Influence of Venture Capital and Knowledge Transfer on Innovation Performance in the Big Data Environment

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Conceptual Model and Model Hypotheses

2.1. Conceptual Model for VC and Knowledge Transfer of a Firm

2.2. Model Hypotheses

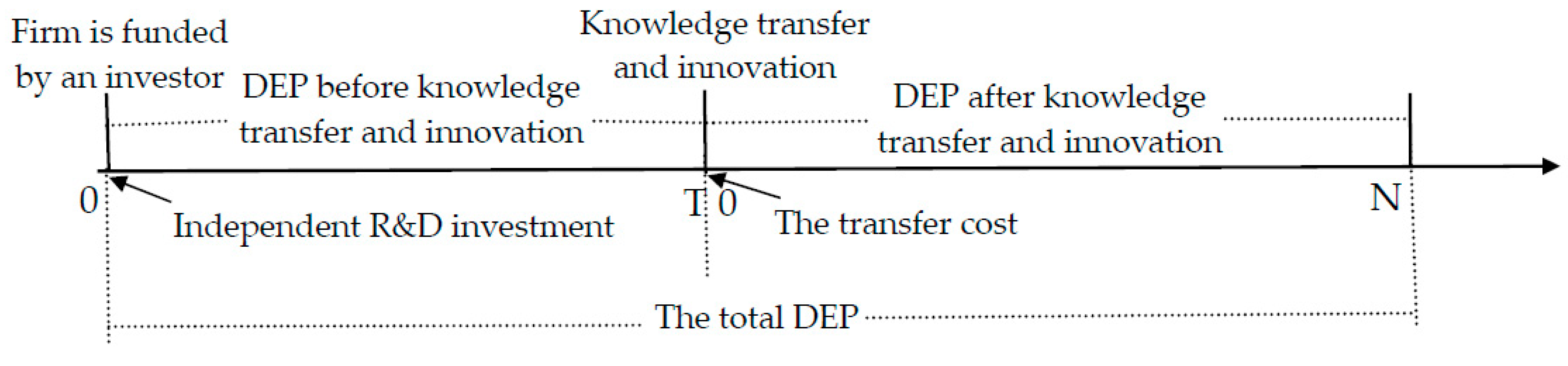

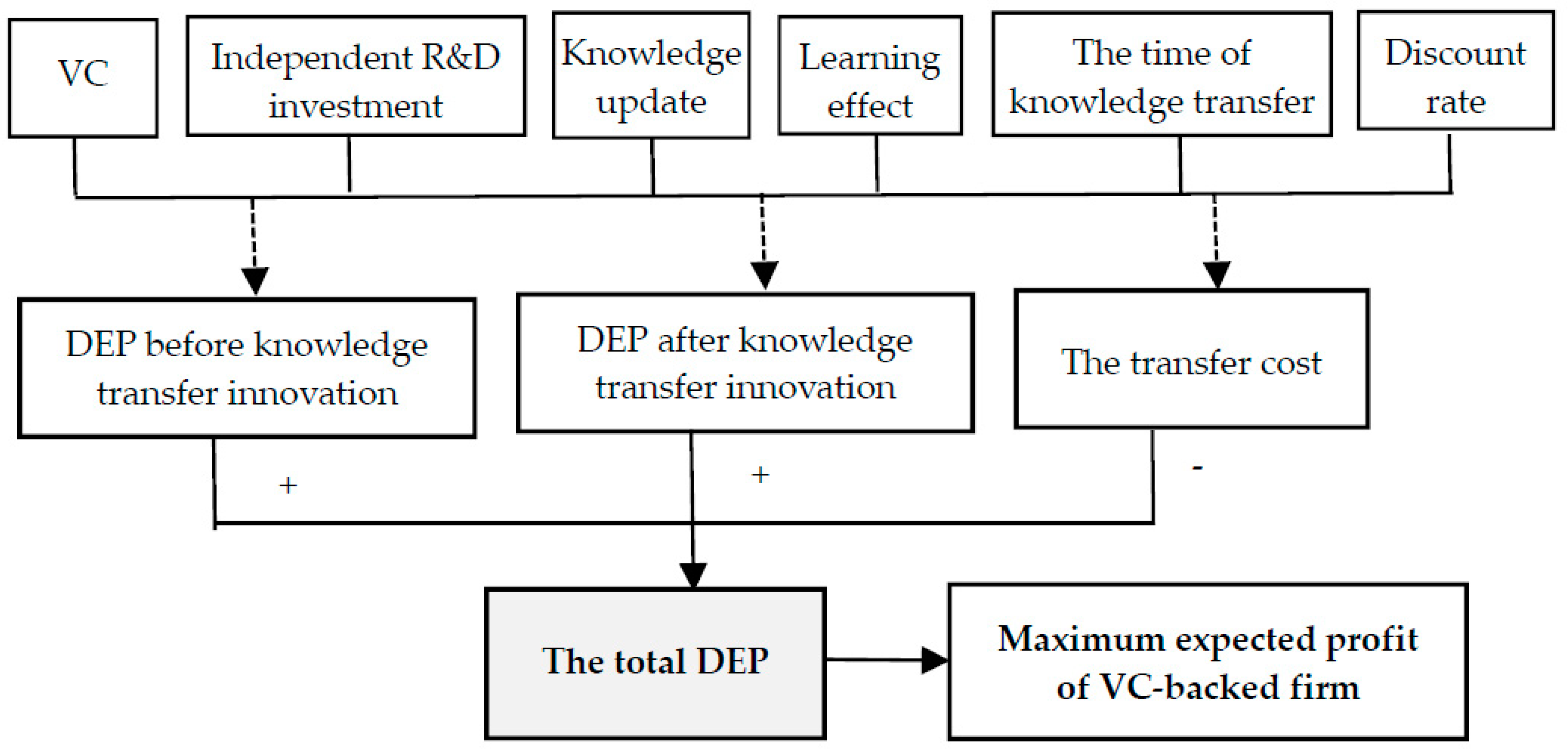

3. Decision Model of VC and Knowledge Transfer in the Big Data Environment

3.1. DEP before Knowledge Transfer and New Product Innovation

3.2. Cost of Knowledge Transfer and Innovation

3.3. DEP after Knowledge Transfer and New Product Innovation

3.4. Total DEP of a Venture-Backed Firm

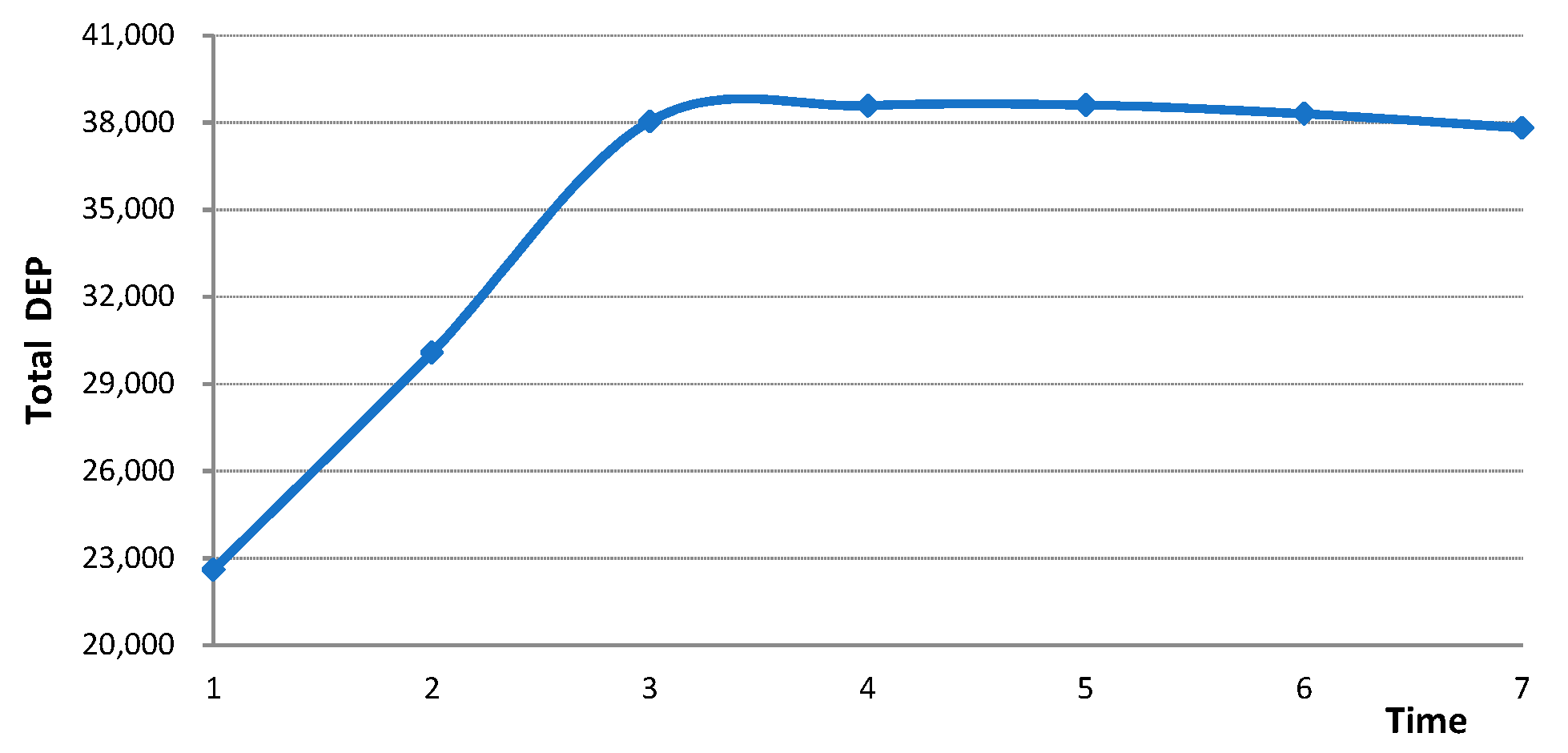

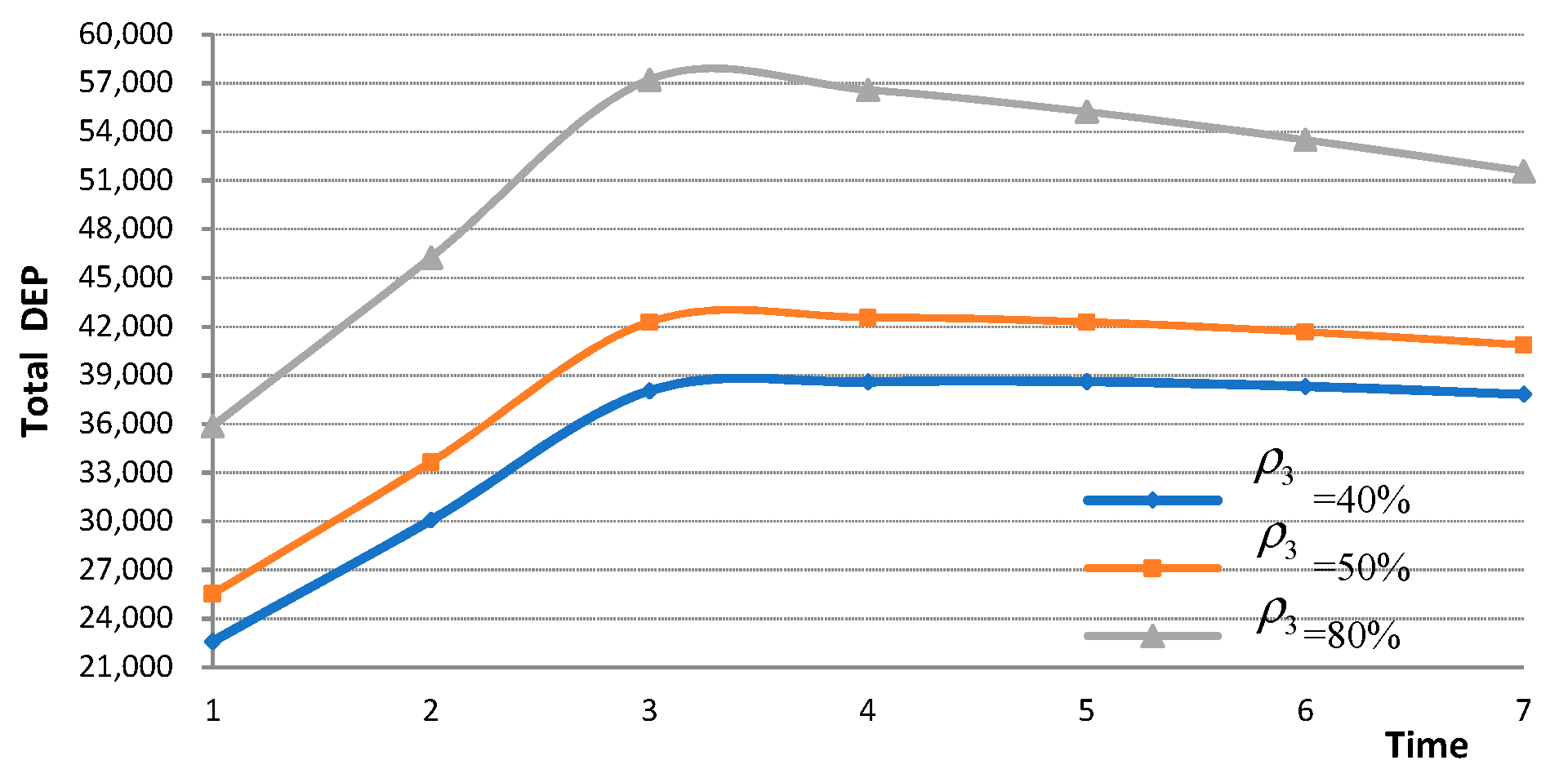

4. Simulation Experiments

4.1. Model Solution and Parameter Setting

4.2. Simulation Experiment

4.2.1. Simulation with IRR

4.2.2. Simulation with the Scale of Investment

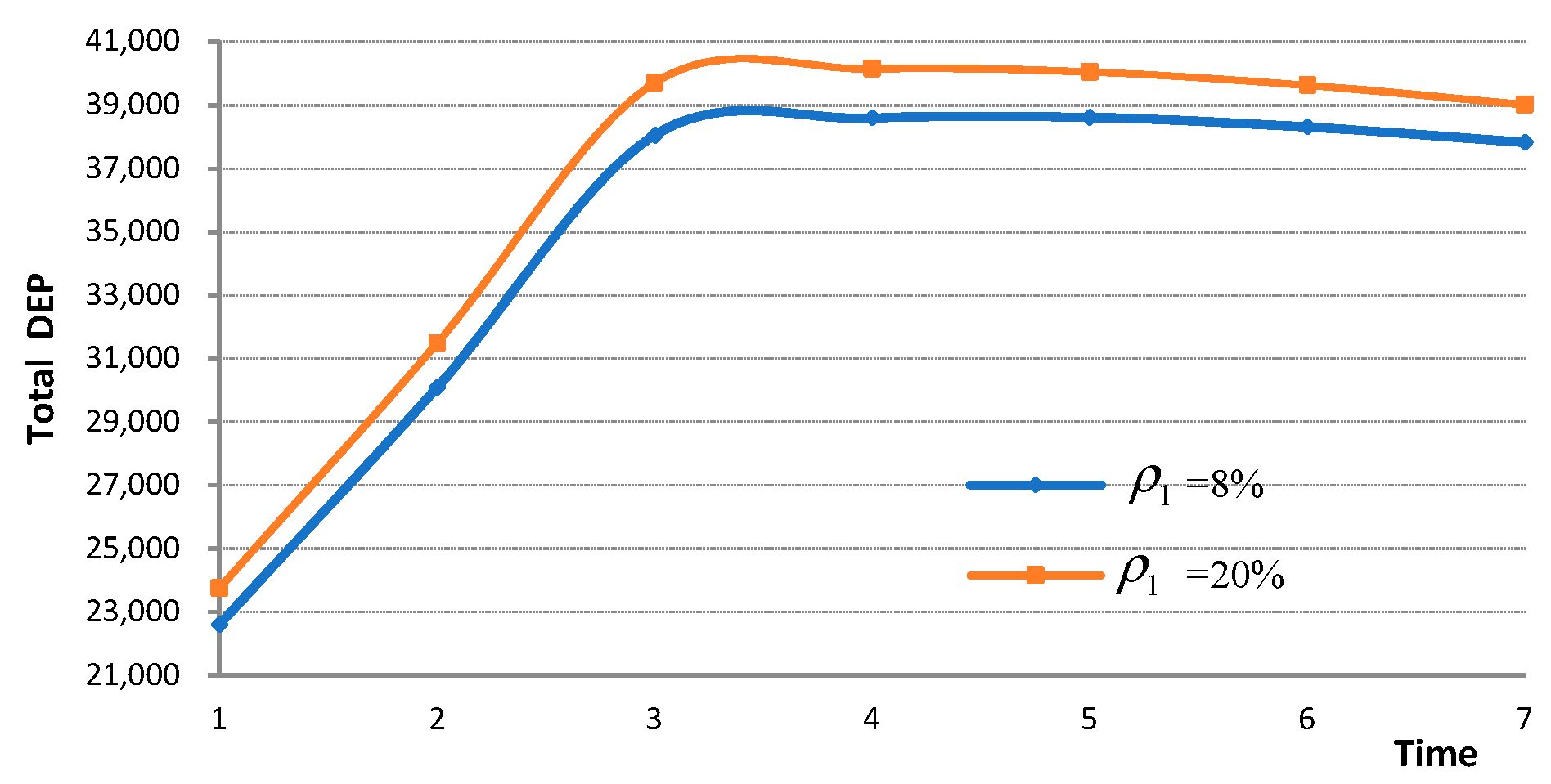

4.2.3. Simulation with

4.2.4. Simulation with

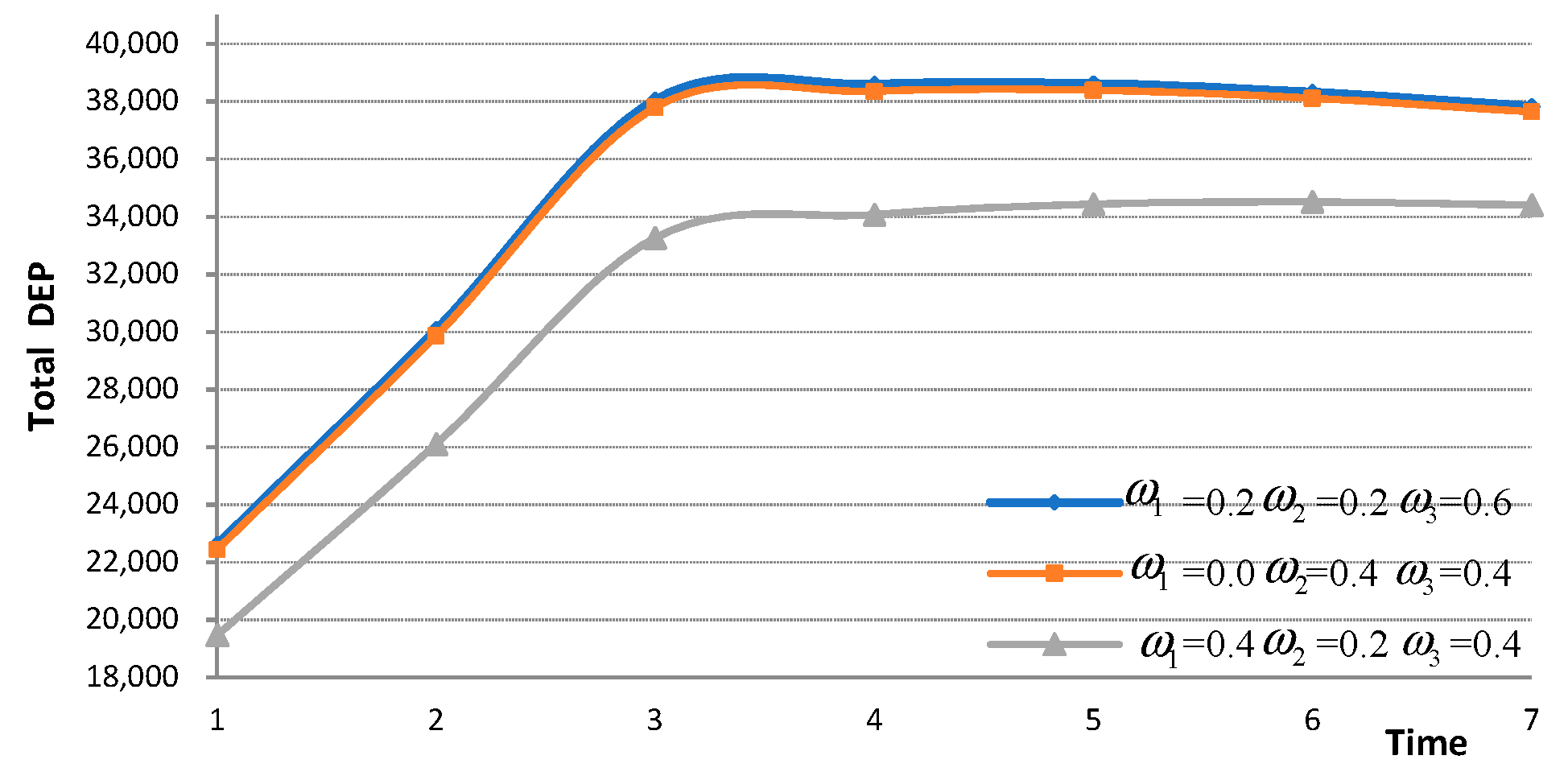

4.2.5. Simulation with the Weight of Each Type of Knowledge

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Bottazzi, Laura, Marco Da Rin, and Thomas Hellmann. 2008. Who are the active investors? Evidence from venture capital. Journal of Financial Economics 89: 488–512. [Google Scholar] [CrossRef] [Green Version]

- Bottazzi, Laura, Marco Da Rin, and Thomas Hellmann. 2009. What role of legal systems in financial intermediation? Theory and evidence. Journal of Financial Intermediation 18: 559–98. [Google Scholar] [CrossRef] [Green Version]

- Cassiman, Bruno, and Reinhilde Veugelers. 2006. In search of complementarity in innovation strategy: Internal R&D and external knowledge acquisition. Management Science 52: 68–82. [Google Scholar]

- Da Rin, Marco, and María Fabiana Penas. 2015. Venture capital and innovation strategies. Industrial and Corporate Change 2: 1–17. [Google Scholar]

- Dai, Hongkun, and Jiuping Xu. 2007. Optimal model of technology adoption time with learning effect and its simulation. Journal of Management Sciences in China 5: 21–27. [Google Scholar]

- Dessi, Roberta, and Nina Yin. 2015. Venture capital and knowledge transfer. TSE Working Papers 27: 51–54. [Google Scholar] [CrossRef] [Green Version]

- Doraszelski, Ulrich. 2004. Innovations, improvements and the optimal adoption of new technology. Journal of Economic Dynamics and Control 28: 1461–80. [Google Scholar] [CrossRef]

- Douglas, James M. 1988. Conceptual Design of Chemical Processes. New York: McGraw-Hill, pp. 1–601. [Google Scholar]

- Engelen, Andreas, Harald Kube, Susanne Schmidt, and Tessa Christina Flatten. 2014. Entrepreneurial orientation in turbulent environments: The moderating role of absorptive capacity. Research Policy 43: 1353–69. [Google Scholar] [CrossRef]

- Farzin, Y. Hossein, Kuno J. M. Huisman, and Peter M. Kort. 1998. Optimal timing of technology adoption. Journal of Economic Dynamics and Control 22: 779–99. [Google Scholar] [CrossRef] [Green Version]

- Gonzalez-Uribe, Juanita. 2014. Venture capital and the diffusion of knowledge. SSRN Electronic Journal 1: 1–95. Available online: https://www.ixueshu.com/document/2414547eb9a2e132318947a18e7f9386.html (accessed on 16 September 2019). [CrossRef]

- Hall, Bronwyn H., Adam Jaffe, and Manuel Trajtenberg. 2005. Market value and patent citations. RAND Journal of Economics 36: 16–38. [Google Scholar]

- Helmers, Christian, Manasa Patnam, and P. Raghavendra Rau. 2017. Do board interlocks increase innovation? Evidence from a corporate governance reform in India. Journal of Banking & Finance 80: 51–70. [Google Scholar]

- Hirukawa, Masayuki, and Masako Ueda. 2011. Venture Capital and Innovation: Which is first? Pacific Economic Review 16: 421–65. [Google Scholar] [CrossRef]

- Horst, Peter, and Robert Duboff. 2015. Don’t let big data bury your brand. Harvard Business Review 93: 78–86. [Google Scholar]

- Huang, Jinsong, Ping Zhao, Gao Wang, and Qibin Lu. 2004. Market share research based on customer orientation. Chinese Journal of Management Science 12: 96–101. [Google Scholar]

- Jain, Bharat A. 2001. Predictors of performance of venture capitalist-backed organizations. Journal of Business Research 52: 223–33. [Google Scholar] [CrossRef]

- Koman, Gabriel, and Jana Kundrikova. 2016. Application of big data technology in knowledge transfer process between business and academia. Procedia Economics & Finance 39: 605–11. [Google Scholar]

- Kortum, Samuel S., and Josh Lerner. 1998. Assessing the contribution of venture capital to innovation. RAND Journal of Economics 31: 674–92. [Google Scholar]

- Lerner, Josh. 1995. Venture capitalists and the oversight of private firms. Journal of Finance 50: 301–18. [Google Scholar] [CrossRef]

- McGuire, Tim, James Manyika, and Michael Chui. 2012. Why big data is the new competitive advantage. Ivey Business Journal 76: 1–4. [Google Scholar]

- Mellichamp, Duncan A. 2017. Internal rate of return: Good and bad features, and a new way of interpreting the historic measure. Computers and Chemical Engineering 106: 396–406. [Google Scholar] [CrossRef]

- Mollica, Marcos A., and Luigi Zingales. 2007. The Impact of Venture Capital on Innovation and the Creation of New Businesses. Available online: http://conference.nber.org/confer/2007/ENTf07/luigi.pdf (accessed on 16 September 2019).

- Pahnke, Emily Cox, Rory McDonald, Dan Wang, and Benjamin Hallen. 2014. Exposed: Venture capital, competitor ties, and entrepreneurial innovation. Academy of Management Journal 58: 1334–36. [Google Scholar] [CrossRef]

- Popov, Alexander, and Peter Rosenboom. 2009. Does Private Equity Investment Spur Innovation? Evidence from Europe. Working Paper, No. 1063. Available online: https://core.ac.uk/download/pdf/6601640.pdf (accessed on 16 September 2019).

- Rosenbusch, Nina, Jan Brinckmann, and Verena Müller. 2013. Does acquiring venture capital pay off for the funded firms? A meta-analysis on the relationship between venture capital investment and funded firm financial performance. Journal of Business Venturing 28: 335–53. [Google Scholar] [CrossRef]

- Rymkul, Ismailova, Amina Mussina, and Nurgul Ismagulova. 2015. Venture capital as a source of innovation’s financing. Australian Journal of Basic and Applied Sciences 9: 120–24. [Google Scholar]

- Sahlman, William, and Michael Gorman. 1989. What do venture capitalists do? Journal of Business Venturing 4: 231–48. [Google Scholar]

- Smolarski, Jan, and Can Kut. 2011. The impact of venture capital financing method on SME performance and internationalization. International Entrepreneurship and Management Journal 7: 39–55. [Google Scholar] [CrossRef]

- Wadhwa, Anu, Corey Phelps, and Suresh Kotha. 2016. Corporate venture capital portfolios and firm innovation. Journal of Business Venturing 31: 95–112. [Google Scholar] [CrossRef]

- Weber, Barbara, and Christiana Weber. 2007. Corporate venture capital as a means of radical innovation: Relational fit, social capital, and knowledge transfer. Journal of Engineering and Technology Management 24: 11–35. [Google Scholar] [CrossRef]

- Wu, Chuanrong, and Feng Li. 2019. Multi-objective fuzzy optimization of knowledge transfer organizations in big data environment. International Journal of Embedded Systems 11: 419–26. [Google Scholar] [CrossRef]

- Wu, Chuanrong, Evgeniya Zapevalova, and Deming Zeng. 2019a. Optimization model of price change after knowledge transfer in the big data environment. International Journal of Computational Science and Engineering 19: 284–92. [Google Scholar] [CrossRef]

- Wu, Chuanrong, Evgeniya Zapevalova, Yingwu Chen, and Feng Li. 2018. Time optimization of multiple knowledge transfers in the big data environment. Computers Materials & Continua 54: 269–85. [Google Scholar]

- Wu, Chuanrong, Veronika Lee, and Mark E. McMurtrey. 2019b. Knowledge composition and its influence on new product development performance. Computers Materials & Continua 60: 365–78. [Google Scholar]

- Xu, Minli, and Zigang Zhang. 2001. Application of real options theory to R&D project evaluation. Systems Engineering 1: 10–14. [Google Scholar]

- Yang, Xiaoming, Sunny Li Sun, and Haibin Yang. 2015. Market-based reform, synchronization and product innovation. Industrial Marketing Management 50: 30–39. [Google Scholar] [CrossRef]

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, C.; Yang, X.; Lee, V.; McMurtrey, M.E. Influence of Venture Capital and Knowledge Transfer on Innovation Performance in the Big Data Environment. J. Risk Financial Manag. 2019, 12, 188. https://doi.org/10.3390/jrfm12040188

Wu C, Yang X, Lee V, McMurtrey ME. Influence of Venture Capital and Knowledge Transfer on Innovation Performance in the Big Data Environment. Journal of Risk and Financial Management. 2019; 12(4):188. https://doi.org/10.3390/jrfm12040188

Chicago/Turabian StyleWu, Chuanrong, Xiaoming Yang, Veronika Lee, and Mark E. McMurtrey. 2019. "Influence of Venture Capital and Knowledge Transfer on Innovation Performance in the Big Data Environment" Journal of Risk and Financial Management 12, no. 4: 188. https://doi.org/10.3390/jrfm12040188

APA StyleWu, C., Yang, X., Lee, V., & McMurtrey, M. E. (2019). Influence of Venture Capital and Knowledge Transfer on Innovation Performance in the Big Data Environment. Journal of Risk and Financial Management, 12(4), 188. https://doi.org/10.3390/jrfm12040188