EU Stock Markets vs. Germany, UK and US: Analysis of Dynamic Comovements Using Time-Varying DCCA Correlation Coefficients

Abstract

:1. Introduction and Literature Review

2. Methodology and Data

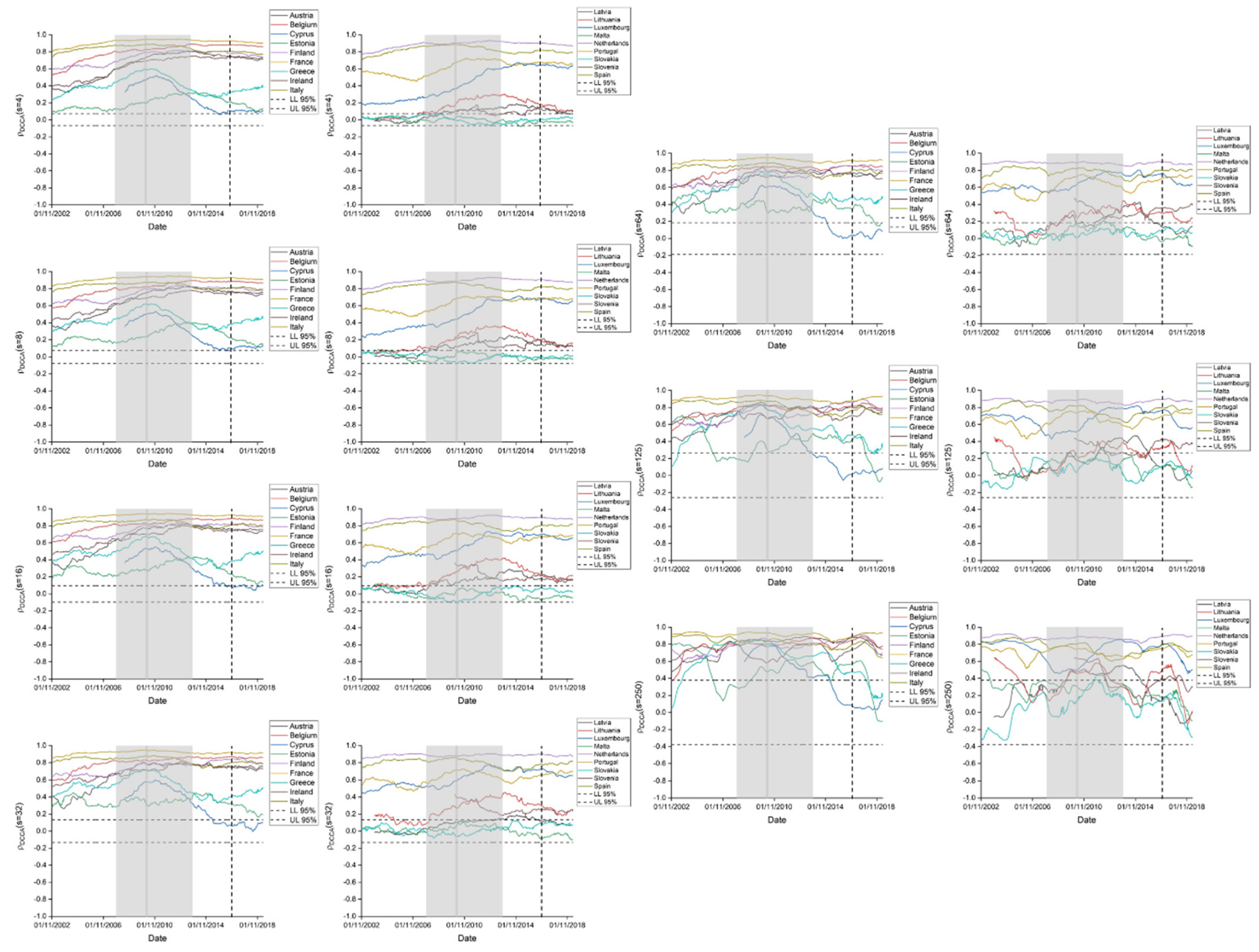

3. Results

3.1. Evolution of the DCCA Correlation Coefficients over Time

3.2. Dynamic Stock Market Comovements

4. Discussion and Concluding Remarks

Author Contributions

Funding

Conflicts of Interest

Appendix A

Appendix B

Appendix C

References

- Allegret, Jean-Pierre, Hélène Raimond, and Houda Rharrabti. 2017. The impact of the European sovereign debt crisis on banks stocks. Some evidence of shift contagion in Europe. Journal of Banking & Finance 74: 24–37. [Google Scholar]

- Ang, Andrew, and Geert Bekaert. 2002. International asset allocation with regime shifts. The Review of Financial Studies 15: 1137–87. [Google Scholar] [CrossRef]

- Ang, Andrew, and Joseph Chen. 2002. Asymmetric correlations of equity portfolios. Journal of Financial Economics 63: 443–94. [Google Scholar] [CrossRef]

- Apergis, Nicholas, Christina Christou, and Iason Kynigakis. 2019. Contagion across US and European financial markets: Evidence from the CDS markets. Journal of International Money and Finance 96: 1–12. [Google Scholar] [CrossRef]

- Ayub, Usman, Syed Zshah, and Qaisar Abbas. 2015. Robust analysis for downside risk in portfolio management for a volatile stock market. Economic Modelling 44: 86–96. [Google Scholar] [CrossRef]

- Bannigidadmath, Deepa, and Paresh Narayan. 2016. Stock return predictability and determinants of predictability profits. Emerging Markets Review 26: 153–73. [Google Scholar] [CrossRef]

- Beine, Michel, Antonio Cosma, and Robert Vermeulen. 2010. The dark side of global integration: Increasing tail dependence. Journal of Banking & Finance 34: 184–92. [Google Scholar]

- Bekaert, Geert, Campbell Harvey, and Christian Lundblad. 2005. Does financial liberalization spur growth? Journal of Financial Economics 77: 3–56. [Google Scholar] [CrossRef] [Green Version]

- Bekaert, Geert, Campbell Harvey, Christian Lundblad, and Stephan Siegel. 2013. The European Union, the Euro and equity market integration. Journal of Financial Economics 109: 583–603. [Google Scholar] [CrossRef] [Green Version]

- Bekaert, Geert, Michael Ehrmann, Marcel Fratzscher, and Arnaud Mehl. 2014. The Global Crisis and Equity Market Contagion. The Journal of Finance 69: 2597–649. [Google Scholar] [CrossRef] [Green Version]

- Berben, Robert-Paul, and Jos Jansen. 2005. Comovement in international equity markets: A sectoral view. Journal of International Money and Finance 24: 832–57. [Google Scholar] [CrossRef] [Green Version]

- Bertero, Elisabetta, and Colin Mayer. 1990. Structure and performance: Global interdependence of stock markets around the crash of October 1987. European Economic Review 34: 1150–80. [Google Scholar] [CrossRef]

- Burdekin, Richard, Eric Hughson, and Jinlin Gu. 2018. A first look at Brexit and global equity markets. Applied Economics Letters 25: 136–40. [Google Scholar] [CrossRef]

- Burzala, Milda. 2016. Contagion effects in selected European capital markets during the financial crisis of 2007–2009. Research in International Business and Finance 37: 556–71. [Google Scholar] [CrossRef]

- Cajueiro, Daniel, and Benjamin Tabak. 2004a. The Hurst exponent over time: Testing the assertion that emerging markets are becoming more efficient. Physica A 336: 521–37. [Google Scholar] [CrossRef]

- Cajueiro, Daniel, and Benjamin Tabak. 2004b. Evidence of long-range dependence in Asian equity markets: The role of liquidity and market restrictions. Physica A 342: 656–64. [Google Scholar] [CrossRef]

- Cajueiro, Daniel, and Benjamin Tabak. 2006. Testing for predictability in equity returns for European transition markets. Economic Systems 30: 56–78. [Google Scholar] [CrossRef]

- Cajueiro, Daniel, and Benjamin Tabak. 2008. Testing for time-varying long-range dependence in real estate equity returns. Chaos Solitons & Fractals 38: 293–307. [Google Scholar]

- Calvo, Sara, and Carmen Reinhart. 1996. Capital flows to Latin America: Is there evidence of contagion effects? In Private Capital Flows to Emerging Markets after the Mexican Crisis. Edited by Guillermo Calvo, Morris Goldstein and Eduard Hochreiter. Washington, DC: Institute for International Economics, pp. 151–71. [Google Scholar]

- da Silva, Marcus, Éder Pereira, Aloísio Filho, Arleys Castro, José Miranda, and Gilney Zebende. 2016. Quantifying the contagion effect of the 2008 financial crisis between the G7 countries (by GDP nominal). Physica A 453: 1–8. [Google Scholar] [CrossRef]

- Dajcman, Silvo, Merja Festic, and Alenka Kavkler. 2012. European stock market comovement dynamics during some major financial market turmoils in the period 1997 to 2010—A comparative DCC-GARCH and wavelet correlation analysis. Applied Economics Letters 19: 1249–56. [Google Scholar] [CrossRef]

- Dimitriou, Dimitrios, Dimitris Kenourgios, and Theodore Simos. 2013. Global financial crisis and emerging stock market contagion: A multivariate FIAPARCH–DCC approach. International Review of Financial Analysis 30: 46–56. [Google Scholar] [CrossRef]

- El Alaoui, Marwane, and Saâd Benbachir. 2013. Multifractal detrended cross-correlation analysis in the MENA area. Physica A 392: 5985–93. [Google Scholar] [CrossRef]

- Fama, Eugene. 1970. Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance 25: 383–417. [Google Scholar] [CrossRef]

- Ferreira, Paulo. 2017. Portuguese and Brazilian stock market integration: A non-linear and detrended approach. Portuguese Economic Journal 16: 49–63. [Google Scholar] [CrossRef] [Green Version]

- Ferreira, Paulo. 2018. Long-range dependencies of Eastern European stock markets: A dynamic detrended analysis. Physica A 505: 454–70. [Google Scholar] [CrossRef]

- Ferreira, Paulo, and Andreia Dionísio. 2015. Revisiting covered interest parity in the European Union: The DCCA approach. International Economic Journal 29: 597–615. [Google Scholar] [CrossRef] [Green Version]

- Ferreira, Paulo, Andreia Dionísio, and Gilney Zebende. 2016. Why does the Euro fail? The DCCA approach. Physica A 443: 543–54. [Google Scholar] [CrossRef]

- Forbes, Kristin, and Roberto Rigobon. 2002. No contagion, only interdependence: Measuring stock market co-movements. The Journal of Finance 57: 2223–61. [Google Scholar] [CrossRef]

- Fry-McKibbin, Renée, Vance L. Martin, and Chrismin Tang. 2014. Financial contagion and asset pricing. Journal of Banking & Finance 47: 296–308. [Google Scholar]

- Gabriel, Anton. 2012. Evaluating the Forecasting Performance of GARCH Models. Evidence from Romania. Procedia-Social and Behavioral Sciences 62: 1006–10. [Google Scholar] [CrossRef] [Green Version]

- Globan, Tomislav, and Petar Soric. 2017. Financial integration before and after the Crisis: Euler Equations (re)visit the European Union. Ekonomickýčasopis/Journal of Economics 65: 237–62. [Google Scholar]

- Grammatikos, Theoharry, and Robert Vermeulen. 2012. Transmission of the financial and sovereign debt crises to the EMU: Stock prices, CDS spreads and exchange rates. Journal of International Money and Finance 31: 517–33. [Google Scholar] [CrossRef]

- Guedes, Everaldo, Andréa Brito, Florêncio Filho, Basílio Fernandez, Arleys Castro, Aloísio Filho, and Gilney Zebende. 2018a. Statistical test for DCCA cross-correlation coefficient. Physica A 501: 134–40. [Google Scholar] [CrossRef]

- Guedes, Everaldo, Andreá Brito, Florêncio Filho, Basílio Fernandez, Arleys Castro, Aloísio Filho, and Gilney Zebende. 2018b. Statistical test for DCCA: Methods and data. Data Brief 18: 795–98. [Google Scholar] [CrossRef]

- Guedes, Everaldo, Paulo Ferreira, Andreia Dionísio, and Gilney Zebende. 2019. An econophysics approach to study the effect of BREXIT referendum on European Union stock markets. Physica A 523: 1175–82. [Google Scholar] [CrossRef]

- Horta, Paulo, Sérgio Lagoa, and Luís Martins. 2014. The impact of the 2008 and 2010 financial crises on the Hurst exponents of international stock markets: Implications for efficiency and contagion. International Review of Financial Analysis 35: 140–53. [Google Scholar] [CrossRef]

- Kearney, Colm, and Brian Lucey. 2004. International equity market integration: Theory, evidence and implications. International Review of Financial Analysis 13: 571–83. [Google Scholar] [CrossRef]

- Kristoufek, Ladislav. 2012. Fractal market hypothesis and the global financial crisis: Scaling, investment horizons and liquidity. Advances in Complex Systems 15: 1250065. [Google Scholar] [CrossRef] [Green Version]

- Kristoufek, Ladislav. 2014a. Measuring correlations between non-stationary series with DCCA coefficient. Physica A 402: 291–98. [Google Scholar] [CrossRef] [Green Version]

- Kristoufek, Ladislav. 2014b. Detrending moving-average cross-correlation coefficient: Measuring cross-correlations between non-stationary series. Physica A 406: 169–75. [Google Scholar] [CrossRef] [Green Version]

- Lyócsa, Štefan, Tomáš Výrost, and Eduard Baumöhl. 2019. Return spillovers around the globe: A network approach. Economic Modelling 77: 133–46. [Google Scholar] [CrossRef] [Green Version]

- Ma, Feng, Qian Zhang, Peng Chen, and Yu Wei. 2014. Multifractal detrended cross-correlation analysis of the oil-dependent economies: Evidence from the West Texas intermediate crude oil and the GCC stock markets. Physica A 410: 154–66. [Google Scholar] [CrossRef]

- Martin-Montoya, Ligia, Natali Aranda-Camacho, and Carlos Quimbay. 2015. Long-range correlations and trends in Colombian seismic time series. Physica A 421: 361–70. [Google Scholar] [CrossRef] [Green Version]

- Mohti, Wahbeeah, Andreia Dionísio, Isabel Vieira, and Paulo Ferreira. 2019. Financial contagion analysis in frontier markets: Evidence from the US subprime and the Eurozone debt crises. Physica A 525: 1388–98. [Google Scholar] [CrossRef]

- Morana, Claudio, and Andrea Beltratti. 2008. Comovements in international stock markets. Journal of International Financial Markets, Institutions and Money 18: 31–45. [Google Scholar] [CrossRef]

- Narayan, Paresh, and Susan Sharma. 2015. Does data frequency matter for the impact of forward premium on spot exchange rate? International Review of Financial Analysis 39: 45–53. [Google Scholar] [CrossRef]

- Niţoi, Mihai, and Maria Pochea. 2019. What drives European Union stock market co-movements? Journal of International Money and Finance 97: 57–69. [Google Scholar] [CrossRef]

- Niţoi, Mihai, and Maria Pochea. 2020. Time-varying dependence in European equity markets: A contagion and investor sentiment driven analysis. Economic Modelling 86: 133–47. [Google Scholar] [CrossRef]

- Obstfeld, Maurice. 1994. Risk-taking, global diversification, and growth. The American Economic Review 84: 1310–29. [Google Scholar]

- Papadamou, Stephanos, Nikolaos Kyriazis, and Panayiotis Tzeremes. 2019a. Unconventional monetary policy effects on output and inflation: A meta-analysis. International Review of Financial Analysis 61: 295–305. [Google Scholar] [CrossRef]

- Papadamou, Stephanos, Nikolaos Kyriazis, and Panayiotis Tzeremes. 2019b. US non-linear causal effects on global equity indices in normal times versus unconventional eras. International Economics and Economic Policy, 1–27. [Google Scholar] [CrossRef]

- Papadamou, Stephanos, Costas Siriopoulos, and Nikolaos Kyriazis. 2020. A survey of empirical findings on unconventional central bank policies. Journal of Economic Studies. [Google Scholar] [CrossRef]

- Peng, Chung-Kang, Sergey Buldyrev, Shlomo Havlin, Michael Simons, Harry Eugene Stanley, and Ary Goldberger. 1994. Mosaic organization of DNA nucleotides. Physical Review E 49: 1685–89. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Peters, Edgar. 1994. Fractal Market Analysis-Applying Chaos Theory to Investment and Economics. New York: John Wiley & Sons, Inc. [Google Scholar]

- Phylaktis, Kate, and Lichuan Xia. 2009. Equity market comovement and contagion: A sectoral perspective. Financial Management 38: 381–409. [Google Scholar] [CrossRef]

- Podobnik, Boris, and Harry Stanley. 2008. Detrended cross-correlation analysis: A new method for analysing two non-stationary time series. Physical Review Letters 100: 084102. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Podobnik, Boris, Zhi-Qiang Jiang, Wei-Xing Zhou, and Harry Eugene Stanley. 2011. Statistical tests for power-law cross-correlated processes. Physical Review E 84: 1–8. [Google Scholar] [CrossRef] [Green Version]

- Raileanu-Szeles, Monica, and Lucian Albu. 2015. Nonlinearities and divergences in the process of European financial integration. Economic Modelling 46: 416–25. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, and Ioannis Tsakalos. 2013. How can a small country affect the European economy? The Greek contagion phenomenon. Journal of International Financial Markets, Institutions and Money 25: 18–32. [Google Scholar] [CrossRef]

- Shi, Wenbin, Pengjian Shan, Jog Wang, and Aijing Lin. 2014. Multiscale multifractal detrended cross-correlation analysis of financial time series. Physica A 403: 35–44. [Google Scholar] [CrossRef]

- Sornette, Didier. 2003. Why Stock Markets Crash? Critical Events in Complex Financial Systems. Princeton: Princeton University Press. [Google Scholar]

- Syllignakis, Manolis, and Georgios Kouretas. 2011. Dynamic correlation analysis of financial contagion: Evidence from the Central and Eastern European markets. International Review of Economics & Finance 20: 717–32. [Google Scholar]

- Tilfani, Oussama, Paulo Ferreira, and My Youssef El Boukfaoui. 2019a. Revisiting stock market integration in Central and Eastern European stock markets with a dynamic analysis. Post-Communist Economies. [Google Scholar] [CrossRef]

- Tilfani, Oussama, Paulo Ferreira, and My Youssef El Boukfaoui. 2019b. Dynamic cross-correlation and dynamic contagion of stock markets: A sliding windows approach with the DCCA correlation coefficient. Empirical Economics, 1–30. [Google Scholar] [CrossRef]

- Valls, Claudia. 2012. Rational integrability of a nonlinear finance system. Chaos Solitons & Fractals 45: 141–46. [Google Scholar]

- Virk, Nader, and Farrukh Javed. 2017. European equity market integration and joint relationship of conditional volatility and correlations. Journal of International Money and Finance 71: 53–77. [Google Scholar] [CrossRef] [Green Version]

- Wang, Gang-Jin, Chi Xie, Feng Han, and Bo Sun. 2012. Similarity measure and topology evolution of foreign exchange markets using dynamic time warping method: Evidence from minimal spanning tree. Physica A 391: 4136–46. [Google Scholar] [CrossRef]

- Wang, Gang-Jin, Chi Xie, Min Lin, and Harry Stanley. 2017. Stock market contagion during the global financial crisis: A multiscale approach. Finance Research Letters 22: 163–68. [Google Scholar] [CrossRef]

- Zebende, Gilney. 2011. DCCA cross-correlation coefficient: Quantifying a level of cross-correlation. Physica A 390: 1643–62. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Index | Country | Index |

|---|---|---|---|

| GERMANY | DAX35 | NETHERLANDS | AEX Index |

| AUSTRIA | ATX | PORTUGAL | PSI 20 |

| BELGIUM | BEL 20 | SLOVAKIA | SAX 16 |

| CYPRUS | CySE General | SLOVENIA | SBITOP |

| ESTONIA | OMX Tallin | SPAIN | IBEX 35 |

| FINLAND | OMX Helsinki | BULGARIA | SOFIX |

| FRANCE | CAC 40 | CROATIA | CROBEX |

| GREECE | Athex 20 | CZECH REPUBLIC | PX Index |

| IRELAND | ISEQ 20 | DENMARK | OMXC 20 |

| ITALY | FTSE MIB | HUNGARY | BUX |

| LATVIA | OMX Riga | POLAND | WIG Index |

| LITHUANIA | OMX Vilnius | ROMANIA | BET |

| LUXEMBOURG | LSE | SWEDEN | OMX Stockholm 30 |

| MALTA | MSE | UK | FTSE 100 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tilfani, O.; Ferreira, P.; Dionisio, A.; Youssef El Boukfaoui, M. EU Stock Markets vs. Germany, UK and US: Analysis of Dynamic Comovements Using Time-Varying DCCA Correlation Coefficients. J. Risk Financial Manag. 2020, 13, 91. https://doi.org/10.3390/jrfm13050091

Tilfani O, Ferreira P, Dionisio A, Youssef El Boukfaoui M. EU Stock Markets vs. Germany, UK and US: Analysis of Dynamic Comovements Using Time-Varying DCCA Correlation Coefficients. Journal of Risk and Financial Management. 2020; 13(5):91. https://doi.org/10.3390/jrfm13050091

Chicago/Turabian StyleTilfani, Oussama, Paulo Ferreira, Andreia Dionisio, and My Youssef El Boukfaoui. 2020. "EU Stock Markets vs. Germany, UK and US: Analysis of Dynamic Comovements Using Time-Varying DCCA Correlation Coefficients" Journal of Risk and Financial Management 13, no. 5: 91. https://doi.org/10.3390/jrfm13050091

APA StyleTilfani, O., Ferreira, P., Dionisio, A., & Youssef El Boukfaoui, M. (2020). EU Stock Markets vs. Germany, UK and US: Analysis of Dynamic Comovements Using Time-Varying DCCA Correlation Coefficients. Journal of Risk and Financial Management, 13(5), 91. https://doi.org/10.3390/jrfm13050091