Crowdfunding in a Competitive Environment †

Abstract

:1. Introduction

2. Literature Review

3. Crowdfunding and Monopoly

- Firm chooses c. is determined.

- Firm chooses s. p is determined.

4. A Market with Competition

- Firms decide whether to use crowdfunding (this strategy will be denoted CF) or not (S).

- Firms observe each other’s decisions.

- Firms choose . is determined.

- Firms choose . p is determined.

5. Imperfect Information

6. The Main Implications of The Model and Its Contribution to The Literature

7. Model Extensions and Robustness

7.1. Different Types of Market Structure

7.2. Platform Fees

7.3. Fixed Start-Up Costs

7.4. Risk of Crowdfunding Campaign Failure

7.5. Number of Backers

7.6. The Distribution of Types

7.7. Changing the Value of the Reward

7.8. Different Types of Crowdfunding

7.9. Risk-Averse Entrepreneurs

8. Conclusions

Funding

Conflicts of Interest

Appendix A

Appendix A.1. Proof of Proposition 2

Appendix A.2. Pooling Equilibrium Analysis

Appendix A.3. Proof of Proposition 4

Appendix A.4. Cournot Duopoly with Cost

References

- Agrawal, Ajay, Christian Catalini, and Avi Goldfarb. 2015. Crowdfunding: Geography, Social Networks, and the Timing of Investment Decisions (Summer 2015). Journal of Economics & Management Strategy 24: 253–74. [Google Scholar] [CrossRef] [Green Version]

- Ahlers, Gerrit K. C., Douglas J. Cumming, Christina Guenther, and Denis Schweizer. 2015. Signaling in Equity Crowdfunding. Entrepreneurship Theory and Practice 39: 955–80. [Google Scholar] [CrossRef]

- Alegre, Ines, and Melina Moleskis. Crowdfunding: A Review and Research Agenda (October 7, 2016). Working Paper. Available online: http://dx.doi.org/10.2139/ssrn.2900921 (accessed on 22 February 2020).

- Ahlstrom, David, Douglas Cumming, and Silvio Vismara. 2018. New methods of entrepreneurial firm financing: Fintech, crowdfunding and corporate governance implications. Corporate Governance: An International Review 26: 310–13. [Google Scholar] [CrossRef]

- Allaz, Blaise. 1992. Oligopoly, Uncertainty and Strategic Forward Transactions. International Journal of Industrial Organization 10: 297–308. [Google Scholar] [CrossRef]

- Askew, Peter. 2016. Digital Farmers Market Aims to Disrupt the Duopoly by Directly Supporting Aussie Farmers. Available online: https://www.linkedin.com/pulse/digital-farmers-market-aims-disrupt-duopoly-directly-supporting (accessed on 22 February 2020).

- Beaulieu, Tanya, Suprateek Sarker, and Saonee Sarker. 2015. A Conceptual Framework for Understanding Crowdfunding. Communications of the Association for Information Systems 37: 1–31. [Google Scholar] [CrossRef]

- Belleflamme, Paul, Thomas Lambert, and Armin Schwienbacher. 2014. Crowdfunding: Tapping the Right Crowd. Journal of Business Venturing: Entrepreneurship, Entrepreneurial Finance, Innovation and Regional Development 29: 585–609. [Google Scholar] [CrossRef] [Green Version]

- Belleflamme, Paul, Nessrine Omrani, and Martin Peitz. 2015. The Economics of Crowdfunding Platforms. Information Economics and Policy 33: 11–28. [Google Scholar] [CrossRef]

- Bolton, Patrick, and David Scharfstein. 1990. A Theory of Predation Based on Agency Problems in Financial Contracting. American Economic Review 80: 93–106. [Google Scholar]

- Brander, James, and Tracy Lewis. 1986. Oligopoly and Financial Structure: The Limited Liability Effect. American Economic Review 76: 956–70. [Google Scholar]

- Burtch, Gordon, Anindya Ghose, and Sunil Wattal. 2013. An empirical examination of the antecedents and consequences of contribution patterns in crowd-funded markets. Information Systems Research 24: 499–519. [Google Scholar] [CrossRef] [Green Version]

- Chakraborty, Soudipta, and Robert Swinney. 2019. Signalling to the Crowd: Private Quality Information and Rewards-Based Crowdfunding. Manufacturing and Service Operations Management Forthcoming. Available online: http://dx.doi.org/10.2139/ssrn.2885457 (accessed on 22 February 2020).

- Chaney, Damien. 2019. A principal–agent perspective on consumer co-production: Crowdfunding and the redefinition of consumer power. Technological Forecasting and Social Change 141: 74–84. [Google Scholar] [CrossRef]

- Chang, Jen-Wen. 2016. The Economics of Crowdfunding (August 30, 2016). Available online: https://ssrn.com/abstract=2827354 (accessed on 22 February 2020).

- Chemla, Gilles, and Katrin Tinn. 2019. Learning Through Crowdfunding. Management Science. Forthcoming. [Google Scholar] [CrossRef] [Green Version]

- Chen, Tianxu, Mark Tribbitt, Yi Yang, and Xiaomei Li. 2017. Does rivals’ innovation matter? A competitive dynamics perspective on firms’ product strategy. Journal of Business Research 76: 1–7. [Google Scholar] [CrossRef]

- Cho, In-Koo, and David Kreps. 1987. Signaling Games and Stable Equilibria. The Quarterly Journal of Economics 102: 179–221. [Google Scholar] [CrossRef]

- Cholakova, Magdalena, and Bart Clarysse. 2015. Does the Possibility to Make Equity Investments in Crowdfunding Projects Crowd Out Reward-Based Investments? Entrepreneurship Theory and Practice 39: 145–72. [Google Scholar] [CrossRef]

- Cordova, Alessandro, Johanna Dolci, and Gianfranco Gianfrate. 2015. The Determinants of Crowdfunding Success: Evidence from Technology Projects’. Procedia Social and Behavioral Sciences 181: 115–24. [Google Scholar] [CrossRef] [Green Version]

- Cumming, Douglas, and Lars Hornuf. 2018. The Economics of Crowdfunding Startups, Portals and Investor Behavior. London: Palgrave Macmillan. [Google Scholar] [CrossRef]

- Cumming, Douglas, and Sofia Johan. 2017. Crowdfunding and entrepreneurial internationalization. In The World Scientific Reference on Entrepreneurship. Singapore: The World Scientific Publishers, chp. 5. pp. 109–26. [Google Scholar] [CrossRef]

- Cumming, Douglas J., Gael Leboeuf, and Armin Schwienbacher. 2019. Crowdfunding Models: Keep-it-All versus All or Nothing. Financial Management. forthcoming. [Google Scholar] [CrossRef]

- Cunningham, Katelan. 2016. With $1.5M Success on Kickstarter, Hardware Startup Prynt Reinvents Photo Printing. Available online: http://thinkapps.com/blog/development/prynt-case-crowdfunded/ (accessed on 22 February 2020).

- Dixon, Huw David. 1992. The Competitive Outcome as the Equilibrium in an Edgeworthian Price-Quantity Model. The Economic Journal 102: 301–9. [Google Scholar] [CrossRef]

- Dixon, Huw David. 2001. Surfing Economics. Palgrave-MacMillan. Available online: https://www.amazon.co.uk/Surfing-Economics-Huw-David-Dixon/dp/033376062X (accessed on 22 February 2020).

- Dushnitsky, Gary, Massimiliano Guerini, Evila Piva, and Christina Rossi-Lamastra. 2016. Crowdfunding in Europe: Determinants of Platform Creation across Countries February. California Management Review 58: 44–71. [Google Scholar] [CrossRef]

- Dushnitsky, Gary, and Markus Fitza. 2018. Are We Missing the Platforms For the Crowd? Comparing Investment Drivers Across Multiple Crowdfunding Platforms. Journal of Business Venturing Insights 10: e00100. [Google Scholar] [CrossRef]

- Estrin, Saul, Daniel Gozman, and Susanna Khavul. 2018. The Evolution and Adoption of Equity Crowdfunding: Entrepreneur and Investor Entry into a New Market. Small Business Economics 51: 425–39. [Google Scholar] [CrossRef] [Green Version]

- Fairchild, Richard, Weixi Liu, and Yang Yao. 2017. An Entrepreneur’s Choice of Crowd-Funding or Venture Capital Financing: The Effect of Entrepreneurial Overconfidence and CF-Investors’ Passion. Working Paper. Available online: http://dx.doi.org/10.2139/ssrn.2926980 (accessed on 22 February 2020).

- Frydrych, Denis, Adam Bock, Tony Kinder, and Benjamin Koeck. 2014. Exploring entrepreneurial legitimacy in reward-based crowdfunding. Journal Venture Capital An International Journal of Entrepreneurial Finance 16: 247–69. [Google Scholar] [CrossRef]

- Fudenberg, Drew, and Jean Tirole. 1991. Game Theory. Cambridge: MIT Press, Available online: https://mitpress.mit.edu/books/game-theory (accessed on 22 February 2020).

- Gambardella, Massimiliano. 2012. How to (crowd-) fund and manage the (user-) innovation: The case of Big Buck Bunny. Paper presented at Workshop on Open Source and Design of Communication, Lisboa, Portugal, June 11. [Google Scholar]

- Gerber, Elizabeth, Julie Hui, and Pei-Yi Kuo. 2012. Crowdfunding: Why People are Motivated to Post and Fund Projects on Crowdfunding Platforms. Conference: Computer Supported Cooperative Work 2012. Available online: https://pdfs.semanticscholar.org/c1e2/a1068f0af1c3120c62be5943340518860ecb.pdf (accessed on 22 February 2020).

- Gleasure, Rob, and Joseph Feller. 2016. Emerging technologies and the democratisation of financial services: A metatriangulation of crowdfunding research. Information and Organization 26: 101–15. [Google Scholar] [CrossRef]

- Gleasure, Rob. 2015. Resistance to crowdfunding among entrepreneurs: An impression management perspective. The Journal of Strategic Information Systems 224: 219–33. [Google Scholar] [CrossRef]

- Greenberg, Michael, and Elizabeth Gerber. 2014. Learning to Fail: Experiencing Public Failure Online Through Crowdfunding. Paper presented at Conference Proceedings, 32nd Annual ACM Conference on Human Factors in Computing Systems, Toronto, ON, Canada, April 26–May 1. [Google Scholar]

- Harris, Milton, and Artur Raviv. 1991. The Theory of Capital Structure. The Journal of Finance 46: 297–355. [Google Scholar] [CrossRef]

- Hesse, Brendan. 2019. The Best Mobile Printers for Your Smartphone, Business Insider. Available online: https://www.businessinsider.com/best-mobile-printer?r=US&IR=T#the-best-for-printing-in-multiple-sizes-5 (accessed on 22 February 2020).

- Hildebrand, Thomas, Manju Puri, and Jörg Rocholl. 2016. Adverse Incentives in Crowdfunding. Management Science 63: 587–608. [Google Scholar] [CrossRef] [Green Version]

- Hughes, John S., and Jennifer L. Kao. 1997. Strategic Forward Contracting and Observability. International Journal of Industrial Organization 16: 121–33. [Google Scholar] [CrossRef]

- Jeitschko, Thomas, Ting Liu, and Tao Wang. 2016. Information Acquisition, Signaling and Learning in Duopoly. Working Papers from Stony Brook University, Department of Economics. Available online: https://ideas.repec.org/p/nys/sunysb/16-07.html (accessed on 22 February 2020).

- Kgoroeadira, Reabetswe, Andrew Burke, and André van Stel. 2019. Small Business Online Loan Crowdfunding: Who Gets Funded and What Determines the Rate of Interest? Small Business Economics 52: 67–87. [Google Scholar] [CrossRef]

- Kleinert, Simon, Christine Volkmann, and Marc Grunhagen. 2020. Third-party Signals in Equity Crowdfunding: The Role of Prior Financing. Small Business Economics 54: 341–65. [Google Scholar] [CrossRef]

- Kumar, Praveen, Nisan Landberg, and David Zvilichovsky. 2015. (Crowd)funding Innovation. Working Paper. Available online: https://www.aeaweb.org/conference/2016/retrieve.php?pdfid=661 (accessed on 22 February 2020).

- Kuo, Pei-Yi, and Elizabeth Gerber. 2012. Design principles: Crowdfunding as a creativity support tool. Paper presented at 2012 ACM Annual Conference on Human Factors in Computing Systems, Austin, TX, USA, May 5–10. [Google Scholar]

- Kuppuswamy, Venkat, and Barry Bayus. 2015. A Review of Crowdfunding Research and Findings. Handbook of New Product Development Research. Working Paper. Available online: http://dx.doi.org/10.2139/ssrn.2685739 (accessed on 22 February 2020).

- Leland, Hayne, and David Pyle. 1977. Information Asymmetries, Financial Structure, and Financial Intermediation. Journal of Finance 32: 371–87. [Google Scholar] [CrossRef]

- Lenz, Rainer. 2016. Peer-to-Peer Lending—Opportunities and Risks. European Journal of Risk and Regulation 7: 688–700. [Google Scholar] [CrossRef]

- Li, Li, and Zixuan Wang. 2019. How does capital structure change product-market competitiveness? Evidence from Chinese firms. PLoS ONE 14: 1–14. [Google Scholar] [CrossRef] [PubMed]

- Llopis, Juan A. Sanchis, José María Millán, Rui Baptista, Andrew Burke, Simon Parker, and Roy Thurik. 2015. Good Times, Bad Times: Entrepreneurship and the Business Cycle. International Entrepreneurship and Management Journal 11: 243–51. [Google Scholar] [CrossRef] [Green Version]

- Lubit, Roy. 2001. Tacit Knowledge and Knowledge Management: The Keys to Sustainable Competitive Advantage. Organizational Dynamics 29. [Google Scholar] [CrossRef]

- Miglo, Anton. 2018. Crowdfunding in a Duopoly Under Asymmetric Information. Working Paper. Available online: https://mpra.ub.uni-muenchen.de/89016/1/MPRA_paper_89016.pdf (accessed on 22 February 2020).

- Miglo, Anton. 2020. Crowdfunding Under Market Feedback, Asymmetric Information And Overconfident Entrepreneur. Entrepreneurship Research Journal. Forthcoming. Available online: https://mpra.ub.uni-muenchen.de/89015/1/MPRA_paper_89015.pdf (accessed on 22 February 2020).

- Miglo, Anton, and Victor Miglo. 2019. Market Imperfections and Crowdfunding. Small Business Economics Journal 53: 51–79. [Google Scholar] [CrossRef] [Green Version]

- Mochkabadi, Kazem, and Christine Volkmann. 2018. Equity Crowdfunding: A Systematic Review of the Literature. Small Business Economics. forthcoming. [Google Scholar] [CrossRef]

- Modigliani, Franco, and Merton Miller. 1958. The Cost of Capital, Corporation Finance And the Theory of Investment. American Economic Review 48: 261–97. [Google Scholar]

- Mogg, Trevor. 2017. Indiegogo Now Offers a Marketplace Where You Can Buy Its Coolest Stuff. Available online: https://www.digitaltrends.com/cool-tech/indiegogo-marketplace-online-store/ (accessed on 22 February 2020).

- Mollick, Ethan R. 2014. The Dynamics of Crowdfunding: An Exploratory Study. Journal of Business Venturing 29: 1–16. [Google Scholar] [CrossRef] [Green Version]

- Moritz, Alexandra, and Joern Hendrich Block. 2014. Crowdfunding: A Literature Review and Research Directions. Available online: http://ssrn.com/abstract=2554444 (accessed on 22 February 2020).

- Nachman, David, and Thomas Noe. 1994. Optimal Design of Securites under Asymmectric Information. Review of Financial Studies 7: 1–44. [Google Scholar] [CrossRef]

- Petruzzelli, Messeni, Angelo Natalicchio, Umberto Panniello, and Paolo Roma. 2019. Understanding the Crowdfunding Phenomenon and Its Implications for Sustainability. Technological Forecasting & Social Change 141: 138–48. [Google Scholar] [CrossRef]

- Rampini, Adriano. 2004. Entrepreneurial Activity, Risk, and the Business Cycle. Journal of Monetary Economics 51: 555–73. [Google Scholar] [CrossRef] [Green Version]

- Rear, Jack. 2018. Indiegogo’s New Marketplace Wants to Help Crowdfunders Stand Out. Available online: https://www.verdict.co.uk/indiegogo-marketplace/ (accessed on 22 February 2020).

- Santos, Vasco. 2017. The Economics of Crowdfunding: Surplus Appropriation, and Allocative Efficiency’. Working Paper. Available online: https://editorialexpress.com/cgi-bin/conference/download.cgi?db_name=EEAESEM2017&paper_id=2396 (accessed on 22 February 2020).

- Schiavone, Francesco. 2017. Incompetence and Managerial Problems Delaying Reward Delivery in Crowdfunding. Journal of Innovation Economics & Management 2: 185–207. [Google Scholar] [CrossRef]

- Schleifer, Theodore. 2017. Crowdfunding Site Indiegogo Will Now Let You Sell Products as It Shifts into Commerce. Available online: https://www.vox.com/2017/10/16/16474794/indiegogo-crowdfunding-commerce-amazon (accessed on 22 February 2020).

- Schwartz, Andrew. 2015. The Nonfinancial Returns of Crowdfunding. Review of Banking and Financial Law 34: 565–80. [Google Scholar]

- Singer, L., N. Seyff, and S. Fricker. 2011. Online social networks as a catalyst for software and IT innovation. Paper presented at 4th International Workshop on Social Software Engineering, Szeged, Hungary, September 5. [Google Scholar] [CrossRef] [Green Version]

- Smith, Craig. 2020. 15 Interesting Indiegogo Facts and Statistics (2020): By the Numbers. Available online: https://expandedramblings.com/index.php/indiegogo-facts-statistics/ (accessed on 22 February 2020).

- Strausz, Roland. 2017. Crowdfunding, Demand Uncertainty, and Moral Hazard—A Mechanism Design Approach. American Economic Review 107: 1430–76. [Google Scholar] [CrossRef] [Green Version]

- Sung-Min, Park. 2012. New business applications for social networking. SERI Quarterly 5: 121–25. [Google Scholar]

- Takahashi, Dean. 2018. Indiegogo Moves Beyond Crowdfunding to Help Startups with Manufacturing. Available online: https://venturebeat.com/2018/01/15/indiegogo-moves-beyond-crowdfunding-to-help-startups-with-manufacturing/ (accessed on 22 February 2020).

- Villot, Michel. 2011. Entrepreneurship and the Role of Risk: A Theoretical and Empirical Analysis of the Relationship between Entrepreneurship and Risk and the Differences Bet. Economics. Available online: http://hdl.handle.net/2105/9815 (accessed on 22 February 2020).

- Vismara, Silvio. 2016. Equity Retention and Social Network Theory in Equity Crowdfunding. Small Business Economics 46: 579–90. [Google Scholar] [CrossRef]

- Vismara, Silvio. 2018a. Information Cascades Among Investors in Equity Crowdfunding. Entrepreneurship Theory and Practice 42: 467–97. [Google Scholar] [CrossRef]

- Vismara, Silvio. 2018b. Signaling to Overcome Inefficiencies in Crowdfunding Markets. In The Economics of Crowdfunding. Amsterdam: Elsevier. [Google Scholar] [CrossRef]

- Vulkan, Nir, Thomas Åstebro, and Manuel Fernandez Sierra. 2016. Equity Crowdfunding: A new Phenomena. Journal of Business Venturing Insights 5: 37–49. [Google Scholar] [CrossRef]

- Wang, Yu-Lin, and Andrea Ellinger. 2011. Organizational Learning: Perception of External Environment and Innovation Performance. International Journal of Manpower 32: 512–36. [Google Scholar] [CrossRef]

- Williams, Joseph. 1995. Financial and industrial structure with agency. The Review of Financial Studies 8: 431–475. [Google Scholar] [CrossRef]

- Zvilichovsky, David, Yael Inbar, and Ohad Barzilay. 2013. Playing Both Sides of the Market: Success and Reciprocity on Crowdfunding Platforms. Economics, Computer Science. SSRN Electronic Journal 4. [Google Scholar] [CrossRef] [Green Version]

| 1 | Other types are equity-based crowdfunding, debt-based crowdfunding and donation-based crowdfunding. We will discuss them in Section 7 |

| 2 | https://www.kickstarter.com/help/stats, retrieved 08/02/2020. |

| 3 | |

| 4 | |

| 5 | |

| 6 | |

| 7 | |

| 8 | |

| 9 | |

| 10 | The fact that the crowdfunding decision is well observed publicly, given the nature of crowdfunding where firms use public websites (platforms) to conduct crowdfunding campaigns, makes crowdfunding different from other pre-sale methods such as forward sales for example. Although there is literature that argues that the disclosure of these contracts is desirable (see, among others, Hughes and Kao (1997) and Allaz (1992)), this issue remains quite ambiguous. As another example note that the development of a product within a private company that uses private financing is not as transparent as it would be with crowdfunding etc. |

| 11 | |

| 12 | |

| 13 | It may include discounts on the firm’s products/services, early access to some of its services, exclusive access to some services etc. Also note that as was mentioned previosuly there exists two types of reward-based crowdfunding: AON and KIA. We focus on KIA. In Section 7 we provide some comments about how the difference between AON and KIA can affect the model’s results, |

| 14 | For simplicity, production costs are not considered. In Section 7 and Appendix A.4, we argue that it does not affect the model’s results. |

| 15 | Note that (9) implies that should be relatively low (i.e., ). If it is not, a corner (“uninteresting”) solution arises where crowdfunding is not used at all. Throuought the article we mostly assume that this condition holds. |

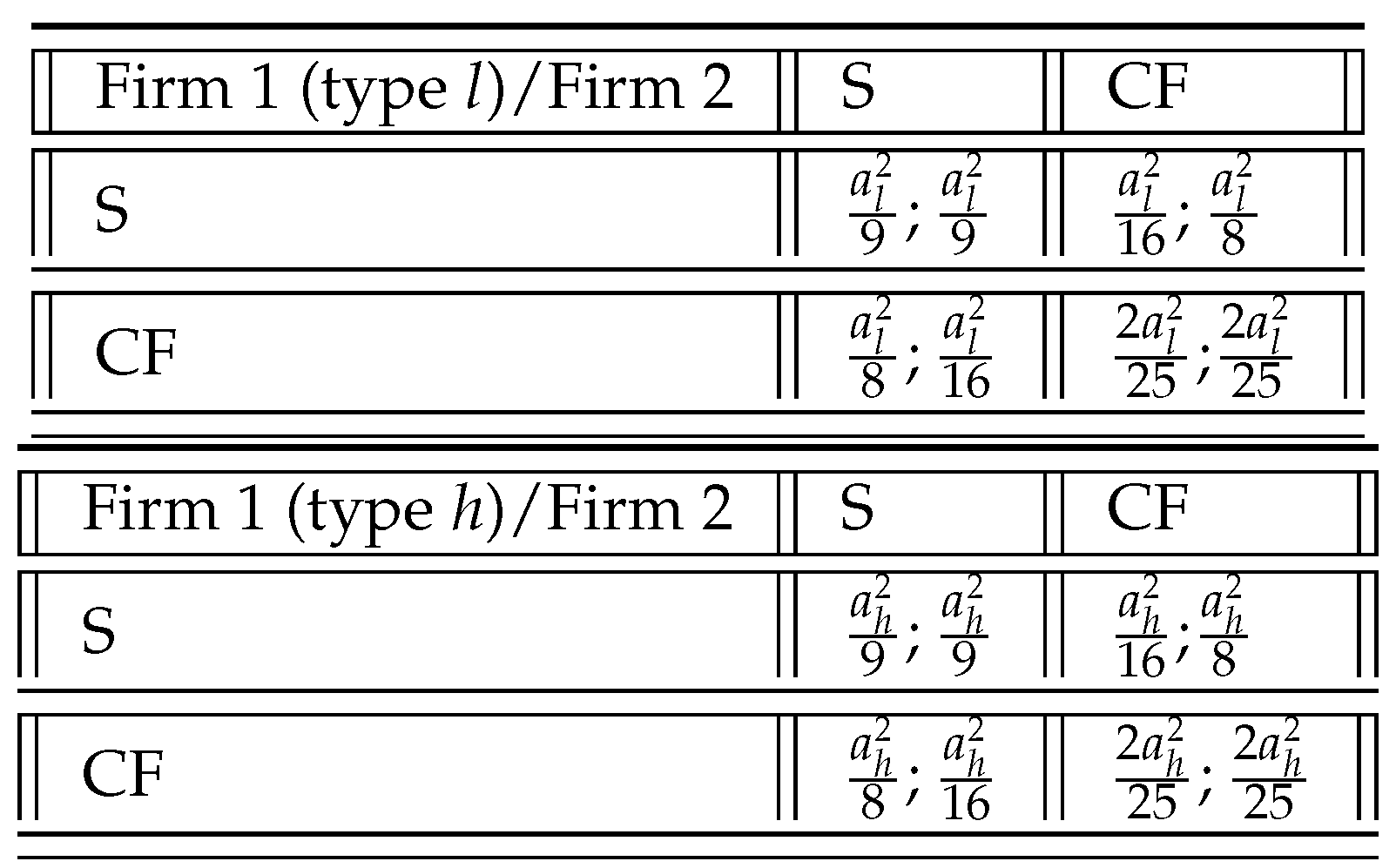

| 16 | It follows from Figure 1 that the equilibrium may be Pareto-inefficient. Indeed Pareto-efficiency of (CF,CF) depends on the following: . If this holds, (CF,CF) is Pareto-efficient and vice versa. This can be written as . This does not hold because . |

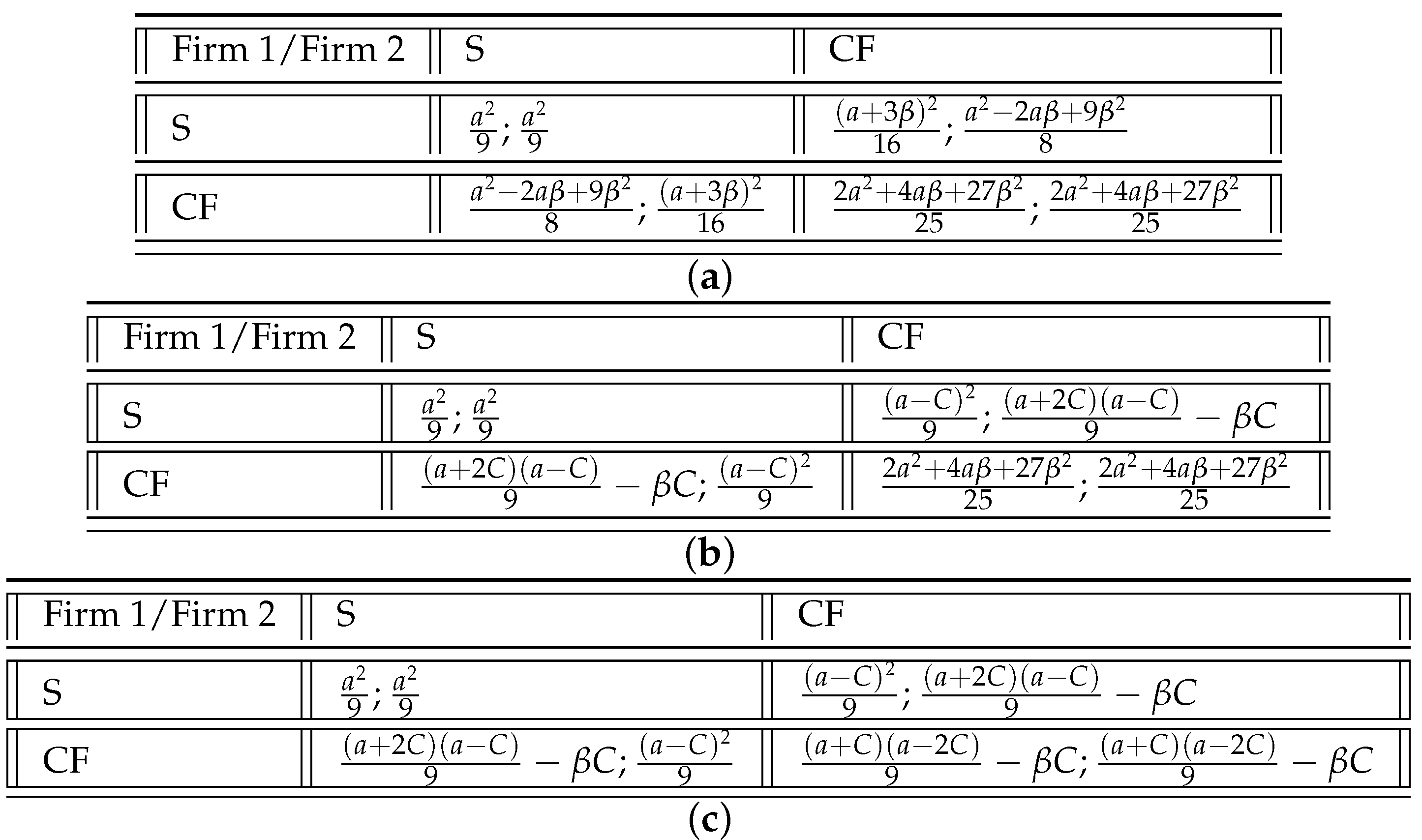

| 17 | (11) applies to the case where Firm 1 plays CF and Firm 2 plays S. Here it is an opposite case. |

| 18 | In order for this equilibrium to exist the following should hold: (see Appendix A.2). This implies that (26) decreases in because it’s derivative with respect to equals . |

| 19 | As follows from (33) and (36), f should be less than in order to avoid a corner solution where crowdfunding is not used at all. In practice, f is usually in the range of 3%-15%. See, for example, https://www.thebalancesmb.com/entrepreneurs-guide-to-fees-on-crowdfunding-platforms-985187 |

| 20 | |

| 21 | The calculations are very similar to Section 5 so they are omitted for brevity. |

| 22 | |

| 23 | Proofs are omitted for brevity. Note that the calculations become much longer and technically more complicated, which is very typical for multiple type games with asymmetric information. |

| 24 | For a literature on equity-based crowdfunding see, for example, Vulkan et al. (2016); Vismara (2016); Estrin et al. (2018); Mochkabadi and Volkmann (2018); Kleinert et al. (2020) or Miglo (2020). For debt-based crowdfunding see, for example, Kuo and Gerber (2012); Lenz (2016) and Kgoroeadira et al. (2019). |

| 25 | |

| 26 | |

| 27 | In a similar spirit, to some extent, Dushnitsky and Fitza (2018) suggest that crowdfunding research should focus more on comparing different crowdfunding platforms and respectively on analyzing competition between platforms. |

| 28 | The formal proof is omitted for brevity. |

| 29 | Intuitively, it is because Firm 2 is more aggressive when it believes that the type is h (high demand). In this case it increases sales which ultimately reduces its competitor’s profit. It makes any deviations by Firm 1 less attractive. |

| 30 | Full calculations are very similar to Section 4 so they are omitted for brevity. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Description |

|---|---|

| a | parameter in the demand function |

| parameter in the demand function for the level of demand | |

| in a model with demand uncertainty | |

| probability that demand is high | |

| c | crowdfunding pre-sales |

| crowdfunding pre-sales for firm in the model | |

| with two firms | |

| benefits for backers | |

| s | spot sales |

| spot sales for firm in the model | |

| with two firms | |

| q | quantity produced, |

| quantity produced for firm in the model | |

| with two firms | |

| p | spot price |

| crowdfunding price | |

| f | platform fee per unit sold |

| F | platform up-front fee |

| firm profit | |

| firm j profit in the model with two firms, | |

| C | maximal number of backers in crowdfunding stage |

| B | the cost of crowdfunding campaign failure |

| probability of campaign success |

| The Model’s Predictions |

|---|

| Competition increases the chances of using crowdfunding compared to the monopoly case |

| Firms can use crowdfunding strategically to signal a high level of demand for their products |

| The likelihood of crowdfunding increases with demand uncertainty |

| Higher cost of waiting/rate of discounting decreases the likelihood of crowdfunding |

| Higher platform fee (per value) may lead to higher firm profits in equilibrium |

| The amount of (reward-based) crowdfunding is pro-cyclical |

| A non-monotonic relationship exists between the risk of crowdfunding campaign failure and firm profit |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Miglo, A. Crowdfunding in a Competitive Environment. J. Risk Financial Manag. 2020, 13, 39. https://doi.org/10.3390/jrfm13030039

Miglo A. Crowdfunding in a Competitive Environment. Journal of Risk and Financial Management. 2020; 13(3):39. https://doi.org/10.3390/jrfm13030039

Chicago/Turabian StyleMiglo, Anton. 2020. "Crowdfunding in a Competitive Environment" Journal of Risk and Financial Management 13, no. 3: 39. https://doi.org/10.3390/jrfm13030039

APA StyleMiglo, A. (2020). Crowdfunding in a Competitive Environment. Journal of Risk and Financial Management, 13(3), 39. https://doi.org/10.3390/jrfm13030039