1. Introduction

Bankruptcy and bankruptcy prediction is a very real issue worldwide both in academic research and in practice considering the evolution at a global level: the upward trend in business insolvencies continued in 2018 (increase by 10% in 2018 compared to 2017), mainly due to the surge in China by 60% and, to a lesser extent, an increase in Western Europe by 2% (

Euler Hermes 2019).

In Western Europe, although a downside trend in insolvencies was recorded from 2014 to 2017, the increase mentioned by 2% in 2018 compared to 2017 was determined by different evolution by other countries: a noticeable upturn of 12% in the UK due to the Brexit-related uncertainties that added headwinds on businesses; a stabilization of insolvencies can be seen in France, Spain and Belgium, although in France in 2018, 54,751 companies went bankrupt, corresponding to a fairly high 1.3% of the active business universe (

Dun and Bradstreet 2019); an increase in the Nordic countries of 10% in Sweden, 3% in Norway, 19% in Finland and 25% in Denmark. This trend comes from economic and fiscal reasons or exceptional factors, especially for Denmark and Finland. At the same time, other countries of the region registered slower declines in 2018 compared to 2017, notably the Netherlands (from −23% to −6%), Portugal (−12%), Ireland (−10%) and Germany (−4%). In Italy, 11,207 companies filed for bankruptcy in 2018, down by a significant 5.8%, but the newly-elected populist government is likely to embark on a series of populist policies that are at odds with improving the country’s operating environment (

Dun and Bradstreet 2019).

According to

Euler Hermes (

2019), in Central and Eastern Europe, we can see economies that forecast to moderate in line with the slowdown in the Eurozone, but remain robust enough to see another decrease in insolvencies, albeit at more limited time, i.e., Hungary from −18% in 2018 to −11% in 2019 and the Czech Republic, respectively −17% and −10%. Romania registered a rebound in insolvencies, −3% in 2018 and +3% in 2019. Other countries continued to rise in insolvencies: 3% for Bulgaria in 2019 where the changes in the Insolvency law done in 2017 kept on boosting the bankruptcies of sole proprietorships, Slovakia of 16%, Poland of 5% where businesses have a structural problem of profitability and will face a noticeable deceleration of the economy.

Over time, researchers have tried to find diverse methods to estimate business failure: patrimonial method based on net working capital and treasury; financial ratios method especially based on individual analysis of profitability, liquidity, solvency and financial autonomy; and score method highlighted in numerous models for which

Altman (

1968),

Ohlson (

1980), and

Zmijewski (

1984) models are the most cited ones and that are based on accounting variables (

Avenhuis 2013). These bankruptcy prediction models use different explanatory variables and statistical techniques and may provide valuable information about the financial performance of the companies and their risks. More than that, we must mention that the predictive power of these bankruptcy prediction models differ between countries, sectors of activity, time periods, firms’ ages, or firms’ sizes.

There is a constant effort to use the models developed for firms in different economies, even if decision makers know or at least should know that assumptions used for fitting the original models are probably not valid anymore. There is a continuous concern and preoccupation for designing models for prediction risk of bankruptcy. Assessing of the level of advancement of bankruptcy prediction research in countries of the former Eastern Bloc, in comparison to the latest global research trends in this area,

Prusak (

2018) found that the most advanced research in this area is conducted in the Czech Republic, Poland, Slovakia, Estonia, Russia, and Hungary. In addition, the best world practices are reflected in the research provided in Poland, the Czech Republic, and Slovakia.

The main problem of the bankruptcy prediction models developed in the literature is that these models cannot be generalized because these were developed using a specific sample from a specific sector, specific time period and from a specific region or country. As the above-mentioned statistics show, there are many other specific factors that increase the bankruptcies in a country: changes in economic environments, law frameworks, incomparability of populations of interest, etc. (

Král’ et al. 2016). That is why it is necessary to adapt these models to the specificity of the sector, country or time period analyzed and to use combined techniques of estimation in designing these specific models.

In this paper, considering the context presented, the large companies from the European Union are analysed. The aim of this research is twofold: to improve the knowledge of bankruptcy prediction for European large companies and to analyse the predictive capacity of factor analysis, such as Principal Component Analysis (PCA) using as a basis the discriminant analysis (models for assessing bankruptcy risk, commonly used in the literature). Our paper is distinguishing from other studies by using a sample of large companies active in the EU-28 countries in the period 2006–2015 and by own original selection of bankruptcy prediction models (Altman, Conan and Holder, Tafler, Springate and Zmijewski) used in the PCA analysis.

The rest of the paper is organised as follows: in

Section 2, the literature review on risk, bankruptcy prediction, models and techniques used to assess and forecast the risk of bankruptcy is presented. The data and methodology are presented in the

Section 3. The paper then follows with analysis of results and discussions in

Section 4. Concluding remarks pointing out some policy implications, future research suggestions and limitations of the study are discussed in the

Section 5.

2. Literature Review

Financial risks show the possibility of losses arising from the failure to achieve financial objectives. The financial risks related to the financial operation of a business may take many different forms: market risks determined by the changes in commodities, stocks and other financial instruments prices, foreign exchange risks, interest rate risks, credit risks, financing risks, liquidity risks, cash flow risk, and bankruptcy risk. These financial risks are not necessarily independent of each other, the interdependence being recognized when managers are designing risk management systems (

Woods and Dowd 2008). The importance of these risks will vary from one firm to another, in function of the sector of activity of the firms, the firm size, development of international transactions, etc.

Bankruptcy refers to the situation in which the debtor company becomes unable to repay its debts and can be considered to be the consequence of a company’s inability to survive market competition, reflected in terms of job losses, the destruction of assets, and in a low productivity (

Aleksanyan and Huiban 2016). The risk of bankruptcy or insolvency risk shows the possibility that a company will be unable to meet its debt obligations, respectively the probability of a company to go bankrupt in the next few years. Assessing of bankruptcy risk is important especially for investors in making equity or bond investment decisions, but also for managers in financial decision making of funding, investments and distribution policy. Failure prediction models are important tools also for bankers, rating agencies, and even distressed firms themselves (

Altman et al. 2017).

The essential information for executive financial decisions, but also for investors decisions are provided by financial statements. Thus, companies’ financial managers should develop the financial performance analysis and problem-solving skills (

Burns and Balvinsdottir 2005;

Scapens 2006), without limiting their duties in verifying accounting data (

Diakomihalis 2012) in order to maintain the firm attractive for investors. The image of financial performance of companies is affected by the estimation of its position in front of investors, creditors, and stakeholders (

Ryu and Jang 2004). For this estimation there are used many indicators that reflect the company’s position such as: net working capital, net treasury, liquidity, solvency, profitability, funding capacity, cash-flow, etc., or a mix between them, such as Z-scores.

In the literature of bankruptcy prediction, the models of

Altman (

1968),

Ohlson (

1980), and

Zmijewski (

1984) are the most cited ones that are based on accounting variables. These bankruptcy prediction models use different explanatory variables and statistical techniques. Therefore, the predictive power of these bankruptcy prediction models differs. However, when the original statistical techniques are used, the accuracy rates for the models of

Altman (

1968),

Ohlson (

1980), and

Zmijewski (

1984) are respectively 80.6%, 93.8%, and 95.3% (

Avenhuis 2013). Studying the efficacy of Altman’s z-score model in predicting bankruptcy of specialty retail firms doing business in contemporary times,

Chaitanya (

2005) found that all but two of the bankruptcies (94%) would have been accurately predicted.

Ashraf et al. (

2019) found that both models by

Altman (

1968) and

Zmijewski (

1984) are still valuable for predicting the financial distress of emerging markets and can be used by businessmen, financial specialists, administrators, and other concerned parties who are thinking about investing in an organization and/or want to enhance their organization performance.

Elviani et al. (

2020) studied the accuracy of the

Altman (

1968),

Ohlson (

1980),

Springate (

1978) and

Zmijewski (

1984) models in bankruptcy predicting trade sector companies in Indonesia using binary logistic regression. Their results proved that the most appropriate and accurate models in predicting bankruptcy of trade sector companies in Indonesia are the Springate and Altman models.

Related to methodologies used in creating bankruptcy risk models we can mention bankruptcy prediction models based on: statistical methodologies (Models of

Altman 1968,

2000,

2002;

Altman et al. 2017; Model of

Springate 1978; Model of

Conan and Holder 1979; Models of

Taffler 1982,

1983,

1984; Model of

Fulmer et al. 1984), stochastic methodologies (Model of

Ohlson 1980; Model of

Zmijewski 1984; Model of

Zavgren 1985;

Theodossiou 1991), and artificial intelligence methodologies (

Zhang et al. 1999;

Kim and Han 2003;

Shin et al. 2005;

Li and Sun 2011) and data envelopment analysis (DEA) methodologies (

Koh and Tan 1999;

Cielen et al. 2004;

Paradi et al. 2004;

Shetty et al. 2012;

Ouenniche and Tone 2017).

Aziz and Dar (

2006) reviewed 89 studies on the prediction of bankruptcy risk in the period 1968–2003 in order to carry out a critical analysis of the methodologies and empirical findings of the application of these models across 10 different countries (Finland, Norway, Sweden, Belgium, UK, Italy, Greece, USA, Korea and Australia). They found that the multi-variable models (Z-Score) and logit were most popular in the 89 papers studied.

The multitude of models created demonstrate an intense concern for bankruptcy prediction, considering also the evolution of number of bankruptcies in the world. However, the first bankruptcy models are still applied and provide important information. For example, Altman’s model was applied to Jordanian companies, non-financial service and industrial companies, for the years 1990–2006. The study shows that Altman’s model has an advantage in company bankruptcy prediction, with a 93.8% average predictive ability of the five years prior to the liquidation incident (

Alkhatib and Bzour 2011).

Chung et al. (

2008) also examined the insolvency predictive ability of different financial ratios for ten failed financial companies during 2006–2007 in New Zealand and found that, one year prior to failure, four of the five

Altman (

1968) ratios were superior to other financial ratios for predicting corporate bankruptcy. In other countries, such as Romania aggregate indexes of financial performance assessment for the building sector companies were created (

Bărbuţă-Mişu 2009;

Bărbuță-Mișu and Codreanu 2014) or well-known modes, such as the Conan and Holder model were adjusted to the specificity of Romanian companies (

Bărbuţă-Mişu and Stroe 2010). In studies about bankruptcy prediction, in Romania was preferred

Conan and Holder (

1979) model to evaluate the financial performance of the companies.

The majority of authors proposed models adapted to the specificity of the economies.

Brédart (

2014) developed an econometric forecasting model on United States companies using three simple and a few correlated and easily available financial ratios as explanatory variables and their results show a prediction accuracy of more than 80%.

Dakovic et al. (

2010) developed statistical models for bankruptcy prediction of Norwegian firms acting in the industry sector. They modelled the unobserved heterogeneity among different sectors through an industry-specific random factor in the generalized linear mixed model. The models developed are shown to outperform the model with Altman’s variables.

To solve the problem of bankruptcy prediction some statistical techniques such as regression analysis and logistic regression are used (

De 2014). These techniques usually are used for the company’s financial data to predict the financial state of company as healthy, distressed, high probability of bankruptcy. As we know,

Altman (

1968) used financial ratios and multiple discriminant analysis (MDA) to predict financially distressed companies. However, further, it was found that the usage of statistical techniques or MDA depends on the constraint as linear separability, multivariate normality and independence of predictive variables (

Ohlson 1980;

Karels and Prakash 1987). Thus, bankruptcy prediction problem can be solved using various other types of classifiers, such as neural network that compared to MDA, logistic regression and k-nearest neighbour method proved a higher performance. For instance,

Tam (

1991) found that the neural network performs better than other prediction techniques.

Otherwise,

Xu and Zhang (

2009) have investigated whether the bankruptcy of certain companies can be predicted using traditional measures, such as Altman’s Z-score,

Ohlson’s (

1980) O-score, and the option pricing theory-based distance-to-default, previously developed for the U.S. market, in order to find if these models are useful for the Japanese market. They have found that the predictive power is substantially enhanced when these measures are combined.

In addition,

Jouzbarkand et al. (

2013) compiled two models for the prediction of bankruptcy, related to the Iranian economic situation. Using the logistic regression method, they studied the

Ohlson (

1980) and

Shirata (

1995) models, examining and comparing the performance of these models. Their results show that models created are able to predict the bankruptcy. For classifying and ranking the companies, they used their business law to determine the bankrupt companies and a simple Q-Tobin to specify the solvent companies.

Discriminant analysis was the prevailing method, and the most important financial ratios came from the solvency category, with profitability ratios also being important (

Altman et al. 2017). The performance of five bankruptcy prediction models, such as

Altman (

1968),

Ohlson (

1980),

Zmijewski (

1984),

Shumway (

2001) and

Hillegeist et al. (

2004) was studied by

Wu et al. (

2010) building their own integrated model using a dataset for U.S.A. listed firms.

Wu et al. (

2010) found that

Shumway’s (

2001) model performed best,

Hillegeist et al.’s (

2004) model performed adequately,

Ohlson’s (

1980) and

Zmijewski’s (

1984) models performed adequately, but their performance deteriorated over time, while Altman’s Zscore performed poorly compared with all other four models analysed. However, the integrated model outperformed the other models by combining both accounting and market data, and firms’ characteristics.

The factor analysis is often used together with other methodologies, in order to improve bankruptcy prediction models (

Cultrera et al. 2017). Principal Component Analysis (PCA), the statistical procedure that uses an orthogonal transformation to convert a set of observations of possibly correlated variables into a set of values of linearly uncorrelated variables called principal components started to be used in analysis and prediction of bankruptcy risk.

Adalessossi (

2015) used discriminant function named Z-scores model of Altman, financial ratio analysis, and the principal component analysis on a sample of 34 listed companies from different sectors and sizes in order to find out if the three methods used in this study converge toward similarity results. The comparison of the three methods indicates unanimously that, out of the 34 companies, only eight companies have had the best financial performances and are not likely to go on to bankruptcy.

Onofrei and Lupu (

2014) have built a quick warning model for the Romanian companies in difficulty, using the following methodologies: the Principal Components Analysis, the multivariate discriminant analysis and the logit analysis in order to determine which are the best predictors of bankruptcy for the Romanian companies. They found that the best predictor for the Romanian market is the multiple discriminant analysis method with a predictive power between 68–95%, while the logit method registering slightly weaker results with a predictive power between 53–82%.

De (

2014) developed the principal component analysis (PCA) and general regression auto associative neural network (GRAANN) based hybrid as a one-class classifier in order to test the effectiveness of PCA-GRAANN on bankruptcy prediction datasets of banks from Spain, Turkey, US and UK. They concluded that PCA-GRAANN can be used as a viable alternative for any one-class classifier. Checking related literature, we found that PCA is more used with artificial neural network methods for prediction bankruptcy risk where the effectiveness was proved. However, in this paper we proposed to use PCA based on the five discriminant analysis measures, i.e., Z-score determined by the following models: revised Z-score Altman, Conan and Holder, Tafler, Springate and Zmijewski in order to test the efficiency in predicting the risk of bankruptcy. Afterwards, we made use of econometric techniques and the PCA score created by country and year to test its influence over performance. The principal component analysis to build the bankruptcy risk score of the five models selected is used, since there is no consensus in the literature so as to which is the best bankruptcy prediction model. In this way we may capture the components that will exert more impact in bankruptcy prediction.

4. Results and Discussion

As we presented in the

Section 3.1, in this study we used data from European large companies where insolvencies are more present.

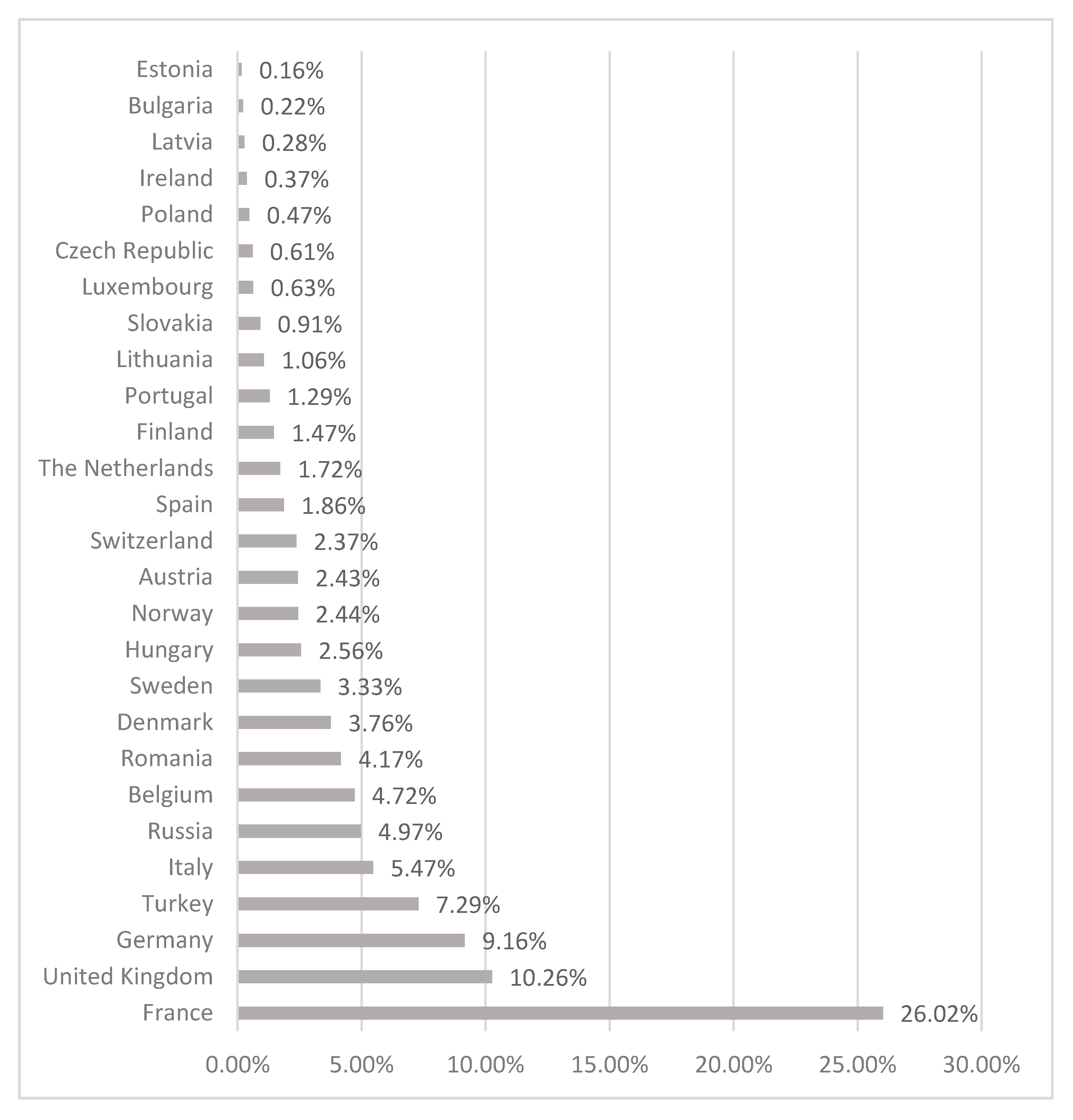

Figure 1 plots the frequency of corporate insolvencies in Europe by country for 2018 (

Euler Hermes 2019). We can see that the first place in the frequency of bankruptcies was occupied by France (with 26.02%) corresponding to 54,965 companies bankrupted, followed by United Kingdom with 10.26% frequency corresponding to 21,669 companies bankrupted and 9.16% to Germany with 19,350 companies bankrupted. In our sample we used a great part of these countries. As we are able to observe, among countries with a high number of corporate insolvencies were also Italy, Belgium, Romania, Denmark, Sweden, Hungary, Norway, and Austria. From the countries used in our sample, France, United Kingdom, Germany, Turkey, Italy, Belgium, Romania, Denmark and Sweden were in the top ten of the Frequency of corporate insolvencies in Europe in 2018 (

Figure 1).

Table 1 presents the number of companies from EU-28 countries included in the sample. We can observe that a high number of firm-year observations from large companies came from United Kingdom i.e., 28.60% of all observations analysed (also the country with the second number of bankruptcies), followed by Germany with 16.17%, Italy with 11.49%, France with 9.97% and Spain with 7.28%. Related to the number of firm-year observations of large companies by years, we can observe that the highest number of observations was in 2014 (18,513 companies) and 2013 (18,395 companies), respectively 12.02% and 11.94% of the sample analysed.

Table 2 presents the data descriptive statistics for the variables used for calculation of Z score for all five models used. In average, the companies from the sample show a need of exploitation capital of 14% by the total assets, an operational profitability of 6%, a rotation speed of assets 1.48 times per year, a current liquidity by 2.31 showing the capacity to pay debts by converting of assets in cash, the share of financial expenditure of 0.11% by sales, the share of personnel expenses of 69% in value added and a degree of debts of 64% by total assets. In addition, from

Table 2 it is visible the disparity of values of mean and standard deviation of the bankruptcy measures. Moreover, the different number of observations considered for both the creation of financial ratios as well as bankruptcy indicators of interest are clearly visible.

Table A1 and

Table A2 (at the

Appendix A) presents the correlation matrix among the variables used both to produce the bankruptcy risk indicators and the five bankruptcy risk scores. In addition,

Table A1 and

Table A2 presents the Pearson correlation values and statistical significance. From here it is seen that there are ratios used to produce the bankruptcy indicators which are highly correlated among them, significantly, with negative or positive correlation (i.e., strong positive significant correlation (0.821) between Book Value of Equity/Book Value of Total Debt and Current Assets/Total Liabilities; strong positive significant correlation (0.778) between Book Value of Equity/Book Value of Total Debt and (Current assets − Stocks)/Total Liabilities, almost perfect positive correlation (0.998) between EBIT/Current liabilities and Profit Before Tax/Current Liabilities etc.), but mostly have low to moderate correlation. However, between bankruptcy indicators constructed through discriminant analysis, correlation values are very low, and very close to zero with statistical significance.

Table 3 indicates that after applying PCA, the number of observations decreased as compared to

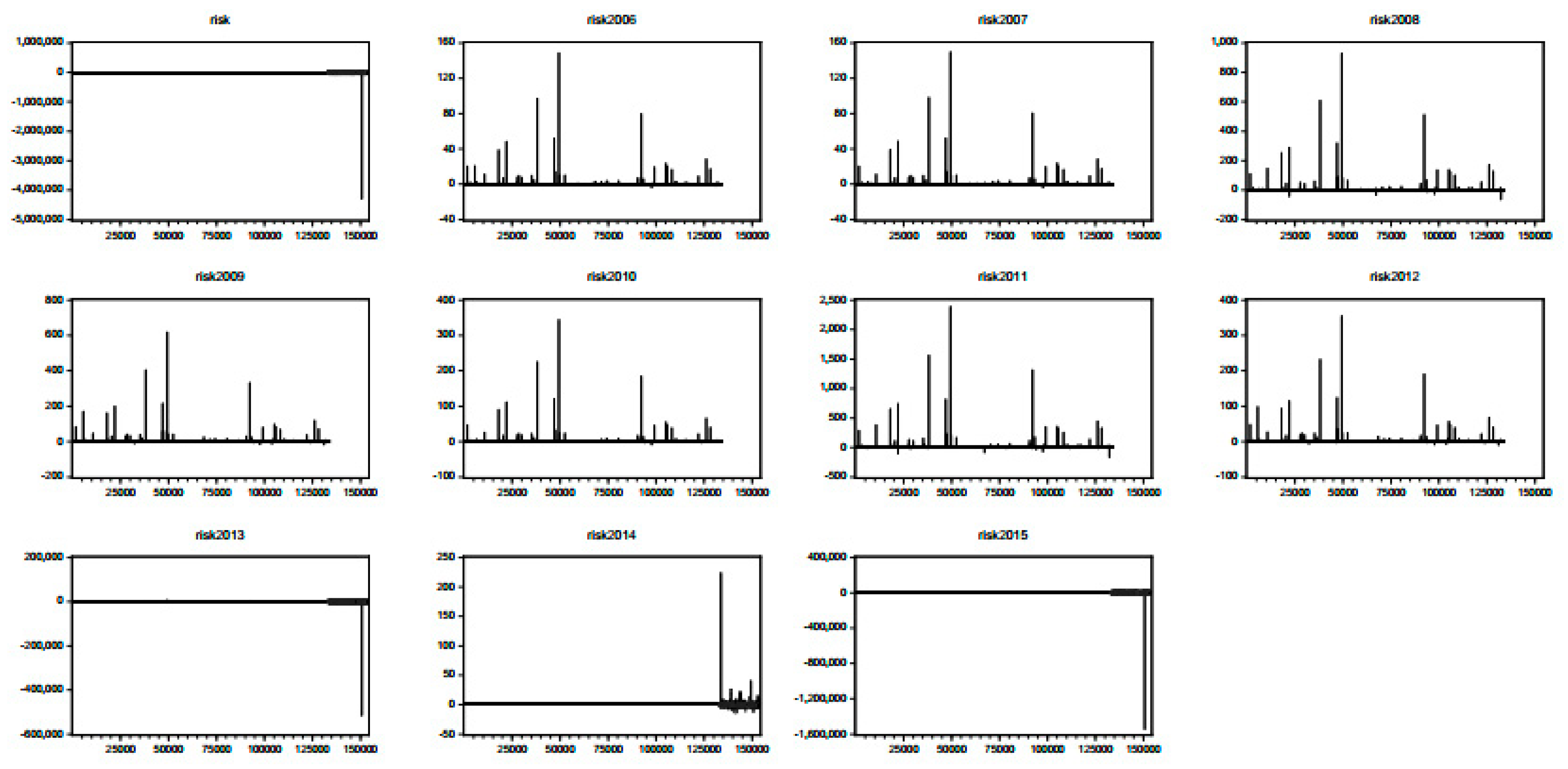

Table 2. In fact, by restricting the sample to all those values obtained for the general risk score greater than 3 or smaller than 3, our sample was reduced to 133,751 firm-year observations. Risk is the score computed through PCA considering all companies, years and countries.

Overall, countries presented higher mean scores as well as negative mean for some countries, and also standard deviation is higher for countries scores. A plot of year bankruptcy risk scores will allow us to see their behaviour along years.

Figure 2 presents these data evolution for countries. After the final data treatment, the total number of companies available to analyse by country and year are presented in

Table 4.

Correlation values (

Table 5) seem to be very strong among Austria and Spain, Croatia, Italy, the Netherlands, Poland and Sweden; strong (higher than 90% and positive; some near perfect linear positive correlation) between Belgium, Czech Republic, Germany, Finland, France, Great Britain, Hungary, Portugal, Romania, and Slovakia; Bulgaria and Ireland; Germany, Finland, France, Great Britain, Hungary, Portugal, Romania, and Slovakia; Spain, Croatia, Italy, the Netherlands, Poland, and Sweden; Finland, France, Great Britain, Hungary, Portugal, Romania, and Slovakia; between France, Great Britain, Hungary, Portugal, Romania and Slovakia; among Great Britain and Hungary, Portugal, Romania, and Slovakia; Croatia, Italy, the Netherlands, Poland, and Sweden; between Hungary, Portugal, Romania, and Slovakia; Italy, Poland, and Sweden; the Netherlands, Poland and Sweden; Between Poland and Sweden; Portugal, Romania, and Slovakia; and finally between Romania and Slovakia. As such, no clear pattern is identified regarding for instant the geographic distance among the countries, but high correlation values maybe due to commercial transactions performed among these countries.

Regarding year, whose correlation values are presented in

Table 6, the score Pearson correlation values were very high, near to one and positive. In the next we will be analysing the evolution plots of scores of bankruptcy risk by country and by year.

Figure 2 and

Figure 3 present these evolutions respectively.

Figure 2 plots the evolution of the score values obtained through PCA from the discriminant indices calculous by country. There are some countries which evidence a very similar behaviour like Belgium, Czech Republic, Finland, France, Great Britain, Hungary, Portugal, Romania, Slovakia and Germany. Another group of similar behaviour in terms of scores is that of Austria, Spain, Italy, Croatia, the Netherlands, Poland and Sweden. The two other similar countries in terms of scores are Ireland and Bulgaria.

Regarding years, the years 2006 until 2012 were very similar years in terms of score behaviour. As such, unstable values are more observed in these years with peaks and downs, which included all countries. In the following we decided to apply first a dynamic panel-data model by regressing the ratio EBIT over Total Assets in the bankruptcy scoring variables by year and a probit estimation considering as dependent variable risk and as independent variables firm performance measures.

Table 7 presents the estimation results of the panel-data model.

The dynamic panel data results indicate that the only score risk variables which have not been omitted due to collinearity issues were the risk measures for years 2014, 2013, 2011 and 2009. The years 2009 until 2011 are characterized by the financial crisis which has spread out through Europe, having a negative influence over firm performance as measured by the ratio of Earnings Before Interest and Taxes and Total Assets, but with significance only for the year 2009 at 5%.

Aleksanyan and Huiban (

2016) study confirm also the dramatic increase in bankruptcy risk in the French food industry observed over the period 2010–2012, highlighting that among food industry sub-sectors, the meat industry was primarily responsible for the evolution of bankruptcy risk in the period mentioned.

The years of 2013 and 2014 were years of starting recovery, and we might infer from the results that despite the negative influence of 2013 risk score over performance, in 2014 we already have a positive contribution of bankruptcy risk score over performance, both years with statistical significance at 5%.

Table 8 reports the Tobit estimation results for general risk among countries, while

Table 9 presents the same Tobit estimation results but this turn by country. This turn we are testing the influence of performance measures over risk scores since we are analysing the dependent censored variable risk.

Model significance was confirmed at 5% and results seem to indicate that performance measures positively influence risk scores. Thus the higher the performance is the higher will be the risk score and as such bankruptcy risk decreases with performance, a result which was expected. Bankruptcy is one of the most discussed topics in the literature, owing to its importance to the economy of any country. Bankruptcy costs are high and authors have tried to develop bankruptcy prediction models through years. Our scoring methodology through PCA applied to discriminant analysis of bankruptcy risk therefore indicates that performance is the solution to decrease this risk.

Discriminant analysis of bankruptcy risk argues that positive high values of bankruptcy risk positions companies in the safe zone, meaning a low risk of bankruptcy or a probability of bankruptcy lower than 30% (zcc index). Lower values positions firms between the grey zones or in the distress zone (see

Section 3.2). Therefore, we may argue that for our sample of firms, these large companies had good chances for performance provided their higher results, thus being non-bankrupt or with lower chances to become so. However, these results depended on the year of analysis provided that

Table 7 demonstrates that 2009, 2011 and 2013 were years of negative influence of bankruptcy risk scores over companies’ results.

Company performance variables were all statistically significant and with a positive impact over the bankruptcy risk score in Austria, Bulgaria, Spain, Finland, Great Britain, Croatia, Ireland, Italy, The Netherlands, Portugal, Romania, and Sweden. The ratio sales to total assets had a negative and non-significant impact over the risk score in Belgium, Czech Republic, Hungary and Slovakia. It is positive and non-significant in Poland and France. The only countries where performance (independently of its measure) did not seem to exert an influence over the bankruptcy risk score were Germany and Poland.

Since Germany is on the top ten of the number of corporate insolvencies, this might mean that other corporate variables despite the ones considered here to represent performance in our analysis, might be influencing bankruptcy risk scores under the years in analysis. The Principal Component Analysis here employed to build a bankruptcy risk scored based on discriminant analysis indices was found to be effective for determining the influence of corporate performance over risk. It was useful to understand that different countries evidence different results regarding this influence, as well as different risk scores with respect to years reveal to be different. It could be useful to understand this impact in the future by using other scoring techniques, like data envelopment analysis, or even by detailing years and countries analysis.

{kind=link}

{kind=link}

{kind=link}