Option Pricing Incorporating Factor Dynamics in Complete Markets

, ,

, ,

Abstract

:1. Introduction

- Step 1:

- Introduce a continuous-time arbitrage-free model for the underlying stock price, for example, a geometric Brownian motion with instantaneous mean log-return and volatility , where r is the risk-free rate.

- Step 2:

- From the arbitrage-free asset pricing model5, obtain the continuous-time risk-neutral option price dynamics. In the case of geometric Brownian motion in the first step, these dynamics depend only on r, , and the option’s contract-specifications.

- Step 3:

- Construct a binomial tree on the risk-neutral world, ensuring convergence6 of the pricing tree to the limiting, risk-neutral, continuous-time price process.

2. Donsker–Prokhorov Invariance Principle and Binomial Option Pricing

2.1. Donsker–Prokhorov Invariance Principle

- (i)

- for every is a sequence of independent random variables, and is a sequence of independent normal random variables;

- (ii)

- . Letwhere: ; ; ; and , for .

- (i)

- ;

- (ii)

- weakly converges (Billingsley 1999) to as , and , for every and ;

- (iii)

- There exists22 a probability space with random elements and with values in such that (a) the probability law of coincides with the probability law of (i.e., ), for all ; (b) ; (c) ; and (d) , for every and .

2.2. General Binomial Pricing Tree and Its Limits via DPIP2

- (i)

- let , be the times at which an option trader, who holds a short position in the -contract, effects trades; and

- (ii)

- define the -pricing tree, , which (a) is -adapted, (b) is determined by the nodes , and (c) has the price dynamics,where . In (5), is the probability for upward movement of the stock price in .

2.3. Estimation of

3. General Binomial Option Pricing

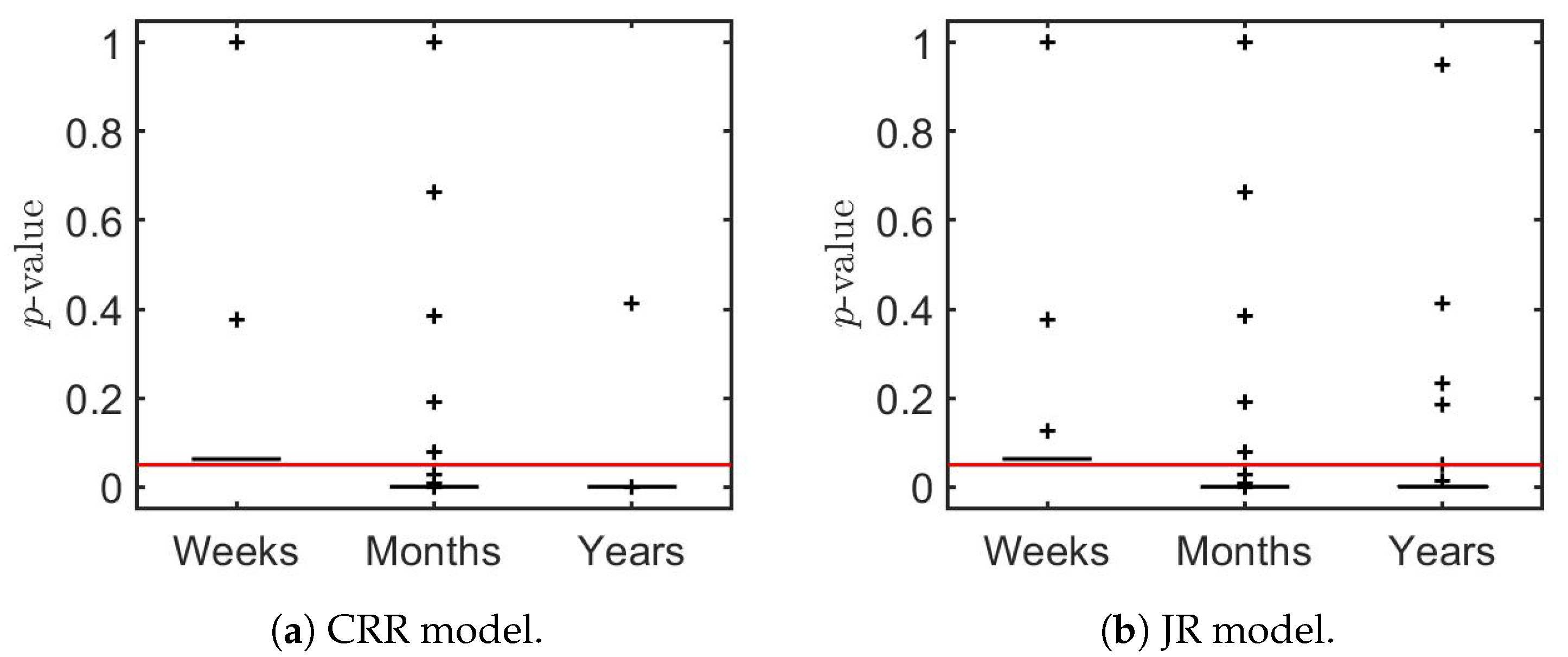

3.1. Comparison with CRR and JR Models

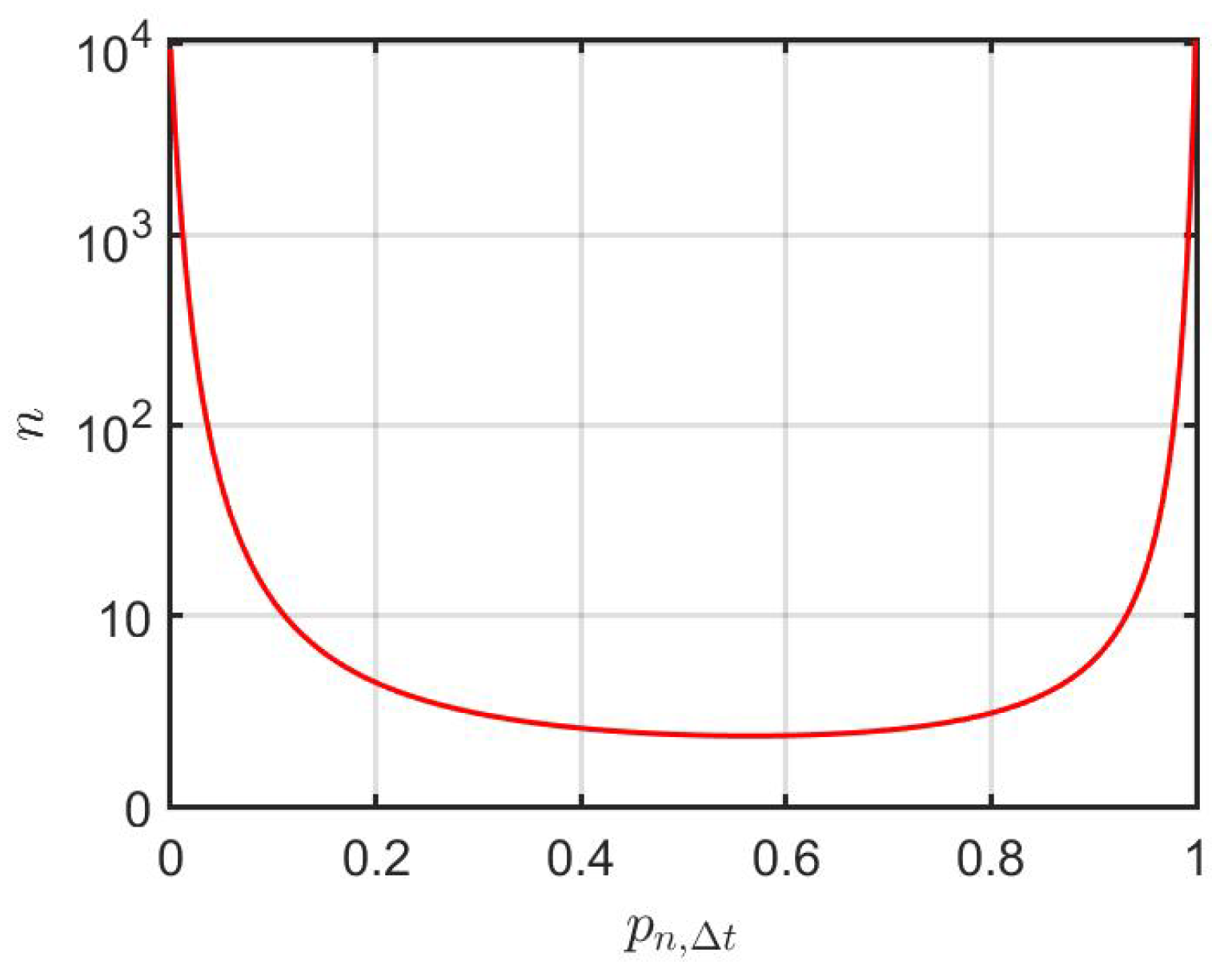

3.2. Rate of Loss of as Hedging Rate Increases

3.3. Estimation of the Implied Risk-Neutral Probability

4. Cherny–Shiryaev–Yor Invariance Principle and Path-Dependent Stock Log-Return Dynamics

- (i)

- ;

- (ii)

- for every compact interval J, there exists such that ;

- (iii)

- on each , the function is continuous, and has finite limits at those endpoints of which do not belong to .

4.1. An Extension of the Cherny–Shiryaev–Yor Invariance Principle

4.2. An Example

5. Option Pricing When the Underlying Stock Log-Returns Are Path-Dependent

An Example

6. Option Pricing for Markets with Informed Traders

6.1. Forward Contract Strategy

6.2. Option Pricing under Statistical Arbitrage Based on Forward Contracts

6.3. Implied Information Intensity

7. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

References

- Aragon, George O., and Wayne E. Ferson. 2006. Portfolio performance evaluation. Foundations and Trends in Finance 2: 83–190. [Google Scholar] [CrossRef] [Green Version]

- Audrino, Francesco, Robert Huitema, and Markus Ludwig. 2019. An empirical implementation of the Ross Recovery Theorem as a prediction device. Journal of Financial Econometrics. [Google Scholar] [CrossRef]

- Aït-Sahalia, Yacine, and Jean Jacod. 2014. High-Frequency Financial Econometrics. Princeton: Princeton University Press. [Google Scholar]

- Billingsley, Patrick. 1962. Limit theorems for randomly selected partial sums. Annals of Mathematical Statistics 33: 85–92. [Google Scholar] [CrossRef]

- Billingsley, Patrick. 1999. Convergence of Probability Measures, 2nd ed. New York: Wiley-Interscience. [Google Scholar]

- Black, Fischer, and Myron Scholes. 1973. The pricing of options and corporate liabilities. Journal of Political Economy 81: 637–54. [Google Scholar] [CrossRef] [Green Version]

- Borisov, Igor Semenovich. 1984. On the rate of convergence in the Donsker-Prokhorov invariance principle. Theory of Probability and Its Applications 28: 388–93. [Google Scholar] [CrossRef]

- Boyle, Phelim P. 1986. Option valuation using a three-jump process. International Options Journal 3: 7–12. [Google Scholar]

- Boyle, Phelim P. 1988. A lattice framework for option pricing with two state variables. Journal of Financial and Quantitative Analysis 23: 1–12. [Google Scholar] [CrossRef]

- Breloer, Bernhard, Hannah Lea Hühn, and Hendrik Scholz. 2016. Jensen alpha and market climate. Journal of Asset Management 17: 195–214. [Google Scholar] [CrossRef]

- Carhart, Mark M. 1997. On persistence of mutual fund performance. Journal of Finance 52: 57–82. [Google Scholar] [CrossRef]

- Chen, Louis H.Y., Larry Goldstein, and Qi-Man Shao. 2011. Normal Approximation by Stein’s Method. Berlin: Springer. [Google Scholar]

- Cherny, Aleksander S., Albert N. Shiryaev, and Marc Yor. 2003. Limit behavior of the “horizontal-vertical” random walk and some extensions of the Donsker-Prokhorov invariance principle. Theory of Probability and Its Applications 47: 377–94. [Google Scholar] [CrossRef] [Green Version]

- Coleman, Thomas F., and Yuying Li. 1996. A reflective Newton method for minimizing a quadratic function subject to bounds on some of the variables. SIAM Journal on Optimization 6: 1040–58. [Google Scholar] [CrossRef]

- Coviello, Rosanna, Cristina Di Girolami, and Franesco Russo. 2011. On stochastic calculus related to financial assets without semimartingales. Bulletin Des Sciences Mathématiques 135: 733–74. [Google Scholar] [CrossRef] [Green Version]

- Cox, John C., Stephen A. Ross, and Mark Rubinstein. 1979. Options pricing: A simplified approach. Journal of Financial Economics 7: 229–63. [Google Scholar] [CrossRef]

- Crimaldi, Irene, Dai Pra Paolo, Pierre-Yves Louis, and Ida G. Minelli. 2019. Synchronization and functional central limit theorems for interacting reinforced random walks. Stochastic Processes and Their Applications 129: 70–101. [Google Scholar] [CrossRef] [Green Version]

- Davydov, Youri, and Vladimir Rotar. 2008. On a non-classical invariance principle. Statistics & Probability Letters 78: 2031–38. [Google Scholar]

- Delbaen, Freddy, and Walter Schachermayer. 1998. The fundamental theorem of asset pricing for unbounded stochastic processes. Mathematische Annalen 312: 215–50. [Google Scholar] [CrossRef] [Green Version]

- Dhaene, Jan, Ben Stassen, Pierre Devolder, and Michel Vellekoop. 2015. The minimal entropy martingale measure in a market of traded financial and actuarial risks. Journal of Computational and Applied Mathematics 282: 111–33. [Google Scholar] [CrossRef] [Green Version]

- Donsker, Monroe D. 1951. An invariant principle for certain probability limit theorems. Memoirs of the American Mathematical Society 6: 1–10. [Google Scholar]

- Dudley, Richard M. 1968. Distances of probability measures and random variables. Annals of Mathematical Statistics 39: 1563–72. [Google Scholar] [CrossRef]

- Dudley, Richard M. 2018. Real Analysis and Probablity. Boca Raton: CRC Press. [Google Scholar]

- Duffie, Darrell. 2001. Dynamic Asset Pricing Theory, 3rd ed. Princeton: Princeton University Press. [Google Scholar]

- Duffie, Darrell, and Henry R. Richardson. 1991. Mean-variance hedging in continuous time. The Annals of Applied Probability 1: 1–15. [Google Scholar] [CrossRef]

- Easley, David, and Maureen O’Hara. 2003. Microstructure and asset pricing. In Handbook of the Economics of Finance. Edited by G. M. Constantinides, M. Harris and R. M. Stulz. Amsterdam: Elsevier, vol. 1, pp. 1021–51. [Google Scholar]

- Esche, Felix, and Martin Schweizer. 2005. Minimal entropy preserves the Lévy property: How and why. Stochastic Processes and Their Applications 115: 299–27. [Google Scholar] [CrossRef] [Green Version]

- Fama, Eugene, and Kenneth French. 1993. Common risk factors in the returns on stocks and bonds. Journal of Financial Economics 33: 3–56. [Google Scholar] [CrossRef]

- Fama, Eugene, and Kenneth French. 2004. The capital asset pricing model: Theory and evidence. Journal of Economic Perspectives 18: 25–46. [Google Scholar] [CrossRef] [Green Version]

- Fama, Eugene, and Kenneth French. 2015. A five-factor asset pricing model. Journal of Financial Economics 116: 1–22. [Google Scholar] [CrossRef] [Green Version]

- Fama, Eugene, and Kenneth French. 2017. International tests of a five-factor asset pricing model. Journal of Financial Economics 123: 441–63. [Google Scholar] [CrossRef]

- Fischer, Hans. 2011. A History of the Central Limit Theorem. From Classical to Modern Probability Theory. New York: Springer. [Google Scholar]

- Florescu, Ionut, and Frederi G. Viens. 2008. Stochastic volatility: Option pricing using a multinomial recombining tree. Journal of Applied Mathematical Finance 15: 151–81. [Google Scholar] [CrossRef]

- Fortet, R., and E. Mourier. 1953. Convergence de la répartition empirique vers la répartition théorique. Annales Scientifiques de L’École Normale Supérieure 70: 267–85. [Google Scholar] [CrossRef]

- Fujiwara, Tsukasa, and Yoshio Miyahara. 2003. The minimal entropy martingale measures for geometric Lévy processes. Finance and Stochastics 7: 509–31. [Google Scholar] [CrossRef]

- Gikhman, Iosif I., and Anatoly V. Skorokhod. 1969. Introduction to the Theory of Random Processes. Philadephia: W.B. Saunders Company. [Google Scholar]

- Gut, Allan. 2009. Stopped Random Walks, 2nd ed. New York: Springer. [Google Scholar]

- Hasbrouk, Joel. 1996. Modeling microstructure time series. In The Handbook of Statistics. Edited by G. S. Maddala and C. R. Rao. Amsterdam: Elsevier, vol. 14, pp. 47–691. [Google Scholar]

- Hasbrouk, Joel. 2007. Empirical Market Microstructure. New York: Oxford Press. [Google Scholar]

- Hu, Yuan, Abootaleb Shirvani, Stoyan V. Stoyanov, Young Shin Kim, Frank J. Fabozzi, and Svetlozar T. Rachev. 2020. Option pricing in markets with informed traders. International Journal of Theoretical and Applied Finance. [Google Scholar] [CrossRef]

- Hull, John C. 2018. Options, Futures, and Other Derivatives, 10th ed. New York: Pearson. [Google Scholar]

- Jabbour, George M., Marat V. Kramin, Timur Kramin, and Stephen D. Young. 2005. Multinomial Lattices and Derivatives Pricing. In Advances in Quantitative Analysis of Finance and Accounting. Edited by C. -F. Lee. Singapore: World Scientific, vol. 2, pp. 1–17. [Google Scholar]

- Jackwearth, Jens C., and Marco Menner. 2020. Does the Ross recovery theorem work empirically? Journal of Financial Economics 137: 723–39. [Google Scholar] [CrossRef]

- Jacod, Jean, and Philip Protter. 2012. Discretization of Processes, Stochastic Modeling and Applied Probability. Heidelberg: Springer, vol. 67. [Google Scholar]

- Jarrow, Robert A., and Andrew Rudd. 1983. Option Pricing. Homewood: Richard D. Irwin. [Google Scholar]

- Jensen, Michael C. 1968. The performance of mutual funds in the period 1945–1964. Journal of Finance 23: 389–416. [Google Scholar] [CrossRef]

- Jensen, Michael C. 1969. Risk, the pricing of capital assets, and the evaluation of investment portfolios. Journal of Business 42: 167–247. [Google Scholar] [CrossRef]

- Johnson, R. Stafford, James Pawlukiewicz, and Jayesh Mehta. 1997. Binomial option pricing with skewed asset returns. Review of Quantitative Finance and Accounting 9: 89–101. [Google Scholar] [CrossRef]

- Kim, Young Shin, Stoyan V. Stoyanov, Svetlozar T. Rachev, and Frank J. Fabozzi. 2016. Multi-purpose binomial model: Fitting all moments to the underlying Brownian motion. Economics Letters 145: 225–29. [Google Scholar] [CrossRef] [Green Version]

- Kim, Young Shin, Stoyan V. Stoyanov, Svetlozar T. Rachev, and Frank J. Fabozzi. 2019. Enhancing binomial and trinomial option pricing models. Finance Research Letters 28: 185–90. [Google Scholar] [CrossRef] [Green Version]

- Madan, Dilip, Frank Milne, and Hersh Shefrin. 1989. The multinomial option pricing model and its Brownian and Poisson limits. Review of Financial Studies 2: 251–65. [Google Scholar] [CrossRef]

- Major, Péter. 1978. On the invariance principle for independent identically distributed random variables. Journal of Multivariate Analysis 8: 487–517. [Google Scholar] [CrossRef] [Green Version]

- Merton, Robert C. 1973. Theory of rational option pricing. Bell Journal of Economics and Management Science 4: 141–83. [Google Scholar] [CrossRef] [Green Version]

- O’Hara, Maureen. 1998. Market Microstructure Theory. Malden: Blackwell. [Google Scholar]

- Pesšta, Michal, and Ostap Okhrin. 2014. Conditional least squares and copulae in claims reserving for a single line of business. Mathematics and Economics 56: 28–37. [Google Scholar] [CrossRef] [Green Version]

- Prokhorov, Yuri V. 1956. Convergence of random processes and limit theorems in probability theory. Theory of Probability and its Applications 1: 157–14. [Google Scholar] [CrossRef]

- Rachev, Svetlozar T. 1985. The Monge-Kantorovich mass transference problem and its stochastic applications. Theory of Probability & Its Applications 29: 647–76. [Google Scholar]

- Rendleman, Richard J., and Brit J. Bartter. 1979. Two-state option pricing. Journal of Finance 34: 1093–110. [Google Scholar] [CrossRef]

- Ross, Stephen A. 2015. The recovery theorem. Journal of Finance 70: 615–48. [Google Scholar] [CrossRef] [Green Version]

- Rubinstein, Mark. 2000. On the relation between binomial and trinomial option pricing models. Journal of Derivatives 8: 47–50. [Google Scholar] [CrossRef] [Green Version]

- Senatov, Vladimir V. 2017. On the real accuracy of approximation in the central limit theorem. II. Siberian Advances in Mathematics 27: 133–52. [Google Scholar] [CrossRef]

- Sierag, Dirk, and Bernard Hanzon. 2018. Pricing derivatives on multiple assets: Recombining multinomial trees based on Pascal’s simplex. Annals of Operations Research 266: 101–27. [Google Scholar] [CrossRef]

- Silvestrov, Dmitrii S. 2004. Limit Theorems for Randomly Stopped Stochastic Processes. London: Springer. [Google Scholar]

- Skorokhod, Anatoliy V. 1956. Limit theorems for stochastic processes. Theory of Probability and its Applications 1: 261–90. [Google Scholar] [CrossRef]

- Skorokhod, Anatoliy V. 2005. Basic Principles and Applications of Probability Theory. Heidelberg: Springer. [Google Scholar]

- Tanaka, Katsuto. 2017. Time Series Analysis. Nonstationary and Noninvertible Distribution Theory, 2nd ed. Hoboken: Wiley. [Google Scholar]

- Whaley, Robert E. 2006. Derivatives: Markets, Valuation and Risk Management. Hoboken: Wiley. [Google Scholar]

- Yamada, Yuji, and James A. Primbs. 2004. Properties of multinomial lattices with cumulants for option pricing and hedging. Asia-Pacific Financial Markets 11: 335–65. [Google Scholar] [CrossRef] [Green Version]

- Yuen, Fei Lung, Tak Siu, and Hailiang Yang. 2013. Option valuation by a self-exciting threshold binomial model. Mathematical and Computer Modeling 58: 28–37. [Google Scholar] [CrossRef]

| 1. | |

| 2. | Cox et al. (1979) used the central limit theorem for triangular series, which can be viewed as a special case of DPIP. |

| 3. | See Jarrow and Rudd (1983); Hull (2018); Boyle (1986, 1988); Madan et al. (1989); Rubinstein (2000); Jabbour et al. (2005); Whaley (2006); Florescu and Viens (2008); Yuen et al. (2013); Sierag and Hanzon (2018). |

| 4. | On rare occasions, the weak convergence of the càdlàg price process generated by the binomial (trinomial or multinomial) pricing tree is shown. |

| 5. | This step is based on the Fundamental Theorem of Asset Pricing, see Delbaen and Schachermayer (1998), Duffie (2001), Chapter 6. |

| 6. | The convergence is either (a) in terms of one-dimensional distributions of the process generated by the risk-neutral pricing tree, or (b) in terms of multivariate distributions, or (c) in Skorokhod -topology. |

| 7. | |

| 8. | |

| 9. | We denote “with probability” as “w.p.” for brevity. The condition guarantees that the binomial series generated by over multiple time steps is recombining. It also enables the analysis to pass naturally to the classical Black–Scholes–Merton continuum limit. We note that the same argument can be extended for any ; see Rendleman and Bartter (1979), and Hu et al. (2020) for various extensions. Under these extensions, the forms for u and d become more complicated. |

| 10. | |

| 11. | |

| 12. | |

| 13. | For example, Billingsley (1962); Silvestrov (2004), Chapter 4; Gut (2009), Chapter 5; Tanaka (2017), Chapter 2; Cherny et al. (2003); and Crimaldi et al. (2019). |

| 14. | The options data are from CBOE options on MSFT, see https://datashop.cboe.com/option-trades. |

| 15. | See Cox et al. (1979) for the CRR-binomial option pricing model; Jarrow and Rudd (1983) and Hull (2018) for the JR-binomial option pricing model. |

| 16. | |

| 17. | The risky asset is the stock and will be denoted by . |

| 18. | The risk-free asset will be a bond and will be denoted by . |

| 19. | The option or derivative will be denoted by . |

| 20. | See Rachev (1985), , where . The Skorokhod space is the space of all functions that are right continuous with left-hand limits (càdlàg functions), and , which is the Skorokhod–Billigsley metric in with being the Skorokhod–Billingsley metric in ; see Section 12 of Billingsley (1999); Skorokhod (1956). |

| 21. | |

| 22. | |

| 23. | See Davydov and Rotar (2008). |

| 24. | Applying DPIP1 to binomial option pricing will allow the trading of the replication portfolios to occur in time-instances with general time-varying trading frequency , which is an important issue in market microstructure. To go beyond the dynamic asset pricing model of Delbaen and Schachermayer (1998) will require approaches based upon market microsctructure. (See, e.g., O’Hara (1998); and Hasbrouk (2007).) We believe that DPIP1 will provide a bridge between dynamic asset pricing and market microstructure. Applying DPIP2 restricts the trading frequency to . |

| 25. | Coviello et al. (2011) discussed dynamic asset pricing models based on so-called A-semimartingales. A-semimartingales can appear as limits in the DPIP1. This paper falls within the framework of reconciling dynamic asset pricing theory with market microstructure. |

| 26. | |

| 27. | |

| 28. | The theoretical bounds for the rate of convergence in DPIP have been the subject of numerous papers, see for example, Borisov (1984). In our univariate case, the theoretical bounds of the rate of convergence are known as Berry–Esseen bounds; see for example Chen et al. (2011), Chapter 3. |

| 29. | |

| 30. | The CBOE Mini-SPX option contract, known by its symbol XSP, is an index option product designed to track the underlying S&P 500 Index. See https://www.cboe.com/tradable_products/sp_500/mini_spx_options. |

| 31. | Here, use 10-year Treasury rate as risk-free rate, see https://www.treasury.gov/resource-center/data-chart-center/interest-rates/pages/textview.aspx?data=yield. |

| 32. | This reflects the desire of a central bank not to disturb the tendencies of the real world by too large a factor. See, e.g., Dhaene et al. (2015), Esche and Schweizer (2005) and Fujiwara and Miyahara (2003) for related work on minimal entropy martingale measures applied to markets. |

| 33. | Each can be a closed, open, semi-open interval or a point. |

| 34. | |

| 35. | The summations can be changed to have the weights linearly increasing toward present time without affecting any of the convergence properties of the model. |

| 36. | Obviously other functions in the class of CSY piecewise continuous functions are possible, including, for example, Student’s t or generalized hyperbolic distributions to capture heavy tailed behavior. The choice should be governed by the desire to obtain a “good calibration”. |

| 37. | See Coleman and Li (1996). |

| 38. | It is tempting to include the historical data on upturns of the log-return series of MSFT as its own “index”. However, this is inherently inconsistent with our findings that the stock price dynamics does not follow the discrete dynamics of a generalized Brownian motion. |

| 39. | |

| 40. | See Fama and French (1993). More general factor models can also be considered (e.g., Carhart (1997), Fama and French (2004, 2015, 2017)). |

| 41. | |

| 42. | We set 1 July 2019 as . Based on the information on 1 July 2019, the initial capital , and annual risk-free rate . |

| 43. | |

| 44. | By observing the price trajectory , ℵ knows whether the log-return process is above or below the “benchmark level” with probability . |

| 45. | We assume that has a continuous first derivative. |

| 46. | To have the inequalities, , satisfied, we assume functions and are uniformly bounded, and furthermore, is sufficiently large. |

| 47. | The parameter will be optimized and will enter the formula for the non-negative yield that ℵ will receive when trading options; see Section 6.2. The long position in the forward contract could be taken by any trader who believes that is more likely to happen. |

| 48. | |

| 49. | The case of a misinformed trader can be considered in a similar manner. A misinformed trader with trades long-forward (resp. short-forward) when the informed trader with trades short-forward (resp. long-forward). A noisy trader (the trader with ) will not trade any forward contracts, as he has no information about stock price direction. |

| 50. | The long position in the option contract is taken by a trader who trades the stock S with market perceived stock dynamics given by (19). |

| 51. | With every single share of the traded stock with price at , ℵ simultaneously enters forward contracts. The forward contracts are long or short, depending on ℵ’s views on the sign of . It costs nothing to enter a forward contract at with terminal time . |

| 52. | If ℵ is a misinformed trader, the opposite of an informed trader is followed, that is, what is a profit for the informed trader will be a loss for the misinformed trader. Thus, in general, if , for some , the dividend yield , is given by , where , if ; , if ; and , if . |

| 53. | The data set includes MSFT price data over the period 1 July 2018 to 30 June 2020 (Yahoo Finance); S&P 500 price data from 1 July 2019 to 30 June 2020 (Yahoo Finance); 10-year Treasury rate from 1 July 2019 to 30 June 2020 (U.S. Department of the Treasury); and the call option price data for the MSFT at 1 July 2019 (CBOE). |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Factor | RMSE | ||||||

|---|---|---|---|---|---|---|---|

| S&P | 0.0016 | 0.0020 | 0.29 | 8.8 | 0.089 | 0.0214 | |

| S&P | 0.0016 | 0.37 | 9.9 | 0.44 | 0.052 | 0.0214 | |

| S&P Hist | 0.014 | 0.0014 | 0.13 | 1.09 | 0.10 | 0.0214 | |

| S&P with ARMA(1,1)-GJR GARCH(1,1) innovations modeled by: | |||||||

| ghyp | 0.0013 | 0.0078 | 0.073 | 0.35 | 0.072 | 0.0254 | |

| stud t | 0.0017 | 0.011 | 0.22 | 1.1 | 0.10 | 0.0252 | |

| norm | 0.0018 | 0.0038 | 0.077 | 1.1 | 0.10 | 0.0253 | |

| J | 0.0019 | 0.0065 | 0.083 | 73 | 0.11 | 0.0244 | |

| J | 0.0020 | 0.0062 | 0.0000 | 0.0027 | 0.84 | 0.0244 | |

| FF3 | 0.0019 | 0.0049 | 0.012 | 0.0008 | 0.0249 | ||

| FF3 | 0.0018 | 0.0044 | 0.0068 | 0.59 | 1.09 | 0.0249 | |

| Student’s t | Generalized Hyperbolic | |||||||

|---|---|---|---|---|---|---|---|---|

| Parameter | Estimate | SE | t-Value | p-Value | Estimate | SE | t-Value | p-Value |

| 0.067 | 0.94 | 0.06 | 0.95 | |||||

| 0.37 | 0.87 | 0.38 | 0.30 | 0.40 | 0.77 | 0.44 | ||

| −0.45 | 0.35 | −1.3 | 0.19 | −0.44 | 0.37 | −1.2 | 0.24 | |

| 0.32 | 0.75 | 1.46 | 0.14 | |||||

| 0.24 | 0.35 | 0.68 | 0.50 | 0.24 | 0.13 | 1.82 | 0.07 | |

| 0.727 | 0.024 | 29 | 0 | 0.724 | 0.05 | 14 | 0 | |

| −0.10 | 0.14 | −0.67 | 0.51 | −0.11 | 0.16 | −0.68 | 0.50 | |

| shape () | 13 | 6.3 | 2.05 | 0.04 | 2.5 | 58 | 0.04 | 0.97 |

| skew () | −0.31 | 7.5 | −0.04 | 0.97 | ||||

| −5.8 | 42 | −0.14 | 0.89 | |||||

| Robust standard errors | ||||||||

| parameter | estimate | SE | t-value | p-value | estimate | SE | t-value | p-value |

| 0.0024 | 0.017 | 0.99 | 0.054 | 0.96 | ||||

| 0.79 | 0.41 | 0.68 | 0.30 | 0.51 | 0.60 | 0.55 | ||

| −0.45 | 0.64 | −0.71 | 0.48 | −0.44 | 0.44 | −1.0 | 0.32 | |

| 0.034 | 0.97 | 0.48 | 0.63 | |||||

| 0.24 | 3.4 | 0.070 | 0.94 | 0.24 | 0.38 | 0.64 | 0.52 | |

| 0.727 | 0.52 | 1.4 | 0.16 | 0.724 | 0.089 | 8.1 | 0 | |

| −0.10 | 0.18 | −0.54 | 0.59 | −0.11 | 0.31 | −0.34 | 0.73 | |

| shape () | 13 | 110 | 0.12 | 0.91 | 2.5 | 343 | 0.007 | 0.99 |

| skew () | −0.31 | 43 | −0.007 | 0.99 | ||||

| −5.8 | 229 | −0.026 | 0.98 | |||||

| Estimate | Standard Error | t-Statistic | p-Value | |

|---|---|---|---|---|

| 0.00 | 0.00 | 0.52 | 0.6 | |

| 0.33 | 0.44 | 0.74 | 0.45 | |

| −0.45 | 0.42 | −1.08 | 0.28 | |

| 0.00 | 0.00 | 2.08 | 0.04 | |

| 0.71 | 0.07 | 10.85 | 0.00 | |

| 0.25 | 0.08 | 3.36 | 0.00 | |

| 13.7 | 12.75 | 1.07 | 0.28 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hu, Y.; Shirvani, A.; Lindquist, W.B.; Fabozzi, F.J.; Rachev, S.T. Option Pricing Incorporating Factor Dynamics in Complete Markets. J. Risk Financial Manag. 2020, 13, 321. https://doi.org/10.3390/jrfm13120321

Hu Y, Shirvani A, Lindquist WB, Fabozzi FJ, Rachev ST. Option Pricing Incorporating Factor Dynamics in Complete Markets. Journal of Risk and Financial Management. 2020; 13(12):321. https://doi.org/10.3390/jrfm13120321

Chicago/Turabian StyleHu, Yuan, Abootaleb Shirvani, W. Brent Lindquist, Frank J. Fabozzi, and Svetlozar T. Rachev. 2020. "Option Pricing Incorporating Factor Dynamics in Complete Markets" Journal of Risk and Financial Management 13, no. 12: 321. https://doi.org/10.3390/jrfm13120321

APA StyleHu, Y., Shirvani, A., Lindquist, W. B., Fabozzi, F. J., & Rachev, S. T. (2020). Option Pricing Incorporating Factor Dynamics in Complete Markets. Journal of Risk and Financial Management, 13(12), 321. https://doi.org/10.3390/jrfm13120321