Do Profitable Banks Make a Positive Contribution to the Economy?

Abstract

:1. Introduction

2. Overview of the Banking Sectors

2.1. Small Emerging Economies

2.2. Large Emerging Economies

2.3. Developed Economies

3. Literature Review

4. Dependent and Independent Variables

4.1. Dependent Variables

4.2. Independent Variables

4.2.1. Key Independent Variables

4.2.2. Control Variables

5. Data and Methods

5.1. Description and Sources of Data

5.2. Methods

- (a)

- There will be a unidirectional causality from bank profitability to economic growth if the coefficient of the lagged value of bank profitability is statistically significantly different from zero and the coefficient of the lagged value of GDP is not statistically significant (0 and 0);

- (b)

- There will be a unidirectional causality from economic growth to bank profitability if the coefficient of the lagged value of GDP is statistically significantly different from zero and the coefficient of the lagged value of bank profitability is not statistically significant (0 and 0);

- (c)

- There will be a bi-directional causality between bank profitability and economic growth if the coefficient of the lagged value of GDP and the coefficient of the lagged value of bank profitability are statistically significantly different from zero (0 and 0); and

- (d)

- There will be no causal relationship between bank profitability and economic growth if the coefficient of the lagged value of GDP and the coefficient of the lagged value of bank profitability are not statistically significantly different from zero (0 and 0).

6. Empirical Results

6.1. Regression Results

6.2. Effect of Key Variables across Developed, Small Emerging, and Large Emerging Economies

6.3. Bank Profitability and Economic Growth—A Causality Analysis

7. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

Appendix B

{kind=link}

| Correlation Matrix | GDP | (1 + ROA) | SIZE | INF | EXP | TRADE | MKTCAP |

|---|---|---|---|---|---|---|---|

| GDP | 1 | ||||||

| (1 + ROA) | 0.49 | 1 | |||||

| SIZE | −0.19 | −0.04 | 1 | ||||

| INF | 0.15 | 0.33 | −0.23 | 1 | |||

| EXP | 0.48 | 0.35 | −0.33 | 0.21 | 1 | ||

| TRADE | 0.02 | −0.02 | −0.13 | −0.03 | −0.07 | 1 | |

| MKTCAP | 0.18 | 0.03 | 0.17 | −0.09 | −0.08 | −0.09 | 1 |

| Variable | VIF | 1/VIF |

|---|---|---|

| (1 + ROA) | 4.81 | 0.20 |

| INF | 1.95 | 0.51 |

| SIZE | 1.84 | 0.54 |

| EXP | 1.24 | 0.81 |

| PSC | 1.2 | 0.83 |

| NPLS | 1.14 | 0.88 |

| TRADE | 1.11 | 0.90 |

| MKTCAP | 1.09 | 0.92 |

| Mean VIF | 2.06 |

References

- Ahmed, Syed M., and Mohammed I. Ansari. 1998. Financial sector development and economic growth: The South-Asian experience. Journal of Asian Economics 9: 503–17. [Google Scholar] [CrossRef]

- Anandarajan, Asokan, Iftekhar Hasan, and Cornelia McCarthy. 2007. Use of loan loss provisions for capital, earnings management and signalling by Australian banks. Accounting & Finance 47: 357–79. [Google Scholar]

- Anari, Ali, James Kolari, and Joseph Mason. 2005. Bank asset liquidation and the propagation of the US Great Depression. Journal of Money, Credit and Banking 37: 753–73. [Google Scholar] [CrossRef]

- Andersen, Lill, and Ronald Babula. 2009. The link between openness and long-run economic growth. Journal of International Commerce Economics 2: 31–50. [Google Scholar]

- Arellano, Manuel, and Stephen Bond. 1991. Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations. The Review of Economic Studies 58: 277–97. [Google Scholar] [CrossRef] [Green Version]

- Asteriou, Dimitrios, and Konstantinos Spanos. 2019. The relationship between financial development and economic growth during the recent crisis: Evidence from the EU. Finance Research Letters 28: 238–45. [Google Scholar] [CrossRef] [Green Version]

- Athanasoglou, Panayiotis P., Sophocles N. Brissimis, and Matthaios D. Delis. 2008. Bank-specific, industry-specific and macroeconomic determinants of bank profitability. Journal of international Financial Markets, Institutions and Money 18: 121–36. [Google Scholar] [CrossRef] [Green Version]

- Bernanke, Ben S. 1983. Nonmonetary Effects of the Financial Crisis in the Propagation of the Great Depression. The American Economic Review 73: 257–76. [Google Scholar]

- Botev, Jaroslava, Balázs Égert, and Fredj Jawadi. 2019. The nonlinear relationship between economic growth and financial development: Evidence from developing, emerging and advanced economies. International Economics 160: 3–13. [Google Scholar] [CrossRef]

- Buffie, Edward F. 1984. Financial repression, the new structuralists, and stabilization policy in semi-industrialized economies. Journal of Development Economics 14: 305–22. [Google Scholar] [CrossRef]

- Calomiris, Charles W., and Joseph R. Mason. 2003. Consequences of bank distress during the Great Depression. American Economic Review 93: 937–47. [Google Scholar] [CrossRef] [Green Version]

- Claeys, Sophie, and Koen Schoors. 2007. Bank supervision Russian style: Evidence of conflicts between micro-and macro-prudential concerns. Journal of Comparative Economics 35: 630–57. [Google Scholar] [CrossRef] [Green Version]

- Cole, Rebel A., Fariborz Moshirian, and Qiongbing Wu. 2008. Bank stock returns and economic growth. Journal of Banking & Finance 32: 995–1007. [Google Scholar]

- Creel, Jérôme, Paul Hubert, and Fabien Labondance. 2015. Financial stability and economic performance. Economic Modelling 48: 25–40. [Google Scholar] [CrossRef] [Green Version]

- De Gregorio, Jose, and Pablo E. Guidotti. 1995. Financial development and economic growth. World Development 23: 433–48. [Google Scholar] [CrossRef]

- Demetriades, Panicos O., and Khaled A. Hussein. 1996. Does financial development cause economic growth? Time-series evidence from 16 countries. Journal of Development Economics 51: 387–411. [Google Scholar] [CrossRef]

- Dia, Mohamed, Amirmohsen Golmohammadi, and Pawoumodom M. Takouda. 2020. Relative Efficiency of Canadian Banks: A Three-Stage Network Bootstrap DEA. Journal of Risk and Financial Management 13: 68. [Google Scholar] [CrossRef] [Green Version]

- Dietrich, Andreas, and Gabrielle Wanzenried. 2011. Determinants of bank profitability before and during the crisis: Evidence from Switzerland. Journal of International Financial Markets, Institutions and Money 21: 307–27. [Google Scholar] [CrossRef]

- European Central Bank. 2016. Financial Stability Review. Available online: https://www.ecb.europa.eu/pub/pdf/other/financialstabilityreview201611.en.pdf (accessed on 1 March 2020).

- Goldsmith, Raymond William. 1969. Financial Structure and Development. No. HG174 G57. New Haven: Yale University Press. [Google Scholar]

- Harrison, Paul, Oren Sussman, and Joseph Zeira. 1999. Finance and Growth: Theory and New Evidence. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=186142 (accessed on 4 April 2020).

- Jun, Sangjoon. 2012. Financial development and output growth: A panel study for Asian countries. Journal of East Asian Economic Integration 16: 97–115. [Google Scholar] [CrossRef]

- Kar, Muhsin, Şaban Nazlıoğlu, and Hüseyin Ağır. 2011. Financial development and economic growth nexus in the MENA countries: Bootstrap panel granger causality analysis. Economic Modelling 28: 685–93. [Google Scholar] [CrossRef]

- King, Robert G., and Ross Levine. 1993a. Finance and growth: Schumpeter might be right. The Quarterly Journal of Economics 108: 717–37. [Google Scholar] [CrossRef]

- King, Robert G., and Ross Levine. 1993b. Finance, entrepreneurship and growth. Journal of Monetary Economics 32: 513–42. [Google Scholar] [CrossRef]

- Klein, Paul-Olivier, and Laurent Weill. 2017. Bank Profitability: Good for Growth? Working Paper 2017-02. Paris: Institut de France. [Google Scholar]

- Koivu, Tuuli. 2002. Do Efficient Banking Sectors Accelerate Economic Growth in Transition Countries? Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1015710 (accessed on 12 February 2020).

- Kumar, Vijay, Sanjeev Acharya, and Ly TH Ho. 2020. Does monetary policy influence the profitability of banks in New Zealand? International Journal of Financial Studies 8: 35. [Google Scholar] [CrossRef]

- La Porta, Rafael, Florencio Lopez-de-Silanes, and Andrei Shleifer. 2002. Government ownership of banks. The Journal of Finance 57: 265–301. [Google Scholar] [CrossRef] [Green Version]

- Levine, Ross. 1997. Financial Development and Economic Growth: Views and Agenda. Journal of Economic Literature 35: 688–726. [Google Scholar]

- Levine, Ross, and Sara Zervos. 1998. Stock markets, banks, and economic growth. American Economic Review 88: 537–58. [Google Scholar]

- Levine, Ross, Norman Loayza, and Thorsten Beck. 2000. Financial intermediation and growth: Causality and causes. Journal of Monetary Economics 46: 31–77. [Google Scholar] [CrossRef] [Green Version]

- Lucas, Robert E. 1988. On the mechanics of economic development. Journal of Monetary Economics 22: 3–42. [Google Scholar] [CrossRef]

- Ndlovu, Godfrey. 2013. Financial sector development and economic growth: Evidence from Zimbabwe. International Journal of Economics and Financial Issues 3: 435. [Google Scholar]

- Önder, Zeynep, and Süheyla Özyıldırım. 2013. Role of bank credit on local growth: Do politics and crisis matter? Journal of Financial Stability 9: 13–25. [Google Scholar] [CrossRef] [Green Version]

- Patrick, Hugh T. 1966. Financial development and economic growth in underdeveloped countries. Economic Development and Cultural Change 14: 174–89. [Google Scholar] [CrossRef]

- Pradhan, Rudra P., Mak B. Arvin, John H. Hall, and Sahar Bahmani. 2014. Causal nexus between economic growth, banking sector development, stock market development, and other macroeconomic variables: The case of ASEAN countries. Review of Financial Economics 23: 155–73. [Google Scholar] [CrossRef]

- Prochniak, Mariusz, and Katarzyna Wasiak. 2017. The impact of the financial system on economic growth in the context of the global crisis: empirical evidence for the EU and OECD countries. Empirica 44: 295–337. [Google Scholar] [CrossRef] [Green Version]

- Robinson, Joan. 1952. The Rate of Interest and Other Essays. London: MacMillan. [Google Scholar]

- Rodriguez, Francisco, and Dani Rodrik. 2001. Trade policy and economic growth: a skeptic’s guide to the cross-national evidence. Edited by Ben S. Bernanke and Kenneth S. Rogoff. NBER Macroeconomics Annual 200: 261–338. [Google Scholar]

- Shaw, Edward Stone. 1973. Financial Deepening in Economic Development. New York: Oxford University press. [Google Scholar]

- Stern, Nicholas. 1989. The economics of development: a survey. The Economic Journal 99: 597–685. [Google Scholar] [CrossRef]

- Trujillo-Ponce, Antonio. 2013. What determines the profitability of banks? Evidence from Spain. Accounting & Finance 53: 561–86. [Google Scholar]

- Van Wijnbergen, Sweder. 1983. Interest rate management in LDC’s. Journal of Monetary Economics 12: 433–52. [Google Scholar] [CrossRef]

- Wachtel, Paul. 2001. Growth and Finance: What do we know and how do we know it? International Finance 4: 335–62. [Google Scholar] [CrossRef]

- World Bank. 2005. Financial Sector Assessment—A Handbook. Washington, DC: World Bank. [Google Scholar]

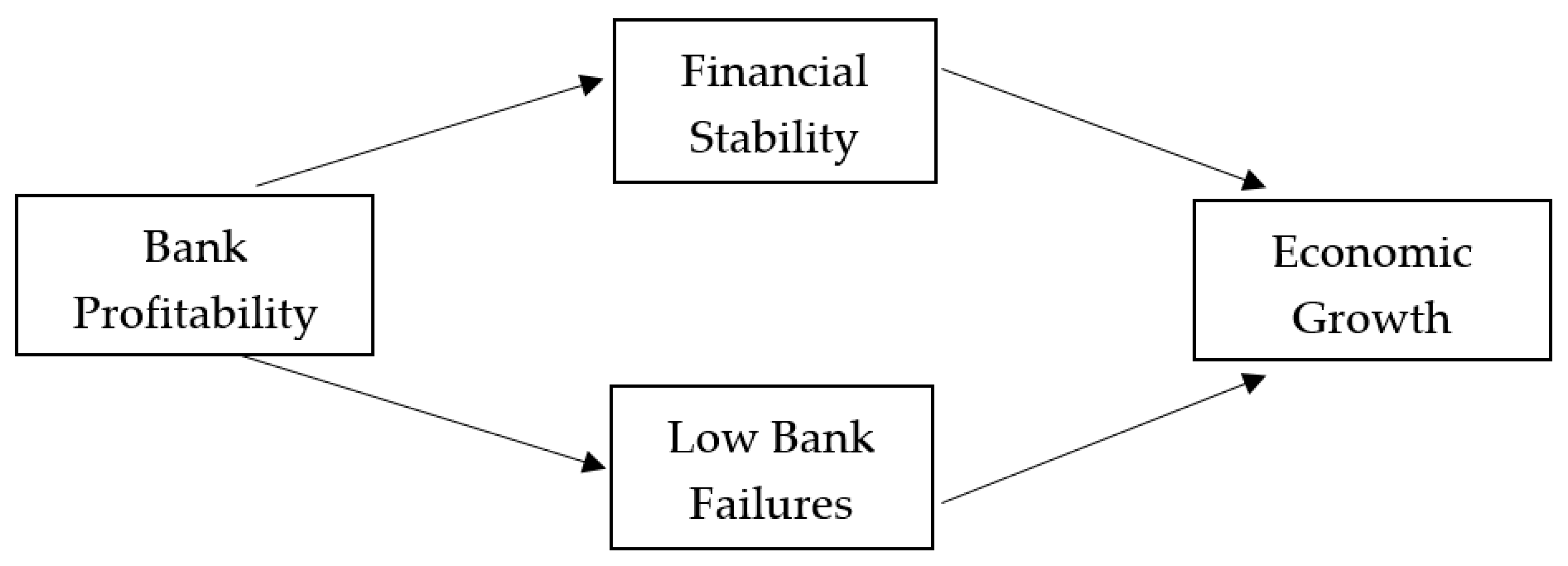

| 1 | Refer to the conceptual nexus between bank profitability and economic growth in Figure A1 (Appendix A). |

| 2 | The countries are Australia, Bangladesh, China, Hong Kong, India, Indonesia, Japan, Malaysia, Pakistan, and Singapore. |

| 3 | For example, most of the central banks in these countries require banks to maintain capital adequacy ratios and a certain percentage of deposits as cash reserves. |

| 4 | Capital adequacy ratio is the amount of capital maintained by banks to cover unexpected losses (Anandarajan et al. 2007). |

| 5 | It is a comprehensive database with over 12,000 banks around the world and covers around 90% of the banks in every country. |

| 6 | The results of pooled OLS are not reported but are available on request from the corresponding author. |

| Country Name | Bangladesh | Indonesia | Malaysia | Pakistan |

|---|---|---|---|---|

| Total assets (USD) | 107 billion | 440 billion | 602 billion | 100 billion |

| Number of conventional banks | 48 | 109 | 37 | 28 |

| * Number of Islamic banks | 25 | 34 | 16 | 20 |

| Minimum capital adequacy ratio requirement4 | 10% | 8% | 8% | 10% |

| Cash reserve requirement | 5% | 6% | 4% | 5% |

| Non-performing loan (NPL) criteria | +90 days | +365 days | +90 days | +90 days |

| Financial inclusion (branches/100,000 adults) | 8 | 9.6 | 11 | 9 |

| Bank assets to GDP ratio | 80% | 42% | 193% | 43% |

| Country Name | China | India |

|---|---|---|

| Total assets (USD) | 24.5 trillion | 1.8 trillion |

| Number of banks | 672 | 89 |

| Minimum capital adequacy ratio requirement | 8.50% | 9.00% |

| Cash reserve requirement | 19% | 4% |

| Non-performing loan (NPL) criteria | +90 days | +90 days |

| Financial inclusion (branches/100,000 adults) | 8 | 12 |

| Bank assets to GDP ratio | 292% | 95% |

| Country Name | Australia | Hong Kong | Japan | Singapore |

|---|---|---|---|---|

| Size (USD) | 2.8 trillion | 2.1 trillion | 8 trillion | 779 billion |

| Number of banks | 70 | 56 | 198 | 124 |

| Minimum capital adequacy ratio requirement | 8% | 8% | 8% | 10% |

| Cash reserve requirement | 0% | 0% | 0.1–1.3% * | 3% |

| Non-performing loan (NPL) criteria | +90 days | +90 days | +90 days | +90 days |

| Financial inclusion (branches/100,000 adults) | 30 | 23 | 34 | 9.5 |

| Bank assets to GDP ratio | 179% | 700% | 163% | 261% |

| Variables | Notation | Measure | Expected Sign |

|---|---|---|---|

| Dependent Variable | |||

| Gross Domestic Product | GDP | Annual GDP growth rate (%) | |

| Independent Variables | |||

| Key Independent Variables | |||

| Lagged Gross Domestic Product | Lag GDP | Lagged value of annual GDP growth rate (%) | + |

| Return on Assets | ROA | (1 + Profit before tax/Total assets) | + |

| Lagged (1 + Return on Assets) | Lag ROA | Lagged value of (1 + Profit before tax/Total assets) | + |

| Banking Sector Size | SIZE | Annual percentage change in total bank assets (%) | + |

| Control Variables | |||

| Inflation | INF | Annual percentage change in CPI (%) | − |

| Government Consumption | EXP | Annual percentage change in government consumption (%) | +/− |

| Openness to Economy | TRADE | Annual percentage change in sum of exports and imports (%) | + |

| Stock Market Capitalization | MKTCAP | Annual percentage change in market capitalization (%) | + |

| Variable | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|

| GDP | 5.25 | 3.141 | −1.51 | 12.69 |

| Lag GDP | 5.2 | 3.20 | −1.51 | 12.69 |

| (1 + ROA) | 1.10 | 0.37 | 0.31 | 1.83 |

| Lag (1 + ROA) | 1.12 | 0.38 | 0.31 | 1.83 |

| SIZE (Change in total assets) | 5.30 | 10.99 | −15.82 | 22.16 |

| INF | 4.72 | 3.68 | −0.7 | 13.65 |

| EXP | 10.51 | 9.18 | −7.77 | 31.43 |

| TRADE | −1.97 | 11.31 | −37.48 | 16.47 |

| MKTCAP | 8.93 | 40.47 | −64 | 110.01 |

| Dependent Variable: GDP Growth (%) | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Explanatory Variables | |||||

| Key independent variables | |||||

| Lag GDP | 0.106 | 0.108 | 0.121 | 0.0378 | 0.00240 |

| (1.09) | (1.11) | (1.28) | (0.39) | (0.02) | |

| Lag (1 + ROA) | 4.581 *** | 4.293 *** | 4.282 *** | 7.26 *** | |

| (3.24) | (2.96) | (3.07) | (3.19) | ||

| (1 + ROA) | 0.848 | ||||

| (0.61) | |||||

| Lag (1 + ROA)—Small banking sectors | 8.74 * | ||||

| (1.85) | |||||

| Lag (1 + ROA)—Large banking sectors | 5.483 *** | ||||

| (3.78) | |||||

| SIZE (Change in total assets) | −0.0459 ** | −0.0461 ** | −0.0121 * | −0.0321 | −0.0376 |

| (−2.37) | (−2.34) | (−1.89) | (−1.62) | (−1.49) | |

| Lag (1 + ROA)*SIZE | −0.891 ** | ||||

| (−2.44) | |||||

| Lag (1 + ROA)*SIZE—Small banking sectors | −1.118 ** | ||||

| (−2.11) | |||||

| Lag (1 + ROA)*SIZE—Large banking sectors | −0.0330 * | ||||

| (−1.67) | |||||

| Control variables | |||||

| INF | −0.134 | −0.200 * | −0.198 | ||

| (−1.08) | (−1.66) | (−1.63) | |||

| EXP | 0.101 *** | 0.0697*** | 0.0637 ** | ||

| (3.97) | (2.63) | (2.39) | |||

| TRADE | 0.0180 | 0.0107 | 0.00839 | ||

| (0.84) | (0.51) | (0.40) | |||

| MKTCAP | 0.00908 * | 0.00515 | 0.00440 | ||

| (1.78) | (0.95) | (0.82) | |||

| During GFC | −2.309 *** | −2.265 *** | −2.111 *** | −2.442 *** | −2.411 *** |

| (−4.87) | (−4.65) | (−4.36) | (−5.00) | (−4.77) | |

| Constant | 0.230 | −0.406 | −0.199 | 0.0314 | 0.921 |

| (0.14) | (−0.21) | (−0.12) | (0.02) | (0.35) | |

| Number of countries | 10 | 10 | 10 | 10 | 10 |

| Number of banks | 654 | 654 | 654 | 654 | 654 |

| AR(1) (p-value) | 0.0233 | 0.0289 | 0.0289 | 0.0461 | 0.0265 |

| AR(2) (p-value) | 0.3128 | 0.3111 | 0.3111 | 0.3044 | 0.2357 |

| Sargan test (p-value) | 0.962 | 0.894 | 0.605 | 0.729 | 0.978 |

| Subsamples | Lag (1 + ROA) | Lag (1 + ROA)*SIZE |

|---|---|---|

| Developed (B0.Xit) | 9.626 *** | −0.257 |

| B1.D1.Xit | −3.710 *** | −0.309 *** |

| B2.D2.Xit | −4.720 | −0.236 |

| Small Emerging (B0 + B1) | 5.916 *** | −0.566 *** |

| Large Emerging (B0 + B2) | 4.906 *** | −0.493 ** |

| Null Hypothesis | Lag Order: 1 | Lag Order: 2 |

|---|---|---|

| p-Value | p-Value | |

| H0: Bank profitability does not Granger-cause GDP Growth. | 0.000 *** | 0.000 *** |

| H0: GDP Growth does not Granger-cause Bank profitability. | 0.702 | 0.000 *** |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kumar, V.; Bird, R. Do Profitable Banks Make a Positive Contribution to the Economy? J. Risk Financial Manag. 2020, 13, 159. https://doi.org/10.3390/jrfm13080159

Kumar V, Bird R. Do Profitable Banks Make a Positive Contribution to the Economy? Journal of Risk and Financial Management. 2020; 13(8):159. https://doi.org/10.3390/jrfm13080159

Chicago/Turabian StyleKumar, Vijay, and Ron Bird. 2020. "Do Profitable Banks Make a Positive Contribution to the Economy?" Journal of Risk and Financial Management 13, no. 8: 159. https://doi.org/10.3390/jrfm13080159

APA StyleKumar, V., & Bird, R. (2020). Do Profitable Banks Make a Positive Contribution to the Economy? Journal of Risk and Financial Management, 13(8), 159. https://doi.org/10.3390/jrfm13080159