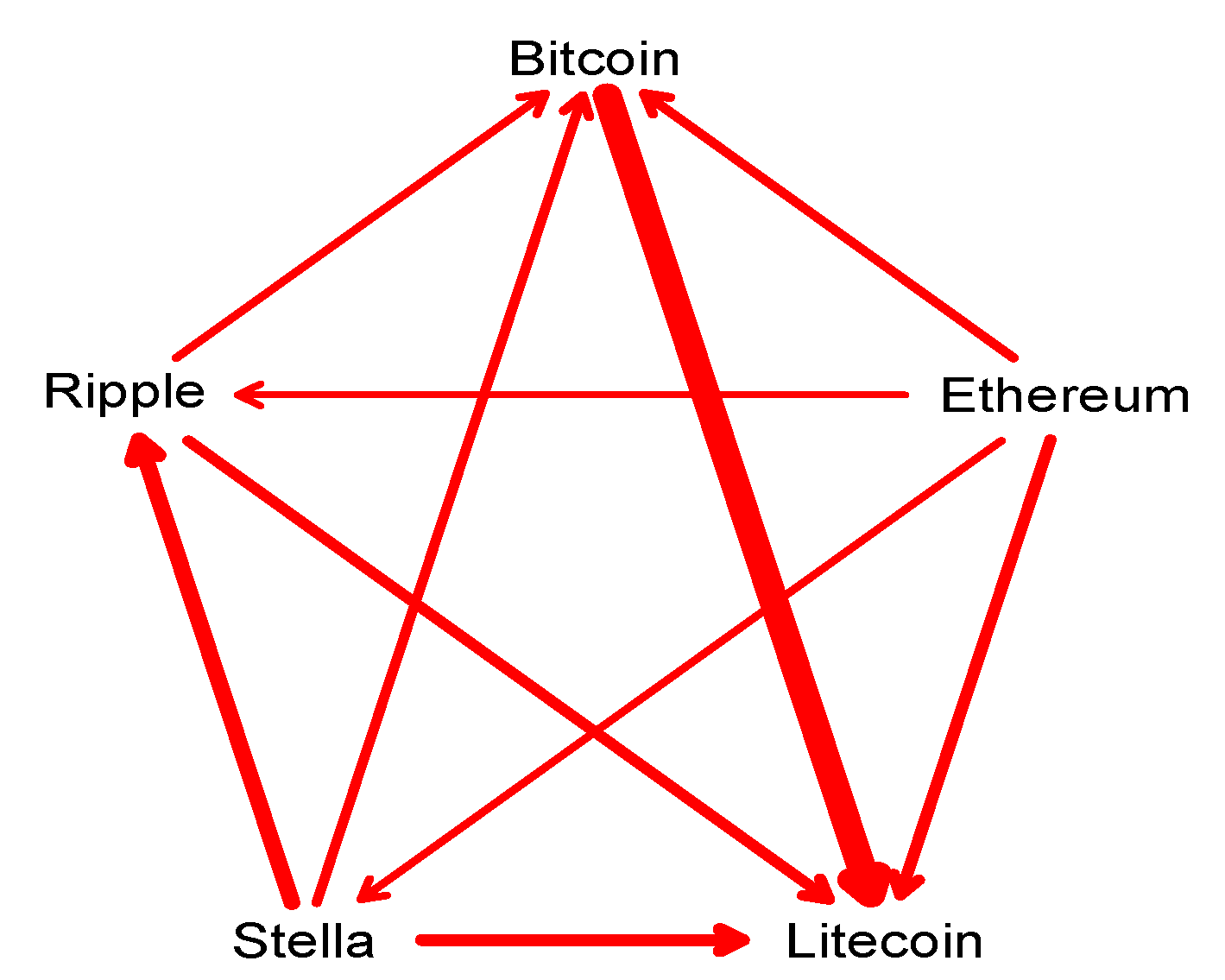

3.2. Results

4. Discussion

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Azoff, E. Michael. 1994. Neural Network Time Series Forecasting of Financial Markets. New York: John Wiley and Sons. [Google Scholar]

- Bação, Pedro, António Duarte, Helder Sebastião, and Srdjan Redzepagic. 2018. Information Transmission Between Cryptocurrencies: Does Bitcoin Rule the Cryptocurrency World? Scientific Annals of Economics and Business 65: 97–117. [Google Scholar] [CrossRef]

- Bouri, Elie, Syed Jawad Hussain Shahzad, and David Roubaud. 2019a. Co-explosivity in the cryptocurrency market. Finance Research Letters 29: 178–83. [Google Scholar] [CrossRef]

- Bouri, Elie, Rangan Gupta, and David Roubaud. 2019b. Herding behaviour in cryptocurrencies. Finance Research Letters 29: 216–21. [Google Scholar] [CrossRef]

- Bouri, Elie, Brian Lucey, and David Roubaud. 2019c. The volatility surprise of leading cryptocurrencies: Transitory and permanent linkages. Finance Research Letters. [Google Scholar] [CrossRef]

- Breitung, Jörg, and Bertrand Candelon. 2006. Testing for short-and long-run causality: A frequency-domain approach. Journal of Econometrics 132: 363–78. [Google Scholar] [CrossRef]

- Chang, Eric C., Joseph W. Cheng, and Ajay Khorana. 2000. An examination of herd behaviour in equity markets: An international perspective. Journal of Banking & Finance 24: 1651–99. [Google Scholar]

- Cherubini, Umberto, Fabio Gobbi, Sabrina Mulinacci, and Silvia Romagnoli. 2011. Dynamic Copula Methods in Finance, 1st ed. New York: John Wiley and Sons. [Google Scholar]

- Corbet, Shaen, Andrew Meegan, Charles Larkin, Brian Lucey, and Larisa Yarovaya. 2018. Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters 165: 28–34. [Google Scholar] [CrossRef]

- Diebold, Francis X., and Kamil Yilmaz. 2012. Better to give than to receive: Predictive directional measurement of volatility spillovers. International Journal of Forecasting 28: 57–66. [Google Scholar] [CrossRef]

- Diebold, Francis X., and Kamil Yilmaz. 2016. Trans-Atlantic equity volatility connectedness: U.S. and European financial institutions, 2004–2014. Journal of Financial Econometrics 14: 81–127. [Google Scholar] [CrossRef]

- Dyhrberg, Anne Haubo. 2016. Bitcoin, gold and the dollar-A GARCH volatility analysis. Financial Research Letters 16: 85–92. [Google Scholar] [CrossRef]

- Faraway, Julian, and Chris Chatfield. 1998. Time series forecasting with neural networks: A comparative study using the airline data. Applied Statistics 47: 231–50. [Google Scholar] [CrossRef]

- Ferrari, Silvia, and Francisco Cribari-Neto. 2004. Beta regression for modelling rates and proportions. Journal of Applied Statistics 31: 799–815. [Google Scholar] [CrossRef]

- Gkillas, Konstantinos, and Paraskevi Katsiampa. 2018. An Application of Extreme Value Theory to Cryptocurrencies. Economics Letters 164: 109–11. [Google Scholar] [CrossRef]

- Masarotto, Guido, and Cristiano Varin. 2017. Gaussian Copula Regression in R. Journal of Statistical Software 77: 1–26. [Google Scholar] [CrossRef]

- Guolo, Annamaria, and Cristiano Varin. 2014. Beta regression for time series analysis of bounded data, with application to Canada Google Flu Trends. The Annals of Applied Statistics 8: 74–88. [Google Scholar] [CrossRef]

- Hencic, Andrew, and Christian Gouriéroux. 2015. Noncausal Autoregressive Model in Application to Bitcoin/USD Exchange Rate. In Econometrics of Risk. Studies in computational intelligence. Cham: Springer, vol. 583, pp. 17–40. [Google Scholar]

- Hertz, John, Anders Krogh, and Richard Palmer. 1991. Introduction to the Theory of Neural Computation. Redwood City: Addison-Wesley. [Google Scholar]

- Hyndman, Rob, George Athanasopoulos, Chrisoph Bergmeir, Gabriel Caceres, Leanne Chhay, Mitchell O’Hara-Wild, Fotios Petropoulos, Slava Razbash, Earo Wang, and Farah Yasmeen. 2019. Forecast: Forecasting Functions for Time Series and Linear Models, R Package Version 8.8; Available online: http://pkg.robjhyndman.com/forecast (accessed on 5 August 2019).

- Ji, Qiang, Elie Bouri, Chi Keung Lau, and David Roubaud. 2019. Dynamic connectedness and integration in cryptocurrency markets. International Review of Financial Analysis 63: 257–72. [Google Scholar] [CrossRef]

- Jondeau, Eric, and Michael Rockinger. 2006. The copula-garch model of conditional dependencies: An international stock market application. Journal of International Money and Finance 25: 827–53. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi. 2017. Volatility estimation for Bitcoin: A comparison of GARCH models. Economics Letters 158: 3–6. [Google Scholar] [CrossRef] [Green Version]

- Katsiampa, Paraskevi. 2019. An empirical investigation of volatility dynamics in the cryptocurrency market. Research in International Business and Finance 50: 322–35. [Google Scholar] [CrossRef]

- Kim, Jong-Min, and Sun-Young Hwang. 2017. Directional Dependence via Gaussian Copula Beta Regression Model with Asymmetric GARCH Marginals. Communications in Statistics: Simulation and Computation 46: 7639–53. [Google Scholar] [CrossRef]

- Kojadinovic, Ivan, and Jun Yan. 2010. Modeling multivariate distributions with continuous margins using the copula R package. Journal of Statistical Software 34: 1–20. [Google Scholar] [CrossRef]

- Kristoufek, Ladislav. 2013. Bitcoin meets Google Trends and Wikipedia: Quantifying the relationship between phenomena of the Internet era. Scientific Reports 3: 3415. [Google Scholar] [CrossRef]

- Kuan, Chung-Ming, and Halbert White. 1994. Artificial neural networks: An econometric perspective (with discussion). Econometric Reviews 13: 1–143. [Google Scholar] [CrossRef]

- Masarotto, Guido, and Cristiano Varin. 2012. Gaussian copula marginal regression. Electronic Journal of Statistics 6: 1517–49. [Google Scholar] [CrossRef]

- Nelsen, Roger B. 2006. An Introduction to Copulas, 2nd ed. New York: Springer. [Google Scholar]

- Phillips, Peter, Shuping Shi, and Jun Yu. 2015. Testing for multiple bubbles: Historical episodes of exuberance and collapse in the S&P 500. International Economic Review 56: 1043–78. [Google Scholar]

- Ripley, Brian D. 1996. Pattern Recognition and Neural Networks. Cambridge: Cambridge University Press. [Google Scholar]

- Sklar, Abe. 1973. Random variables, joint distribution functions, and copulas. Kybernetika 9: 449–60. [Google Scholar]

- Stavroyiannis, Stavros, and Vassilios Babalos. 2017. Herding, faith-based investments and the global financial crisis: Empirical evidence from static and dynamic models. Journal of Behavioral Finance 18: 478–489. [Google Scholar] [CrossRef]

- Sungur, Engin A. 2005. A note on directional dependence in regression setting. Communications in Statistics: Theory and Methods 34: 1957–65. [Google Scholar] [CrossRef]

- Ziȩba, Damian, Ryszard Kokoszczyński, and Katarzyyna Śledziewska. 2019. Shock transmission in the cryptocurrency market. Is Bitcoin the most influential? International Review of Financial Analysis 64: 102–25. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| LBTC | LETH | LLTC | LXLM | LXRP | |

|---|---|---|---|---|---|

| Minimum | −20.7530 | −31.5469 | −39.5151 | −36.6358 | −61.6273 |

| Q1 | −0.9719 | −2.6806 | −1.6928 | −3.2394 | −2.1367 |

| Q2 | 0.2967 | −0.0894 | 0.0000 | −0.4066 | −0.3564 |

| Mean | 0.2775 | 0.4836 | 0.2283 | 0.3886 | 0.3407 |

| Q3 | 1.8199 | 3.2674 | 1.7673 | 3.1298 | 1.8960 |

| Maximum | 22.5119 | 41.2337 | 51.0348 | 72.3102 | 102.7356 |

| Skewness | −0.2519 | 0.5072 | 1.3240 | 2.0427 | 2.9787 |

| Kurtosis | 7.9613 | 7.6037 | 16.1616 | 18.0902 | 40.6386 |

| r | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| LETH | LLTC | LXLM | LXRP | LETH | LLTC | LXLM | LXRP | ||

| LBTC | 0.369 | 0.591 | 0.342 | 0.285 | LBTC | 0.136 | 0.350 | 0.117 | 0.081 |

| LETH | 0.359 | 0.257 | 0.239 | LETH | 0.129 | 0.066 | 0.057 | ||

| LLTC | 0.366 | 0.345 | LLTC | 0.134 | 0.119 | ||||

| LXLM | 0.540 | LXLM | 0.292 | ||||||

| LBTC | LETH | LLTC | LXLM | LXRP |

|---|---|---|---|---|

| NNAR(1,1) | NNAR(4,2) | NNAR(8,4) | NNAR(9,5) | NNAR(18,10) |

| (U,V) | V → U | U→ V | Diff = (V→ U - U→ V) | ||||

|---|---|---|---|---|---|---|---|

| Estimate (Diff) | Bias (Diff) | Std. Error (Diff) | MSE (Diff) | Boot 95% CI of Diff | |||

| (LBTC, LETH) | 0.1325 | 0.1028 | 0.0295 | 0.000002 | 0.000175 | 0.00000003 | (0.0291, 0.0298) |

| (LBTC, LLTC) | 0.3852 | 0.3890 | −0.0037 | 0.000003 | 0.000360 | 0.00000013 | (−0.0044, −0.0030) |

| (LBTC, LXLM) | 0.1299 | 0.1159 | 0.0143 | 0.000001 | 0.000180 | 0.00000003 | (0.0139, 0.0146) |

| (LBTC, LXRP) | 0.1141 | 0.1006 | 0.0138 | 0.000004 | 0.000186 | 0.00000003 | (0.0134, 0.0142) |

| (LETH, LLTC) | 0.1240 | 0.1578 | −0.0333 | 0.000007 | 0.000197 | 0.00000004 | (−0.0337, −0.0329) |

| (LETH, LXLM) | 0.1016 | 0.1090 | −0.0075 | −0.000003 | 0.000161 | 0.00000003 | (−0.0078, −0.0072) |

| (LETH, LXRP) | 0.0893 | 0.0974 | −0.0082 | −0.000002 | 0.000160 | 0.00000003 | (−0.0085, −0.0079) |

| (LLTC, LXLM) | 0.1863 | 0.1611 | 0.0250 | −0.000001 | 0.000219 | 0.00000005 | (0.0246, 0.0255) |

| (LLTC, LXRP) | 0.1587 | 0.1450 | 0.0134 | −0.000006 | 0.000224 | 0.00000005 | (0.0129, 0.0138) |

| (LXLM, LXRP) | 0.2111 | 0.2208 | −0.0093 | 0.000004 | 0.000208 | 0.00000004 | (−0.0097, −0.0089) |

| BTC | ETH | LTC | XLM | XRP | |

|---|---|---|---|---|---|

| Minimum | 12,712,600 | 102,128 | 507,480 | 491 | 24,819 |

| Q1 | 68,338,000 | 8,933,050 | 2,374,230 | 31,416 | 722,260 |

| Q2 | 277,084,992 | 69,245,600 | 12,755,200 | 543,934 | 5,013,190 |

| Mean | 2,347,742,132 | 821,315,142 | 224,843,171 | 37,125,273 | 307,798,172 |

| Q3 | 3,961,080,064 | 1,475,939,968 | 302,471,008 | 40,041,100 | 249,264,000 |

| Maximum | 23,840,899,072 | 9,214,950,400 | 6,961,679,872 | 1,513,270,016 | 9,110,439,936 |

| BTC | ETH | LTC | XLM | XRP | |

|---|---|---|---|---|---|

| r | 0.937 | 0.893 | 0.763 | 0.706 | 0.778 |

| 0.879 | 0.797 | 0.582 | 0.499 | 0.606 | |

| 0.950 | 0.862 | 0.757 | 0.774 | 0.778 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hyun, S.; Lee, J.; Kim, J.-M.; Jun, C. What Coins Lead in the Cryptocurrency Market: Using Copula and Neural Networks Models. J. Risk Financial Manag. 2019, 12, 132. https://doi.org/10.3390/jrfm12030132

Hyun S, Lee J, Kim J-M, Jun C. What Coins Lead in the Cryptocurrency Market: Using Copula and Neural Networks Models. Journal of Risk and Financial Management. 2019; 12(3):132. https://doi.org/10.3390/jrfm12030132

Chicago/Turabian StyleHyun, Steve, Jimin Lee, Jong-Min Kim, and Chulhee Jun. 2019. "What Coins Lead in the Cryptocurrency Market: Using Copula and Neural Networks Models" Journal of Risk and Financial Management 12, no. 3: 132. https://doi.org/10.3390/jrfm12030132

APA StyleHyun, S., Lee, J., Kim, J. -M., & Jun, C. (2019). What Coins Lead in the Cryptocurrency Market: Using Copula and Neural Networks Models. Journal of Risk and Financial Management, 12(3), 132. https://doi.org/10.3390/jrfm12030132